Abstract

With the intensification of economic uncertainty and the increasingly fierce competition in the fund industry, how to use the organizational network to improve the sustainable performance of the fund has become a very urgent issue. However, most of the existing research focuses on the impact of the microstructure of a single social or business network before fund leaders make decisions on the performance of fund organizations, which has the defects of incomplete information sets and the inability of leaders to identify all information and then affect organizational learning and performance. This paper constructs two kinds of fund co-holding networks as two kinds of inter-fund organization networks based on the indirect relationship between the co-holding of large and small funds and the co-holding of large funds. The study not only overcomes the above defects, but also finds that: (a) the status and power of different organizations in the two networks are unbalanced in terms of the macro overall network, the meso community and the micro individual structure, and the “super excellent community” and “benchmark fund” group occupy the core position in the network. (b) With the fund co-holding network as a tool, fund leaders can reduce risks and improve the sustainable performance of funds by observing and learning the behaviors of excellent associations and benchmark funds in the network. We provides a reference for further understanding the characteristics of inter-fund organizational networks and the rational use of organizational networks by leaders of financial organizations for organizational learning and sustainable performance improvement.

Keywords

Introduction

How to improve the sustainable performance of an organization has always been an important issue of common concern for organizational managers and scholars (Asif & Rathore, 2021; Eccles et al., 2014; Kantabutra, 2019). Especially in financial organizations, the improvement of sustainable performance plays an important role in employee, organizational, and economic and social development. Therefore, financial organization managers have taken many measures to promote the improvement of organizational sustainable performance, and promoting the improvement of organizational sustainable performance has become one of the important management tasks of financial organization leaders (Cheng et al., 2014; Choi & Wang, 2009; J. M. Li et al., 2023). In financial enterprises, especially for fund companies that raise funds to the public, aim for investment and profit, and whose performance directly affects reputation and scale, this characteristic is more obvious.

In the management practice, with the intensification of economic uncertainty and the increasingly fierce competition among enterprises, the “connotative” development of fund enterprise leaders relying on internal resources is far from meeting the needs of organizational performance improvement. As a special type of inter organizational network, the inter leader social network can not only provide channels for leaders to access external resources, but also provide a medium for them to obtain useful decision-making information and knowledge, thereby affecting the sustainable performance of the organization from both external and internal aspects (Anvari & Janjaria, 2023). Therefore, in the era of digital and network economy, the network relationships, and network capabilities of leaders have become one of the most valuable resources and capabilities of organizations (Mehra et al., 2006; Shu et al., 2018; Venkataramani et al., 2014). For public fund organizations that are highly dependent on funds and information for profit, the importance of leaders’ network relationships and network capabilities is even more prominent.

Traditional research on fund performance mainly focuses on the influencing factors of fund performance from three perspectives: fund characteristics, fund manager characteristics, and fund company characteristics (Bacon, 2023; J. M. Li et al., 2023). With the continuous deepening of the application of social networks in the financial field, many scholars have begun to consider the impact of various social networks in which fund leaders (i.e., fund managers) operate on their behavioral decisions and organizational performance (Calluzzo, 2023; Cohen & Frazzini, 2008; Cohen et al., 2008, 2010; Firth et al., 2013; Hong et al., 2005; Pool et al., 2012, 2015; Reuter, 2006; Zhang et al., 2023).

In fact, before making fund investment decisions, fund leaders often rely on a large number of social networks (such as alumni, colleagues, fellow townspeople, and business relationship networks) to obtain various investment information. The cost of obtaining information is often high, and there are problems such as incomplete information sets, disturbances, and even conflicts between different information. The actual investment decisions and the impact of information on asset prices are often a combination of the above information and have time-varying characteristics (Pareek, 2012). Therefore, finding networks that can overcome these shortcomings and utilizing network features and conducting organizational learning on the network is the key for fund leaders (i.e., fund managers) to improve the sustainable performance of fund organizations.

The funds’ co-holding network is an indirectly related organizational network constructed based on the actual shareholding behavior of the fund after the decision of the fund leader. It not only overcomes the many shortcomings brought by the direct social relationship network research of the above leaders, but also provides a powerful tool for leaders to observe the overall macro characteristics of the network, the behavior of excellent associations, and excellent leadership funds in the network (Ozsoylev et al., 2014). As scholars Brass and Krackhardt (1999) proposed, “Organizational networks may be the first and most important step in cultivating 21st century leaders.” However, it is regrettable that existing research has paid less attention to the meso community structure and micro individual characteristics of the “inter fund organizational network” indirectly formed by mutual shareholding between funds, as well as the investment behavior of core organizations. Especially, research on how fund managers (leaders) observe network characteristics, conduct organizational learning, and improve sustainable performance of fund organizations is scarce.

Based on above, this article draws inspiration from the ideas of organizational networks and organizational learning, and constructs the large small fund inter fund shareholding network Network 1 and the large fund inter fund shareholding network Network 2 based on the indirect correlation of mutual shareholding between funds. They are used as two types of inter fund organizational networks, and their meso and micro characteristics are compared and studied. The investment behavior characteristics of core organizations and how leaders can construct FOF fund portfolios and improve the sustainable performance of funds based on the above network characteristics. This study can provide some reference and reference for a deeper understanding of the characteristics of inter fund organizational networks and the rational use of organizational networks by financial organization leaders for organizational learning and performance improvement (as shown in Figure 1).

