Abstract

Based on online survey data from 2020, the present study employed a logit model to examine the effects of COVID-19 on household financial behaviors in China. Additionally, the KHB (Kohler, Karlson, Holm) model was employed to explore the pathway through which COVID-19 affects household financial behaviors. These analyses revealed that household saving and borrowing behaviors were more sensitive to COVID-19 than insurance and investment behaviors. Moreover, the effects of COVID-19 on household saving and investment behaviors were found to be mediated by attitudes toward COVID-19. These findings suggest that more effective measures to reduce households’ panic attitude to public health emergencies can diminish fluctuations in household financial behaviors in the short term.

Introduction

Public health emergencies have inflicted enormous losses on the economic and financial development of many countries (Babuna et al., 2020). Since January 2020, COVID-19 has spread rapidly throughout China and around the world, dramatically affecting financial markets (Akhtaruzzaman et al., 2020; Yue et al., 2020). Many studies have explored the effects of COVID-19 on the economy and the financial market (Gherghina et al., 2020; Topcu & Gulal, 2020; Wojcik & Ioannou, 2020; D. Zhang et al., 2020). For example, as of March 16, 2020, the Dow Jones Industrial Average had dropped by 12.9% and the S&P (Standard & Poor’s) 500 Index had lost nearly 12% within a single day (Aslam et al., 2020). The potential economic effects of COVID-19 include slowed consumption and investment growth (Mohsin et al., 2021). As the pandemic became worse, the stability of banking decreased (Lagoarde & Leoni, 2013).

The public health emergency has also changed household behaviors (Li et al., 2021). Existing studies observed that finance professionals’ investments in the experiment were 12% lower in March 2020 than in December 2019 (Huber et al., 2021). Personality traits moderate the effect of financial literacy on individual mortgage delinquency during the COVID-19 pandemic (Chhatwani, 2022). Households that lose confidence in the economy during COVID-19 are more likely to change their investment portfolios (Yue et al., 2020). Households are among the most important constituents of society, and their financial behaviors epitomize the financial development of a country. Although prior researches have indicated that sense of fear plays a mediator between pandemic severity and conformity consumer behavior (Li et al., 2021; Sauer et al., 2020). However, there is still a lack of focusing on the short-term changes of household financial behaviors during the public health emergency, and the pathways of short-term shocks of public health emergency affect household financial behavior. The KHB (Kohler, Karlson, Holm) model performs well within a logit model (Smith et al., 2019). and it is employed to explain the mediating effect of investment experience between financial literacy and cryptocurrency investment (Zhao & Zhang, 2021).While the KHB method is slowly gaining popularity among social sciences and economics (Welsh & Kaciak, 2019; Zhao & Zhang, 2021), it is still a lack of using KHB model to analyze the household financial behaviors.

Although COVID-19 has spread rapidly throughout China, few studies have explored whether COVID-19 has affected household financial behaviors within the context of China. This study aimed to address the gaps in the literatures. Using data from 1,070 households in China, the models of binary logit and the KHB were employed to address the following research questions. First, does COVID-19 affect household financial behaviors? Second, what is the pathway through which COVID-19 affects household financial behaviors? This study provided empirical evidence on financial behaviors during COVID-19, thus contributing to the emerging branch of literature concerning the effects of public health emergencies on household financial behaviors.

Theoretical Background and Hypotheses

Household Financial Behaviors

Household finance, also known as consumer finance, is an important branch of finance that describes the asset allocation choices of households (Campbell, 2006). Consumer finance includes four main functions: payment, risk management, savings or investment, and credit (Tufano, 2009). Household financial behaviors reflect the comprehensive management of financial assets and liabilities, including borrowing, saving, asset portfolio management, investment decisions, and insurance behavior (Liebenberg et al., 2012). Financial liabilities mainly refer to households’ borrowing activities (Tobias & Andreas, 2018). Based on prior studies, this study mainly analyzed the effects of COVID-19 on household saving, borrowing, investment, and insurance behaviors within the context of China.

Direct Effects of COVID-19 on Household Financial Behaviors

Prior studies have revealed that emergencies such as economic cycle fluctuations, policy or system changes, and international situation changes can directly affect household financial behavior (Fabrigar et al., 2006; Lim et al., 2018). However, many of these studies have focused on the effects of emergencies on household investment behaviors (Yue et al., 2020), and on long-term household saving and borrowing behaviors (Vanlaer et al., 2020). Few studies have explored whether COVID-19 has affected household financial behaviors in the short term.

