Abstract

Gender interests are crucial in the redistributive equity of the pension system. This paper investigates the gender gap in retirement pension incomes of urban employees in China by using data from the Chinese Household Income Project and decomposes the main factors contributing to the gender gap. We find that the pension income of female employees after retirement is significantly lower than that of male employees. Decomposition reveals that age, pre-retirement wage level, and type of work unit are the main factors contributing to the gender gap. Further, we find that the gender gap in pension incomes is lower for employees employed in the public sector than for those employed in enterprises, because enterprises are more affected by the market environment than the public sector, and female employees tend to suffer more market discrimination. In general, females still face the challenge of having significantly lower pension standards than males after retirement.

Plain language summary

Pensions serve as a primary source of economic support for many insured employees after retirement, guaranteeing them a basic standard of living. However, gender inequality in pension income is evident in social life, with the pension income of female employees often lower than that of male employees. This study confirms this phenomenon by examining the gender gap in pension income for urban employees in China. The study finds that age, pre-retirement wage level, and type of work unit are the main factors contributing to the gender gap. In addition, the gender gap in pension income is smaller for public sector employees compared to enterprise employees, due to China’s unique market environment, where the pension income of female enterprise employees is more negatively affected by market discrimination. Therefore, policy recommendations are proposed to appropriately extend the statutory retirement age for females, increase the wage level of the female labor force, and allow females to share their husbands’ pensions. These recommendations aim to increase the pension incomes of female employees after retirement, thereby averting their risk of elderly poverty.

Introduction

China has formally entered into an aging society in the 21st century, and population aging has become one of the important issues facing China’s social development. According to data from the sixth population census of China in 2010, the proportion of people aged 65 and over in the total population was 8.9% (National Bureau of Statistics, 2010). However, according to the data from the seventh population census of China in 2020, the proportion has risen to 13.5% (National Bureau of Statistics, 2020). Compared with 2010, the proportion of the elderly population has increased by 4.6 percentage points. This means that the aging of China has further deepened, and it is impossible to ignore the problem of pension income for the elderly population after retirement. The average life expectancy of Chinese males in 2020 is 75.37 years, while the average life expectancy of females is 80.88 years, which is 5.51 years higher for females than for males. Compared to males, females have a longer life expectancy after retirement, face greater longevity risks, and require more adequate pensions to sustain their retirement life.

The lack of access to adequate pension benefits stands as a significant factor contributing to markedly higher rates of old-age poverty among females compared with those in males. According to the OECD, the average old-age poverty rates for females and males are 16.2% and 11.6%, respectively (OECD, 2021), and the average old-age poverty rate for females is 4.6 percentage points higher than that of males, which implies that females are likely to have a lower overall standard of living than males in their retirement years. The current pension insurance system in China fails to provide adequate old-age protection for females, who have weaker indicators in the three aspects of the coverage rate, the level of benefits, and the substitution rate than males (Chen & Huang, 2018). Furthermore, the data from the seventh population census in China show that, among the widowed elderly population aged 60 and over in 2020, the proportion of female widows was 73.1%, and the number of female widows was 2.72 times higher than the number of male widows, which made it more difficult for females to share in the pension from their male husbands. In the above background, attention to the issue of pension income security for elderly female employees after retirement becomes paramount.

The pension income in this paper refers to the funds obtained by urban retirees from pension plans, while the gender gap refers to the income gap between males and females in pension benefits. As an important research topic in the field of social security, studying the gender gap in pension income is of significant importance for promoting the fairness of the pension insurance system and achieving common prosperity.

The contribution of this study is to examine the extent of the gender gap in pension income among urban employees in China and identify the main factors causing this gap. In addition, it aims to propose potential solutions to narrow the gender pension gap in China. The novelty of this study lies in the use of a combination of regression analysis and decomposition analysis, which addresses the limitations of previous studies solely employing actuarial models to examine the gender gap in pension income. Actuarial models primarily focus on comparing pension system parameters, without adequately considering the impact of variables related to basic personal characteristics and lacking reflection on the gender gap in real life. The purpose of this study is to conduct a more comprehensive analysis of the gender gap in pension income in China by combining regression analysis with decomposition analysis.

