Abstract

This paper proposes a theoretical model with two types of households to explore the distributional effects of inflation, assess the non-neutrality of money; and in return, to provide a guideline for policymakers in setting inflation rate. An impatient borrower who faces a borrowing constraint holds a positive amount of debt in equilibrium while a patient lender engages in consumption smoothing. Hence, inflation affects net worth of borrowers via nominal debt by redistributing resources away from lender, rendering welfare gains for the borrower and losses for the lender; and the structure of borrowing constraint gives rise to non-neutrality of anticipated inflation. The utilitarian welfare gain from generating inflation in a cashless economy is amplified when heterogeneous productivity levels are assumed. Yet, incorporating money demand in the form of money-in-utility model suggests that an inflation tax as an additional distortion reverses the overall positive effect of generating inflation in the cashless economy.

Plain Language Summary

This paper proposes a theoretical model with two types of households to explore the distributional effects of inflation, assess the non-neutrality of money; and in return, to provide a guideline for policy planners in setting inflation rate. Anticipated inflation is shown to affect the net worth of borrowers via nominal debt by redistributing resources away from lender, rendering welfare gains for the borrower and losses for the lender; and the structure of borrowing constraint gives rise to non-neutrality of anticipated inflation. The utilitarian welfare gain from generating inflation in this setting is depicted to rise when heterogeneous productivity levels are assumed. Yet, incorporating money demand into this theoretical environment suggests that an inflation tax as an additional distortion reverses the overall positive effect of generating inflation. The decision by central banks toward using the inflation rate as an instrument to improve utilitarian welfare relies on the presence of money demand motive, the pro-lender/borrower bias, the relationship between intertemporal elasticity of substitutions and the heterogeneous productivity levels among agents. Furthermore, the contribution of this study is that it illustrates the non-neutral effects of the anticipated inflation in a theoretical model as opposed to the unanticipated inflation in the previous literature; and this non-neutrality of inflation is indicated even in the absence of heterogeneity among households contrary to the existing literature.

Introduction

Inflation has always been a concern for policymakers as costs arise due to both unanticipated and anticipated inflation. With the stabilization of inflation becoming a primary objective for central banks, first, many industrial countries adopted inflation targeting in the 1990s; and then, developing countries followed the same regime. In this regard, most of the central banks target an inflation rate between 1% and 3%. Despite the targets set by central banks, many countries are still having difficulty in the stabilization of inflation and closing the gap between actual and target inflation rates, questioning the level of the target. For instance, single-digit, close-to-zero inflation targets might be achievable for developed countries and better in optimizing welfare implications of inflation whereas low but double-digit inflation targets could be more feasible for developing countries for the same purposes. Furthermore, in recent decades, since the money holdings are observed to be at their highest level, raising the inflation rate, in return the target, has also become a new debate for central banks (e.g., Aruoba & Schorfheide, 2016; Bank of Canada, 2016; Blanchard et al., 2010). In fact, Fed and ECB announce that rather than fighting inflation aggressively, they pursue monetary policies that mind low- and middle-income households (Ioannidis et al., 2021; Powell, 2020, 2021; Schnabel, 2021). Deduced by these anecdotes, it can be inferred that the welfare effects of low or high inflation policies are still debatable as the welfare consequences are sensitive to whether the assets and liabilities are fixed in nominal terms or are inflation-indexed; and whether unanticipated or anticipated inflation is considered.

The existing literature has been concentrating on unanticipated inflation and its redistributive effects on welfare since the anticipated inflation changes are neutral (Barro, 1978; Frydman & Rappoport, 1987; Lucas, 1972) and only unexpected monetary policy shocks can create real effects on economies (Friedman, 1968; Phelps, 1967). However, the papers proving the non-neutrality of money (Chari et al., 1996; Weil, 1991) and showing the real effects of inflation (Bullard & Keating, 1995; Khan et al., 2006) give rise to a revisitation of anticipated inflation and effects of inflation under specific settings. Because, if real variables, such as capital stock, output and consumption, can be affected even by the anticipated inflation, then policymakers can induce real impacts in the economy by changing the inflation rate they set. Motivated by these observations, the analysis in this paper revolves around anticipated inflation.

In welfare analyses, inflation is shown to have disproportionate effects on different types of households. Specifically, an increase in inflation reduces the real value of a debt obligation, thereby benefiting the borrower. On the other hand, it decreases the real value of debt repayment, by that, harming the lender. In other words, the size of the welfare implications of inflation can only be adequately measured with the adoption of a model including heterogeneous agents. Otherwise, a representative agent model abstracts from any heterogeneity; hence, misses the consumption, money-holding and productivity-related asymmetries. Such asymmetries make the conduct of monetary policy even more crucial in terms of the impacts that can be achieved on income inequality. Therefore, this study utilizes a heterogeneous agent model.

With the proposed analytical model comprising two types of households, this paper aims to explore the redistributive effects of anticipated inflation and assess the non-neutrality of money. Note that the scope, here, is not to pinpoint an optimal inflation rate, but rather to discuss the welfare implications of anticipated inflation. Because with the intervention of monetary policymaker, changing inflation rates and inflation targets can alter the real variables, redistributing resources, affecting welfare and adjusting inequality. Contrary to the existing literature, the theoretical model does not require aggregate and idiosyncratic risks, distortionary taxes or generational gaps to present the non-neutrality and redistributive effects of anticipated inflation. The differences in time preference of households define their types as lenders or borrowers. When introduced, different labor productivity levels create income inequality among the types per se. Both types of households optimize inter-temporally while impatient borrowers are subject to a borrowing constraint, and the equilibrium level of lending and borrowing is endogenized. Although there is no risk in this setting, the bond market can be considered incomplete with nominally non-contingent bonds. In fact, the term incomplete financial market is used here in a slightly different terminological sense than the literature has been using. Bonds are non-contingent in the sense that when the period of maturity comes for repayment, the amount of repayment is diminished by the inflation rate at the time of maturity. Moreover, a less developed financial market where neither future income nor durable goods can be pledged for securitization of the debt obligation is considered such that lending is restricted by current income (e.g., Bianchi, 2011; Korinek, 2009; Laibson et al., 2003). This, however, results in nominal friction, as higher inflation reduces the real value of debt in terms of commodities at maturity, which tends to benefit borrowers. Therefore, even the anticipated inflation becomes non-neutral due to the structure of the borrowing constraint. Additionally, since debt contracts are predetermined in nominal terms, inflation can influence the borrowers’ net worth. In particular, an increase in the inflation rate lowers the real debt repayments for a given outstanding debt; thereby redistributing resources from lenders to borrowers. In short, by changing the inflation target, policymakers can influence the real variables and manage (in)equality between the household types.

