Abstract

This study has conducted a meta-literature review examining the past, present and possible future trends of Fintech research using 360 selected articles published between 2006 and June 2020. Both quantitative and qualitative techniques were applied. In the quantitative approach, a bibliometric citation analysis using HistCite and VOSviewer software was conducted and the qualitative analysis covered the identification of four main research streams related to (i) Bitcoin and digital currency, (ii) crowdfunding, (iii) mobile payment, and (iv) blockchain. The study results highlight the most influential aspects of the FinTech literature, such as the leading countries, institutions, journals, authors, and articles. Suggestions for the potential future direction of FinTech literature have also been made.

Introduction

Financial technology (Fintech) is probably one of the most noticeable recent innovations in the financial sector. Its potential to radically transform the financial sector by providing convenience and security to financial transactions has been highly appreciated. Innovative entrepreneurs have primarily led FinTech so far. However, it has also gained the attention of academicians and is being critically followed by regulators. It is a broad term and applies to many innovations such as InsurTech, RegTech, Robo advisers and AdTech. According to Gai et al. (2018), FinTech is a novel technology used in the financial services industry. Zavolokina et al. (2016) have opined that FinTech is the marriage of finance and information technology.

The new revolutionary FinTech technology is turning the world into a unique biosphere, one with more straightforward transactions and higher security. An innovative FinTech solution is available whenever and wherever one has to undertake a transaction, for example, riding a cab, shopping at a small retail store, or any online transaction. In many ways, it is changing the financial sector; minimizing the financial sector’s costs, improving the quality of financial services, and helping organizations manage their finances efficiently with high security against cyber-attacks (Subbarao, 2017). There are many factors behind this rapid development of FinTech, the most prominent of these is the increased role of IT in our day-to-day activities. Phenomenons like cloud computing, the internet, and big data have made it possible for the financial sector to enhance processes, services, and business models. InsurTech, Robo advisory services, and crowdfunding platforms have changed the horizon of the insurance, investment, and financial sectors (Puschmann, 2017). Another factor contributing to the rise of FinTech is the use of a more focused and specialized approach in the insurance and financial industry. The process of restructuring and resizing critical financial sector operations and the inclusion of Fintech startups for these operations has led to the development of a new ecosystem. The recent corporate inclusion trend from outside the financial sectors like O2 Telefonica and the Fidor Bank is one example of the change mentioned above. Studies like Nüesch et al. (2015) have indicated the increased use of electronic channels by customers to be another prominent factor for the growth of FinTech. The increasing fusion of the digital and the physical world has led to the development of new customer interaction methods (Brenner et al., 2014). The frequency of the use of interaction channels by customers has increased in the last decade. Hybrid client interactions have been introduced by most financial service providers resulting in the widespread use of FinTech. Limited regulations and encouraging response to the launching of initiatives like FinTech “sandbox” are other factors contributing to the rapid growth of FinTech. The actions of regulators in London, Singapore and Hong Kong showcase the presence of a soft regulatory framework in this regard.

Various studies have emerged on the theoretical and practical aspects of financial technology. From the adoption and technology acceptance perspective, S. Singh et al. (2020) suggested a research framework by adding the substructures of the technology acceptance model. Lee and Shin (2018) discussed the components of the FinTech ecosystem as comprising of technology developers, startups, financial institutions, end-users and regulators. Similarly, the utility and involvement of FinTech are present in several other technology sectors, for example, crowdfunding (Ahlers et al., 2015; Belleflamme et al., 2014; Hervé & Schwienbacher, 2018), mobile payments, (Shankar & Datta, 2018; Verkijika, 2020), virtual currencies (Baur, Hong et al., 2018; Dwyer, 2015; Urquhart, 2016), blockchain technology (Ahluwalia et al., 2020; Dai & Vasarhelyi, 2017), and cloud computing (Park & Park, 2017).