Research route and framework.

Construction of the Chinese Public Funds’ Co-Holding Networks and Network Topology Indicators

Data Sources and Construction of the Chinese Public Funds’ Co-holding Networks

The research subject of this article is Chinese public funds participating in the Chinese A-share market investment (hereinafter referred to as the “fund co-holding network”). The research data in this article comes from the quarterly position report of Chinese public funds in the WIND database, the sample period of the data used is from January 2005 to December 2021.

Construction of the Chinese Public Funds’ Co-Holding Networks

There are currently two approaches to the definition of a common holding relationship between funds; one approach is based on the determination of a fund’s holdings as a percentage of the fund’s net worth, which usually assumes that there is a nexus between funds if both funds hold the same stock and both holdings are greater than 5% of the fund’s net value (J. M. Li et al., 2024; Pareek, 2012), and the other is based on the percentage of a fund’s holdings of outstanding shares, which usually assumes that there is a nexus between funds if both funds hold a single stock and their holdings are greater than 5% of the outstanding shares (Crane et al., 2019).

However, this article found through the use of data statistics from Wind Information that due to the low proportion of public funds among the entire institutional investors, when the scope is narrowed down to active stock based and partial stock hybrid funds, their scale is smaller. If the shareholding ratio exceeds 10% as the threshold, the joint shareholding relationship between funds is very small, and the network formed is also extremely sparse, it is not conducive to the study and comprehensive characterization of fund co holding behavior in this article. Therefore, this study lowered the threshold to an average of 0.1% of the sample fund’s holdings in outstanding shares, and constructed a second network based on this.

Based on the above analysis, the following two types of Chinese public fund co holding networks are constructed:

(1) Network 1 (The Co-holding network between large and small funds): If both funds hold at least the same stock and the shareholding of both funds accounts for more than 5% of the net value of the fund, the funds are considered to be linked. Since there are large funds and small funds in the fund market, small funds cannot be screened by this method. Therefore, the constructed fund co-holding network includes both large funds and small funds.

(2) Network 2 (The Co-holding network between large funds): If two funds jointly hold at least one stock and their respective holdings account for more than 0.1% of the outstanding shares, there is a link between the funds. Since this method takes the ratio of shareholding to stock outstanding shares as the threshold, it can filter most of the small funds, so the fund co-holding network constructed is basically large funds.

Analysis of the Micro Individual Network Characteristics and Investment Behavior of the Mutual Holding Network of Two Funds

In network analysis, which nodes are the most important core nodes and how many other nodes these nodes are connected to are usually the primary concerns of research. Degree centrality is the most direct measure of the position and centrality of nodes in complex network analysis. The greater the degree of a node, the higher its degree centrality, and the more important it is in the network.

Referring to the research method of network centrality used by Hochberg et al. (2007), this study uses the indicators: Absolute degree centrality D1 and D2 for analysis. Although their connotations are different, they all reflect the degree to which nodes are located at the center of the network, which can measure the influence or relative importance of each fund in the mutual fund holding network (Hochberg et al., 2007).

Calculation of Micro Individual Characteristics and Analysis of Distribution Characteristics of Funds’ Co-Holding Networks

Degree Centrality is an important index used to measure node centrality in network analysis. It reflects the sum of the number of relationships of a node in the network, that is, the degree to which the node is connected to other nodes. The higher the degree centrality is, the more central the node is in the network and the greater its influence on the network.

In this article, the nodes in the network refer to each public fund, and the node degree of the network refers to the number of funds associated with a public fund. The different positions of each node in the network have different degrees of impact on the network. Generally speaking, public funds with higher node degrees also have greater importance in the network, and their connections with other nodes become closer. Therefore, they are in a more advantageous position in resource sharing and information communication. According to the formulas of degree centrality of nodes, this article calculates the absolute centrality of Network 1 and Network 2, respectively (M. Newman, 2018).

It can also be observed from Figure 2 that the degree distribution of nodes in the two networks is unbalanced, and the absolute centrality degree distribution is more in the range of small degree values, followed by medium degree, and there are fewer nodes with large degree. Obviously, this shows that a few head funds in the market have more links, while a large number of funds do not have many links; This also shows that the more connections between funds is not the better. Instead, a trade-off will be made between the benefits of establishing the connection and the maintenance costs of the connection. Compared with Network 1, network 2 shows little difference in the number of small degree nodes, but a significant increase in the number of medium degree nodes. This indicates that the nodes of network 2 are more connected than those of network 1, implying that larger funds have a higher probability of investing in the same stock.

Absolute degree centrality D1 and D2 distribution histogram of two Networks.

Analysis of Investment Behavior of Core Nodes Based on the Characteristics of Micro Individual Networks

Network theory suggests that highly numbered nodes in a network are often located at the center of the network, often playing the role of “opinion leaders” in the network. Their investment behavior is often representative and easy to be noticed and imitated by low numbered nodes. Therefore, this section mainly analyzes the investment behavior of the top 10 funds in various network centrality rankings based on the above formula and the calculation of the centrality of each node in the network. It mainly analyzes the investment behavior of core nodes (funds) from four aspects: the characteristics of the fund itself, the characteristics of holding stocks, regional preferences, and industry preferences.