To depict the non-neutrality of inflation and to gauge its redistributive effects, simulation exercises are conducted. They demonstrate that there is a conflict of interest on the inflation rate between the borrowers and the lenders as the welfare of borrowers rises with inflation whereas that of lenders decays in all parameterizations, revealing the redistribution effect of inflation. This conflict of interest would cause a corner solution at either of the extremes in the determination of the inflation rate unless there is a social planner. A simple calculation of utilitarian welfare with different weights attached to two types shows that the importance given to the borrower in the utilitarian welfare by the hypothetical social planner matters. Specifically, utilitarian welfare can be decreasing in inflation with low weights (i.e.,

The money demand motive is introduced to the economy in order to assess the welfare effects of inflation in a setting where decisions regarding money holding generate another distortion in addition to the borrowing constraint. Investigating the effects of monetary policy requires a model with cash as the money demand is also affected by the changes in inflation. Without accounting for money-holding decisions, the social planner can set an implausibly high inflation rate, because doing so would hurt only the lender by redistributing away from them. However, the introduction of money demand incurs the same distortion that is generated in the form of inflation tax on both types, preventing the social planner from choosing such a high inflation rate. Hence, this analysis aims to distinguish the effects of inflation under the presence of a money demand motive and compare the welfare consequences of inflation tax in this economy with the cashless economy so as to provide a guideline to the policy planner in setting the inflation rate. The results from the simulations imply that the additional distortion in the form of inflation tax can affect even the constrained households negatively, resulting in a loss in utilitarian welfare from generating inflation. When borrowers are worse off because of the higher inflation, this renders a welfare loss as the lenders are always hurt by higher inflation. Nevertheless, the cases where the borrowers are better off due to higher inflation do not translate into welfare gains when the types are equally treated in the utilitarian welfare function. This suggests that the loss of the lenders is larger than the gain of borrowers from higher inflation.

Furthermore, when households take multiple decisions in addition to money holding, the relative magnitudes of the intertemporal elasticity of substitution (IES) of these choices must be considered when setting the inflation rate. In particular, when the inverse IES of real money balances is higher than that of consumption, the behaviors of money demand with respect to rising inflation are mirrored in the utility of borrowers. On the other hand, when the IES of real money balances is larger than that of consumption, the response of consumption designates the outcome on the utility of the borrowers. These results follow from the fact that the smaller the IES for consumption is, the stronger the consumption smoothing compared to money demand. In return, this results in the devotion of more resources toward consumption spending; enhancing the household’s utility with a greater impact. This points out to the criticality of the impact of IES on welfare. To clarify this relative importance of IESs on welfare, the specific cases of the inverse of the elasticity of money holdings, namely safe haven and black hole, of the money-in-utility (MIU) model are investigated. Specifically, in the former case, the reciprocal of the IES of real money balances is set to a lower value than in the latter case. The simulations of this analysis suggest that while the borrowers can be still better off from rising inflation in the safe haven case even under the presence of an additional distortion, they are worse off in the majority of the cases of MIU setting due to the desire for holding money. The augmentation of money demand motive into the economy requires favoring the borrowers, such as

The contribution of this paper to the literature is three-fold. First, the distributional consequences of inflation are based neither on different productivity levels nor on unexpected inflation changes as in the existing literature. Inflation has a direct impact on a household’s net worth by reducing the maximum amount of debt that can be issued as the debt contracts are agreed on in nominal terms. Because of the lowered real value of debt repayment received by the lender from the borrower, even expected inflation has redistributive effects from lenders to borrowers. Although the amplification of the redistributive effects from monetary policy is observed when heterogeneous productivity levels are introduced, redistribution is found to be still present even with homogeneous productivities. Second, even in the absence of idiosyncratic income shock, of market incompleteness stemming from aggregate risk, of the utilization of the overlapping generations (OLG) model, and of money demand together with anticipated inflation, this study shows that changes in inflation have real effects contrary to the previous literature. Third, the current paper does not incorporate money into the framework to ensure self-insurance in the form of precautionary money demand. In other words, rather than substituting as a tool for a guarantee, attaching value to money introduces additional friction to the economy in the form of an inflation tax in contrast to the existing literature. Additionally, this study endogenizes the labor supply decision and money creation which the existing literature lacks; and attempts to reconcile the divergent results in this line of literature.

The concept that has been investigated here, in essence, is related to the inflation risk of the bond. Bonds have nominal face values unless they are inflation-indexed. Hence, their real values change with the inflation rate. As stated by Campbell and Viceira (2001), while the prices of both nominal government and inflation-indexed bonds vary with the real interest rate, the prices of nominal government bonds also change with the expected inflation, leading to an impact on investors’ risk premia by inflation risk. Furthermore, the nominal bond returns respond to both the real interest rates and the expected inflation. For instance, Campbell et al. (2017) find that high inflation is associated with high bond yields and low bond returns. In modern economies, investors (i.e., lenders) can avoid the loss by hedging themselves against this inflation risk associated with nominal bonds via holding the inflation-indexed bonds issued by governments or corporate firms. In this study, the debt securities (i.e., bonds) are issued by the borrower households; and the results are compatible with the literature, implying a loss for the lenders (i.e., investors) due to the higher expected inflation in the absence of inflation-indexed bonds (i.e., rational borrowing constraint).

