Abstract

This study analyses the effectiveness of vertical integration for motion pictures’ box office revenues and the moderating effects of environmental uncertainty on China’s film industry, where a market economy was introduced in 2002. We analyzed a sample of 1,824 films released between 2005 and 2016 using a PROCESS model. We found strong evidence that vertical integration positively influenced box office revenues, which were higher under greater environmental uncertainty post reforms than under relative stability. We also found films that (1) had major producers or distributors, (2) were based on intellectual property, (3) belonged to the action or fantasy genre, or (4) featured superstars performed better. This study demonstrates the current operating level of the market economy in China’s film industry and offers a unique, fresh dataset comprising almost all films released in Mainland China and produced by enterprises in Greater China.

Keywords

Introduction

Until 2001, China’s film industry experienced a sustained stagnation; however, when China joined the World Trade Organization (WTO) in 2001, the film industry’s market would need to be more open than before. To meet this mandate, the Chinese government implemented various reform policies to inject market economy characteristics into its industry that also encouraged a rapid growth of the film industry. Additionally, since the beginning of industrial reform, the Chinese government has encouraged vertical integration (VI) among production, distribution, and exhibition to cultivate the domestic industry through a series of regulations such as Principle Opinions on the Further Promotion of the Film Group Formation promulgated in 2001 and Opinions on Accelerating the Development of the Film Industry promulgated in 2004, and various vertically integrated entities have developed. The increased quota for foreign revenue-sharing* mega-productions in 2012 further vitalized this market. In 2018, there were approximately 60,079 total screens in China, the largest number worldwide. Box office revenues that year were CNY 60.9 billion, making 2018 the most successful year in industry history (Daily, 2019). Moreover, as China’s urbanization continues, the number of theaters and filmgoers is rising, which ensures the steady growth of the industry.

Within the industry, however, growth has not been uniform. Most films fail to realize profits during their theatrical runs, and the core industry survives only because of a handful of films that become blockbusters and make hundreds of millions of yuan. Filmmakers run significant risks in this highly uncertain environment and the increasingly open market, requiring them to actively respond to environmental changes to survive and prosper. Cinematic success is highly contingent on making visionary decisions.

VI’s capacity to counter this type of uncertainty has been studied extensively (Coase, 1937; Parc, 2021; Silver & Alpert, 2003; Williamson, 1979). When the government began encouraging VI in 2002 to prepare for the influx of foreign films, it focused on integrating originally independent production, distribution, and exhibition entities to strengthen the domestic market’s competitiveness. As competition in the industry intensified, these enterprises increasingly employed VI strategies. However, systematic management studies on this topic in the Chinese context are scarce.

To fill this research gap, this study addresses the basic research question, “Is a VI strategy more effective in an uncertain environment or a relatively stable market?” It uses an empirical investigation of the effects of VI strategies on China’s film industry. It also analyses the industry at two time points with clearly different environmental uncertainties. Further, it examines a sample of nearly all films released in Mainland China’s cinemas from 2005 to 2016.

This study makes several contributions. First, by conducting comprehensive research on the reforms in the Chinese film industry, this study can provide scholars and industry practitioners with a better understanding of the marketization of the industry. Second, it fills an important gap in the literature pertaining to the effectiveness of VI strategies and the moderating role of environmental uncertainty in the context of the Chinese film industry, and it provides a direct test of the relation between outcomes and strategy. Third, studies on the film industry have largely focused on the U.S. and European markets. The consequences of China’s industrial reform on the Chinese film industry and the strategies and performance of industry participants have rarely been empirically investigated. This study included VI strategies and several control variables to provide empirical evidence on the current operating level of the market economy in the Chinese film industry. Fourth, we built and analyzed a unique and comprehensive dataset instead of relying on disparate, small, and secondary data sources. China’s film industry is still in the development stage, and the market is moving in the direction of more openness. It will therefore be worthwhile to study how the uncertainty, strategies, and strategy effects examined in this study change over time.

China’s Film Industry

The Domestic Film Industry in Crisis

China’s film industry was nationalized in 1949 as a part of a Soviet-style planned economy and state-ownership model (Su, 2014; Yang & Limb, 2018). All activities, from production through exhibition, were conducted, according to government planning, as a tong gou tong xiao (unified purchase and sale).

