Abstract

Imperfect external capital market and internal soft budget constraints are important reasons for the issue of enterprise financing constraints. This paper studies the impact of financing constraints and influencing factors of financing constraints in municipal infrastructure investment and construction for local governments by using the panel data from 2003 to 2018 in China. The results show that, first, there are great financing constraints in municipal infrastructure investment and construction for local government in China. Second, the increase of self-financing capacity and external financing capacity can reduce the level and uncertainty of financing constraints, thus improving the efficiency of municipal infrastructure investment and construction. Third, the expansion of the city scale may reduce the uncertainty of financing constraints, but improve the level of financing constraints thus reducing the efficiency of municipal infrastructure investment and construction.

Keywords

Introduction

The investment and construction of municipal infrastructure is the material foundation of urbanization development and an important means for local governments to fulfill government functions in China. Since the 1990s, China has entered an unprecedented stage of rapid and comprehensive urbanization in human history, and the demand for municipal infrastructure has increased significantly. The investment and construction of municipal infrastructure that involves several generations is a long-term development issue, and the current financial resources are unable to support the investment and construction of municipal infrastructure. The cost of municipal infrastructure investment and construction should be shared between generations. Due to the imperfect capital market in China, financing constraints have become an important constraint factor in the investment and construction of municipal infrastructure. Substantial empirical papers illustrate the existence of financing constraints in the investment and construction of municipal infrastructure in China (Ji et al., 2015; S. Liu et al., 2020; L. Zhang et al., 2018). The explanations mainly focus on the adverse selection problem that arises from financing constraints when firm insiders have better information than outsiders about the value of their firm (Myers & Majluf, 1984). An important implication of adverse selection is that firms with positive-net-present-value investment opportunities will forgo profitable projects to avoid the excessive cost of external financing. Since the 1990s, China has started market-oriented reform in the field of municipal infrastructure, which includes gradually liberalizing access restrictions and using local government financing platforms to broaden the sources of funds for investment and construction. These specific reforms have promoted the investment and construction of municipal infrastructure. However, China’s local governments have accumulated huge amounts of debt due to the investment and construction of municipal infrastructure. As of the end of 2018, the balance of local government debt in China reached 18.4 trillion yuan, an increase of 172.0% compared to 2010 (Fan & Mo, 2014; C. Liu et al., 2020). Especially, the majority of local government debt is short-term bank loans in China. The level and uncertainty of financing constraints which are easily influenced by macroeconomic policies and other factors, may lead to unsustainable sources of funding in the investment and construction of municipal infrastructure, and then transform into the risk of local government debt default. The issue of financing constraints in the investment and construction of municipal infrastructure in China has attracted widespread attention. At present, the characteristics of China’s centralized political and decentralized economy determine that local governments face both exogenous financing constraints and endogenous financing constraints. The exogenous financing constraint is mainly caused by the unsoundness of the external capital market, while the endogenous financing constraint is mainly caused by the soft budget constraint of local governments. According to Dewatripont and Maskin (1995), unprofitable projects may nevertheless be financed even when shown to be low-quality if sunk costs have already been incurred. It seems pertinent to “soft budget constraint” problems in centralized economies. This will encourage local governments to invest excessively and expand the degree of financing constraints. Currently, there is far from consensus among the theoretical, policy, and practical communities on the core issues of financing constraints in the investment and construction of municipal infrastructure in China.

This paper aims to quantitatively measure the impact of financing constraints on the efficiency of the investment and construction of municipal infrastructure in China, and then investigate the influencing factors of the level and uncertainty of financing constraints. The investigation is important not only for intellectual curiosity but also for policy purposes. The contributions of the paper are reflected as follows: First, this paper quantitatively measures the impact of financing constraints on the efficiency of municipal infrastructure investment and construction in China by the heterogeneous one-tier stochastic frontier model. Second, this paper investigates the influencing factors of the level and uncertainty of financing constraints. Third, this paper studies soft budget constraints which will cause endogenous financing constraints through heterogeneity analysis. This effort is a marginal improvement over existing research.