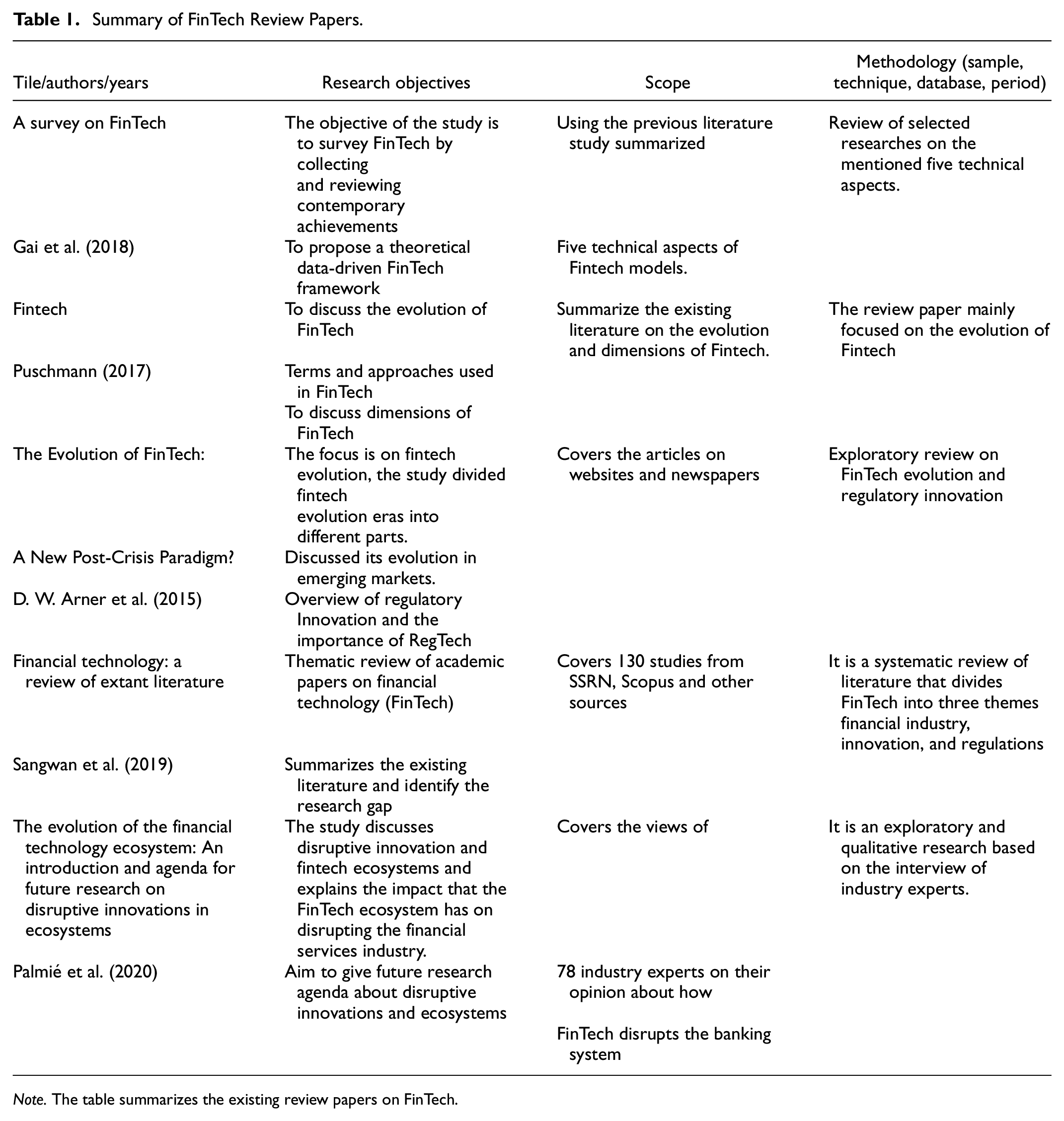

The majority of the FinTech literature emerged after the year 2015 (see Figure 2). Consequently, in recent years, various books, papers, and conference papers have also analyzed the existing FinTech literature (Gai et al., 2018; Gomber et al., 2017; Palmié et al., 2020; Puschmann, 2017; Sangwan et al., 2019). However, previous bibliometric reviews have either not undertaken an exhaustive literature search (see Table 1), or they were limited by their topic selection. Most previous studies provide limited information regarding the influential institutes and researchers in different streams or key technology aspects of FinTech. These studies have also not comprehensively covered the potential future research directions in FinTech. Against this backdrop, this study attempts to contribute to the existing literature by providing a more extensive bibliometric review of FinTech research by covering a large number of articles not covered before. The study will attempt to answer the following questions (1) What are the main areas of FinTech research? (2) Which are the leading institutions, countries, journals, and authors in the domain? (3) Which are the most influential and trending articles and topics? What are the key research streams in the FinTech literature? (4) What are the further research questions? This study goes beyond the limited scope of previous bibliometric review studies on FinTech. The researchers have conducted a detailed bibliometric analysis of the existing literature, published between January 1996 to March 2020. We selected the WOS database for the study and 1,360 published papers were selected. A comprehensive bibliometric citation analysis, a burgeoning technique mostly used by the review papers in the domain of management and social sciences, was then conducted (Bahoo et al., 2020). The majority of the review papers in finance have been based on the conventional survey method, focusing on a particular topic or issue (Ballester et al., 2019; Deku et al., 2019; French & Vigne, 2019; Garner et al., 2016; Nguyen & Boateng, 2015). However, some recent review studies in finance have used bibliometric citation techniques, for example, Helbing (2019) for literature on IPO, Paltrinieri et al. (2019) for literature on Sukuk, and Paltrinieri et al. (2019) for credit risk literature.

Summary of FinTech Review Papers.

Note. The table summarizes the existing review papers on FinTech.

This study has multiple findings; The results of the study highlight the influential aspects of FinTech literature, including the top authors, institutions, countries, country collaborations, journals, and articles. It also identifies and discusses the main streams of FinTech literature; these include Bitcoin, Blockchain, Crowdfunding, and Mobile payment streams. Finally, the authors identify the questions for future research in the field using the content analysis technique.

The rest of the paper is structured as follows; section 2 presents the research methodology, section 3 discusses the influential aspects of FinTech literature, section 4 provides an overview of the research streams and section 5 presents future research directions. Lastly, the conclusion is presented in section 6.

Research Methodology

Glass (1976) described meta-analysis as “the analysis of analysis.” It is a combination of different analysis types and is an ever-growing domain covering various aspects of the previous studies. A bibliometric approach is used to map and analyze academic research. The significant advantage of bibliometrics probably resides in the fact that the information yielded is generally highly compact, easy to handle, and likely to be objective (Jokić & Ball, 2006). In comparison, bibliometric citation analysis is a method used to create a citation network among various studies focusing on a particular area of research. Citation analysis is a burgeoning technique used in management, finance, and business research (Zamore et al., 2018). This study utilized citation analysis along with content analysis of the existing literature to bring forward the most eminent facets of the different streams in the FinTech literature. Previous studies in the management and finance literature have used the same methodology to explore various research domains (Bahoo et al., 2020; Fetscherin et al., 2010; Gaur & Kumar, 2018; Paltrinieri et al., 2019).