The remainder of the paper is as follows. Section 2 reviews the literature. Section 3 lays out the model environment. Section 3.1 defines the equilibrium of the cashless economy, Section 3.2 discusses the steady state of the cashless economy and Section 3.3 contains the simulation exercises of the cashless economy. In Section 4, the MIU model is introduced; and the equilibrium together with simulation results is presented. Finally, Section 5 discusses the results.

Literature Review

From the theoretical perspective, the redistributive effects of monetary policy in the literature are generally attributed to unanticipated inflation changes and exogenous heterogeneity between households. In the paper of Beetsma and Van Der Ploeg (1996), heterogeneity arises because of the different productivity of labor; and in an attempt to redistribute from the rich to the poor, they levy unanticipated inflation taxes to erode the real value of debt kept by the rich. According to Albanesi (2007), the redistributional effect of inflation relies on the equilibrium differences in transaction patterns across households which depend on the labor productivity differences. Pescatori (2007) finds that inflation has redistributional effects on the rich and the poor where households are categorized according to an exogenous distribution of assets. In their OLG model with age and cohort effects, Cao et al. (2021) find that an unexpected increase in inflation redistributes wealth as young household gains wealth from mortgage holdings while older household loses due to long-term nominal assets and pension positions.

Non-neutrality of monetary policy is investigated in theoretical frameworks with aggregate or idiosyncratic risks, capital market imperfections, capital tax distortions, labor supply distortions, distortionary redistribution of seigniorage, and different market structures. Doepke and Schneider (2006) suggest that since the borrowers tend to be younger than the lenders, the redistribution caused by unanticipated inflation has a negative effect on the output which is a result attained by the use of the OLG model. Algan and Ragot (2010) use heterogeneous households, who can partially insure themselves against idiosyncratic income shocks, facing credit constraints. They show that inflation has real effects as long as the financial borrowing constraint is binding as it would induce endogenous decision-making in money demand. Sheedy (2014) studies an incomplete financial market setting where aggregate uncertainty in output results in non-contingent debt contracts; and shows that in the case where there is no uncertainty about the growth of real output and no unexpected changes in inflation, the equilibrium steady state is independent of monetary policy. Mongey (2021) explores the effect of monetary policy shocks via different firm structures on top of idiosyncratic and aggregate shocks. Complementarity between a firm’s and competitor’s prices generates larger output responses with respect to large idiosyncratic shocks when oligopoly is modeled rather than monopolistically competitive firms. Aruoba et al. (2022) show monetary non-neutrality, that is consistent with the micro and macro evidence, with a model featuring strategic complementarities, Kimball demand system and idiosyncratic productivity and demand shocks.

The existing heterogeneous agent monetary economy studies examine the settings where money is valued, at least partly, as it grants the agents self-insurance against idiosyncratic shocks. The motivation for holding money in these papers is derived from market timing frictions, cash-in-advance constraints and the precautionary role of money. They differ in whether money is the only available asset for agents’ portfolio decisions and also in their results. Akyol (2004) considers an incomplete market economy in which agents hold bonds and money against idiosyncratic productivity shocks. In his paper, market-timing friction together with positive inflation redistributes income from the high- to low-income agents. Molico (2006) introduces a random matching model where agents are hit by i.i.d shocks that restrict them to be a buyer or a seller and suggests that if inflation is low, higher inflation can enhance social welfare as it decreases price dispersion and wealth. In a dynamic general equilibrium model where agents with different capital and money endowments buy final goods with cash (i.e., cash-in-advance constraint) or credit, Chang et al. (2022) show that agents reallocate their consumption between credit or cash goods and their assets between capital and money to hedge against inflation as inflation increases. With strong substitutability between cash and credit goods, income inequality is shown to be decreasing in rising inflation.

On the contrary, in their matching model, Boel and Camera (2009) assert that inflation does not cause large losses in social welfare; yet, the consequences on distribution can be immense, depending on the financial structure of the economy. Camera and Chien (2014) examine an economy where ex-post heterogeneity is formed with labor productivity shocks that follow a Markow process; agents are allowed to hold money and bond, considering a cash-in-advance constraint; and the money supply evolves deterministically. They show that when only money is available in self-insurance, inflation alleviates wealth disparities; otherwise, it may rise wealth inequality. Hazra (2018) analyzes the segmented asset market together with limited access to the credit market by introducing (non-)participant households to financial markets in which they have (no) access to various means of payment. An increase in the inflation rate brought by an expansionary monetary policy is shown to redistribute consumption from non-participants to participants of the financial market by diminishing the improvement of the overall welfare in a non-segmented market setting. Bielecki et al. (2022) study an OLG model with New Keynesian characteristics and a rich asset structure including nominal and real rigidities. They discover that an expansionary monetary policy reduces net worth inequality linked to life-cycle motives and redistributes welfare from the old to the young generation.

The recent heterogeneous agent monetary policy literature analyzes the optimal monetary policy. Nuño and Thomas (2022) study a model with uninsurable idiosyncratic risk and long-term nominal bonds considering Fisher and liquidity channels for the transmission of monetary policy. Ramsey-optimal monetary policy under commitment redistributes consumption from creditors to debtors. In turn, relative to a zero-inflation regime, the optimal inflationary policy leads to welfare losses for creditors and gains for debtors. Yang (2022) characterizes the rules for the optimal monetary policy in a heterogenous agent New Keynesian (HANK) model. According to the model, inflation has redistributive effects on households via their nominal wealth positions, consumption baskets and earnings elasticity to economic cycles. As a result, an asymmetric monetary policy rule by the utilitarian central bank is suggested where it adopts an accommodative rule toward inflation and an aggressive one toward deflation. Dávila and Schaab (2023) investigate the optimal monetary policy under discretion and commitment in a HANK model. The former leads to an inflationary bias that increases with the planner’s motive for redistributing toward the indebted households whereas the latter implies zero inflation.

