Abstract

Even though the determinants of sustainability reporting have been highly studied, the influence of Board Governance characteristics on sustainability reporting has mainly remained understudied in Africa, especially Nigeria, despite the overwhelming Business opportunities in the country. This study, therefore, investigates the influence of Board Governance on sustainability accounting and reporting, drawing insights from large businesses listed in Nigerian stock exchanges. Using a sample of 167 reports drawn from three sources—annual reports, sustainability reports, and website over the period 2015 to 2020, this study employs content analysis to quantify three layers of sustainability disclosure and fixed effects regression estimation model to predict the influence of Board governance variables on sustainability reporting quality. Our results indicate that Board governance characteristics such as Board capacity, board independence and Board Incentives are significant factors that affect sustainability reporting quality. The results further suggest that although the number of directors on the board is positively associated with the quality of sustainability reporting, CEO duality is insignificant and has a negative association with the quality of sustainability reporting. This study provides evidence that setting up long-term incentive-based compensation affects sustainability reporting positively in developing countries, such as Nigeria.

Plain language summary

This paper investigates the influence of Board Governance characteristics on sustainability accounting and reporting in a developing country using a sample of 167 reports drawn from three sources - annual reports, sustainability reports, and website over the period 2015 to 2020. The study employs content analysis to quantify three layers of sustainability disclosure and a fixed effects regression estimation model to predict the influence of Board governance variables on sustainability reporting quality. Our results indicate that Board governance characteristics such as Board capacity, board independence and Board Incentives are significant factors that affect sustainability reporting quality. The results further suggest that although the number of directors on the board is positively associated with the quality of sustainability reporting, CEO duality is insignificant and has a negative association with the quality of sustainability reporting. This study provides evidence that setting up long-term incentive-based compensation affects sustainability reporting positively in developing countries, such as Nigeria.

Keywords

Introduction

This paper critically assesses the influence of Board governance characteristics on sustainability accounting and reporting (SAR), which includes social, economic and environmental reports. Although many studies have addressed the determinants of sustainability accounting and reporting using either internal firm characteristics such as firm size, leverages, and listing age, other studies have used external influences, for example, political, legal, and regulations, as factors that affect corporate voluntary disclosures(Anugerah et al., 2018). Aside from these characteristics, other studies have used elements such as corporate governance characteristics such as board diversity and structure ( El-Deeb et al., 2022; El-Deeb & Elsharkawy, 2019) as factors affecting the quality of voluntary disclosure; such studies are more in developed countries than as it is in developing countries such as Nigeria. While El-Deeb et al. (2022) studied the impact of board characteristics on the disclosure of forward-looking information in Egypt, such a study concentrated on forward-looking information rather than specifically on sustainability reporting. Sustainability reporting is one form of voluntary disclosure that needs adequate attention in Nigeria. Even though Nigeria, a developing country, has not progressed in voluntary disclosure of sustainability reporting in the past, Nigeria is attracting international attention as the first country in the world to adopt IFRS sustainability standards and show “signs” of change in corporate practice. With these efforts, studying factors that improve the quality of sustainability reporting becomes necessary to enable the country to position itself well after adopting the standards. Moreover, we have observed that the relationship between corporate governance and sustainability reporting is also neglected despite the increasing awareness of the importance of sustainability reporting in recent times (Akhtaruddin et al., 2009; Dienes et al., 2016; Lozano, 2019; Marte et al., 2012).

Given the importance of sustainability reporting, efforts have been made to improve firm transparency in Nigeria, necessitating the Federal Government of Nigeria to enact a Nigerian Code of Corporate Governance Act of 2018 available for private and public-owned firms. The code is aimed at institutionalizing best practices in corporate governance and creating an environment for sustainable business operations, as well as providing a framework to ensure good governance practices by articulating a broad set of principles on corporate accountability and transparency for sustainable business practices. The Nigerian Corporate Governance Code aims to achieve sustainable development. Through sustainability reporting, firms contribute to the global call for sustainability development in all spheres of human endeavor, including accounting. A robust Board governance structure is a factor that could promote the quality of sustainability accounting and reporting, given the importance of Board governance in making an informed decision that could promote stakeholder interest and performance (Alshehhi et al., 2018). Following agency theory, there are two primary roles of the Board: decision management, which includes initiating and carrying out choices, and decision control, which includes approving and overseeing decisions (Fama & Jensen, 1983). In line with the above assertion, board governance is a critical factor that should be considered viable for promoting voluntary disclosure, such as sustainability reporting in developing countries (Vural, 2018). Earlier work demonstrates that businesses which provide sustainability reports benefit from long-term competitive advantages and stakeholder credibility (Dobbs & van Staden, 2016). Investors would also profit from prudent business decisions and successful risk management and be able to reward managers who operate in a socially and environmentally responsible manner (Noah, 2017).

Although sustainability reporting is becoming a more crucial accounting reporting practice, developing nations (like Nigeria) still have a limited understanding of sustainability reporting (Daferighe et al., 2019; Haladu & Bt. Salim, 2017; Nwobu & Adaeze, 2017) and the majority of the companies do not report sustainability information. Other recent studies that investigated this concluded that additional study is needed in the area of sustainability reporting and factors that affect sustainability accounting and reporting (see, for example, Daferighe et al., 2019; El-Deeb et al., 2022; Kumar et al., 2015; Le et al., 2019; Nnamani et al., 2017). Using board governance as a factor, this study critically assesses how Board governance variables affect the quality of sustainability accounting and reporting in Nigeria. Although there has been some research in this area in both developed and developing countries, Nigeria is still lagging in studies that examine Board governance effect on the quality of sustainability reporting. This is the main issue motivating this study. To the best of our knowledge, this is the first study to have identified board governance as a factor affecting sustainability accounting and reporting in Nigeria. This study adds to the body of knowledge on sustainability reporting by demonstrating that corporate governance indices impact the quality of sustainability accounting and reporting in Nigeria.

