Abstract

Recruiting professionals in tax consultancy and auditing is becoming increasingly difficult in Germany and Austria. This study analyzes the attractive factors of a profession, specifically the tax consultancy and auditing profession, based on a survey of students (n = 225) and practitioners (n = 148) in a German-speaking setting. We find that the most attractive factors for tax consultancy and auditing are different company insights and consulting activities. Career opportunities and auditing activities are perceived as incentives to enter the auditing profession. Knowledge obtained during studies is perceived as less satisfactory for students compared to practitioners who assess it as good in retrospect. Students from different regions valued the tasks differently, which implies that strategies must be adapted to attract students. The number of accounting courses and internships significantly influenced career entry for both professions. Thus, higher education institutions are responsible for making professions more appealing to students.

Introduction

Although a continuously high percentage of students are enrolled in economics, social sciences, and law (e.g., Eurostat, 2016; EY, 2020b), a career in tax consultancy and auditing seems less attractive. This leads to a decrease in the number of professional aspirants and a higher staff turnover rate. Our research expands the literature on the attractiveness of the accounting profession by examining the insights provided by 148 practitioners and 225 students using a multi-perspective approach. As accounting can be divided into several fields (e.g., financial, management, audit, and tax), a decrease in professional newcomers is observed in the highly regulated tax consultancy and auditing profession, and has already been investigated in specific parts of Europe, the US, and Australia (e.g., Detzen et al., 2021; Jackling & Natoli, 2015; Madsen, 2015; Paguio & Jackling, 2015; Tan & Laswad, 2006). Studies in the last two decades focusing on Germany and Austria have revealed a high demand for young professionals in tax consultancy and auditing (Accountancy Europe, 2017; Bravidor et al., 2016; Guldner, 2020; KPMG Austria, 2019; Luttermann, 2017; Velte, 2020).

We analyzed the factors of professional life that are specifically attractive to students and professionals to gain a better understanding of the perceived attractiveness of both professions and the role of higher education in this context. The chosen survey environments of Germany (i.e., Bavaria) and Austria (i.e., Tyrol) include two regions with the same cultural background (e.g., values, language, history) owing to geographical proximity but have regional differences regarding the availability of different career opportunities in both professions. According to Mastrolia and Willits (2013), economic conditions highly influence future employees and should be considered when investigating occupational possibilities. Bavaria offers multiple job and career opportunities in tax consultancy, auditing, and accounting (larger firms and salaries). The situation in Tyrol differs, as the local economy is mainly characterized by smaller structures (smaller companies) that affect career opportunities and salary levels. Thus, our sample enabled us to consider regional differences in investigating job attractiveness in specific areas of both professions.

In addition to economic factors, prior literature identified three important areas of concern. First, stereotyping of the accountancy profession can lead to students not considering it a viable profession. One reason for the (mainly negative) stigmatism is the public misunderstanding of the tasks of a tax consultant, especially of an auditor. Tax consultancy focuses on numbers and calculations, mathematics, and spreadsheets. Soft skills are associated less with this profession but are becoming increasingly important (Dolce et al., 2020). Public opinion on the audit of financial statements is more exhaustive than it actually is. Previous studies suggest that audit education may support the closure of the audit expectations gap (Fulop et al., 2019; Levy, 2017). The expectation gap comprises deviations of expectations from reality regarding the audit profession. The German Institute of Accountants (Institut deutscher Wirtschaftsprüfer [IDW], 2020) found that the lack of young professionals does not lie in the unattractiveness of the profession but in a lack of awareness of the associated tasks. Following the expectation gap theory, graduates may not assess the accounting profession as attractive and, therefore, do not start an accounting career.

Second, if stigmatism prevents students from considering this profession as their initial choice, study programs may also be perceived as less attractive. Thus, initial accounting courses are vital for raising interest and attracting future professionals. Knowledge of the role of higher education in the perceived attractiveness of a profession could help reduce the (negative) stigmatism of the accounting profession. This knowledge might help reduce the existing expectation gap and make the profession more attractive. Therefore, young professionals might be keen to be a part of the social group of “accountants” and, following social identity theory (e.g., Bamber & Iyer, 2002; Mael & Ashforth, 1992), the attractiveness of the profession increases.

Third, the turnover rate of young professionals within the accounting sector is high, which may lead to loss of expertise and trust, loss of clients, and an increase in personnel costs for further recruitment and training. In recent years, the number of young professionals working in accounting and audit companies has significantly decreased from 5 to 3 years. Previous research shows that a high staff turnover rate in companies is common, with a 15% to 28% annual turnover rate, especially in larger audit firms (Accountancy Europe, 2017; KPMG Austria, 2019). Steps to improve the awareness and perceived attractiveness of both professions to address the demands of future professionals have already been undertaken (e.g., Handelsblatt, 2008; Institut Österreichischer Wirtschaftsprüfer, 2019; Kammer der Wirtschaftstreuhänder, 2015; Schulte, 2019).

We built on that and conducted a survey to gain insights into identifying attributes that make a profession generally attractive, and the tax consultancy and auditing professions in particular. We investigate the catchment area of bachelor’s and master’s programs performed at Leopold-Franzens-University Innsbruck (University of Innsbruck) that involves parts of Tyrol (Austria), Southern Bavaria (Germany), and South Tyrol (Italy); and the Friedrich-Alexander-University Nuremberg (University of Nuremberg), which encompasses parts of Southern Bavaria (Germany). This study investigates the expectations of students concerning their future profession, students’ perceptions of the attractiveness of both professions, the occupational factors perceived as attractive among students and practitioners, and whether the demands of students and practitioners differ. The results shed light on the lack of interest in these two professions in specific German-speaking areas.

Our results in a cross-European setting show regional differences, implying that different marketing strategies should be considered when recruiting young professionals. Although these are roughly similar study programs, local differences regarding the preferences of the two professions exist: students studying in Bavaria (Germany) prefer tax consultancy but value all tasks concerning both professions moderately. Students studying in Tyrol (Austria) favor the profession of an auditor but value the tasks in both professions comparatively higher. Contrastingly, the level of the study program (master’s or bachelor’s) had no impact on the perceived attractiveness of a profession. However, passing an internship and more accounting courses positively affect the probability of considering a career start in both professions.

Our study contributes to the literature by extending existing studies on recruiting young professionals from both professions (EY, 2020b; Johnson, 2014; McKnight & Wright, 2011). These studies with national foci suggest conducting further studies on regional differences concerning relevant skills and measures to attract students to both professions. To address the potential gap between students’ expectations and professional reality, we included the perceptions of both students and practitioners. Prior studies mainly investigated the perceptions and comparisons of students studying in diverse years (e.g., Ahmed et al., 1997; Ali et al., 2016; Mauldin et al., 2000; Tan & Laswad, 2006). To our knowledge, this is the first study to use a multi-perspective approach to investigate the perceived attractiveness of both professions and the role of higher education in cross-European settings.

This paper is organized as follows. The literature review in Section 2 addresses factors describing the attractiveness of both professions, provides a theoretical background, and derives the research hypotheses. Section 3 describes the research design and method. Section 4 presents the results. The discussion is presented in Section 5. Section 6 concludes.

Student’s Perception on the Attractiveness of the Tax Consultancy and Auditing Profession

As we investigated students’ opinions as one group (with a majority of students being in their twenties), we refer to studies that popularly label people born after 1980, such as Millennials and Generation Y, and people born after 1997 (Generation Z). The differences between Generation Y and Z and prior generations result from the notably changed attitudes regarding occupational and environmental matters, changing lifestyles owing to rapid technical improvements, globalization, and increasing diversity open space for interesting new investigations (Ng et al., 2010; Tiron-Tudor et al., 2019). We stick to the term “students” instead of millennials considering other popular designations.

