Abstract

This paper investigates the impact of foreign fund’ flow on the Indonesian stock index incorporating other variables, namely the international stock market, gold price, foreign exchange rate, and the oil price. GJR-GARCH (1,1) model is used to analyze daily time-series data on IDX, foreign fund flows, the S&P 500, and gold, currency, and oil prices from 2014 to 2019. There is an evidence of leverage effect. It means that there is an asymmetric news impact on the conditional variances. Currency and oil prices are the only variables to have an impact on the Indonesian stock market index, while the rest of the variables do not influence the index. The government may provide infrastructures to attract foreign investors. At the same time, the government has to issue the policy that will protect the economy from stock market shocks. Finally, investors may include gold in their portfolio to diversify their investments.

Introduction

Stock index movement is influenced by investors’ expectations of the national economy, as well as the global economy. In the global era, countries become borderless, and investors from all around the world are able to invest their money in a country’s stock market. However, the risk is hand in hand with money from foreign investors. Since most of the investors are expected from the capital gain, that is, short-term investors, the selling action from the foreign investors will increase the risk of an economic shock in the country. Wang (2000) suggested that foreign selling had a significant impact on market volatility in the period 1996 to 2000, even though foreign investors are net buyers of Indonesian stocks, and foreign selling accounts for only 13% of daily trading. On the other hand, transactions between foreign investors account for 26% of daily trading but do not affect the volatility of the local market. Furthermore, Wang (2007) investigated a negative relationship between foreign ownership and the future volatility of Indonesian stocks. Frensidy (2008) concluded the same outcome, i.e., that foreign cash flow influences the index movement in Indonesia.

Other than the studies above, to the best of the authors’ knowledge, a study on the impact of foreign investors’ flow on the Indonesian stock index employing Glosten-Jagannathan-Runkle Generalized AutoRegressive Conditional Heteroskedasticity (GJR-GARCH) method and incorporating other variables, namely the international stock market, gold price, foreign exchange rate, and the oil price, has not been done yet. Furthermore, there is an evidence that the investor base composition has changed. As reported by the Indonesia Central Securities Depository (KSEI) that the number of foreign investors has decreased to 47.35% since 2017, which brings the consequences to a change of the amount of foreign cash flow into the market. Hence, it is fruitful to investigate the effect on the index.

Several reasons for the importance of the study are as follows. Large inflows or outflows of foreign funds can cause price fluctuations and market instability. Simultaneously, capital inflows can boost the country’s economic growth by raising investment in local businesses, company expansion, and creating employment opportunities. In addition, studying the impact of fund flows on the stock market can assist policymakers in developing appropriate policies that balance the advantages of foreign investment with possible market stability issues. For investors and financial managers, the findings might be helpful for investment strategies. By diversifying their investment in foreign markets, investors may minimize the risk of relying on their local stock market. Finally, the study is to contribute to the existing theory of stock market movement, especially from emerging countries’ points of view.

Literature Review

According to the literature, many factors influence the volatility of the stock market; among them are the international stock market, foreign fund flows, the oil price, the gold price, and foreign currency. The research findings show evidence of co-movement between stock markets internationally. G. Meric et al. (2016) suggested that the correlation between Latin American stock markets and the world’s other stock markets has increased significantly. Furthermore, Kaabia (2015) argued that the existence of cross-sectional patterns both in regional and USA market correlations with OECD equity markets.

Meanwhile, Kaminsky and Reinhart (2001) and Nagayasu (2000) suggest that contagion exists between emerging countries. The co-movement also exists in the ASEAN markets. Employing a VEC model, Aumeboonsuke (2019) indicated that the movements of the UK and US stock market returns have some degree of influence on several of the ASEAN stock markets. However, the benefits of portfolio diversification in Asian stock markets become insignificant from 2001 to 2011, since the contemporaneous co-movements of the markets become closer (I. Meric & Kim, 2012). The authors concluded that the most influential stock markets in Asia are the Singapore, Indian, and Japanese markets, while the Philippine and South Korean markets are the least influential. Further, the USA market is the primary information producer, and it exerts a dominant influence in the other world markets. Generally, the small markets are affected by the major markets (Drimbetas et al., 2006; Sariannidis et al., 2006). Following the prior studies, the hypothesis is as follows:

H1: The international stock market movement has an impact on the domestic stock price index

Literature has inferred two conclusions in regard to the effects of foreign investors’ flows on the stock market. The first implication is to focus on whether there is a correlation between foreign investors’ flows and stock returns. Research findings support the phenomenon of the relationship between the funds’ flow of foreign investors and the stock returns (Adaoglu & Turan Katircioglu, 2013; Clark & Berko, 1996; Dahlquist & Robertsson, 2004). The second implication is to focus on trend-chasing. Trend-chasing is the tendency to sell the low past return assets and buy the high past returns assets. Trend-chasing is specifically common among individual and inexperienced investors’ returns (Fong, 2014). Trend-chasing is also called positive feedback trading. The empirical studies suggest that there is evidence of positive feedback trading in aggregate stock market indices (Choe et al., 1999; Dahlquist & Robertsson, 2004; Froot et al., 2001; Kim & Jo, 2019; Koutmos, 2014).

Further, Kim and Jo (2019) argued that the behavior of foreign investors substantially increased volatility in the stock returns of the two largest market capitalization companies in the Korea Stock Market. Dai and Yang (2018) add the sentiment factor for analyzing positive feedback trading. The authors presented evidence of how sentiment influences the behavior of both feedback traders and rational investors. In contrast, Adaoglu and Turan Katircioglu (2013) argued that negative feedback trading by foreign investors is found during the pre-EU accession negotiations period in Turkey. Following the prior studies, the hypothesis is as follows:

H2: Foreign fund flow affects the domestic stock price index.

Theoretically, the mechanism of the effect of oil prices on the stock market behavior works through five channels (Degiannakis et al., 2018). The first is the stock valuation channel; that is, the effect is through the cost of production of goods and services, which eventually affects the profit margins of the listed companies (Basher & Sadorsky, 2006; Garefalakis et al., 2011). The second is the monetary channel. The oil price changes will influence the expected discount rates of future cash flows, which are at least composed of expected inflation and expected real interest rates (Mohanty & Nandha, 2011). If a central bank increases a short-term rate, the discount rate will increase, eventually leading to fewer positive NPV projects or lower cash flows. Thus, due to increase discount rates (lower cash flows), stock prices decrease in value. The third channel is the output channel. The increase in oil prices leads to lower aggregate demand, with lower expected cash flows for firms, which eventually leads to lower stock prices (Svensson, 2005, 2006).

Nevertheless, the impact is not expected to hold for all economies. It depends on whether the economy is oil-exporting or oil-importing. The effect on the stock market is negative if the economy is oil-importing. And, likewise, the impact on the stock market will be positive if the economy is oil-exporting. The fourth channel is a fiscal one. The channel is initially concerned with oil-exporting economies, which use their oil revenues for financing physical and social infrastructure (Emami & Adibpour, 2012; Farzanegan, 2011). Increased oil prices tend to lead to a transfer of wealth from oil-importing economies to oil-exporting ones. Eventually, the increased oil prices lead to a bullish stock market (Dohner, 1981). The last channel is the uncertainty one (Brown & Yucel, 2002). Climbing uncertainty about future oil costs motivates the household to postpone both investment and consumption. Thus, households choose to save more. Consequently, this brings the economic growth prospects to decrease, and thus the stock market returns (Edelstein & Kilian, 2009).

