Abstract

In classical literatures, the informal sector is regarded as all those economic activities that are neither taxed nor monitored by any form of government. However, with the downturn of economic activities in Nigeria due to the dwindling oil revenue which forms the major revenue generation and export earnings of Nigeria, the informal sector, specifically the motorcycle transport business popularly known in Nigeria as Okada has come under some form of government taxation and monitoring in some states in the country. This was to shore up their revenue base which has dwindled over the years. Extant literatures have not been able to examine the contribution of informal sector, specifically, the motorcycle transport business to internally generated revenue of the sub-units, especially Ebonyi State within the period under study. Thus, we pose the question: has the taxation of the motorcycle transport business operation improved on the internally generated revenue of Ebonyi State between 2015 and 2021? We anchored our analysis on Public Choice Theory of politics and economics. Data for the study were collected through both primary and secondary sources. The study found that despite the intensive taxation of the informal sector in Ebonyi State, specifically, the motorcycle transport business; the internally generated revenue of the state seems to be decreasing rather than increasing, given the number of taxable objects that has been brought under its internally generated revenue sources. The study recommended that the government should do more in the area of its internally generated revenue to ensure efficiency in collectability and remittances.

Plain language summary

The study found that despite the intensive taxation of the informal sector in Ebonyi State, specifically, the motorcycle transport business; the internally generated revenue of the state seems to be decreasing rather than increasing, given the number of taxable objects that has been brought under its internally generated revenue sources.

Introduction

The capacity of the informal sector of the Nigerian economy to persist and generate economic development has often been underrated. This according to Udeogu (2016) was as a result of the prevailing optimism in the 1950s and 1960s inspired by the modernization theory of development championed by Arthur W. Lewis, which was that traditional forms of work and production which today technically come under the informal sector, would disappear as a result of economic progress in the developing countries. Thus, Carr and Chen (2001) had noted that the inspiring thrust of this optimism could, however, not be sustained when most of the developing countries did not create enough formal jobs in their development plans. Hence, they went ahead to state that the direct consequence of this failure to create formal jobs was the formation of an informal sector that did not solely include marginal works but actually profitable opportunities.

Moreover, this underrating of the informal sector of the Nigerian economy has led to its general negligence in development policies and national accounting. This has been the case irrespective of the fact that the sector has been noted to account for about 83% of employment in Africa and 85% of total employment in Sub-Saharan African countries (ILO, 2022) and about 57.7% of the gross domestic product (GDP) in Nigeria (Monye & Abang, 2020). Dada (2016) noted that the reason for the non collapse of the Nigerian economy is the sustaining power and ability of the neglected informal sector of the economy. Thus, with the persistence and the resilience of the informal sector, as well as the dwindling of the federally collectable revenue from oil, attention of the sub-units in Nigeria has turned to the informal sector as an alternative means of revenue generation for developmental purposes. Consequently, Ebonyi State government now captures the motorcycle transport business in its tax net through a joint account with the local government but managed by the State. It is against this background that we examined the taxation of motorcycle transport business and internally generated revenue of Ebonyi State within these periods.

Statement of the Problem

States in Nigeria currently face the problem of financial mobilization for their enormous development programs and projects. This is as a result of heavy reliance on the federally allocated revenues which has been on the decline as a result of plummeting oil revenues that serve as the back bone of the Nigerian economy. Recently, Chete et al. (2017) in addressing the important role oil and oil products play in the economic development of Nigeria asserted that: “oil and gas sector, in particular, continues to be a major driver of the economy, accounting for over 95% of export earnings and about 85% of government revenue between 2011 and 2012”. Moreover, Onuba (2017) had reported that as at 2014, oil still contributed 92% of Nigeria’s earnings.

However, the non-oil sector has taken over from the oil sector contributing 93.25% to Nigeria’s GDP in the fourth quarter of 2016 and 89.96% in the third quarter of 2017. The annual contribution of the oil and non-oil sector to the Nigerian GDP in 2016 was 91.32% and 91.65% respectively (NBS, 2018). Meanwhile, crude oil price in the global market plunged, dropping from $112 per barrel in 2014 to almost $38 per barrel as at the end of 2015 due to the incessant and massive supply of Shale oil by the United States to the global market (Olayungbo & Olayemi, 2018). Hence, federally collected revenues and consequently, amount of federal transfers to states in Nigeria have significantly dwindled since 2015. Therefore, this creates a considerable challenge to state governments in managing their budgets as a significant reduction in revenue hinders the ability of state governments to provide basic public services to the citizens.

Accordingly, Nigeria’s Governors Forum—NGF (2015) had pointed out that many states in Nigeria are currently making efforts to diversify and increase internally generated revenue (IGR). Measures range from extensive tax policy reforms to administrative measures like improved remittances and recording. Some of these measures which cut across the states involve the expansion of tax base by bringing more persons and activities into the tax net, including taxing of the informal sector (Presumptive Tax Initiative) (NGF, 2015).

Thus, Ebonyi State government resorted to intensive tax and taxation of various business activities including the motorcycle transport business as the alternative means of financial mobilization. The emergence of the motorcycle transport business has attracted the attention of scholars on the nature, dynamics and different aspects of the business activities. Among the study on the motorcycle transport business, few are Asekhame and Oisamoje (2013) that appraised the ban on commercial motorcycle operation in Benin City, Akume et al. (2014) that inquired into the implications of the interdiction of motorcycle transport business on transportation, for human security, poverty reduction, and sustainable development in Kaduna State, Oluwaseyi et al. (2014) that assessed commercial motorcycle operation as a means of urban mobility, Al-Hasan et al. (2015) that tried to find out the motives of people engaged in the operation of motorcycle transport business and their job satisfaction, Udeogu (2016) who investigated the motorcycle transport business and employment generation in Nsukka, Enugu State and more recently Ezeibe et al. (2017) who investigated collective organizing of motorcycle taxis in Nigerian cities among many other literatures.

Notwithstanding the fact that various writings and researches on the motorcycle transport business have tended to reflect different aspects of motorcycle transport business both as a means of transportation, employment generation and collective organizing among the members, etc.; none has tried to examine the state taxation of the motorcycle transport business and internally generated revenues in Ebonyi State. Thus, this study was guided by this research question: has the taxation of motorcycle transport business operation improved on the internally generated revenue of Ebonyi State between 2015 and 2021?

