Abstract

This study set out to investigate the role played by human capital development in the nexus between financial inclusion and economic growth in Africa. We use GMM as the estimation technique to analyze country-level data pooled from 40 African countries from 2005 to 2018. The findings suggest the presence of a non-linear U-shaped relationship between financial inclusion and economic growth. It was also found that human capital development fully mediates the relationship between financial inclusion and economic growth in Africa. Hence, the growth-enhancing benefits of financial inclusion are transmitted through human development. Whilst pursuing their financial inclusion targets, efforts should be made by governments across the African continent to simultaneously improve the level of human capital development to realize the positive benefits of financial inclusion.

Plain language summary

Providing people with easy access to affordable financial services is seen as one of the surest ways to promote economic prosperity. Whilst some studies have been conducted to test this assertion, their findings are mostly conflicting. We attempt to unravel this puzzle in Africa by arguing that the relationship is both negative and positive depending on the extent to which people have access to financial services. We argue that the possibility that access to finance will promote economic prosperity is dependent on the productive capacity of the people. To empirically test these, we collect archival data across 40 African countries from 2005 to 2018 which we analyzed using the GMM regression technique. We conclude from our findings that, the effect of access to finance on the economy is negative when a large proportion of the population is excluded from the financial system. However, as many more people obtain access to financial services the effect becomes positive. Also, we conclude that access to finance improves overall economic well-being via an enhancement of the productive capacity of the population. Therefore, we recommend that policymakers across the continent speed up their efforts to ensure near-universal access by the adult population to financial services; in that, it is then that the positive benefits on the economy will be guaranteed. Our study did not determine the exact level of access required to transform the effects of access to finance from negative to positive due to data limitations and this can be addressed in future research.

Introduction

Researchers have over the decades attempted to investigate the factors responsible for the growth of economies globally. In Africa, there has been an attempt to determine whether factors stimulating growth in the Western world are applicable. Understanding the dynamics of economic growth especially in the developing nations of Africa is crucial given that we lag behind other parts of the world regarding socio-economic development. Indeed, there is still a broadening gap in growth between advanced countries and developing countries (Chakamera & Pisa, 2021) . Africa’s estimated average growth in GDP slowed from 4.1% (2021) to 3.6% (2022) and is projected to dip further to 3.1% in 2023 (World Bank, 2023). Africa is also experiencing a gradually diminishing capital stock which has increased attention to the drivers of growth in the region (Othman & Jenkins, 2020). As a result, research into the determinants of economic growth remains essential in Africa. One very critical factor that can stimulate economic growth is financial inclusion (FI) which has continued to attract policy and research attention around the globe. Developments in financial technology have led to the emergence of a vibrant virtual economy (Singh & Stakic, 2021) and this has intensified the financial inclusion discourse as a tool for promoting economic prosperity.

Financial inclusion (FI) involves making financial services readily accessible and affordable to households and businesses. Sethi and Acharya (2018) aptly describe the ways through which FI translates into economic growth. The first is by making credit readily available to finance the entrepreneurial activities of vulnerable groups which enhances their incomes, and human development and then stimulates economic growth. Indeed, they argue that financial exclusion can hinder the growth of an economy through an inadequate supply of financial services. The second is by making saving and investment services widely available; this they argue promotes capital accumulation and economic growth (see Figure 1 below for a detailed illustration). In support of the above, other researchers have provided further arguments or evidence (Aghion & Bolton, 1997; Nizam et al., 2020; Van et al., 2021). The World Bank (2022) for instance, identifies FI as an enabler of the 17 SDGs and further argues that success in the financial inclusion strategies of nations is critical to reducing extreme poverty and promoting inclusive growth. Having said that, about 30% of the global population remains financially excluded (Kim et al., 2018). Africa is the region with the lowest level of FI around the globe (Makina & Walle, 2019).

Financial inclusion-economic growth linkage.

Empirical studies that focus on financial inclusion (FI) and how it impacts growth in Africa are critical now given the high level of poverty, low FI level, and the quest for development in the continent. The above arguments linking FI to economic growth have led to a recent attempt by many countries in Africa (with the World Bank’s support and other development partners) to develop and implement various National Financial Inclusion Strategies. In this regard, Ozili (2020) observes that FI is attracting increasing attention in policy circles across the African continent. The importance being attached to FI by governments thus calls for more research on all aspects of the FI-growth relationship to provide evidence that can inform related policies for the realization of the intended growth rewards of FI.

Several studies on financial inclusion (FI) exist in the extant literature. The focus of these works in the early 2000s was on the fundamental idea of FI and the nature of financially marginalized groups (Dev, 2006; Devlin, 2005; Panigyrakis et al., 2002); these were followed by a stream of studies that focused on the measures of FI on one hand and the FI and economic growth nexus on another hand. Investigations into the inclusion-growth relationship have produced diverse results. These findings can be classified into three categories. The first group of findings reports a direct link between FI and economic growth (Singh & Stakic, 2021; Nizam et al., 2020; Van et al., 2021). Whilst the second category of findings reflect a negative relationship (Barajas et al., 2016; Erlando et al., 2020; Nkwede, 2015), the third strand of studies concludes that there is an insignificant link between FI and growth (Dahiya & Kumar, 2020; Huang et al., 2021; Okoye et al., 2017). What accounts for these variations in findings especially in Africa is a critical question that remains unanswered; at least empirically. One possibility is that the relation between FI and growth is not linear (Nizam et al. (2020). Unfortunately, however, previous studies have often assumed linearity in the relationship. The inconsistency in the findings of past studies could be a pointer to a more complex relationship between FI and growth. When one variable affects another through different channels, their relationship becomes more complex; the use of linear models does not help us properly understand such complex real-life relationships (Shahbaz et al., 2017). A non-linear study provides a better understanding of the complex FI-growth relationship which can lead to more accurate policy decisions. This brings to the fore the need to explore the possible non-linearity in the relationship as this has been ignored in previous studies.

Furthermore, the available studies attempt to estimate the inclusion growth nexus based on the adoption of single measures of financial inclusion (Guru & Yadav, 2019; Makina & Walle, 2019; Moyo, 2018; Osei et al., 2019; Rasheed et al., 2016) and often limited in scope to single-country studies (Emara & Said, 2021; Kim et al., 2018; Makina & Walle, 2019). This could partly be responsible for the variations in findings in that no single measure can be said to completely capture the degree of FI. Unfortunately, the few studies that adopt a multi-dimensional measure of financial inclusion tend to focus on developed economies and developing nations other than those in Africa. Hence the literature in this subject area remains scant within the African context. Though African countries have some similarities, they are in different stages of economic growth which could make the generalization of single-country studies also problematic. Africa thus provides a unique setting for studies on FI and economic growth. Apart from being the poorest region in the world (Balcilar et al., 2020), the financial systems in Africa are also the most underdeveloped (Otchere et al., 2017) and the region has the lowest level of FI around the globe (Makina & Walle, 2019). These coupled with the efforts to develop the financial sector and promote financial inclusion make it imperative for studies of this kind in the continent. This will either provide evidence in support of the current development efforts or provide new directions in our development agenda.