Research has empirically supported that the price of crude oil negatively influences stock markets (Cong et al., 2008; Jones & Kaul, 1996; Kling, 1985; Sadorsky, 1999; Wei, 2003). Investigating the Saudi Stock Market, Almohaimeed and Harrathi (2013) proved that oil prices have a negative volatility spillover effect on the stock market. However, the stock market has both a negative shock effect and a positive volatility effect on oil prices. Furthermore, with regard to oil prices and sector stock returns, the authors showed that only oil price volatility affects sector stock returns. Following the prior studies as an oil-exporting country, the hypothesis is as follows:

H3: the price of crude oil has an impact on the domestic stock price index

It has been a decade that the investors use gold as a diversification tool for their investment. Gold is mainly a safe-haven investment tool. The gold price moves along with inflation; hence, gold acts as an inflation hedge (Ghosh et al., 2004; Levin & Wright, 2006). Investors tend to keep gold during periods of political and economic uncertainty as protection from stock and currency shocks. Tully and Lucey (2007) stated that investors traditionally use gold as a hedge and that the price of gold increases sharply during equity market crashes. Johnson and Soenen (1997) concluded with the same findings that gold can be part of an investment strategy, as a diversification tool, during periods of equity turmoil. However, gold has recently been used as a speculative investment strategy in combination with equity. The S&P 500 index price plays a more crucial role in gold price movement than monetary variables such as the U.S. Consumer Price Index and the monetary aggregate during the period from 1996 to 2006 (Batten et al., 2010). Following the prior studies, the hypothesis is as follows:

H4: Gold prices have an impact on the domestic stock price index.

The relationship between the currency market and the stock market has been the subject of an inconclusive result. Some of the research findings concluded no significant relationship between these two markets (Bartov & Bodnar, 1994; Jorion, 1990). The others showed a significant long-term relationship between exchange rate and stock prices (Bartram, 2004; Islam et al., 2007). Moreover, Abbass et al. (2022) suggested that global exchange rate has an impact on the conventional stock index during the period of a bullish trend. A cross-quantilogram approach applied by Han and Lee (2016) suggested that an asymmetric bi-directional spillover between two markets exists, and empirically, one market has significant predictive power on the other in Korea. The exchange rate appreciation (depreciation) leads to a significant gain (loss) in the Korean stock market the next day. Jebran and Iqbal (2016) came to the similar conclusion that there exists a bidirectional volatility spillover of the foreign exchange market and stock market for Pakistan, Sri Lanka, Hong Kong, and China.

Nevertheless, the unidirectional stock market volatility spillover to the foreign exchange market is shown only in the Indian market. Moreover, there is no evidence of volatility spill over between the foreign exchange market and the stock market in Japan. All markets show the asymmetric spillover of volatility, which is negative shocks generate more volatility than positive shocks. Following the prior studies, the hypothesis is as follows:

H5: The currency market has an impact on the domestic stock price index.

Methodology

Data

For the empirical analysis, daily observation of the Indonesia Stock Index (IDX), S&P500, gold is quoted in the Indonesia Rupiah per ounce, the Rupiah/US dollar, Indonesia net foreign stocks investments value (stock-flow), and OPEC basket price over a time period from the 2nd of January, 2014, to the 5th of November, 2019. The data is obtained from Bloomberg and OPEC. All the data are transformed into the daily return Rt = Pt − Pt-1/Pt-1. Rt is a daily return of the series for day t, Pt is the current-day closing price, and Pt-1 is the closing price of the previous day.

Method

The preliminary statistical result of the IDX series shows that the series has an Autoregressive Conditional Heteroskedasticity (ARCH) effect—that is, the volatility clustering. GARCH is a suitable method to overcome the ARCH effect. However, GARCH models assume that only the magnitude excess returns determine the conditional variances. The model does not incorporate the positivity or negativity (asymmetry) shocks on excess returns. GJR-GARCH models overcome the asymmetric features of the data.

The GJR-GARCH (1,1) model is stated as follows:

The mean equation:

Where Xt is a vector of exogenous variables

The conditional variance equation:

Where

Result and Discussion

Descriptive Statistics

Table 1 shows the descriptive statistics of all series of daily returns. The mean values of all series, except foreign flows, are close to zero. Only foreign flow series have a high standard deviation, that is, the standard deviation is more than 1. This means that the flow has a broad price range; in other words, the flows have high price volatility, while the rest of the series have low standard deviations.

Summary Statistics.