Theoretical Considerations

The underlying theoretical considerations for this study conflate social identity theory with expectation gap theory. Social identity theory (Ashforth et al., 2008; Mael & Ashforth, 1992) combined with self-categorization theory (Hogg & Terry, 2000; Tajfel & Turner, 1986) outlines how being a member of a group affects self-perception. Expectation gap theory refers to the gap between the skills employers require and educators offer students (Asonitou & Hassall, 2019; Edeigba, 2022). Mael and Ashforth (1992) define professional identification as “the extent to which an individual defines himself according to the work he performs and according to the characteristics generally attributed to the people who perform that type of work” (p. 106), According to this definition, a group can be an organization that includes the whole entity, department, or a team (Hogg & Terry, 2000; van Knippenberg, 2000). Social identity theory is regularly used in accounting research to analyze various settings, such as the conflict between organizational and professional identity (e.g., Bamber & Iyer, 2002; Garcia-Faliéres & Herrbach, 2014), (interorganizational) prestige (e.g., Hiller et al., 2014), the design of incentive and information systems (Heinle et al., 2012), and the role of identity in management accounting change (Taylor & Scapens, 2016). Suchman (1995) found that the career expectations of millennials comprises system encompassing norms, values, and beliefs that characterize the members of both professions. For example, future tax consultants or auditors are attracted by the strict structure and order, the mathematical focus, or the variety of laws and regulations; however, they may find that mathematical skills are not the most important accounting skill, laws change rapidly, and the strict order may be subject to time pressure in busy seasons. Consequently, if a student perceives that the characteristics associated with tax advisers and auditors are not socially acceptable, this student will not aim to belong to the group or start a career in this sector.

According to the social identity theory, students’ professional identification is higher if the tax adviser and/or auditing professions represent attributes students feel associated with. Consequnetly, if the perception does not correspond to reality owing to stigmatization, then the tax consultancy and audit profession may lose new talent (Levy, 2017; Richardson et al., 2015). Increasing professional identification is important for the auditing and tax advisory profession as it might reduce the staff turnover rate and increase staff loyalty (Bamber & Iyer, 2002). This study seeks to analyze and compare different attributes determining daily business in the auditing and tax consultancy profession and those that are assessed to determine a very attractive profession. Therefore, we assume that a smaller difference in assessment between the most attractive attributes in general and the (auditing and tax consultancy) professions’ most important attributes indicates a higher social identification with the profession.

If future professionals are attracted to the profession because of their positive perception of the “typical” characteristics (Tan & Laswad, 2006), there is a risk of an expectation gap between future professionals’ perceptions and reality. Because this study compares expectations and the assessments of various factors describing properties of the respective professions from the different perspectives of students and practitioners, we address a question closely related to the audit expectation gap.

Expectation gap theory is usually applied to explain the gap between the tasks an auditor must conduct and the stakeholders’ imagination of these tasks (Quick, 2020); however, also appears as the expectation-performance gap in accounting education (e.g., Asonitou & Hassall, 2019; Bui & Porter, 2010; Fulop et al., 2019; Jackling & De Lange, 2009; Maali & Al-Attar, 2020; Webb & Chaffer, 2016). Asonitou and Hassall (2019) show for Greece, that accounting education does not meet the needs of accounting professionals, and researchers have attempted to explore different combinations of stakeholders’ perceptions of the most important technical and generic skills to be delivered. Fulop et al. (2019) found that the audit expectation gap can be influenced by education as it improves students’ awareness. They show that stakeholders are not expected to be conscious of the auditor’s tasks when accounting students sometimes show a lack of fundamental knowledge and expertise. They suggest focusing on improving audit education rather than continuously improving audit standards to avoid financial scandals. Webb and Chaffer (2016) highlighted the importance of graduate employability and proper accounting education. They showed that prior research found that only 55% of employers were satisfied with the wider generic skills demonstrated by graduates. Conversely, Edeigba (2022) shows that for New Zealand, employers are quite satisfied with a broad range of technical accounting (e.g., financial and managerial accounting) and generic skills, but a gap is identified between employers’ expectations regarding auditing and tax accounting skills. The German IDW (2020) found that the unattractiveness of the accounting profession is more an issue of graduates’ expectations not being met than professional activities. Hence, reducing the gap between graduates’ expectations and professional reality might increase the attractiveness of auditing and tax consulting professions.

These theoretical frameworks are linked. Through the existing expectation gap, students may not identify themselves as part of the auditing and/or tax adviser profession as a potential social identity group, and therefore do not consider entering the professions. Overall, these theoretical concepts help explain whether the lack of interest in the investigated professions is attributable to different expectations (and the existence of an expectation gap) or which factors limit the attractiveness of the jobs in case of homogenous expectations.

Students’ Occupational Desires

Students seem to not seek commitment to work at an early stage of their career, and their personal lives should not be sacrificed. The tax consultancy, and especially the audit profession, have been traditionally understood as implying demanding and stressful working times, strict deadlines, busy seasons, and peak periods, continuously changing laws and regulations, rising demands from clients, quality controls, and frequent work trips; thus, they are not considered attractive professions (Bunget et al., 2019; Church, 2014; Jones et al., 2010; Tiron-Tudor et al., 2019). Although both professions have been perceived as boring and uninspiring professions operating “only” with work sheets, pencils, and erasers, they have transformed into professions conducted in a complex business environment continuously changing owing to globalization and digitalization. The requirements of these professions have changed. Technology decreases the time required for manual, repetitive activities, and opens space for accountants to add value to the firm through superior decision support (Aldredge et al., 2021; Cory & Pruske, 2012; Tan & Laswad, 2018).

Studies in the UK (Terjesen et al., 2007) and Belgium (Dries et al., 2008) indicate that students’ expectations and career goals are unrealistic, disconnected concerning workload and reward and “supersized.” Thus, attitudes concerning expectations of an occupation are assumed to differ between practitioners and students. PwC (2013) found that the working desires of “millennial employees” and practitioners differ but to a manageable extent. It revealed that millennials who were committed to hard work tended to focus on flexibility and working hours. Millennials prefer personal conversations in addition to communicating through technological devices and place a high value on work–life balance. Importantly, millennials’ attitudes are not globally unique, and significant conformity is visible among the USA, Canada, and Western Europe; however, regional differences occur.

Dahlmanns (2014) found that making a valuable contribution is key when choosing a profession, followed by flexible, family friendly working hours, higher scope for self-expression, and self-organization. Additionally, challenging activities and good remuneration are considered attractive. Durocher et al. (2016) emphasized that travel activities and teamwork are perceived as highly important by millennials. A survey in Austria found that starting salary, diversified activities, and salary development are the three most attractive factors assessed by students when considering a profession. However, the perception of “attractive starting salary” varies widely depending on the company a student aims to work for. Thus, a company’s marketing strategies are a key factor in attracting young professionals (Hauser & Loder-Neuhold, 2021). In Germany, the most important aspects of the future profession are job safety, salary development, and compatibility between family and work (Avantgarde Experts, 2019; EY, 2020b; Kötter, 2010). Career opportunities are assessed as less important (EY, 2020b).

Project-related working methods, job-specific skills, and interesting activities are considered specific attributable factors to the accounting profession in the field of tax consulting and auditing (International Federation of Accountants—International Accounting Education Standards Board [IFAC], 2019). Thus, these factors were also considered within the analysis of factors that describe the attractiveness of a profession in general. The factors used to evaluate a profession’s attractiveness are summarized in Table 1.