According to the life cycle theory (Modigiani & Brumberg, 1954.), savings—especially precautionary savings—will increase when uncertainty is substantially enhanced (Mody et al., 2012). Emergencies tend to boost household saving behavior to prepare for unexpected needs. Thus, household saving has increased since the onset of the current global financial crisis (Vanlaer et al., 2020). Additionally, COVID-19 has imposed potential and actual threats to households’ income sources (Li et al., 2021), further contributing to the increase in saving behavior.

Due to liquidity constraints, the decline in expected household income has reduced the occurrence of household borrowing behavior (Christopher et al., 1994). While unemployment, disaster, and disease tend to increase borrowing behavior to smooth household consumption (Kinnan & Townsend, 2012). The COVID-19 pandemic increased household financial stress (Kuang et al., 2020), they became more likely to borrow.

Compared to other household financial behaviors, household financial asset allocation is less influenced by temporary external shocks, consistent with persistent income theory (Angerer & Lam, 2009). While COVID-19 has increased the long-term probability that a household will change its investment portfolio, it has caused a 9.15% decrease in total investment amounts (Yue et al., 2020). The present study focused on the temporary shock of COVID-19. According to the persistent income hypothesis, household investment behavior is a long-term asset portfolio that will not change with temporary external shocks (Brunnermeier & Nagel, 2004).

Psychological account theory has revealed that funds allocated to each insurance account diminish as income decreases (Thaler, 1999). The availability bias may lead an actor to misestimate the probability of risk occurrence, thus affecting the demand for insurance (McClelland et al., 1993). For example, under the threat of dengue fever, residents of Taiwan were willing to pay between NT$793 and NT$1086 per person annually to purchase health insurance (Lin et al., 2020). Under the protection of universal healthcare in Britain, households do not typically buy commercial insurance to protect against health risks; however, this may change if the quality of free healthcare deteriorates (Guariglia & Rossi, 2004). Given that the Chinese government provides free healthcare for COVID-19, household insurance behavior in China is less affected by COVID-19.

Following related existing studies, the first hypothesis of this study focuses on the direct effects of COVID-19 on households’ financial behaviors:

H1: Household saving and borrowing behaviors are more likely and directly to be affected by COVID-19, while household investment and insurance behaviors are less affected by COVID-19 in the short term.

Indirect Effects of COVID-19 on Household Financial Behaviors, Mediated by Cognition and Attitude

The COVID-19 pandemic represents a worldwide threat to mental health, and households’ cognition and attitudes regarding COVID-19 affect their behaviors (Sauer et al., 2020). According to behavioral finance theory, risk attitude affects consumer behavior (Ki & Hon, 2012). Specifically, attitude plays a significant mediating role in financial knowledge and investment behavior (Lim et al., 2018). Pessimistic attitudes have detrimental effects on the behavioral response to COVID-19 (Sauer et al., 2020). Similarly, cognition is frequently linked to asset market participation, the stock adjustment rate, the savings rate, and portfolio choices (Cooper & Zhu, 2015). According to the competence hypothesis, people tend to invest when they have high levels of risk cognition (Heath & Tversky, 1991). However, prior studies have mainly explored the long-term effects of emergency-related cognition on financial behaviors. In the short term, COVID-19 may affect financial behaviors insignificantly. Based on the existing research, the second hypothesis was put forth to examine the mediating effects of cognition and attitudes regarding COVID-19:

H2: Household cognition and attitudes regarding COVID-19 indirectly affect household financial behaviors.

H2a: The financial behaviors of households with high levels of cognition regarding COVID-19 will not change significantly in the short term.

Saving behavior is mainly influenced by risk attitude, in that cautious households with an incentive to prevent risk tend to save (Cooper & Zhu, 2015). Conversely, optimistic attitudes toward emergencies encourage consumers to borrow (Aslam et al., 2020). As risk attitude increases, people are more likely to reduce their investment behaviors (Lin et al., 2020). Households who have experienced emergencies tend to exhibit pessimistic attitudes toward investment in stocks and are less likely to save for the future (Fajardo & Dantas, 2018).

H2b: The financial behaviors of households with highly panic-oriented attitudes toward COVID-19 will change significantly in the short term.

The conceptual framework shown in Figure 1 was developed based on the literature review and hypotheses detailed above.

Conceptual framework.

Methods

Participants and Procedure

The research data was collected from February 26th to March 11th, 2020, covering 1,104 households from 30 provinces and 121 cities of China (Excluding Hong Kong, Macao, Taiwan, and Tibet). After observations with missing data or outliers were excluded, the number of observations totaled 1,070. Of the participants, 54.8% were female and 45.2% were male. The Mage was 24.03 years (range: 18–69 years). Additionally, 84.7% of the participants had graduated from college. Overall, the respondents accurately and comprehensively described their behavior, cognition, and attitudes during the COVID-19 pandemic. The variable descriptions are shown in Table 1.