The skewness of the series shows that the series departs from a normal distribution curve. The Jarque Berra p-value leads to the conclusion of non-normal distributions. With regard to the skewness, IDX and S&P500 are relatively symmetrical. The skewness is between −0.5 and 0.5. However, the currency return series is moderately negatively skewed. This means that more currency returns, which has a higher value than average. The fact that Indonesia’s currency has continued depreciating since the Jokowi regime took over the government in 2014 offers speculators more opportunities to earn higher returns.

The gold and oil series are moderately positively skewed. More returns have less value than average. When the rupiah becomes weak, the price of gold becomes relatively more expensive, while a stronger rupiah might make gold relatively less expensive. The high gold price might be a reason for fewer returns of gold. Trading in currency is more attractive for investors due to the liquidity and a greater chance of profit.

Furthermore, foreign flows are highly positively skewed. This shows that the total rupiah value of foreign investors’ net buy is far more than the average value. It is due to the consistency of the rupiah’s depreciation against US$ and the slow pace of Indonesia’s economic growth. According to an analyst, the flow of foreign funds to IDX is to benefit from the low share prices. The share prices have been relatively stagnant this year, and the potential gains from Indonesian stocks were relatively outperformed by those in other markets (Rahman, 2019). Kurtosis shows that all the data, except IDX, have substantial outliers, that is, leptokurtic. However, IDX shows the opposite, that is, platykurtic. In terms of unit root data, the ADF test sowed that all the series were stationary.

Discussion

Figure 1 exhibits the clustering volatility of the IDX return series. It confirms the preliminary statistical result of the series, that is, the existence of the ARCH effect. Furthermore, the Akaike Information Criterion of several models of GJR-GARCH comes up with GJR-GARCH (1,1) as the best model. The goodness of fit and appropriateness of the model are performed by testing the serial correlations and ARCH effect of both the standardized residuals and the squared standardized residuals of the estimated models. As can be seen in Table 2, the LB (n) statistics for both standardized residuals and squared standardized residuals confirmed no autocorrelation up to 36 lags. LM (ARCH of order 2) returns the same conclusion, that is, no ARCH effect.

IDX index return.

Test For Autocorrelation and ARCH Effects on Standardized and Squared Standardized Residuals.

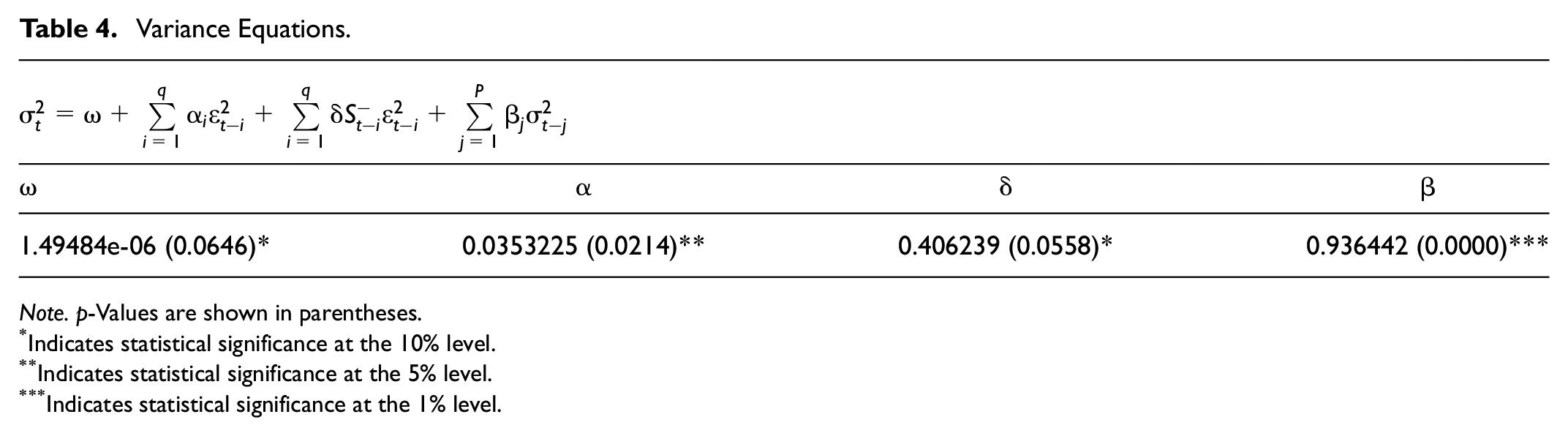

Tables 3 and 4 present the result of mean equations and variance equations, respectively. From Table 4, we conclude that the leverage effect exists. This means that there is an asymmetric news impact on the conditional variances. It is consistent with the theory that negative news has more impact on the volatility of the stock return than good news.

