Abstract

Open banking is one of the main transformational levers to improve competitiveness in retail banking by enabling client data sharing with third-party providers. This study enhances the traditional Technology Acceptance Model (TAM) constructs with two additional factors, initial trust and social influence, to understand clients’ behavioral intention to adopt open banking. The study analyzes a sample of 553 surveys in Spain, a country with an established open banking regulation (European Union’s Second Payment Services Directive). The proposed model showed robust explanatory capacity (R2 = 85%). Results show that perceived usefulness, social influence, and initial trust are essential in determining the behavioral intention to embrace open banking. Nevertheless, perceived ease of use plays a minor role, an outcome aligned with current fintech adoption literature. Our study implies that private agents should focus on highlighting the benefits of open banking while policymakers should work on regulatory frameworks to increase clients’ initial confidence.

Introduction

The open banking model sought to remedy the issue of limited competition in the traditional banking industry (Basso et al., 2018). As a general rule, the design and pricing of financial products and services are heavily customized to the customer’s profile (Winter, 2002). Client knowledge is critical to competing in all banking products and services, including onboarding new clients, lending, financial advisory, transactional services, and insurance products distribution. For this purpose, first, in all jurisdictions, financial institutions are obliged to assess the fraud risk that a new customer entails (Know Your Customer processes, KYC) and carry out various regulatory controls (e.g., prevention of money laundering) (Al-Suwaidi & Nobanee, 2021; Koster, 2020). Second, credit products require an assessment of the customer’s default risk, which translates into different limits and prices depending on the client’s specific risk (Z. He et al., 2020). Regarding financial advisory, investment products require knowing the customer’s propensity for risk and the expected return for a given level of risk (Jung et al., 2019). Likewise, transactional products must be adapted to the different types of transactions preferred by the customer. The same transactional need can be met with various financial instruments such as traditional transfers, immediate transfers, direct debits, payments with credit cards, debit cards, or alternative means of payment such as Paypal or Alipay (de la Mano & Padilla, 2018). Finally, banks distribute risk coverage products for various circumstances (car, home, health) that also require a high level of customer knowledge (X. He et al., 2022). Due to all of the above, it is very complex for a new entrant to compete with the incumbent financial entities, given the existing asymmetry regarding customer knowledge (Ramdani et al., 2020).

The starting premise of open banking models was that the inability to access customer data makes it almost impossible for new entrants to compete with traditional financial institutions. Thus, access to customer data lowers the entry barriers for new competitors, enhancing higher competition. The need for data access and the consolidation of the API technology constitute the core of the open banking philosophy. The first formulation of open banking was the development of the “Open Bank Project” by Simon Redfern in 2010. According to Redfern, “Standardised RESTful JSON APIs protected by OAuth and powered by open-source software could raise the bar of financial transparency and foster greater innovation around bank accounts” (Redfern, 2021). Thus, open banking frameworks should allow higher levels of competitiveness in the banking sector, facilitating the entrance of third-party providers through a level playing field with incumbent financial institutions (Nicholls, 2019).

Open banking can be defined as “an initiative which facilitates the secure sharing of account data with licensed third parties through Application Programming Interfaces (APIs), empowering customers with ownership of their own data. The initiative aims to increase competition in retail banking by developing innovative products and services which will bring increased value to customers” (O'Leary et al., 2021). Open banking can be understood as follows: (1) as a synonym for platformization of retail banking, (2) as data sharing, (3) as financial technology, and (4) as regulation. This study regards open banking as financial technology (fintech). It is essential to distinguish between fintech as technology and fintech as an agent that leverages it. Fintech as a technology refers to the set of disruptive technologies transforming the banking business (e.g., blockchain, API, mobile, cloud, quantum) (M. R. Lee et al., 2018) and the industry built around them (Schueffel, 2017). Fintech as an agent refers to start-up companies that, using these disruptive technologies, are breaking into the financial sector. This study analyzes the adoption of open banking fintech (mainly API-fication) and not the adoption of fintechs as providers of financial products (Gogia & Chakraborty, 2022).

Open banking is based on three essential elements. First, a stable regulatory framework that facilitates the transition to banking customers’ data sharing. However, there are also data-sharing cases (e.g., United States) based on private agreements without a specific regulatory framework (Greenberg, 2021). Second, generalizing APIs as interconnection technology within an ecosystem facilitates data sharing between its actors. Nevertheless, data-sharing models can also be based on alternative technologies such as screen scraping (Liu, 2020). Finally, customer consent is an essential element in the evolution of the open banking model in all cases (Stiefmueller, 2020). Open banking is impossible without the clients’ prior consent for a third party to access their bank data. Contrary to what happens with the regulatory framework and technology, there is no substitute for customer consent in any open banking scheme.

Existing research about open banking is centered around three axes. First, a strand of literature analyzes open banking from the perspective of business model innovation (Omarini, 2020; Ozcan et al., 2019). A second strand focuses on the regulatory view of open banking and its specificity in the different jurisdictions (Ziegler, 2021). Finally, the third strand analyzes the technological aspects of open banking and the perspective of data sharing (Farrow, 2020). However, the analysis of the perspective of the final customer in open banking models is minimal, especially considering the central role of the customer in open banking models. This study aims to deepen our understanding of the drivers of adopting services based on open banking by retail banking clients. The research question underlying this study is: What drives customers’ intention to adopt open banking-based products and services?