Variables Definition and Description (N = 1,070).

The data were derived from a survey conducted via the Chinese online social networking platform WeChat. First, the research group designed a questionnaire regarding consumer finance (Campbell, 2006), mainly focusing on short-term changes in household financial behaviors following the outbreak of COVID-19. Then, this initial questionnaire was revised following a pre-survey. The data collection process followed the principle of random sampling. Additionally, the researchers ensured that the participant samples were representative by confirming that the Internet Protocol addresses of the sampled households were consistent with the region under study. The eligibility criteria included a minimum age of 18 years and informed consent to participate in the study. Respondents agreed to provide accurate, objective responses based on their knowledge of COVID-19.

To test for systematic errors arising from similarity in the data source, environment, and characteristics of the sampled households, a Harman’s single-factor test was used to detecting the common method bias (CMB) of the data. The results showed that the variation of the unrotated first factor was 33.21%, less than the critical standard of 40%, indicating that CMB was not significant.

The reliability and validity of the data were also tested. Cronbach’s α was greater than .7 for all variables, indicating that the data had good reliability. All the construct reliability (CR) values were greater than .7, and all the average variance extracted (AVE) values were greater than .5, indicating that the questionnaire items had excellent validity.

Measures

Household financial behaviors

Household financial behaviors are the dependent variables consisted of saving behaviors, borrowing behaviors, insurance behaviors, and investment behaviors. These included financial behaviors occurring on both online and offline platforms. The dependent variables were binary, in that 1 denoted the occurrence of a household financial behavior and 0 denoted otherwise.

As reported in Table 1, 12.2% of the households engaged in saving behavior, 8.2% borrowed money during the COVID-19 pandemic, 10.2% engaged in insurance-related behaviors, and 20.8% invested during the investigation period. The households’ investment behaviors mainly included the purchasing of funds, stocks, bonds, fixed financial products, and precious metals.

COVID-19

The short-term constraints on households caused by COVID-19 are undoubtedly key independent variables. The COVID-19 pandemic has led to changes in the income levels and frequency of going out in China (Yue et al., 2020). Therefore, the present study characterized COVID-19 shock in terms of changes in income, lockdown measures, and the frequency of going out. During the sample period, the Chinese government took specific regulated actions to handle COVID-19, such as lockdown management. People were not allowed to go outside or travel to neighboring villages, especially those living in regions with high numbers of COVID-19 cases. To some extent, household financial behaviors reflected overall behavioral changes during the COVID-19 pandemic.

Mediators

Literature has widely shown that risk attitude affects consumer behavior (Ki & Hon, 2012). Mediators were household cognition and attitude regarding COVID-19. In line with prior studies, a sense of fear during the pandemic was used to measure attitudes toward COVID-19 (Li et al., 2021). Household attitude regarding COVID-19 was measured directly by asking respondents four items regarding COVID-19. Specifically, households’ attention to COVID-19, households’ behaviors to prevent COVID-19, such as staying at home, wearing masks at home, and households’ sense of fear regarding COVID-19 were included. The Cronbach’s α for this variable was .880, indicating good data reliability.

Cognition regarding COVID-19 was measured with five items: knowledge of contact transmission, droplet transmission, aerosol transmission, fecal-oral transmission, and no special drug for COVID-19. These variables were rated on a five-point scale, ranging from extremely disagree to extremely agree. The sampled Chinese households exhibited higher levels of cognition regarding COVID-19 than households in Congo, only 30% of which exhibited knowledge of COVID-19 in a prior study (Carsi et al., 2020). The Cronbach’s α for this variable was .858, indicating good data reliability.

Covariates

To minimize potential confounding, we controlled for a series of covariates. Household characteristics were as covariates based on the prior researches about household financial decision making (Campbell & Watanabe, 2002; Fernandes et al., 2014). Household financial behavior is affected by factors such as age, gender, size, income, and education. Household characteristics such as these have been found to explain 9.7% of the variation in asset allocation decisions (Zhang et al., 2018). Older consumers are likely to engage in more positive financial behaviors (Jing et al., 2006). Compared to men, women are more likely to choose conservative investment strategies (Salem, 2019). Furthermore, the asset holdings of higher-income households tend to be more diversified (Arrondel et al., 2014). Education affects household financial behaviors mainly through increased average income (Cooper & Zhu, 2015) and is positively correlated with household participation in the stock market (Campbell, 2006). Higher education levels have been found to increase the financial literacy of respondents, thus altering their saving and borrowing behaviors (Sayinzoga et al., 2014). In addition, households with unemployment and new children are more inclined to buy insurance (Liebenberg et al., 2012), and the locations of banks affect the use of financial transaction services (Goodstein & Rhine, 2016). Finally, household financial behaviors are influenced by social relationships with relatives and friends (Zhang et al., 2018).