The remainder of the paper is organized as follows. A brief assessment of the literature on the factors influencing sustainability reporting is presented in Section 2. That section also included the theoretical frameworks that serve as the study’s direction, while methodology and techniques for data analysis are covered in section 3. Section 4 presents the results, while section 5 presents the study’s conclusions and limitations.

Theoretical Framework of the Study

Stakeholder theory and legitimacy theory, propounded by Freeman (1984) and Dowling and Pfeffer (1975), respectively, are all linked to the institutional theory. Prior applications of stakeholder and legitimacy theories are extended to the examination of sustainability accounting and reporting. To be accountable to stakeholders and society at large, businesses have increased the issuance of non-financial information and have provided additional reports above the minimum explaining the impact of their activities on the environment and the use of natural resources. The institutional theory is related to the stakeholder and legitimacy theories put out by Dowling and Pfeffer (1975) and Freeman (1984). For us to examine sustainability accounting and reporting, previous applications of stakeholder and legitimacy theories are expanded by concentrating on why businesses provide more disclosure than is required using institutional theory. Businesses have increased the release of non-financial information and have provided more reports than the bare minimum outlining the effects of their operations on the environment and using natural resources to be more accountable to stakeholders and society (Khan et al., 2013).

The theoretical framework utilized to investigate external influences on sustainability accounting and reporting by Nigerian businesses is the New Institutional Sociology (NIS) lens. The literature on sustainable management and accounting has frequently employed NIS as a theoretical lens (Christ et al., 2020; Glover et al., 2014). NIS is the best because it provides a good lens for creating the context for management’s reaction to sustainability reporting. NIS was first created by DiMaggio and Powell in 1983. NIS seeks to explain why businesses in particular environments adopt similar structures and practices, which deviates from the standard management reasoning that structural change should be “driven by competition or by the need for efficiency” (DiMaggio & Powell, 1983, p. 147). DiMaggio and Powell (1983), in their landmark work, describe three kinds of pressure that, in their view, would result in the homogeneity of organizational and corporate activity. They refer to these pressures and the homogenization process as being isomorphic.

Accordingly, coercive, mimetic, and normative pressures are the three sources of isomorphic pressure. Coercive isomorphism concerns legitimacy and comes from substantial stakeholders on whom a corporation or organization depends. Although coercive pressure is also used as a result of “cultural expectations in the society within which organizations function” in the original article, many studies operationalize this type of isomorphism as having to do with the government and regulations (DiMaggio & Powell, 1983, p. 150). Mimetic isomorphism is the pressure induced by uncertainty that leads companies to imitate other organizations similarly. This is known as a “safety in numbers” strategy (Christ & Burritt, 2019: 44).

The demands of professionalization from the educational system, professional networks, and economic connections are called normative isomorphism (Christ & Burritt, 2019). DiMaggio and Powell (1983) contend that companies achieve greater legitimacy and are better able to face conditions classified as uncertain, something inherent in the grand challenge of voluntary reporting, by responding to these sources of pressure and adapting their activities accordingly (Brammer & Pavelin, 2019; Christ & Burritt, 2019).

A lack of awareness of these mechanisms and how they combine in global projects might lead to unexpected costs and reporting challenges. Thus, institutional theory provides a veritable lens for addressing management responses to sustainability issues. Admittedly, in most developing countries, practice is not currently based on coercion from the government through legislation. Nevertheless, for several reasons, the paper adopts a new institutional theory to study the effect of Board governance on the sustainability reporting quality in Nigeria.

Literature Review

Determinants of Sustainability Reporting

Prior studies have investigated the factors that influence sustainability reporting and accounting in industrialized and developing nations (Akhtaruddin et al., 2009; Al-Dhaimesh & Zobi, 2019; El-Deeb,2019; El-Deeb et al., 2022). According to Cooke and Wallace (1990), the environment impacts accounting. In this respect, numerous studies have attempted to explain the technological and environmental aspects that may have impacted the growth of corporate disclosure in a country (Raddebaugh & Gray, 2002). Studies have also shown that social, economic, cultural, political, regulatory, and trade-related factors impact how companies disclose information and how they account for it. Others have pointed to technical advancements, including the internet, mobile devices, and other types of computer software (Xiao, 2006). Several of these characteristics were combined in other studies to explain why disclosures vary widely among companies. As seen in Figure 1, prior researchers specifically discussed the connection between variations in accounting systems and the reasons that cause such variations on national and international levels.

Factors affecting sustainability accounting and reporting.

Depending on the researchers’ perspective, one component of the factor that has recently gained attention is the qualities of corporate governance (El-Deeb et al., 2022). Corporate governance has been referred to as the way companies are managed and directed. Corporate governance is intended to increase the accountability of businesses to prevent significant failures brought on by conflicts of interest or management tendencies toward opportunism (El-Deeb & Elsharkawy, 2019). Corporate governance aids in improving the calibre of financial reporting.