Literature Review

The Role of Local Government Debt

Debt financing has been an important financing channel for easing financing constraints for local governments in China. However, in recent years, China’s local governments have also generated and accumulated huge local government debts. Some local governments mainly rely on borrowing new bonds to repay old debts. From a liquidity perspective, the level and uncertainty of financing constraints can transform into the risk of local government debt default. The issue of local government debt in China has also attracted much attention from academics in recent years. There are still some differences in the role of local government debt. Debt financing has a positive effect on local economic growth (Guo et al., 2020; Hu & Gu, 2016). Debt financing is detrimental to regional economic growth (Chen & Chen, 2015; C. Liu et al., 2020). Enterprises are the main force of local economic development. The more financial assets especially short-term financial assets is allocated by the enterprises after credit expansion, and a lack of subjective willingness for innovation is more likely to be the reason why credit expansion does not bring about new firms’ innovation(Wen et al., 2024). The impact of debt financing on regional economic growth has a nonlinear pattern (He & Wang, 2020; J. Mao & Huang, 2018).

The Reasons of Financing Constraints

The reasons for financing constraints mainly focus on the adverse selection problems caused by asymmetric information (Carpenter & Guariglia, 2008; Myers & Majluf, 1984). A firm’s financial structure is irrelevant to investment because external funds provide a perfect substitute for internal capital. If internal and external capital are not perfect substitutes, a firm’s investment may depend on financial factors, such as the availability of internal finance, access to new debt or equity finance, or the functioning of particular credit markets (Fazzari et al., 1988; Fazzari & Petersen, 1993; Himmelberg & Petersen, 1994; Whited, 1992). The reduction of local government financial resources and the expansion of expenditures are the main reasons for financing constraints in China (Jiang & Hu, 2016; Pang & Chen, 2015). Another reason for financing constraints mainly focuses on “soft budget constraint” problems which will cause excessive investment and widen the funding gap. The pursuit of economic growth goals for local government is the main motivation for the excessive investment because local governments face soft budget constraints in China (Guo et al., 2016; S. Yang & Li, 2013). The lack of strict relevant supporting institutional arrangements is the inability to effectively control the excessive investment of local governments as well as the expansion of financing constraints (Diao, 2017; F. Wang et al., 2017). Economic policy uncertainty can enhance financing constraints, but the level of social trust can alleviate the adverse effects of economic policy uncertainty on financing constraints (Su & Gu, 2024).

The Ways to Alleviate Financing Constraints

The third focus is to study the ways to alleviate financing constraints of local governments. Local government officials can influence bank executives and bank credit decisions through activities such as policy-making, inspections, meetings, and interviews to obtain more financial support (C. Cao et al., 2014; L. Zhang, 2020). The actual control of local governments over urban commercial banks also gives local governments to influence the operations of urban commercial banks, which leads to local financing platform companies obtaining bank loans with lower interest rates (Qian et al., 2011; D. Zhang & Li, 2012). The growth of land transfer revenue is a driving factor for the continuous expansion of the investment and construction of municipal infrastructure (W. Mao & Lu, 2020; L. Zhang et al., 2018). The LPR reform has significantly increased the scale of short-term and long-term loans of enterprises and alleviated the financing constraints of enterprises, by alleviating and the asymmetric information of banks and enterprises (Xu & Liu, 2024).

These research results have laid a good foundation for an in-depth study of the impact of financing constraints on the efficiency of investment and construction in the municipal infrastructure. To shed additional light on the relationship between cash flow and investment expenditure, we intend to use the heterogeneous one-tier stochastic frontier model to quantitatively measure the impact of financing constraints on the efficiency of the investment and construction of municipal infrastructure, and then investigate the influencing factors of the level and uncertainty for financing constraints.