Sample Selection Process

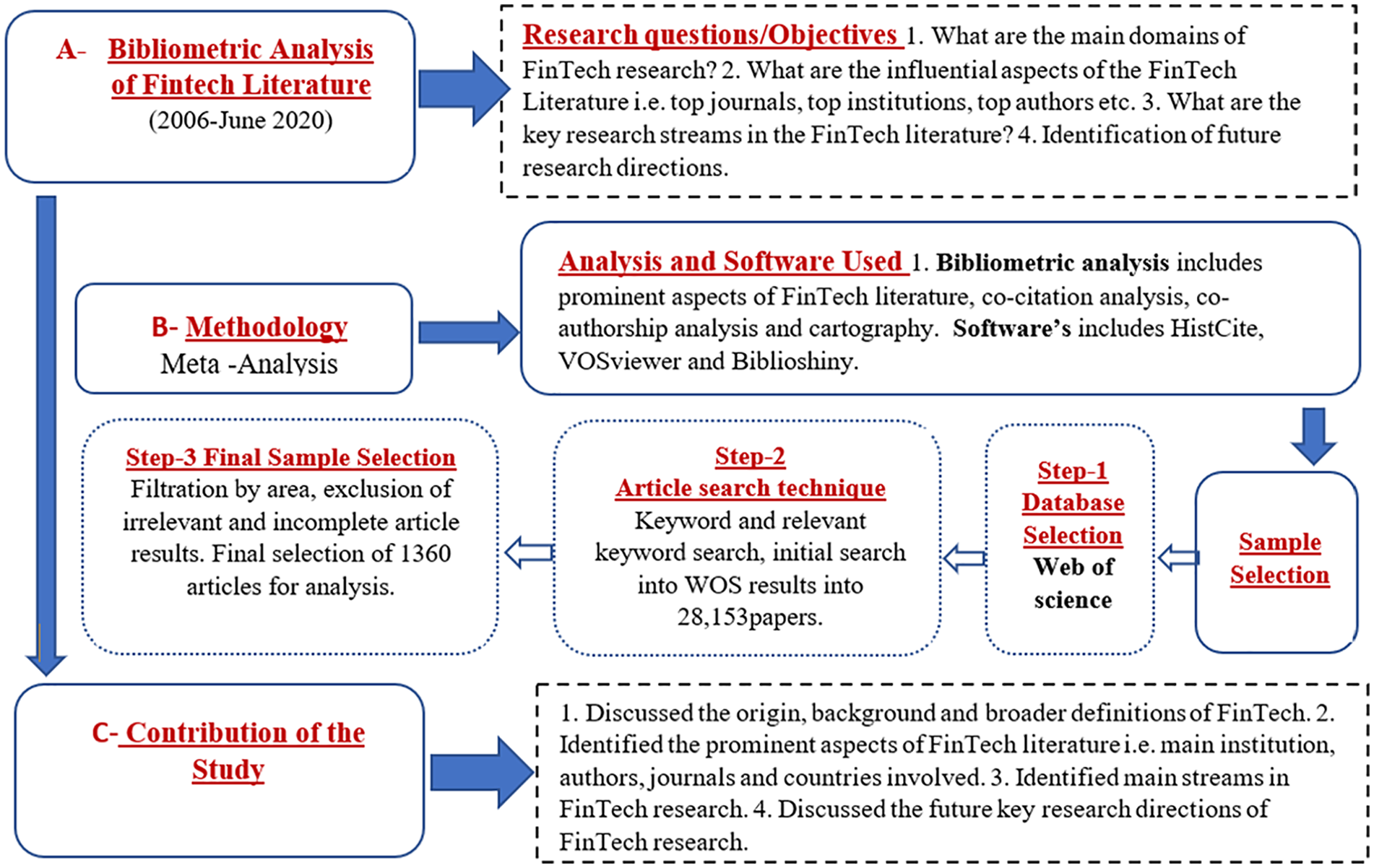

The sample selection process moved through three phases as shown in Figure 1. The first phase involved the selection of a database. For this purpose, the Web of Science database was chosen. The Clarivate Analytics’ Web of Science is a comprehensive and popular database for academic research studies encompassing high-quality scientific publications. It covers more than 12,000 multidisciplinary high impact factor journals and includes 55 social science disciplines (Analytics).

Methodology flowchart.

The second phase involved a literature search of the database using keyword search criteria. The selection of appropriate keywords was crucial in this phase to ensure that the full body of literature was covered. The keyword base selected by J. Liu, Li et al. (2020), given the scope of earlier studies on the topic and the need for more comprehensive coverage in the current study. Further keywords like RegTech, PropTech, big data, Samsung pay, micropayment, sandbox, ICO, GovTech, altcoin and digital wallet were also added. The following search query was used:

TS = (fin-tech OR fintech OR “Fin tech” OR “financial technology*” OR “P2P lending platform” OR “Online lending” OR Crowdfund* OR “Transaction terminals” OR “Payment terminals” OR “Cashless payment*” OR Paypal OR Alipay OR Blockchain OR “Smart contract” OR “Digital currency” OR “Bitcoin” OR “Cryptocurrency” OR “Mobile payment” OR “Mobile point of sale” OR “Robo-advisors” OR “Automated portfolio management” OR E-bank* OR “mobile bank*” OR InsurTech OR micropyament* OR “micro payment*”)

One of the objectives of the extensive keyword query was to conduct an exhaustive search for relevant articles and to include those not covered by earlier studies. 28,153 papers were, thus retrieved in the pre-filtration phase.

The third phase of the sample selection process involved data filtration. After a keyword search, the retrieved sample must be assessed for authenticity and relevance. The filtration process ensures this in a study (Budgen & Brereton, 2006). Here it involved many steps. During the data filtration process, all studies from scientific fields not related to the area of research were excluded. Only studies related to the fields of economics, finance, business, and management were kept. Furthermore, papers with incomplete and missing information were excluded. Finally, following Zott et al. (2011), the authors ensured that all of the articles in the final selection were related to Fintech. Two independent authors contributed to the process to ensure that the articles were filtered according to the study criteria. The process resulted in 1,360 highly relevant records. These included 1,239 journal articles, 66 editorial materials, 45 review papers, 8 proceeding papers, 1 book chapter and 1 data paper. Book reviews and meeting abstracts were excluded.

The quantitative assessment (citation analysis) was conducted using HistCite and VosViewer software. Both are powerful tools for such analysis and have been used in previous studies (Alon et al., 2018; Bahoo et al., 2020; Helbing, 2019; Paltrinieri et al., 2019).

Meta-Literature Review

The meta literature review was conducted in multiple stages following Paltrinieri et al. (2019). These involved (i) identifying the influential aspects of FinTech Literature, (ii) conducting the co-citation and co-authorship analysis, and cartography, and (iii) conducting the content analysis. First, a citation analysis was conducted using the HistCite software to determine the influential aspects of the FinTech literature. The database search yielded 1,360 articles by 2,672 authors published in 424 different journals. A co-citation andco-authorship analysis was done using the VOSviewer. The distance-based mapping technique was used in the VOSviewer to visualize connections (van Eck & Waltman, 2010). Co-citation analysis was useful in the identification of streams and clusters in the selected literature. Similarly, co-authorship analysis helped identify the authors working in the same area of research. Cartography analysis was also conducted. It analyzes the network of reoccurring keywords obtained by using VOSviewer. The analysis is based on the assumption that keywords represent the content in an article, and similar keywords create a cluster in a field (Ding et al., 2001). The keywords in the cartography network represent the extensions of research surrounded by the main research domain.

Finally, a brief content analysis of the main streams in the literature was conducted using citation analysis. The dimensions and findings of these have been discussed in the identified streams. It is a useful technique to recognize and confirm bibliometric citation analysis; it also helps identify future research directions (Paltrinieri et al., 2019).

The Influential Aspects of the FinTech Literature

Annual Scientific Production

Figure 2 presents the year-wise publications, total local citations received per year (TLC/t), and total global citations received per year (TGC/t) trends in FinTech research between 2006 and 2019. The trend analysis shows that publications and citations have gradually increased over time, with most growth seen between the years 2017 and 2019. The most productive years were 2018 and 2019 with 299 and 499 publications, respectively. However, the maximum TLC/t (447) and TGC/t (1254) appeared in 2018.

Yearly research Trend.

Top Influential Countries and Institutions

Although the FinTech domain is relatively new, the swift growth in FinTech literature in recent years is worth mentioning. Therefore, it is vital to identify the centers of excellence related to FinTech research in terms of countries and institutions.

Table 2, indicates the top 10 countries involved in FinTech research. We have identified top countries based on the number of papers published (PFT > 50), total local citations, and (TLC) and total global citations (TGC). The country-wise analysis showed that the United States of America, the United Kingdom, China, Germany, France, Italy, and Canada were the most active countries in terms of publications and citations. As can be seen, they are listed among the top 10 in all three categories. The USA and the UK were the top two countries in all three categories of the list. The USA is ranked one in all three categories (PFT = 319, TCL = 2,099, TGC = 6,235), followed by UK (PFT = 183, TCL = 1,253, TGC = 3,242). China and Germany are ranked third and fourth rank with 164 and 117 publications, respectively; however, China received only 434 TCL and 1835 TGC. France, Italy, and Canada have produced 115, 64, and 55 publications and received 2,469, 912, 1,234 TGC each.