This complex distribution system delayed distribution and created little revenue for theaters and producers to utilize because the governments at each level received certain percentages of box office revenues. Moreover, production under the planned system was inefficient because the division of labor and specialization were lacking, and the quality of films did not satisfy the consumers. The government’s many attempts to redistribute profits and revitalize film studios before 1993 were merely adjustments made within the confines of the planned economy.

In 1994, China implemented the common foreign approach of revenue-sharing and began importing about 10 foreign mega-productions per year. Foreign films were much more popular than domestic films in China and, in 1995, the government set the limit that more than two-thirds of screened motion pictures had to be domestic films. Despite that mandate, the 10 foreign mega-productions that were imported annually garnered more than 60% of total box office revenues (Shen, 2006). When China joined the WTO in 2001, the quota of imported films was increased to 20, and the domestic film industry was in a critical situation.

Film Industry Reform

To revitalize the film market, which was in a serious recession until 2002, the Chinese government implemented several industry-wide reforms to bring market mechanisms to bear. These efforts were centered on the notion of the yuanxian (theater chain) system, a Chinese government experiment to establish a distributional pathway in the market economy. The idea of the theater chain, like franchise management, was one film enterprise with multiple theaters as investments or under contract (Yang & Limb, 2018). Under that system, the Chinese government reclaimed the distribution rights of the distribution enterprises owned by various lower governments (Ding, 2014). Now a film’s producers and distributors in the theater chain system could directly distribute that film to theater chain exhibitors, simplifying the earlier complex distribution system.

This change established a value chain comprising the production, distribution, and screening aspects of the industry in a market economy with a rational income distribution (which was universally the case in developed countries). The theater chain system destroyed the government’s planned multi-layered distribution model. The theater chain enterprise, located downstream of the industry’s value chain, was the closest link to the theaters. This proximity provided these enterprises with exclusive bargaining power in film distribution. Thus, producers and distributors needed to integrate with the theater chain enterprises.

The government also reformed the industry across all stages of production, distribution, and screening to create freely competitive environments and revitalize its market. First, production was opened to private capital investment in 2002. With respect to screening, the prohibitions against private capital’s participation in the theater business were lifted; in 2002, the Chinese government allowed all domestic capital to participate in building or renovating facilities in China. Finally, regarding distribution, the foreign films that dominated the box office, previously monopolized by the China Film Group Corporation, began to be handled by Huaxia, a newly established state-owned distributor, creating a duopoly with the intent to promote competition. To facilitate the distribution of domestic films, the government permitted capital infusions into the distribution arena in 2003.

Vertically integrated film enterprises started to emerge in response to these government efforts and capital inflows, which strengthened the competitiveness of domestic film enterprises. In February 1999, when WTO membership negotiations were to begin, several state-owned film enterprises merged into the conglomerate China Film Group Corporation, and, by 2008, China had created seven huge state-owned film groups. After the film industry allowed inflows of private capital, many private vertically integrated enterprises developed. For example, Wanda, China’s largest theater chain, participates in production and distribution. Bona Film Group Ltd, historically a distributor, also operates a production business. These film enterprises have vertically structured themselves to encompass production, distribution, and exhibition in various ways ever since they were first encouraged to compete with foreign film enterprises.

In sum, the freedom to invest private capital in the film industry created a foundation for private film enterprises to grow. The reforms of 2002 opened the way for rapid capital infusion, which quickly expanded the state-owned and private vertically integrated film enterprises. Many Chinese film enterprises started using VI strategically to manage the intensity of the competition and the uncertainty of success. The opening of the market and the industrial reforms in response to WTO membership created a market economy for the film industry that had operated for so long within the confines of the planned state-owned monopoly. It also created an environment in which state and private enterprises freely competed. The theater chain system was particularly instrumental to this change because it simplified the distribution process and was considered an essential aspect of the film industry’s market growth (Han, 2018).