Research Hypothesis

The Impact of External Financing

Since the implementation of the tax-sharing reform in China in 1994, local governments have actively sought external financing to bridge the fiscal gap due to the serious mismatch between their financial and administrative powers. According to Ji et al. (2015), the fiscal gap caused by the mismatch between matter and financial has increased financing constraints of local governments, while financial development has alleviated financing constraints. According to Zhu and Wang (2018), the market constraint generated by the self-repayment pilot of local government bonds conducted in 2014 significantly reduced the risk premium of municipal bonds. Further tests show that the effect of the self-repayment pilot reduces the risk premium of municipal bonds more significantly in regions with high fiscal transparency and fiscal balance, but not in regions with low fiscal transparency and fiscal imbalance. According to G. Cao et al. (2020), fiscal pressures lead to the establishment of local government financing platforms, and local governments are more inclined to establish financing platforms to alleviate financing constraints when local governments face more intense interregional competition and lower initial fiscal endowments.

The Impact of Self-Financing

Local governments’ self-financing mainly includes public revenue, land concession income, and state capital operation income, which are the ultimate sources of funds for municipal infrastructure investment and construction. According to L. Wang and Chen (2015), the influence of the government’s implicit guarantee on interest rates depends on the economic development of the issuer. And the bond interest rate is not affected by the implicit government guarantee when the regional economic development is unsatisfactory, on the contrary, the implicit government guarantee can reduce the bond interest rate. According to Zhong et al. (2016), the bond guaranteed by rating agencies and local governments’ public revenues contributes to the improvement of bond ratings but has no significant effect on the reduction of bond credit spreads. According to J. Yang et al. (2018), the changes in land value and land mortgage value have a significant impact on the growth of municipal infrastructure investment bonds, and local government debt risk should focus on the impact of land value fluctuations on local government debt. It can be seen that self-financing has an important impact on local government municipal infrastructure investment and construction through the collateral channel and the direct supply channel of funds.

The Impact of Urban Scale

The economy of scale brought by the expansion of urban scale is an important source of modern economic growth. According to Lu (2017), cities can achieve human capital accumulation, increase the return on human capital, and achieve regional economic growth better when the free movement of labor is easier. According to Chang and Lu (2017a), the new city with higher density, close to the main urban, will gradually reduce local government indebtedness during the period of the construction and completion of new cities in small and medium-sized cities with population outflows. While in large cities with population inflows, the new city with high density will increase the financial burden of local governments in the early stage, but the effect of the population agglomeration will gradually reduce the local government debt ratio. According to Chang and Lu (2017b), effective urban construction must be based on the free movement of labor, so that land demand matches the actual needs of population and industrial development.

The Impact of Soft Budget Constraint

China’s unique pattern of economic decentralization and political centralization with the central government’s underwriting responsibility for local government behavior, and the promotion tournament system based on economic growth, will cause the soft budget constraint. The soft budget constraint will encourage local governments to invest excessively and cause financing constraints. According to Miao and Fu (2015), there is a positive correlation between soft budget constraint and extra-routine debt growth under the condition of local government official promotion incentives based on economic growth. According to Y. Wang et al. (2016), the default risk of local government debt is not reflected in the yield spreads of municipal investment bonds in China, which reflects the existence of a soft budget constraint for local government. According to Peng and Lu (2019), the investment and construction of new cities have become the main driving force for short-term economic growth in small and medium-sized cities with low labor productivity, and fewer opportunities for economic development, but with adequate land supply and low land prices.

Hypothesis 1, Hypothesis 2, and Hypothesis 3 support the pecking order hypothesis (Myers & Majluf, 1984). The pecking order hypothesis mainly focuses on the adverse selection problem that arises from financing constraints when firm insiders have better information than outsiders about the value of their firm. The policy implication of the pecking order hypothesis is to improve the external capital market.

Hypothesis 4 supports the free cash flow hypothesis (Jensen, 1986), focuses on the agency issue. The free cash flow hypothesis argues that managers can increase their wealth at the expense of shareholders by investing a firm’s free cash flow in unprofitable investment opportunities rather than paying out those funds in the form of dividends, debt-financed share repurchases, and the like. The policy implication of the free cash flow hypothesis is to improve internal corporate governance.