Most Influential Countries in FinTech Research (2006–June 2020).

Note. The table shows the ranking of 10 influential countries based on various classifications.

Countries sorted based on the number of published papers in the period selected.

Countries sorted based on TLC.

Countries sorted based on TGC.

Figure 3 displays the top 20 country research collaboration map by Biblioshiny software based on the affiliation of authors involved in the Fintech research. The minimum edge parameter was taken as 5. The United States of America emerged as a top collaborator with the United Kingdom (31 publications), China (27 publications), France (19 publications), followed by China with the United Kingdom (18 publications), and France with Lebanon (17 publications) and others.

Research collaboration.

Further, the top 10 organizations producing research publications on FinTech are shown in Table 3. The table shows the ranking of the top 10 most influential institutions based on the number of published papers (PFT > 10) in the period selected as well as based on TLC. The study results showed that the University of Montpellier, France, Holy Spirit University, Lebanon, Southampton University, United Kingdom, University of Dublin, Ireland, and Politecnico di Milano, Italy, were the most active organizations in terms of publications and local citations. They were among the top 10 in both categories. The University of Montpellier, France, and the Holy Spirit University, Lebanon, were the two most successful and productive organizations in both categories of the list. As can be seen, the University of Montpellier is ranked first in both categories (PFT = 23, TLC = 385), followed by the Holy Spirit University (PFT = 17, TLC = 235). The Southampton University is ranked fifth (PFT = 13, TLC = 253), and the University of Dublin is ranked fourth rank (PFT = 11, TLC = 200) on the list. The Politecnico di Milano is ranked at the bottom of the list with 10 publications and 194 local citations.

Most influential Institutions in FinTech Research.

Note. The table shows the ranking of 10 influential institutions producing research in the area of FinTech. TLC = total local citations.

Institutions sorted based on the number of published papers in the period selected.

Institutions sorted based, on TLC.

Table 4 shows the top 15 influential departments within institutions producing research in the area of FinTech. The list of departments/schools are sorted based on the number of published papers in the period selected. In the case of multiple departments with the same number of publications, priority was given to the department with the highest local citation score. The USEK Business School, the Holy Spirit University, the Montpellier Business School, the University of Montpellier, the Trinity College, Dublin, and the University of Dublin, remained the most productive Institutions. Such findings would be useable for other countries and institutions while deciding on collaborations on multiple research projects and organizing workshops on FinTech (Fetscherin & Heinrich, 2015).

Prominent Departments/Schools Within Most Influential Researching Institutions.

Note. The table shows the influential departments within institutions producing research in the area of FinTech.

Departments/schools sorted based on the number of published papers in the period selected. In the case of multiple departments with the same number of publications, priority is given to the department with the highest LCS (local citation score).

Most Influential Journals

The awareness regarding top journals and prominent authors in FinTech research would be beneficial for researchers working in the area. Within our main dataset, the 1,360 selected articles have been published in 424 journals related to finance, economics, management, and some multidisciplinary areas. These journals’ impact in terms of the number of publications, total local citations per year (TLC/t), and total global citations per year (TGC/t) are highlighted in Table 5. Three journals had over 40 publications. We also identified the top 10 most influential journals to promote their recognition. We determined the leading 10 journals in three categories based on the number of articles published, TLC/t, TGC/t received per year. The top three journals in the PFT category included Finance research letters, Economics letters, Electronic commerce research, and applications. The Entrepreneurship Theory and practice and the Journal of business venturing also remained influential in TLC and TLG categories, respectively.

Most Influential Journals in Fintech Research.

Note.The table shows the ranking of 10 influential journals based on various classifications.

journals sorted based on the number of published papers in the period selected,

journals sorted based on TLC/t.

journals sorted based on TGC/t.

Most Influential Authors and Co-authorship Networks

Table 6 highlights the top 10 influential authors/researchers in the FinTech literature. They are ranked based on the total local citations received per year (TLC/t). It can be seen that three authors had more than 10 publications each, but David Roubaud had the highest 113.5 TLC/t amongst all. Similarly, Elie Bouri, who is ranked second on the list, had 18 publications, 98.5 TLC/t and 327 TLC, followed by Andrew Urquhart with 62.9 TLC/t, 237 TLC and eight publications, and Ethan Mollick with 51.35 TLC/t, 339 TLC and three publications. Brian Lucey, who is at the bottom of the table, had eight Fintech publications and received 35 TLC/t, 93 TLC citations.

Most Influential Authors and Co-Authorship Networks in FinTech Research (2006–June 2020).

Note. This table indicates the top 10 influential authors among all authors using HistCite software. The ranking is done based on the total local citations received per year (TLC/t).

The major co-authorship networks among authors working in the domain of FinTech were also investigated. The analysis was performed using the VOSviewer (Piette & Ross, 1992). For this purpose, criteria were set at a minimum of seven collaborative publications and a minimum of 50 citations. As indicated by Figure 4, we found four main clusters of authors working in collaboration. Table 7 highlights these co-authorship networks with key references. Such networks show research collaboration, which is a key mechanism that links distributed knowledge and competencies into novel ideas and research avenues (Heinze & Kuhlmann, 2008). Furthermore, co-authorship in research articles is considered a reliable proxy of research collaborations (Barnett et al., 1988).

Co-authorship networks.

Co-Authorship Network.

Influential and Trending Articles

HistCite software was used to highlight the most influential and trending articles based on citations. Due to the growing nature of the literature in FinTech, such analysis might help researchers to set their future directions and research agenda. The influential articles included articles with high local citations per year TLC/t. The trending articles included the articles that have received high citations in the last period under selection TLCe, which comprised of the last 3 years in our data.

There are three articles in this list that have received over 27 TLC/t and were top-ranked in both citation categories. These include articles by Mollick (2014), who attempted to explore the dynamics of success and failure among crowdfunding endeavors; Belleflamme et al. (2014), who compared two forms of crowdfunding using a theoretical framework; and Ahlers et al. (2015), who have empirically examined the effectiveness of signals on the success of equity crowdfunding. Interestingly all the top three articles were from the crowdfunding domain, indicating the popularity of the domain. Other prominent papers in the list include those by Urquhart (2016), Cheah and Fry (2015), and Bouri et al. (2017), which highlight the inefficiency of bitcoin, speculative bubbles in bitcoin pricing, and bitcoin as a diversifiable asset, respectively. It is worth mentioning here that bitcoin is the other major domain that remained the most influential and trending apart from Crowdfunding (Tables 8 and 9).