Factors: Profession’s Attractiveness in General.

Regarding the perceived attractiveness of a profession in general, we expected no differences between the two groups of students (Innsbruck & Nuremberg), as they are part of the same generation, with similarities in cultural background and focus on their study programs. We formulated the following hypotheses to account for perceptions of the perceived attractiveness of a profession in general (Table B1 in Appendix B contains a summary of all hypotheses):

H1: The perceived attractiveness of professional factors, in general, is assessed similarly by both student groups.

To determine whether there are differences in what students and practitioners generally assess as attractive, we formulated H2. As cultural background and educational focus are the same, we do not expect differences between students’ and professionals’ perceptions.

H2: The perceived attractiveness of professional factors, in general, is assessed similarly by students and practitioners.

Important Job-Specific Tasks

Understanding how to attract students to certain occupations is a necessity for any profession; thus, the accounting profession cannot ignore the changes in expectations of future employees. Accounting firms are already making efforts to make working tasks more attractive to millennials. This implies a competitive risk if a company disregards the joint influence of millennials on the accounting profession (Durocher et al., 2016).

International Education Standard (IES) 3 (revised) showed that the profession requires a variety of skills. Nevertheless, specific tasks must be performed within the tax consultancy and audit working environment. The IFAC (2019) released a list of professional skills essential for the accounting profession (IES 3, revised). Focusing on both professions, we identified as most relevant factors “project-related working method,”“job-specific skills,”“diversified and interesting activities,”“consulting and auditing activities,” and “working with accounting standards” (IFAC, 2019). These skills are crucial for both professions, as tax consultants and auditors interact to play an important role in providing a functioning economy, effective tax systems, business advisory, and ethical issues. An auditor’s expertise influences tax systems, and a tax consultant’s knowledge affects the preparation of a financial statement (Guthrie, 2014).

We measured diversity using two items—“diversified activities” and “different company insights”—as different company insights inherently include diversity. According to Jackling and Natoli (2015) and Paguio and Jackling (2015), teamwork is in high demand among practitioners; however, young professionals do not execute it efficiently to satisfy their employers. Buchheit et al. (2016) investigated the intensive workload within the accounting profession and its effects on professionals. These attributes were emphasized in the study by Elam and Mendez (2010). Another issue is that the quota to pass the exam to be appointed as a tax consultant or auditor is lower than 50% and is therefore considered an obstacle (Braun et al., 2014; Friedrich, 2017; Schulte, 2019). We analyzed how participants classified their willingness to pass the state examinations.

Focusing on Germany, Tiberius and Hirth (2019) found that the most interesting factors for students to become auditors are income and reputation, whereas reputation suffered owing to auditing scandals and audit fees is under pressure, possibly leading to reduced remuneration. In Austria, salary is as important as diversified activities, professional training, and development, which seem to fit both professions (Hauser & Loder-Neuhold, 2021). While the starting salary is low compared to other professions, salary development is quite good in the accounting profession. Accounting firms mainly point out that the low starting salary is owing to the intense and costly training that young professionals receive in their corporations. Additionally, audit employees seem to agree to accept lower starting salaries but expect higher future benefits (Hammami et al., 2020; Hoopes et al., 2018). Furthermore, it is necessary to consider the different environments in which the various participants are working or will work. Although a lack of young professionals exists in both Austria and Germany, career possibilities differ concerning specific job requirements. In the southern part of Germany, for example, larger Big 4 accounting branch offices offer more positions with a focus on accounting and auditing skills for larger clients. EY (2020a) revealed that students in Germany are willing to move to explore professional possibilities, and Bavaria is their favorite location. In Tyrol, the branch offices are smaller and therefore provide positions with different requirements, considering the needs of smaller clients. Owing to the specific location of Innsbruck (and the master’s program in “Accounting, Auditing and Taxation”), many students from the region of South Tyrol (Northern Italy) study in Innsbruck.

Table 2 shows the technical or content related factors (project-related working methods, consulting activities, auditing activities, and working with accounting standards), and organizational factors (travel activities, starting salary, salary development, teamwork, work-life balance, prestige, possibility for self-employment, different company insight, and state exam required) included into our analyses.

Job-specific Factors (Tax Consultancy and Audit Profession).

Regarding students’ perceptions of the tax consultancy and audit profession, we do not expect differences between the two groups of students owing to the same reasoning as for H1. Based on the selected factors, we established the following hypotheses, focusing on tax consultancy and audit profession separately:

H3a: The perceived attractiveness of factors regarding the tax consultancy profession is assessed similarly by both student groups.

H3b: The perceived attractiveness of factors regarding the audit profession is assessed similarly by both student groups.

To capture the gap between students’ expectations and practical reality, we formulated H4a and H4b. In line with prior research indicating the existence of an expectation gap between students and professionals, we also expected differences in perceived attractiveness.

H4a: The perceived attractiveness of factors regarding the tax consultancy profession is not assessed similarly by students and practitioners.

H4b: The perceived attractiveness of factors regarding the audit profession is not assessed similarly by students and practitioners.

Impact of Higher Education Institutions

Higher education institutions have observed increased pressure to educate accounting graduates and make them highly skilled young professionals. Practitioners have already raised their dissatisfaction with the number of graduates and the quality of their skills and expertise. An educational gap exists between the courses taught at universities and the job requirements in accounting practice (Dombrowski et al., 2013; Jackling & De Lange, 2009). Dolce et al. (2020) found that in Italy, graduates are not aware of the demands of employers because employers currently give more importance to soft skills than to technical skills. Mandilas et al. (2014) investigated a Greek setting and found that employers focused more on social and participation skills than on technical skills. Johnson (2014) extended this knowledge through a qualitative study and emphasized the importance of practical experience. Brink and Stoel (2018) found that business communication, problem-solving ability, and data interpretation, instead of data visualization, are ranked as the most important. Dzuranin et al. (2018) indicated that the development of critical thinking should be the focus. Ali et al. (2016) identified employers’ skill requirements as written communication skills, continuous learning, and decision-making skills.

Fogarty (2008) suggests involving technology to a great extent, implementing mathematical tasks into games or quizzes, offering group work, and focusing on creativity and fun to better educate future professionals. Sutherland and Hoover (2007) recommend making students feel special to shelter them, showing them the importance and value of their learning, and relieving pressure, expanded by Accountancy Europe (2017), revealing the necessity of promoting students’ achievements and the value that the accounting professions give to society. EY (2020b) found that for Germany, students choose their study programs based on their interests, except for students aiming to study law and economics, where income is the most important factor and interest is the lowest. Career opportunities are of low attractiveness, which seems to not go along with the willingness to undertake an intensive trainee program being obligatory in both professions; however, as business students seek a high income, the importance of high working input may nevertheless be accepted.

Referring to previous studies, we determine whether practitioners are satisfied with their study courses in retrospect, and if students perceive that they have gained appropriate knowledge.

H5a: Satisfaction with the study content is equally high among both student groups.

H5b: Satisfaction with the study content is equally high among students and practitioners.

Fulop et al. (2019) found that the audit expectation gap can be influenced by education, thus improving student’s awareness. Christopher et al. (2013) addressed the potential of academia faculty internships reducing the expectation gap. We gained narrative evidence that students assess both professions as more attractive after gaining deeper insight into practice. We focus on internships, as they can provide deeper insights into the profession and thus contribute to better aligning students’ expectations about professional practice. In this sense, internships help to reduce the audit education-related expectation gap. To capture the potential effect of internships on the perceived attractiveness of the respective profession, we formulated the following:

H6a: The experience of an internship leads to a higher willingness of students to start a career in the tax consultancy profession.