Research Design

Empirical Model

The influence of investment opportunity on some firms’ investment expenditure is described by the Q models of investment (Fazzari et al., 1988; Vogt, 1994). Under the consideration of financing constraints, we will use the extended Q models of investment determined by equations (1) and (2) to describe the expenditure of municipal infrastructure investment and construction of local government.

where i and t represent different cities and time series of years, respectively. The dependent variable lninvt is the natural logarithm of the investment and construction expenditure of municipal infrastructure per unit of land. The independent variable lnFQ reflects the investment opportunity, which is the natural logarithm of FQ. According to Kumbhakar and Christopher (2009), the variable

Where

Variables and Their Definition.

It should be noted that equations (1), (2), and (3) constitute the heterogeneous one-tier stochastic frontier model. This setting makes the subsequent analysis very flexible in this paper. First, we can simultaneously analyze the effects of exogenous variables on the level and uncertainty of financing constraints. Second, by using this model, we can quantitatively analyze the loss of investment and construction efficiency due to financing constraints, which is impossible based on the linear regression analysis previously.

Efficiency Measurement

The heterogeneous one-tier stochastic frontier model consisting of equations (1), (2), and (3) can be estimated by using the maximum likelihood method. This paper analyzes the impact of financing constraints on local government municipal infrastructure investment and construction behavior from two aspects. First, the likelihood ratio test is used for qualitative analysis. The original hypothesis is that financing constraint is non-existent, and the corresponding alternative hypothesis is that financing constraint is existent. The likelihood ratio statistic asymptotically obeys the chi-square distribution. At the same time, we can also use the likelihood ratio test to examine whether the heterogeneity of the model is set correctly. Second, the index of investment and construction efficiency, which represents the deviation of the actual investment expenditure compared to the target investment expenditure for local governments, is constructed for quantitative analysis. It is defined as

The value of

Data Sources

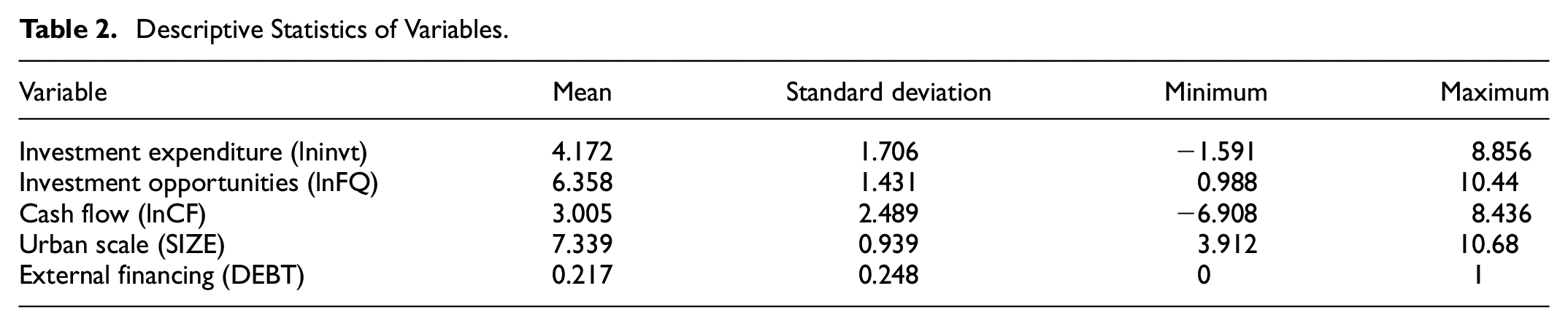

This paper matches the collated panel data of municipal infrastructure investment and construction expenditures, urban development opportunities, urban scale, external financing, and self-financing for cities to test the theoretical hypotheses. From 2003 to 2018, some pilot reforms have been carried out in the capital funding for municipal infrastructure investment and construction of local governments in China. The pilot reforms have the characteristics of quasi-natural experiments, which can reduce endogenous problems in the estimation of parameters. The paper uses the panel data for 283 municipal districts of cities above the prefecture level in China from 2003 to 2018. The original data for each variable are mainly from the China Statistical Yearbook (2004–2019), China Statistical Yearbook of Urban Construction (2004–2019), and China Urban Statistical Yearbook (2004–2019), etc. Descriptive statistics of the main variables are shown in Table 2.