Theoretical Framework

The study adopted the public choice theory as its theoretical framework. Mbaku (2008) pointed out that public choice theory was developed in the early 1960s by Gordon Tullock and James M. Buchanan, who had been studying the political dimension of wealth creation and economic growth and introduced the public choice model as a more effective and intellectually satisfying paradigm for the analysis of public policy. The pioneers of the public choice theory are James M. Buchanan and Gordon Tullock with their book “The Calculus of Consent,” however, Kul and Yuksel (2018, p. 91) cited in Firidin (2022) pointed out that Buchanan and Tullock (1962) were influenced by Knut Wicksell and even considered Wicksell as one of the first pioneers of the Public Choice approach. Public choice theory is a theory that explains the relationship between decisions taken in public administration with politics and economy and the behavior of individuals operating in this field. The assumption of the public choice theory is that individuals see their individual benefits above the public interest when making political decisions. According to this theory, the individual does not consider the needs of the public institution and citizens as a priority when making political or administrative decisions. The important thing for him is to satisfy his individual profit and pleasure

According to the public choice theory, people, decision makers in particular, do not act on the principle of social benefit. For the Public Choice Theory, there are four basic groups that make up the economic and social life. These are politicians, bureaucrats, voters, and pressure and interest groups (Kul & Yüksel, 2018, p. 99, cited in Firidin, 2022). Public Choice Theory also is the result of individual subjective evaluations faced by groups or organizations independent of individuals, unlike the social interest approach (Özer and Kartal, 2021, p. 50, cited in Firidin, 2022). The Public Choice Theory emphasizes that all four groups will exhibit attitudes toward their own benefit maximization and that the political equilibrium will be reached through an exchange in which each group will provide its own benefit (Kul and Yüksel, 2018, p. 99, cited in Firidin, 2022). According to Buchanan, Public Choice Theory aims to establish a link between economics and political science. It is a working discipline (Odabaş, 2019, p. 99, cited in Firidin, 2022). Public choice is a discipline that explains the decisions and practices taken in the political process with the tools, methods and assumptions used by economics. In other words, Public Choice analyzes the issues of political science with the help of the tools and techniques of economics (Baysuğ, 2017, p. 91, cited in Firidin, 2022). In keeping with Lane (1990, pp. 76–80) as cited in Firidin (2022), the principles of public choice theory in the literature are listed as follow:

Methodological Individualism: According to this principle, decision makers are individuals. In social groups or other similar formations, decision makers are individuals. Therefore, when making decisions, individuals give priority to their own interests rather than the general interests of the human community.

Homo Economicus: Public choice theory rejects the idea that social interest can be produced. Individuals work for their own interests within the framework of certain rules and priorities. In order to talk about a social interest, it is necessary to calculate the total interests of people as individuals.

Politics as Exchange: The axiom of politics as exchange means that each and every public policy must be based on the consent of all the citizens, as unanimity is the criterion for which the policy works in the interest of the citizen. This is certainly, as Buchanan emphasizes a very optimistic interpretation of the nature of politics as legitimated by the interests of the citizens. However, this is not positive theory but elements of an ethical theory of the state. In the public choice domain, which the public choice approach is aimed at understanding, politics reveals itself in a number of different ways. These are coercion over corporate interests formed at the expense of consumer interests and the few cases where broad citizen interests rule. The unanimity rule introduced by Wicksell may be given two different interpretations between which Buchanan does not distinguish. Additionally, we have the positivist interpretation meaning that politics is exchange between individuals in a setting of political institutions.

Application of the Theory to the Study

The significance of this theory to the study is that, the imposition of tax on the motorcycle transport business operators in Ebonyi State by Ebonyi State government is a public choice. This choice aims to shore up the revenue of the government so as to be able to provide public good for the citizens and residents of the state. However, due to the divergence between the public good and the individual perception of their own economic good, there is a thigh tendency for malpractices among the tax agents and the motorcycle transport business operators. This can take the form of tax evasion or non remittance of collectable taxes to the appropriate authority. Even though, taxation is a tool that enhances the state’s financial position in the provision of public good, some of the tax collection agents may see this as an avenue to enrich their pockets or to trade favors with some of the motorcycle transport business operators for sundry reasons. Moreover, some of the motorcycle transports business operators who may not see any bearing between taxation and their personal economic interests may resort to tax evasion and avoidance, all these leading to low revenue yield to the state from the business activity and other taxable revenue yielding activities in the state. Hence, the need for unanimity of purpose in tax administration between the tax administrators, the tax collection agents and motorcycle transport business operators.

Methodology

This study combined both the ex post facto and descriptive designs to cover for the qualitative and quantitative research strategies used in the study. An ex post facto design is used when experimental research is not possible, such as when people have self-selected levels of an independent variable or when a treatment is naturally occurring and the researcher could not “control” the degree of its use. Cohen and Manion (1980) define the ex post facto design as those studies which investigate possible cause-and-effect relationships by observing an existing condition and searching back in time for plausible causal factors. Lammers and Badia (2005) when tracing the origin of ex post facto design noted that the assignment of participants to the levels of the independent variable is based on events that occurred in the past, this is where the name is derived from. In the context of this research, the researcher does not have control over the capacity of state taxation of the motorcycle transport business to improve on the revenue of Ebonyi Sate or otherwise. Thus, there is no control or variation group in this design.

The diagram below will aid this study to explain the causal-comparative design of series of before observations, one case and a series of after observations.

Where:

= Observation

= Observation

= Random assignment of subjects to experimental groups and random assignment of experimental treatments to experimental groups.

= Random assignment of subjects to experimental groups and random assignment of experimental treatments to experimental groups.

= Independent experimental variable which is experimentally manipulated.

= Independent experimental variable which is experimentally manipulated.

= Independent experimental variable.

= Independent experimental variable.

= Before observation

= Before observation

= After observation.

= After observation.

Source. Adopted from Asika (2006) and Leege and Francis (1974).

The logical argument is to demonstrate that (X) is the factor that determines (Y), this infers that (X) as an independent variable informs (Y) as a dependent variable. In other words, whenever (X) occurs there is likelihood that (Y) will follow at some point later. However, testing structural causality based on ex post facto analysis of the independent variable (X) and the dependent variable (Y) is based on concomitant variation. In applying the single case ex post facto design to our study, the test of the hypothesis involves observing the independent variable (state taxation of the motorcycle transport business) and dependent variable (improved revenue); at the same time because the effects of the former on the latter have already taken place before this investigation. A trend selection of series of “before” and “after” observations of the impact of taxation of motorcycle transport business on Ebonyi State internally generated revenue was used to test the hypothesis.

Therefore, the study relied on both primary and secondary sources for data collection. For the primary sources, the study relied on survey method of data collection using in-depth interview and focused group discussions (FGD). Some of the stakeholders in the motorcycle transport business were interviewed on their negotiation with the state government before arriving at N100 daily fee as motorcycle road tax for the motorcycle transport business operators. Meanwhile a group of thirty (30) motorcycle transport business operators were engaged in a focused group discussion on September 3, 2020 to ascertain if there were wide consultations and engagements between them and their union executives as well as the government before arriving at the agreed levy.