From the above, the need to empirically explore the possible reasons for the variations in the findings of prior studies is apparent. Are there some critical factors mediating the inclusion and growth relationship? Whether there is a significant association or not and the nature of this relationship could both be conditioned on some other variables. Ozili (2020) notes that FI influences economic growth through existing subsystems. It is in this regard that Madichie et al. (2014) argue that output growth is not feasible without considering the important role of human capital development which is made possible through improved access to financial services. Wang and Guan (2017) also observe that the level of development in human capital is crucial in understanding the extent to which financial inclusion may influence economic growth. Empirically, the above evidence indicates that the benefits of FI are transmitted through human capital to economic growth. In Figure 1 below, the relation between FI, human capital, and growth is demonstrated. Financially included individuals can obtain funding for their entrepreneurial activities. This can transform their livelihoods by improving their income levels. Subsequently, such individuals can access quality education, and health care services amongst others leading to enhanced human capital development. The higher human capital development (manifested via well-educated and healthy citizens with longer life expectancy), tends to stimulate productivity and boost economic growth. The implication here is that human development remains a potential hindrance to the financial inclusion agenda (Hasan et al., 2021) and this could affect its potential impact on growth. Despite the overwhelming evidence on the importance of human development in the FI-growth nexus, there is currently no known study in Africa that has sought to empirically examine this.

This paper therefore seeks to make the following contributions to literature in the following manner: first, unlike previous studies, we investigate the FI-growth nexus using a more comprehensive multidimensional measure of FI (FI index) involving a much wider scope of 40 African countries as opposed to the mostly single-country studies conducted in the past. Our study thus addresses the deficiency of relying on single measures of financial inclusion as prior studies have done. In addition, the broader scope of our study makes the findings here more generalizable with relevant policy implications for the subregion especially given the increasing advocacy for greater regional integration. Second, we also make a significant contribution to the current discourse on the FI-growth relation by deviating from the approach of past studies which often assumed linearity in the relationship. Here, we go with the suggestion of Nizam et al. (2020) that the relationship between FI and economic growth could be non-monotonic. We thus use a quadratic function in the estimation of the relationship. To our best knowledge, this is the first time this has been done in Africa. We hence provide a unique set of results not known from prior studies in Africa. Third, in our attempt to partly address the question of why various studies so far have yielded mixed findings, we contribute by going beyond the norm of testing just the direct association between FI and growth to assume that the relationship is conditioned on other variables. We thus adopt the human capital development variable which has been identified as a key variable that can transmit the benefits of FI into growth (Wang & Guan, 2017). We contribute here by testing for the mediation role of human capital in the FI-growth relationship. Again, this has not been tested in our current context and will help provide key insights for FI and economic growth-related policies.

We organize the rest of this paper as follows. In the next section, we provide a review of the empirical and theoretical literature. We present our methodology in the third section. We present results and discuss our findings in the fourth section whilst last section presents the conclusion and policy recommendations.

Theoretical Framework and Empirical Literature Review

Considerable attention has been given to the financial development-economic growth literature in recent decades (Le et al., 2019). Indeed, the financial sector and its development is considered the engine of economic growth. Consequently, financial inclusion cannot be ignored in the economic development agenda of developing nations. It is thus not surprising that financial inclusion was formally recognized as a key pillar for global developing at the 2010 G20 Summit in Seoul, South Korea. Many studies since the early 2000s have attributed the high poverty levels in developing nations to the exclusions of a large number of adults from the mainstream financial sector (Makina & Walle, 2019). The implication of FI is that people and businesses are given access to a wide range of financial products that satisfy their transactional, payments, credit, savings, and insurance needs (Erlando et al., 2020). It starts with obtaining a basic deposit account at a financial institution and expands to include making and receiving various payments and a number of other financial services.

Sethi and Acharya (2018) provide a theoretical description of the financial inclusion-economic growth nexus which is adapted and presented in Figure 1 below. They observe that there are two main avenues through which FI contributes to economic growth. The first is based on the argument that access to affordable credit by low-income households and small businesses could kick-start production activities by both the rural and urban poor. The authors note that access to credit thus allows for value creation by the vulnerable households and small businesses in both rural and urban areas which translates into output growth at the level of the macro economy. The improved production activities create job opportunities for many more individuals. The resulting initial improvement in income levels facilitates human development. The higher levels of human development (as reflected by indicators such as health, nutrition, and education) further stimulates production activities and leads to further economic growth. The second is that with accessibility to insurance and deposit services, financial inclusion facilitates the aggregation of funds within the financial system which enhances capital accumulation. The financial system then efficiently and effectively allocates these funds into profitable investments. An increase in investment boosts job creation and increases income levels. This translates into economic growth through human development.

Empirical Literature and Hypothesis Development

Numerous studies have examined the link between FI and economic growth; the human capital development-economic growth link; and FI and human capital development. In the paragraphs that follow we present a review of some of the very current studies in these areas. The hypotheses developed emerged from the literature based on the Baron and Kenny (1986) mediation model adopted in this study. This mediation model presented in Figure 2 illustrates the various relationships to be tested in an attempt to establish the existence of mediation in the link between FI as the independent variable and economic growth as the outcome variable. The details are explained in the methodology section.

A simple mediation model.

Financial Inclusion and Economic Growth

Another strand of studies has investigated the financial inclusion (FI) and economic growth nexus and the results of some are reviewed here. Chinoda (2020) investigates the nexus between economic growth and FI in Africa based on a panel data of thirty countries from 2004 to 2017. The study finds a one-way causal link from economic growth to FI. Similarly, Van et al. (2021) provide international evidence of a direct association between FI and growth. They conclude a stronger link exists for low-income economies and countries with lower FI levels. A study by Kim et al. (2018) from 1990 to 2013 and a list of 55 OIC nations find that a positive relation is present between FI and economic growth for OIC nations. The authors further show that the high degree of FI is a key factor in producing economic growth. Also, Sethi and Acharya (2018) examine the connection between FI and growth for 31 nations and conclude that FI spurs economic growth. Thomas (2017) analyzes the association between the accessibility of finance and growth in SAARC economies from 2007 to 2015 by using the GMM technique. Out of the eight indicators used, seven of them are significant, showing that, high accessibility of finance leads to higher income and increases growth in the economy. The study also confirms that progress in financial access variables has a higher effect on growth in developing economies than in middle-income nations.