Bigger Market and Fiercer Competition: An Institutional Perspective

In 2012, China’s film industry’s revenues surpassed Japan’s by more than CNY 17 billion at the box office, making China the second largest film industry worldwide. The reason for this success was the continuing growth in the number of theaters in China’s rapidly growing cities. However, the most important factor was the increased number of foreign mega-productions, which have always dominated China’s film market; while stimulating industrial growth, these foreign films threaten domestic ones (Yin, 2019).

During President Xi Jinping’s visit to the United States in February 2012, the quota for foreign revenue-sharing mega-productions increased to 34 a year; most of these films were American blockbusters. This increase is considered a major historical event that changed the pattern of China’s film industry (Jia, 2012), mainly because the foreign film quota was extremely important to its marketization. The increased quota directly intensified environmental uncertainty in the industry regarding production, distribution, and exhibition, and filmmakers felt unprecedented external pressure (Ouyang, 2016).

From an institutional theory perspective, by which an “institution” reflects shared rules (e.g., laws, collective understandings, or explicit or tacit agreements; Fligstein, 1996), the increase in foreign revenue-sharing mega-productions created a distinct environment change. The domestic industry had been protected by the government’s import quota system until 2012, and the expansion in foreign revenue-sharing mega-productions after 2012 forced domestic producers to compete in a far freer market.

This institutional change is further evidenced by some recent studies that argue that the increase in the foreign quota in 2012 was an important turning point since the industry’s reforms began in 2002. Y. Zhang (2015) argues, “Since 2012…Chinese films have entered the second stage of market opening and competition ”( p. 1). Lu (2016) similarly claims, “By 2013, the new wave of the film industry reforms had fundamentally changed the industry…and the commercialization of the film industry reached a new level of maturity” (p. 10). These quotes indicate that the institutional logic of the film industry changed from a protected to a freer market because of the increased quota for the foreign revenue-sharing mega-productions. Chinese film industry experts agree that this division of the industry into stages is realistic in terms of co-production, market opening, and the box office annual growth rate (Rao & Li, 2017; Wang et al., 2018).

Additionally, as the ratio of domestic film productions to total number of releases (i.e., the release rate) has increased significantly since 2012 (see Figure 1), individual films are facing even greater uncertainty because more competitors have entered the market. Based on the changes in the competitive environment and experts’ widely shared beliefs (W. R. Scott, 1987, 2005), we classify the period before 2012 as “relatively stable” and the period from 2012 to the present as “uncertain.”

Domestic motion picture release rate (2002

Theoretical Perspectives and Hypotheses

Uncertainty in the Film Industry

The main characteristic of culture-oriented industries such as the film industry is that high levels of uncertainty are routinely present at all points of the value chain (Caves, 2000; Faulkner & Anderson, 1987). It is extremely difficult to plan for complex interactions, and, thus, impossible to anticipate how a film will be processed (Faulkner & Anderson, 1987). Consequently, predicting performance is impossible. When this uncertainty is coupled with high film production costs, the risks regarding film production increase.

The aspect of uncertainty that this study mainly considers is conflicts of interest. Among the film industry’s three sectors (production, distribution, and exhibition; Einav, 2007; Eliashberg et al., 2006; Silver & Alpert, 2003; Squire, 2004), production leads the industry. Producers use distributors to exhibit their films on large screens. Distributors promote these films through various channels. When a producer and a distributor are vertically integrated, the distributor does its best to promote the focal film to maximize revenue, which is completely consistent with the interests of the producer. Otherwise, the distributor might concentrate on other films which would compel the producer to make a specific effort to contract with the distributor and monitor the distributor’s contractual compliance. Distribution activities link production to the exhibition and influence the extent of a film’s financial success.

Exhibitors try to maximize box office revenue and generate additional revenue from related sources, such as concession stand sales. Gil and Hartmann (2007) explain that while distributors and producers only profit from ticket sales, exhibitors also profit from secondary revenues, such as food and drink sales. To increase their numbers of customers (which increases food and drink profits), exhibitors lower the prices of tickets, which undermines distributors’ and producers’ profits. Exhibitors’ secondary sources of profit may lead them to make different decisions than distributors would regarding when to exhibit a particular film. Because exhibitors’ and distributors’ incentives may not align, exhibitors usually welcome new releases, whereas distributors may not. Thus, conflicts of interest add significant uncertainty to the film industry. Such conflicts among the three sectors mean that the terms of cooperative and revenue-sharing agreements must be contracted. The interacting enterprises should monitor each other for contractual compliance, which incurs the costs described by transaction economics (Raut et al., 2008).