For the secondary sources of data, the study relied on documentary sources. These documentary sources included the official register of the motorcycle transport union in the state. Here, data on the number of the registered operators of the business activity in the state within the periods under study were collected. Also, the financial records of the Motorcycle transport union in the state, as the tax agent of the government within the periods under study, were employed in the study; this is where information on the collected revenues from the business activity within the periods under study were drawn. Moreover, the financial records of Ebonyi State Ministry of Finance, specifically, the States Board of Internal Revenue which is the final authority in tax administration in the state, were utilized in generating data on the monthly remitted revenues from the motorcycle transport business operators through their unions within the periods under study. A comparative analysis of the expected tax income to be generated from the business activity (Using the number of registered operators within these periods; assuming that all pays as at when due) with the actual income remitted to the States Board of internal Revenue was used to analyze the revenue gains and losses to the state from the taxation of the motorcycle transport business operators

Population of the Study

The population for this study in respect of answering the research question entailed all the collectable tax revenues that were collected by Ebonyi State Motorcycle Transport Union from all their registered members and remitted to Ebonyi State Ministry of Finance through the States Board of Internal Revenue within the periods under study.

State Taxation of Motorcycle Transport Business and Internally Generated Revenue in Ebonyi State Between 2015 and 2021

Ebonyi State was created in 1996. It was one of the most newly created states in Nigeria. Projecting from the 2006 population census, the state has a population of about 2.3 million people and has a land mass of approximately 5,670 km2 (Quadri, 2021). The state has thirteen (13) Local Government Areas and Twenty one (21) Development Centers. Politically, the state has three senatorial zones namely; Ebonyi North, Ebonyi Central, and Ebonyi South Senatorial Zones. There exist three major commercial areas in the state, which includes; Abakaliki Commercial area, Onueke Commercial area, and Afikpo Commercial area. The state is predominantly rural.

Economically, the basic occupation of the people is farming. It has been estimated that over 80% of the total population of Ebonyi State are employed in agricultural sector (Umeh et al., 2018). Modern industrial establishments are few and are concentrated in Abakaliki the capital city and its environs.

Thus, due to the fact that the state is economically a growing state, there exist many small-scale enterprises and informal sector activities in the state. Most of these small-scale enterprises and informal sector activities fall within the range of farming/extractive enterprises to processing and service oriented enterprises with a few manufacturing enterprises. Some of these enterprises include; quarry industries, block industries, rice mill industries, poultry farms, and motorcycle transport business among others.

Availability of robust revenue sources is a measure of the health of any state’s economy. For any economy to grow and develop, the state must device a revenue source that will enable it carry out its responsibilities to the people. In Ebonyi State, the revenue sources includes: Internally generated revenues (IGR), Capital Receipts which includes federally collected revenue, and loans. However, due to the low development of the IGR mechanism of the state, the state relies heavily on federally collectable revenues and loans (internal and external) and less on the IGR. This can be gleaned from the 2014 budget estimates of the state government as presented in Table 1.

Summary of Revenue Sources to Ebonyi State Government.

Source. 2014 budget of Ebonyi State Government.

However, with the dwindling of federally collectable revenue since 2015, the state has been making effort to shore up its revenue through its internally generated revenue base. It is in this connection that the motorcycle transport business was captured in the tax net of Ebonyi State Government.

Economic Crunch and the Taxation of the Informal Sector in Nigeria

The inability of the state in Nigeria to mobilize adequate financial resources for its development programs and projects led to a reliance on internally generated revenues by the taxation of businesses that were previously not captured in its tax net, including the informal sector economic activities and small scale businesses. This was occasioned by the dwindling oil revenues to the federation account which the component units in Nigeria heavily rely on as their main source of financial mobilization.

To buttress the point, The Economy (March 12, 2015) had one of its articles titled, “2015: Year of Austerity Budgets for the States in Nigeria.” In that article it was pointed out that the year 2015 does not look promising for the states in Nigeria based on the crash in international price of crude oil which is the cash cow of the Nigerian economy, with its attendant dwindling revenue. Hence, to contend with challenges of the dwindling economic fortunes of the country, many state governments have proposed what has been termed as “austere” budgets for 2015. From the budget proposals presented by various state governments and the Federal Government, barring supplementary appropriations, the total amount budgeted by the governments at the federal and state levels was about N10.6 trillion for 2015 as against N12.188 trillion budgeted for 2014 (Ocheni, 2015). In this regard, the prevailing free fall of crude oil price, the decision of the United States (at the time Nigeria’s major oil importer) to stop patronizing Nigeria oil following the discovery of Shale oil and the discovery of alternative energy sources by many developed societies were already hurting Nigeria’s finances before the inception of the new tax regime in Ebonyi State (Ocheni, 2015). Furthermore, financial statistics on States for 1 year, running from June 2014 to June 2015 indicated causes for concern. Report from NGF (2015, p. 7) had made the following observations: In the one year from June 2014 to June 2015, Federal Accounts Allocation Committee (FAAC) revenue pool has shrunk by nearly 45 percent to N409.3 billion following a sharp drop in the price of oil. Nigerian States and the FCT Abuja jointly account for $14.1 billion in both domestic and external debts, against an aggregate of N780 billion ($3.9 billion) raised in internally generated revenues, a deficit of over N2 trillion ($10 billion) over N700 billion ($3.5 billion) of these debts are in commercial bank loans, mostly anchored on Nigeria’s very abnormal and volatile interest rates. Currently, 78 percent of States rely solely on the FAAC allocations for 80 percent of revenue. About 40 percent are presently insolvent, with high risk of defaults and working to reschedule debts. The Federal Debt Management Office (DMO) has already packaged lifelines totaling N575 billion for 23 States to help them meet recurrent obligations (Staff salaries and contractual arrears). Two factors further compound the financial position of States. The first is that recourse to short term commercial bank loans is constrained by CBN’s directive to banks not to give loans to States without clearance from the Federal Ministry of Finance. While this is driven by the legitimate fear of the federal government to forestall potential defaults and moral hazard, it has meant that even capacity for short term liquidity options is limited among States. The second factor is that access to long term loans is constrained by the crowding-out effect of FGN bond issuances in the domestic debt market on the one hand, and by states’ weak book keeping, accounting and auditing infrastructure. Instances exist where States wishing to borrow from the capital market are unable to present either admissible audit reports or acceptable project proposals.