However, some other studies have either found an insignificant, indirect, or negative link for the inclusion-growth nexus. In India and elsewhere for instance, some authors have established an insignificant association between FI and economic growth (see: Dahiya & Kumar, 2020; Huang et al., 2021; Okoye et al., 2017), on the contrary, some evidence from Indonesia, Nigeria, MENA, support a negative influence of FI on growth. For instance, Erlando et al. (2020) examine FI, poverty alleviation and economic growth in Indonesia and find a significant negative relationship. Nkwede (2015) found evidence of an inverse association between FI and economic growth in Nigeria. Naceur and Ghazouani (2007) demonstrate that bank development index, credit to the private sector by banks in MENA nations has a negative effect on the growth of such economies. Similarly, Moore and Craigwell (2003) claim that providing minor financial services does not generate any higher return financially in relation to the operating cost of finance for providing them. Employing GMM dynamic panel methodology to examine whether FI and economic growth effects vary among countries and particularly in certain regions, oil-dependent, and low-income countries, find financial inclusion to negatively affect economic growth.

Furthermore, Singh and Stakic (2021) examine the link between FI and economic growth with the use of annual data spanning 2004–2017. The findings show the existence of a threshold effect on the inclusive finance and growth relationship, which suggests that the association between inclusive finance and growth is non-monotonic. At a high level of inclusion, the positive influence is more noticeable than when inclusion is at a lower level. Sahay et al. (2015) also examine the linkage between FI and economic growth. The authors find that higher accessibility to finance by companies improves economic growth, but only to an extent, after which the advantages of extra inclusion begin to fall or even get negative in many developed economies.

On the FI-growth nexus, our survey of the literature yields the following observations. First, several related studies are found in Africa, Asia, and other developing and middle-income countries. These available studies have often focused a lot of attention on the simple direct relationship. A few have attempted to examine the direction of causality and conduct threshold analysis. Second, the conclusions of existing studies are often mixed ranging from those that find no relationship, those that find a positive relationship to those that find a negative relationship. These findings could be explained variously. We explain the positive relation as follows: greater access to financial products improves financial sector liquidity, which helps to provide affordable capital to businesses and individuals and this can spur growth (Singh & Stakic, 2021). Furthermore, as many people get included in the financial system, it promotes capital accumulation which stimulates growth. As nations pursue their financial inclusion agenda effectively, we expect the impact to be positive on economic growth. However, in some instances, this impact may not be realized, and no relationship may be observed. An explanation to this could be that, having access to financial products may be one thing and utilization of such services another (Dahiya & Kumar, 2020). Where there is just mere access without utilization, we may not observe any significant link between inclusion and growth. The possibility that accessibility to financial services could yield a negative effect on growth could be explained by the observation that the increased access to funds may not necessarily lead to a flow of such funds into the real sectors of the economy to directly fund production activities. If these funds flow to affect the monetary sector instead, then the potential positive impact of inclusion could become negative (Erlando et al., 2020).

Third, we also observe that the inclusion-growth relation could be positive or negative at different levels of financial inclusion which suggests the relationship is non-linear. However, the only available studies to have tested this non-linearity were conducted in Asia and the developed countries. Our current study thus also makes an important contribution in this regard. From all the discussion presented above, we finally hypothesize that;

H1a: the direct relationship between financial inclusion and economic growth is significantly positive.

H1b: the link between financial inclusion and economic growth is significantly, non-linear.

Financial Inclusion and Human Capital Development

Employing a panel of Sub-Saharan African economies, Matekenya et al. (2021) investigate how FI affects human capital development. The authors find FI to exert a significantly positive influence on human development in Sub-Saharan Africa. Similarly, Ababio et al. (2021) investigate the linkage between FI and human development in frontier markets and find that using the banking sector to promote FI is essential to stimulate human development. Datta and Singh (2019) examine the link between FI and human development in advanced and developing economies. Using an index of FI, the authors find FI to have a positive relation with human development. Using the HDI and a modified HDI, Nanda and Kaur (2016) found a positive link between FI and human development in 68 economies. Raichoudhury (2016) analyzes the link between FI and human development in a cross-country study and finds financial inclusion to enhance human development.

Arora and Kumar (2021) employ the ARDL bound test and Granger causality techniques to investigate the association between FI and the human development index in India. The authors find evidence of a long-term relation between FI and human development. Further, the Granger causality test shows the presence of bidirectional causality between FI and human development in India. Thathsarani et al. (2021) also examine the role of FI in economic growth and human capital among South Asian economies. The authors find that in South Asian economies, FI exerts a long-term effect on human capital development.

The available studies from Africa, Asia, and other developing and developed nations thus appear mostly unanimous in their conclusions that financial inclusion impacts positively on human development. This conclusion cuts across different economies with varied degrees of growth. Thus, any country that focuses on widening accessibility to financial products to its people, is most likely going to see an improvement in their human development level. This is to be expected as accessibility to financial services can improve the earning capacity of households and businesses. As earning capacity improves such individuals can afford quality education, nutrition, and health care amongst others. This helps to improve the standard of living and increase life expectancy in the country. Following from the empirical evidence here, we hypothesize that

H2: financial inclusion exerts a significant and positive impact on human development.

Human Capital Development and Economic Growth

On the nexus between human capital development and economic growth, Sarwar et al. (2020) posit that even in the absence of exogenous technology advancements, if capital is popularly referred to as human capital, it loosens the constraints of falling returns and supports long-run economic growth. Empirically, Chowdhury et al. (2018) investigate the influence of human capital on the economy of Bangladesh using data from 1979 to 2013. The authors find a strong positive link between human capital and growth. In the same vein, Qamruzzaman and Karim (2020) examine how human capital influences economic growth and report that improved human capital drives economic growth positively. Moreover, Han and Lee (2020) find that human capital influences economic growth because it has an effect on the productivity of labor. In Zambia, Hakooma and Seshamani (2017) investigate how human capital influences economic growth and find the relationship to be significant in the long-run.

Also, Eigbiremolen and Anaduaka (2014) examine human capital development and national output. The study finds that human capital development positively and significantly influence output level. Poças (2014) study human capital in developed countries and find that improvements in health significantly benefit economic growth. Notwithstanding the positive associations, Adeyemi and Ogunsola (2016) analyze the influence of human capital on economic growth and find the link to be statistically insignificant. The authors further show that a negative long-term association exists between school enrolment, public expenditure on health, and economic growth.

From the survey of the available literature, we again find a high level of consistency in the findings on the human capital development-economic growth nexus. These studies have either failed to establish a significant relationship at all or have established a negative relationship depending on the proxy used. The overwhelming majority of studies, however, point to a positive association between human capital and economic growth which confirms what one would expect from a theoretical viewpoint. For instance, when people are generally well nourished and sheltered, they become healthier; and healthier people are generally more productive and produce a healthy economy. Also, with quality education, people develop their skills and become more efficient in the production process. These work together to stimulate growth in the economy. From the review provided above, we develop the following hypothesis between human capital development and economic growth;

H3: Human capital development exerts a significant and positive influence on economic growth in Africa.