H6b: The experience of an internship leads to a higher willingness of students to start a career in the audit profession.

Research Design and Method

Questionnaire Design

To prepare the questionnaire and collect data, we used soscisurvey.de. The questionnaire comprised three parts: Section A, questions regarding the attractiveness of professional factors in general and questions concerning education, work experience, and career level; Section B solicited information regarding job-specific factors in the accounting profession; and Section C addressed study satisfaction. Students’ questionnaires comprised 20 questions, divided into 13 closed and 7 open questions. Practitioners’ questionnaires comprised 18 questions, divided into 13 closed questions and 5 open questions. Using open questions, every participant had the option to provide additional comments. The closed questions provided answer alternatives. Each closed question in the questionnaire was assessed using a six-point Likert scale. An even number of answer categories forces a decision to either a more positive or a more negative valuation. The possibilities for answering the questions included categories from either “very satisfied (1)” to “not satisfied (6)” or “very attractive (1)” to “not attractive (6).” The questionnaires are provided in the Supplemental Material. The questionnaires were originally prepared and sent out in German.

Internal Consistency

To control for internal consistency, we calculated Cronbach’s α. The Mann–Whitney U test showed a low Cronbach’s α for a profession in general (students: .674, students vs. practitioners: .659), an acceptable Cronbach’s α for tax consultancy (students: .780, students vs. practitioners: .775), and a high α for audit (students: .817, students vs. practitioners: .816). Self-assessment (students: .732; students vs. practitioners: .722) and satisfaction (students: .714; students vs. practitioners: .775) were acceptable. The regression analyses showed satisfactory values for taxes (α = .785) and audits (α = .779). Our results produced Cronbach’s αs between .659 and .817, indicating acceptable internal consistency (Hulin et al., 2001).

Participants

Accounting students and practitioners were surveyed. The study population comprised 373 individuals. Table 3 provides an overview of the number of participants, proportion of professionals and young professionals, and distribution of the study levels of students.

Number and Distribution of Participants.

The practitioners (148) were addressed using the local chambers of auditors and accountants (Institute of Austrian Certified Public Accountants and Chamber of Chartered Accountants and Tax Consultants) as well as using the reach of branch offices of the Big 4 companies. The questionnaire was sent out via e-mail and was available on the homepages of professional institutions. As 852 persons in Austria are certified auditors, we estimate the response rate to be 17.37%.

Regarding students, we investigate the catchment area of the bachelor and diploma programs related to accounting, the master’s programs in both “Accounting, Auditing and Taxation” that covers parts of Tyrol, Southern Bavaria, and South Tyrol as well as “Finance, Auditing, Controlling, Taxation” covering parts of Southern Bavaria. The curricula of both master’s studies are structured similarly to some extent, depending on students’ interest; they focus either on accounting/finance/controlling, taxation, or auditing. To collect data, we sent e-mails to all students majoring in accounting at the University of Innsbruck (Austria) and the University of Nuremberg (Germany). The data collected from the South Tyrolean students were used for a master’s thesis, covering the survey area of South Tyrol. During the survey period, nearly 1088 students were active students with a specific accounting major. Thirty-five out of 195 students commute from South Tyrol and study at the University of Innsbruck. Hence, we estimated a response rate of 20.68%. All participants took part voluntarily. Not all questions were answered by all participants, and the response rate varied very slightly in relation to the single questions asked. The questionnaire was sent out in April 2019, and the responses were evaluated until the end of November 2019. The principal goal of the survey is not striving for generalization but to gain first impressions about the assessment of the professional tax consultancy and auditing environment, showing certain explorative motives.

Results

First, we present our data descriptively by summarizing the ranks 1 (“very important”) and 2 (“important”) to demonstrate agreement. Second, to test our hypotheses, we used the Shannon-Weaver entropy index, which shows the diversity of answers. The higher the diversity, the higher the index. Statistical analyses were conducted with the Mann–Whitney U test. Significance was set at p < .05. Finally, we conduct a regression analysis to analyze the probability of entering the tax consultancy and auditing professions.

Attractiveness of Tasks (Profession in General)

Table 4 presents the assessment of the attributes’ attractiveness by students from the University of Nuremberg, University of Innsbruck, and surveyed practitioners.

Attractiveness of a Profession in General.

Note. The highest numbers per column are marked in bold.

The Shannon-Weaver entropy index indicates low diversity for factors that have a high degree of attractiveness. This coincides with most participants having been assessed on a scale of 1 or 2 or vice versa. Contrastingly, we found a higher diversity for, for example, attribute travel activities or teamwork, as participants were likely to use the full scales available.

Students and practitioners agree that interesting activities make the profession highly attractive. Additionally, a consensus is reached on the importance of salary development, which is assessed as being more attractive than the starting salary. Diversified activities are more attractive to practitioners than to students, similar to job-specific skills. Students from the University of Nuremberg assessed career opportunities as the second most important attribute, while students from the University of Innsbruck considered it to be the fourth most attractive. Work–life balance is more important for students from the University of Innsbruck than for students from the University of Nuremberg. Teamwork and project-related working methods were both assessed as medium attractive factors for all groups. Comparing the opinions of students from the University of Innsbruck and the University of Nuremberg to check for regional differences revealed no significant differences for most factors (Table 5).

Statistical Analysis: Profession in General (Students).

Grouping variable: student groups.

p < .05. **p < .01. ***p < .001.

Regarding the project-related working method, students from Nuremberg (M = 3.59) showed significantly lower interest in that factor than students from Innsbruck (M = 2.77). Travel activities are generally not assessed as attractive; students from Nuremberg (M = 4.50) assess traveling as significantly less attractive than students from Innsbruck (M = 3.69). Thus, H1 is supported, as both groups of students value general job factors as mostly similarly attractive.

Further, untabulated analyses revealed that there were no significant differences between the opinions of bachelor’s and master’s students. Thus, we infer that the perceptions of bachelor’s and master’s students primarily align. Hence, this suggests that generally speaking, bachelor’s and master’s students are attracted to similar factors (Table 6).

Statistical Analysis: Profession in General (Students and Practitioners).

Grouping variables: students and practitioners.

p < .05. **p < .01. ***p < .001.

Differences between students and practitioners were observed for six factors. Most factors were categorized as organizational factors (e.g., career opportunities and work–life balance), whereas only two are classified as technical or content-related factors (diversified activities and job-specific skills).

According to descriptive statistics, both career opportunities and work–life balance are of lower relevance for practitioners than for students. Further, the assessment of the attractiveness of the “starting salary” is highly diverse and significantly different. For future employees, the desire for a high starting salary after years of study is higher than for professionals, where development is more important. “Diversified activities” are significantly more important for practitioners. This may be the reason experienced practitioners place more emphasis on variety because of experience, and students prefer routine to start with.

Overall, H2 cannot be supported, as both groups of students mainly act as one unit, and the practitioners value job factors regarding an occupation, in general, mostly dissimilar attractive. This indicates that even at a general level, the perceived attractiveness of relevant factors differs between practitioners and students.

Regarding the factors “travel activities” and “project-related working methods”, further analyses were conducted to determine whether the significant (travel activities) and non-significant (project-related working method) persist. When comparing German students with practitioners’ opinions, we found significant differences concerning project-related working methods. When comparing Austrian students’ opinions with practitioners’ opinions, we found significant differences concerning travel activities. This indicates that the above-mentioned results are driven by a larger group of students from Innsbruck, whereas more detailed analyses reveal differences between German students and practitioners regarding project-related working methods (Appendix A).