Uncertainty and the VI Strategy

In general, uncertainty may dramatically constrain enterprises’ strategic decisions by reducing the accuracy of decision-making, which may negatively influence organizational performance and survival(Khan et al., 2020; Milliken, 1987). Consequently, enterprises take various strategic steps to reduce their risks of uncertainty. VI has been studied as a strategy for mitigating this uncertainty(Coase, 1937; Krickx, 2000; Parc, 2021; Silver & Alpert, 2003; Williamson, 1979). To avoid uncertainty, organizations choose to economize transaction costs by vertically integrating their transactions through hierarchical and governance-based organizations (Williamson, 1975, 1979, 1993). Some empirical studies based on the perspective of transaction cost economics have found relationships between uncertainty and VI (Heide & John, 1990; Helfat & Teece, 1987; John & Weitz, 1988).

Economics research suggests that VI may help reduce transaction costs or contractual frictions(Coase, 1937; Guan & Rehme, 2012; Lieberman, 1991; Williamson, 1979); moderate demand-side uncertainties and risk aversion(Arrow, 1975; Matsui, 2012; Riordan & Sappington, 1987); and avoid or reduce the scope of moral hazard, principal-agent, and double marginalization problems (Spengler, 1950). Negro and Sorenson (2006) demonstrate that VI changes competitive dynamics by: (1) buffering vertically integrated enterprises from environmental dependence and (2) intensifying competition among non-vertically integrated organizations.

Of particular relevance to the present study, Yu and Jung (2021) examined the Korean movie industry and found that when an integrated exhibitor screens its own integrated distributor’s movie, the movie tends to get more screenings and more favorable screening times in the opening week. Corts (2001) and A. Scott (2004) examined the transaction cost problem in film production and distribution and found that although the vertically integrated production subsidiaries of the studios internalize the external effects of competition, bilateral contracts in vertical relationships create inefficiencies, and a vertically integrated production enterprise tends to be more efficient. Gil and Hartmann (2007) found that when vertically integrated distributors distribute films in their own theaters, they not only save the costs of negotiating a contract but also avoid ex-post opportunistic behaviors. Fu (2009) compared the effects of VI between distributors and exhibitors and found that the vertical efficiencies that accrue from exhibiting VI films reduce screen availability for non-VI films. Thus, previous studies on film industries in some developed countries suggest that VI may increase the predictability and stability of film production by increasing the extent of cooperation among the involved organizations(Fu, 2009; Gil, 2008; Mezias & Mezias, 2000; Yu & Jung, 2021). We, therefore, set forth our first hypothesis.

Vertically integrated enterprises balance incentives better than non-vertically integrated enterprises do using contracts (Gil, 2008; Williamson, 1979); when environments are more uncertain, more contingencies can disrupt contractual relationships (Argyres & Mayer, 2007; Williamson, 1975), which, in turn, may lower the effectiveness of non-VI strategies. In other words, VI strategies have comparative advantages over non-VI strategies, particularly in the context of high demand uncertainties. Gil (2008) analyzed the effects of VI on the runtime of a film in the Spanish film industry and found that vertically integrated enterprises have a comparative advantage because they are better able to balance incentives than non-vertically integrated distributors do. Moreover, this effect tends to be stronger for films with relatively high demand uncertainty. Thus, VI benefits may be lower for uncertain films but may increase for films that are more uncertain. To verify the moderating effect of environmental uncertainty, we establish the following hypothesis.

Materials and Methods

Sampling and Data Collection

The data used for this study comprise all films released in Mainland China and produced in Greater China (Mainland China, Hong Kong, Macau, and Taiwan) from 2005 to 2016 that earned at least CNY 10,000. Of the 1,945 films that made the list, 121 were dropped from the dataset owing to missing data for some variables, and 1,824 valid films were analyzed. The film list was obtained from 58921.com and maoyan.com.