Our research contributes both to theory and practice in three ways. First, it is a first attempt to analyze the intention of customers to adopt open banking models and the underlying explanatory factors. This analysis is especially relevant for those jurisdictions where open banking regulations have not yet been adopted, considering the significant investments in deploying open banking models. Additionally, in specific geographies where there is already an open banking regulation, the convenience of evolving it to include transactional accounts and all the client’s financial products (Open Finance in the UK or the latest update of the Payment Service Directive [PSD3] in Europe) is being analyzed (Anne-Sophie, 2020). This research can provide relevant insights for regulatory policy. The academic literature is emerging around specific open banking-based services (Rosati et al., 2022) or overall open banking adoption. To this regard, some studies analyze the phenomenon in Australia (Chan et al., 2022), India (Sivathanu, 2019), Brazil (Fernandes, 2020; Valarini & Nakano, 2021), Colombia (Zuleta Londoño & Giraldo Botero, 2021) and the Netherlands (Marzouk, 2021). However, our geographical focus, Spain, combines unique elements: digital savvy banking clients (Carbó-Valverde et al., 2021), an open banking regulation (PSD2), a highly competitive banking market and a dynamic fintech ecosystem (Valero et al., 2020). Second, our research contributes also to the literature on technology adoption models. Although technology adoption models have indeed been successfully tested in the past in various technologies, this is not the case with “API-fication” or data-sharing-based technologies. Therefore, our contribution is especially relevant in the analysis of the adoption path of this technology. Finally, this study analyzes the role of initial trust (INT) and social influence (SI) in technology adoption processes. Our results show that both factors are significant in explaining open banking-based services adoption, resulting in a model with high explanatory power (R2 = 85%). Additionally, we confirm the importance of Perceived Usefulness (PU) as well as the declining relevance of perceived ease of use (PEOU) in technology adoption, a significant shift from traditional technology adoption literature. Our research contributes to understanding the role played by both elements in the field of fintech, especially open banking. Our results are especially relevant for private and public agents. Financial services providers must understand the role of INT and SIN in adopting business cases and value propositions based on open banking—for example, when launching new solutions on the market. At the same time, policymakers, especially, regulators and supervisors, must work on legal frameworks that ensure the reliability of the new third-party providers to promote open banking-based services adoption.

Literature Review and Research Objectives

Literature Review

Three key elements in the definition of open banking must be considered to understand customer intention to adopt open banking: the regulatory framework, the data sharing, and the supporting technology.

Open banking regulatory frameworks are either deployed or are in the implementation phase in several countries worldwide. While there are differences in these regulations across jurisdictions (Ziegler, 2021), there is a common axis—the need for the client to authorize data sharing with third parties. Open banking-based relationships exist even in jurisdictions without open banking regulations, subject to clients’ approval (Arner et al., 2020; Podder, 2021). Therefore, the regulatory aspect is secondary in analyzing the clients’ intention to adopt models based on open banking.

Furthermore, a relevant body of academic literature exists around clients’ motivations to transfer their data to third parties (Borgogno & Colangelo, 2020) and the relevance of privacy (Jeff Smith et al., 2011). In the open banking context, consumers have shown a limited but growing interest in banking data sharing (Open Banking Implementation Entity, 2022). The question on data sharing focuses not only on sharing but also on the trust in the data recipient and the rewards received in exchange for the data (Dimachki, 2019).

Finally, although several technologies might support data sharing, API is the reference technology for open banking in most jurisdictions (Premchand & Choudhry, 2018; Zachariadis & Ozcan, 2017). It can be argued that API is mainly an interconnection technology (Jacobson et al., 2012) and that, as such, it is transparent for end customers. However, open banking has its specificities as a customer-oriented technology—for example, how to give consent to third parties to account data or existing frictions within the open banking customer journey (Gencheva, 2018). Thus, open banking can be considered a new fintech. Consequently, we leverage technology adoption theories and tools to analyze customer intention to use open banking.

Technology adoption is a phenomenon widely analyzed in the academic literature. Technology Acceptance Models (TAMs) have their roots in the innovation diffusion theory (Rogers, 2003) and emerged in the 1970s (Rondan-Cataluña et al., 2015). Currently, diverse models are being applied to analyze information systems (IS) adoption: Theory of Reasoned Action (TRA) (Fishbein & Ajzen, 1977), TAM (Davis, 1986), TAM2 (Venkatesh & Davis, 2000), technology readiness and acceptance model (TRAM) (Lin et al., 2007), TAM3 (Venkatesh & Bala, 2008), unified theory of acceptance and use of technology (UTAUT) (Venkatesh et al., 2003), and UTAUT2 (Venkatesh et al., 2012).

The academic literature analyzing fintech and open banking adoption through technology adoption models is significant (Table 1).

Summary of Financial Technology Adoption Research.

Note. DTPB = decomposed theory of planned behavior; TAM = Technology Acceptance Model; TRA = Theory of Reasoned Action; TRAM = technology readiness and acceptance model; UTAUT = unified theory of acceptance and use of technology.

There is tension between early parsimonious models such as TAM and the latest, more complex approaches such as UTAUT2, which includes many variables. Our analysis adopted a two-tiered process and extended TAM by adopting some elements from UTAUT and other relevant variables.