Awareness of Tax Consultancy and Auditing Professions

Figure 1 shows the awareness of students concerning both professions (answer options yes or no), the perceived attractiveness of these professions, and the likeliness of students to pursue a career within this specific accounting area (using a scale ranging from 1 to 6).

Awareness, attractiveness, and considered career entry.

Generally, awareness of the tax consultancy profession is high among both German and Tyrolean students. Students from the University of Nuremberg are more interested in the tax consultancy profession than are students from the University of Innsbruck. Of the attracted German students, 61.54% considered starting a career in the tax consultancy profession, indicating that the majority considered that career path. Nearly half of students from the University of Innsbruck considered their career as a tax consultant (56.60%).

Awareness of the audit profession is assessed as being lower among German students (80%) compared to Tyrolean students (98.74%). Students from the University of Nuremberg assessed the attractiveness of the auditing profession at a low level (51.85%). Contrastingly, students from the University of Innsbruck assessed the attractiveness of the audit profession to be higher at 70.11% (tax consultancy profession: 56.92%). A possible career entry in auditing was considered more often by Tyrolean than by German students.

We calculated the Shannon-Weaver entropy index for each item and different groups of students. For six different items, the maximum Shannon-Weaver Entropy Index was 1.7918, which indicates a diversified answer scheme (Shannon & Weaver, 1949). Hence, we find quite a diverse answering behavior and therefore a distribution among all answer alternatives for most questions, except for the questions regarding the awareness of both professions assessed by students at the University of Innsbruck, where high agreement prevails.

Insights provided by the IDW (2020) claimed that the awareness of both professions among potential future employees is low; thus, the willingness to enter a career declines. Contrastingly, we found high awareness, moderate attractiveness, and a low willingness to start a career. To analyze the causes of this, we conducted further analyses.

Attractiveness of Tasks (Tax Consultancy)

Participants were asked which factors they assessed as attractive related to the tax consultancy profession. Table 7 shows the evaluation of the attractiveness of tasks regarding the tax consultancy profession by the groups of students and practitioners is presented, whereby practitioners have not been asked about “starting salary.”

Attractiveness of the Tax Consultancy Profession.

Note. The highest numbers per column are marked in bold.

The Shannon-Weaver entropy index in this analysis indicated a diversified answer pattern. Attributes with a lower diversity of answers, such as different company insights, salary development, travel activities, or the required state exam, indicate that all answer alternatives are relevant.

In general, these results are more diverse than those related to the profession. Compared to the valuation of attractiveness in Table 4, the overall attractiveness of the tax consultancy profession is valued high among students from the University of Nuremberg; however, the single tasks are assessed with moderate perceived attractiveness. Even students from the University of Innsbruck, who previously expressed moderate interest, assessed the single factors related to the tax consultancy profession with higher attractiveness than students studying at the University of Nuremberg.

The perceived attractiveness of the starting salary is widespread and almost twice as attractive for students at the University of Innsbruck. Concerning tax consulting, consulting activities are valued by the groups of participants as more attractive than auditing activities. Travel activities are valued low by students at the University of Nuremberg (4.00%), higher by practitioners (14.91%), and highest among students at the University of Innsbruck (26.28%). The attribute of the “work–life balance” is strikingly low for the German students (23.08%) compared to the Tyrolean students (59.62%). Practitioners also valued this at a lower level (36.84%). Prestige in connection to tax consultancy was the lowest assessed by practitioners (49.26%), followed by Tyrolean students find it moderately attractive (56.41%) and German students found it most attractive (65.38%).

As presented in Figure 1, students from the University of Nuremberg value tax consultancy as more attractive; however, the descriptive analysis (Table 7) shows a higher evaluation of students from the University of Innsbruck regarding specific tasks. Table 8 shows the six significantly different assessments of both groups of students regarding specific tasks of the tax consultancy profession.

Statistical Analysis: Tax Consultancy Profession (Students).

Grouping variable: student groups.

p < .05. **p < .01. ***p < .001.

Regarding the tax consultancy profession, the opinion of the attractiveness of the “project-related working method” is similar; regarding a profession in general, it was significantly different. “Travel activities” were perceived significantly different by both student groups. In tax consultancy, starting salary and salary development are perceived as unattractive. Students from the University of Nuremberg perceive it as slightly attractive; consequently, an improved presentation may be conducted regarding salary in the Bavarian area.

Furthermore, the possibility of self-employment was significantly different, and it is more attractive among Tyrolean students. Overall, the attractiveness of the state exam is at a medium level among students from the University of Innsbruck and a low level for students at the University of Nuremberg. Nevertheless, H3a is supported, as 7 out of 13 occupational factors regarding the tax consultancy profession are assessed similarly by both groups of students. Hence, although different assessments exist, more factors were evaluated in a similar manner. Those factors that are perceived as significantly different belong to the group of organizational factors, whereas no significant differences exist regarding technical or content-specific factors. Comparing the opinions of students to those of the practitioners shows that 5 of the 12 factors are perceived to be significantly different (Table 9).

Statistical Analysis: Tax Consultancy Profession (Students and Practitioners).

Grouping variables: students and practitioners.

p < .05. **p < .01. ***p < .001.

The work–life balance and travel activities are comparable to the results shown in Table 6. Salary development revealed a significantly different opinion, as the assessment by practitioners was more negative. Investigating the data of both groups of students separately to the practitioners (Appendix A) implied that practitioners and students from Nuremberg are not satisfied with their salary. It is thus worth emphasizing the proper presentation of salaries. Auditing and consulting activities are also perceived differently by practitioners and are perceived as less attractive by the practitioners. In summary, although we expected an expectation-performance gap that more significant differences than similarities exist, H4a is not supported, as 7 out of 12 occupational tasks are perceived as similar. Nevertheless, our analyses revealed the factors that were significantly different. The differences in auditing and consulting activities, as well as the relevance of the work–life balance, indicate a technical or content-related difference in expectations between students and practitioners.

Attractiveness of Tasks (Auditing)

Based on the descriptive presentation, the perceptions of the factors of the audit profession also diverge. Students from the University of Innsbruck evaluated the task with the highest attractiveness in contrast to students from the University of Nuremberg and the practitioners (Table 10).

Attractiveness of the Audit Profession.

Note. The highest numbers per column are marked in bold.

The Shannon-Weaver entropy index indicates a lower diversity for attributes with a high agreement rate—for example, salary development and different company insights—however, starting salary, travel activities, or prestige had a higher diversity of answers. Thus, participants’ opinions were not uniform, and a variety of assessments were conducted.

In our sample, the student groups have a different understanding of whether the starting salary is attractive. Students from the University of Innsbruck assessed audit-specific tasks as the most attractive.

Compared to the tax consultancy profession, students assessed travel activities as more attractive. Work–life balance was less attractive in the auditing profession. As work–life balance seems to be vital for students in a profession in general, it may be focused on presenting this professional task in a more attractive way regarding both specific professions.

Unlike students from the University of Innsbruck and practitioners, students from the University of Nuremberg perceived consulting activities to be more attractive than audit activities. Practitioners assessed the attractiveness of both consulting (50.00%) and auditing activities (55.56%) at a moderate level. Working with accounting standards is also rated as moderately attractive, and project-related working methods in a specific profession have a lower rating. The factors of different company insight and diversified activities may be emphasized in the center of professionals’ presentation, as they are perceived as the most attractive.

Statistical analysis revealed more disagreements than consensus among the student groups. General factors receive similar assessments but auditing/tax accounting activities differ in that regard. Eight of the 13 tasks were perceived as unequally attractive, which does not support H3b (Table 11).