Earlier research connected low levels of financial reporting with bad corporate governance practices. Studies in developed regions have connected corporate governance with businesses’ capacity to offer forward-looking information (Aljifri & Hussainey, 2007). These investigations frequently used fair value and forward-looking information as dependent variables. The Board of Directors acts as the control over all other controls in corporate governance systems, which is why it is so important. To encourage effective board governance, the diversity of the Board is equally crucial. The material that is currently available demonstrates that there are two types of board diversity (see Kagzi & Guha, 2018). These are demographic and structural diversity. Board demographic diversity covers traits like board gender, age, nationality or ethnicity, and educational variety, whereas board structure diversity includes traits like board size, CEO duality, and board independence. According to the Corporate governance code, there are twenty-eight broad sets of principles, of which sixteen relate to board governance, structures, and diversity, four to risk management, whistleblowing, and audit procedures, three to relationships with stakeholders, and two to business ethics and fair treatment of stakeholders. Two of the guiding principles focus on the disclosure of information in a transparent manner and the adoption of environmentally and socially responsible corporate practices. A diversified board can assist businesses in producing trustworthy and quality sustainability reports. According to past studies, poor corporate governance practices are also associated with weak internal control systems, high levels of financial fraud and poor financial reporting quality (El-Deeb et al., 2022).

According to agency theorists, the Board has two primary responsibilities: decision management, which includes initiating and carrying out choices, and decision control, which includes ratifying and overseeing decisions (see Fama & Jensen, 1983; Shaukat & Trojanowski, 2017). The ability to initiate, implement, ratify, and monitor reporting that gives stakeholders comprehensive information about the performance of their businesses are all aspects of effective board governance. This implies that the Board is responsible for providing the three components of quality sustainability accounting and reporting. According to published research, the primary goal of sustainability reporting is for businesses to express their commitment to sustainable development and to provide information on the outcomes of their actions in the social, economic, and environmental dimensions (Talebnia et al., 2013). The quality of sustainability reporting is determined by a company’s internal structure, according to several research strands (see, for instance, Anugerah et al., 2018; Barako, 2007; Dienes et al., 2016; Dissanayake et al., 2016).

Furthermore, profitability, capital structure, and business age do not directly correlate with environmental reporting ( Dienes et al., 2016). Similar findings were made by Barako (2007), who discovered that internal organizational characteristics such as firm size, profitability, and leverage influence the level of environmental information disclosure and had a negative correlation with voluntary disclosure. Other research looked into how outside variables, including politics and law, impacted voluntary disclosure procedures.

Researchers have only recently begun to concentrate on developing countries and the factors that affect corporate environmental reporting and social reporting (Dissanayake et al., 2016; El-Deeb et al., 2022; Jessop et al., 2019; Okaro et al., 2018). Felix Erhinyoja (2019) emphasizes that context-specific studies are needed because the sustainability reporting SR factors and their impacts are significantly different in poor nations compared to rich countries. Other studies that looked into this concluded that more needs to be done in the area of sustainability reporting and the variables that affect how much sustainability information is disclosed in other developing nations (Daferighe et al., 2019; Kumar et al., 2015; Le et al., 2019; Nnamani et al., 2017). According to Dienes et al. (2016), the most significant determinants of sustainability reporting in Germany are firm size, media presence, and ownership structure. Corporate governance only impacts the establishment of an audit or sustainability committee. However, similar studies in underdeveloped nations come to the opposite conclusion (Dobbs & van Staden, 2016; El-Deeb et al., 2022; Yu & Rowe, 2017). Accordingly, these studies show that corporate governance aims to institutionalize best practices in corporate governance and create an environment for sustainable business operations. They also show that corporate governance provides a framework to ensure good governance practices by disclosing information beyond financial, such as integrated reporting and other voluntary disclosure initiatives (El-Deeb, 2019). The results of such studies are also mixed and contradictory depending on the country. Developed countries have robust governance system which is propelled by ethicality. At the same time, the same cannot be accurate for developing countries, especially in Nigeria, which has highly corrupt practices (Transparency Index, 2021) and weak legal systems and institutional reforms.

Bearing that sustainability reporting is a voluntary disclosure matter, the question raised by Elsayed and Hoque (2010) remains very cardinal. “Why do some firms disclose more information than other firms?” Similarly, Von Alberti-Alhtaybat et al. (2012) also questioned from the perspective of managerial theory—what keeps humans accountable and what makes a person strive to do the right thing. Drawing from the above analysis and prior literature, this study will make three postulations. First, we expect that board capacity, board independence and board incentives will affect the quality of sustainability accounting and reporting in developing countries like Nigeria. We will decompose board capacity into Board size and the number of Board meetings, while board independence is also decomposed into independent directors and CEO duality.

Similarly, board incentives will include short-term and long-term incentives for executive directors. Scholars have used these metrics to measure the association between corporate governance and sustainability disclosure in Singapore. It is replicated in Nigeria since Singapore and Nigeria are developing countries but have different institutional mechanisms. For example, there has been an effort by the Nigerian government to control incessant corrupt practices by officers in public office, culminating in the institutionalizing of different anti-graft bodies (e.g. Economic and Financial Crime Commission, corporate governance code and other similar legislation. The rate of corrupt practices in Nigeria cannot be said to be the same in Singapore or any other developing country. However, given the general weakness in corporate institutional management in developing countries, effective board management would enhance the ability of firms to disclose sustainability information to stakeholders. These three broad variables will be discussed in detail in the next section.

Board Capacity: Board Size and Board Meetings

Given that coercive, mimetic, and normative pressures are the three sources of isomorphic pressure that could affect the quality of sustainability reporting in any jurisdiction, Board capacity is one of the essential factors. Weak Boards typically will be coerced through government legislation to provide relevant information. On the other hand, some Boards will ordinarily decide to incorporate good disclosure practices because they have made it a culture.