Mediation Variables in the Financial Inclusion and Economic Growth Nexus

Generally, numerous studies have examined a moderation of the finance-growth nexus (see: Alimi & Adediran, 2020; Chatterjee, 2020; Ehigiamusoe et al., 2019; Ehigiamusoe & Lean, 2019; Ehigiamusoe & Samsurijan, 2021; Emara and El Said, 2021). Chatterjee (2020), for instance, examines financial inclusion, ICT diffusion, and economic growth using a fixed-effect model for 41 countries. The findings show that FI independently and when interacted with mobile and internet penetration can enhance growth in per capita GDP. Similarly, Emara and El Said (2021) assess the role of governance in the link between FI and economic growth in MENA countries. The results show that financial inclusion positively and significantly influence economic growth in the MENA region. However, the findings show that the significant effect is only realized when there are strong institutions.

Ehigiamusoe et al. (2019) use inflation as a moderator in the financial development-economic growth nexus and observe that financial development exerts a positive influence on economic growth among West African economies; while interacting inflation and financial development negatively affects economic growth. Ehigiamusoe and Lean (2019) examine the finance-growth nexus using the real exchange rate as a moderator. The study shows that financial development positively influences long-run economic growth; however, this positive effect is weakened by the real exchange rate. Ehigiamusoe and Samsurijan (2021) examine factors that moderate the finance-growth nexus and show that increased development in finance and the economy, quality institutions, and stability in the macroeconomic environment enhance the influence of development in the financial sector on economic growth.

Empirically, however, a lot remains to be known about the factors that mediate the financial inclusion-economic growth link. Very few studies have investigated this phenomenon and shown that some of the major mediating terms include mobile penetration. Andrianaivo and Kpodar (2011) find that, the mediating factor, mobile penetration, significantly and positively mediates the FI and growth nexus of 44 African economies. A similar result is found by Swamy (2014) for gender dimension and rate of growth. In all these studies, there is a conclusion that economic growth can be affected by financial inclusion through certain channels. Liu et al. (2021) also attempted to identify the mediating factors in the FI and growth relationship; they established that entrepreneurship and household consumption are key mechanisms through which digital FI influences economic growth.

We observe from the available literature, that, the attempts to explain the mixed nature of the findings of various studies on this topic, have led to several moderation studies which attempt to introduce an interaction term in the nexus between FI and growth. This has consequently led to the identification of several moderators in the inclusion-growth nexus. Unfortunately, mediation studies that attempt to systematically examine the channel through which inclusion transmits into economic growth are empirically rare in the literature. The possible mediating factors have not been comprehensively identified especially in our current context of Africa and this is a major contribution that our studies seek to make. In an attempt to identify further mediating variables, we adopt human capital development in our empirical study based on the argument that the level of human capital development performs an important role in understanding the extent to which financial inclusion may influence economic growth (Wang and Guan, 2017). Consequently, we hypothesize as follows:

H4: Human capital development fully mediates the financial inclusion and economic growth relationship.

Methodology

Data and Data Sources

Country-level secondary data on selected variables were used in this study. The data was sourced from the World Bank’s databases and covers the 14-year period from 2005 to 2018. The selection of the key variables of interest was informed by both the literature and data availability (see Table 1 for the details of the variables). The macroeconomic indicators were obtained from the WDI database. Data on the measures of FI were sourced from the International Financial Statistics database. The study involved 40 countries in Africa conveniently selected based on data availability. The countries are: Algeria, Burundi, Benin, Burkina Faso, Botswana, Central African Republic, Côte d’Ivoire, Cameroon, Congo, Comoros, Cabo Verde, Djibouti, Egypt, Eswatini, Ghana, Guinea, The Gambia, Equatorial Guinea, Kenya, Liberia, Libya, Lesotho, Morocco, Madagascar, Mali, Mozambique, Mauritania, Mauritius, Malawi, Niger, Nigeria, Rwanda, Sudan, Senegal, Seychelles, Chad, Togo, Tunisia, Uganda, and South Africa. The data period and sampled countries were conveniently chosen based on data availability.

Variable Description, Measurement, and Expected Sign.

Model Specification

The general dynamic baseline model used in our estimations of the direct relation between economic growth and FI is specified in Equation 1 below.

Where the outcome variable (economic growth), is proxied by the annual GDP per capita growth rate (GDPPC).

We adopt the Baron and Kenny (1986) mediation model in our estimation of the hypotheses here. According to Baron and Kenny (1986) determining the mediating role of a variable in a given relationship requires the estimation of four separate equations. These equations reflect four sets of relationships as follows: the first, is an equation that estimates the relation between the main explanatory variable (financial inclusion) and the explained variable (economic growth) and this relationship must be significant. The first Baron and Kenny condition for mediation analysis is tested by Equation 1 above which captures the hypothesis, H1a. In addition, we slightly modify Equation 1 above by including the squared term of the independent variable to test for the possible non-linearity in the relationship as reflected by hypothesis, H1b which is tested empirically by Equation 2 below following Kasman and Kasman (2015) and Gupta and Moudud-Ul-Huq (2020), we add the squared term of the financial inclusion index to capture a potential non-linear relationship and specify Equation 2 below as follows:

The second in the Baron and Kenny mediation model is an equation that estimates the direct relation between the mediating variable (human capital development) and the independent variable (financial inclusion) such that, the mediating variable now acts as a dependent variable. We represent this relationship in Equation 3 below which empirically tests the hypothesis: H2

The third equation in the Baron and Kenny mediation model estimates the link between the mediating variable (human capital development) and the outcome variable (economic growth). We specify this relationship which tests the hypothesis: H3 in Equation 4 below.

According to Baron and Kenny (1986), we can conclude that mediation exists in the nexus between the explanatory variable (financial inclusion) and explained variable (economic growth) when the main relationships estimated by Equations 1, 3, and 4 are all significant. In other words, H1a, H2, and H3 must all be significant to conclude that the third variable (human capital development) mediates the nexus between financial inclusion and economic growth. However, to determine the exact nature of the mediation relationship (whether full or partial mediation), they recommend that Equation 1 above be modified by the introduction of the mediating variable (human development). This modification is introduced in Equation 5 below. If the association between the explanatory variable (financial inclusion) and explained variable (economic growth) remains significant in Equation 5 (as in the case of Equation 1) with only a decrease in the magnitude of the coefficient, then we conclude there is a partial mediation relationship. However, if the link between economic growth and FI becomes insignificant in Equation 5, then, there is a full mediation relationship. A pictorial representation of the Baron and Kenny mediation model and the related hypotheses are presented in Figure 2 below.