Ranking of the Top 10 Influential and Trending Articles and Topics in FinTech Literature.

Note. This table represents the most influential and trending articles/topics.

The influential articles/topics are sorted based on TLC/t having a minimum number.

Trending is based on the criterion of a minimum TLC(e/b). the list of journals is provided in Appendix A.

Summary of Key Papers in Each Stream.

This table represents the most influential and trending articles/topics. 1 = The influential articles/topics are sorted based on TLC/t having a minimum number. 2 = Trending is based on the criterion of a minimum TLC(e/b). the list of journals is provided in Appendix A,

Keyword analysis

Figure 5 reveals the results of the cartography analysis conducted through the VOSviwer software. This type of analysis helps to identify the keywords under each research stream in a research area. The minimum selected scale of co-occurrence for a keyword was set at 20. Out of the 2,475 keywords used by authors, only196 met the threshold (criterion). The distance and size of the bubble define the number of keyword occurrences and associational links. These 196 keywords are associated with four main clusters. Each color represents the cluster with associational links among the keywords.

Keyword analysis.

The largest cluster, in blue, represents the studies relating to bitcoin and digital currency. These studies discussed the topics relating to volatility, hedging properties, risk, and return relating to bitcoin. Whereas, the red color cluster represents the cluster of Crowdfunding articles associated with Kickstarter, peer to peer lending, equity and crowd investing, etc., comprise this cluster. The green cluster is the third-largest cluster and includes studies relating to Fintech, innovation, and mainly issues relating to blockchain technology. Similarly, the yellow color cluster highlights mobile payment, mobile banking, and other related studies.

Three-Factor Analysis (Organizations, Keywords, and Country)

Figure 3 presents a diagram of the published literature on Fintech focusing on the relationship among three factors, that is, top keywords, organizations, and countries. The top 10 keywords included Crowdfunding, entrepreneurship, Fintech, marketing, innovation, Blockchain, bitcoin, mobile payment, cryptocurrency, equity crowdfunding. These keywords seemed to have a relationship with 10 organizations, including the University of Minnesota; the University of California, Berkeley; the Southwestern University of Finance & Economics; the University of Science & Technology, China; the Perking University; the Copenhagen Business School; the University of Illinois at Urbana–Champaign; Montpellier Business School; and the Holy Spirit University of Kaslik. Furthermore, these organizations mainly had a strong relationship with 10 countries, that is, the United States of America, China, France, Italy, Germany, Canada, the United Kingdom, Australia, Spain, and India (Figure 6).

Three-factor analysis.

Review of FinTech Research Streams

As discussed earlier, a co-citation analysis of the FinTech literature was also conducted in this study. Co-citation analysis is a kind of investigation intended to map out the linkages between the top-cited articles and the articles citing them (Alon et al., 2018). Following the studies of Alon et al. (2018) and Bahoo et al. (2020), we used HistCite to conduct this analysis. This type of analysis depends upon the size and the growth of the literature. We used a two-step strategy to perform the co-citation analysis. In the first step, we used the top 75 cited articles in the sub-samples with (TLC ≥ 20) and highlighted the main clusters of studies around one topic. The detail of the analysis is given in Figure 7 given below. The cited articles are positioned along the horizontal axis in the Figure, whereas the years are mentioned along the vertical axis. In the second step, two independent authors conducted the content analysis of the selected sample of articles. This analysis includes the review of title, author, journal data, methodology and key findings of the studies.

Co-citation analysis.

This content analysis, along with the bibliometric analysis conducted in the previous section, enabled us to identify four main interrelated streams in the FinTech literature, that is, (1) the bitcoin and digital currency stream, (2) the crowdfunding stream, (3) the blockchain technology stream, and (4) the mobile payment technology stream. Further study of these streams revealed the interesting sub-streams available in the literature. Given below is a brief discussion on these four streams and sub-streams.

Bitcoin and Digital Currency Stream

The emergence of Bitcoin in 2013 is probably one of the most prominent events in the currency markets in recent years. Its launch by computer hobbyists has started a new era of a digital asset class. Since its inception, not only Bitcoin’s exchange rate has broken all the records, but a unique assortment of digital currencies have also flooded the market. Since the inception of the idea of Bitcoin idea by Satoshi Nakamoto, considerable debate has emerged on its different traits among academic, professional, and regulatory circles. A large number of articles in our selection also discussed the various features of Bitcoin. Topics like the volatility, return behavior, hedging and diversification properties of Bitcoin, its efficiency as an asset class, and its regulatory aspects have gained a lot of attention.

Market efficiency of Bitcoin

Urquhart (2016) found the Bitcoin market to be an inefficient one with a probability of moving toward a more efficient market. Similarly, Panagiotidis et al. (2019) explored the effects of variables like capital market returns, Federal Reserves and European Central Bank rates, gold, exchange rates, oil returns, and internet trends on bitcoin returns. The study observed that bitcoin enjoyed a strong interaction with traditional stock markets and had a weaker association with foreign exchange markets as well as the macroeconomy.

Volatility of Bitcoin

Besides, the volatility pattern of Bitcoin viz-a-viz other assets like gold, currencies, and oil is a significant concern. Anne Haubo Dyhrberg (2016) posited that using the scale from pure medium of exchange advantages to pure store of value advantages, bitcoin may fall between gold and the American dollar. Fang et al. (2019) showed that the economic policy uncertainty affects global equities, commodities and Bitcoin’s long-run volatilities. Moreover, Bitcoin also serves as a hedge against specific economic uncertainty conditions as global economic policy uncertainty exerts a significantly negative impact on Bitcoin-bonds correlation while positively and significantly influencing Bitcoin-equities and Bitcoin-commodities correlations. Köchling et al. (2020) assessed the quality of Bitcoin volatility forecasting of GARCH-type models by applying different volatility proxies and loss functions by constructing model confidence sets. They found these models to be systematically smaller for asymmetric loss functions and a robust jump proxy.

Bitcoin returns

It is also important to examine issues related to the predictors of bitcoin returns and the uncertainties involved in achieving bitcoin returns. Smales (2020) observed that a single principal component explained a substantial proportion of cryptocurrency returns variation. This component is highly correlated with bitcoin returns and exhibits the greatest explanatory power for larger cryptocurrencies. Baur et al. (2019) observed time-specific anomalies in Bitcoin returns but no persistent effects across time by investigating intra-day, time-of-day, day-of-week, and month-of-year effects for Bitcoin returns and trading volume. In comparison, they observed persistent differences in trading activity across all exchanges experiencing lower activity during local evening hours and on weekends.