We choose TAM for several reasons. First, the model is based on TRA (Ajzen, 1991), a psychological theory adapted for IS adoption. TAM is a robust, effective, and parsimonious model for predicting user acceptance (Legris et al., 2003). The model is based only on two internal variables, namely PU and PEOU, to explain the behavioral intention (BI) to use a specific system. It has been extensively used in fintech, specifically in open banking adoption. Our analysis extends TAM, including two additional variables—INT and SI.

The reason for choosing an extended version of the TAM and not the UTAUT directly is two-fold. According to (Rondan-Cataluña et al., 2015) there are two fundamental differences between the most advanced versions of the TAM and the UTAUT. First, the UTAUT includes two additional variables, SI and the “Facilitating Conditions” (FC), defined as “the degree to which a person believes that the existing organizational and technical infrastructure can support the use of technology.” However, as (Venkatesh et al., 2003) explains, CFs are not a direct antecedent of BI but of Actual Usage (AU). In fact, the FCs are fully endorsed by the PEOU as an antecedent of BI. Therefore, in our case, it would not make sense to include them in our study since our variable to explain is BI and not AU. Secondly, UTAUT analyzes the moderating effect of certain variables (Gender, Age, Experience, Voluntariness). According to the methodology used in the academic literature as well as the results on the adoption of open banking applying UTAUT, none of the four have any impact as moderating factors of PU, PEOU or SI in BI. In summary, since open banking is in an early stage of development, with very limited usage, inhibiting the inclusion of FC as an explanatory factor in the technology adoption model and previous studies show that Gender, Age, Voluntariness and Experience have no moderating effect, the model chosen is an extended TAM instead of UTAUT.

There is a large number of academic publications studying trust (Lewicki et al., 2006). Trust has been analyzed as a relevant factor in customer-bank relationships (Carbo-Valverde et al., 2013) and specifically in banking IS adoption (Joubert & Van Belle, 2013; Kaabachi et al., 2017; Yousafzai et al., 2009). There are two main approaches when analyzing trust. According to the knowledge-based trust model, trust is a consequence of interaction. Hence, trust develops over time and from experience (Mayer et al., 1995). However, extensive research shows a certain level of trust at the very early stages of human interaction. (McKnight et al., 1998) formalized this idea of “initial trust,” which has been extensively applied in technology adoption (Chiu et al., 2017; Maadi et al., 2016). We leverage this INT approach due to the novelty of the open banking technology.

Moreover, SIN can be relevant in explaining the adoption of a significantly regulated interaction like open banking. It is a factor in UTAUT, which is considered the evolution of TAM in the history of technology adoption models (Rondan-Cataluña et al., 2015).

Research Gap and Objectives

Our study focuses on bridging several literature gaps. First, although nascent literature has analyzed open banking adoption, this is the first analysis that enhances a purely internal approach (i.e., TAM) with internal (PU, PEOU, INT) and external (SI) variables. This approach allows us to better understand the moderating factor of external variables in the adoption of fintech, specifically open banking. Second, we investigate the relevance of INT and SIN within the context of open banking adoption in a jurisdiction with consolidated open banking regulation. This perspective lets us compare the results with previous studies performed in emergent economies or jurisdictions with non-consolidated open banking regulations. Third, we focus our research in Spain, a geography with an open banking regulation (PSD2) and a highly competitive banking market and dynamic fintech ecosystem (Valero et al., 2020). Finally, we analyze the BI to use open banking-based services, adding significant insights to existing research on this matter.

Conceptual Framework and Hypotheses Structure

Conceptual Framework

The core variables are common across most technology adoption models. In the case of TAM, TAM2, UTAUT and UTAUT2, PU and performance expectancy on the one hand and PEOU and effort expectancy on the other can be interpreted as the same underlying constructs. Although these constructs progressed in the academic literature, most authors recognized their similarities. The proposed models use constructs from existing approaches by incorporating or removing some constructs to make them applicable to the open banking context (Table 2). Specifically, building on existing TAM, we extend the model to analyze the moderating impact of INT and SIN in open banking technology acceptance.

Definition of Variables.

Note. PU = perceived usefulness; PEOU = perceived ease of use; BI = Behavioral intention; SI = social influence; INT = initial trust; TAM = Technology Acceptance Model; UTAUT = unified theory of acceptance and use of technology

Hypotheses Development for the Proposed Model

Figure 1 summarizes our proposed model with the eight hypotheses tested in this article.

Augmented TAM model.

Perceived Usefulness

PU is arguably the most relevant driver of technology adoption. The underlying rationale is that individuals will not adopt new technology if it does not have a positive impact on their performance. Studies have confirmed that PU is relevant in explaining fintech adoption, especially for open banking-based services adoption (Chan et al., 2022; Sivathanu, 2019). Hence, we hypothesize that the following:

Hypothesis 1 (H1): Users’ PU positively impacts the BI to use open banking-based services.

Perceived Ease of Use

Similarly, PEOU is highly relevant in explaining technology adoption, as supported by several studies (Table 1). Studies have supported its relevance for open banking adoption as well (Marzouk, 2021; Valarini & Nakano, 2021).

Hypothesis 2 (H2): Users’ PEOU has a positive impact on the BI to use open banking-based services.

Hypothesis 3 (H3): Users’ PEOU has a positive impact on the PU of open banking-based services.

Social Influence

SIN was introduced early in the TAMs. TRA (Fishbein & Ajzen, 1977) and TAM2 (Venkatesh & Davis, 2000) include subjective norm as an antecedent of the concept. (Venkatesh et al., 2003) include SIN in a voluntary adoption context as a differential factor in the adoption of new technologies, and it has been supported in fintech (Najib et al., 2021) and open banking-based-services adoption (Chan et al., 2022).