It is in this connection that Ocheni (2015, p. 6) posited that the then fiscal situations of governments in the country are unsustainable and anti-growth. He further noted that, Sharp drops in expenditure, whether capital or recurrent, have social, economic and political implications. Therefore, governments in Nigeria then had the opportunity to take the same set of measures taken in 1979/80 and 1985/86 or seek innovative means of increasing their capacity from sustainable financing. Moreover, the latter will come through simultaneous cuts in the cost of governance, reduction in wastes (through better book keeping and other measures), enforcement of compliance through court and increasing internally generated revenue.

Though, according to NGF (2015), the rebasing of Nigeria’s Gross Domestic Product (GDP) by the National Bureau of Statistics (NBS) in April 2014 to better reflect the structure of the Nigeria economy led to an increase of the GDP by 89% in 2013. Following this, NGF (2015) maintained that Nigeria became Africa’s largest economy with an estimated GDP of $510 billion in 2013 (compared to the $270 billion reported previously). Despite this, NBS (2015) asserted that the country continues to face challenges relating to its fiscal federalism. It furthered that, the tax revenue to GDP ratio declined from about 20% to 12% and non-oil tax from 7% to 4%. These are some of the lowest ratios in the world according to NBS (2015) which also pointed out that the resource allocation in Nigeria is attached to a revenue sharing formula that first gathers all resources to the center and thereafter allocates to each tier of government (local, state, and federal) according to a specified sharing formula which has been a source of friction among federating units since the country transited into full scale federalism in the 1960s.

Moreover, not only are there concerns about the sharing formula for Federally Collected Revenues, there are challenges emanating from the mono product nature of the source of funding, with up to 70% coming from oil. Oil (and other commodity) prices are known to be unstable and such instability is often transmitted first to revenue and thereafter to the rest of the domestic economy (NBS, 2015). The volatility of oil revenues as a result of the instability of global oil market is one major source of concern for such dependence of the Nigerian state governments on revenues accruing to the federation account.

There are issues with the options, capacity, and opportunities for some of the federating units (particularly the states and local governments) to raise internally generated revenues. A number of revenue line items assigned to States by the Constitution are yet to be developed enough to yield robust revenues to them (NGF, 2015). Likewise, that the capacity to harness the revenue sources and collect what is needed is limited almost in all States. Hence, with significant revenue sources in the hands of the federal government therefore, many states depend on transfers from the Federation account for as much as 80% of their fiscal resources. Hence, this has affected the capacity of the States to run the most basic machineries of government without the monthly allocation, NBS (2015) had maintained. Meanwhile the Punch (2017, April 20) had affirmed that: As the price of crude oil in the global market plunges, moving from about $115 in June 2014 to less than $60 in September 2015, governments across the three tiers are experiencing fiscal crunch. Federal transfers to States have significantly reduced. This poses significant challenges to the State governments in managing their budgets as a significant reduction in revenues hampers the ability of State governments to deliver basic services (education, health and others) to citizens. The situation is particularly acute in States where internally generated revenue is low. Such States have been in arrears of civil servants’ salaries, pension, suppliers and contractors payment for several months. Recently, States using the Nigeria’s Governors Forum (NGF) platform requested for the urgent financial support from the federal government. While the request was granted, they were advised to improve efficiency of public spending by cutting waste and duplication as well as mobilizing internally generated revenue.

Moreover, according to Ocheni (2015), calls and efforts to improve internally generated revenue across Nigerian States have been on for many years. He put forward that different governments at all times and across all regions of Nigeria have shown interest in improving their revenues. Some have worked more deliberately with varying results while others merely discussed the need to work on it. In his words: While oil prices and sales remained favourable, States could afford to be laissez-faire about improving non-oil, internally generated revenue. However, given Nigeria’s current fiscal position, and the short to medium term financial forecasts, improving internally generated revenue is no longer an option among many; it is currently the only one available (Ocheni, 2015, p. 8)

Therefore, it is in this connection that the resort by Ebonyi State government to shore up its revenue position through a new tax regime that entails the taxation of small scale businesses and the informal sector should be understood and explained.

Taxation of Informal Sector in Ebonyi State Within the Context of Nigerian Economic Crunch

With the fact stated above, one can be in a better position to understand the general economic environment under which a new tax regime was introduced in Ebonyi State. To corroborate this fact, in a 2017 budget presentation of Ebonyi State Government by the Governor, His Excellency David Umahi, had averred that: The gross domestic product (GDP) of Nigeria shrank by 1.3% (year-on-year) in the fourth quarter of 2016 from a 2.24% decline in the corresponding period of 2015. Inflation worsened from 12.77% in 2016 to 17.77% in 2017. The exchange rate regime which was N196.5 to $1 in March 2016 weakened to N306 to $1 in March 2017 at the official rate. Thus, in Ebonyi State, our well articulated plans and policies for inclusive growth and poverty reduction – the pillar planks of the 2017 Budget estimates were also threatened.

Furthermore, to lend more credence to the above assertion from the Governor, News Express (October 31, 2015) had observed that Ebonyi State Government in 2015 budgeted for N80 billion which is lower than the downward revised budget of N85.6 billion for 2014. Therefore, when the incumbent Governor of the state, David Umahi took over office from May 29, 2015, he through the state House of Assembly enacted new tax laws. The Governor said that the new revenue law introduced by his administration was done in the best interest of the people. The Governor, at a press conference, said the taxes were not intended to punish the people but to cushion the impact of the dwindling allocation accruing to the state from the federation account on the state. Explaining further, the Governor pointed out that with an improved internal revenue base the government would be able to execute projects that would transform the state and better the lots of the citizenry. Consequently, there has been an increasing taxation of businesses including the small-scale enterprises and the informal sector. Of more interest in Ebonyi, is the consolidation of all taxes collectable in the state including that of the local governments into a Treasury Singular Account (TSA) controlled by the State Government. The Ebonyi State House of Assembly had to pass into law that revenues generated by all the local governments in the state will be going into the joint account which the state government has with the local governments and that local governments have no power to execute any contract again except jointly done with the state government (Jimatex, 2015). In an interactive session I had with a member of the State House of Assembly, Humphrey Nwauruku, representing Ikwo South state assembly, he put forward that the TSA was conceived in other to avoid financial wastages and leakages in the Local Governments and to enhance the state’s overall strategic development. Thus, this forms the bedrock of state taxation of motorcycle transport business in Ebonyi State, which was not formally taxed. Table 2 shows the table of taxes collectable by Ebonyi State government among others.

Taxes Payable in Ebonyi State.

Source. Ebonyi State Board of Internal Revenue Headquarters, Abakaliki.