The capacity of the Board can mitigate managerial domination and reduce potential conflicts of interest (Hu & Loh, 2018; Mak & Roush, 2000; Zahra & Pearce, 1989). Large board size is a veritable source of human and social capital to firms because of the valuable expertise they will bring, the pool of talent and resources, and diverse knowledge of the company’s external environment (Certo, 2003), which can promote the quality of sustainability disclosure. Furthermore, large board sizes facilitate the intercompany imitation of strategies and practices (Hu & Loh, 2018). Large board sizes are also more likely to keep abreast with the latest sustainability reporting trends in the company (Hu & Loh, 2018), given that the directors may come from different backgrounds. Early studies on board size—sustainability relationship indicate a positive relationship (Amran et al., 2014; Mahmood et al., 2018; Wang, 2017).

Another aspect of the Board’s capacity is the frequency of board meetings. The frequency of board meetings reflects board activities and indicates the Board’s time capacity. Hu and Loh (2018) suggest that the most common problem that limits the effectiveness of the Board is the need for more time to perform their activities/responsibilities as a board. Conger et al. (1998) provide that effective decision-making is a function of the frequency of board meetings because it enables firms to effectively discuss the firm’s sustainability issues and engagement strategies, among other problems. Hu and Loh (2018) also pointed out that the frequency of interactions among board members through meetings would help them to monitor better and address the needs of stakeholders, which would help them to secure legitimacy. Based on the above, we expect a large board and frequency of meetings to influence sustainability reporting positively in Nigeria. Large boards may have those technically savvy in sustainability issues and those caring for the environment that lay the golden egg. Hence, the Board can mimic other foreign companies in producing quality sustainability reporting. This leads us to the following two hypotheses regarding onboard capacity:

HIa: There is a positive association between board size and sustainability reporting in Nigeria.

H1b: There is a positive association between the number of meetings and sustainability reporting in Nigeria.

Board Independence: Independent Directors and CEO Duality

Another factor that affects the choice of sustainability accounting and reporting is the independence of the Board of Directors. Available evidence shows that board independence reduces agency costs by monitoring management activities. Independent directors are more vigilant in their monitoring capacity than non-independence directors and less likely to tolerate managerial opportunism at stakeholders’ expense (Kesner & Johnson, 1990). Empirical evidence suggests that a higher percentage of independent directors is expected to drive positively the levels of accountability, transparency and sustainability reporting. Firms with more independent directors on the Board provide more comprehensive financial disclosure (Lim et al., 2007).

Despite the importance of independent directors as a driving force for more voluntary disclosure, CEO duality (i.e., one person serves as both chairman and CEO of the company) can affect board independence. The superior governance power can undermine the Board’s effectiveness and render the Board less effective in monitoring and controlling functions, threatening the completeness of information transfer and reducing voluntary disclosure. Although empirical evidence on the effect of CEO duality on voluntary disclosure is mixed, it is expected that the separation of the office of CEO from that of the chairman of the Board would enhance the completeness of information transfer and sustainability reporting as the two persons may provide a pool of talents, expertise that would trigger the sustainability reporting positively. Based on this, we hypotheses as follows:

H2a: There is a positive association between the proportion of independent directors on the Board and sustainability reporting in Nigeria.

H2b: There is a positive association between CEO duality and sustainability reporting in Nigeria.

Board Incentives: Short-Term and Long Term Incentives for Directors

Strategies of director’s remuneration packages are another factor that affects the quality of sustainability accounting and reporting. The Board of Directors is an essential part of the organization, so their remuneration packages must be aligned with the stakeholder’s interests. By their position, executive directors are responsible for the day-to-day running of the business. Rewarding them based on short-term performance without taking cognizance of the long-term implications of their actions may lead to short-termism (Hue & Loh, 2018). This will cause damage to long-run value creation (Laverty, 1996). Since sustainability reporting provides firms with long-term strategies, the arrangement of incentives-based compensation could be an essential determinant of sustainability reporting. Early empirical evidence supports this (Hu & Loh, 2018). Based on this, we expect a positive association between board incentives and sustainability accounting and reporting quality. Following prior studies and theories, we developed the following hypotheses:

H3a: There is a negative association between short-term incentives and sustainability reporting in Nigeria.

H3b: There is a positive association between long-term incentives and sustainability reporting in Nigeria.

Research Method

Sample and Data Collection

The sample of this study was composed of the top 50 firms listed on the Nigerian Stock Exchange (NSE) as of 31st December 2020. The selection of a firm is based on the market capitalization of the firm. This study used data downloaded from each firm’s reports (sustainability reports, annual reports, and websites) extracted from two primary sources: the Nigerian Stock Exchange website, which serves as the mandatory repository for firms listed in the stock exchange, and the second source the GRI international sustainability website—Sustainability Disclosure Database (SDD) for each year. In total, 167 reports were downloaded and analyzed (see Table 1). The selected firms were drawn from different sectors following NSE classifications, as shown in Table 1. To be considered for selection, a company must have either published annual reports or accounts during the study period that provide substantial support for sustainability performance indicators or a standalone sustainability report of either type (for example, sustainability reports, corporate social responsibility reports, corporate social responsibility progress reports, integrated reports, and corporate environmental reports). Because laws mandate them to provide annual reports, annual reports were used (e.g., Company and Allied Matters Acts).

Summary of Sample Selection and Distribution of Sample Firms by Industry.

Note. The numbers of firms selected were relatively equal to avoid any selection bias which might distort the outcomes.

Dependent Variable

Sustainability reporting quality represents our dependent variable. We assessed each company’s annual and sustainability reports of each firm to determine the quality of the reports. Prior literature provides that sustainability reporting has three pillars: environmental, social, and economic. We evaluated and measured each of these sustainability pillars according to the quantity and quality of the information provided. Dissanayake et al. state that there are 79 performance indicators in the GRI, 50 of which are recognized as essential indicators.

