Abstract

The objectives of this study are to examine whether the current accounting curricula of Jordanian universities fit the Jordanian market demand, in addition to determining the skills and competences that Jordanian businesses require from accounting graduates. To achieve these objectives, an analysis of current accounting curricula of Jordanian universities took place, interviews with professionals and academics were conducted, and a questionnaire survey was administrated to a large sample of academics and professionals. The study found the presence of a significant gap between the courses covered in the accounting curricula of Jordanian universities and the skills acquired by the students versus the market’s requirements and needs. This is mainly due to the fact that the accounting curricula of Jordanian universities are structured based on specific requirements set by the Accreditation and Quality Assurance Commission for Higher Education Institutions (AQACHEI), leaving no freedom for universities to develop curriculums that meet the market’s need. It is also argued that that current exam-based assessment methodology adopted by Jordanian universities largely contributes to expanding the gap. The study recommends giving Jordanian universities more freedom in setting the curriculum for accounting programs, and that they should start revising their accounting curriculums to take into account current market needs.

Introduction

The ultimate objective of the accounting education is to develop the necessary skills and competences required for good accountants. Universities and colleges should educate their students by implementing curricula that fit the needs of the labor market (Marzo-Navarro et al., 2009). The contents of the educational program are specified by a curriculum, which is subject to “much debate between various stakeholders about the need for accounting graduates to develop a broader set of skills to be able to pursue a career in the accounting profession” (Kavanagh & Drennan, 2008, p. 279). Venter (2001) argues that the curriculum content provides students with the basic theoretical framework necessary for understanding business management and, at the same time, provides students with knowledge and techniques which are indispensable to start up and manage small businesses effectively. Of course, the business environment has been subject to continuous change, especially with the latest trend for digital transformation. Accountants, and thus accounting education, should follow the changes in business technologies and provide curriculums that will reinforce the accountant’s efforts to respond sufficiently to such developments (Mandilas et al., 2014).

Due to the importance of accounting in almost all sectors of the economy, most Jordanian universities, both public and private, offer accounting undergraduate degrees. Statistics show that accounting remains a favorite university major for many Jordanian students (Al-Khadash, 2013). However, there has been continuous criticism aimed at accounting departments in Jordanian universities for being too academic and not equipping students with the necessary skills needed in the labor market (Al-Hussein Fund for Excellence, 2012). Both accounting professionals and academics realize that there is an increased gap between accounting education and accounting practice (Al-Hayek & Al Khasawneh, 2013; Matar et al., 2015; Nassar et al., 2013). Perhaps this problem is not unique to Jordan; researchers argue that the current accounting education in many parts of the world does not prepare students for the practicalities of the business world (Andrews & Higson, 2008; Siegal et al., 2010).

The gap between accounting education and practice has significant influence on the readiness of students to tackle appropriate functions, and affects the graduate’s employability (Webb & Chaffer, 2016). Furthermore, employers are the main stakeholders affected by this gap; unqualified new entrants to the job market would require more effort and costs to qualify them. With new technological innovations such as industry 4.0 and big data, it is expected that “accountants will need to learn new skills when the more traditional tasks become automated and the technical maintenance and analytic needs of the work increase substantively” (Zhang et al., 2018, p. 20). If current traditional teaching methods continue without incorporating the new technologies in the curriculum, the gap between accounting education and practice will increase in the future. As argued by Cheng (2019), accounting higher education shall accelerate the pace of educational innovation and personnel training.

This article aims to examine whether current accounting curriculums in Jordanian universities fit the Jordanian market demand, and to determine the skills and competences that Jordanian businesses require from accounting graduates. This led to the identification of the mismatch between market needs and current curricula. This was tackled through conducting interviews with different stockholders, in addition to administrating a questionnaire survey. The results of the survey were compared with the current content of accounting curricula in Jordanian universities to provide recommendations to improve the contents of accounting curricula to make it more market-oriented. Although this study is confined to Jordan, but as will be explained in the following section, the structure of accounting curricula in Jordanian universities is largely affected by those in western universities (Alsharari, 2017). Jordan, with a growing economy in the Middle East, is an example for less developed countries.