Hedging and diversification properties of bitcoin

It is worth mentioning that bitcoin can be effectively used for hedging. Hussain Shahzad et al. (2020) reported that bitcoin had hedging properties, however, gold was a superior hedging instrument as compared to bitcoin. Ehlers and Gauer (2019) found that Bitcoin, Ethereum, Dash, CAD, JPY, and EUR contributed toward the reduction of the variance of a mixed portfolio. Moreover, in a portfolio comprising of only cryptocurrencies, Bitcoin and Ripple exhibited the largest diversification effect. Damianov and Elsayed (2020) observed that Bitcoin was relatively isolated from traditional industries and showed a near-zero correlation with traditional financial assets. Although it provided investors with some diversification benefits, these benefits are counterbalanced by the asset’s volatility.

Moreover, in terms of the liquidity and diversification benefits of Bitcoins, Anne H Dyhrberg et al. (2018) found that, for retail size transactions, Bitcoin was highly investible as the average quoted and effective spreads for Bitcoin were found to be lower than spreads on major equity exchanges. Baur, Dimpfl et al. (2018) demonstrated that Bitcoin offered distinctively different returns, volatility, and correlation characteristics than other assets like the US dollar and gold.

Crowdfunding Stream

One of the most critical needs of all new projects is the initial capital requirement. Crowdfunding is an innovative mechanism for fulfilling the financing needs of new for-profit, social, and cultural projects. The initial founders of such ventures may request funds from local or global contributors and the return of the contribution can be in the form of equity or future product (Mollick, 2014). The size and the objectives of the crowdfunding ventures vary. These may include individual skill-based projects with small seed capital requirements to the projects that require millions of dollars as initial requirements for which traditional venture capitalists were used as funding sources. Although Crowdfunding resembles concepts like micro-finance and crowding sourcing, it still has its uniqueness, with a growing number of websites developed for different types of Crowdfunding.

Equity crowdfunding

There are several kinds of crowdfunds. To begin with, equity crowdfunding (ECF) provides entrepreneurs with an online social media marketplace which facilitates their access to numerous potential investors who are in a position to supply financing for projects in exchange for an ownership stake. Estrin et al. (2018) observed that ECF platforms were instrumental in channelizing large financial flows to entrepreneurs in the UK. Such investments are deemed as high risk with high returns. Ahlers et al. (2015) empirically examined the effectiveness of signals provided by entrepreneurs to motivate investors for a funding commitment to investigate the success factors for an Equity Crowdfunding campaign. The study concluded that detailed information about the venture’s inherent risks would be a useful signal with the potential to make the campaign successful.

Entrepreneurial aspect of crowdfunding

Since the traditional financing sources have remained subpar for many types of social entrepreneurial ventures, Crowdfunding has attracted the attention of entrepreneurs in this regard. Websites like Kickstarter have proved to be vital sources of funding for a variety of entrepreneurs, especially for social entrepreneurs. Parhankangas and Renko (2017) examined the linguistic style of crowdfunding campaigns and concluded that a more relevant and logical linguistic style was important for a campaign’s success. Amedomar and Spers (2018) showed that Technology-Based Companies selected reward-based Crowdfunding as a funding model. In their early developmental stages, they required funds for financing specific projects and exhibited motivations not directly involving the raising of funds.

Reward-based crowdfunding

Contributors of the capital in a reward-based Crowdfunding campaign receive non-monetary benefits as a return. It may include pre-ordering of product, an acknowledgment, credit for a game, etc. Entrepreneurs have raised a considerable amount of money by posting their projects on reward-based crowdfunding websites. The role of incentives and pledges has been discussed by Crosetto and Regner (2018), who posited that the project’s success is only partially path-dependent as the bulk of projects eventually succeeding do not follow a successful track for 75% of their funding period. Although early pledges may predict project success, it does not necessarily imply that their absence will result in failure.

Moreover, the role of geography in Crowdfunding’s success has been discussed by Giudici et al. (2018), who showed that certain salient features of the geographical area, where entrepreneurs performed the business activity, influenced the crowdfunding success projects they proposed. In this respect, people’s altruism in the vicinity enhances the probability of success, depending upon the area’s level of social capital.

Peer to peer lending

In recent times, Peer-to-peer (P2P) lending has surfaced as a network form of Crowdfunding facilitating loan originations outside the traditional banking model. This platform provides anonymous connectivity between borrowers and lenders. It encourages both borrowers and lenders by providing a source of funding and investment outside the orthodox intermediary circles (Barasinska & Schäfer, 2014). Studies like Nisar et al. (2020) have examined the known risks to Chinese P2P companies. The regression model results indicate several factors such as marriage, income, and house property that could predict risk and financial management.

Mobile Payment Stream

In recent years, mobile phone devices surpass routine communication requirements. Now more and more value-added services, including mobile commerce and payments are outdoing the regular mobile uses. Moreover, the mobile phone is the most used device for product sale and purchase, product delivery and other e-commerce services (Dahlberg et al., 2008). Mobile payment is one such function of the, smartphone, which has witnessed remarkable growth in recent years. The payment function of mobile phones covers a variety of scenarios for example, payment of utility bills, money transfer, payments at the point of sales etc. This growing and novel use of mobile payment is no doubt very innovative. This innovation has been undoubtedly an important attribute behind the success of mobile payments. Zhong and Nieminen (2015) found that inter-organizational co-innovation was a successful strategy for mobile payment service innovation.

Trust of mobile payments

The trust of mobile payments is an important issue. N. Singh and Sinha (2020) measured the influence of variables like perceived usefulness, perceived compatibility, perceived cost, awareness, perceived customer value addition, and perceived trust on a merchant’s intention to use a mobile wallet technology. Their findings revealed that perceived customer value addition had the highest effect on merchants’ intention, followed by the perceived usefulness of the technology. The perceived trust showed a small but significant mediating effect on the perceived usefulness. Shao et al. (2019) investigated the differences between female and male consumers in respect to several trust-building mechanisms in the context of mobile payments. They found security to be the most significant antecedent of customers’ trust, followed by platform reputation, mobility and customization. For the male customers, mobility and reputation had stronger influences in building trust. On the other hand, for the female customers, security and customization had more pronounced effects on trust.

Adoption and acceptance of mobile payments

In terms of the adoption of mobile payments, Humbani and Wiese (2019) assessed the adoption and the intention to continue the use of mobile payment applications. They found the “drivers” better explained adoption as compared to the “inhibitors,” whereas satisfaction emerged as the strongest predictor of continuance intentions. de Luna et al. (2019), however, indicated that mobile payment behavior could not be applied globally.

Gupta and Arora (2019) observed that performance expectancy, effort expectancy, habit, and facilitating conditions were significant predictors of behavioral intention that, in turn, significantly predicted the use behavior regarding the use of mobile payment systems. Moreover, both social influence and hedonic motivation were found to be weak predictors of behavioral intention.