Estimation Technique

According to Van et al. (2021), there is a dynamic effect with the growth of economies, which means that its current value is closely linked to its former values. As a result, a dynamic panel model is employed to analyze the influence of FI on economic growth. The GMM proposed by Arellano and Bond (1991) and Blundell and Bond (1998) is used to account for the problem of endogeneity which results from including the lag of an explained variable as one of the explanatory variables. We rely on the GMM estimation technique to estimate a dynamic baseline equation where economic growth depends on its initial lag (Equation 1). This method permits the estimation of a dynamic model with the use of lagged levels and first differences as instruments for a system of equations. The first-difference GMM normally produces biased and inaccurate outcomes (Alonso-Borrego & Arellano, 1999; Blundell & Bond, 1998). However, Blundell and Bond (1998) recommend using the system-GMM technique instead of the difference-GMM. This study therefore used a system-GMM as it incorporates difference GMM and level approaches. This estimation technique is most appropriate when: the values of the outcome variable are influenced by past values; the selected independent variables are also presumed to be endogenous, and the panels have a relatively small T and large N as is the case with this study (T = 14 and N = 40). Apart from taking care of endogeneity issues, the GMM offers a more robust error estimation in measurement likened to the OLS approach. Consistency of the GMM technique is dependent on two main assumptions. The foremost assumption is that there should not be serial correlation in the error terms and the second assumption is that there must be validity in over-identifying restrictions. Two specification tests are suggested to ensure that these assumptions are true (Arellano & Bond, 1991; Arellano & Bover, 1995; Blundell & Bond, 1998). These are the Sargan and Hansen test of over-identifying restrictions. This test ensures validity in the instruments. The other test examines the presence of second-order serial correlation. The STATA 13 statistical software is used in analyzing the data for this study.

Principal Component Analysis (PCA)

We compute an index for FI using Principal Component Analysis (PCA). Financial inclusion has different dimensions. To comprehensively measure FI, we estimated the index using three dimensions of FI namely: the number of commercial bank branches for every hundred thousand (100,000) adults (CBBA) and the number of ATMs per one hundred thousand (100,000) adults (ATMA) and private sector credit to GDP (PSC). The first two indicators measure access to financial services whilst the last indicator measures actual usage of financial services. The index for financial inclusion used in this study thus captures different dimensions and would make our results reflect more comprehensively the construct under study. Our approach in this paper is consistent with studies such as Anarfo et al. (2019). Using PCA to compute the index is advantageous because this method computes a cumulative relation between the variables (Naik, 2017), which helps to create a comprehensive measure for FI. Accordingly, in the PCA technique, the jth factor index is specified as;

where FII j is the Financial Inclusion Index; Wj is the parameter’s weight and factor score; X is the initial value of the various components; whereas P is the number of variables. Following Van et al. (2021), the composite index for financial inclusion is computed with three dimensions. These dimensions include the number of commercial bank branches for every hundred thousand (100,000) adults (CBBA) and the number of ATMs per one hundred thousand (100,000) adults (ATMA) and private sector credit to GDP (PSC).