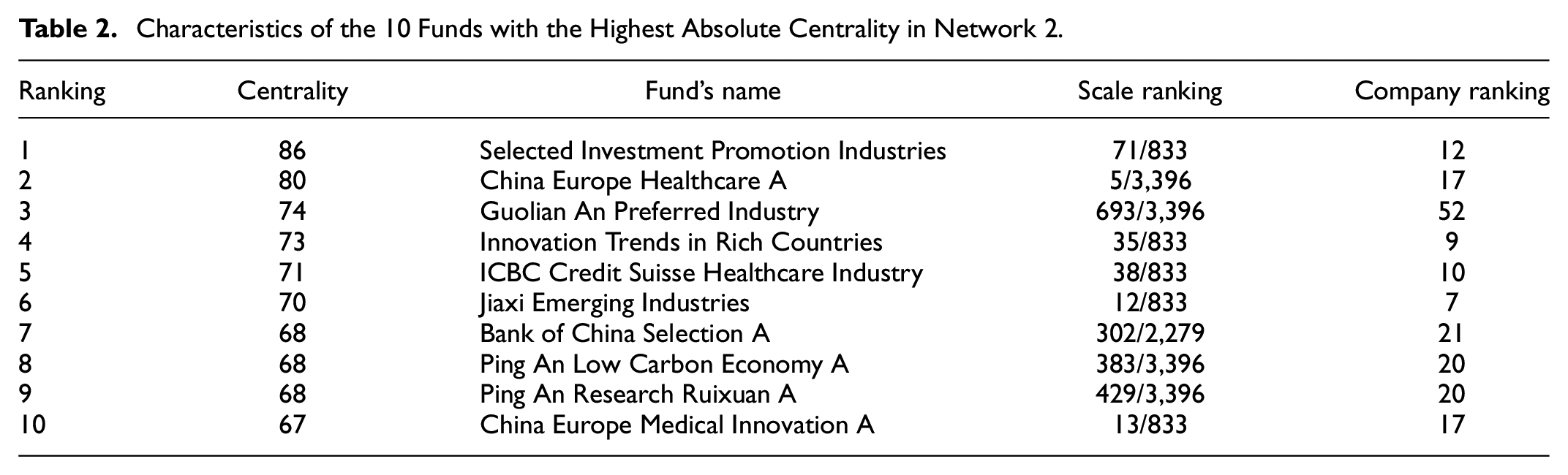

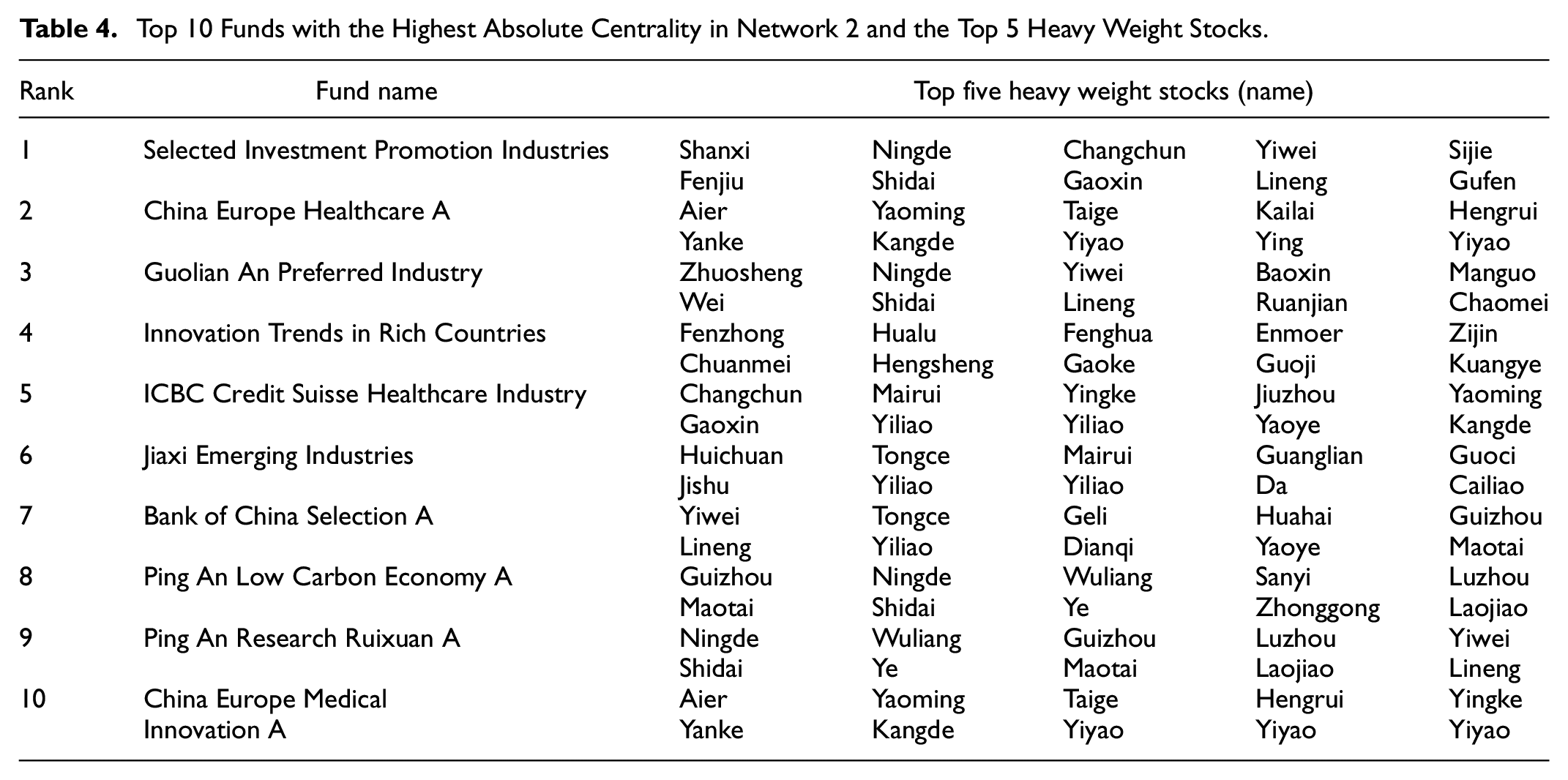

In this paper, the degree centrality of all nodes is calculated according to the formula. The 10 funds with the highest absolute centrality in Network 1 and Network 2 and their main characteristics are listed in Tables 1 and 2; Tables 3 and 4 also list two types networks simultaneously. The top 5 heavyweight stocks held by the top 10 funds with the highest absolute centrality in the network.

Characteristics of the 10 Funds with the Highest Absolute Centrality in Network 1.

Characteristics of the 10 Funds with the Highest Absolute Centrality in Network 2.

The Top 10 Funds with the Highest Absolute Centrality in Network 1 and the Top 5 Heavy Weight Stocks.

Top 10 Funds with the Highest Absolute Centrality in Network 2 and the Top 5 Heavy Weight Stocks.

Firstly, by observing Tables 1 to 4, it can be observed that funds with high numerical centrality have the following characteristics:

(1) From the perspective of fund companies, as shown in Tables 1 and 2, Huitianfu Fund, Bank of China Fund, Anxin Fund, Ping An Fund, and China Europe Fund are among the top mutual shareholding fund companies with relatively high degree centrality; Among these fund companies, Agricultural Bank of China and Huili, Huitianfu Meili 30A, Bank of China Consumer Theme, China Merchants Industry Selection, China Europe Healthcare A, and Guolian An Preferred Industry are among the top three funds in Network 1 and Network 2 in terms of degree centrality. Most of these funds rank among the top in the same type of scale, and their fund companies often have the highest number of funds and net asset value in the industry. This indicates that funds under large and high-performing fund companies often have higher degree centrality.

(2) From the perspective of specific positions of funds, as shown in Tables 3 and 4, most of the funds with the highest absolute centrality hold “leading white horse shares” recognized in the market, such as Kweichow Moutai and Wuliangye, the leading liquor companies, Midea Group and Haier Zhijia in the household appliance industry. The corporate governance of “leading white horse shares” is relatively perfect, the industry “moat effect” is obvious, the performance is stable and the growth is relatively certain.

As a result, it has become a scarce investment target pursued by various institutional investors. One of the direct reasons for the high centrality of funds in the network is their “clustering” and “heating up in groups” on such investment targets.

Optimization of FOF Fund Investment Portfolio Based on Microstructures in Mutual Holding Networks Between Fund Organizations

FOF Fund Development and Its Importance to Fund Organization Performance

FOF fund, also known as “fund of funds,” are constructed with various funds as investment targets. According to Wind Information, as of September 2023, there were a total of 463 publicly offered FOF funds in mainland China, with a total scale of 182.6 billion yuan, an increase of nearly 10 times compared to the scale when the first batch of FOFs were established in 2007. Currently, FOF funds have become a new profit growth point for fund companies and play a crucial role in improving their sustainable performance.