Theoretical Model: Cashless Setting

Inflation costs tend to be unevenly distributed across household types due to the wide differences in their money holdings and other nominal positions. This heterogeneity should be accounted for to assess the overall welfare consequences of inflation. Therefore, the model proposed in this paper has two types of households, namely patient and impatient. In monetary economy studies, frictions can be introduced to the theoretical models via cash-in-advance constraints and borrowing constraints. Cash-in-advance constraints necessitate households to have a sufficient amount of cash to purchase goods by creating cash goods versus credit goods distinction. On the other hand, borrowing constraints limit the amount of resources that could be borrowed from savers, government or banks by making it impossible for the borrower to have infinitely large consumption currently. In the cashless setting, there is no room for money-holding decisions. Furthermore, analytical models with borrowers and lenders are likely to use borrowing constraints to complement the framework. Hence, cash-in-advance constraint is not utilized in the theoretical models, instead, nominal friction is incorporated into the model via a borrowing constraint.

The discrete time, infinite horizon model is populated by patient and impatient households. The heterogeneity in them stems from the difference between their time preference in addition to labor productivity. Both types of households decide on how much to consume, work and hold assets in the form of bonds. Additionally, impatient households are allowed to accumulate debt funded by patient households. Competitive firms produce the final goods by utilizing the labor supplies from both types. Monetary policy is assumed to control the inflation rate.

The patient households differ from the impatient ones as they exhibit higher patience rates (e.g., Iacoviello, 2005; Monacelli, 2006). This, in return, defines their position toward bond holding, which identifies them as lenders or borrowers. The interaction between the borrowers and the lenders, therefore, occurs in the bond market. Lenders hold the bonds issued by borrowers in the sense that what is defined as an inflow of funds for one type means an outflow for the other type of household. There is no explicit default and aggregate uncertainty in the economy. Yet, the bond market can still be considered incomplete with nominally non-contingent bonds. Bonds are non-contingent in the sense that when the period of maturity comes for repayment, the amount of repayment is diminished by the inflation rate at the time of maturity and the time preference of the borrowers because of the period difference between obtaining the loan and maturity. In addition to this, a less developed financial market where neither future income nor durable goods can be pledged for securitization of the debt obligation is considered such that lending is restricted by current income. Monetary policy has a direct impact on a household’s net worth by diminishing the real value of outstanding debt by determining a path for the price level.

Both types of households choose the sequence for real consumption

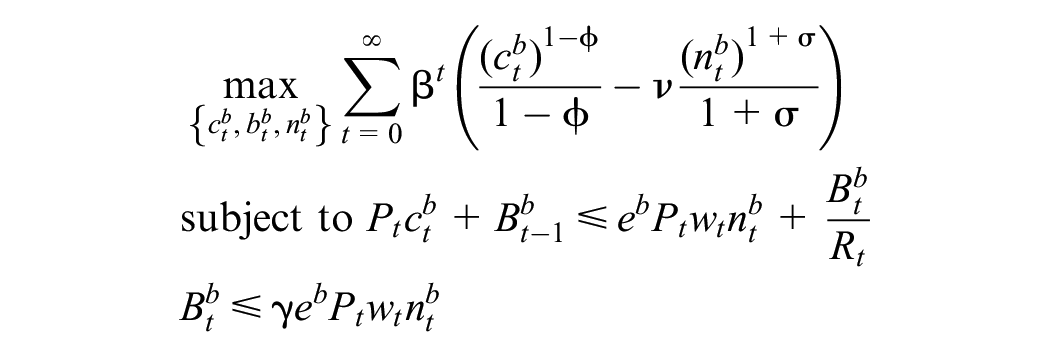

The borrowers maximize a lifetime utility function subject to a budget and a borrowing constraint

where the discount rate is

In the budget constraint,

Household debt can broadly be categorized into two groups, namely non-collateralized and collateralized debt. At the theoretical level, alternatives to this type of credit constraints are given in terms of durable goods, such as land and housing, in the case of collateralized debt (Iacoviello, 2005; Kiyotaki & Moore, 1997 among many others), and of exogenous net indebtedness limit (such as Zeldes, 1989) and tradable goods in an open economy context (see, Monacelli, 2006). However, this is a closed economy model; and there are no durable goods markets to be attached to the loan as collateral (for a similar approach i.e., adopted in this paper, see Bianchi, 2011; Korinek, 2009). Such modeling assumption can be attributed to less developed financial markets where sophisticated financial instruments, compared to income, such as collateralized debt obligations, are not available. Hence, the lenders can only guarantee the repayment from the borrowers, similar to Laibson et al. (2003), by evaluating the borrowers according to their current income. In return, loans provided by the lenders are assumed to be conditioned on the current income of the borrowers. It is important to note that Fafchamps (2014) also emphasizes that granting the poor in developing countries with credit depends on whether they have regular income rather than collateral.

At the empirical level, there are also studies supporting the assumption that the borrowing constraint is given by the current income. For instance, Jappelli (1990) shows that the current income is a major determinant of credit market access. Mishkin (1996) notes that the legal system in developing countries makes securing the credits with collateral a time-consuming and costly process. Additionally, Del-Rio and Young (2005) examine the determinants of participation in the unsecured loan market for 1995 and 2000 in the U.K. and find that the main determinant is the individual income level. Hence, attaching income for securitization of the debt obligation can be referred to in both developing and developed country contexts.