Literature Review

The pension insurance system serves as a vital instrument for income distribution regulation (Y. Z. Wang et al., 2016). However, in the face of population aging, the system’s positive impact on overall income distribution is diminished (W. Wang & Jin, 2022). In examining the fairness of income redistribution within the pension insurance system, gender interests emerge as a critical component.

The gender gap in pension income exists in many countries. Most scholars have investigated the gender gap in pension income through micro-databases. Based on the European Union Statistics on Income and Living Conditions, Zanier and Crespi (2015) found that the average pension gender gap in the EU-27 is 39%, with 4% in Estonia, 12% in Lithuania, 15% in Hungary, 27% in Belgium, 34% in Portugal, 36% in Italy, 38% in France, 42% in Austria, and 46% in Luxembourg. Based on the Survey of Health, Aging and Retirement in Europe, Haan et al. (2017) found that women received 19.6% less retirement pension income annually compared to men of the same age in Denmark. Based on the Linked-Employer-Employee-Data of the IAB, Niessen-Ruenzi and Schneider (2022) found that a substantial gender pension gap in Germany of about 26% on average still exists. Based on data from the China Health and Retirement Longitudinal Study in 2013, Y. F. Yang et al. (2016) found that the average pension income of female elderly in China was only 39.9% of that of male elderly. Similarly, based on data from the China Health and Retirement Longitudinal Study in 2015, Zhan (2020) found that the pension income of male elderly in China is about 1.9 times higher than that of female elderly. Drawing on data from China’s National Bureau of Statistics in 2020, Lu and Dandapani (2023) found that white-collar females retire with a monthly pension payment of only 66% of the pension level of males, while blue-collar females retire with a monthly pension payment of only 52% of the pension level of males. All of the above studies point to the fact that male pension income is higher than female pension income.

The pension income of employees is intricately linked to the labor market, where female disadvantage directly results in the gender gap in pension income (R. Zhao & Zhao, 2018). Substantial disparities in employment between males and females significantly contribute to discrepancies in pension entitlements, with pension payments for males being 26% higher than those for females across 34 OECD countries (OECD, 2021). Moreover, the level of pension benefits is intricately linked to various factors such as wage income, employment status, and career continuity, as noted by Sun and Ji (2017). Female inequality in the labor market manifests in these areas in distinct ways. Compared to their male counterparts, females often work fewer hours, with their employment typically concentrated in lower-level and lower-wage positions (Glass & Fodor, 2011; Warren, 2006). Traditional gender roles further exacerbate this disparity, as women typically shoulder more household labor and childcare responsibilities than men. Consequently, female employees are more likely to transition from full-time to part-time work or experience career interruptions due to child-rearing responsibilities (Chhaochharia et al., 2021; Y. Wang & Zhang, 2018). Consequently, women encounter a “motherhood penalty” in terms of wages (Anderson et al., 2002; Harkness & Waldfogel, 2003; Kingsbury, 2019) and experience a more fragmented pension contribution period (Bonnet et al., 2018), further impacting their engagement with the pension insurance system and consequent redistributive benefits. In general, lower incomes for women throughout the life cycle translate directly into lower entitlements to pension assets (Kuhn, 2020).

Moreover, the design and reforms of the pension insurance system also contribute to gender disparities in pension income. The retirement age dictates the number of years of employment, and the lower retirement age for women results in reduced accumulated contributions to pension accounts, leading to lower pension incomes post-retirement compared with that for men (H. D. Wang & Li, 2013). Notably, the structural differences within China’s pension insurance system, characterized by a multi-track system, exacerbate the pension income divide among elderly people (Zhang et al., 2022). Public sector employees typically enjoy significantly higher pensions than those in the private sector, while employees in monopolistic industries receive higher pensions than those in competitive industries. Additionally, individuals employed in the eastern region of China tend to receive higher pensions than their counterparts in the central and western regions (Hou & Cheng, 2015). W. Wang et al. (2023) found that under the dual-track pension system reform, retirees from the public sector generally have a significant pension advantage compared to those from the non-public sector, which declined from 2013 to 2015 and then increased from 2015 to 2018. In addition, the pension reforms could also increase the gender pension gap, such as the application of the pro-rata mechanism additionally penalizing women’s pension (Abatemarco & Russolillo, 2023).