Mean Equations.

Note. p-Values are shown in parentheses.

Indicates statistical significance at the 5% level.

Indicates statistical significance at the 1% level. The structural break is tested for several break points (25/8/15; 14/11/16; and 19/07/18). The results show no indication of the structural breaks (test results are provided by the authors upon request).

Variance Equations.

Note. p-Values are shown in parentheses.

Indicates statistical significance at the 10% level.

Indicates statistical significance at the 5% level.

Indicates statistical significance at the 1% level.

We observe in Table 3 that all the signs of the independent variables are consistent with the existing literature. Nevertheless, only two variables, namely currency and oil, have a significant impact on the Indonesian stock index return.

The significant and negative impact of currency on stock index return is in line with previous studies (Bartram, 2004; Han & Lee, 2016; Islam et al., 2007; Jebran & Iqbal, 2016). The exchange rate appreciation (depreciation) leads to a significant gain (loss) in the stock market. The impact of currency appreciation on stock price increase depends on where companies in a country make their money, that is, at home or abroad. Since the end of 2013, the rupiah has continued depreciating against the US dollar. The exchange rate is an instrument a country uses to support its economic activities. One of them is funding resources, for example, government and private debt resources. The Indonesian government has increased the debt amount to USD 395.6 billion in Sep 2019 from USD 122 billion in 2014, that is, the central government debt has increased by about 225% since President Jokowi Widodo came to office in 2014, or more than double that of the previous administration (“Indonesia External Debt,” 2019). The government has allocated much of its debt money to developing infrastructure as a key priority of Jokowi’s administration. The weakness of the rupiah sharpens the amount of debt repayment. The debt amount puts more burdens on the government’s budget.

Consequently, debt repayment has reduced funds for economic developments. At the same time, the weakness of rupiah, coupled with the increase in oil prices, effectuate the increased financial burdens of private sectors (companies). It leads to the reduction of profits. Eventually, the stock price is expected to decline.

Furthermore, the oil price has a significant positive effect on the index. Consistent with the theory, the oil price has a positive effect on the stock index through the output channel for an oil exporting country. However, Indonesia has been a net oil importer country since 2003, and the import doubled in 2014. This is because oil consumption has been more than oil production after the year 2000 (Samanta, 2015). The positive impact of the oil price on the stock index for oil importing countries is supported by the findings of Youssef and Mokni (2019), and Filis et al. (2011). The authors argued that the interdependency of world financial markets had escalated since the global financial crisis of October 2008. The correlations between oil price returns and stock markets have strengthened and become positive for the oil importing countries. The positive correlation is explained by the fact that such a crisis caused stock markets to decline and caused oil prices to decrease substantially (Filis et al., 2011).

The rest of the variables, namely S&P500, gold, and foreign investors’ flow, do not have a significant correlation with the IDX. The insignificant influence of S&P500 on IDX is supported by the findings of Purnomo and Rider (2012). The authors suggested that there is no evidence of cointegration among the Indonesia stock index and the U.S. and Japanese stock markets. It means that the Indonesia stock index is influenced by regional stock markets.

Gold is a safe haven for investors. Literature suggests that the correlation between the price of gold and stock prices is negative. If the stock return is bullish, the price of gold will decline because investors will choose the stock market for their investments, and vice versa. However, there is a lack of evidence for this correlation in the Indonesian market. According to the officer of the Indonesia Stock Exchange, the number of domestic investors is around 0.4% of the total Indonesian population (Widiyatno, 2019). This number leads to the conclusion that Indonesians remain skeptical about the stock market. In the meantime, Indonesian people traditionally prefer buying gold as their chief mode of investment. These two groups portray different views of investments. Traditional investors view gold as the safest investment since gold is resistant to inflation. Gold is treated as an alternate currency. They do not like stocks because of the uncertainty of returns, and they are not familiar with the market. Thus, gold is for people who do not have any access to or trust in the financial market.