The lenders maximize the following utility function subject to a budget constraint

where

The constraints of the households can be rewritten in real terms. For the borrowers, the budget and the borrowing constraints follow

Competitive firms produce the final goods,

This is a cashless economy where money is not needed for any transactions. Since there is no cash, the monetary authority is only responsible for determining the inflation rate,

Competitive Equilibrium

A competitive equilibrium is a set of sequences

where Equations 1 and 2 are the marginal rate of substitution (MRS) between labor supply and consumption and Euler Equation (EE) for the labor supply of the borrowers; and Equations 5, 6 are those of the lenders respectively. Note that alternative equations to Equations 2 and 6 would be

Market clearing conditions are represented by:

where Equation 7 denotes that of the goods market, Equation 8 of the labor market, and Equation 9 of the bond market.

The production follows

where Equation 12 is the solution to the representative firm’s maximization problem.

Steady State of the Competitive Equilibrium

In the deterministic steady state, the constraints are always binding. Starting with the first-order condition (FOC) with respect to consumption for the borrowers would reveal that the budget constraint has to bind since

The steady state of Equation 6 implies

Notice that

By rearranging the terms in Equation 14, the labor supply decision of the borrowers is obtained:

The unit of labor supply for borrowers increases with the shadow value of borrowing. Intuitively, devoting more time to work enables marginally relaxing the borrowing constraint. Notice that the steady state is indeterminate when

The positive amount of debt holding can be found by evaluating the borrowing constraint together with Equation 15:

Debt is also increasing in the shadow value of borrowing since the additional unit of labor supply accelerates the accumulation of debt.

Similarly,

As the shadow value of the resources within the period (i.e.,

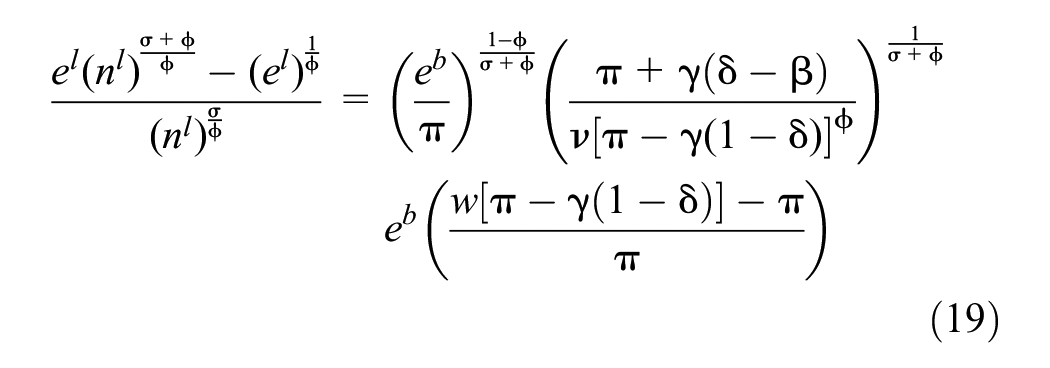

Equations 15 and 16 are not closed-form solutions as they are defined in terms of

where w = 1 at the steady state is introduced. Then, the shadow value of borrowing can also be found from Equation 14:

Now,

Similarly, for

Although

The situation explained above can be understood from the definition of financial market incompleteness by Sheedy (2014). Financial markets are called incomplete when the debt contracts cannot guarantee the debt repayments for all future event realizations. Even though there is no explicit financial incompleteness in the environment studied above, monetary non-neutrality still arises with similar reasoning. Specifically, when the maturity of debt comes (i.e., future event), the value of debt repayment is not the same as the amount of loan obtained from the lender (i.e., realization of event) due to the period difference between obtaining the loan and paying it back. Furthermore, the lender cannot seize the income of the borrower in the case of such a gap (i.e., bad realization of the future event) as there are no durable goods market and future income for pledging as collateral for outstanding debt obligations. This is why the bonds market can be considered incomplete due to nominally non-contingent bonds.

On the other hand, an alternative to the given nominally non-contingent borrowing would be a rational borrowing constraint in a well-established financial market. In such a case, the lenders would limit the borrowing of the impatient households to an amount of income earned at the period of maturity, that is,

A similar problem of not attaining the closed-form solutions of lenders’ choices persists. Hence, complex expressions are not listed here to save space.

At the steady state, one would get the following allocations for borrowers:

The closed-form equations suggest that the rational borrowing constraint would impose monetary neutrality. The comparison of the EE from the rational and the nominally non-contingent debt contracts indicates that since the changes in the inflation rate translate into the changes in the interest rate, the monetary neutrality is sustained. Intuitively, the lag difference in time between obtaining the loan and paying it back is compensated by receiving back an amount that is inflation-indexed at the time of maturity. Therefore, departing from the rational borrowing constraint entails nominal friction which, in particular, stems from the bond market incompleteness that manifests itself in the form of nominal non-contingent debt contracts. In this regard, borrowing constraint in the nominally non-contingent debt contracts causes non-neutral effects in employing monetary policy.

Simulation

Monetary non-neutrality and redistributional effects of anticipated inflation are tractable via the utilization of a simulation exercise. In the simulations below, the gross inflation rate varies between [1;4]; and under this variation, the variables of interest are calculated at the steady state for given inflation rates; and those points are interpolated to allow for an evaluation of the behaviors of these variables. The calibration of parameters follows the standard procedure of assigning values from the relevant literature and of achieving average values observed in the data.

In this simulation, the numerical results assume a quarterly frequency. In order to avoid any results that are dependent on some specific parameters, alternative parameter values are also checked (see,

Parameter Values for Cashless Economy.

Note. IES = intertemporal elasticity of substitution; TPF = total factor productivity; RBC = Real Business Cycle.