Optimization Principles of FOF Fund Investment Portfolio from the Perspective of Organizational Networks and Organizational Learning

From the perspective of management practice, the construction of FOF fund investment portfolio is actually a problem of how organizational leaders make optimal management decisions based on the established funds, information, and resources of the organization in an uncertain environment (Freitas & Junior, 2023). Essentially, there are three objectives for leaders to optimize their investment portfolios: (a) finding better and more profitable investment targets; (b) To minimize the correlation between high-quality investment targets found, that is, there should be diversity and heterogeneity among investment targets; (c) Under the above two conditions, it is necessary to minimize the cost of information search and decision-making as much as possible (Bhalla, 2008). The funds co-holding networks, a special organizational network, is a powerful tool for fund leaders to achieve the above three goals through organizational learning on the network (Easterby-Smith et al., 2000).

Fund co-holding network is a kind of indirectly related organizational network constructed according to the actual shareholding behavior of fund after the decision of fund leaders. It not only overcomes the shortcomings of incomplete information, interference or even conflict between different information, and inability to identify all information and timely change characteristics caused by the direct social relationship network of fund leaders, but also provides leaders with the ability to observe the position information of benchmark funds in such networks. It creates conditions for organizational learning and improving the sustainable performance of funds (Askim et al., 2008; DiBella et al., 1996).

Therefore, inspired by the research on the combination of complex networks and stock investment portfolios mentioned above, as well as the literature on leaders in the field of management using organizational networks to improve organizational performance, this article intends to combine complex network community detection and network centrality theory with the construction and optimization of FOF fund investment portfolios, According to the results of the community division and centrality analysis of the fund co ownership network based on the similarity of fund co-ownership, investment weights are allocated between and within communities, and FOF fund investment portfolios are constructed and optimized. It can be expected that fund organization leaders should achieve good results in optimizing FOF fund investment portfolios based on the meso community structure and micro individual characteristics of the fund co holding network. The following will be validated based on the idea of computer simulation experiments.