Additionally, disparities in investment behavior between genders contribute to the gender pension income gap. Variations in risk preferences lead to differences in the levels of asset management and investment returns between female and male employees (Austen et al., 2014; Sunden & Surette, 1998). Furthermore, financial literacy plays a crucial role in investment decision-making (Huston, 2010), and women generally exhibit lower levels of financial literacy than men (Lusardi & Mitchell, 2008). This often results in a more conservative approach to investing among women, leading to lower investment returns compared with those for male counterparts (Almenberg & Dreber, 2015). The cautious investment behavior and subsequent lower investment returns of women further widen the income gap with men after retirement. Niu et al. (2020) found that a significant portion of the Chinese population, particularly the elderly, women, and individuals with lower levels of education, lack financial knowledge. In China, the gender disparity in investment behavior is more evident in the willingness to purchase personal pension products (Zhuang & Wang, 2022). The cautious investment behavior and subsequent lower investment returns of women further widen the income gap with men after retirement.

The repercussions of the pension income gap extend beyond mere financial disparities, impacting various aspects of individuals’ well-being. Women often experience lower income and consumption levels than men due to this gap, resulting in poorer housing quality, deteriorated health conditions, and increased social isolation (Kvist, 2015). Moreover, Intra-generational inequality in China’s pensions not only widens the income gap between groups of older people, but also between children and grandchildren when inter-generational economic exchanges are taken into consideration (Y. N. Yang et al., 2019).

The existing conclusions and methodologies from scholars investigating the gender pension income gap provide valuable reference points for the present research. However, the literature on China’s pension income gap from a gender perspective remains limited and lacks sufficient depth for thorough exploration and analysis. Furthermore, there are some differences between China’s labor market environment and pension system and those of other countries in the world, and international comparisons alone cannot fully explain the reasons for the gender pension income gap in China.

Therefore, this paper focuses on the gender gap in pension income as its primary research entry point, proposing the research hypothesis that there is a significant gender gap in pension income among retired urban employees in China. Utilizing data from the Chinese Household Income Project, the study examines the gender gap in pension income among retired urban employees in China. Through this research, we aim to gain a deeper understanding of the underlying causes of the gender gap in China’s pensions and propose targeted policy recommendations.

Pension Scheme in China

The current pension insurance system in China comprises three primary pillars. The first pillar is the State-dominated basic pension insurance system, which includes both a coordinated account and an individual account. Contributions for the coordinated account are set at 16% for the work unit, while individuals contribute 8% to their individual accounts. Both accounts require a minimum contribution period of 15 years. Upon retirement, the monthly pension payment standard for the coordinated account is determined based on the average monthly wages of local employees in the previous year and the average indexed monthly contribution wages of the employee. The monthly standard for individual account pensions is the amount accumulated in the individual account divided by the number of months for which the pension is payable. The number of months of payment is determined based on factors such as the employee’s retirement age, life expectancy, and interest rates, among other relevant considerations.

The second pillar is the employer-dominated pension system, which includes enterprise annuity and occupational annuity. The distinction between these systems is as follows: (1) Enterprise annuity primarily benefits enterprise employees, while occupational annuity primarily benefits public sector personnel. (2) Participation in an enterprise annuity is voluntary, whereas participation in an occupational annuity is mandatory. (3) Retirees receiving benefits from enterprise annuities can choose between a one-time sum payment or periodic installments, while retirees of occupational annuities receive their benefits on a monthly basis.

The third pillar comprises personal-dominated savings pension insurance and commercial pension insurance, supported by government policy, voluntary participation by individuals, and market-oriented operation. This pillar implements tax incentives in China, typically exempting contributions and investment earnings from taxation, with taxation occurring only at the retirement collection stage. However, due to a lack of knowledge and experience, many Chinese are still unaware of or unfamiliar with the third pillar pension scheme (Niu et al., 2020).