Blockchain Stream

A blockchain is an Internet-based peer-to-peer system constituting an integrated framework of independent and connected computers capable of simultaneously recording and verifying transactions. It improves business efficiency, lowers costs, enhances transparency, and provides a comprehensive history of all transactions. Nevertheless, it carries certain risks like data security issues, third-party vendor risks, technological risks, and interoperability risks. There were around 270 papers in the selected database that discussed various themes related to Blockchain.

The concerns about Blockchain

The security concerns are an essential caveat in the growth of Blockchain. White et al. (2020) emphasized that auditors who were advising clients on blockchain technology should possess the relevant knowledge and expertise of the technology and have the capability to assess the risks inherent in it. Park and Park (2017) focused on the security concerns related to the blockchain technology being used by governments. The study found that the security risk could be reduced if 10 fundamental objectives like data privacy, transparency, integrity, cost, etc., were addressed properly. Moreover, key strengths and weaknesses of blockchain technology have been reported by Babich and Hilary (2020). The key strengths identified were aggregation, visibility, automation, validation, and resiliency. On the other hand, the lack of standardization, black box effect, lack of privacy, garbage in/ garbage out, and inefficiency were highlighted as weaknesses of the technology.

Blockchain and smart contracts

The emergence of Blockchain technology has facilitated the debate on smart contracts. One key element of this debate is the idea of decentralized consensus, which is a technique for large network participants to arrive at a perfect agreement on a shared document. Since blockchain technology enlarges the contracting space and has the characteristics of cryptographical algorithms and decentralized consensus, it facilitates the emergence of smart contracts (Cong & He, 2019). By virtue of enhanced entry and competition, smart contracts may remove information asymmetry and improve welfare and consumer surplus. However, the distribution of information during consensus generation could promote more significant collusion.

Blockchain and the accounting profession

Although the scope of blockchain technology was initially limited to recording cryptocurrency transactions, over time, its application has increased in banking and finance, financial markets, electoral voting systems, the insurance sector and the accounting and audit sector (Dai & Vasarhelyi, 2017). Yu et al. (2018) discussed the application of Blockchain in financial accounting and its possible effects. They suggested that, in the short run, public Blockchain could be used as a platform for firms to disclose information voluntarily. It could effectively reduce disclosure and earnings management errors, improve the quality of accounting information, and mitigate information asymmetry in the long run. Furthermore, through an accurate and timely automatic assurance system, technology could become convenient in the audit profession (Dai & Vasarhelyi, 2017). Schmitz and Leoni (2019) listed themes like transparency, trust issues and governance in the blockchain ecosystem to argue that accounting and auditing have distinguished businesses’ requirements based on Blockchain.

Future Research Directions

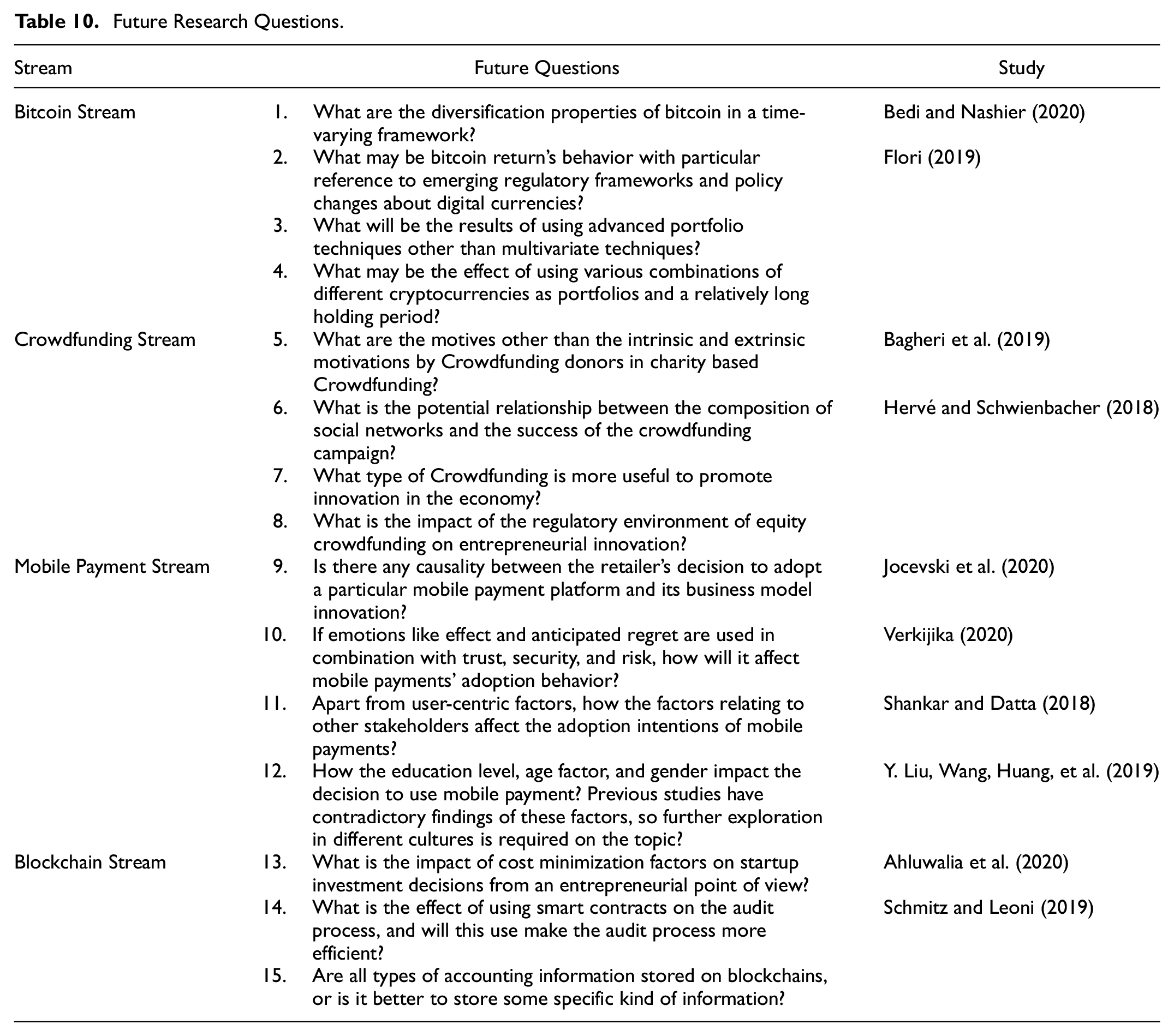

The various analyses conducted in the study, including the citation analysis, the examination of influential aspects, and the investigation into the contents of the major streams, have enabled us to highlight future research directions in the Fintech literature. This future research agenda is presented in Table 10.