Optimization Experiment and Evaluation of FOF Investment Portfolio Based on Microstructures in Mutual Fund Holding Networks

Simulation Experiment Design

Complex network community is essentially a collection of individuals with certain similar attributes, and in the fund market, fund companies are essentially an aggregation of multiple funds. Therefore, fund companies can be directly regarded as associations in the fund co-holding network and the combination of network micro individual characteristics to verify the feasibility and effectiveness of FOF fund portfolio optimization. This paper designs a set of simulation experiments from the perspective of practical application.

The idea is to extract 10 funds from all funds of the two networks using different methods and then determine the optimal portfolio (called the efficient frontier of the portfolio) using the mean-variance model (MV) model that can balance return and risk in portfolio construction and optimization. Finally, the returns and risks of the FOF portfolio are calculated on this basis (Markowitz & Todd, 2000). The sampling methods mainly include the meso community method based on the network and the micro individual centrality method, with a total of six types: (a) the inter-community and intra-community random sampling combination (RRP1), that is, five funds are randomly selected from all the fund companies in China’s public offering fund market, and then two funds are randomly selected from each of the five companies; (b) Non-random inter-community and random intra-community sampling combination (NRP1), that is, the five largest fund companies are selected from all fund companies in the market, and then two funds are randomly selected from each of the five fund companies; (c) Non-random inter-group and intra-group sampling combination (NNP1), that is, selecting the five largest companies from all fund companies in the market, and then selecting the two funds with the highest core degree from each group of these five companies; (d) Randomly sampling portfolios from all individuals (ARP2), that is, randomly sampling 10 funds from all individuals in the network for portfolios; (e) Based on the micro individual centrality (non-random sampling) (DDP2), the top 10 funds with micro individual centrality are selected from all individuals in the network as the portfolio; (f) Based on the micro inter-individual centrality (non-random sampling) (BDP2), the top 10 funds with micro inter-individual centrality are selected from all individuals in the network as the portfolio. For the above six methods involving random sampling, the sample was repeated 1,000 times and the average return and risk were calculated for each constructed asset portfolio. The results obtained are shown in Tables 5 and 6.

FOF Investment Portfolio Effect Based on Network 1 Topology Structure.

FOF Investment Portfolio Effect Based on Network 2 Topology Structure.

Evaluation of Simulation Experiment Effect

To evaluate the experimental results, observe the simulation results in Tables 5 and 6, it can be seen that:

(1) The FOF investment portfolio constructed based on the mesoscopic community structure (or micro individual centrality) of the network, whether based on Network 1 or Network 2, exhibits returns of RRP < NRP < NNP (or ARP < BDP < DDP), and risks of RRP > NRP > NNP (or ARP > BDP > DDP), indicating that compared to random sampling (RRP) between and within communities or random sampling (ARP) among all individuals, the investment portfolio is constructed using Method 1 (or Method 5), The other four FOF investment portfolio strategies constructed based on complex fund co holding network community structure or micro individual centrality significantly improve the returns of the portfolio and can reduce the risks of the portfolio, namely: FOF investment portfolio optimization strategies based on micro characteristics in the fund co holding network are feasible and effective;

(2) In the experiment, two types of investment portfolios were constructed based on the centrality of mesoscopic communities and micro individuals. Each type of portfolio strategy is a process of decreasing randomness and deepening the utilization of the structural characteristics of the mutual fund holding network. From the data in Tables 5 and 6, it can be seen that the returns of each type of three strategies are gradually increasing and the risks are also slightly decreasing; This indicates the necessity of mining the topology structure of the network for portfolio construction and optimization; At the same time, if combined with the principles of FOF fund portfolio optimization from the perspective of organizational network and organizational learning, the above results also indicate that fund managers (leaders) can improve the sustainable performance of the organization through organizational learning and information acquisition on the inter organizational network.

(3) Network 1, which combines both large and small funds and has a larger scale, has higher returns but greater risks compared to Network 2, which is mainly composed of large funds and has a smaller scale. The reason is that the diversity of members in Network 1 is more abundant, providing a more diversified selection of fund investment targets for FOF portfolio construction.

Robustness of Simulation Experiment Results

The simulation experiment design, implementation process, and implementation results in this paper are robust for the following reasons:

Firstly, the idea of FOF portfolio optimization experiment based on microstructure in fund co-holding network in this section comes from the computer simulation and experiment method of management science and engineering. It is different from the traditional econometric and empirical economics research paradigm and method that first carries out descriptive statistics and regression analysis and then carries out robustness test. This method has three advantages: (1) It can simulate complex systems, especially in management science and engineering, which can simulate the operation process of actual complex systems. (2) The construction of this simulation method and model is relatively flexible, and the model structure and parameters can be adjusted according to specific problems to adapt to different scenarios. (3) This simulation method can conduct virtual experiments to test the impact of different decisions and strategies on the system and provide reference for decision-making. This section precisely considers the Fund as a complex system and tests the impact of different methods on the sustainable performance of the system by flexibly setting three different FOF portfolio optimization methods. Therefore, due to the characteristics of this method and the robustness of the method itself, this study does not need to do a similar econometric robustness test.