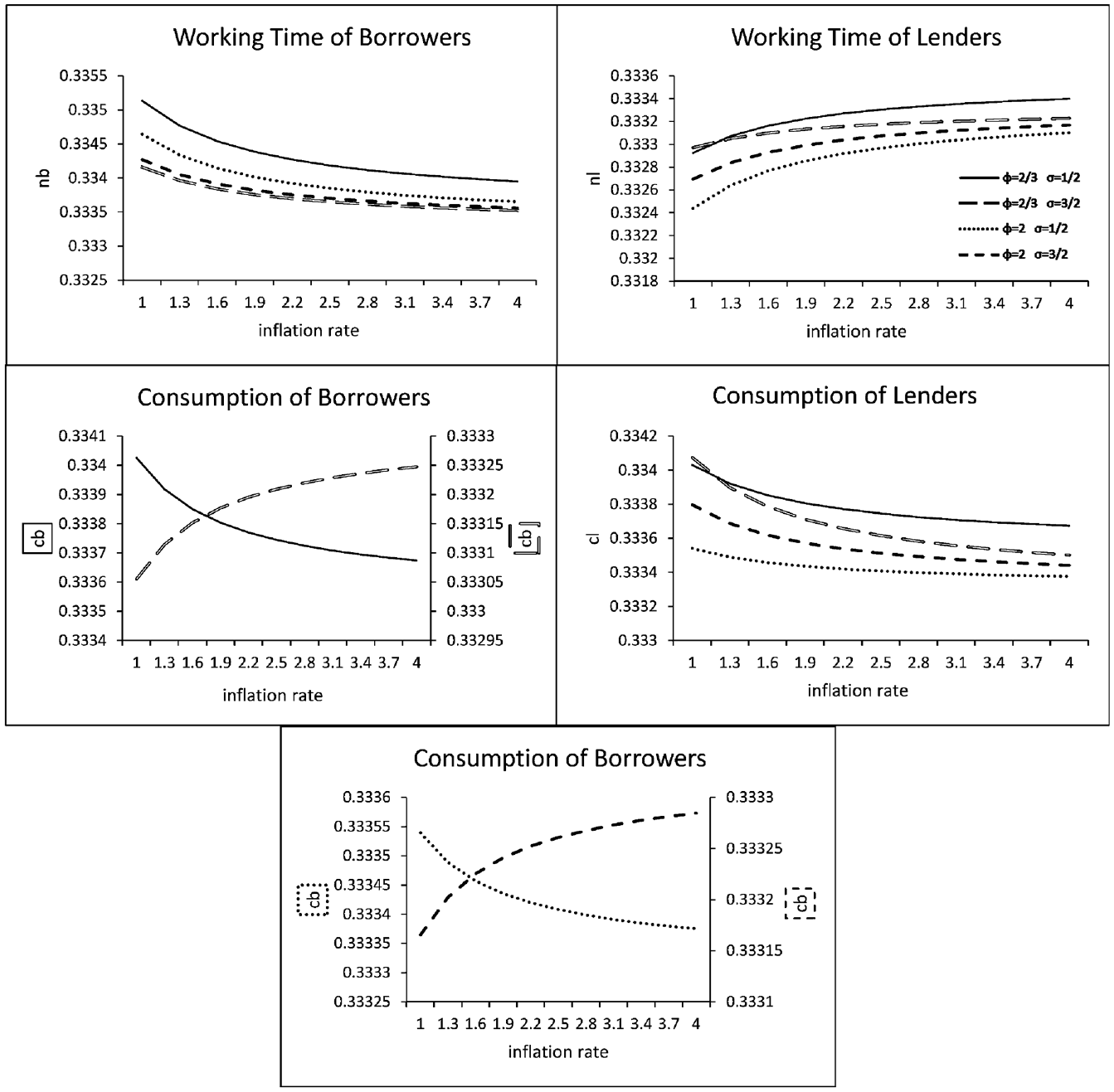

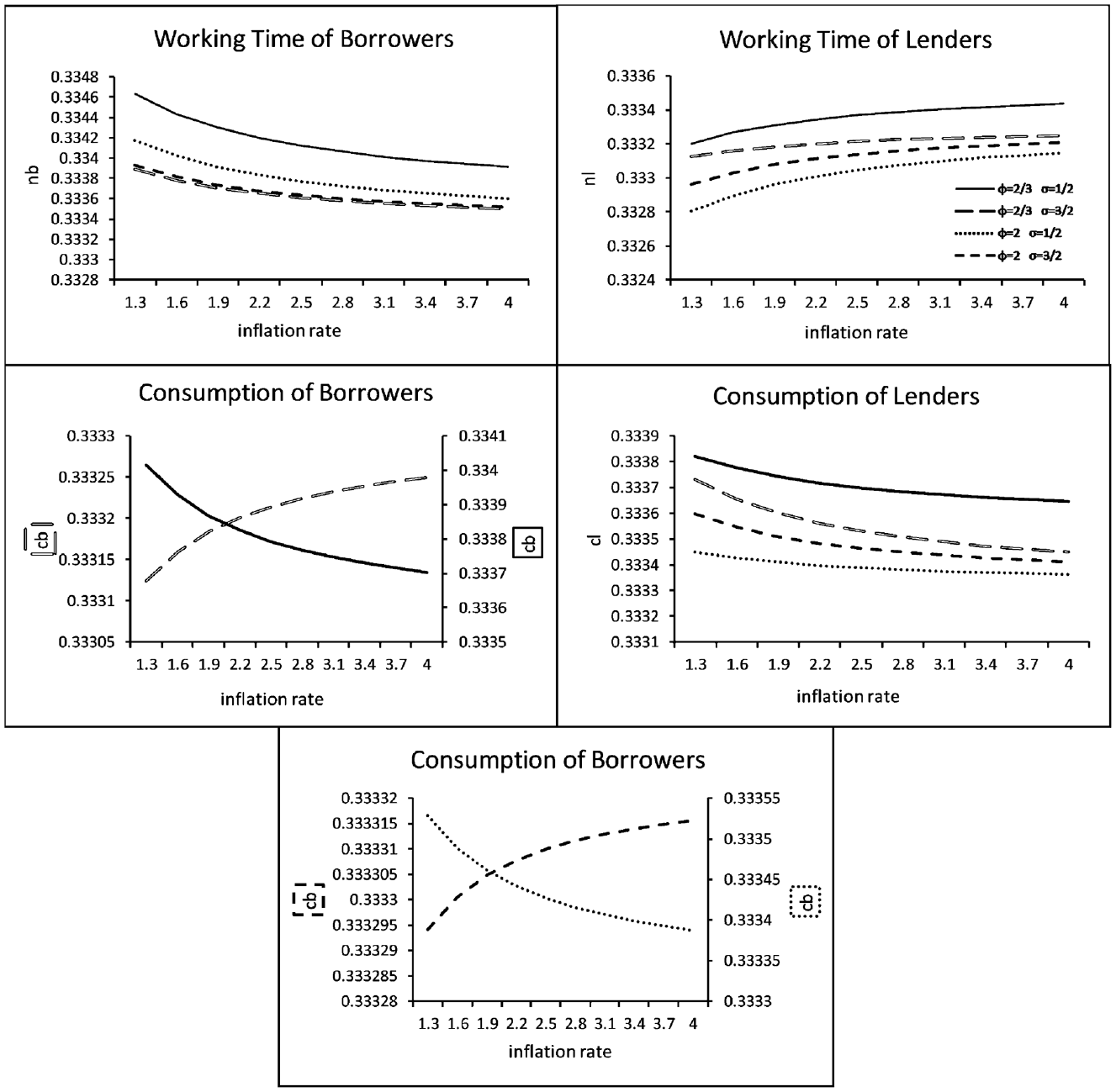

As indicated in Figure 1, when two types of households are homogeneous in terms of their productivity levels, their steady-state labor supplies start at a similar level (i.e.,

Cashless Economy with

Cashless Economy with

The consumption for lenders is a decreasing function of the inflation rate in both homogeneous and heterogeneous productivity levels, as shown in Figures 1 and 2. In the case of equal productivity, the steady state level of consumption for lenders is always less than the one in a different productivity level as the higher productivity level provides more resources available for consumption spending. Although the labor supply of the lenders rises with inflation, this does not manifest itself in the trend of their consumption. The reason for this decrease in consumption is the fact that the value of the debt they loan out decreases with increasing inflation, yielding fewer resources for consumption. For the borrowers, the consumption is increasing in inflation rate when

The individual behaviors in consumption and working time of the two types give rise to the depicted utility trends toward increasing inflation rates as in Figures 3 and 4. The utility of borrowers rises whereas that of lenders decays in all cases. Since the higher productivity of the lender enlarges the economic pie in the heterogeneous productivity case, both types enjoy larger utilities here compared to their homogeneous counterpart. The differing impacts of inflation on the utilities of two types suggest that the borrower prefers higher inflation rates than the lender as they benefit from inflation contrary to the lenders. A simple calculation of utilitarian welfare with different weights attached to two types is analyzed to see the behavior of the social welfare of the economy for various inflation rates. For instance,