Analytical Strategy

Since household financial behaviors are all binary variables, we employed binary logit regression in this analysis to estimate the short-term effects of COVID-19 on household financial behaviors. Household characteristics were controlled in binary logit regression.

Subsequently, to reveal the direct and indirect effects of COVIV-19 on household financial behaviors through household cognition and attitude regarding COVID-19, we conducted KHB mediation analysis. Due to the non-linear (binary) nature of the dependent variables, the standard mediation procedure (Baron & Kenny, 1986) is not applicable. Thus, the KHB method is particularly attractive in this study to understand the effects of mediators in non-linear models (Connelly et al., 2016; Welsh & Kaciak, 2019). The KHB model measures total, direct, and indirect effects through the logit method (Karlson et al., 2010). Total effects can be decomposed into direct and indirect effects by comparing the coefficients of the linear model (Breen et al., 2013). The basic idea was to compare the full model with a reduced model that substitutes (for the mediator variable) the residuals of the mediator from a regression of the mediator on the key variables. This method allows separation of the change in the coefficient due to either confounding or rescaling (L. Zhang et al., 2020).

Results and Discussion

Effects of COVID-19 on Household Financial Behaviors

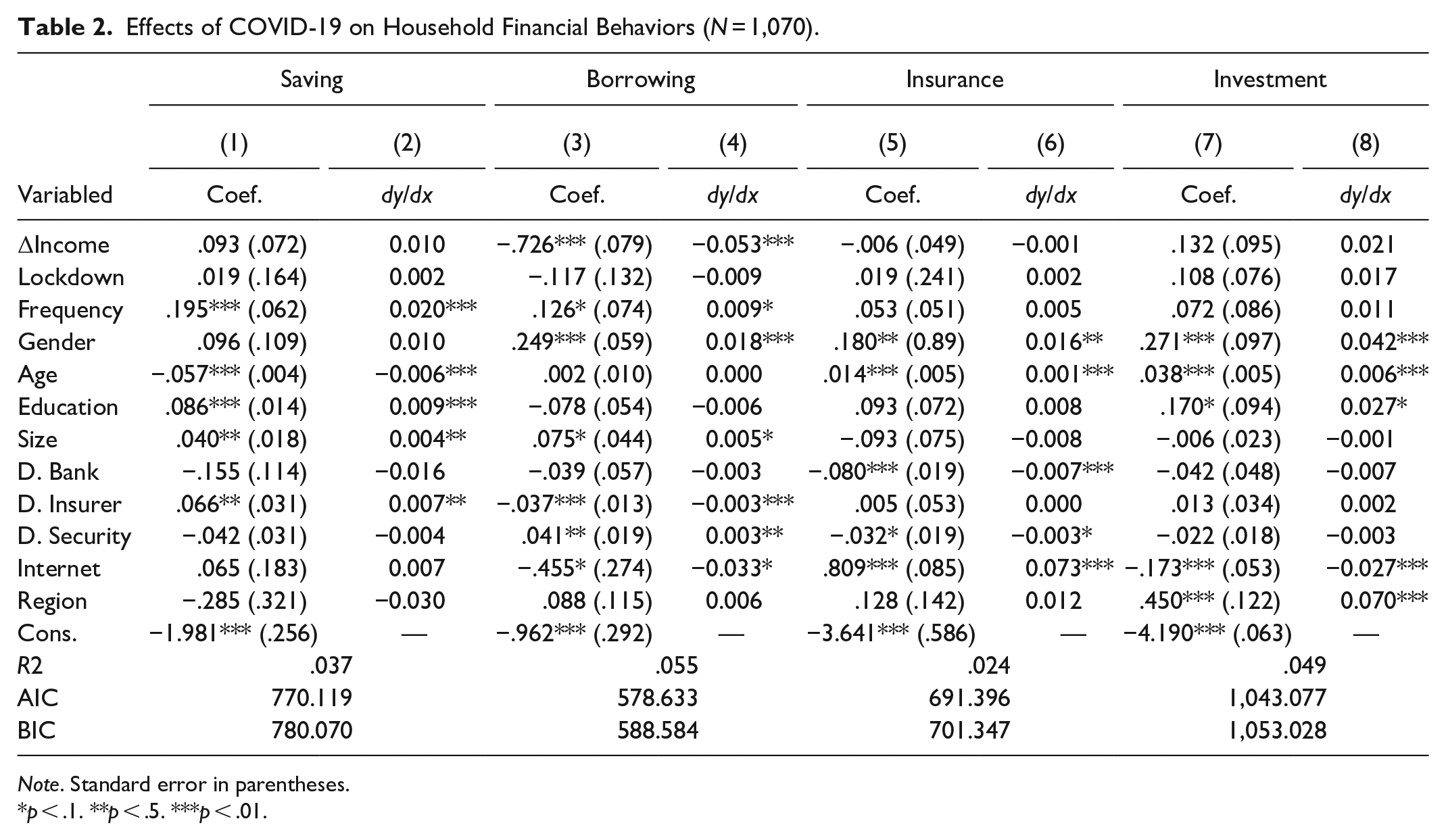

The effects of COVID-19 on household financial behaviors were examined using a logit model (Yue et al., 2020). Four binary logit regression models were calculated, and ∆ Income, Lockdown, and Frequency were used to represent COVID-19 in these models. Columns (1) and (2) take household saving behavior as the dependent variable, and Columns (3) and (4) explore the effects of COVID-19 on household borrowing behavior. Columns (5) and (6) examine effects on household insurance behavior and Columns (7) and (8) present effects on investment behavior. Table 2 presents the results regarding marginal effects and cluster standard errors by regions of China. Overall, the results indicated that COVID-19 significantly affected household saving and borrowing behaviors, validating H1.

Effects of COVID-19 on Household Financial Behaviors (N = 1,070).

Note. Standard error in parentheses.

p < .1. **p < .5. ***p < .01.

As shown by Columns (1) and (2), COVID-19 significantly affected household saving behavior. The frequency of going out positively affected household saving behavior with significance at the 1% level, whereas ∆ income and lockdown measures had no significant effects on household saving behavior. For a single unit increase in the frequency of going out, the probability of household saving behavior increased by 2%. The frequency of going out altered the degree of household social interaction. According to behavioral finance theory (Campbell, 2006), households that engage in a higher degree of social interaction are more inclined to change their asset allocation. Financial asset allocation behavior is directly reflected in the finding that household saving behavior increased as the frequency of going out increased. This also reflects the households’ need for precautionary savings. However, changes in income during the pandemic had no significant effects on household saving behavior. Rather, households chose to keep more liquid cash to meet their living needs in the short-term shock of COVID-19.