Variables

Dependent Variable: Film Performance

Following previous research (Basuroy et al., 2003; Hennig-Thurau et al., 2007; Litman & Kohl, 1989; Ravid, 1999), this study uses domestic box office sales which are the representative performance in the film industry, to measure film performance. Specifically, we use the actual revenues earned during a film’s release period in Mainland China (adjusted for inflation). To satisfy the assumption of a normal distribution, logarithmic values are computed and analyzed. The information on domestic box office sales was obtained from www.cbooo.cn.

Moderator: Environmental Uncertainty

The key relationship being analyzed is the influence of the extent of a film’s VI on its performance (

Main Independent Variable: Extent of VI

The main independent variable is the extent of VI achieved by the film’s producer, distributor, and exhibitor. Harrigan (1986) argues that VI strategies reflect combinations of decisions regarding whether an enterprise should provide goods and services in-house through its business units or purchase them externally. These decisions concern how much of a particular good or service to transfer in-house and how far backward or forward to integrate in a vertical chain of activities (number of processing stages). Enterprises combine the dimensions that they determine to be the most appropriate ways to achieve their strategic goals. This study measures the extent to which a film’s producer vertically integrates forward (to distribution and exhibition).

To categorize the extent of a film’s VI strategy into five groups, we first determine whether the film’s producer and distributor are the same enterprise, and then whether the distributor is vertically integrated with an exhibitor that is a theater chain. If the film’s distributor is the same as the producer and vertically integrated with a theater chain, then the VI strategy is at the highest level and the film is assigned five points (“PDT”). When a film’s producer and distributor are the same but not integrated with a chain and, instead, work with other distributors that own theater chains, the VI strategy is at the second highest level, and the film is assigned four points (“PD/DT”). When a film has the same producer and distributor but does not have a theater chain and does not work with other distributors that own theater chains, the strategy is the third highest level, and the film is assigned three points (“PD/T”). When the producer and distributor are not the same enterprise, but the distributor has a theater chain, the VI strategy is the fourth highest and the film is assigned two points (“P/DT”). The lowest VI level is when the producer and distributor are not the same enterprise and neither enterprise has a theater chain (one point, “P/D/T”). The information on producers and distributors was obtained from www.mtime.com, www.cbooo.cn, and the focal film’s poster. Figure 2 illustrates the distinctions among the five VI strategy types, and Figure 3 shows the distributions of the five VI strategies across films during T1 and T2.

Typology of the vertical integration strategy levels of the films (n = 1,824).

Percentage distributions of the five vertical integration strategies across films during T1 and T2 (n = 1,824).

Control Variables

Many other factors influence box office sales, and we therefore analyze some variables that have shown significant effects in previous studies.

Major Producer/Distributor

Because the status of the producers and distributors is important to a film’s performance (box office revenue), as highlighted by previous studies (Chen, 2002; Corts, 2001; Gemser et al., 2007; Shugan & Swait, 2000), an indicator of that status as “major” is included in the analysis. We included whether the focal film’s producer and distributor are major firms as individual control variables by checking their market shares in the year before the focal film’s release. We created dummy variables that indicate that the producer and distributor are major if they ranked in the top 10 (otherwise, they are defined as non-major). The information on the market shares of the producers and distributors were obtained from annual reports on the Chinese film industry released by EntGroup.

State-Ownership Composition of the Producer/Distributor

Because culture plays a vital role in maintaining China’s one-party system, the extent of state-ownership of a film’s producer and distributor influences the film’s performance. Thus, we control for the effects of state-ownership of the producer and the distributor separately. If the producer or distributor had no state-ownership (private ownership), the dummy variable was coded “0.” If it was co-owned by the state and private firms, it was coded “1,” and if it was solely owned by the state, it was coded “2.” The information for these two variables was obtained from the websites of the focal film’s producer and distributor and online searches.

IP

The term intellectual property (IP) is now frequently used by the Chinese film and television industry. An IP film is one derived from creative products with IP rights, such as novels and dramas. IP has previously been found to influence box office revenue (Basuroy & Chatterjee, 2008; Prag & Casavant, 1994; Ravid, 1999), and a measure of IP is included in the analysis to control for its effects on the dependent variable. We indicated whether films were adapted or derived from a novel, drama, webtoon, play, previous film, video game, or myth, or were intended as a sequel, using a dummy variable defined by 1 = IP film and 0 = otherwise. The information to create this variable was obtained from the focal film’s poster and online searches.