The remainder of this article is structured as follows: “Accounting Education in Jordan” section discusses accounting education in Jordan; “Literature Review” section sheds light on relevant literature. The methodology is explained in “Research Methodology” section. “Findings” section is devoted to discussing the results of the analysis. The conclusions are explained in “Conclusion” section. “Recommendations” section is devoted to recommendations for decision makers based on the empirical study.

Accounting Education in Jordan

Jordan, with 10 public universities and 18 private universities, has a well-established accounting education system. Except for three universities, all Jordanian universities offer accounting undergraduate degree programs, and many of them offer master’s degree programs, in addition to many community colleges that offer accounting education. The accounting bachelor degree programs in Jordan follow the credit hours system, with the requirement of completing around 132 credit hours in most universities—except for German Jordanian University, with 145 credit hours. The study plan for the accounting program usually includes compulsory and elective courses. The language of teaching for the accounting program differs across universities, with some universities teaching in Arabic while others in English. Jordanian universities have much similarity in the accounting curricula because they are all constructed in the general criteria set by the Accreditation and Quality Assurance Commission for Higher Education Institutions (AQACHEI). Thus, Jordanian universities do not have much flexibility in designing their own accounting program curricula. AQACHEI has many other roles in the Jordanian educational system; in addition to setting and monitoring the contents of study plans, they set requirements regarding the number of faculty members teaching in the programs and their ranks, in addition to the facilities that should be available in universities.

The approach utilized in accounting education by Jordanian universities emphasizes “transfer of knowledge, with learning defined and measured strictly in terms of knowledge of principles, standards, concepts, facts and procedures at a given point in time” (Nassar et al., 2013, p. 112). Alsharari (2017) argues that Jordan has adopted accounting education practices from developed countries, “notwithstanding considerably different environmental factors, the Jordanian accounting education system and accounting profession have been developed toward the accounting environments and the private sector practices of the USA and the UK” (p. 737). The accounting profession in Jordan seems isolated from accounting education. Preliminary interviews with a member of the Jordan Association for Certified Public Accountants, conducted in this study, suggested that this organization does not play any role in developing accounting curricula for Jordanian universities, nor was it consulted in setting the general guidelines for the accounting curricula in Jordanian universities as required by AQACHEI.

For example, for the bachelor’s degree in accounting, AQACHEI largely specifies the structure of the curricula by specifying “Knowledge Fields” in accounting curricula such as Financial Accounting, Auditing and Auditing Standards, Specialized Accounting Systems. Within each knowledge field, the curricula have to include a minimum number of courses. For this, much similarity is found between the accounting curricula in Jordanian universities. The current AQACHEI’s methodology leaves no room for Jordanian universities to enhance the structure of their study plans. Furthermore, despite the presence of high-quality education standards for professional accountants issued by International Federation of Accountants (IFAC; 2015), literature on accounting education in Jordan (e.g., Aleqab et al., 2015; Al-Khadash, 2013; Matar et al., 2015) suggests that such standards are not employed by Jordan. A deeper look at the AQACHEI’s standards by authors reveals that such standards were not taken into account when AQACHEI standards were developed for accounting curricula. An analysis of the contents of the current accounting curricula for Jordanian universities has been conducted as part of this research, as explained in “Findings” section.

Literature Review

Accounting education plays a key role in the professional development of accountants and in improving their professional skills. Accounting education is also changing to keep pace with the rapidly changing economic environment. Accounting education, as part of the whole university education, has been subject to continuous improvement and change to keep pace with the changing environment and market needs. In Europe, for example, changes in higher education institutions began with the Bologna Convention (1999) and resulted in the introduction of new concepts for higher education institutions such as the learning outcomes, the European Credit Transfer and Accumulation System (ECTS), and the European Qualifications Framework (Asonitou, 2015).