Results and Discussion

Descriptive Statistics

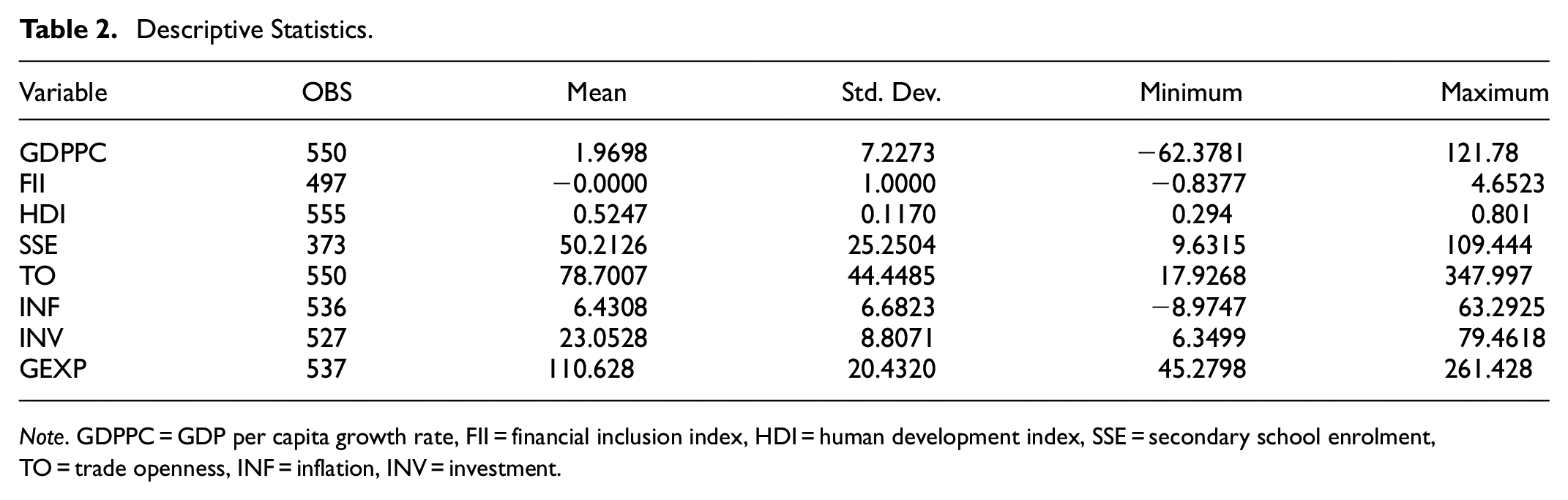

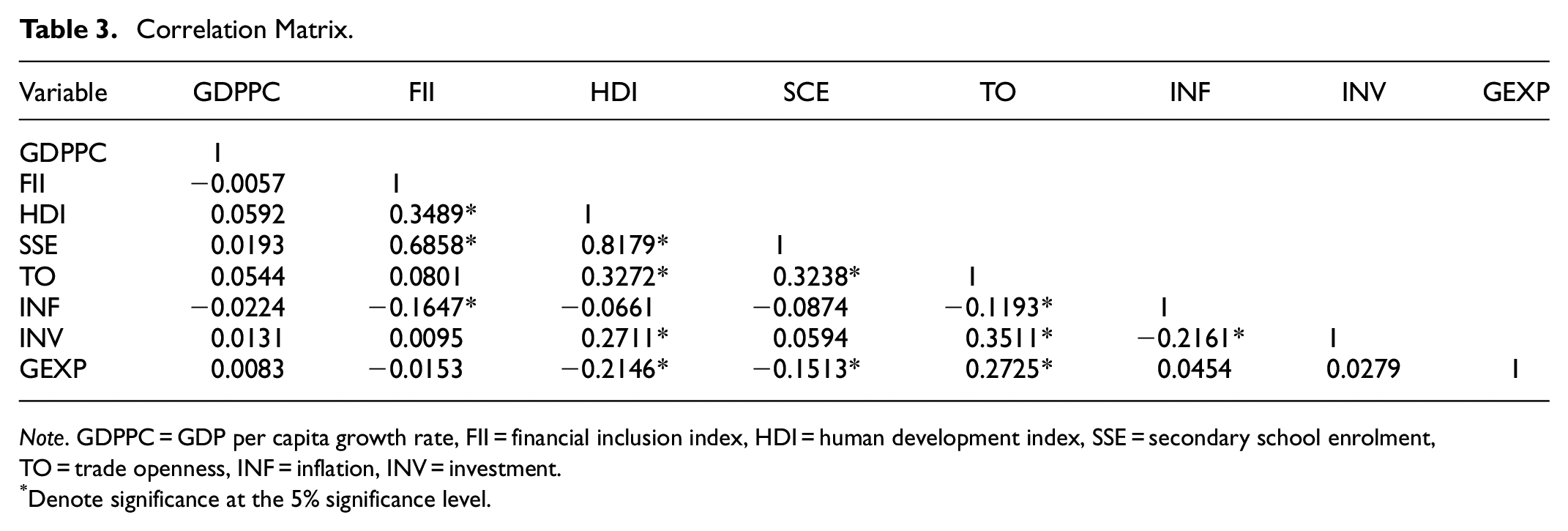

We present descriptive statistics in Table 2. GDP per capita growth rate shows an average of 1.97% with a standard deviation of 7.23. Generally, the economic growth appears very low though there appear to be wide variations across the sample. The very low mean for the financial inclusion index (−0.0000) indicates a low demand and access to financial products. The minimum and maximum values for financial inclusion are −0.8377 and 4.6523 respectively. The relatively low standard deviation for financial inclusion also indicates less variation in financial inclusion among the selected countries. Indeed, a large number of people remain marginalized from the mainstream financial system in the continent of Africa. The average (standard deviation) for human capital development (HDI) is 0.5247 (0.1170) with minimum and maximum values of 0.294 and 0.801 respectively. Trade openness (TO), Inflation (INF), Investment (INV), and Government expenditure (GEXP) have averages of 78.70%, 6.43%, 23.05%, and 110.63% respectively. The correlation matrix of the variables is presented in Table 3. It shows there is no problem of multicollinearity as no two independent variables have a correlation value greater than .80 (Kennedy, 2008). The signs of the correlation coefficients are as one would expect in most instances.

Descriptive Statistics.

Note. GDPPC = GDP per capita growth rate, FII = financial inclusion index, HDI = human development index, SSE = secondary school enrolment, TO = trade openness, INF = inflation, INV = investment.

Correlation Matrix.

Note. GDPPC = GDP per capita growth rate, FII = financial inclusion index, HDI = human development index, SSE = secondary school enrolment, TO = trade openness, INF = inflation, INV = investment.

Denote significance at the 5% significance level.

The Direct Relationship Between Financial Inclusion (FI) and Economic Growth

The paper sought to establish the possible mediation in the nexus between FI and economic growth. To achieve this, we follow the four-step approach of Baron and Kenny (1986). The foremost step or condition involves testing the direct association between the explanatory (financial inclusion) and explained (economic growth) variables. This relationship is specified in Equation 1 and the results are presented in column 2 of Table 4.

Regression Results.

Note. Robust standard errors are in (). GDPPC = GDP per capita growth rate, FII = financial inclusion index, HDI = human development index, TO = trade openness, INF = inflation, INV = investment, DV = dependent variable.

, **, and *** denote 10%, 5%, and 1% significance levels, respectively.

The results show that the lag of the dependent variable (economic growth—GDPPC) is significant and positively related to its current value, suggesting that, growth in the previous year stimulates growth in the current year. We also find that the coefficient of FI is positive (2.5554) and significant at the 5% significance level. This suggests that a rise in the level of FI stimulates growth in the economies of the selected African states. More specifically, our finding shows that a unit rise in the level of FI would cause an average growth in the selected economies of 2.5554 at a 95% confidence level. The results thus confirm our hypothesis: H1a. The statistically significant relation between FI and economic growth satisfies the first condition of the Baron and Kenny mediation model. We explain the results here by the fact that an increase in FI enables the poor and marginalized to access and use financial services which enhances economic activity and improves national output. As observed by Singh and Stakic (2021) increase in the level of FI enhances liquidity in the financial system, and makes capital more affordable and widely available and this can work to promote economic growth.

Our results thus, confirm FI as a significant driver of economic growth in Africa. Policymakers across Africa should thus not relent in implementing far-reaching reforms that will bring the majority of the population into the mainstream financial sector. Our evidence is consistent with that of Kim et al. (2018), Sethi and Acharya (2018), and Van et al. (2021) who also find FI to positively influence economic growth. Our finding, however, contradicts those of Dahiya and Kumar (2020) and Huang et al. (2021) who established no relationship on one hand, and that of Erlando et al. (2020) and Nkwede (2015) who reported negative associations on the other hand.

Furthermore, amongst the three control variables used only investment was found to be significant and positively linked to economic growth. Trade openness was positive whilst government expenditure was negative. Though the sign of the coefficients is as one would expect, the relationships were both insignificant.

Non-Linearity in the Financial Inclusion and Economic Growth Nexus

One of the key contributions of this study is to establish the nature of the relationship between FI and growth. In other words, we sought to determine whether the relationship is non-linear as this could help explain to some extent the mixed findings reported by prior studies. To do this, we estimate Equation 2 which contains our measure of FI (financial inclusion index) and the squared term of the financial inclusion index as explanatory variables. The results are presented in column 3 of Table 4.

We find the coefficient of FI (FII) as shown in Table 4, to be negative and statistically significant (−20.0444; p < .01). However, the squared term of the financial inclusion (FII2) variable (included to test for non-linearity) is positively and significantly related to economic growth (1.5878; p < .01). The Wald χ2 is significant at the 1% significance level which means that variations in the outcome variable are significantly explained by the explanatory variables. Also, we do not reject the null hypothesis of the Sargan test of over-identification restriction, indicating that, there is overall exogeneity of the instruments used in all our models. The p-values for AR (2) indicate that there is no second-order autocorrelation. In sum, the postestimation diagnostics indicate a well-specified model. This is true for all the models specified in this study. We do not comment on the diagnostics for subsequent models for the sake of brevity.

The results reported on these two variables combined in Equation 2 give an indication of the presence of a non-linear association. The results suggest that initially, an increase in financial inclusion leads to a reduction in economic growth but subsequently, further increases in FI positively affect growth. The evidence thus suggests the presence of a U-shaped relationship between FI and economic growth; where at lower levels of financial inclusion, its influence on growth is observed to be negative but it turns positive at higher levels of FI. We explain that this is one of the reasons why past studies have reported a mixture of positive and negative findings. Our results therefore confirm the hypothesis: H1b, that, there is a non-linear association between FI and economic growth in Africa. We justify our results by arguing that, at lower levels of FI the problem of information asymmetry and inefficient or unproductive use of financial services is pervasive and this may negatively impact growth. Eventually, however, as financial inclusion continues to increase, the impact on growth becomes positive in that, information asymmetry becomes less of a problem allowing for better monitoring which goes a long way to ensure productive use of funds. We further explain this non-linear association by arguing that, as factors such as human capital develop with time, FI exerts a significant and positive influence on economic growth as people efficiently make good use of available financial products (See e.g., Sethi & Acharya, 2018). Our results are in tandem with that of Singh and Stakic (2021) who also report from their study of eight Asian countries that the positive influence of financial inclusion becomes noticeable only at higher levels of financial inclusion. Our results, which indicate the presence of a non-linear relation between inclusion and growth, also confirm the findings of Daud and Ahmad (2023) who report from their study that there is a threshold of financial inclusion required to realize the positive effect of financial inclusion on economic growth.