The sources of Ebonyi States internally generated revenues are varied as can be seen in Table 3.

Sources of Ebonyi State Internally Generated Revenue.

Source. 2017 Budget of Ebonyi State Government as presented by the governor to the State House of Assembly.

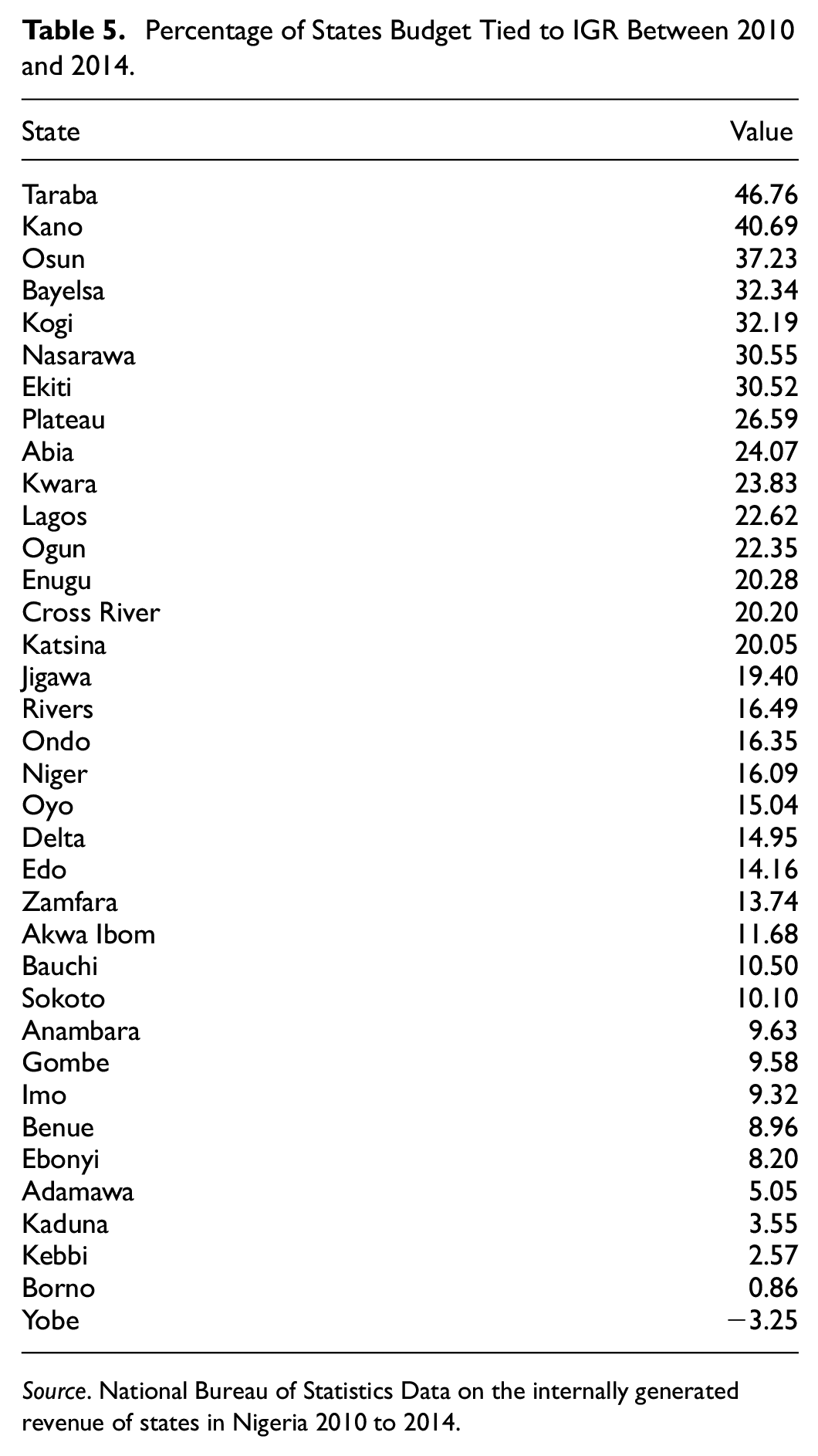

It important to point out at this juncture that the internally generated revenue of Ebonyi State has always been low and had been stagnating over the years compared to most other states in Nigeria. It ranked 31st out of the 36 states of the federation, and coming only before the five states of Adamawa, Kaduna, Kebbi, Borno, and Yobe. Meanwhile, it should be noted that these states are mainly the states being ravaged by the scourge of insurgency of Boko Haram and Fulani Herdsmen over the years in Nigeria, thus the extractive powers of the government in these states may have been limited. Moreover, security strategic interest was of more germane to the states than IGR strategic interest. In some of these states FEWSNET (June 11, 2015, p. 6) had this to say: Though major markets continue to operate, they function at reduced levels. Demand has decreased, production is below average, and trade routes are disrupted. Semi urban and rural markets are more negatively impacted by the crisis and operate at still lower levels. Demand is low due to decreased purchasing power among people who have not fled affected areas. Decreased economic activity in the region is also reducing activity on markets in areas not directly affected by the conflict. Staple food prices are high, particularly in Borno state. Market stocks were generally below average in May 2015 on markets monitored in Yobe, Adamawa and Borno state, which is a seasonal phenomenon, though stocks were relatively higher on markets less affected by the crisis. This is due to a combination of successive poor harvests, high transaction costs and trader fears.

But Ebonyi State which has experienced relative peace within this period is at the lower wrung of the ladder of IGR. Table 4 is illustrative of the average growth of IGR across states between 2011 and 2014.

Average IGR Growth Across States, 2011 to 2014.

Source. Computation based on data from National Bureau of Statistics, 2011 to 2014.

From Table 4, it could be seen that the internally generated revenue of Ebonyi State stagnated over the period in three years before 2015. This goes to show that within the period between 2011 and 2014 there were no significant improvement on the internally generated revenue of the state.

To buttress the point further, between the period 2010 and 2014, Ebonyi State government always hinged its budgetary proposal on the 8.20% of internally generated revenue (IGR) as can be gleaned from Table 5, which shows the percentage of states budget tied to IGR of the states:

Percentage of States Budget Tied to IGR Between 2010 and 2014.

Source. National Bureau of Statistics Data on the internally generated revenue of states in Nigeria 2010 to 2014.

We now turn to the revenues accruable to Ebonyi State Government from the motorcycle transport business operators. This is with a view to understanding if this business activity has improved on the internally generated revenue of the state within the period under study.