The development of a multi-pillar pension insurance system in China aims to address the increasingly diverse and multi-level needs of the elderly population, mitigate the various risks associated with aging, and combat elderly poverty (Y. N. Yang, 2022). Li et al. (2020) found that for every 1% increase in public pension expenditure, the Gini coefficient decreases by 0.8% in China. Zhou and Tan (2021) decomposed the sources of income among the elderly in China and found that the contribution of pension income to income inequality among the elderly has decreased. This suggests that the pension system has played a role in decreasing the Gini coefficient and has had a redistributive effect on income.

The standard of basic old-age pension insurance benefits in China has been steadily increasing, as illustrated in Table 1. However, factors such as age, education level, and labor market discrimination have led to a gender imbalance in pension redistribution (R. Zhao & Zhao, 2018). Consequently, elder male individuals tend to receive higher pension benefits compared with their female counterparts. Moreover, considering the growing elderly population and declining birth rates in China, the pressure on public expenditure for pension insurance is expected to rise further. Q. Zhao and Mi (2019) estimated the annual pension gap of China’s urban employee basic pension insurance system and found that the cumulative balance of the pension plan will be depleted by 2035. As a result, elderly female individuals may face a decline in pension levels in the future, potentially leading to a lack of sustainable basic income security and an increased risk of declining living standards among this demographic.

Adjustments to China’s Basic Pension Insurance Benefits Since 2010.

Source. Circular of the Ministry of Human Resources and Social Security and the Ministry of Finance of China on the Adjustment of Retirees’ Basic Pension in Past Years.

Research Methodology

Methods

The main methods employed in this study are regression analysis and decomposition analysis. Regression analysis is utilized to establish the pension income equation for the elderly in urban China. Decomposition analysis can be paired with regression models to link outcome variables to individual characteristics, to help us gain a deeper understanding of the underlying causes of gender differences in pension income among different demographic groups. This method identifies the contributions of various factors, such as education level, wage level, and type of work unit, to the gender gap in pension income, while also determining the most significant influencing factors. Such comprehensive analysis aids in accurately determining the most effective interventions to reduce the gender gap in pension income.

We employ the Oaxaca–Blinder decomposition, as proposed by Oaxaca (1973) and Blinder (1973), to facilitate a comprehensive understanding of the factors contributing to the gender pension gaps across different groups. Initially, pension income equations are separately formulated for elderly male and female individuals in urban China.

where

The gender pension income gap for the elderly in urban China can be decomposed as follows:

The formula can be transformed into:

The formula indicates that the pension income gap for the elderly in urban China can be decomposed into two components.

Data Sources and Description

We use data from the 2018 urban sample of the Chinese Household Income Project. The database tracks the dynamics of income distribution among Chinese residents and provides detailed basic information on the elderly group, including individual age, education level, employment status, pension income, etc., which provides data source support for this paper to carry out the research on the gender gap in the pensions of Chinese urban employees and its causes.

In accordance with the needs of the study, this paper begins with the pre-processing of the data. Firstly, the sample of the elderly group is selected according to the legal retirement age. Secondly, the main research object of this paper is urban workers, so the sample data of the new rural social pension insurance type is excluded. Thirdly, the sample data of missing pension income is excluded. After the above pre-processing, the total sample size of the study is 3,876, of which the male sample size is 1,912 and the female sample size is 1,964.

The explanatory variables of the model in this paper are the logarithm of individual pension income, the core explanatory variable is gender, and the control variables include individual characteristics and basic social characteristics affecting pension income such as age, level of education, type of household registration, type of work unit, type of occupation, logarithm of pre-retirement wage, and region (Zhan, 2020; R. Zhao & Zhao, 2018). The descriptive statistics of these variables are presented in Table 2.

Variable Names, Definitions, and Descriptive Statistics.

To provide a more illustrative depiction of pension income among Chinese urban employees, the study details the pension income of male and female employees across different age groups, education levels, types of units, and occupations. Detailed results are displayed in Table 3, with amounts expressed in Chinese Yuan (CNY) for clarity and consistency.

Data Descriptive Statistics.

Source. 2018 Survey data from the Chinese Household Income Project (CHIP).