Household borrowing behavior was significantly affected by COVID-19. Specifically, ∆income negatively affected household borrowing behavior, while the frequency of going out was positively correlated with household borrowing behavior. The probability of borrowing behavior decreased by 5.30% while income increased by 1% during COVID-19. As it grows to meet household needs, increased income greatly reduces the occurrence of borrowing behavior. For a single unit increase in the frequency of going out, the probability of borrowing behavior increased by 0.90%. Over 60% of the surveyed households experienced declining income during COVID-19. Among the households that were able to go out, borrowing behavior increased to smooth consumption. Within the social network formed by geography and kinship, borrowing behavior plays a role in smoothing expenditure (Kinnan & Townsend, 2012).

Household investment and insurance behaviors were not significantly affected by COVID-19. More specifically, ∆ income, lockdown measures, and the frequency of going out had no significant effects on household investment and insurance behaviors. Previous studies have provided sufficient evidence to support these results. Household investment behavior is a long-term asset portfolio that will not change with short-term changes in household income (Brunnermeier & Nagel, 2004). According to persistent income theory and life cycle theory, risks have little effect on household financial asset selection in the short term (Angerer & Lam, 2009). Under the protection of free universal healthcare for COVID-19, Chinese households have had little incentive to buy commercial insurance. Contrary to the present findings, one prior study showed that 19.97% of households changed their investment portfolios due to COVID-19 (Yue et al., 2020). This discrepancy may have been due to the prior study mainly focus on the long-term effects of COVID-19 on households’ investment decisions (Yue et al., 2020). However, the effects of COVID-19 on households’ investment behaviors are insignificant in the short term.

Furthermore, the results of the present analysis showed that age, education, household size, and distance from the household residence to the nearest financial company had significant effects on household financial behaviors. The gender of the head of the household had a significant effect on the occurrence of household borrowing, investment, and insurance behaviors, in that male-headed households were more likely to engage in financial behaviors during COVID-19 than female-headed households. Overall, women were more likely to choose conservative financial strategies (Zhang et al., 2018). Respondent age had a significantly negative effect on household saving behaviors and significantly positive effects on investment and insurance behaviors at a significance level of 1%. Older respondents tend to reduce their saving behaviors, possibly to maintain more liquid assets (Cooper & Zhu, 2015). Consistent with previous studies, the present results indicated that higher education level significantly promotes household saving and investment behaviors (Cooper & Zhu, 2015). Specifically, education increased the financial literacy of the respondents, thus changing their saving behavior (Sayinzoga et al., 2014). Furthermore, Internet-connected households exhibited significantly reduced investment behavior, possibly due to the greater acuity of investment information on the Internet.