Tax Revenues From Motorcycle Transport Business Operators in Ebonyi State

The taxation of the motorcycle transport business in Ebonyi State was supposed to follow a presumptive tax system. Here, the tax authorities assess a taxpayer on the basis of perceived income. That is in the opinion of the tax authorities, what is the quantum of income the taxpayer would have made in the relevant period? Deloitte (n.d.). However, some of the findings from a focused group discussions (FGDs) held with some of the operators on June 17, 2020 revealed that the state government initially arbitrarily levied the operators the sum of N40,000 yearly as road tax without due recourse to earnings of the operators and ability to pay. Thus, the operators protested against it through their union to the state government. Consequently, the Governor of the state dissolved the Executives of the Union on September 12, 2015 and appointed a Caretaker Committee to head the Union. These were the people that negotiated the commercial motorcycle road tax with the government. Moreover, it was revealed by the focused group discussions that, there were no wide consultations and constructive engagement between the actual motorcycle transport business operators in the state by neither the government nor the imposed caretaker committee before arriving at a tax rate and its full implementations through the force strategy. However, in the course of negotiation and renegotiations with the government, as reported by the Motorcycle Transport Union Caretaker Committee Chairman in the state in an interview he granted alongside his co-members on May 25, 2019, due to high tax resistance, evasion, and avoidance among the operators of the business activity, an agreement was reached with the state government that the motorcycle transport business operators pay the sum of one hundred naira (N100) daily to the government through the motorcycle transport business union caretaker committees revenue collectors, with a caveat that all the operators must pay the said sum on all the days of the week, except Saturdays and Sundays which is declared as tax holidays for the operators. This will then be transmitted to the state’s Board of Internal Revenue through the Caretaker Committee. The Chairman of the Caretaker Committee of the union posited that, the essence of the piecemeal payment of the tax was to ensure ease of payment and convenience to the operators of the business activity. He pointed out that asking the operators to pay a lump sum of N40,000 to the government may be problematic and difficult, hence the split. In a separate interview with the immediate ex-chairman of the Motorcycle Transport Union before the imposition of the caretaker committee in the State, on June 4, 2019 he declared that the motorcycle transport business operators are compulsorily demanded to pay their fees whether they operated for each day or not. Hence, the revenue collection officers are meant to demand for the receipt of payment for a previous day before collecting for a particular day. Moreover, he pointed out that it is demanded that any motorcycle transport business operator that whishes to quit the business were required to report to the Union so that his name will be delisted from the list of operators.

Nonetheless, from the findings of the study, there are indications that the taxation of the motorcycle transport business has contributed, but has not improved on the internally generated revenue of Ebonyi State within the period under study. The state targeted to generate the sum of N13,964,887,074.00 and N10,000,000,000.00 as internally generated revenue in 2018 and 2019 but was able to generate N5,263,080,008.59 and 6,500,826,208.08 respectively within the period (Ebonyi State Approved Budget, 2020). However, of the amount that was generated, the motorcycle transport business contributed N220,852,900 and N237,117,700 between these periods. Within the period of this study, the motorcycle transport business contributed a total sum of N1,123,734,830 as IGR to the state (Ebonyi State Board of Internal Revenue Financial Records, 2022). Conversely, between the periods of 2010 and 2014 when the new tax regime has not been implemented, the percentage of the state’s budget tied to IGR stood at 8.20% as can be gleaned from Table 4. However, with the introduction of the new tax regime from the year 2015, where the motorcycle transport business was captured by the state in its tax net, the percentage of budget tied to the IGR came down to 6.70% throughout the periods of the years 2015 and 2018. One would have expected a rise in the percentage of the state’s budget tied to the IGR to increase given number of new articles added and captured in the tax net of the state, especially the commercial motorcycle road tax. Table 6 below is illustrative.

The Expected Sources of Revenue for 2018 Fiscal Year.

Source. An address by his Excellency, Engr. Dr. David Nweze Umahi, Executive Governor of Ebonyi State, on the occasion of the presentation of the 2018 budget of Ebonyi State government to the Ebonyi State House of Assembly on the 22nd day of December 2017.

With the massive taxation of businesses in the state between these periods, one would have expected that the percentage of the budget tied to the IGR would have increased, but that has not been. The state still relies heavily on federally collectable revenue and financial borrowings to finance its capital projects. The motorcycle transport business tax as a component of the IGR of the state has not been well harnessed. There seems to be a high rate of tax evasion/avoidance and underhand dealings in tax payments among the operators of the business activity as well as in the collection and remittance by the collecting and tax administration authority on this aspect of business activity. This may also be true of other source of IGR of the state. Below are the tabular presentations of the monthly remitted tax from the motorcycle transport business to Ebonyi State government within the period under study (Table 7).

Record of Revenues That Accrued to the State From the Motorcycle Transport Business Operators from the Month of October 2015 to December 2021.

Note. “NA” in this study indicates that the data for the month is not applicable. This is because the new tax regime came into effect from June 2015. However, from the time of negotiation by the Motorcycle Transport Union with the government and the time of full implementation of the new tax regime started in October 2015.