Overall, the average monthly pension for females is 3,013 Chinese Yuan (CNY), which is 822 Chinese Yuan (CNY) less than that of males. It is evident that as employees’ age increases after retirement, their pension incomes also increase. Additionally, individuals with higher education levels have higher pension incomes after retirement. Moreover, employees working in the public sector generally receive higher pension incomes after retirement compared with those employed in enterprises. Furthermore, white-collar employees have higher pension incomes after retirement than blue-collar employees. However, it is notable that in all of these aspects, the pension income of males is consistently higher than that of females.

Research Results

Gender Gap and Decomposition of Urban Employee Pension Income

We conducted OLS on pension income, in which males, under 60 years old, illiterate, agricultural households, blue-collar, and center-western region are the reference groups, and the results are shown in Table 4.

Urban Employee Pension Income Regression Results.

Source. 2018 Survey data from the Chinese Household Income Project (CHIP).

Note. Standard errors are presented in parentheses; Significance level: ***p < 0.01.

We proceed to discuss the results of the regression estimation. According to Table 4, the estimated coefficient of pension income for female employees is significantly lower than that of males, being 13.5% less than that of male employees. The pension income of employees is significantly correlated with their age, being 11.7%, 20.1%, and 41.6% higher for employees aged 60 to 69, 70 to 79, and 80 and over, respectively, than for employees aged under 60. This phenomenon can be attributed to both the normal adjustment mechanism for basic pensions established by the government, which elevates the level of basic pension benefits in alignment with factors such as the growth of average wages and price inflation (as depicted in Table 1), and the effect of individual account funds held by retired employees, which serve to preserve and increase the value of pension funds, thus enabling the accumulation of more pension wealth.

The positive gradient effect of education is also significant. Employees who have completed primary school, junior high school, Senior high school and above, undergraduate and above have higher pension incomes than those who are illiterate. The pension income of employees with non-agricultural household registration (urban household registration) is 23.8% higher than the pension income of employees with agricultural household registration. It should be noted that the conditions for participation in pension insurance for employees working in China are not defined on the basis of their household registration. The pension income after retirement of employees in the public sector is 28.4% higher than that of employees in enterprises, and the pension income after retirement of white-collar employees is 13.3% higher than that of blue-collar employees. Both the type of work unit and the type of occupation are closely linked to the labor market environment. For each 1% increase in the average monthly wage prior to retirement, the pension is increased by 0.054%. The pension incomes of employees in the Eastern region are 9.4% higher than those of employees in the Center-Western region, which is due to the higher level of economic development of the cities in the Eastern region of China, having a favorable market environment. In the Eastern region, there is a greater willingness of work units to contribute to social security for their employees. Simultaneously, the level of contribution to the pension system has increased due to the relatively high income of employees.