Accounting researchers have recognized the existence of a gap between accounting education in universities and market needs. Perhaps such recognition for the gap started at the beginning of the 20th century in the United States (Bloom et al., 1994). The gap between accounting education in universities and accounting practice is named by Bloom et al. (1994) as “schism.” Elwell (1917) attributes the reasons for this gap to the inadequacy of recognition of accounting educators by the professional accounting communities. Wilson R.M. (2014) argues that the changes and development of the surrounding environment of the accounting profession has made it difficult for the status of current accounting education to fulfill the requirements of the work environment. Wilson R.M. (2014) introduced many factors such as increased complexity and risk, increased change in financial markets, and the increasing technological change that necessitate change of accounting education to meet the market’s needs. Perhaps with rapid technological advancements, focusing on subject-specific knowledge while ignoring long-life skills and competences would be dangerous and irrelevant. Some accounting researches have argued that current accounting education and the skill levels of accountants are not in line with what is required in the dynamic environments of global business (Mohamed & Lashine, 2003).

As argued by Tatikonda and Savchenko (2010), the problems in accounting education have evolved to an accounting crisis due to the lack of conformity between accounting education and the curricula adopted by universities. The majority of this problem lies in what is termed “expectation gap” between what accounting academics provide and the generic skills required by the employers (Webb & Chaffer, 2016). Such an expectation gap is largely “caused by differences in the way academicians and practitioners view competencies. Academicians view based on theory, while practitioners view based on practical experience and the requirements of business” (Pratama, 2015, p. 19). Lightweis (2014) attributed a large part of this problem to the fact that “accounting educators who only lecture and accounting students who memorize the information provided in these lectures. Accounting students need opportunities to build their professional skills through learning activities that mimic real-world situations” (p. 18). Of course, the expectation gap in accounting education would lead to what Brewer and Stout (2014) called a competency crisis a gap that is “between the competencies needed for professional success and those taught in our college classrooms today” (p. 30). Lately this has created other problems for accounting education; Douglas and Gammie (2019) found out that in some countries, this has led employers to respond by seeking out graduates holding nonaccounting degrees, who they perceive to have better developed these skills. This might lead, as argued by Albrecht and Sack (2001), to dramatic decreases in student enrolments in accounting programs, which would create further problems for accounting educators. Of course, there should be a fit between the accounting curriculum and market needs, as argued by Ngoo et al. (2015); if accounting graduates do not have adequate skills and competences, many of them will be unaware of the employment reality, and they will be either shocked or unprepared to adapt to the working environment or find it difficult to cope with their job responsibilities (Ngoo et al., 2015). Business discipline educators should start to alter the curriculum to prepare accounting graduates with a good range of skills and attributes for the work environment (Braun, 2004).

Accounting researchers and professional accounting associations worldwide have realized that a gap exists between accounting education and market needs. In 2014, a Joint Cubiculum Task Force was formed by the American Accounting Association and the Institute of Management Accountants (two of the largest accounting professional bodies in the United States and the world) and jointly published a report that addresses the gap between accounting education and practice in the United States, and included curriculum recommendations for accounting majors in U.S. universities. Researchers in the United States (Palmer et al., 2004), England (Chaffer and Webb, 2017), Australia (Jackson & Chapman, 2012; Kavanagh & Drennan, 2007), India (Bhasin, 2013), Greece (Mandilas et al., 2014), Saudi Arabia (Mallak, 2018; Zureigat, 2015), and in other countries have studied the market needs and accounting curricula in their respective countries. Literature to date has cited many skills and competences that are required by the market, but not emphasized in the accounting curriculum of universities. Information technology is identified as one of the most important skills that accounting graduates should have (Aleqab et al., 2015; Amirul et al., 2017; Laing & Perrin, 2012; Senik & Broad, 2011; Tan & Ferreira, 2012). Teamwork is found to be important from the perspective of employers (Crawford et al., 2011; Parham et al., 2012; Reyad et al., 2019; Riebe et al., 2017; Watty et al., 2013). Literature also discussed other skills such as written communication, problem-solving, language skills, and negotiation skills (Arquero Montaño et al., 2001; Chaffer & Webb, 2017; Howcroft, 2017; Jackson & Chapman, 2012; Latif et.al., 2019; Low et al., 2016; Mandilas et al., 2014; Marzo-Navarro et al., 2009; Sithole, 2015; Zureigat, 2015) and found such skills, in varying degrees, important for accounting graduates and should be included in the accounting curriculum.