Descriptive Statistics of Variables.

Analysis of Empirical Results

The Results of Model Estimation

Table 3 summarizes the estimation results of model parameters under various settings. Model 1, which is the focus of discussion in this paper, does not impose any constraints on the parameters of the heterogeneous one-tier stochastic frontier model. Models 2 to 5 are obtained by imposing various constraints based on Model 1. Model 2 assumes that variables such as urban scale, external financing capacity, and internal financing capacity do not affect the uncertainty of financing constraints. Model 3 assumes that variables such as urban scale, external financing capacity, and internal financing capacity have no effect on the level of financing constraints, but have an effect on the uncertainty of financing constraints. Model 4 assumes that financing constraint obeys a heterogeneous half-normal distribution truncated at zero, but these variables such as urban scale, external financing capacity, and internal financing capacity affect the uncertainty of financing constraints. As a comparison, this paper also estimates the traditional Q model, Model 5 in Table 3.

Model Estimation Results.

Note. (1) The value of t is in square brackets; (2) LR1 and LR2 are the chi-square values obtained from the likelihood ratio tests of the corresponding models for model 5 and model 1, respectively.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

As can be seen from Table 3, the coefficient of the investment opportunity (LnFQ) is significantly positive at the 1% level for all models, and the annual time effect is also highly significant. These indicate, to some extent, that China’s municipal infrastructure investment and construction expenditure are influenced by investment opportunities (LnFQ), and financing constraints are influenced by macroeconomic policies.

The results of the likelihood ratio test in Table 3 show that the heterogeneous one-tier stochastic frontier model 1 is more effective, regardless of whether the original hypothesis of the likelihood ratio test is set to no financing constraints (matching LR1) or heterogeneous financing constraints (matching LR2). From the perspective of likelihood value, the heterogeneous one-tier stochastic frontier model 1 is more effective, because the Log likelihood value of model 1 is the largest among the five models. In particular, model 1 significantly outperforms model 5, which indicates that China’s municipal infrastructure investment and construction expenditures are significantly affected by the level and uncertainty of financing constraints. Therefore, the subsequent analysis in this paper will be based on the heterogeneous one-tier stochastic frontier model 1.

From the parameter estimation results of the heterogeneous one-tier stochastic frontier model 1 in Table 3, we can see that the coefficient of lnCF is significantly negative at the 1% level in the level of financing constraints equation and the uncertainty of financing constraints equation. These indicate that the increase of local government’s self-financing capacity can not only alleviate the level of financing constraints but also reduce the uncertainty of financing constraints, thus improving the efficiency of local government municipal infrastructure investment and construction, which is consistent with the expectation of hypothesis 2, because internal funds have a cost advantage over new debt or equity finance.

The coefficient of SIZE is significantly positive at the 1% level in the level of financing constraints equation, and the coefficient of SIZE is significantly negative at the 1% level in the uncertainty of financing constraints equation. These indicate that the increase of the urban scale will not alleviate the level of financing constraints for local government, but reduce the uncertainty of financing constraints for local government which is consistent with the expectation of hypothesis 3, because the impact of urban scale on municipal infrastructure investment and construction expenditure is significantly positive and the expansion of urban scale is conducive to more stable municipal infrastructure financing.

The coefficient of DEBT is significantly negative at the 1% level in the level of financing constraints equation and the uncertainty of the financing constraints equation. These indicate that the increase of external financing capacity can not only alleviate the level of financing constraints for local government but also reduce the uncertainty of financing constraints for local government, thus improving the efficiency of local government municipal infrastructure investment and construction, which is consistent with the expectation of hypothesis 1, because external funds provide a certain substitute for internal capital.