The results also indicated that ∆ income during COVID-19 had a significant negative effect on household borrowing behavior but had no significant effects on household saving, insurance, or investment behavior. According to life cycle theory, short-term changes in household income during COVID-19 should not affect household asset allocation in the long term (Cooper & Zhu, 2015), especially insurance and investment behaviors. With the rapid development of Internet finance, households can purchase insurance and invest through smartphones, computers, and other channels. Therefore, lockdown measures and the frequency of going out had no significant effects on insurance and investment behaviors. The empirical results also showed that the Internet had significant effects on both insurance and investment behaviors, which was in line with prior findings (Babuna et al., 2020; Yue et al., 2020).

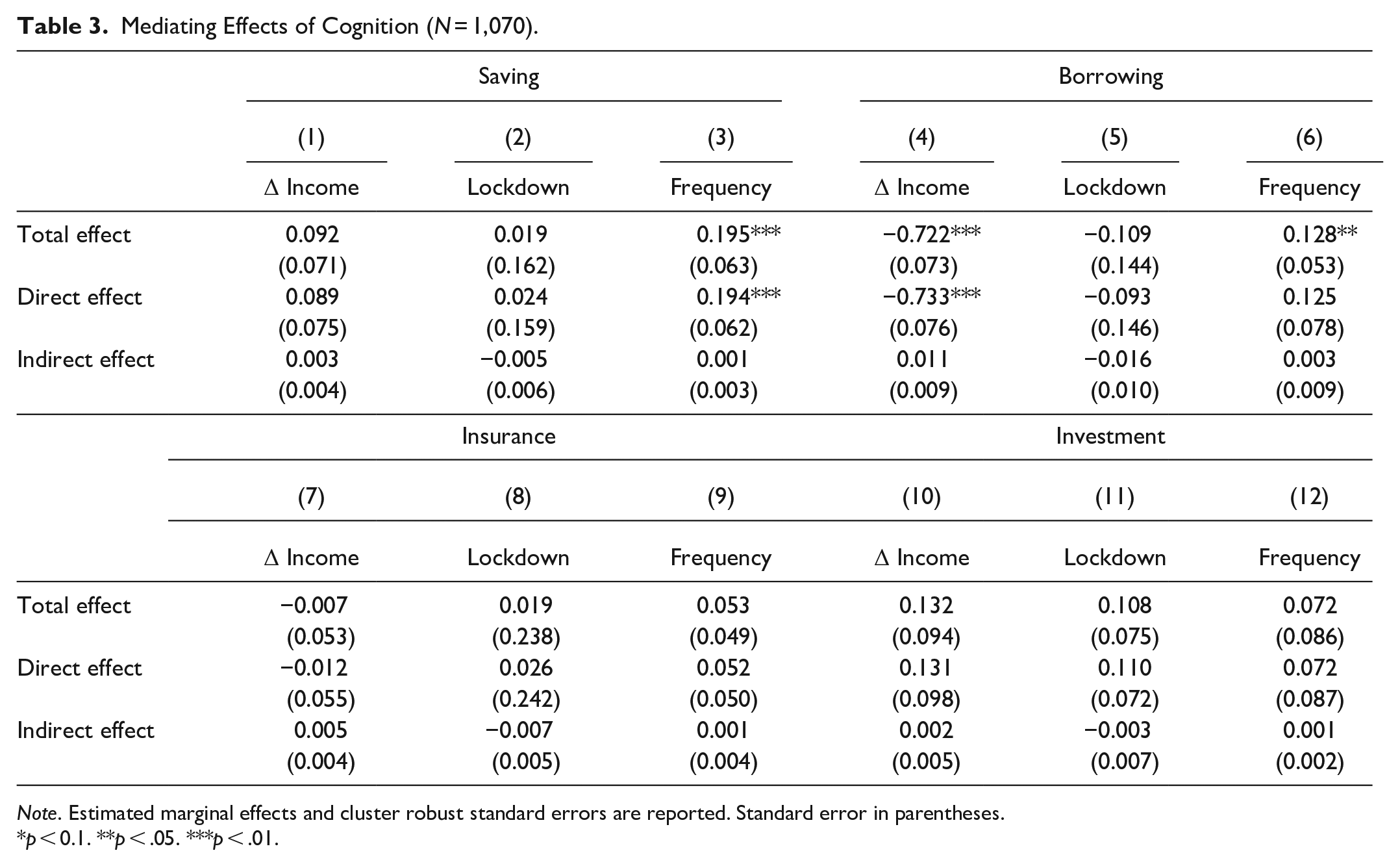

Indirect Effects of COVID-19 on Household Financial Behaviors, Mediated by Cognition