Co-Production

Li (2017) recently found that most films co-produced with foreign partners are created solely to make money, and large productions with popular actors are standard in those films. Since 2002, co-produced films have dominated China’s box office (Rao & Li, 2017). Thus, we controlled for whether the focal film was cooperatively produced by producers from two or more countries. If it was a co-produced film, the dummy variable was coded “1,” and “0” otherwise. This information was obtained from www.mtime.com and www.cbooo.cn.

Genre

Some previous studies argue that a film’s genre has a complex influence on box office revenue (DeVany, 2003; Litman & Kohl, 1989; Simonoff & Sparrow, 2000; Wallace et al., 1993; Walls & DeVany, 2014). Based on previous research, we categorized the films as romance, comedy, action, horror, animation, war, fantasy, drama, musical/history/documentary, crime, or other. As action and fantasy films perform the best, we controlled for the effects of the genre by merging action and fantasy films and coding them “1,” and others, “0.” The information on genre was obtained from www.cbooo.cn.

Presence of a Superstar

Deng (2011) proposes that one characteristic of Chinese blockbuster films is the presence of high-profile, extremely successful actors (“superstars”). Many previous studies on box office success include a superstar variable to account for this factor (Ainslie et al., 2005; Basuroy et al., 2003; Chang & Ki, 2005; Elberse, 2007; Hennig-Thurau et al., 2013; Litman & Kohl, 1989; Ravid, 1999; Wallace et al., 1993). In this study, we controlled for the effects of having at least one superstar among the two leading actors in the cast. Because of the lengthy time span of the data used in this study, it was difficult to find a consistent and objective index to measure the star power of the actors. Thus, we developed a measure based on multiple coders’ judgments. Three graduate students with experience in the Chinese film industry research coded whether the two leading actors starring in every focal film were superstars. An actor is identified as a superstar if at least two of the coders agreed. If at least one of the two leading actors was a superstar, it was coded “1,” and “0” otherwise. The information used to determine superstar status was obtained from the focal film’s poster.

Annual Market Size

To control for year-specific effects, the annual market size (box office revenue) was used as a proxy variable. Recently, film performance has been increasing rapidly with the fast growth of the Chinese film industry. Consequently, although uncertainty is relatively high during T2, film performance tends to be higher than in T1. Thus, there may be misspecifications between environmental uncertainty and film performance. Because this is a 12-year study, if the year is included only as a dummy variable, the number of exogenous variables that need to be controlled increases sharply, as do the number of required observations (Breaugh, 2006). To overcome this problem, we used market size as a control variable that influences environmental uncertainty but does not directly affect film performance (Kerlinger & Lee, 2000; Rosenberg, 1968). The annual market size (2005–2016) data are obtained from Yin (2019, p. 485).

Analytical Methods

The analysis is performed using the PROCESS macro with bias-corrected bootstrapping and 95% confidence intervals (CI) created by Hayes (2013) to test the hypotheses. PROCESS uses a bootstrapping method that has previously demonstrated excellent power compared to assuming a normal distribution. The ordinary least squares method, which has a low risk of error, is used to estimate the regression coefficients and generate the p-values of the t-distributions. PROCESS automatically calculates changes in the coefficient of determination (ΔR2), F-values, and p-values, meaning that manually calculating the change in the model’s explanatory power in a hierarchical regression analysis is unnecessary, and has the advantage of providing additional analyses to help interpret the interactions.

Results

PROCESS Estimation Results

Table 1 presents the descriptive statistics of all the variables in the analysis. Film performance is positively correlated with the extent of VI, having a major producer, having a major distributor, IP, co-production, genre, and the presence of a superstar, and it is not significantly correlated with the state-ownership composition of the producer or the distributor.

Descriptive Statistics (n = 1,824).

1 = (ln)Film performance, 2 = environmental uncertainty, 3 = extent of VI, 4 = major producer, 5 = major distributor, 6 = state-ownership composition of producer, 7 = state-ownership composition of distributor, 8 = IP, 9 = co-production, 10 = genre, 11 = presence of superstar, and 12 = annual market size.