Statistical Analysis: Audit Profession (Students).

Grouping variable: student groups.

p < .05. **p < .01. ***p < .001.

This indicates that six organizational and two technical or content-related factors are assessed differently by students. Based on these findings, we conducted a comparative analysis of students and practitioners separated by university origin. Assuming the existence of an expectation gap, we presume that students’ and practitioners’ expectations regarding the most important factors in the auditing industry differ significantly (H4b).

Table 12 shows the Mann–Whitney U test concerning the perceived attractiveness of factors regarding the audit profession assessed by students at the University of Innsbruck and practitioners.

Statistical Analysis: Audit Profession (Students Innsbruck and Practitioners).

Grouping variables: students (Innsbruck) and practitioners.

p < .05. **p < .01. ***p < .001.

Six of the 12 factors were significantly different. This comprises three organizational and three technical or content-related factors that support H4b, predicting different expectations between students and practitioners on tasks related to the job of an auditor. The same analysis comparing practitioners’ answers with those of students from the University of Nuremberg leads to different results (Table 13).

Statistical Analysis: Audit Profession (Students Nuremberg and Practitioners).

Grouping variables: students (Nuremberg) and practitioners.

p < .05. **p < .01. ***p < .001.

We found only differences for three of the factors. These factors were assessed as organizational factors; hence, between practitioners and students in Nuremberg, no different evaluations of technical or content-related topics were found. This indicates that H4b is not supported.

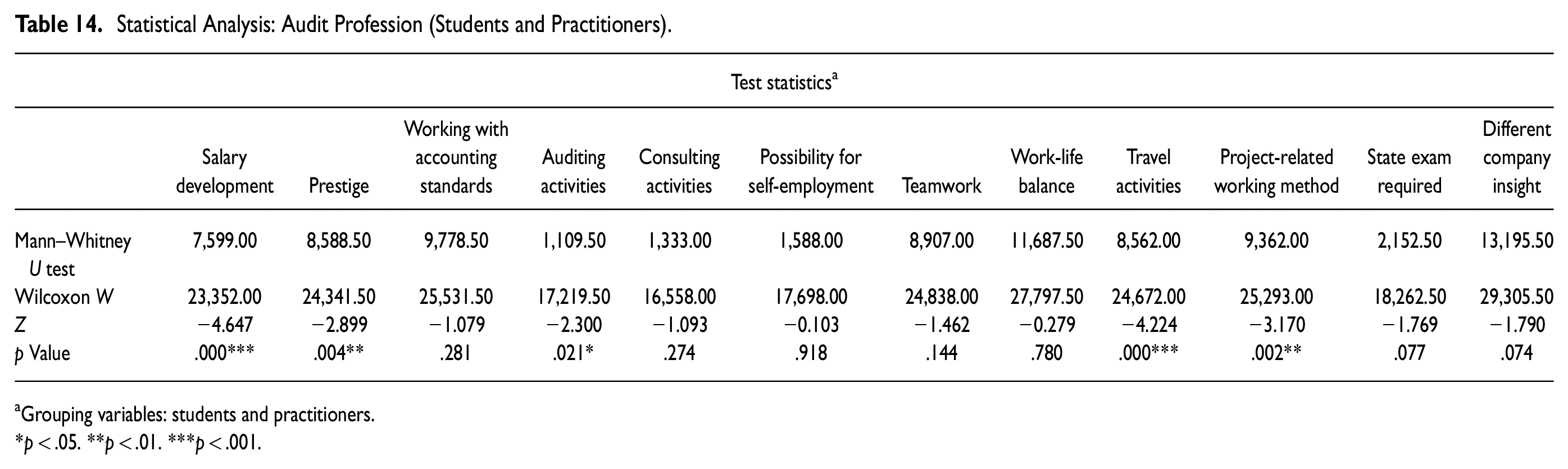

Against the background of these diverging results, we conducted another Mann–Whitney U test with all students as one group and the practitioners as the second group, which reveals that 5 out of 12 occupational factors were perceived to be significantly different (Table 14).

Statistical Analysis: Audit Profession (Students and Practitioners).

Grouping variables: students and practitioners.

p < .05. **p < .01. ***p < .001.

These diverging results indicate that to some extent, differences occur; these differences mainly refer to organizational factors, whereas technical or content-related factors are usually assessed as similarly attractive. This indicates that to some extent, an expectation gap exists; however, this is highly dependent on different groups of students. Therefore, different groups of students might have different expectations, and when attracting young professionals, professional bodies, and auditing firms should be aware of these differences.

Satisfaction With Higher Education

Higher education institutions have a crucial impact on career decisions and the success of their careers. We evaluated the answers given by students and practitioners concerning their perceived satisfaction with the study courses and their expertise. This should explain if different satisfaction with their study program affects their assessment (Table 15).

Perceived Satisfaction: Overall Study Course.

Note. The highest numbers per culumn are marked in bold.

Overall satisfaction was moderate among students, and the Shannon-Entropy index indicated a diversity of answers. Practitioners reviewed the study program to be the least satisfactory. Their satisfaction with the content was moderate, and their practical relevance was assessed as low (Table 16).

Statistical Analysis: Overall Study Course (Students).

Panel A: Students.

Grouping variable: students.

p < .05. **p < .01. ***p < .001.

Panel B: Students Versus Practitioners.

Grouping variable: students and practitioners.

p < .05. **p < .01. ***p < .001.

Statistical analyses showed that two out of the four study-related perceptions differed significantly (Table 16, Panel A) between the different groups of students. When comparing students and practitioners (Panel B), three out of the four factors were perceived differently. The overall study course was assessed quite well by both groups of students. Although students from the University of Nuremberg were more satisfied with their study courses, they evaluated the attractiveness of tasks of the tax consultancy and audit profession on a lower level. As the two groups of students perceived satisfaction with the study differently, H5a was rejected.

The ratings of students compared with those of the practitioners are shown in Panel B. One of the four factors coincided with the other. Regarding practical relevance, the low rating of students from the University of Innsbruck is balanced by the better rating of students from the University of Nuremberg in the practitioners’ direction. In retrospect, practitioners were the least satisfied with their previous studies; however, current students seemed to be more satisfied than practitioners. Consequently, H5b must be rejected because our data do not show that students and practitioners have similar satisfaction rates in their studies.

The untabulated results show low-to medium-level satisfaction with their gained expertise within different courses. Answers from all three groups indicated a variety of opinions on knowledge regarding different topics; for example, information-technology knowledge, national and international accounting, taxation, tax laws, and cost accounting. Hence, concerning both general and specific aspects of education, higher education institutions should apply measures to increase student satisfaction with education. This might be accomplished by clearly communicating the learning objectives and outcomes of the courses or by adapting the study contents to the needs of students and employers.