The Analysis of Efficiency Measurement

Figure 1 shows the frequency distribution of the efficiency index (IEI) is an obvious left bias, which indicates that the investment and construction of municipal infrastructure face relatively large financing constraints for local government in China. The mean of the efficiency index (IEI) for local government in China is 0.41. The efficiency index (IEI) for most local governments is concentrated between 0.3 and 0.5. This indicates that there is a large gap between the actual expenditure and their willingness on the investment and construction of municipal infrastructure for local governments in China. This gap may be large due to exogenous financing constraints caused by inadequate external capital markets and endogenous financing constraints caused by soft budget constraints of local governments.

Frequency distribution of the investment and construction efficiency index (IEI).

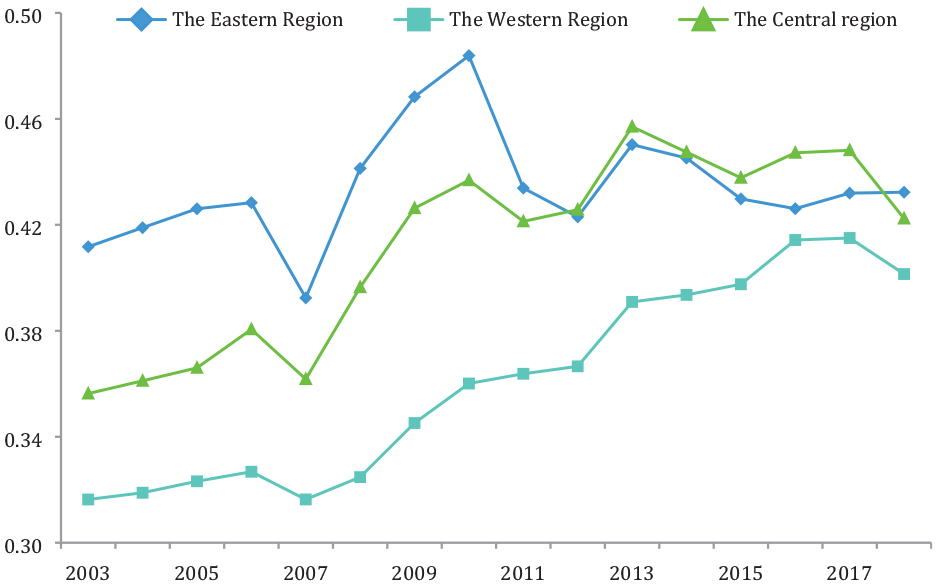

From Figure 2, the efficiency of investment and construction on municipal infrastructure for local government in China generally shows an upward trend from 2003 to 2018. However, we find that the efficiency of investment and construction on municipal infrastructure is the highest in the eastern region, the efficiency is the lowest in the western region, and the efficiency is between the eastern region and the western region in the central region. In other words, the eastern region which faces financing constraints on the investment and construction of municipal infrastructure is the least, the central region is the second, and the western region is the largest.

Investment and construction efficiency index of different regions.