In contrast, we have taken out two in our study, leaving a balance of 48. More than 40% of the annual reports and accounts or sustainability reports of the companies chosen do not have these two metrics. This left us with 48 sustainability information items (Aspects) employed in this study since they are important and pertinent to most stakeholders. There are 0 to 48 different sustainability information items. Finding the sustainability data in all the reports was simple by utilizing the “FIND” button. As a result, the sustainability quality score is determined by dividing the amount of sustainability information a company provides by the entire amount of information intended to be disclosed. This approach has been used by Ching et al. (2017) and Akhtaruddin et al. (2009), respectively.

Independent Variables

The independent variables of this study include board capacity, board independence and board incentives. We have further decomposed these three variables into (1) Board capacity measured by (i) Board size, that is, number of directors on the Board (NODOB), and (ii) Board meetings, that is, number of board meetings held within the period (NOMH). (2) Board independence is measured by (i) the number of independent directors on the Board (IND) and (ii) CEO duality (CEO). Moreover, the third independent variable is board incentives, which are also decomposed into (i) short-term incentives (STI) and (ii) long-term incentives (LTI). As a general rule, we assigned the value of 1 if a company discloses sustainability information in their annual reports, sustainability reports, or websites.

Aside from the six independent variables listed above, we have three other control variables. They are auditor type (Audit), firm size measured by the logarithm of total assets (logSize) and listing Age of firms (AGE). These variables have frequently been used by prior scholars as determinants of voluntary disclosures and are helpful as control variables in this work.

Regression Model

In line with previous studies, we use the panel effect regression model to examine the hypotheses regarding the impact of board governance characteristics on sustainability reporting quality in Nigeria. Sustainability reporting quality (SR_Q) is the dependent variable, while the independent variables consist of the various factors affecting the choice of sustainability reporting. Based on previous studies, we introduce three other factors widely reported as factors affecting firms’ voluntary disclosure as control variables. These are Auditor type, Size, and Listing age. The panel regression model allows for the control of individual unobserved heterogeneity, given that firms are studied across sectors and the heterogeneity of the firms. Drawing from previous studies (Babin & Anderson, n.d.; Diamantopoulos & Winklhofer, 2001), we specify the panel regression, which shows the relationship between the dependent variable and the various measures of the exogenous variables as follows using the general fixed effect model as shown in model 1;

Where Y is the dependent variable; α = (i = 1 …) is the unknown intercept for each entity (n entity specific intercepts); β is the vector containing coefficients of independent variables; X represents vectors of the independent variables, µit is the error term; t is the time (year), i is the company and j represents the industry. According to Fifka (2012; Babin & Anderson, n.d.; Sharma et al., 1978), this model allows for the control of individual unobserved heterogeneity.

Expanding X to generate the baseline econometric model, we have:

We introduced the three control variables discussed earlier to account for the three control variables used in the work. These include the type of audit firm (AUDIT), size of firms (SIZE), and listing age (AGE). Thus, this leads to equation (3).

To allow for the possible effect of the autoregressive process on the stochastic term, a one-year lagged dependent variable (SRQIt-1) is included in the equation and then fitted into an autoregressive model where

Where SR_Q stand for sustainability reporting quality

NODOB is the number of directors on the Board

NOMH is the number of meetings held within the periods

IND is the number of independent directors on the Board

CEO is the CEO duality

STI is the short-term incentive packages

LTI is the long-term incentive package for directors

AUDIT represents the auditor type, and

SIZE represents the firm’s size, while Age is the listing age of the firm.

Results and Discussion

Descriptive Analysis

The variables in the sample dataset are listed in Table 2, along with their minimum, maximum, mean, and standard deviation. Our finding demonstrates that there are apparent variations in the sample. The dummy variable SRQ has a mean value of 0.65, which reflects that, on average, 65% of the sampled companies report on sustainability in various ways, including standalone reports, annual reports, and websites. The outcome also shows that the sample firms’ sustainability reporting increases from 0.57 to a maximum of 0.84 with a standard deviation of 0.069. This demonstrates how committed Nigerian businesses are to informing stakeholders about sustainability. The table also suggests that, on average, Nigerian firms have approximately 7 (6.71) with a mean of 9.04. Our result also suggests that the number of meetings firms hold in Nigeria ranges from a minimum of 0 to 45, with a mean of 0.032. The analysis also indicates that independent director on the Board ranges from a minimum of 5 to a maximum of 9 Directors with a mean of about 7.02.

Descriptive Statistics.

Results also show that the sampled firms held an average of 45 meetings per year (almost two monthly) and that a significant proportion used short-term incentive packages (STIR). In contrast, approximately 72% use long-term incentive packages to motivate their directors. We also observed that the average Age of the sample firms stands at 73, while disclosure ranges from a minimum of 11.0 to 34.0. Our statistics also indicate that Big 4 audit firms audit 78% of the samples (39 out of 50).

Correlation

We tested for the presence of multicollinearity using the Pearson moment correlation test. Our result provides evidence to conclude the absence of multicollinearity issues among the independent variables in our regression model (Table 3).

Pearson Correlation Analysis.

Correlation is significant at the .01 level.

Correlation is significant at the .05 level.