Secondly, in the selection of sampling methods in the design and implementation of specific computer simulation methods, this section adopts two categories, including network meso-community detection method and micro-individual centrality method, and six sampling methods, including RRP1, NRP1, NNP1, ARP2, DDP2, and BDP2 (see the part of Simulation Experiment Design and Evaluation of Simulation Experiment Effect for details). The above six methods represent the most common types of fund portfolio decisions, and the sample is repeated 1,000 times, and then the average return and risk of the asset portfolio constructed each time is calculated. Therefore, the implementation process and implementation results of this method are robust.

Finally, the size of the fund often has a great impact on the construction of the fund portfolio and the sustainable performance of the fund. This is equivalent to the robustness test has been done simultaneously in the specific implementation and analysis of simulation experiments. To sum up, this section is robust in terms of the method characteristics of computer simulation and experiment, specific simulation method design, implementation process and implementation results.

Discussion of Simulation Experiment Results

Based on the characteristics of meso associations and micro individuals in the co-holding network of the two funds and the investment behavior characteristics of excellent associations and benchmark funds in Part 2, this section designs simulation experiments to further verify the feasibility and effectiveness of FOF fund portfolio optimization based on the meso community structure and micro individual characteristics in the co-holding network of funds. The experimental results show that: (1) the FOF portfolio constructed with the meso community structure (or micro individual centrality) of the two networks has a significant increase in return and a decrease in risk; (2) In the construction of FOF portfolio, the more the method relies on the above characteristics of the network, the above improvement degree of the portfolio is more obvious than that of random sampling, which fully demonstrates that the FOF portfolio optimization strategy based on the micro characteristics of the fund co-holding network is feasible and effective; (3) The above characteristics are more obvious in Network1 with both large and small funds and more obvious diversification, because Network1 is a co-holding Network with both large and small funds. Compared with Network 2, it has more samples and more obvious differences in individual micro characteristics and community structure between funds. This is beneficial to fund managers’ portfolio management to expand the investment scope and carry out more extensive inter-organizational learning and performance improvement.

Fund Portfolio Optimization and Sustainable Performance Improvement from the Perspective of Organizational Network and Organizational Learning

The above experimental results fully prove that using the fund co-holding network as a tool can optimize the fund portfolio, reduce risks and improve sustainable performance. So, why can the above methods achieve such good results? Why can fund leaders use the fund co ownership network to improve organizational sustainable performance?

Combining the Optimization Principles of FOF Fund Investment Portfolio from the Perspective of Organizational Networks and Organizational Learning, as well as the practical environment in which fund organizations operate, this article argues that in the unique ecological environment of Chinese stock market, The fund co ownership network constructed by utilizing the co ownership behavior between fund organizations and the characteristics of the meso community and micro individual presented in the network provide a powerful tool for fund leaders to observe and learn the behavior of excellent sustainable communities and benchmark funds in the network, and use it to optimize investment portfolios and improve organizational sustainable performance of various funds, including FOF funds (as shown in Figure 3).

Fund portfolio optimization and sustainable performance improvement from the perspective of organizational network and organizational learning.

The imperfect governance system of China’s stock market and the ecological environment of “sudden rise and fall” have that fund investment is often to “warm up” by forming a network through common shareholding, while fund companies and funds with better performance sustainability are often in the core position. From the perspective of organizational networks, the inter fund co ownership network is essentially an organizational network formed by fund organizations to achieve common goals or interests. It is this feature that creates conditions for fund leaders to use networks for exploitative learning, exploratory learning and learning from benchmark funds to improve their sustainable performance (Bozionelos, 2003; de Oliveira Maciel & Netto, 2020; Maurer et al., 2011; Moore, 2009; Nonino, 2013; Paruchuri & Awate, 2017). Meanwhile, the inter fund co holding network and other organizational networks provide important carriers for fund leaders to benchmark and imitate organizations, and improve the sustainable performance of funds through two ways: increasing returns and reducing costs (Argote, 2012; Chung et al., 2015; Hu, 2014; Iqbal & Ahmad, 2021; Kordab et al., 2020; Schwandt & Marquardt, 1999).

From the perspective of increasing returns, fund organization leaders can directly improve the sustainable performance of the fund by observing and learning from excellent clubs and benchmark funds with high performance sustainability in the network (Kokkaew et al., 2022; Peng et al., 2022). From the perspective of cost reduction, organizational networks such as fund co ownership networks contain rich information resources, Fund leaders can obtain a large amount of decision-making information through the network at a low cost, which indirectly increases the sustainable performance of the organization (Iqbal et al., 2020; Noh, 2019; Piwowar-Sulej & Iqbal, 2022; Spreitzer & Porath, 2012; Xia et al., 2022).

In summary, the fundamental reason why fund organization leaders optimize FOF fund investment portfolios based on the meso community structure and micro individual characteristics of the fund co holding network and achieve good results is that in the special ecological environment of the Chinese stock market, The fund co-ownership network composed of mutual shareholding behavior among fund organizations and the characteristics of meso associations and micro individuals presented in the network provide powerful tools for fund leaders to observe and learn the behavior of excellent associations and benchmark funds in the network, and improve the sustainable performance of the organization through optimizing fund investment portfolios, increasing returns, and reducing costs.