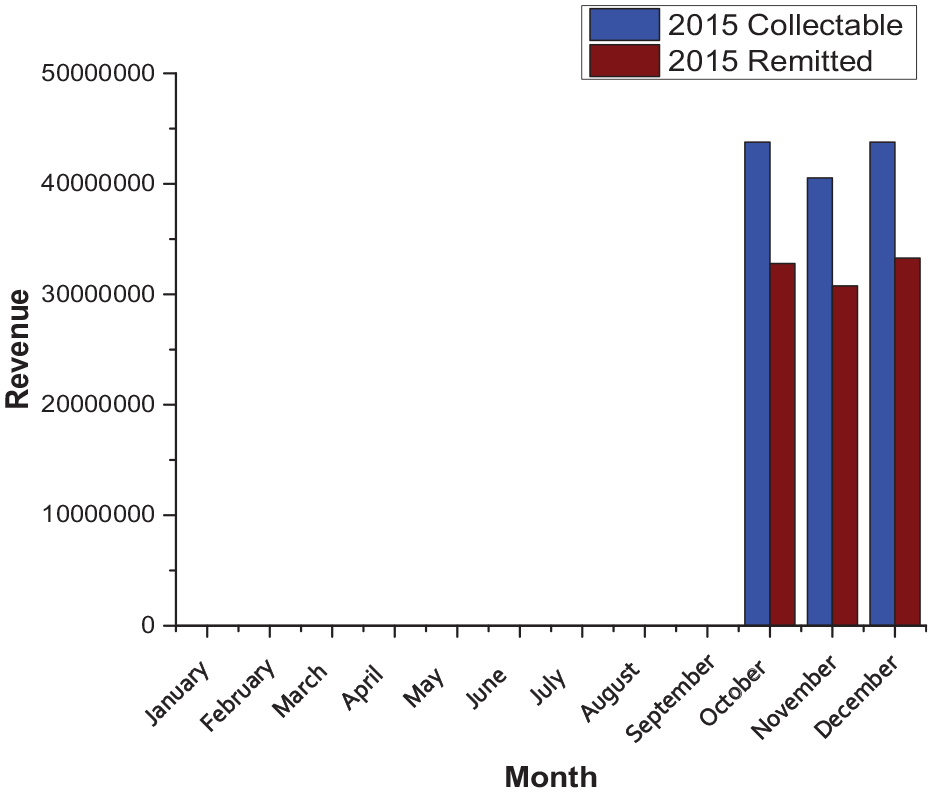

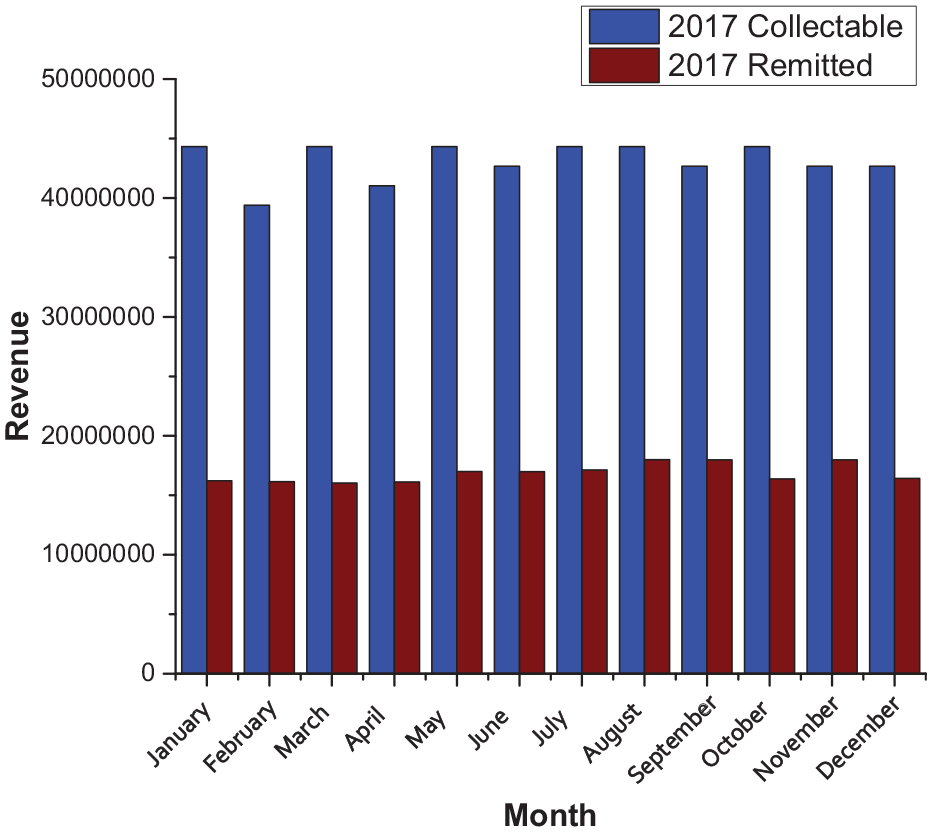

To indicate inefficiency and shortfall in the revenue yield of the state from the motorcycle transport business, the bar charts below on Figures 1 to 7 show the amount of taxable money that ought to have been collected and remitted by the revenue collection officers from the motorcycle transport business for each month of the year and the actual amount collected/remitted. The expected revenue was calculated using the population of the motorcycle transport business operators for each year which is showcased below.

Collectable revenue versus remitted revenue (October–December) for the year 2015.

Collectable revenue versus remitted revenue (January–December) for the year 2016.

Collectable revenue versus remitted revenue (January–December) for the year 2017.

Collectable revenue versus remitted revenue (January–December) for the year 2018.

Collectable revenue versus remitted revenue (January–December) for the year 2019.

Collectable revenue versus remitted revenue (January–December) for the year 2020.

Collectable revenue versus remitted revenue (January–December) for the year 2021.

Table 8 indicates that the percentage of motorcycle transport business operators grew by 0.76% from 2015 to 2016 and 0.47% between 2016 and 2017 while that of 2017 and 2018 was 0.64%. Moreover, there was 1.30%, 0.11%, and 4.57% increase between 2018/2019, 2019/2020, and 2020 and 2021 respectively. Hence, the bar charts below depicts that as the population of the motorcycle transport business operators increased in Ebonyi State, there is no corresponding increase in revenue collection and remittance from the motorcycle transport business operators. This shows that all the due collectable taxes from the motorcycle transport business operators are not collected or remitted. This could mean that most of the operators of the business activity do not pay their due taxes contrary to the popular opinion among the motorcycle transport business operators in response to the question we posed to them during a focused group discussions, “Have you been compliant with the payment of the government fees since your inception of this business?” of which all of them indicated “yes” as their preferred answers or that there might be underhand dealings in tax collection and remittances by agents responsible for the collection and remittance of taxes for/to the state government respectively.

Population of Registered Motorcycle Transport Business Operators for the Years 2015 to 2021.

Source. Compiled by the researcher as supplied by the chairmen of the motorcycle transport business operators in each of the thirteen (13) Local Government Areas of Ebonyi State (2022).

In the bar charts below, the blue bar represents collectable taxes from the motorcycle transport business operators while the red bar represents remitted taxes to the state government.

Meanwhile to buttress our point further, Table 9 shows the revenue gains and losses by Ebonyi State government from the taxes levied on the motorcycle transport business operators between 2015 and 2021.

Monthly Revenue Gain and Loss in Percentage for the Years 2015 to 2021.

Source. Authors compilation.

The findings from the tables shows that in 2015 when the enforcement of the new tax regime commenced full implementation, that the state were able to collect 75.6% of the total collectable taxes from the motorcycle transport business in the state, making a loss of 24.4%. However, in 2016 the state lost 52.1% as against 47.9% in motorcycle road tax. 2017 and 2018 were 60.9% loss and 39.1% gain and 57.0% loss and 43.0% gain respectively. What these mean is that the government needs to improve on its tax collection and remittance strategy from the businesses activity if it hopes to improve on its IGR and also ensuring voluntary tax compliance from the operators of the business activity.