The Heterogeneity Analysis

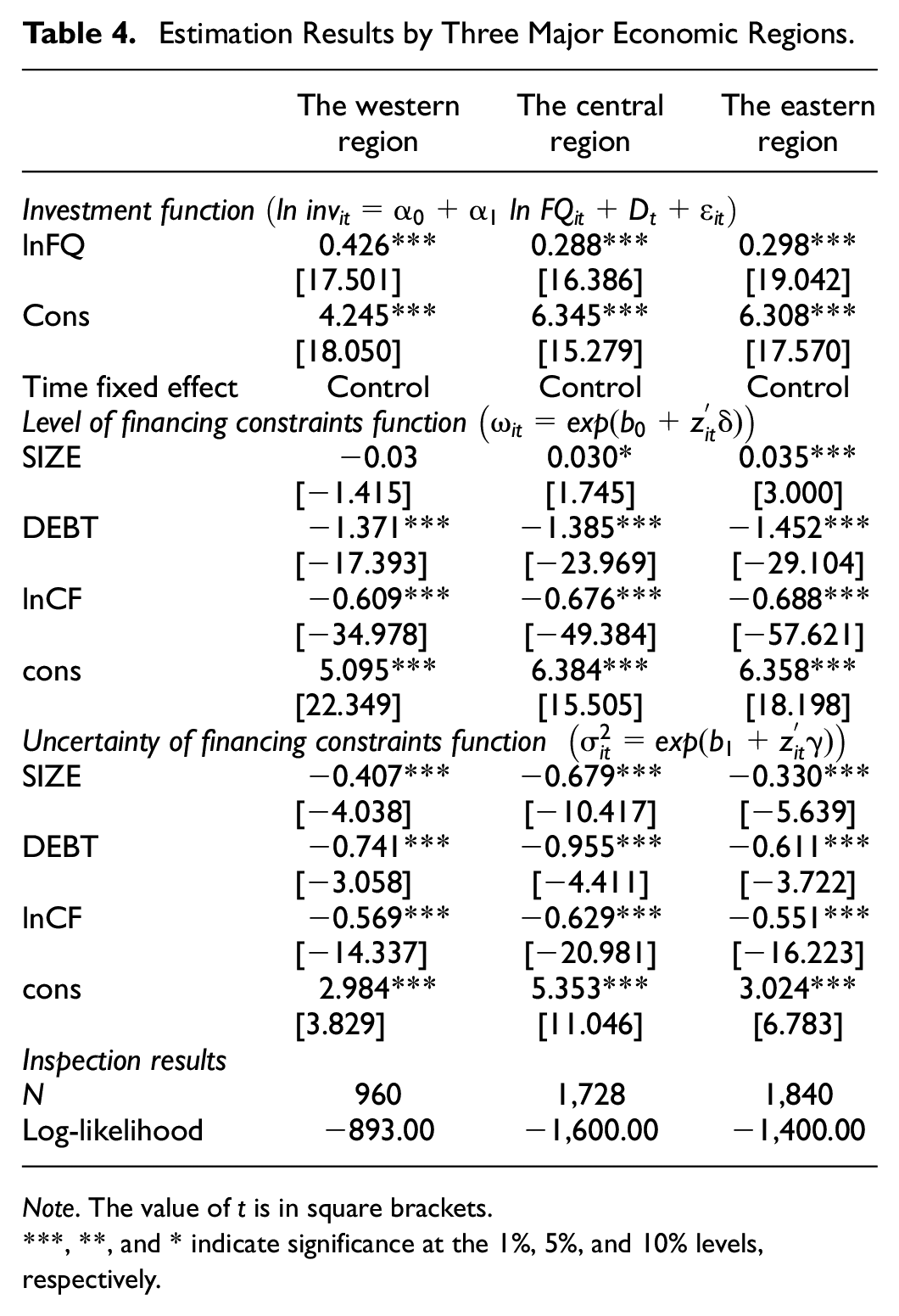

From the results above, there are significant differences in the efficiency of municipal infrastructure investment and construction for local government in China. For this reason, the heterogeneity one-tier stochastic frontier models which are made of equations (1), (2), and (3) are estimated by cities divided into three categories: the eastern region, the central region, and the western region. The results of model estimation are demonstrated in Table 4. The results in Table 4 show that there are significant differences in the municipal infrastructure investment and financing behavior of local governments in the eastern, central, and western regions.

Estimation Results by Three Major Economic Regions.

Note. The value of t is in square brackets.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

The coefficients of LnFQ in the eastern, central, and western regions are all significantly positive at the 1% level, but the coefficients of LnFQ in the western region are significantly larger than those in the eastern and central regions. This indicates that municipal infrastructure investment and construction expenditures in the eastern, central, and western regions are all affected by investment opportunities (LnFQ), but the same investment opportunities for local governments in the western region have greater municipal infrastructure investment and construction expenditures than those in the eastern and central regions. The investment and construction of municipal infrastructure are more likely to become the source of short-term economic growth when local governments in the western region face the reality of relatively slower economic development, which is consistent with the expectations of hypothesis 4.