Hypothesis 4 (H4): SIN has a positive impact on the BI to use open banking-based services.

Hypothesis 5 (H5): SIN has a positive impact on the PU of open banking-based services.

Initial Trust

INT has been extensively analyzed as a key element to explain technology adoption within a fintech context. Recent research shows a significant relationship between INT and PU (Meyliana et al., 2019), both PU and PEOU (Singh et al., 2021), and BI to use (Graužinienė & Kuizinienė, 2021). Based on that, we hypothesize the following:

Hypothesis 6 (H6): User’s INT has a positive impact on the SIN of open banking-based services.

Hypothesis 7 (H7): Users’ INT in open banking-based services has a significant impact on their BI to use open banking-based services.

Hypothesis 8 (H8): Users’ INT in open banking-based services has a significant impact on the PEOU of open banking-based services.

Research Methodology

Instrument Development

The measurement instruments and scales have been adapted from the extant literature on technology adoption and adjusted to meet the requirements of this study (Table 3). Specifically, instruments from the original technology adoption literature have been used (Davis et al., 1989; Venkatesh et al., 2012). As required, we have included instruments from fintech adoption literature (e.g., Akinwale & Kyari, 2022). Table 2 summarizes the measurement instruments.

Measurement Instruments.

Note. PU = perceived usefulness; PEOU = perceived ease of use; BIN = Behavioral intention; SIN = social influence; INT = initial trust.

Following (Venkatesh et al., 2012; Westland, 2015), all items were measured using a seven-point Likert scale. Anchors were set as 1 = “strongly disagree” and 7 = “strongly agree”.

Data Collection

Before collecting data, three subject matter experts were consulted to assess the goals and scope of the analysis, and their feedback was incorporated to develop the questionnaire. The questionnaire was pre-tested with ten respondents with an average knowledge of open banking. The questionnaire was revised according to their feedback to ensure that all the questions were adequately understood. The questionnaire was developed and administered in Spanish.

The study was conducted in Spain, a European Union country where PSD2 regulations have been implemented since 2018 (Real Decreto-Ley 19/2018 de Servicios de Pago y Otras Medidas Urgentes en Materia Financiera). In Spain, open banking-based services are already a reality in the market (Monitor Deloitte, 2020). A market research specialist with previous experience in financial services electronically delivered the survey through an online platform. The market research specialist provided the market research panel, composed of Spanish banking customers, and managed all the required consents. The survey was self-administered and completed using either a laptop, tablet, or mobile devices. We used quotas to ensure that the sample was representative of the age, income, education level, and gender at the national level.

A second pre-test of 50 surveys was delivered between May 9, 2022, and May 18, 2022. The results were analyzed to check that the questionnaire was understandable and that the time to completion was reasonable. The survey was launched between May 23, 2022, and June 10, 2022. A total of 553 responses were received.

On average, respondents hold 1.95 bank accounts and have 1.68 financial services providers. Respondents spent 10.75 min on average answering the survey (standard deviation of 6.8 min). To ensure a proper understanding of the context of the survey, respondents were shown three slides explaining what open banking is (Appendix B). After that, they had to answer two screening questions (Appendices C and D). Only 410 out of the 553 respondents answered both screening questions correctly (107 had only one correct answer, and 36 failed both questions).

Respondents’ Demographics

Concerning demographic aspects, the sample was designed to represent the Spanish population as much as possible (Appendix E). Participants should be at least 18 years old, hold at least one bank account, and be using digital financial services (e.g., online banking or mobile banking). The retained sample after filtering fundamentally maintains Spanish population representativeness. Women comprised 53.17% of the sample. Regarding age, 11.22% were younger than 24 years, 15.61% were between 25 and 34 years old, 38.94% were between 35 and 54, 22.93% were between 55 and 64, and 11.71% were older than 65. As for the education level, 2.68% of the respondents were not educated, 38.29% had completed high school, 41.71% had a first-level university degree, 14.88% had a master’s degree, and 2.44% had a doctoral degree. Finally, 21.71% declared an average income of less than 15,599 Euros per year; 14.39%, between 15,600 and 25,999 Euros; 44.39%, between 26,000 and 41,599 Euros; 15.61%, between 41,600 and 64,999 Euros; and the remaining 3.9%, 65,000 Euros and above. Respondents hold, on average, 1.95 bank accounts and work with 1.68 financial institutions.

Data Analysis

To build the model, the two-stage procedure recommended by Anderson and Gerbing (1988) and further developed by Hair et al. (2011) was followed. The first stage was the development of a confirmatory factor analysis (CFA) to evaluate the measurement model’s validity and reliability. Based on the satisfactory results of the CFA, the causal relationship between the latent variables was modeled using structural equation modeling (SEM). SEM was chosen due to its ability to model phenomena such as technology adoption. By estimating a series of latent variables and exploring their relationships, we attempt to maximize the explanation of the variance of the dependent variable (Kline, 2016).

The statistical software R (lavaan package version 0.6-12) was used to conduct the data analysis, both to perform the CFA and to build the model. The model included BI as the dependent variable and PU, PEOU, SIN and INT as the explanatory factors. The hypotheses developed in Section 3 were tested.