The Effect of Financial Inclusion on Human Capital Development

The second step as recommended in the Barron and Kenny mediation model, is to test the effect of FI on Human capital development. This relation is also specified in Equation 3, the results for which are presented in Table 4 (column 3). The lagged value of human capital development is observed to be positive and significant (0.8767; p < .01). We further find that FI exerts a positive (0.0245) and statistically significant effect on human capital development at the 5% significance level where a 1% rise in FI increases human capital development by 2.45%. We thus accept the hypothesis: H2, that FI exerts a significant positive effect on human capital development.

Our evidence here suggests that the living standards of the poor in Africa can be improved through the implementation of policies related to inclusive finance. Life expectancy could increase significantly where people will live longer and healthier and obtain quality education through inclusive finance. The finding on the inclusion and growth relationship is corroborated by similar evidence from Ababio et al. (2021), Datta and Singh (2019), Matekenya et al. (2021), Nanda and Kaur (2016), and Raichoudhury (2016). This is to be expected because, with access to finance, people are given the opportunity to turn around their economic fortunes for the better. It enhances their capacity to undertake various entrepreneurial activities, create wealth, and improve their quality of life.

Regarding the control variables, we find unsurprisingly that, investment is a significant driver of human capital in Africa. The other control variables are insignificant in terms of their effect on growth.

The Effect of Human Capital Development on Economic Growth

Following the Baron and Kenny Mediation model, we proceed to test for the third condition for mediation analysis which in our case involves the human capital and economic growth link. This relationship is specified by Equation 4 in the methodology section and the results are presented in Table 4 (column 5) above.

Our results show a statistically significant (p < .01) and positive (3,200.783) relation between human capital and economic growth. Consequently, we accept our hypothesis, H3 that human capital development has a significantly positive influence on economic growth. The implication therefore is that as the level of human development improves, the nation is better placed to experience significant growth in the level of economic activities. The reason is that, improved in human capital comes with enhancement in the quality of education and health status of the citizenry. A well-educated and healthy people are generally, more productive, and as productivity improves so too does the level of economic growth. This thus calls for attention by governments across the sub-region to focus on enhancing the quality of life of the populace by investing in quality educational and health systems.

Our evidence is consistent with that of Chowdhury et al. (2018), Eigbiremolen and Anaduaka (2014), Hakooma and Seshamani (2017), Han and Lee (2020), Poças (2014), Qamruzzaman and Karim (2020), Sethi and Acharya (2018). However, our result contradicts Adeyemi and Ogunsola (2016) who find an insignificant relation in the short-run and a negative long-run relation between human capital development and economic growth. With regard to the control variables, trade openness, and government expenditure are found to be significantly related to economic growth. Trade openness is positive (0.5014) whereas government expenditure is negative (−189.2803) and significant at 5% and 1% respectively. The negative relation between government expenditure and economic growth could be an indication that governments are not spending the things that could enhance the productive capacity of the economy.

The Mediating Role of Human Capital Development

According to Baron and Kenny (1986) once the three mediation conditions captured by the following hypotheses: H1a, H2, and H3 above have been confirmed, we can conclude that an indirect relationship exists between FI and economic growth. More specifically, we can conclude from the results so far, that human capital development is a conduit through which financial inclusion influences economic growth in Africa. To determine the exact nature of the mediation, Baron and Kenny (1986) recommend a final test as specified in Equation 5 the results of which are presented in Table 4 (column 6). Equation 5 is essentially the same as Equation 1. The only difference is that Equation 5 introduces the mediating variable (human capital development) into the model as one of the control variables. It is argued that, when there is no mediation amongst the variables, the inclusion growth relationship as estimated in Equation 1 will remain the same when re-estimated by Equation 5. However, if after controlling for the mediating variable as in Equation 5, the inclusion growth relation changes then we conclude that a mediation exists in the relationship (Baron & Kenny, 1986). The results presented in Table 4 (column 6) show that the inclusion-growth relation which originally was positive and significant per the estimation from Equation 1 (2.5554, p < .01) becomes insignificant but negative (−30.7435) when we control for human capital development (see estimations from Equation 5 presented in column 6 of Table 4). According to Baron and Kenny (1986), this result indicates that human capital development fully or completely mediates the FI and economic growth nexus in Africa. Thus, human capital development serves as a channel through which financial inclusion transmits into economic growth in Africa. Among the control variables only investment had a significant relationship with growth albeit negative (−56.0446, p < .05). According to Aladejare (2020), this is possible if the supporting factors that aid investment remain inefficient.

Our findings on the mediation of the inclusion-growth relationship by human capital development, provide an empirical confirmation of the theoretical argument advanced by Madichie et al. (2014), Ozili (2020), and Wang and Guan (2017). These authors all make arguments that suggest that to properly understand how FI affects economic growth there is the need to consider the role played by human capital development. Very few prior studies have attempted to test the possible mediation in the inclusion-growth nexus. The few mediators that have been empirically identified include mobile money penetration (Kpodar and Andrianaivo, 2011), gender (Swamy, 2014), and entrepreneurship and household consumption (Liu et al., 2021). Our study thus provides an addition to the literature by identifying human capital development as a mediator in the financial inclusion-growth nexus.

Robustness Analysis

To test for the robustness of our findings, we employ secondary school enrolment as an alternative measure of human capital development and re-test the following hypotheses: H1a, H2, H3, and H4. The results are presented in Table 5. Essentially, we re-estimate all the conditions necessary to establish mediation based on the Baron and Kenny (1986) model using secondary school enrolment in place of the human capital development index. The first condition is satisfied as financial inclusion is shown in Table 5 column 2 to exert a significantly positive (2.5554, p < .05) influence on economic growth. Furthermore, FI is found to exert a statistically significant and positive (9.3076, p < .05) influence on secondary school enrolment (see Table 5, column 3), which is also consistent with the findings from Table 4 when an index of human capital development is used. Again, consistent with the evidence from the original model in Table 4, secondary school enrolment is found to be positive and significantly related to economic growth (0.3454, p < .05; see Table 5, column 4), which satisfies another condition 3 of the mediation model adopted. To confirm the nature of the mediation, we include FI and secondary school enrolment in the same model with economic growth as the outcome variable (see, Table 5, column 5). Similar to the evidence from Table 4, financial inclusion becomes insignificant when secondary school enrolment is introduced, implying the presence of a complete mediation effect. The findings from Table 5 are therefore consistent with the findings results in Table 4, showing the robustness of our evidence to different measures of the mediating variable (human capital development).

Robustness Analysis.

Note. Robust standard errors are in (). GDPPC = GDP per capita growth rate, FII = financial inclusion index, SSE = secondary school enrolment, TO = trade openness, INF = inflation, INV = investment, DV = dependent variable.