The coefficient of SIZE is significantly positive at the 1% level for the eastern region, significantly positive at the 10% level for the central region, and insignificantly negative for the western region in the level of financing constraints equation. These indicate that the increase in the land area of local government municipal administrative areas increases the level of financing constraints on municipal infrastructure investment and construction for local governments in the eastern and central regions, but has little effect on local governments in the western region, which most likely stems from the combined effect of high land acquisition and demolition costs and insufficient population importation in the eastern and central cities.

In addition, the estimated results of annual effects, coefficients of lnCF and DEBT in the level of financing constraints equation and the uncertainty of financing constraints equation, and coefficients of SIZE in the uncertainty of financing constraints equation in Table 4 are consistent with the estimated results of model 1 in Table 3.

Conclusions and Policy Recommendations

Basic Conclusions

This paper studies the impact of financing constraints on the efficiency of municipal infrastructure investment and construction and the influencing factors of the level and uncertainty of the financing constraints for local governments. The main conclusions are as follows: First, local governments in China face large financing constraints which are mainly from the exogenous financing constraints caused by unsound external capital markets and the endogenous financing constraints caused by soft budget constraints of local governments in municipal infrastructure investment and construction. Second, the increase of self-financing capacity and external financing capacity of local governments in China can reduce the level and uncertainty of financing constraints of municipal infrastructure investment and construction, thus improving the efficiency of municipal infrastructure investment and construction. Third, the expansion of urban in China has reduced the uncertainty of financing constraints for local government in the municipal infrastructure investment and construction but has increased the level of financing constraints for local government in the municipal infrastructure investment and construction, thus reducing the efficiency of municipal infrastructure investment and construction.

Policy Recommendations

Local governments have played a crucial role in China’s economic development since the reform and opening up. However, as China’s social and economic development from the high-speed growth stage to the high-quality growth stage, the weaknesses, distortions, and potential risks contained in the high-speed growth stage have gradually emerged. Based on the above research conclusions, this paper puts forward the following suggestions for resolving the risk of local government debt default and improving the efficiency of municipal infrastructure investment and construction. First, the system of officials’ tenure and the urban development performance assessment should be optimized to guide officials to establish a correct view of performance and reduce the shortsightedness of measures. Second, the integrated development of industry and city should be strengthened. And then the construction land allocation of cities with better economic development and higher net population inflow should be increased. Correspondingly, the construction land allocation of cities with net population outflow should be reduced. Third, the debt default monitor such as the dynamic management of the asset-liability ratio of local government financing platform enterprises should be strengthened. Fourth, the financing platform company of local governments should transform into an entity enterprise, enhance the core business ability and market competitiveness, and supplement the municipal infrastructure investment and construction. Fifth, the fund channels of the municipal infrastructure investment and construction such as asset securitization, PPP model, and other new project financing models should be broadened.

Limitations

Although this paper has obtained some significant results through empirical investigation, it has some major shortcomings. First, the consideration of investment and construction efficiency losses caused by the other agency cost is inadequate, which will lead to overestimation of investment and construction efficiency losses caused by financing constraints of municipal infrastructure investment and construction for local governments in China. Second, the investigation on the impact of financing constraints and the influencing factors of financing constraints lacks the support of typical cases. In future studies, the soft budget constraint and other agency issue for local governments need further attention, and a typical city may be chosen to make some case studies. Third, some variables such as investment and construction expenditure and cash flow are measured using a current price level. In future studies, some variables such as financial variables can be measured using a constant price level as far as possible.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Humanity and Social Science Youth foundation of Ministry of Education of China (Grant No: 18YJC790131) and Zhejiang Public Welfare Technology Application Research Funding Project, China (Grant No. LGF22G010002).

Data Availability Statement

The (DATA TYPE) data used to support the findings of this study are available from the corresponding author upon request.