In Jordan, few related studies have been conducted; Al-Khadash (2013) compared the curriculum of eight public and private universities and the criteria set for accrediting accounting educational programs in Jordanian universities, as set by AQACHEI, with the International Education Standards, which represent guidance for good practice in accounting education issued by IEASB (International Ethics Standard Board for Accountants). He found a gap between accounting curricula in Jordanian universities and the guidance offered by IEASB. Al-Hayek and Al-Khasawneh (2013), by using a questionnaire survey that was distributed to accounting graduates, investigated the suitability of accounting education in Jordanian private universities to the requirement of job markets. Finally, Sawalqa and Obaidat (2014) investigated the relevance of accounting courses offered by Jordanian universities from the perspective of undergraduate students.

However, this study is different from previous studies in that it studies the market needs from the perspective of academic staff and employers. The study compares the views of academic staff and professionals on the importance of different courses included in the accounting curriculum of Jordanian universities. It also analyses the perceived view for the necessary skills and competences required from accounting graduates in Jordan, and whether the current curriculums in Jordanian universities equip the students with such necessary skills and competences. The study collects information via different research techniques and from a relatively large sample.

Research Methodology

To gain better understanding of the current contents of accounting curricula in Jordanian universities, the perceived view regarding the competences, topics, and skills demanded by the market, this research adopted a triangulation approach (Archibald, 2016; Flick, 2018; Wilson V., 2014), that is, many sources of evidence and methods of analysis were used to gain insights on the topic. Three research tools were utilized in this research: analysis of current accounting curricula in Jordanian universities, interviews, and a questionnaire survey. It is worth emphasizing that the first two research tools were aimed at specifying the main items to be included in the questionnaire survey and gaining a deeper insight into the research topic. The research tools are explained in the following sections.

Analysis of Current Contents of Accounting Curricula in Jordanian Universities

As explained in “Literature Review” section of this article, AQACHEI largely specifies the structure of the accounting curricula for Jordanian universities by specifying knowledge fields in the accounting curricula and the minimum number of credit hours within each field. At this stage, the requirements of AQACHEI were analyzed, and the contents of the accounting curricula for Jordanian universities were studied to specify which courses should be included in the questionnaire survey. Although some community colleges offer accounting diploma degree, this study included only full-flagged Jordanian universities Of the 28 public and private universities operating in Jordan, 25 universities offer a bachelor’s degree in accounting.

The study plans in effect for the academic year 2017–2018 were analyzed to specify which courses should be included in the questionnaire survey to understand its importance from the perspective of the accounting academic staff of Jordanian universities and employers. The courses included in the survey are listed if at least seven universities (of the 25 universities) are offering this course. This threshold is chosen as it reflects that more than one quarter, and thus theoretically more than 25% of accounting graduates, have attended this course. However, although some courses, such as Accounting Ethics, are not offered by more than half of the universities, the researchers believe that it is still important to include these courses in the survey to evaluate their importance from the perspective of academic staff and employees.

Interviews

To specify the important skills and competences that an accounting graduate should have and thus included in the questionnaire survey, preliminary semi-structured interviews were conducted at this stage. Interviewing is one of “the most used data collection methods in the social sciences, a common method in accounting research” (Yin, 2003, p. 92). Semi-structured interviews are used when the researcher has a preestablished set of categories and questions that direct the interview (Wengraf, 2001).

Semi-structured interviews were used in this research. Choak (2012) argues that semi-structured interviews enable the researcher to address a defined topic while allowing the respondent to answer in their own terms. Thus, general questions regarding accounting courses and necessary skills were asked, and the respondents, both academic and professional, left to express their opinions, and to raise more issues. In addition, respondents were asked to express their opinions regarding the problems facing accounting education in Jordan and areas of possible improvement. Sixteen semi-structured interviews were conducted, with an average duration of an hour. Six of the interviews were with the academic staff in the accounting departments of three Jordanian universities; nine interviews were held with accountants, financial managers and auditors in Jordan; and one interview was with a member of the Board of Directors of the Jordan Association of Certified Public Accountants (JACPA). The aim of these interviews was to extract the respondents’ views on the skills and competences that accounting graduates should have when joining the market.

An initial list of skills and competences was adapted from Paisey and Paisey (2010), Mandilas et al. (2014), and Sithole (2015). This list was discussed with the interviewees, allowing them to suggest other skills and competences that they think are important for the Jordanian market. After each interview, a contact summary sheet was prepared, containing a summary of the main points raised during the interview, and summarizing the information obtained (Miles et al., 2014). The most cited skills and competences by interviewees became a part of the study questionnaire.