Results

Variables Distribution

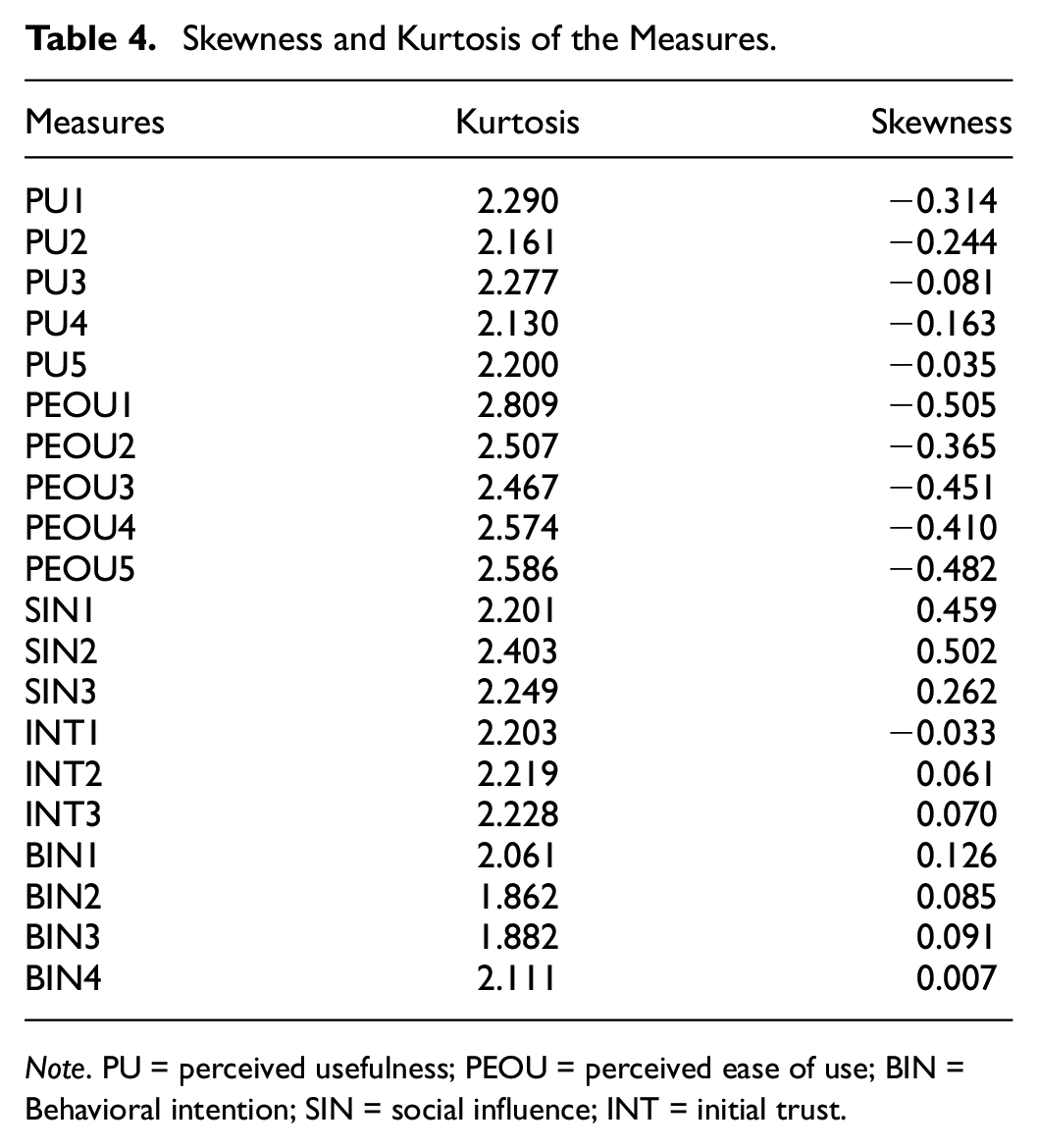

(Anderson & Gerbing, 1988; Hair et al., 2011; Kline, 2016)One of the requirements of the CFA is the normal distribution of the variables. To test that hypothesis, skewness and kurtosis were evaluated for all measures. The kurtosis ranged between 1.862 and 2.809, while skewness ranged between −0.505 and 0.502 (Table 4), both of which are within the acceptable interval to assume a normal distribution (Kline, 2016).

Skewness and Kurtosis of the Measures.

Note. PU = perceived usefulness; PEOU = perceived ease of use; BIN = Behavioral intention; SIN = social influence; INT = initial trust.

Measurement Validity and Reliability

The main target of the CFA is to assess the validity and reliability of the identified measures (Kline, 2016) The outcome of the measurement model is an estimate of the fit between the research model and the data obtained from the survey.