Empirical Results

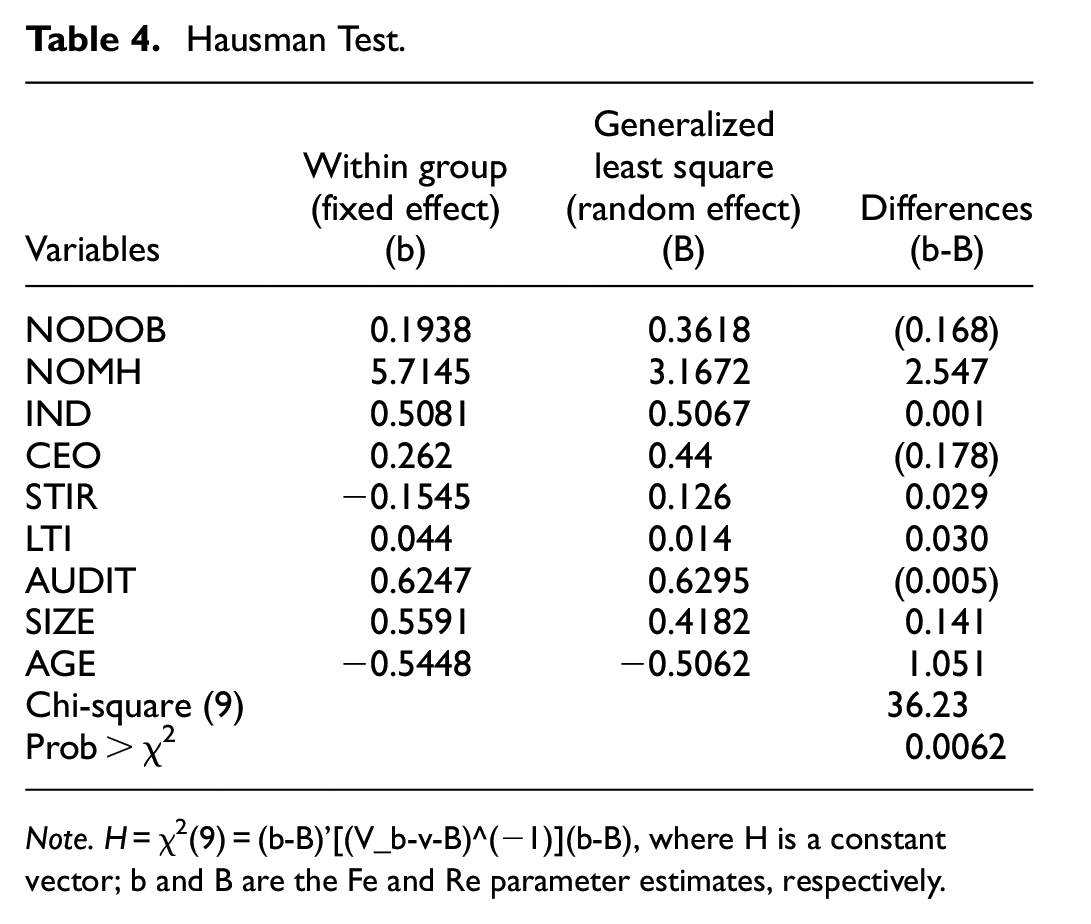

As previously mentioned, the sample frame for this study consists of businesses of all sizes and industries. The issues caused by this degree of heterogeneity are resolved using a panel estimate technique. In most panel estimations, there is always a chance for both fixed effects (FE) and random effects (RE), consistent with the results of earlier studies. The Hausman test method is used to address the problems that occur. To choose between FE and random effect, apply the Hausman test. It examines the relationship between the regressors and the unique errors (ui). The instructions suggest that we utilize Fe if the p-value is significant (i.e., less than .05), but if not, we should use the random effect. The arising results of the Hausman test are presented in Table 4.

Hausman Test.

Note. H = χ2(9) = (b-B)’[(V_b-v-B)^(−1)](b-B), where H is a constant vector; b and B are the Fe and Re parameter estimates, respectively.