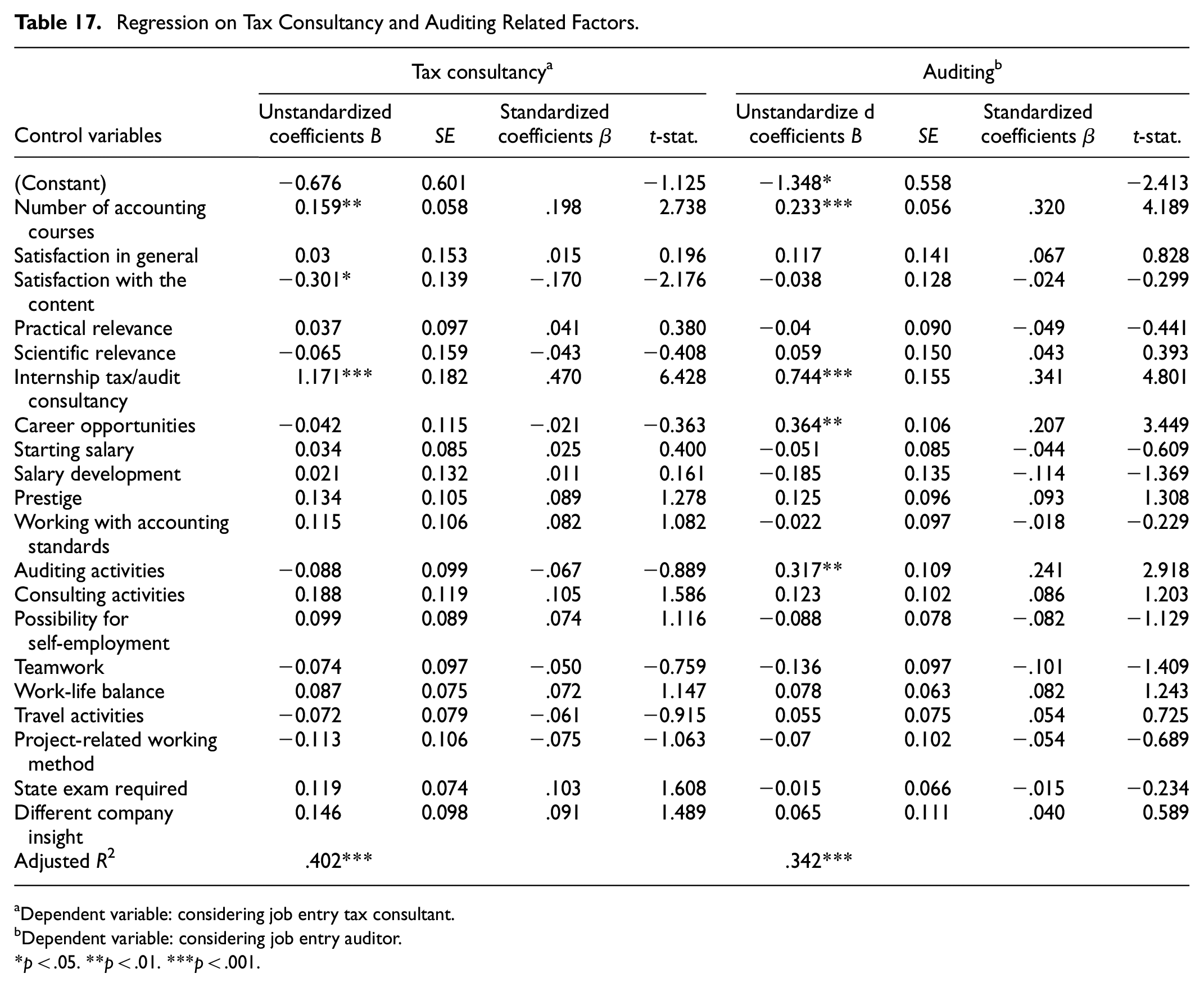

Probability of Entering Tax Consultancy and Auditing Professions

We focused on certain occupational and study-related factors and conducted internships to determine whether these independent variables are likely to increase the probability of starting a career in tax consultancy and auditing. Therefore, we conducted regression analyses using the probability of job entry as the dependent variable. As independent variables, we chose job- and education-specific factors. We also tested whether the level of education in the bachelor’s or master’s program has an impact. We included the number of accounting courses to test whether increased expertise increases the desire for career entry and course dimensions in general. Thus, to investigate the probability of job entry (probEntry) in both professions, we estimated the following model:

Vector

Regression on Tax Consultancy and Auditing Related Factors.

Dependent variable: considering job entry tax consultant.

Dependent variable: considering job entry auditor.

p < .05. **p < .01. ***p < .001.

Regarding the tax consultancy profession, the number of accounting courses, the satisfaction with the study’s content and completed internships significantly affected the decision to consider a job as a tax consultant. Thus, H6a is supported, as an internship increases the willingness to start a career in the tax consultancy profession. The other factors were non-significant. Nevertheless, the adjusted R2 of .402 can be interpreted as high regarding the variety of independent variables and occupational environment.

Regarding the audit profession, the number of accounting courses and internships significantly increased willingness to enter this profession. Therefore, the data support H6b, demonstrating that an internship leads to an increased willingness to start a career during auditing. Although the calculated adjusted R2 is lower than that of the tax consultancy profession (tax: .402 vs. audit: .342), it is acceptable in this context. Moreover, career opportunities and auditing activities increase the perceived attractiveness of the audit profession. Students are convinced of attractive career prospects within the audit area, similar to the positive influence of assessing specific tasks on their career decisions.

Discussion

The starting point of the study was the problems identified in the literature and professional practice in the recruitment of young professionals. This study examines the extent that there are discrepancies between students’ expectations about the job profiles of auditors and tax consultants regarding the tasks and requirements of the professions from the perspective of professionals.

Previous studies refer to the audit education-related audit expectation gap, identifying a gap between the content of education programs and professional requirements in some cases (e.g., Maali & Al-Attar, 2020). This study broadens the perspective on the expectation gap by evaluating the attractiveness of job-specific factors.

Our survey-based results support H1, indicating that both groups of students assess general attributes of job-specific factors similarly, except for project-related working and travel activities, which are assessed as less negative by Austrian students. We identified interesting activities, salary development, career opportunities, and diversified activities as the most important factors with an agreement rate of more than 80%. These results coincide with prior studies focusing on Germany and Austria (e.g., Dahlmanns, 2014, Hauser & Loder-Neuhold, 2021). Contrasting Durocher et al. (2016) who examined a Canadian setting, teamwork and travel activities were assessed as having little attractiveness by students. However, regarding travel activities, the assessment differed significantly between the surveyed student groups. Accordingly, regional aspects may influence student assessment and should be considered in recruiting and retaining strategies.

Contrastingly, H2, which predicted no differences between students and practitioners, was rejected. This indicates that practitioners have different preferences regarding the attractiveness of certain factors that they consider attractive jobs. From practitioners’ perspective, travel activities, starting salary, work–life balance, and career opportunities are of significantly lower importance compared to students. Job-specific skills and diversified activities are even more important than those assessed by students. This indicates that technical- and content-related factors are of higher importance to practitioners. The different assessments of students may be caused by generational factors (Ng et al., 2010; Tiron-Tudor et al., 2019). This discrepancy also indicates that belonging to different groups might (consistent with social identity theory) lead to factors being assessed differently. If so, recruitment and retention strategies should focus on organizational factors as they are more important for students.

Then, we asked students and practitioners for their opinions on the attractiveness of specific factors in relation to the tax accountancy and audit profession. The assessment regarding factors describing tax accounting is mostly similar between different groups of students (supporting H3a); factors that are assessed differently are not related to the technical of content-related factors but organizational factors. As the results indicate no differences for most factors related to tax accounting (H4a was rejected), we conclude that there is no expectation gap regarding tax accounting between students and practitioners.

Contrastingly, for auditing, expectations differ between the two groups of students and between students and practitioners. While expectations diverge less strongly around tax consulting between students and between students and practitioners, there are significant differences in auditing.

Comparing the two groups of students, we find most factors being assessed differently. According to social identity theory, this indicates that these students belong to different groups concerning assessing the auditing profession (H3b was rejected). We highlight that besides organizational factors, we could already find differences, regarding the technical or content-related factors relevant to the auditing profession (e.g., “auditing activities”).