Future Research Questions.

The various aspects of Bitcoin technology have been well researched in the last 10 years, however, certain areas still require further investigation. In recent years, Bitcoin has remained very popular in the investment community. Researchers have also focused their attention on the investment and diversification properties of Bitcoin. Bedi and Nashier (2020) used the VAR and variance approach to examine the diversification properties of Bitcoin combined with five major fiat currencies. However, the authors recommended that future researchers might test Bitcoin’s diversification characteristics in a time-varying framework. Moreover, it is pertinent to observe Bitcoin’s combination with other asset classes in the scenario of regional financial markets in different economic conditions. Another exciting aspect for future research might be the investigation of Bitcoin return behavior in the different regulatory frameworks. Since the FinTech regulations in various parts of the world are still in the evolving phase, the Bitcoin return behavior would be exciting to investigate with the emergence of an ever-changing regulatory setup. Similarly, Flori (2019) suggested some interesting dimensions of future research including the use of advanced portfolio techniques other than the commonly used multivariate methods in the case of bitcoin investment. Furthermore, the study suggested using various combinations of different cryptocurrencies as portfolios; this testing should be done for a relatively long holding period.

The biggest challenge faced by any new venture is to attract funding sources. Crowdfunding is one source of funds that has gained immense popularity in recent times. The research circles have also investigated various aspects of Crowdfunding. However, there are certain aspects of Crowdfunding that require further exploration. Studies like Bagheri et al. (2019) have analyzed the motivations of donors in charity-based Crowdfunding. The study suggested exploring the motivations other than intrinsic and extrinsic motivations by Crowdfunding donors in charity based Crowdfunding campaigns. Moreover, further studies might be conducted to ascertain the linkages between the various features of the crowdfunding platform and the success of the campaign.

Finance and financial institutions are important for the economy because they not only play a role in the selection of investment opportunities and the allocation of resources but also the financing of innovation (Schumpeter, 1912). The function of selecting the best projects is crucial for the economy because innovation is an important source of growth. Since innovation is critical for the overall development of any economy, innovative ideas need necessary funding from both traditional and non-traditional funding sources. Crowdfunding platforms have been proven to be very useful in boosting entrepreneurial innovation. Furthermore, these platforms also allow providers of the fund to participate in the innovation process. In this regard, certain research queries require further attention from researchers. These include, what type of Crowdfunding is more useful to promote innovation in the economy? How is the regulatory environment of equity crowdfunding on entrepreneurial innovation?

Regarding mobile payments, we suggest an investigation into the relationship between the retailer’s decision to adopt a particular mobile payment platform and the innovativeness of its business idea. Similarly, an inquiry should also be made into the factors relating to other stakeholders’ adoption intentions of mobile payments?

Blockchain or distributed ledger technology, which was once known only as Bitcoin’s underlying technology, is now emerging as a disruptive innovation. Its application and usage are penetrating all businesses and even many other domains. It may be potentially able to redesign our interactions in business, politics, and society at large. Concerning Blockchain’s accounting and auditing applications, we suggest an investigation on the effect of using smart contracts during the audit process and how far would this usage make the audit process more efficient? Another important agenda for future research could be exploring the types of accounting information that might be stored on blockchains. Could it be any specific kind of information, or would it be acceptable to store all data types?

Conclusion

An extensive review of the Fintech literature was conducted in this study. The Web of Science Database was selected for data extraction and the initial keywords search yielded 28,153 articles. The final analysis was conducted on 1,360 articles obtained after excluding irrelevant papers. These articles had been published between the year 2006 and June 2020. Biometric Software like HistCite and VOSviewer were used to conduct the data analyses. As a part of the meta literature review, the following types of analyses were undertaken in this study (i) identification of the influential aspects of FinTech literature, (ii) co-citation analysis, (iii) co-authorship analysis, (iv) keyword analysis, (v) content analysis of major streams available in the literature, and (vi) identification of the future directions.

Although there have been many previous reviews available on FinTech, every new study adds value to the existing literature due to the growing nature of the literature. Furthermore, this study might be useful for future researchers as it provides an overview of significant streams and sub-streams available in the FinTech literature. These streams include (i) Bitcoin and digital currency stream, (ii) the crowdfunding stream, (iii) the mobile payment stream, and (iv) the blockchain stream. The study results also identify the main contributors, institutions, primary sources, and influential and trending articles related to FinTech. Future research direction has also been discussed.

Regarding the study’s utility, the updated information about various researchers and institutions would be useful for Fintech professionals and new startups for future collaborations, testing, and upgrading of ideas across multiple business stages. For young academic researchers, the information about main streams and sub-streams might provide useful insights to initiate future research work. Furthermore, such information could be useful for future networking opportunities among researchers and other interested stakeholders.

No study is without limitations and as such this research study was also limited by several factors. Firstly, we have only used the Web of Science as a database to extract the relevant studies. This was because of the limitation inherent to the leading software used for analysis; HistCite, only processes WOS data. FinTech is a growing domain, and new research available in other databases as well such as Scopus and Google scholar has been missed. So any future research may combine the data from all these databases to conduct a more comprehensive study. Another potential limitation is related to the citation analysis. In Citation analysis, we rate studies, authors, and institutions based on the number of citations received. However, some recent good quality articles did not have many citations because of their recent date of publication and were ignored by the analytical software used. These articles would probably gain high citations in the future. So any future research using the same methodology may highlight these articles.

This research was conducted while Dr. Ishtiaq Ahmad Bajwa and Dr. Zaheer Anwer were at Imam Abdulrahman Bin Faisal University, Dammam, and the University of Management and Technology, Lahore, respectively. They are now at Beaconhouse National University, Lahore, and Sunway University, Malaysia and may be contacted at

Footnotes

Appendix

Abbreviations Used for Journals.

| Abbreviation | Name of journal | Abbreviation | Name of journal |

|---|---|---|---|

| FRL | Finance research letters | JBV | Journal of business venturing |

| ECOLET | Economics letters | SBE | Small business economics |

| ECA | Electronic commerce research and applications | IRA | International review of financial analysis |

| POO | Plos one | ETP | Entrepreneurship theory and practice |

| TFC | Technological forecasting and social change | AEE | Applied economics |

| FII | Financial innovation | RIF | Research in international business and finance |

| JOM | Journal of risk and financial management | BHH | Business horizons |

| RIF | Research in international business and finance | LEDGER | Ledger |

| SCF | Strategic change-briefings in entrepreneurial finance | JOIM | Journal of international financial markets institutions & money |

| JEMS | Journal of economics & management strategy | JEP | Journal of Economic perspectives |

| JFS | Journal of financial stability |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.