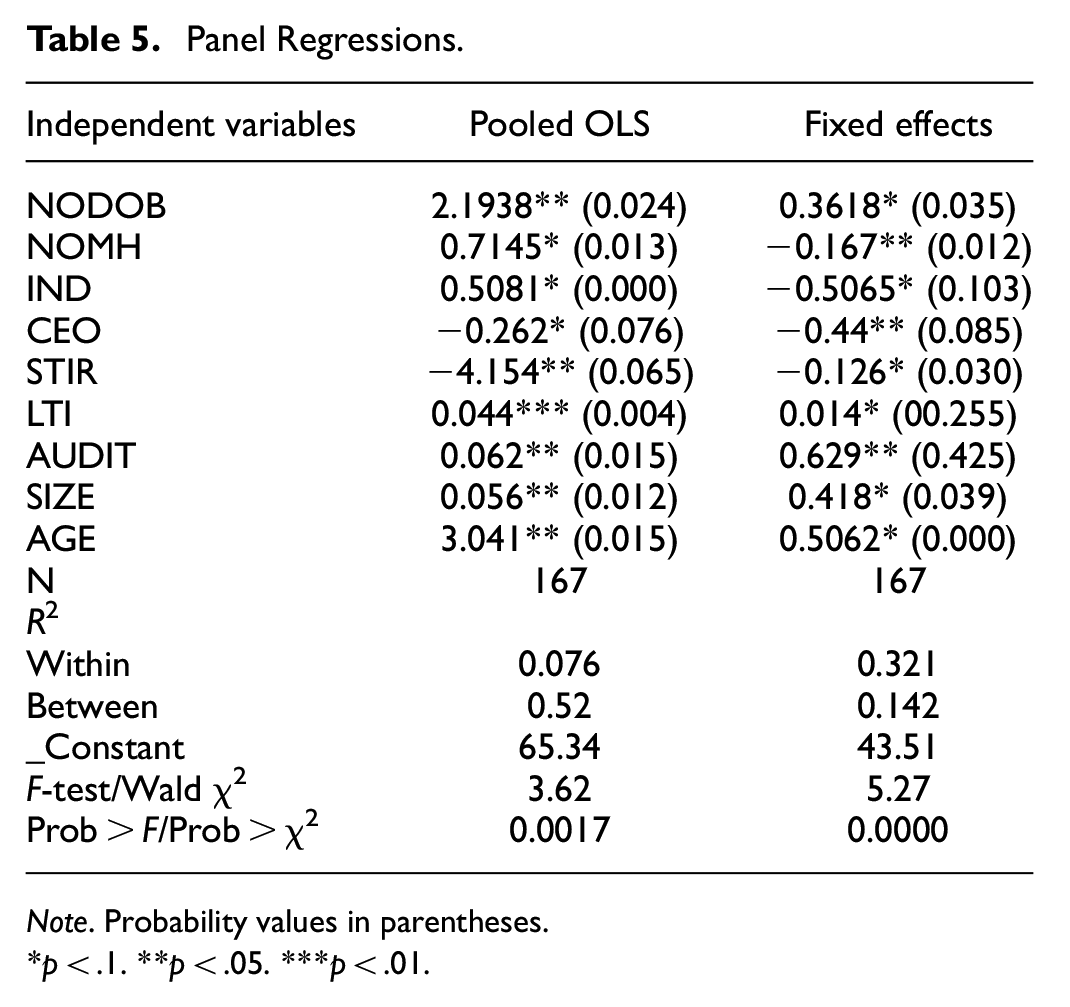

The null hypothesis that the difference in the coefficients of the variables is not systematic is rejected with a test result of 36.23 and an associated probability (p-value) of .0062 (about .01), leading to the selection of the fixed effect regression strategy. The fixed effect regression analysis findings are shown in the following Table 5.

Panel Regressions.

Note. Probability values in parentheses.

p < .1. **p < .05. ***p < .01.

The results from the fixed effects model demonstrate that the quality of sustainability reporting in Nigeria is significantly and favorably correlated with the number of directors on the Board (NODOB). This result suggests that companies with more directors on the Board have a higher degree of sustainability reporting, consistent with the descriptive results stated initially in Table 4 of this paper. This result contradicts the findings of Isukul and Chizea (2017) but is compatible with Hu and Loh’s (2018) earlier. Hue and Loh (2018) found that the Board’s capacity can mitigate managerial domination and reduce potential conflicts of interest. Large board size is associated with human and social capital that would provide valuable expertise to the Board through their pool of talent and resources and diverse knowledge of the company’s external environment. This will promote the quality of sustainability reporting. Our results also indicate that the number of board meetings (NOMH) within the period is significantly positively related to Nigeria’s sustainability reporting quality. Consistent with stakeholder theory, Board performance to safeguard the interest of shareholders is reflected in the number of meetings where critical sustainability issues are brought to attention. Regular meeting of the Board drives directors’ efforts to report sustainability matters. The frequency of board meetings reflects board activities and indicates the Board’s time capacity. Earlier work suggests that the most common problem that limits the effectiveness of the Board is the need for more time to perform their activities/responsibilities as a board. The frequency of interactions among board members through meetings would help them to monitor better and address the needs of stakeholders, which would help them to secure legitimacy.

The finding also indicates that independent directors on the Board have a positive relationship with the quality of sustainability reporting, though insignificant. A higher number of independent directors acts as a check against management excesses and can bring issues of lack or otherwise of sustainability matters to the table for discussion. This would increase the quality of sustainability reporting. The non-significance nature of the variable shows that such is not characteristically a significant factor affecting the quality of sustainability reporting in Nigeria. The result is different from the prior study, which found otherwise. In line with extant literature, Board independence reduces agency costs by monitoring management activities. Independent directors are more vigilant in monitoring than non-independence directors and less likely to tolerate managerial opportunism at the stakeholder’s expense (Kesner & Johnson, 1990). Our study supports that independent directors positively drive Nigeria’s sustainability reporting quality.

Additionally, the results show that CEO duality, short-term incentive plans, and long-term incentive plans are statistically significant predictors of Nigeria’s sustainability reporting quality. Board governance incentives can be used to alter the regulations under which the agent is required to act and reinstate the principal’s interests. The principal must get around the need for more knowledge regarding the agent’s task performance by hiring the agent to represent the principal’s interests. Agents need incentives to behave in the principal’s best interests. By taking into account the interests that drive an agent’s behavior, agency theory can be used to create these incentives effectively. Rules against moral hazard must be in place, and incentives for bad behavior must be eliminated. The strategies of director compensation packages have an impact on reporting on sustainability.

The Board of directors play a crucial role in a business, so their compensation packages must reflect the stakeholders’ interests. By their position, executive directors are in charge of managing the company’s day-to-day operations. Rewarding them for short-term achievement without considering the long-term effects of their choices could promote short-termism (Hue & Loh, 2018).

Results further show that firms with high total assets engage more in actions that improve sustainability reporting. In contrast, firms audited by Big 4 audit firms provide higher sustainability information than others audited by other firms. This means that auditor type has a significant positive relationship with the quality of sustainability reporting. It, therefore, means that firms audited by Big-4 audit firms engage in activities that improve the quality of sustainability accounting and reporting. In line with the new institutional theory, the uncertainty described by DiMaggio and Powell (1983) can be related to the basis of sustainability reporting. Sustainability reporting is mainly voluntary, meaning organizations are free to form the structure and content of their reports. However, with experienced auditors from international backgrounds, firms would engage in reporting above the minimum to satisfy the auditors who properly have versed knowledge about sustainability reporting and would want companies to do the needful. Big 4 Audit firms have a reputation that they always protect.

Our study also found that listing the Age of firms affects the quality of sustainability reporting positively. The finding also shows that firm size has a positive relationship with the quality of sustainability reporting. This is because firms with higher assets are expected to be buoyant enough to provide additional disclosure (sustainability reporting) above the minimum. Research related to company size and sustainability reporting refers to the theory of legitimacy, which states that larger companies receive more public scrutiny, requiring more legitimacy and higher resources. The stakeholders of more prominent companies follow all company activities. The bigger the companies, the more they will disclose high-quality sustainability information.