Questionnaire Survey

Based on the above two stages, a questionnaire survey was constructed. The questionnaire included three sections, the first section aimed at gathering demographic data around the respondents. The second section included the accounting courses and topics covered in the accounting curriculums of Jordanian universities, as identified in Stage 2 above. Respondents were asked to rate their view on a Likert-type scale of 1 to 5, based on the importance of the course or topic. The third section aimed to test two dimensions regarding the necessary skills and competences, as defined in Stage 2 above, that graduates of Jordanian universities should have: first, whether such skills are important in the workplace and needed by the market, and, second, do the graduates have such skills. Thus, respondents were asked to express their view twice regarding each skill and competence using the scale of 1 to 5, the first regarding the necessity of such skills and competences and the second regarding the availability of such skills and competences in the graduates of Jordanian universities. The final list of questions is included in the questionnaire survey.

The study population included the 25 public and private universities that offer an accounting degree. Of which, the questionnaire was distributed in paper form by hand to academics in eight randomly selected public and private universities. This questionnaire is addressed to all lecturers/professors teaching in the accounting departments. A total of 100 questionnaires were distributed, of which 70 were returned and included in the analysis.

For professionals, 300 questionnaires were distributed to auditors, financial managers, and accountants working in 32 companies and institutions randomly selected out of 100 listed industrial companies and audit firms functioning in Jordan. There were 228 applicable replies which were included in the analysis. The statistical software SPSS was used to analyze the questionnaires data. A reliability analysis was conducted to investigate the reliability of the study’s questionnaire. The means for the Ranking and Actual were calculated for each skill; the rank represents the respondents’ view on the importance of the skill, whereas the actual represents the respondents’ view about the actual skills that the graduated students they have.

Findings

Table 1 shows the number of questionnaires distributed and the response rate. Academic responses in Table 2 show that the majority of lecturers have more than 4 years of experience in teaching accounting courses (71.5%) and the reported results in Table 2 also reveal that the majority of the lectures (79.9%) have less than 4 years of professional experience. The characteristics of the professionals are listed in Table 3. This shows categories for the professional certificate they hold and their experience. As can be noticed, the majority of the respondents have a professional certificate and have more than 4 years of experience in the field.

Number of Institutions Contacted and Number of Replies.

Source. Questionnaire survey administrated to academics and professionals.

Academics’ Characteristics.

Source. Questionnaire survey administrated to academics.

Professionals’ Characteristics.

Source. Questionnaire survey administrated to professionals.

The results related to the importance of the courses from the point of view of the academics and professionals have been summarized in Table 4. The results show that there are differences between academics and professionals regarding the importance of the accounting course that should be included in the curriculum. However, both groups generally agreed on the top 10 courses which must be offered to students. In addition, they agreed on the top 10 courses; however, the importance of these courses differs between professionals and academics. For example, the table shows that professionals think accounting information system is a very important course and the average of the responses was the second highest after a tax accounting course, whereas academics think that this course is not an important one. We can notice from the table that the courses that have a special nature such as Government Accounting and Accounting for NGO and Accounting for specialized entities were classified as an unimportant course by both categories.

Ranked Importance of Accounting Courses.

Source. Questionnaire survey administrated to academics and professionals.

Note. IAS = International Accounting Standards; IFRS = International Financial Reporting Standards; NGO = nongovernmental organization.