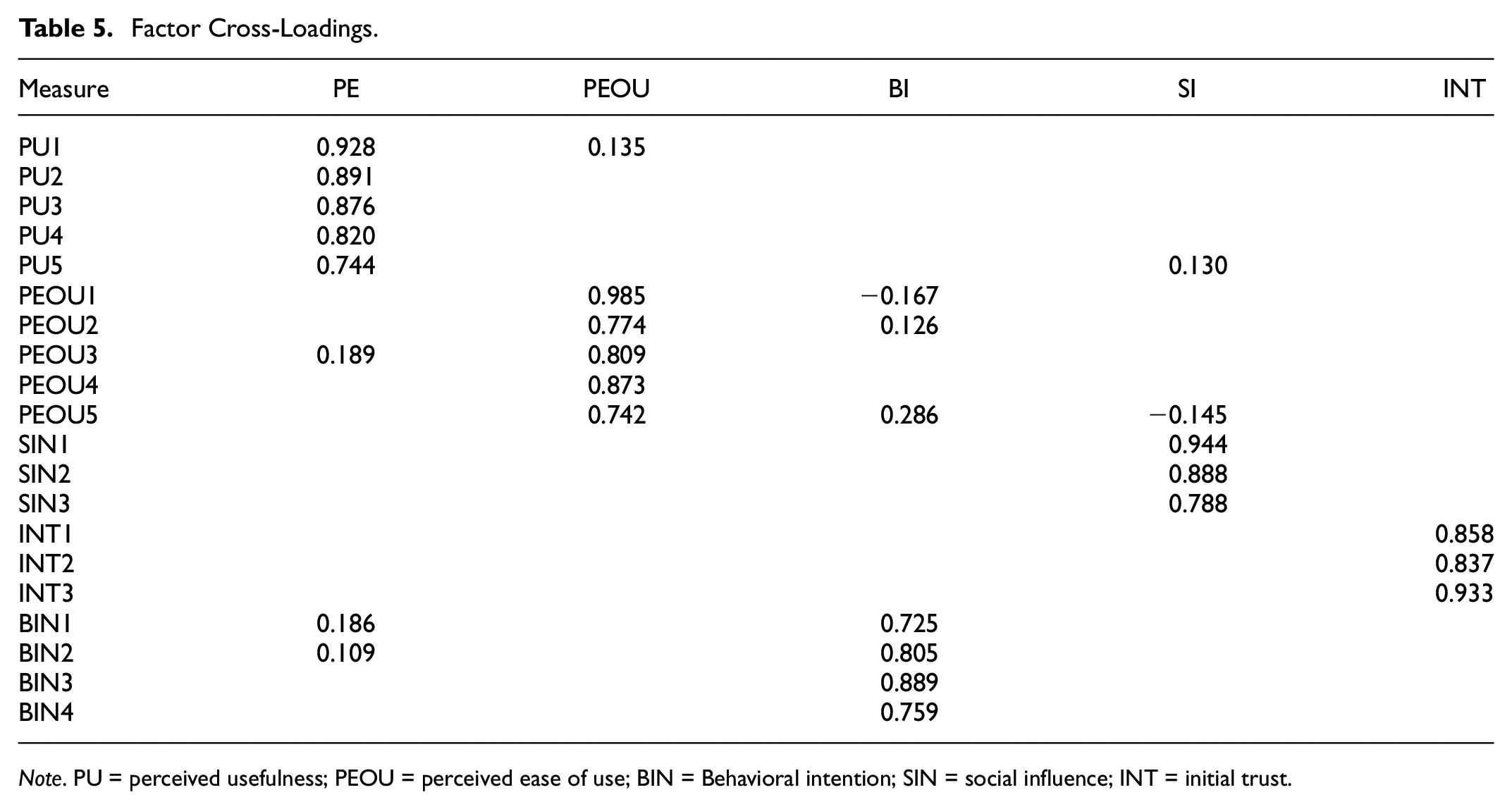

To assess reliability, factor loading and cross-loadings were analyzed. All items had factor loadings well above 0.7. The results reveal that the following conditions were met: primary factor loadings should be above 0.4, cross-loadings should be below 0.3, and the difference between the main factor loading and all the cross-loadings should be higher than 0.2 (Howard, 2016) (Table 5).

Factor Cross-Loadings.

Note. PU = perceived usefulness; PEOU = perceived ease of use; BIN = Behavioral intention; SIN = social influence; INT = initial trust.

Construct reliability was assessed using composite reliability. Composite reliability is equal to or above 0.9 for all five constructs, which is well beyond the accepted threshold of 0.7.

Convergent Validity

Convergent validity was assessed using average variance extracted (AVE). The AVE threshold to accept a sufficient convergent validity is 0.5. In other words, the latent variable can explain at least 50% of the indicators’ variance (Fornell & Larcker, 1981)). AVEs for all constructs range between 0.671 and 0.843 (Table 6).

Convergent Validity of Constructs.

Note. AVE = average variance extracted; CR = composite reliability; PU = perceived usefulness; PEOU = perceived ease of use; BIN = Behavioral intention; SIN = social influence; INT = initial trust

Discriminant Validity

Discriminant validity evaluates if the constructs are properly distinguishable from one another. We verified that the square root of the AVE for each variable exceeded the correlations between the other constructs (Fornell & Larcker, 1981). Table 7 presents the AVE values on the diagonal of the matrix (in bold), which were between 0.819 and 0.918. These values were higher than the correlation between any other two constructs (all the values below the diagonal in the matrix). Overall, discriminant validity could be accepted for this measurement model and the results support the discriminant validity between the constructs.

Discriminant Validity of Constructs.

Note. PU = perceived usefulness; PEOU = perceived ease of use; BI = Behavioral intention; SI = social influence; INT = initial trust.

Structural Model (TAM)

After the verification of the convergent and discriminant validity of the model, we performed a path analysis to evaluate the structural model. The results of the model fit analysis demonstrated satisfactory results for all indicators (Kyndt & Onghena, 2014); however, CMIN/DF was just on the cut-off limit (Table 8).

Goodness of Fit Measures.