On the other hand, gold is viewed as an unproductive asset. Financial market instruments (e.g., stocks, bonds, mutual funds, ETF, and certificates of deposits) will generate wealth and will grow fundamentally more important. These instruments contribute to the growth of the economy (Narayan & Bannigidadmath, 2017). The reasons mentioned above might explain the insignificant impact of gold on the IDX.

Lastly, there is no evidence that the foreign fund flows have an impact on IDX, as supported by Koskei (2017). The author indicated that foreign portfolio equity outflows do not affect Kenya’s stock market returns. In the case of Indonesia, the flow of foreign funds into the IDX has remained high despite the country’s gloomy economic outlook, as seen in the country’s weak export output and slow economic growth. The analyst believes that foreign investors are still able to benefit from the low share prices. Up until now, the Indonesian stock market has been dominated by foreign investors, despite the increase in the number of local investors in recent years. According to data provided by the IDX, foreign ownership in the stocks traded on IDX has reached 52%. However, local investors still dominate daily transactions (Rahman, 2019). This leads to the conclusion that even though foreign investors dominate the IDX, this does not influence the stock market because the daily transactions are still dominated by local investors.

Conclusion

The study of the determinants of the stock exchange movement is very crucial in the global era, since countries have become borderless, and investors from all around the world are able to invest their money in any country’s stock market. The selling flock from foreign investors will increase the risk of an economic shock in the country through its stock market. In the case of IDX, we conclude that the leverage effect exists. It means that there is an asymmetric news impact on the conditional variances. It is consistent with the theory that the negative news gives more impact on the volatility of the stock return rather than the good news.

Furthermore, only two variables, namely the currency and the oil price, affect the movement of IDX. The depreciation of the rupiah creates financial burdens on the state budgets due to the increase of government debt and its impact on the private sector. This leads to slow economic growth, which, eventually, will bring the stock price down.

The positive oil price affects IDX through the outcome channel for the oil-exporting country. However, Indonesia has been a net oil importer country since 2003. The correlation is supposed to be negative. The direction of the correlation has become positive for the oil-importing country since the global crisis of 2008, which caused both stock markets’ oil prices to decrease substantially.

Surprisingly, there is no evidence of the impact of foreign flows on IDX. The daily transaction is still dominated by domestic investors, even though the number of foreign investors still dominates the market. It may explain the reason for the finding.

Two distinct groups of investors might be a reason for the insignificant impact of gold on the stock price. The traditional group of investors is skeptical about the financial system. They do not bother with the movement of the stock price. In contrast, modern investors look at gold as an unproductive asset. Gold does not generate wealth and grows faster than in stocks, bonds, and other financial instruments. Lastly, the influence of SP500 on IDX is insignificant because the Indonesia stock index is influenced by regional stock markets.

The government may provide infrastructures to attract foreign investors. At the same time, the government has to issue the policy that will protect the economy from stock market shocks. Finally, investors may include gold in their portfolio to diversify their investments.

In summary, understanding the relationships between global capital movement and domestic market behavior requires researching how foreign capital flows affect a stock market index. Such investigations help investors, politicians, and regulators make appropriate decisions, which are ultimately supporting market stability, economic growth, and investor confidence. Several limitations and future studies should be addressed, even though this study offers insightful information about the connection between international capital flows and stock market indexes. First, the possibility of reverse causation makes it essential to establish a causal relationship. Other unknown variables may influence the stock market’s success and foreign capital flows. Second, comparative studies between nations with different market openness, economic growth, and regulatory settings may offer a more in-depth knowledge of how foreign capital flows impact stock market indexes in various situations.

Footnotes

Acknowledgements

The authors would like to acknowledge the support of Prince Sultan University for paying the Article Processing Charges (APC) of this publication and for their support.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The publication fee for the article was funded by thePrince Sultan University.