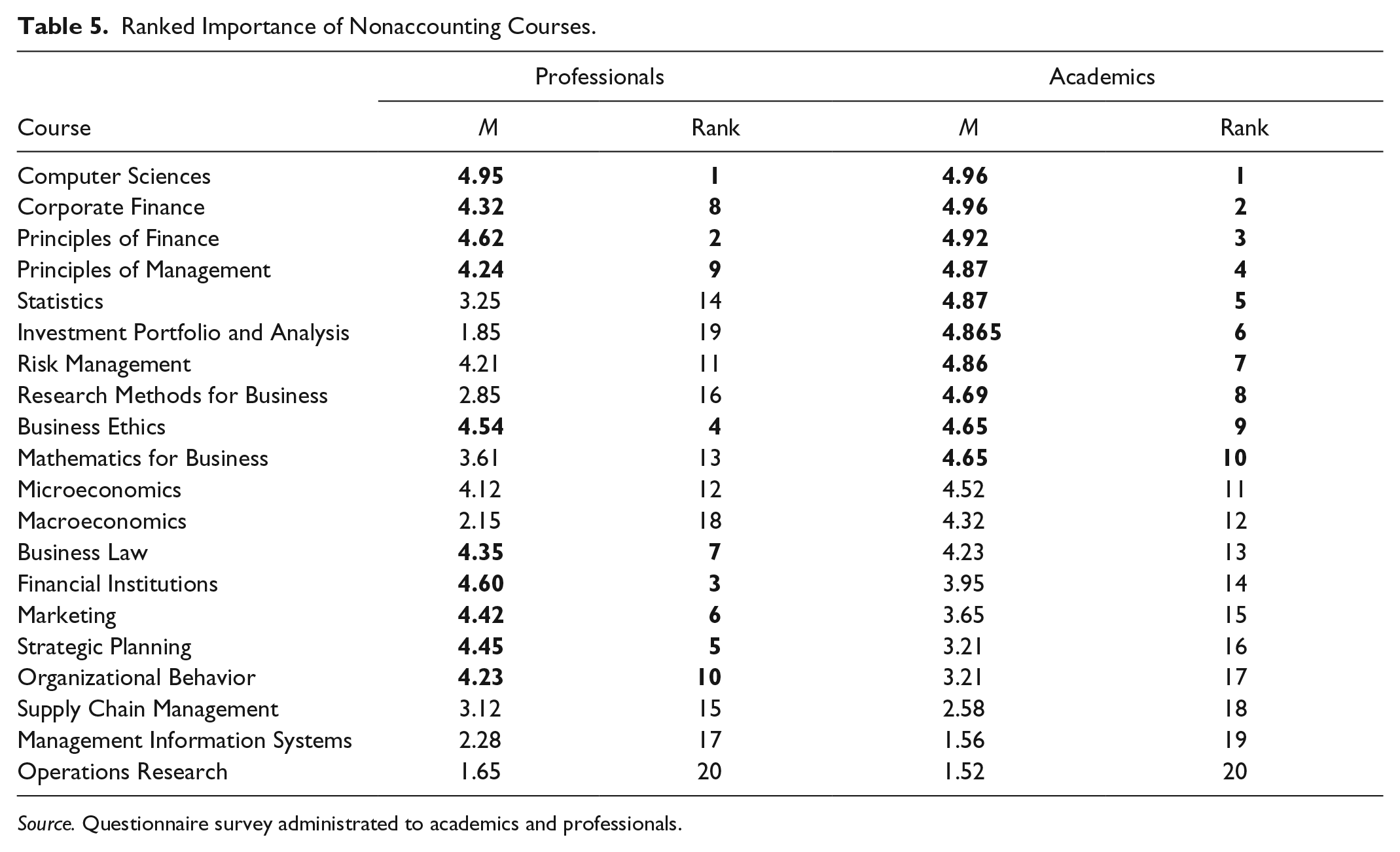

Contrary to the results regarding the importance of the accounting course where there is no significant gap between the two groups, the gap between the two groups is clear regarding the importance of nonaccounting courses (enhancement courses).

The professionals and academics had been asked to give their opinion on the importance for the nonaccounting courses included in the accounting curriculum. Table 5 summarizes the results of analyzing the answers gathered for this question. It can be noticed that both groups agreed on the importance of teaching computer skills to accounting students. This course’s average is the highest among all other courses. On the contrary, we can notice differences in ranking the highest 10 important courses between the two categories. It can be noticed that the academics give preference for finance courses (e.g., corporate finance, investment portfolio, and risk management), whereas the professionals prefer the courses that enhance managerial skills (e.g., strategic planning, organization, behavior and business ethics). The wide gap between academics and practitioners regarding the nonaccounting courses compared with accounting courses might have appeared because of the diverse backgrounds from which the respondents came from. Most of the study sample subjects, from both academics and practitioners, have, at least, an accounting bachelor degree, which affected their choices for the accounting courses as they all experienced and might have practiced many of the accounting topics. However, they graduated from different universities inside and outside of Jordan, with diverse nonaccounting course offerings. Furthermore, diverse working experiences for practitioners affected their choices for necessary nonaccounting knowledge. This would imply that accounting departments in universities, and regulatory bodies should take into account both accounting and nonaccounting knowledge fields when setting the standards for accounting curricula. These differences might be one of the reasons for the gap between market needs and the quality of the graduated students, which will be discussed in the coming part of this article.