Discussion

Theoretical Implications

This article draws on the ideas of organizational networks and organizational learning, regards the mutual shareholding network between funds as a special organizational network, and explores how fund leaders can use the network to construct FOF fund portfolios and improve sustainable performance of the fund based on a thorough study of the micro and micro characteristics of the organizational network and the investment behavior characteristics of the core organization. Compared to previous studies, the contributions and innovations of this article are mainly reflected in the following aspects:

(1) This study extends the study of organizational networks by applying the concept of organizational networks to special financial organizations such as public funds.

Existing research on organizational networks mainly focuses on the characteristics and impacts of various organizational networks within or between industrial enterprises and non-financial commercial enterprises (Gulati et al., 2011; Monaghan et al., 2017; Liu & Yang, 2020; Powell & Oberg, 2017; Soda & Zaheer, 2012) paid less attention to the characteristics and impacts of the special network between financial organizations, such as public funds. This study focuses on the characteristics and impacts of the network between fund organizations, which further expands the research scope of organizational networks from the perspective of research objects.

(2) This study explores the meso organizational and micro individual characteristics of inter fund co ownership networks, as well as the investment behavior of core organizations and core funds. It extends the organizational network from the perspective of previous holistic network research to the meso and micro domains of the network.

Previous research on inter fund networks was mostly based on alumni (Cohen et al., 2008; Lin et al., 2021) and fellow villagers (Hong et al., 2005; Pool et al., 2015); Social relations and investment banks and fund companies (Gu et al., 2019; Reuters, 2006), financial market buyers and sellers (Firth et al., 2013), and investment and investee institutions (Cvijanović et al., 2016); Business relationship networks (Calluzzo & Kedia, 2019) and joint shareholding networks (Gong & Liu, 2023; L. Li et al., 2022; Pareek, 2012); The overall network characteristics of have an impact on the performance of decision-making, with less attention paid to the meso and micro individual characteristics of special organizational networks such as the “fund co holding network” indirectly formed through mutual shareholding between funds, as well as the investment behavior of core communities and core funds. This article focuses on the meso and micro characteristics of organizational networks, expanding the research perspective of organizational networks from previous holistic network research to the meso and micro domains of networks.

(3) This study analyzes how fund managers can use the organizational network to construct FOF investment portfolios and improve the sustainable performance of the organization, and verifies it through computer simulation experiments; This not only expands the relevant literature on organizational networks and organizational learning, but also enriches the research on sustainable performance of fund organizations.

Organizational management theory suggests that organizational learning and the creation of learning organizations can improve organizational performance, and organizational networks are important carriers of inter organizational learning. Many scholars have also studied their impact on organizational performance from the perspective of organizational learning on organizational networks (Ali et al., 2023; Chung et al., 2015; Mowery et al., 1996; Sage et al., 2020; Zappa & Robins, 2016), however, there is little research exploring how fund leaders can optimize and enhance the sustainable performance of organizations based on the microstructure of FOF fund investment portfolios in fund co ownership networks.

Based on a thorough study of the micro to medium characteristics and core organizational behavior characteristics of the fund co ownership network, this study analyzes how fund managers use this organizational network to construct FOF investment portfolios, conduct organizational learning, and improve organizational sustainable performance. The results are validated through computer simulation experiments, further expanding the research on organizational networks, organizational learning, and sustainable performance of fund organizations.

Practical Implications

The conclusions of this paper show that fund co-holding network, as a special organizational network, provides a reliable tool and a unique carrier for fund managers to improve the sustainable performance of their organizations. Specifically, fund managers can explore investment opportunities and improve the sustainable performance of the organization through the following aspects:

Firstly, fund managers should use the fund co-holding network to share and transfer more knowledge. Fund co-holding network provides a carrier and platform for fund managers to share knowledge and transmit information. Organizational learning theory has always emphasized the importance of information sharing and transmission within the organization, which is particularly critical for fund managers who rely on information to make investment decisions. Through this special organizational network, fund managers can share knowledge such as investment strategies, market analysis, industry insights, and promote learning and innovation within the organization. Therefore, fund managers should be good at using the fund co-holding network to share and transfer more knowledge, which not only helps to form a learning organization, but also helps to continuously improve the network ability, intellectual capital and competitiveness of fund managers.

Secondly, fund managers should take the network as the carrier to strengthen collaborative learning and team collaboration among organizations. Fund market is a market that not only needs competition, but also needs cooperation and win-win market. Therefore, the organizational learning of the fund must focus on the concept of collaborative learning and teamwork. Fund managers can conduct collaborative learning and jointly analyze market trends and risk factors through the fund co-holding network. Such collaborative learning can stimulate team collaboration, promote communication and cooperation among members, give full play to their comparative advantages, and thus improve the performance of the entire fund management team.

Thirdly, fund managers should take the network as a platform to strengthen the building of sharing culture and trust among organizations. The purpose of fund managers to build organizational network and conduct organizational learning is to build a learning organization and improve the intelligence level of the organization. The formation of fund co-holding network depends on the cooperation and trust between fund managers. Through the fund co-shareholding network, fund managers can establish closer ties, form a sharing culture, and promote information sharing and resource cooperation. This trust and cooperation help reduce information asymmetry and stimulate the enthusiasm of the team, so as to continuously improve the sustainable performance of the fund.