Mean.

Standard deviation (the details of 1,824 films are available upon request).

p < .05. **p < .01. ***p < .001.

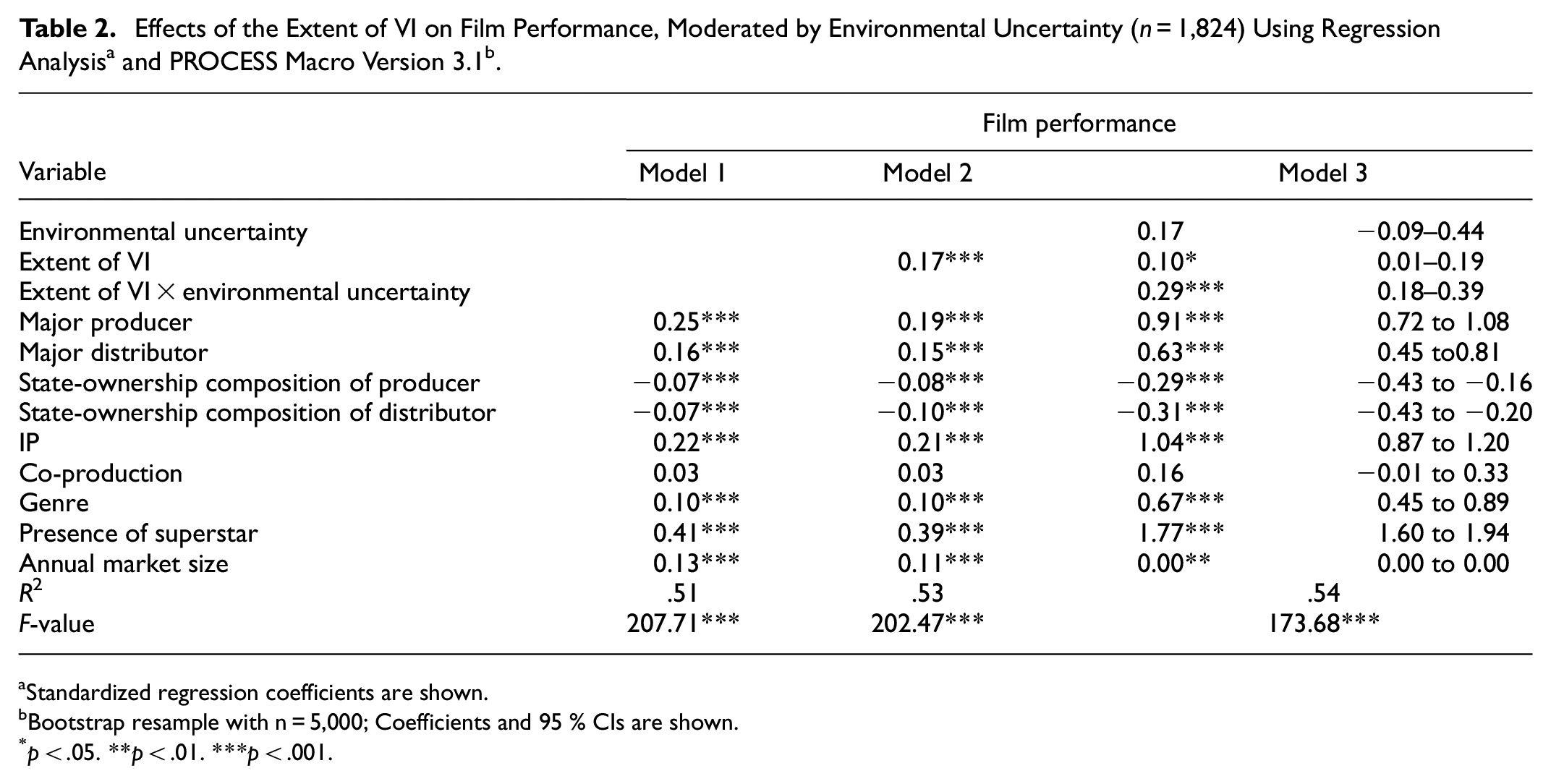

Table 2 summarizes the results of testing the two hypotheses. Model 1 shows the results of the basic regression with the control variables, which together explain 51% of the variance in performance. Model 2 introduces the extent of VI as the independent variable and shows that it significantly influences film performance, supporting

Standardized regression coefficients are shown.