Ranked Importance of Nonaccounting Courses.

Source. Questionnaire survey administrated to academics and professionals.

The results of the skills that the professionals and the academics think that the graduated students have (actual) and what respondents believe they should have (ranked) are summarized in Table 6. It can be noticed that both groups vary regarding the importance of the requested skills. For instance, the first five important skills from the point of view of the professionals are accounting software skills, ability to apply rules and regulations, planning skills, ability to apply theoretical knowledge, and negotiation skills, whereas the five important skills from the point of view of academics are written communication skills, problem-solving skills, computational skills, ability to work under pressure, and accounting software skills.

Skills and Characteristics Accounting Graduates Have (Actual) and Should Have (Ranked).

Source. Questionnaire survey administrated to academics and professionals.

This is calculated based on the calculated mean for the skills where the respondents have been asked to give their opinion about the importance of the skill. b This is calculated based on the calculated mean for the skills where the respondents have been asked to give their opinion about the actual skills that the graduated students have.

The two groups have been asked to give their opinion about the skills that the graduated students actually have. The results which are summarized in Table 6, reveal that the two groups agree on the first ten skills but disagree on the other skills. For example, the academics believe that the graduated students have team management ability which ranks 12 out of the total 23 skills, whereas the professionals think that this skill is almost inexistent among the graduated students. It ranked 20 out of 23 skills.

The results in the two tables reveal that there are differences between the desired skills and the actual skills, which indicate that the educational system might fail in achieving the market needs. For instance, the market considers that planning is a very crucial skill (ranked 3 out of 23; Table 6). The same respondents think that accounting graduates have not attained this skill as they anticipated (ranked 11 out of 23; Table 6). These results are supported by the interviews conducted with the academics and professionals.

To sum up, the results in general indicate there are differences between professionals and academics regarding the importance of the courses offered by Jordanian universities as well as regarding the skills that the graduates should obtain through their studies. These results are in line with prior studies worldwide (e.g., Jackson & Chapman, 2012; Mandilas et al., 2014; Zureigat, 2015).

The above-mentioned results show that professionals prefer to see more skills other than what the graduates already have. This was clear when they were asked about what were the skills that the graduates should have compared with what they actually had. For example, the skills regarding accounting software; professionals believe that this skill is very important—ranked 1; however, they also believe that, currently, this skill is ranked 15 (actual) in terms of the skills “they have now.” This might explain why professionals prefer that students should be taught more nonaccounting courses as they prefer to see more focus on managerial skills. Skills that are related to teamwork and management work such as negotiations, planning, and adaptability to new situations are the preferences for professionals. On the contrary, the academics prefer the skills related to solving problems and communications, mainly written ones.

These differences between academics and professionals might be caused by the educational system that is adopted by all universities in Jordan, which is the exam-oriented system not project-based system; exam-oriented systems enhance individuality and its related skills such as the ability to work independently, whereas the project-based system encourages teamwork and its related skills. In an interview with an accounting professor, she explained, We have time limitations in which we shall finish a specific material within the semester. I do have enough time or support to ask my students to prepare projects. You know, as a public university we have huge number of students, I have two exams during the semester for each course, which is more than enough. (Accounting Professor in a public university)

The results support the idea that the output of the exam-oriented system will not fit directly with the market needs. The results show that from the professional point of view, the graduated students are not attaining the requested skills by the market. For example, they think that the graduates do not have teamwork skills, which, from their point of view, is a very important one.