Finally, fund managers should make full use of the information decision-making advantages of the fund co-holding network and strengthen the adaptability and flexibility of the organization. The adaptability and flexibility of the fund are the preconditions for the organization to have long-term advantages in the fierce market competition, while the learning organization focuses on adaptability and flexibility to adapt to the rapidly changing market environment. The instant sharing and real-time information feedback of a large number of fund shareholding information in the fund co-holding network not only create conditions for fund managers to quickly perceive the change of market status and adjust the portfolio quickly, but also provide a guarantee for fund managers to continuously improve their investment strategies and form a benign learning cycle, so as to establish a benign investment decision-making mechanism of feedback and learning cycle. Thus, the fund co-holding network becomes a low-cost and efficient carrier and channel to strengthen the adaptability and flexibility of the fund to adapt to the new market situation. Therefore, fund managers should make full use of the characteristics of fund co-holding network and the information transmitted, and strengthen the adaptability and flexibility of the organization by improving the ability to respond quickly to key investment information, so as to improve fund performance and make it more sustainable.

In short, fund managers should build an environment conducive to organizational learning through knowledge sharing and transmission, collaborative learning and teamwork, sharing culture and trust building, and strengthening organizational adaptability and flexibility in the co-shareholding network among funds, so as to improve the sustainable performance of funds. This concept of using organizational network for organizational learning and building a learning organization will also fundamentally help fund managers to better respond to market changes and achieve long-term stable performance of fund portfolios and long-term sustainable development of fund organizations.

Limitations and Future Research Directions

On the one hand, there are many institutional investors in China’s financial market, including pension funds, social security funds, securities brokers, commercial banks, the national team, public funds and private funds. This leads to the inevitable lack of data, which in turn may weaken the persuasive power of the findings. Therefore, future research could employ a larger range of data to reduce the aforementioned adverse effects.

On the other hand, in the social network analysis, there are various measurement indicators of network micro individual characteristics and methods to divide the community structure in the network. Limited by many factors, this study only adopts the most commonly used degree centrality, betweenness centrality and Louvain algorithm to analyze the micro characteristics in the fund co-holding network and determine the core community and benchmark fund. This leads to the inevitable incompleteness of the research, which in turn may undermine the persuasive power of the findings. Therefore, future research can adopt more types of measurement indicators to make the research more comprehensive and robust.

Conclusion

This study draws inspiration from organizational networks and organizational learning ideas, and constructs two types of inter fund organizational networks based on the indirect correlation of mutual shareholding between funds: the large small fund shareholding network Network 1 and the large fund shareholding network Network 2. The study compares the micro and medium-sized characteristics of the two networks, the investment behavior characteristics of core organizations, and how leaders construct FOF fund portfolios and improve sustainable performance of funds based on the above network characteristics, Research findings:

(1) In terms of the overall structure of the network, the status and power of each fund organization in the two types of inter fund organizational networks are imbalanced, and the network has small world characteristics. Large fund companies and excellent funds are at the core of the network and hold a large number of shares of excellent listed companies, which is the fundamental reason for their good sustainability of performance.

(2) Based on the results of computer simulation experiments, the FOF portfolio constructed by taking the co-holding network between the two types of funds as a special organizational network can improve the effective optimization of the portfolio, reduce the risk and improve the sustainable performance of the fund.

(3) The unique ecological environment of China’s stock market leads to the generalization of co-shareholding behavior among fund organizations, and excellent fund companies and benchmark funds often have the core community and core position of the network, which provides a powerful tool for fund leaders to observe and learn from the excellent players in the network and improve the sustainable performance of the organization.

This study not only provides a certain reference for the in-depth understanding of the characteristics of the inter-fund organizational network, but also provides a certain reference for the leaders of financial organizations to make reasonable use of the organizational network for organizational learning and sustainable performance improvement.

From the perspective of management practice, the co-holding network between funds provides an effective tool and carrier for fund leaders to conduct organizational learning. By analyzing the medium and micro structure of the network, institutional investors can not only evaluate their position and role in the network and understand their influence in the market, but also identify and track other excellent investors and learn lessons from their investment strategies and position changes to optimize their investment decisions. Further, fund managers can strengthen the adaptability and flexibility of the organization, build an environment conducive to organizational learning, enhance their own competitive advantages and improve the sustainable performance of the fund by strengthening cooperation with core investors, knowledge sharing and transmission, collaborative learning and team collaboration, shared culture and trust building.

Footnotes

Acknowledgements

We sincerely thank the editor and reviewers for their very valuable and professional comments.

Authors’ Contribution

The research is designed and performed by X. P. Guo. The data were collected by X. P. Guo and G. An. Analysis of data was performed by X. P. Guo and G. An and J. Han and Z. J. Wang. All authors wrote the paper and read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was funded by the National Social Science Fund of China, Grant No. 22BJL139 and No. 19BJY176 and Liaoning Provincial Natural Science Foundation Project, Grant No. 2020-YKLH-21 and Key Scientific Research Project of Liaoning Provincial Department of Education, Grant No. LJKR0585 and Key Research Project of Liaoning Provincial Social Science Planning Fund, Grant No. L22AJY006.

Ethical Approval

The data studied in this paper come from the open commercial database, and the data processing and analysis are completed by computer and related application software, which does not involve any ethics and morality of human and animal experiments. So ethics approval was not required for this research.

Data Availability Statement

The data that support the findings of this study are available on request from the first author.