The general importance of starting salary and salary development coincides with previous research (e.g., EY, 2020b; Kötter, 2010). Our results show that the factors were assessed differently depending on students’ location. The provided starting salary and salary development were assessed as more attractive by Austrian than German students. As the two groups of students assessed the factors significantly, we conducted analyses to test H4b by distinguishing between them.

H4b predicts the differences between practitioners and students owing to an expectation gap. Our results regarding H4b are mixed: although students from Innsbruck are more interested in auditing, we find support for H4b, which indicates an expectation gap exists. This gap is mainly related to organizational factors that are assessed to be of higher importance by students, such as work–life balance, prestige, and the required state exam. Recruiting and retaining strategies should focus on these factors to attract students. Contrastingly, students from Nuremberg, who have indicated lower interest in auditing activities, assess factors similar to practitioners. This indicates that no expectation gap exists between these two groups (thus, H4b is rejected).

Because we identified that the assessment of some aspects depends on local differences between the groups of students and between students and practitioners, our results suggest that the phenomenon of an expectation gap is situational. Our results do not indicate a uniform, divergent assessment between students and practitioners but rather seem to be location-related. Thus, we can determine the regional differences between Germany and Austria, which are partly consistent with the “peculiarities” of the respective locations or institutions. However, this finding implies that no generally applicable measures can be derived to close the expectation gap. Hence, situation-specific analysis of the regional situation is required to derive suitable situation-specific recommendations.

Regarding education, our results indicate that satisfaction is assessed as higher by students and lower, from a retro-perspective, by practitioners. Generally, we find a difference between students’ groups and students and practitioners (thus, H5a and H5b are rejected). For example, students from Innsbruck were aware of the limited practical relevance of their studies. Consistent with prior literature (e.g., Christopher et al., 2013), this indicates the necessity to better align students’ education with professional requirements. In this context, our regression analysis showed the high importance of an internship for the willingness of job entry in the tax consultancy and audit profession (supporting H6a and H6b).

Conclusion

The primary objective of this study was to investigate the factors that students seek when planning their future careers, how these factors apply to specific tasks of the investigated professions, and the differences in the perceived attractiveness of the tax consultancy and audit profession between students and practitioners.

Awareness of the tax consultancy and auditing profession is high, attractiveness is moderate, and considerations of career entry are low. This does not support the insights provided by the German Institute of Accountants, who claims that a lack of awareness affects career considerations in both professions (IDW, 2020). We also find regional preferences toward either tax consultancy or auditing as a first hint for the emphasis on implementing regional marketing strategies to attract students to both professions. We further found that the tasks regarding a profession are perceived as roughly similar by students and practitioners. Regarding professional expectations, all groups highly valued interesting activities, followed by salary development, work–life balance, and career opportunities.

Regarding both professions, Tyrolean students perceive specific tasks as being more attractive than do German students and practitioners. Nevertheless, when considering specific strategies to present the tax consultancy profession, the focus should be on different company insights, consulting activities, salary development, and the possibility of self-employment. While our results do not indicate an expectation gap between students and practitioners regarding the tax consulting profession, the situation differs for the audit profession. Our results indicate a region-specific expectation gap between the expectations of students from Innsbruck and those of practitioners.

Regarding the auditing profession, students from Innsbruck express preferences for auditing activities, and company insights are perceived as very attractive but show different assessments to practitioners, particularly regarding organizational factors. Hence, audit and consulting activities should focus on increasing the perceived attractiveness. Attention should also be paid to travel activities as a worst-rated factor. A possible solution is to provide newcomers with a contractual period, which will provide an accurate estimate of travel activities to get them acquainted with working and traveling. The increase in digitalization might have contributed to a decrease in travel activities. Higher congruence consistently predominates between German students and practitioners, indicating that no expectation gap exists between these two groups. In this case, the lower attractiveness of the audit profession is not related to the expectation gap but because the profession itself is not assessed as attractive. Overall, the findings on region–specific expectation gap lead to recommendations for regional recruitment strategies.

Regarding training in higher education institutions, satisfaction with the study program among students and practitioners is at the lowest level of practical relevance. Our study implies that more practice-related education should be offered to fulfill universities’ core tasks in educating young professionals. Cooperation can be arranged between accounting firms on a Big 4 or smaller level and universities to offer internships, as this would increase students’ willingness to enter the accounting profession. Knowledge obtained during studies is perceived as less satisfactory for students than for practitioners assessing it as good in retrospect, which signifies that the benefits of the study program and content are applicable. Further, we found a significant positive influence of completing an internship and the number of completed accounting courses on the willingness to start a career in both professions. Career opportunities and auditing activities have a key impact on auditing job entry.

Limitations regarding survey studies based on questionnaires also arose in this study. Furthermore, participants were only from a certain part of Europe, and the results may not be generalizable to different regions. Regarding regression analyses, an R2 of approximately 40% indicates that the integrated variables only partly explain the probability of job entry in the respective professions. This could serve as a starting point for future research.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440231153100 – Supplemental material for Perceived Attractiveness of Tax Consultancy and Auditing Professions: Insights From a German-Speaking Area

Supplemental material, sj-docx-1-sgo-10.1177_21582440231153100 for Perceived Attractiveness of Tax Consultancy and Auditing Professions: Insights From a German-Speaking Area by Sabine Graschitz, Simona Holzknecht and Marcel Steller in SAGE Open

Footnotes

Appendix A

To support our results, additional analyses were conducted separately, comparing each group of students with the practitioners. The results of the Mann–Whitney U test conducted between the two student groups shown in Table 6 reveals that their opinion on “project-related working method” and “travel activities” are perceived significantly different.

Thus, supporting analyses were conducted between students from the University of Innsbruck and practitioners first and then students from the University of Nuremberg and practitioners. Additional statistical analyses showed that there is a significantly different assessment of project-related working methods between students from the University of Nuremberg and practitioners. This significantly different assessment does not persist for students from the University of Innsbruck or practitioners. Thus, the very low value (students from Nuremberg) and the high valued (students from Innsbruck) level of attractiveness between the student groups result in medium attractiveness, which falsely demonstrates a consensus between both student groups and practitioners.

The same procedure reveals the opposite effect on travel activities. Separating the student groups and comparing them with practitioners revealed agreement between students from Nuremberg (p = .736), and disagreement between students from Innsbruck and practitioners (p < .001) for the perceived attractiveness of travel activities.

The table above shows the supporting analysis with respect to the perceived attractiveness of professional factors, in general, assessed by students at the University of Innsbruck and practitioners.

The table above shows the supporting analysis concerning the perceived attractiveness of professional factors, in general, assessed by students at the University of Nuremberg and practitioners.

Appendix B

Acknowledgements

We thank the Editor and the reviewers for their valuable guidance. We also thank the participants of the EAA Annual Congress 2021 (online) and the Audit and Assurance Conference 2020 (online) for their impactful discussion. Furthermore, we thank the Institute of Austrian Certified Public Accountants and the Chamber of Chartered Accountants and Tax Consultants, the participants of our survey as well as the student assistants of our department for helping us collecting the data we used within this survey.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received financial support from the BAFIT Network (University of Innsbruck) for the publication fees of this article.

Ethical Statement for Animal and Human Studies

No ethical aspects were violated or impaired as we did not undertake medical surveys on animals or human as well as we did not use wrong information manipulating participants for our survey.

Informed Consent

Study participants were informed about the purpose and duration of the survey as well as the anonymity of their data. Informed consent was not requested formally when conducting the survey, as we did not use wrong information manipulation for our survey and no specific personal information was requested.

Research Data

Available on request.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.