Cashless economy with

Cashless economy with

Cashless economy with

Cashless economy with

Finally, the comparison regarding the productivity levels reflects that when heterogeneous productivity levels are assumed, the utilitarian welfare gain is larger in both magnitude and level than the gain in the equal productivity case. For instance, Figures 5 and 6 indicate that when

Theoretical Model: Money-in-Utility Setting

The augmentation of money demand to the cashless economy enables the prescription of varying inflation rates considering the welfare costs of inflation tax as well. Here, to facilitate the comparison with the cashless economy, additive separable utility is assumed, and the maximization problems are expressed in real terms. In this setting, both households have an additional decision to make, namely money holdings, where

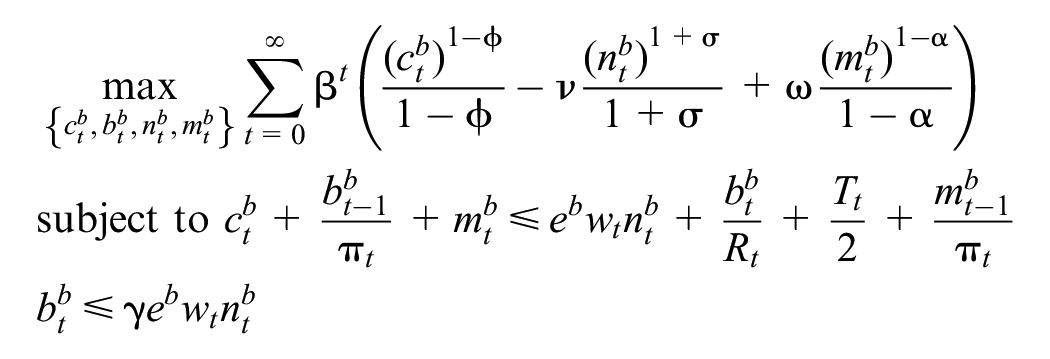

The borrowers maximize their lifetime utility subject to budget and borrowing constraints:

The lenders maximize their lifetime utility subject to only a budget constraint:

where

The competitive equilibrium of this economy is described by the following set of equations:

together with Equations 7–12. As it can be seen from Equations 28, 29 together with 22, 27, the real money balances root in the decisions of the two types of households instead of following an exogenously given rate.

The simulation exercise of the MIU model depends on the previous parameter values in order to simplify the comparison. For the reciprocal of the IES of real money balances,

Parameter Values for MIU Model.

Note. IES = intertemporal elasticity of substitution; TPF = total factor productivity; RBC = Real Business Cycle.