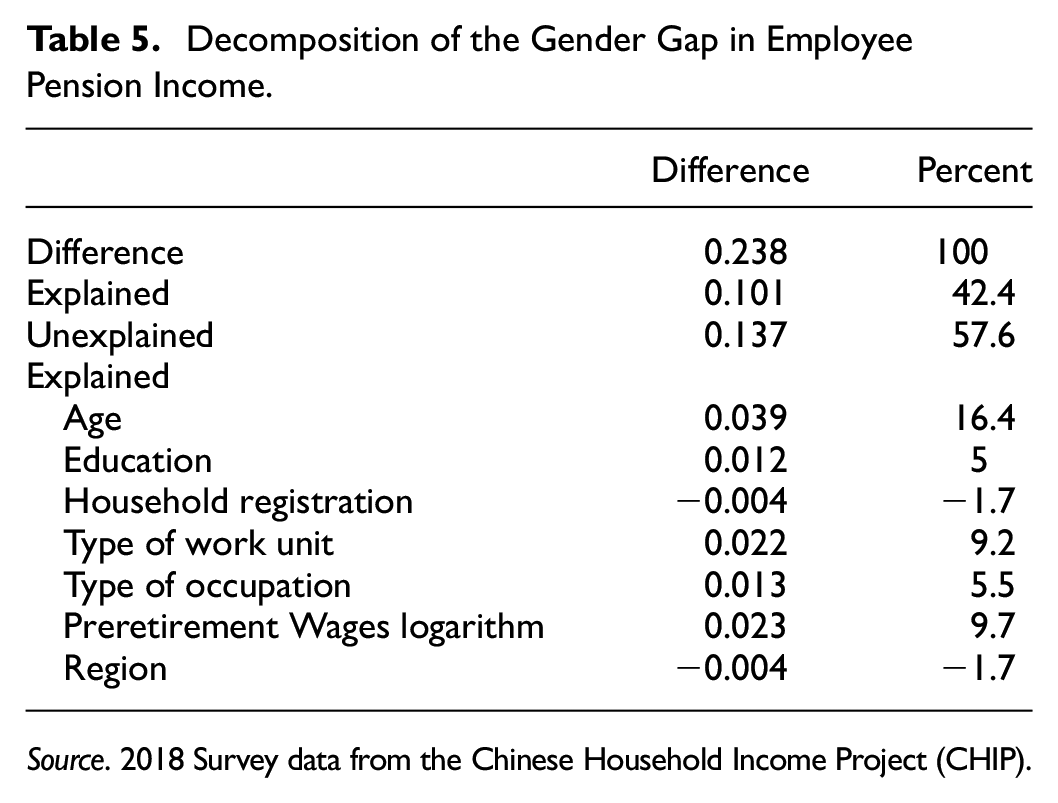

Following the regression results presented in Table 4, we proceed to decompose the gender differences in pensions for urban employees. The decomposition results are summarized in Table 5.

Decomposition of the Gender Gap in Employee Pension Income.

Source. 2018 Survey data from the Chinese Household Income Project (CHIP).

In general, the observed effects of personal characteristics explain 42.4% of the gender gap in employee pension income, while the unexplained portion is 57.6%, which implies a greater impact of market discrimination. The age difference explains 16.4% of the gender pension income gap. This disparity is primarily attributed to the gender difference in the statutory retirement age in China, where female employees typically retire 5 to 10 years earlier than their male counterparts. Consequently, females withdraw from the labor market earlier, resulting in shorter years of pension insurance contributions and a lack of regular wage income during this period.

The gender difference in the logarithm of pre-retirement wages accounts for 9.7% of the gender pension income gap. These wage discrepancies negatively impact the future pension income of employees. Differences in the gender type of work unit and type of occupation explain 9.2% and 5.5% of the gender pension income gap, respectively. Notably, gender differences in household registration and region have contributed to narrowing the gender gap in pension income. This is attributed to the relatively favorable labor market environment for females in eastern urban regions with higher levels of economic development, resulting in a higher labor market participation rate for females and increased contributions to the pension system, thereby partially reducing the gender gap in pension incomes.

Gender Gap and Decomposition of Pension Income of Urban Employees in Different Types of Work Units

The employment attributes of employees in China can be divided into authorized strength employment and non-authorized strength employment. The positions with authorized strength are called “iron rice bowls,” meaning that you can enjoy a stable wage and benefits within the authorized strength, the risk of dismissal is minimal, and the type of work unit is often public sector. Non-authorized strength positions, based on contractual agreements, lack the stability of authorized strength roles and are more common in enterprises.

To delve deeper into the gender income gap in pensions across various workplace types, we performed Ordinary Least Squares (OLS) regression analysis on the pension income of employees within two distinct types of work units. The findings are presented in Table 6.

Pension Income Regression Results for Employees With Different Types of Work Units.

Source. 2018 Survey data from the Chinese Household Income Project (CHIP).

Note. Standard errors are presented in parentheses; Significance level: **p < 0.05, ***p < 0.01.