Voluntary Tax Compliant Among Motorcycle Transport Business Operators in Ebonyi State

The introduction of the new tax regime and the incorporation of the motorcycle transport business into the tax net in Ebonyi State, brought arguments by the motorcycle transport business operators union that the restriction of motorcycle transport business operators outside the highways and double carriage ways has adversely affected their income and therefore may affect their tax compliance level. The argument was that the government should remove the ban on the motorcycle transport business operators from plying the highways and double carriage ways—which to them is the major source of income for their business activity—so as to improve on their daily earnings/incomes and consequently enhance their tax payment voluntarily (ex-Chairman, Ebonyi State Motorcycle Transport Union 2018)

However, our findings from the revenue accruable to the state from the motorcycle transport business indicates a relatively low tax yield resulting either from high level of tax evasion/avoidance by the motorcycle transport business operators, even with the relaxation of the ban from operating on the highways and the double carriage ways or sleaze by the revenue collection agents or both. As can be seen from Table 9, in 2015 the state realized N96.81 million as against N128.06 million that would have accrued to the state if all the motorcycle transport business tax were collected and remitted. The state recorded a loss of N188.39 million in revenues, indicating a tax gain of 75.6% and a loss of 24.4% of accruable tax. In 2016, 2017, and 2018 the state realized N248.59, N202.37, and N148.31million respectively with a total loss of N782.39 million within these periods. In 2019, 2020, and 2021 the state realized the total sum of N575,953,900 as against a total loss of N162,768,200. It was only in the year 2015 that the states relative revenue percentage gain outstripped its loss at 75.6% gain and 24.4% loss as evidenced in Table 9. Meanwhile, the relative high percentage gain in 2015 had been attributed to the perception of the motorcycle transport business operators that the relaxation of the enforcement on the ban of the operators from operating on the high ways and double carriage ways will generally improve on their income. However, this was not to be as the introduction of tricycle as a means of commuter transport had intervened to cut down on their earnings and income. This assertion was warranted going by information the researcher got from focused group discussion (FGD) with the 30 motorcycle transport business operators drawn from across the state. They pointed out that the introduction of tricycle has grossly affected their daily income, because tricycle operators have virtually taken over and are in competition with the motorcycle transport business operators on the transport routs that were previously the exclusive preserve of the motorcycle transport business operators.

Meanwhile, the relative low patronage and income arising from the introduction of tricycle that most of the operators experience seem to be manifesting in tax evasion/avoidance and the consequent low revenue to the state. This could be inferred from the fact that, some of the operators of the business activity were of the view that the government should not tax the business activity. In an in-depth interview with some of the operators of the business activity, they pointed out that hazards involved in the business and the low income yield it generates to the operators of whom are majorly married with children should make the state to rethink its tax policy toward the operators. From the information generated through our focused group discussions, 23 of the 30 member group indicated that they were married; hence, to some of operators of the business activity, the government should exclude them from the tax net, given the responsibility they shoulder as family persons with the corresponding poverty among the people in the state. Moreover, they were of the view that the government should manage the resources it mobilizes from the federation account without necessarily taxing the operators of motorcycle transport business who to them brave all odds to eke out a living. The implication of the above is that the operators of the business activity do not see any benefit in voluntarily complying with state tax. Myers (n.d.) had pointed out that voluntary tax compliance works best when people see the benefit to be gained from complying.

Moreover, many of the operators are hired operators as indicated by the (responses from a focused group discussions) with some of the operators of the business activity), thus, their take home pay may not be such as to sustain their family and other dependents after all expenses are deducted, let alone being willing to comply with tax voluntarily (FGDs, 2020). The ability and willingness of people to pay tax, some of the time depends on the income of such people in their business and livelihood sustainability of the business activity to the general welfare of the individuals concerned. More importantly in enhancing tax administration for collective good is unanimity in tax administration between the state government, the tax administration agents and the motorcycle transport business operators, where each makes a trade off for collective and individual gains.

Conclusion and Recommendations

The findings of the study are that the taxation of motorcycle transport business by Ebonyi State government has contributed but has not improved on its internally generated revenue. This is because the study revealed that there is a divorce between the collectable revenue from the business activity and the actual amount the state generates from them. Hence, the government needs to do more, to enhance voluntary tax compliance from the business activity. In addition, one would have expected that with the incorporation of motorcycle transport business into Ebonyi State tax net, that the proportion of the state’s budget tied to internally generated revenue would have increased, but that was not the case. Before the incorporation of motorcycle transport business into the tax net of Ebonyi State government, the proportion of the state’s budget tied to internally generated revenue stood at 8.20%, however, with the incorporation of the business activity into the tax net of the state government, the proportion of the state’s budget tied to internally generated revenue decreased to 6.70%, indicating that there has been a low revenue yield from the business activity and other informal sector business activities in the state within these periods. On the strength of the findings stated above, the study hereby recommends as follows:

There is the need for unanimity of purpose in tax administration between the state, the tax administrators, the tax collection agents, and the operators of the motorcycle transport business. This can come in the form of political exchange which benefits both the public, serves as incentive to the tax collection agents to exercise due diligence in the discharge of their duties as well as a morale booster to the operators of the motorcycle transport business operators for voluntary tax compliance.

As a corollary to the above, the state to exact voluntary tax compliance among the business activity and shore up its revenue, the government should implement a social welfare package specifically designed for the operators of the business activity. Such package can come in the form of accident insurance; to assist those whose are hospitalized due to motorcycle accident. Also, an easy source of loan to help operators replace damaged parts occasioned by tears and wears among others should be made available to the operators; this will serve as tax incentive to enhance compliance. As Myers (n.d.) had pointed out that voluntary tax compliance works best when people see the benefit to be gained from complying.

However, these packages should be given specifically to only those of them who are up to date in their tax payment.

The government should make effort to have a comprehensive and up to date data of all the operators of the business activity in the State. This will enable them to assess the tax compliance level of the business operators in the state.

The government must make it compulsory that any new entrants as well as exits into and from the business activity must be reported to the relevant government agency for proper documentation.

Of utmost importance is that as the government employs this carrot approach to enhance tax compliance, it must also employ the stick to coerce the recalcitrant members who evade tax from gaining from the benefit of tax compliance. Thus, there should be the application of power and trust as enunciated by Kirchler et al. (2008), in the administration of tax on the motorcycle transport business operators in Ebonyi State.

As the government is ensuring that all the operators pay their taxes as at when due, they should also put up measures to ensure that all the collectable revenue from the motorcycle transport business operators are collected and remitted by the officers or agencies charged with such.

Finally, the study encourages the collective organizing among the operators of the business activity as Ezeibe et al. (2017) had noted that collective organizing can present opportunities for a new form of engagement between the state and the informal economy with the aim of influencing urban governance process, policy, and outcomes through the democratic process when there is cohesion, transparency, accountability within the organized group.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.