Throughout the analysis, homogeneous productivity levels (i.e.,

As depicted by Figure 1 together with Figures 7 and 8, a comparison of the MIU model with the cashless setting demonstrates that the trends of labor and consumption are the same. The decisions are made around the same level as the second decimal with the cashless economy. Both types hold almost the same amount of real money balances with respect to changes in the inflation rate as in Figures 9 and 10. The holdings of real money balances by the lenders are negligibly more than the borrowers. They only differ in the fifth and third decimals in the safe haven and the black hole cases respectively. Although households derive utility from holding real money balances, both the borrowers and the lenders mitigate their money holdings as their value diminishes with rising inflation. The level of real money holdings in the

Safe haven with

Black hole with

Safe haven with

Black hole with

The levels of utilities in MIU are different from the cashless setting as the comparison of Figure 3 and Figures 11 and 12 suggest, stemming from the augmentation of the real money balances into the utility. Since both types of households hold positive amounts of real money balances and derive utility from holding them, the utilities are slightly higher (smaller) in levels in the safe haven (black hole) case compared to the cashless economy. While the behavior of lender’s utility with respect to rising inflation is the same across settings, in other words, lenders are always hurt by higher inflation regardless of the setting and cases, that of borrower’s utility differs with respect to both settings and cases. Specifically, the behavior of utility of borrowers rises with inflation in the cashless setting; decreases with inflation in the black hole case; and depends on the parameterizations in the safe haven case.

Safe haven with

Black hole with

The cashless economy states that the utility of borrowers increases with inflation in all parameterizations. Because either, both decisions are in favor of the utility (i.e.,

As Figure 12 illustrates, the behaviors of the utility of borrowers are decreasing in all parameterizations in the black hole case. The smaller the

When the social planner treats the types equally in the safe haven case, as in Figure 13, the utilitarian welfare reduces with inflation regardless of the occasional positive effects (remember that in

Safe haven with

Black hole with

In short, simulation exercises allow us to trace the effect of inflation on real variables as they change with anticipated inflation, that is, non-neutrality, and redistributive effect of inflation as there are welfare losses and gains.

Conclusion

The optimal monetary policy in the sense of a specific inflation rate offer is beyond the scope of the analysis in this study. Instead, this paper is concerned with the long-run role of the monetary policy; how it influences patient and impatient households; and thereby utilitarian welfare. In turn, it attempts to provide a prescription to a policy planner in setting inflation rates.

In the cashless economy, the presence of nominally non-contingent bonds in the form of nominally non-contingent borrowing constraints creates nominal friction due to the structure of this constraint, which results in non-neutral effects of anticipated inflation. However, with the introduction of sophisticated financial instruments, the rational borrowing constraint sustains monetary neutrality. The debt contracts’ being predetermined in nominal terms causes a redistribution from lenders to borrowers, which is amplified when heterogeneous productivity levels are imposed. In the majority of the cases of the MIU setting, the borrowers are worse off under the presence of an additional distortion, in the form of inflation tax; and the lenders are always losing due to higher inflation. The augmentation of money demand motive into the economy requires favoring the borrowers to be able to achieve occasional welfare gains. On the other hand, the social planner can mute the welfare loss by generating inflation without caring for one type more than the other in the cashless economy. Hence, this study shows that the anticipated inflation rate has long-run real impacts, it disproportionately affects heterogeneous households by redistributing from lenders to borrowers; and whether the inflation rate can be used as an instrument to improve utilitarian welfare relies on the presence of money demand motive, the concern with pro-lender/borrower bias, the relationship between IESs and the heterogeneous productivity levels. In other words, the policy planner should be concerned with these features when targeting an inflation rate to account for the welfare effects of that policy.

In modern economies, with the introduction of cryptocurrencies and the emergence of central bank digital currencies to the economy, the presence of money demand motive might diminish in the future, reducing the impact of inflation on welfare that stems from the relative strength of the smoothing motivations (i.e., IESs). This may imply that central banks can choose higher inflation targets in the future than they are setting now. Because doing so would not incorporate an additional distortion on households as with the money-holding decisions, facilitating an easier balancing of borrowers with lenders in terms of welfare. Specifically, the problem for the policymaker in using the inflation rate as an instrument to improve welfare and reduce inequality might simplify to a cashless setting in this paper with the pro-borrower bias as will be followed by Fed and ECB.

This paper can also be considered as a guide for monetary policymakers in a globally interlinked environment. With an analogy of developing countries as borrowers and developed countries as lenders, this paper suggests that inflation wedges between these countries define the future of developing countries in paying their debts. Since it is hard to immediately identify such consequences in such an analogy, the proposition is better suited to the economic and monetary unions as they are bounded by the decisions of the same policy-maker institution. In unions, the member countries, where not all the economies exhibit the same advancement in terms of characteristics and structure as each other, are subject to non-customized decisions of the policy-maker institution. In other words, a common monetary policy results in the same interest rate and the same inflation rate across the monetary union even though while one country is in an economic boom, the other experiences recession, or one is under a debt burden while the other is relatively prosperous. This study suggests that the actions by the monetary authority can still achieve union-wide welfare gain accounting for the above-stated factors without benefiting only some of the participant countries at the cost of a loss for the rest of the countries embodied in the union. Because it has been shown that an equilibrium inflation initiated for the benefit of the lender is likely to be harmful to the borrower and vice-versa. A particular example, in this case, could be the European Union (EU) where the member countries are tied by the decisions of the ECB. Some countries in the union, such as Germany, have relatively better economic conditions than other countries, such as Greece. Among these member countries, some funds are changing hands in order to sustain solidarity and cohesion in the EU. Keeping in mind the reign of below

As a two-agent model with several heterogeneities and a borrowing constraint, the theoretical model is already complicated and hard to trace without the use of software. This is why, for instance, a simple linear production function is adopted in the model. Yet, with this choice, the model abstains from other rigidities than inflation tax that the recent literature tends to augment. Hence, further endeavors in this topic could be to incorporate monopolistically competitive firms and to pinpoint an optimal inflation rate.

Footnotes

Acknowledgements

I would like to express my gratitude to Andreas Schabert for his suggestions.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data supporting the findings of this study are available from the corresponding author on request.