Bootstrap resample with n = 5,000; Coefficients and 95 % CIs are shown.

p < .05. **p < .01. ***p < .001.

Table 3 provides the results of the conditional moderation analysis, which shows that the effect of the extent of VI on film performance depends on environmental uncertainty. This effect is statistically significant during T1 (effect = 0.10) and T2 (effect = 0.38). Notably, the extent of VI’s effect is stronger during T2 than during T1.

Conditional Direct Effects of T1 and T2 on the Relationship of the Extent of VI With Film Performance (n = 1,824).

Note. SE = standard error; CI = confidence interval.

p < .05. ***p < .001.

To further interpret the conditional effects of environmental uncertainty on the relationship between the extent of VI and film performance, we performed a slope analysis. Figure 4 illustrates that the slope of the conditional effect is steeper during T2 than during T1, meaning that the influence of the extent of VI on film performance is stronger during the period of uncertainty (relatively competitive and unpredictable) than during that of stability (less competition and unpredictability), supporting

Moderating effect of environmental uncertainty on the relationship between the extent of vertical integration and film performance (n = 1,824).

Conclusion

This study analyzed the effects of increasing VI strategies on film performance and the moderating effect of environmental uncertainty on that relationship in China’s film industry, which adopted market reforms in 2002. Our results indicate that VI strategies had a positive influence, suggesting that the more integrated a film’s production, distribution, and exhibition, the better its box office performance. The analysis further assessed the moderating effect of environmental uncertainty because the industry experienced significant changes in 2012 when the increased quota of revenue-sharing mega-production foreign films created anxiety about the domestic film industry’s future. The dire predictions did not materialize, and films that were produced, distributed, and exhibited using VI strategies have become more competitive.

A sample of 1,824 films that included nearly all films released in Mainland China and produced in Greater China between 2005 and 2016 was used to test the hypotheses. As deregulations began in 2002, state-owned film enterprises, which had been insulated from competition in the planned economy, as well as private film enterprises, faced heightened market competition. The market competition intensified in all aspects of production, distribution, and exhibition after 2012, exacerbating the inherent uncertainty of the film industry (Lu, 2016; Ouyang, 2016; Y. Zhang, 2015). Controlling for the effects of several variables, the analysis revealed that the extent of the VI strategy influenced film performance positively, and the effect was stronger during an uncertain environment than during a relatively stable environment. The empirical results regarding the control variables suggest that films that have a major producer or distributor, are from an IP, are in the action or fantasy genre, or include a superstar perform better. However, state-ownership of producers and distributors influenced performance negatively, indicating that, as the Chinese film industry became freer, government intervention was unable to produce positive effects and was even detrimental.

The films released with the first and second strongest VI strategies performed well despite their small shares in T1 and T2, suggesting significant effects of a complete VI of production, distribution, and exhibition, whether within one enterprise or through an intermediary distributor. Managers should be aware that producers can benefit by distributing their films independently in intensely competitive environments and, if possible, collaborating with distributors who own theater chains. Privately-owned production or distribution is more successful when partnering with a private rather than with a state-owned enterprise.

This study has some limitations to consider when interpreting and extrapolating the results, especially since its findings are limited to China’s film industry. Further, although the findings suggest that VI has a positive effect on film performance, many scholars argue that employing a VI strategy may create problems by undermining flexibility and thereby making the organization huge and rigid (e.g., Lampel et al., 2000). Thus, studies of other industries are needed to confirm the generalizability of this study’s results. Second, the definition of the superstar variable is somewhat subjective because the lengthy timespan of the data used in this study makes it difficult to identify a consistent and objective index with which to measure star power. Third, in addition to the control variables that are included, there are many other barriers that can bring about serious effects on the box office of films such as screen quota, censorship, uncertain (much earlier or much later) release dates, “stacked-up” or “bunched-up” releases, and blackout periods. However, all of these were not recorded formally making it impossible to control them in this study.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.