Conclusion

Accounting education in Jordan is mainly structured around AQACHEI’s requirements with specific knowledge fields and courses to be taught by Jordanian universities, with no reference to the market’s needs. This led to the emergence of a gap between the actual output of the education for an undergraduate accounting degree and what employers expect. Employing different research techniques with a large sample of professionals and academics, the results of this study found a significant gap with regard to the courses covered in the accounting curriculums of Jordanian universities, skills acquired by the students, and the market’s needs. It is also interesting that the educators in Jordanian universities perceive that some of the courses they teach are not relevant or essential (e.g., Accounting for Financial Institutions).

With regard to the courses taught by Jordanian universities, professionals and academics have different views regarding the importance of the accounting courses that should be included in the curriculum. However, both groups generally agree on the most important courses that should be taught to students, such as the basic accounting courses, Tax Accounting, International Financial Reporting Standards (IFRS), Computer Sciences, Accounting Information Systems, Finance, and business ethics. However, some of the courses found in the curriculum of Jordanian universities are found to be irrelevant by both groups, and thus shall be dropped, such as Accounting Theory, Accounting for Special Entities, Accounting for Financial Institutions, and Accounting for Governmental and NGOs. Perhaps such courses are of specialized nature that are not required in most businesses. Such very technical knowledge could be acquired by further training if the graduate works in a specialized entity such as a bank or a government entity rather than filling the curriculum with irrelevant courses at the expense of more important skills and knowledge.

For the skills that accounting graduates have, or should have, professionals and academics have different views regarding the importance of the requested skills. The first five important skills from the point view of the professionals are skills on accounting software, ability to apply rules and regulations, planning skills, ability to apply theoretical knowledge, and negotiation skills, whereas the five important skills from the point of view of academics are written communication skills, problem-solving skills, computational skills, ability to work under pressure, and skills on accounting software. However, professional accountants working in Jordanian businesses believe that the graduates of Jordanian universities lack such skills and competences, specially planning skills, teamwork skills, negotiation skills, time management abilities, applying accounting software, adaptability to new situations, and many others.

Perhaps the results of this study ring a bell regarding the whole accounting education system in Jordan, which focuses in transferring pure accounting knowledge and disregards the competences and skills required by the market. Two issues have participated to such a problem in accounting education in Jordan; first, the requirements of AQACHEI that enforces specific courses to be included in the curriculums of Jordanian universities, without regard to market needs. As explained by a panel of expert reviewers for the accounting programs in Jordanian universities, the “students gain technical expertise in accounting, but they are not able to pursue those courses that would develop the whole person” (Al-Hussein Fund for Excellence, 2012, p. 168). Liberalizing the accounting education would result in important improvement for skills acquired by students (Sangster & Wilson, 2014), perhaps it is the time to at least revise the methodology applied by AQACHEI in Jordan. Furthermore, it would benefit the Jordanian accounting educational system to incorporate the high-quality education standards of professional accountants and to facilitate the convergence of international and national education standards (IFAC, 2015).

The second issue, which was raised through the interviews, is that most accounting programs in Jordanian universities depend on exams as the only tool for assessing students, which would affect the communication skills and competences of students. As argued by Kosnik et al. (2013), “traditional testing methods of exams and quizzes do not always adequately assess students’ ability to identify relevant concepts and tools for problem-solving and to correctly apply the chosen models” (p. 623). This is consistent with Lightweis (2014), in which she indicated that a large part of the accounting education dilemma is due to the accounting educators themselves who only lecture and accounting students who memorize the information provided in these lectures, without focusing on the actual skills needed by the market place.

Recommendations

For accounting education in Jordan to be improved, it is suggested that more freedom be given to Jordanian universities in setting the curriculum for accounting programs. The accounting education in Jordan is now more than 50 years old, and universities have the capacity to develop their own curriculums. Accounting departments in Jordanian universities shall start revising their accounting curriculums to take into account market needs. Much of the courses taught now by Jordanian universities are not seen to be relevant to students, even by the educators themselves. Furthermore, more emphasis should be placed on the skills and capabilities of accounting students, rather than focusing merely on accounting knowledge in narrow areas. This would require eliminating many courses from the accounting curriculum of Jordanian universities and including more courses specialized in improving students’ soft skills and critical thinking. Finally, it is also recommended that there should be more involvement from professional accountants working in different economic sectors in setting the accounting curriculums for Jordanian universities.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Deanship of Graduate Studies and Scientific Research, German Jordanian University.