Note. RMSEA = root mean square error of approximation; SRMR = standardized root mean square residual; NFI = normed fit index; IFI = integrated fit index; TLI = Tucker-Lewis Index; CFI = Comparative fit index.

The coefficient of determination (R2) for the overall model is 0.850, which indicates that 89.5% of the variance of the BI to use open banking-based services could be explained by the proposed model. According to academic literature (Hair et al., 2011) and comparable studies, this is a significantly high value (Table 9). R2 can also assess how well the model predicts future values.

R2 of Comparable Studies.

The proposed structural model was evaluated to test eight research hypotheses, as seen in Table 10. This study found that PU (β = .586, p-value < .001), SIN (β = .274, p-value < .001) and INT (β = .581, p-value < .001) had positive impacts on open banking-based services adoption. Thus, H1, H4 and H7 are accepted. However, PEOU (β = .088, p-value = .087) had no significant direct effect on BI to adopt open banking-based services. Hence, H2 is rejected. However, PEOU positively impacted PU (β = .459, p-value < .001). Thus, H3 is accepted. SIN had a positive impact on the PU (β = .561, p-value < .001) and on the PEOU (β = .278, p-value < .001). Thus, H5 and H6 are accepted. Finally, INT had a positive effect on PEOU (β = .777, p-value < .001) and, accordingly, H8 is accepted (Figure 2).

Structural Model Hypotheses Testing.

Note. N.S. = Not Supported; PU = perceived usefulness; PEOU = perceived ease of use; BI = Behavioral intention; SIN = social influence; INT = initial trust.

p < .001.

Results of path analysis. ***p < .001.

Additionally, there were relevant indirect effects of identified constructs in the BI to adopt open banking-based services. Table 11 shows the total effect of latent variables in the endogenous variable, obtained through the multiplication and addition of different path coefficients. The most relevant factor was INT, with an aggregated path coefficient of 0.790 due to its direct impact on SI, PU, and PEOU.

Total Effect Calculation.

Note. PU = perceived usefulness; PEOU = perceived ease of use; BI = Behavioral intention; SIN = social influence; INT = initial trust.

Discussion and Research Implications

Discussion of Findings

A vast body of literature on technology adoption exists, including on TAM and extended TAM models. However, the analysis of the adoption of fintech is still emerging, especially in the case of open banking-based services. To our knowledge, there are no studies as yet in Southern Europe that analyze the BI to adopt open banking services. Our study follows a parsimonious approach regarding the specific studies on the adoption of open banking-based services. It presents evidence of the validity of TAM in the context of adopting fintech and, specifically, of services based on open banking. Additionally, our analysis extends the TAM model, incorporating a key element of the UTAUT model—SI—and the theory of initial trust—INT—thereby significantly increasing the model’s explanatory capacity.

In the context of the literature on technological adoption applied to fintech, our study confirms the relevance of PU as a critical factor in the adoption of fintech in general (Najib et al., 2021; Senyo & Osabutey, 2020) and services based on open banking in particular (Chan et al., 2022; Sivathanu, 2019). However, our conclusions differ regarding the role of PEOU. Although this factor directly influences BI in the literature on the adoption of open banking, the literature on fintech adoption concludes that it is not a relevant factor (Ding et al., 2019; Najib et al., 2021; Senyo & Osabutey, 2020). In this sense, our results align with the existing literature on fintech adoption. Although the PEOU has some indirect impact, the direct effect is not significant.

The findings regarding PEOU align with the outcomes of prior research. According to previous publications (Venkatesh, 2000), during the initial phase of technology or service adoption, the perceived ease of use may not play a significant role in adoption behavior as users are not yet familiar with it or have not had a chance to use it. This highlights that the development of open banking services is still in its infancy, and many banking users have yet to utilize them. In this regard, the lack of relevance of PEOU in adopting open banking-based might be explained by, for example, mobile banking (Munoz-Leiva et al., 2017), where PEOU also plays a minor role. Nevertheless, it is important to highlight that, despite having a limited direct effect, the total impact of PEOU on BI through PU is significant (0.357). This role of PU as a mediating factor of PEOU has already been established in the literature (Pavlou, 2003).

Additionally, our study confirms the emerging hypothesis in the literature (Kesharwani & Singh Bisht, 2012) of the impact of PEOU on PU. Although this relationship is not incorporated in the original TAM or the UTAUT models, our study confirms this point.

Regarding the role of SI, our model confirms the hypothesis of its relevance as an explanatory factor in the adoption of fintech directly and through its impact on the PU. Its total effect on the BI to adopt services based on open banking (0.603) is even more significant than the effect of PU (0.586). The literature is divided on this aspect, as it has been confirmed in some studies (Rosati et al., 2022; Tun-Pin et al., 2019) and rejected in others (Ferdaous & Rahman, 2021; Senyo & Osabutey, 2020).

The results obtained can be better understood in the specific case of services based on open banking due to their innovative nature. So far, many users have not yet had direct experience with this type of service. In this way, as these are new services eminently associated with online banking and mobile banking, feedback from reference persons is an essential element when adopting this type of service by users, both directly (i.e., due to its impact on the BI) and indirectly (i.e., due to its impact on the PU or PEOU).