As shown in Table 3, cognition regarding COVID-19 did not play a significant mediating role in the effects of COVID-19 on household financial behaviors; thus, H2a was validated. The direct effects of COVID-19 on household financial behaviors were dominant in all models. Due to the objectivity of cognition, households with high levels of cognition regarding COVID-19 tended to maintain their behavioral decisions despite short-term shocks.

Mediating Effects of Cognition (N = 1,070).

Note. Estimated marginal effects and cluster robust standard errors are reported. Standard error in parentheses.

p < 0.1. **p < .05. ***p < .01.

As shown by Columns (1) to (3), COVID-19 had a direct effect on household saving behavior and had no significant indirect effects mediated by cognition. The direct effect of the frequency of going out on saving behavior accounted for 96.74% of the total effect, while the indirect effect accounted for only 3.26% and was thus insignificant.

As shown by Columns (4) to (6), COVID-19 had no significant indirect effects on household borrowing behavior, and the direct effects of COVID-19 on borrowing behavior were dominant. The direct effect of ∆income outweighed the total effect, as increased income directly reduced household borrowing behavior. The frequency of going out also directly promoted the occurrence of household borrowing behavior.

The estimated results of the KHB model for household insurance shown in Columns (7) to (9) and those for investment behavior shown in Columns (10) to (12) are consistent with the results shown in Table 2. In the short term, COVID-19 had no significant cognition-mediated effects on household insurance and investment behaviors. With the improvement of medical insurance in China, more households are choosing to trust basic universal medical insurance rather than purchase commercial insurance products. The existing commercial insurance in China does not typically cover treatment expenses for public health emergencies of international concern, such as COVID-19. This may explain why most households have not purchased commercial insurance under the short-term shock of COVID-19.

Indirect Effects of COVID-19 on Household Financial Behaviors, Mediated by Attitude

As shown in Table 4, COVID-19 had significant effects on household saving and investment behaviors through household attitudes toward COVID-19; thus, H2b was confirmed. As shown in Columns (1) to (3), COVID-19 had negative effects on household saving behavior that were significantly mediated by attitude, opposite the total and direct effects. More specifically, income changes and lockdown measures indirectly reduced the occurrence of household saving behavior through attitude, such that COVID-19 encouraged households to hold more cash. The total effect of the frequency of going out on household saving behavior was positive and significant, while the indirect effect was negative and significant. These results suggest that the frequency of going out directly increased household saving behavior but also had an indirect inhibiting effect on household saving behavior through attitude. However, the direct effect outweighed the indirect effect. This finding was inconsistent with the results of previous studies (Cooper & Zhu, 2015), possibly due to the specificity of lockdown measures during the COVID-19 outbreak in China. Restrictions on going out during COVID-19 led households to keep more liquid cash rather than savings.

Mediating Effects of Attitude (N = 1,070).

Note. Estimated marginal effects and cluster robust standard errors are reported. Standard error in parentheses.

p < .1. **p < .05. ***p < .01.

As shown in Columns (4) to (6), the indirect effects of COVID-19 on household borrowing behavior through attitude were not significant. More specifically, ∆income directly reduced the likelihood of household borrowing behavior. Furthermore, the frequency of going out directly promoted the occurrence of household borrowing behavior but had no significant indirect effects on borrowing behavior through attitude in the short term.

Columns (7) to (9) show the effects of COVID-19 on household insurance behavior. The short-term effects of COVID-19 on household insurance behavior were not significant. This is consistent with the regression results regarding cognition as a mediator. Due to the coverage of COVID-19 treatment costs by basic universal health insurance in China, most Chinese households do not intend to purchase commercial health insurance in the short term (Yating et al., 2020).

As shown by Columns (10) to (12), COVID-19 had positive indirect effects on household investment behavior through attitudes toward COVID-19, which were significant at the 1% level. The indirect effect of ∆income on household investment behavior through attitude accounted for 8.33% of the total effect, that of lockdown measures accounted for 16.04%, and that of frequency of going out accounted for 16.44%. The direct, indirect, and total effects of COVID-19 on household investment behavior were all positive, indicating that COVID-19 directly affects household investment behavior but also indirectly affects this behavior through household attitudes toward COVID-19. Consistent with these results, previous research has shown that households with optimistic attitudes regarding risk have a higher probability of changing their investment behavior than other households (Guiso & Paiella, 2008).