According to Tables 2 and 6, the pension income of retired employees of the public sector is higher than that of retired employees of enterprises. There are significant gender gaps in the pension income of employees in different types of work units, but the gender gaps in pension income are significantly larger for employees within enterprises than for employees within the public sector. This is mainly due to the fact that the majority of current elderly individuals retired before October 1, 2014, a time when contributions to and the payment of pensions for employees of the Chinese public sector were typically covered by state finances. In contrast, the pension insurance contributions of enterprise employees are often based on the principle of more contributions, more payouts, and longer contributions, more payouts, with contributions being jointly borne by the person and the enterprise. Compared with their counterparts in the public sector, employees in enterprises encounter various disadvantages, including issues such as omitted or misappropriated contributions to employee pension insurance by the enterprises, a wider gender wage gap, and higher career instability. These factors contribute to widening the gap in retirement pension incomes between employees in these two types of work units.

Moreover, the market economy affects enterprises in China more significantly than the public sector, exacerbating gender disparities in the labor market, particularly in terms of the impact of pension insurance under these two types of units. As a result, the gender gap in pension incomes tends to be narrower among public sector employees and wider among those in private enterprises. Factors such as age, educational level, household registration type, occupation type, pre-retirement wage level, and region can all influence pension income. An interesting observation is that a higher education level has a more notable impact on the pension income of public sector employees than that of the individuals in private enterprises.

Next, we decompose the gender gap in pension income of internal employees under different types of work units, and the results are shown in Tables 7 and 8.

Decomposition of the Gender Gap in Employee Pension Income in the Enterprise.

Source. 2018 Survey data from the Chinese Household Income Project (CHIP).

Decomposition of the Gender Gap in Employee Pension Income in the Public Sector.

Source. 2018 Survey data from the Chinese Household Income Project (CHIP).

Through the decomposition of the gender gap in the pension income of employees in different types of work units, we find that labor market discrimination makes the greatest contribution to the gender gap in the pension income of employees within enterprises, indicating that female employees working in enterprises suffer more from gender discrimination. The main reason for this is that, compared to the public sector, enterprises are self-sustaining and their operating conditions are often influenced by the market environment. As a result, females are exposed to the risk of forced career interruptions and lower wages, which prevents them from participating in and contributing to the pension insurance system in a regular manner. This further leads to a lower accumulation of contributions in female pension accounts than males, which may ultimately lead to an overall lower level of future pension income for females than for males.

Among the differences in the personal characteristics of enterprise employees, differences in age and pre-retirement wage levels are the main factors affecting the gender gap in pensions, explaining 13.62% and 6.81% of the pension income gap, respectively. Among the gender gaps in the pension income of employees within the public sector, differences in the personal characteristics of the employees contribute the largest amount, with age differences explaining 45.04% of the pension income gap. The main reason for this is that employees working in the public sector often face mandatory retirement when they reach the statutory retirement age, and female employees therefore withdraw from the labor market earlier than their male counterparts. Conversely, female employees in the public sector experience less gender discrimination in the market compared to those in enterprises. This is primarily because wages and benefits in the public sector are typically funded by local governments and are less susceptible to the risk of layoffs. Notably, we find that education significantly reduces the gender gap in pension incomes among public sector employees. Overall, retired employees in the public sector generally enjoy a more significant pension advantage than retired employees in enterprises.

Conclusion

In the background of China’s policy of common prosperity, pensions serve as a crucial source of income to ensure the basic living standards of elderly individuals after retirement, playing a significant role in narrowing the wealth gap. The unequal distribution of pensions exacerbates disparities in the living standards of the elderly, which is contrary to the value-oriented goal of achieving common prosperity in China. Against the backdrop of China’s aging population, females are experiencing longer life expectancies and constitute a growing proportion of the elderly population (Zhan, 2020). Therefore, female elderly individuals face increasingly formidable challenges in terms of income security.

Our study reveals persistent gender gaps in pension levels during retirement. Key findings include a significant gender gap in urban employee pension income, with female retirees experiencing a 13.5% lower income compared with their male counterparts. Decomposition analysis identifies age, pre-retirement wage levels, and gender differences in work unit type as primary contributors to this gap, accounting for 16.4%, 9.7%, and 9.2% respectively. The gender disparity in age primarily stems from discrepancies in retirement ages under statutory pension systems, with women retiring 5 to 10 years earlier than men. This variance translates to differences in pension account contributions and accumulations, thereby serving as a major determinant of pension income discrepancies. Notably, gender gaps in pension income are narrower among public sector employees compared with those among their counterparts in enterprises. This is largely attributed to the market’s greater influence on enterprises and the heightened discrimination faced by female employees therein, which is consistent with the findings of Y. K. Wang and Xia (2021). It is evident that female retirees from the public sector generally enjoy more substantial pension advantages than those from enterprises. To narrow the gender gap in pension incomes and ensure a basic standard of living for elderly individuals, especially females, post-retirement, we propose the following policy recommendations:

First, it is imperative to appropriately delay the retirement age for female employees. Currently, under China’s statutory retirement system, females are mandated to retire 5 to 10 years earlier than men. This discrepancy means that females contribute to pension insurance for significantly fewer years than men, resulting in substantially lower accumulated funds in their pension accounts and consequently lower future pension benefits compared with men. Data from the seventh population census of China in 2020 suggest that the average life expectancy of females exceeds that of males by 5.51 years, highlighting the feasibility of raising the retirement age for females. Early retirement for females, especially at a stage when their career earnings typically peak, leads to forfeited future pension benefits. Delaying the retirement age for females appropriately will ensure gender equality in opportunities to work and accumulate pension benefits, thereby effectively narrowing the gender gap in pension incomes post-retirement.

Second, it is crucial to increase the wage level of the female labor force. The gender wage gap prevalent in the labor market directly translates into discrepancies in pension income between genders. Typically, pension contributions are closely tied to an employee’s wage level, with higher wages providing a larger base for personal pension contributions. Females, as a disadvantaged group in the labor market, consistently earn lower wages than males. Consequently, even with equal years of employment and pension insurance contributions, females contribute less to their pensions compared with males, resulting in lower pension income post-retirement. Establishing a fair mechanism for wage increases aligned with market dynamics is essential to ensure that all employees, particularly females, receive justifiable wage increments. This effort aims to rectify the disadvantaged position of females in the labor market concerning wages. By fostering increased earnings throughout their careers, females can approach contribution levels akin to those of males in pension insurance, thereby narrowing the gender gap in pension income after retirement.

Third, females are allowed to share in their husband’s pensions. Within the family, females usually bear the major responsibility for childbearing and child-rearing. However, this division of roles often results in females interrupting their careers at times or engaging in informal work such as part-time jobs. This phenomenon has led to a reduction in female wages and to the interruption of pension contributions, which has had a negative impact on their pension income after retirement. Undeniably, females often make sacrifices for the well-being of their families, and it is unfair for them if they are rendered incapable of ensuring a basic standard of living post-retirement due to these sacrifices. Thus, implementing the practice of allowing females to share their husband’s pensions will offer them financial support during their retirement, acknowledging the sacrifices they have made for their families and in the labor market. This ensures that they can access a portion of the pension income. Undoubtedly, this measure can help address female poverty in old age and promote gender equality and social justice.

Limitations and Future Research Directions

This study only focuses on gender inequality in pension income among urban employees and does not cover the floating population and rural residents. Compared to urban employees, the floating population and rural residents are considered vulnerable groups under the current pension system. Therefore, future research on gender inequality in pension income should also include these two groups.

For research on gender inequality in pension income, the timeliness of data is particularly crucial. However, the data from the Chinese Household Income Project is only available up to 2018, which does not adequately reflect the current status of gender disparities in pension income. As a result, future research could consider using updated data sources to ensure that the research findings remain consistent with the current situation.

Footnotes

Acknowledgements

We want to appreciate Ruiyang Liu and Yanhong Long for their assistance with collecting the literature for this manuscript.

Author Contributions

Conceptualization, Validation, Supervision, Writing-original draft, Writing-review & editing: Dehua Li; Data curation, Methodology, Software, Visualization: Juling Niu.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Supported by Hunan Provincial Innovation Foundation For Postgraduate (Grant ID: CX20220576) and Study on the Construction of Non-Contributory Pension System for Urban Workers in Lianyungang City (Grant ID: 23LKT006).

An Ethics Statement

No animal studies are presented in this manuscript. Ethical review and approval were not required for the study on human participants in accordance with the local legislation and institutional requirements. No potentially identifiable human images or data are presented in this study.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.