According to our analysis, INT is the most relevant factor in adopting open banking. The literature supports this aspect of fintech adoption (Singh et al., 2021) and open banking-based services (Chan et al., 2022). The differential contribution of our article is the identification of the impact of INT, not only indirect but also direct (Graužinienė & Kuizinienė, 2021), for the specific case of services based on open banking, being the factor with the highest total weight (0.955). Finally, it is worth comparing our results with those of (Rosati et al., 2022). In our case, we apply a more parsimonious model (extended TAM vs. UTAUT) and analyze the effects of INT instead of Risk, obtaining a significantly higher explanatory power (R2 of 0.85vs. 0.589 in their study).

INT’s critical role is explained eminently by its financial nature. Thus, unlike other technological services, services based on open banking have a remarkable financial component. In fact, their essence is based on the sharing of financial data with third parties.

Therefore, as thoroughly analyzed in the academic literature on fintech (Alalwan et al., 2017; Mondego & Gide, 2018; Patil et al., 2018) and, specifically, (van der Cruijsen, 2020) in the case of services based on financial data sharing, INT is highly relevant both directly and indirectly, to understand the adoption of services based on open banking.

Theoretical and Practical Implications

Theoretical Implications

Our research extends the applicability of the TAM model to services based on open banking. Previous studies also analyzed the adoption of services based on open banking using the TRAM (Sivathanu, 2019) or UTAUT (Chan et al., 2022) models. There was a gap in the literature exploring the applicability of more parsimonious models such as TAM, and this study provides robust knowledge of its applicability. Second, adding two additional variables, INT and SI, significantly increases the model’s explanatory power: The mean of R2 of the previous related studies was .61 compared to an R2 of .85 obtained in our study (Table 9).

Additionally, our study analyzes the interactions between the different constructs of technology adoption. Identifying the importance of INT as a relevant factor in SIN is pertinent to better understand the dynamics in adopting fintech such as open banking. Likewise, the indirect effect of SIN on PEOU and of the latter on PU had not been adequately identified in the previous literature until now.

Practical Implications

From a practical perspective, our research provides numerous actionable insights for all stakeholders in delivering open banking-based services (Supervisors, regulators, financial institutions and potential new entrants). First, open banking aims to promote increased competition in the retail banking market. Based on the results of our study, INT is the main factor in the adoption of services based on open banking. Therefore, policymakers must foster confidence in open banking schemes. This objective can be achieved through a reinforcement of the guarantees of the open banking framework (e.g., publicity and accessibility of the registers of open banking-based service providers, intensification of the supervisory activity on these activities, or an increase of the official communication on the operational procedures of open banking schemes). Second, SIN is a high-impact factor in adopting open banking-based services. From a perspective of SIN as a cognitive process (Graf-Vlachy & Buhtz, 2017), two types of SIN are distinguished: normative and informational. Regarding normative SI, generalizing open banking as a tool to guarantee that clients receive the best products under the best conditions would reinforce the adoption of open banking. Moreover, intensifying public and private communication about the benefits of open banking would strengthen the informative aspect of SI.

As far as private operators are concerned, it is essential to strengthen communication about the usefulness of services based on open banking. The relevance of the perceived utility variable is very high in the BI to adopt services based on open banking. Therefore, marketers must intensify communication about the customer benefits of using these services. These benefits can be made tangible in terms of better prices, more customized products, or simpler processes. It is also essential to reinforce simplicity in adopting this type of service. Thus, although the PEOU does not directly influence the intention to adopt services based on open banking, it is an important variable in PU. Therefore, marketers need to reinforce the positive trade-off between the benefits of open banking-based services and the complexity of using them.

With regard to new entrants, or the so-called third-party providers, they should prioritize combining all the identified variables to promote the adoption of their services. Thus, adoption rates of their services can be improved by deploying actions aimed at increasing confidence in new entrants that provide services based on open banking. This target can be achieved by enhancing transparency of services or by being endorsed by trusted references in the market. Additionally, the increase in viral marketing and social networks could also influence the reinforcement of SIN for the adoption of this type of service. Finally, clear communication reinforcing the ease of use of the new services based on open banking and the tangible benefits for customers would also boost their adoption.

Limitations and Future Directions

This study presents several limitations that should be addressed in subsequent research:

First, the phenomenon of open banking-based services is still emerging. In the case of Spain, despite the PSD2 regulations being implemented for more than 2 years, the services available in the market are still scarce, and an understanding of the service is limited. In our study, despite prior exposure to the service, only 410 of the 553 respondents answered the screening questions correctly. Therefore, this research should be replicated later when there is a more effective implementation of services based on open banking. Second, the BI to adopt services based on open banking can be a good predictor of their adoption. However, it would be appropriate to introduce the BI and the actual use of the services in the model. Third, our approach could be enriched by adding additional variables. Thus, based on the UTAUT model, the incorporation of facilitating conditions could help explain, for example, how a financial app could have a positive impact on the adoption of services based on open banking. Besides traditional technology adoption models, risk has been incorporated into several technology adoption models and could be interesting to include in this analysis. Finally, various services have different propensities for use within the open banking paradigm. For example, the aggregation of account information for a Personal Financial Manager is not the same as a risk assessment based on open banking or a payment initiation service by a third-party provider. Therefore, replicating our analysis for specific open banking applications could help improve our understanding of the variables that explain the adoption of this technology.

Footnotes

Appendices

Acknowledgements

The authors acknowledge Dr. José Luis Arroyo Barrigüete for sharing his experience to improve the structuring and potential impact of this article

Author Contributions

Both authors contributed equally to this work. All authors have read and agreed to the published version of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Approval

Not required, as the data was obtained through anonymized surveys

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.