Robustness Test

Household subsamples were constructed to check the robustness of the empirical results. These subsamples included respondents aged 20 to 60 years. The KHB model was used to carry out the robustness tests, as shown in Table 5. The results indicated that the direct effects of COVID-19 on household financial behaviors and the indirect effects through household attitudes toward COVID-19 similarly supported the hypotheses. Specifically, COVID-19 directly affected household saving and borrowing behaviors but also indirectly affected saving and investment behaviors through household attitudes toward COVID-19. Furthermore, the financial behaviors of households were not significantly affected by COVID-19 in the short term through their cognition regarding COVID-19.

Robustness Test (N = 890).

Note. Estimated marginal effects and cluster robust standard errors are reported. Standard error in parentheses.

p < .1. **p < .05. ***p < .01.

Conclusions and Implications

Conclusions

The results of this study offer a new perspective on the short-term relationship between public health emergencies and household financial behaviors. Online survey data collected from 1,070 Chinese households from February 26 to March 11, 2020, revealed that COVID-19 not only had significant direct effects on household saving and borrowing behaviors but also had indirect effects on saving and investment behaviors mediated by household attitudes toward COVID-19.

Household saving and borrowing behaviors were more sensitive to COVID-19 than household insurance and investment behaviors. A higher frequency of going out during COVID-19 directly increased household saving and borrowing behaviors. Conversely, increased household income directly reduced the occurrence of borrowing behavior. Most of the surveyed households preferred to hold cash to ensure that their basic living expenses were covered during COVID-19. Household insurance behavior did not change in the short term, likely because China’s basic universal health insurance completely covers the cost of COVID-19 treatment. Furthermore, households did not immediately change their investment plans under the short-term shock of COVID-19. Therefore, the direct effects of COVID-19 on household insurance behaviors were not significant.

In addition to these direct effects, COVID-19 had significant indirect effects on household saving and investment behaviors through household attitudes toward COVID-19. Specifically, COVID-19 indirectly reduced household saving behavior and increased household investment behavior through household attitudes.

Implications

This study offers both theoretical and practical contributions to the body of research on public health emergencies and financial behaviors. Theoretically, this study analyzed the effects of COVID-19 on household financial behaviors to supplement the existing research on behavioral finance. The results uniquely contribute to current theories on this subject by taking a black box perspective on changes in household financial behaviors during public health emergencies, such as COVID-19.

In addition, the results of this study have several practical implications. For one, these results provide direct evidence of short-term changes in household financial behaviors during a public health emergency. Reducing households’ panic attitude of public health emergencies could mitigate fluctuations in household financial behaviors. Therefore, governments should strengthen publicity regarding public health emergencies promptly manner to prevent large fluctuations in financial behaviors, which may affect the stability of the financial market.

Additionally, the present results showed that COVID-19 did not significantly affect household insurance behavior in the short term. The Chinese government provides free treatment to all confirmed COVID-19 patients, whereas China’s commercial insurance carriers do not cover the cost of treatment for COVID-19. Therefore, the short-term effects of COVID-19 did not incentivize Chinese households to buy commercial health insurance. To alleviate public health fiscal expenditure, the commercial insurance market should try to gradually reform the public health emergency insurance system.

Limitations and Future Research Directions

Two major limitations of this study should be noted to inform improvements in the sampling, empirical data, methods, and impact mechanisms of future research. First, this study used only the survey data of households from China and lacked survey data from other countries; this weakened the generalizability of the research conclusions to some extent. Second, the cross-sectional data used in this study cannot capture changes in financial behaviors before and after COVID-19, thus limiting the capacity of this study to identify causality. Therefore, the researchers aim to collect panel data through a longitudinal survey for further study.

It is also worth noting that the present study used only a single-mediator model and cross-sectional data as mechanisms to explain the effects of COVID-19 on household financial behaviors. Furthermore, this study tested only the mediating effects of cognition and attitude. In future studies, it would be meaningful to explore other pathways through which COVID-19 may affect household financial behaviors, such as households’ confidence to economy.

Footnotes

Acknowledgements

The authors also would like to extend our sincere thanks to Dr. Zhao Ding and Mr. Abbas Ali Chandio for supporting the study.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the financial support from the National Office for Philosophy and Social Sciences of China (Grant ID: 21XGL008), the Ministry of education of Humanities and Social Science Project of China (Grant ID: 20YJC790032), and the National Natural Science Foundation of China (Grant ID: 71873018).