, **, and *** denote 10%, 5%, and 1% significance levels, respectively.

Conclusion and Policy Implications

Conclusion

Achieving a higher level of FI has become the target of government policies across the globe, especially in the developing world. It is believed that it generally has positive spill-over effects on the economy. This paper sought to investigate the channels through which FI may transmit into economic growth by focusing the searchlight on human capital development. This is because even though the theoretical literature has presented human capital development as a major transmission channel it has not been empirically tested. Based on the recommendations of Baron and Kenny (1986) four hypotheses were tested in other to achieve this goal. The results satisfied all four conditions for mediation analysis. All the hypotheses tested were confirmed by our results. The study established that a significantly positive relationship exists between FI and economic growth and that this relationship is u-shaped in Africa. Financial inclusion was also found to significantly influence human capital development positively. In addition, we also found that human capital development significantly influences economic growth in Africa. Finally, our results show that human capital development mediates the financial inclusion-economic relationship link in Africa.

This paper has made contributions to the literature in diverse ways. First, previous studies have assumed a linear relation between financial inclusion and economic growth. This has led to so many studies on the topic with mixed findings and conclusions. In this paper, we tested the possible non-linearity in the relationship and found that the inclusion-growth relationship is quadratic in nature. To our knowledge, this is the first time a study of this kind has been conducted in Africa. We established that FI initially exerts a negative influence on growth but eventually, the effect becomes positive. The relationship is negative at lower levels of financial inclusion and positive at higher levels. This helps us to partly address the inconsistencies in the findings of prior studies in this area.

Second, it was also found that though FI significantly affects economic growth, it does so indirectly through improvement in the level of human capital development. Even though this is not the first time a mediation analysis has been done on the inclusion-growth relationship in Africa, it is the first time an important variable like this (human capital development) has been considered in explaining the inclusion-growth relationship.

Implications of Findings

Policy Implication

The findings of this study make significant contributions that present important implications for policy, practice, and research. Our current study makes an important contribution in that the findings provide critical policy implications that can influence policy thinking in the continent of Africa. For instance, based on our findings, we conclude that the link between FI and economic growth in Africa is ‘U’ shaped. It is only at a high level of FI that we observe its beneficial influence on economic growth. The policy implication for governments in Africa is that, for African countries to enjoy the growth benefits of FI, governments need to intensify their financial inclusion efforts. To achieve this, governments need to be deliberate and very aggressive in their design and implementation of strategies that will speed up the attainment of close to universal inclusion of the adult population in the mainstream financial system. This is crucial given that Africa has the lowest level of financial inclusion (Makina & Walle, 2019).

Traditional ways of providing financial services will have to give way to ICT. Technology allows for the design and efficient delivery of financial services to a greater percentage of the population. The convenience and affordability benefits that accrue to clients enhance participation in the formal financial system. Governments across the continent ought to consider making significant investments in providing the requisite ICT infrastructure that the private sector can leverage to extend financial services to the populace.

In addition, a lot of people in Africa appear to be rural. Most formal sector financial institutions also appear to stay away from the rural areas which greatly hinders the inclusion of rural dwellers in the financial system. A policy shift that will twist the regulatory frameworks in ways that can attract financial institutions to extend their services to rural areas is critical if the goal of attaining a near-universal FI in Africa is to become a reality.

Furthermore, attention must be paid in policy making to ensure that any other policies that could be counterproductive to the financial inclusion agenda are avoided. For instance, through the adoption of ICT, we are witnessing a rise in mobile phone usage and internet technology in providing various financial services in Africa. whilst this is good, recent attempts by some governments to introduce taxes on financial transactions conducted via mobile phone for instance (as in the case of Ghana) can have costly consequences on the financial inclusion targets. If such taxes are too high, they could discourage the usage of such services and reverse any financial inclusion gains made. Governments should thus any taxes imposed on such services are well thought through. The taxes should not be too high to the point where that can discourage the use of related financial services.

We conclude that the benefits of financial inclusion are transmitted through human capital development to economic growth. Therefore, African governments that aspire to promote economic prosperity should not only focus on enhancing financial inclusion but in addition to that, they should also seriously implement policies that will enhance the educational and health infrastructural needs of the people. As people have better accessibility to financial services, they can raise their level of human development via access to quality health care and education services. This will then translate into economic growth across the continent. Based on our evidence, governments that wish to design their economic growth strategies around financial inclusion must consider a more holistic framework that captures human capital development otherwise the expected benefits will be missed.

Implications for Practice

Once, our study has thrown up some policy implications, the necessary policy changes can influence practice across the financial sector. Even before policy changes are implemented, private sector Banks should take advantage of the rising adoption of ICT in Africa, to reach out to the unbanked via various ICT channels. This will not only aid in the achievement of governments’ financial inclusion agenda but also will boost the revenue mobilization of such institutions (a win-win solution for all). Our findings also underline the need for governments, civil society organizations, religious bodies amongst others to embark on educating the various segments of society on issues of financial literacy. When financial literacy levels rise, we are most likely going to see the attainment of higher levels of financial inclusion in Africa.

Limitations and Implications for Research

The findings from this study also carry important implications for research in the broad area of FI and economic growth. Though a lot of studies have been conducted in this broad area already, our study contributes significantly to the conversation. We enrich the existing literature. For instance, by testing for non-linearity in the nexus between inclusion and growth, our findings now improve our understanding of why the findings from previous studies are mostly mixed. Furthermore, our consideration of a third variable (human capital) in the financial inclusion and economic growth relationship has provided insights into one of the most critical channels through which the benefits of FI can be harnessed into economic growth. These are insights that were not previously known from the available literature in our current context. Apart from the fact that the findings here enrich our understanding of the existing body of research, it also opens a wide range of areas that could be explored to further broaden knowledge in the topic area for greater impact in the future.

As important as our study is, it has its limitations. Firstly, though we established a U-shape relationship between FI and growth, we did not consider the threshold at which this effect becomes positive. Secondly, the study was based on a dataset from the pre-COVID-19 pandemic era. The period during and after COVID-19 has brought about changes in the way households access goods and services and how payments are made for them. This has implications for financial inclusion but the unavailability of data at the time of conducting this study did not permit us to consider how this global phenomenon could have affected the outcome of our study. Finally, there are a range of factors that can moderate the financial inclusion and growth relationship with important policy implications. However, the focus here was to examine the indirect, pass-through channel in the inclusion growth relationship rather than the interaction/moderating effects.

Consequently, our study has some implications for future research which are outlined as follows. Attention should be directed toward conducting threshold analysis in the future. This will help governments determine the minimum level of FI required to spur growth. Future research could also extend our data beyond the COVID-19 pandemic era to establish whether the pandemic makes any difference in our outcomes. Going forward researchers with interest in this area should venture into comparative studies. This will allow us for instance, to establish whether our findings here vary depending on income level, level of financial development, political and economic stability, and institutional and regulatory quality amongst others.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data available on reasonable request.