Similarly, we used Table 6 to estimate the results of the system-GMM based on our equations (3) and (4). We treated some variables as partly endogenous in all the functions and system-GMM estimations. This aligns with our theory that some form of causality exists between these factors and the dependent variable.

System GMM Estimation Results.

Note. AR(1) and AR(2) represent the first and second order autocorrelations of residuals. Model I is the system GMM results when the three c control variables are excluded while model II represents results when the control variables are included.

, **, and *** indicate that coefficients are significant at 10, 5, and 1% levels respectively.

Table 6 shows the system–GMM estimation results. The correlation results (1 and 2) the first and second-order autocorrelations of residuals are asymptotically distributed, while our test for heteroskedasticity consistent asymptotic robust standard errors is given in parentheses. Wald 1 and 2 are Wald tests for the joint significance of estimated coefficients, asymptotically distributed as χ2 (df) under the null of no relationship. At the same time, Wald 2 is a Wald test for the joint significance of the time dummies also distributed as χ2 (df) under the null of no relationship, excluding the first year (2015) and the last year (2020) which are dropped due to collinearity problems. Our Sargans test for both the system GMM (SYS_GMM) and the differenced GMM(DIF-GMM) is a test of over identifying restrictions asymptotically distributed as χ2 (df) under the null instrument’s validity.

We applied the two steps version of the system GMM techniques developed by Blundell and Bond (1998) which is found to have the capacity to control for the correlation of errors over time, heteroskedasticity across firms, simultaneity and measurement errors due to the utilization of orthogonal conditions on the variance-covariance matrix (Anthoniou et al., 2008). More specifically, our choice of the system GMM is motivated by three considerations. (1) the nature of our data set (more diminutive size of T = 5, Relative to a larger size of N = 167). (2) The possibility of the variance of the time-invariant unobservable firm-specific effects increasing relative to the variance of the serially uncorrelated time-varying disturbance terms and (3) the likelihood of the autoregressive parameter or the adjustment speed approaching unity. Blundell and Bond established that the system-GMM estimator becomes more helpful in reducing the finite–sample biases associated with the differenced GMM-estimator. Our results for the various tests are shown in Table 6.

Overall, the model’s variables are all significant and successfully predict roughly 76% of the changes in the dependent variable. A large f-value, or greater than the F-critical value, generally denotes the variable’s overall significance. The F-test typically evaluates the regression model’s overall fit and contrasts the combined effects of all the variables. As the overall f-test is significant, we can deduce that the R-square does not equal zero and that there is a statistically significant correlation between the model and the dependent variable.

Conclusion

The main goal of sustainability reporting is for businesses to express their commitment to sustainable development and to provide information on how their actions have affected social, economic, and environmental performance. This paper, therefore, has investigated factors that drive the choice of sustainability accounting and reporting as a business strategy by drawing insight from large businesses listed in Nigeria stock exchanges using descriptive statistics and fixed effects regression estimation model. Our study finds new evidence that Board governance characteristics are significant factors affecting Nigeria’s sustainability reporting quality. The results suggest that although the number of directors on the Board is positively associated with the quality of sustainability reporting, CEO duality is insignificant and negatively associated with the quality of sustainability reporting in Nigeria. We observed that the number of meetings held by directors and listing age significantly affect the quality of sustainability reporting; firm size, however, is significant but exhibits a negative association. The study also finds that setting up incentive-based compensation for board directors affects sustainability reporting positively for long-term incentives and negatively for short-term incentives. Our findings support long-term incentive packages for directors rather than short-term incentives. This study adds more proof to the knowledge that effective board governance influences the choice of sustainable accounting and reporting in a developing country.

This study offers three contributions. First, it adds a comprehensive analysis of the factors influencing sustainability reporting in Nigeria to the literature on sustainability reporting in emerging economies, particularly Nigeria. The study also expands and updates the findings from earlier research, contextualizing them in a developing economy. By doing this, this paper, unlike most earlier studies that focused on established markets, offers new evidence on the sustainability issue in the context of developing economies. Our study, therefore, supports the request for additional context-specific research in poor nations (Ali et al., 2017; Duran & Rodrigo, 2018). Finally, the results add to the body of literature used to promote expanding our knowledge on the subject by offering more proof of the importance of particular factors.

This study’s main flaw is that it only includes data from one country, Nigeria, and a limited sample of businesses, which could make generalization difficult. Based on those mentioned above, future researchers should assess sustainability across regions by including more countries or changing the basis to a regional one. Our study demonstrates that the effectiveness of sustainability accounting and reporting in Nigeria is influenced by the Board’s capability, independence, and incentives. Therefore, the government should focus more on providing incentives for companies that provide extensive sustainability reporting to encourage management to pay attention to the issue of sustainability reporting.

Supplemental Material

sj-xls-1-sgo-10.1177_21582440231224235 – Supplemental material for Influence of Board Governance Characteristics on Sustainability Accounting and Reporting in a Developing Country: Evidence From Nigeria Large Businesses

Supplemental material, sj-xls-1-sgo-10.1177_21582440231224235 for Influence of Board Governance Characteristics on Sustainability Accounting and Reporting in a Developing Country: Evidence From Nigeria Large Businesses by Isaac Monday Ikpor, Otu Otu Akanu, Joy Ugwu, Gabriel Obasi Chidozie Udu, Fabian Udum Ulo, Nicholas Achilike, Linus Adama and Bethel Oganezi in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Data Availability Statement

The data that support the findings of this study are available on request from the corresponding author.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.