Abstract

This study examines the relationship between audit committee independence (by using stockholding as a measure to assess substantive independence) and auditor reporting for financially distressed companies. Based on hand-collected data for 86 financially distressed companies listed on Pakistan Stock Exchange (PSX) for the period 2011 to 2019, our logistic regression results show that the greater the percentage of audit committee stockholding, the less likely the auditor is to issue going concern report. Further, this relationship is exacerbated by CEO influence. The results are robust to alternative estimation techniques, different measures of audit committee independence and CEO influence, and endogeneity issue. These results suggest that alongside procedural independence, it is important to focus on substantive independence of audit committees by using stockholding as an independence measure and assessing its impacts on auditor reporting. This study has important implications for shareholders and investors.

Keywords

Introduction

Audit committee independence is regarded as the most significant factor to ensure the overall effectiveness of an audit committee and lead to better monitoring of the company’s financial reporting practices (Bliss et al., 2011; Carcello, Neal, Palmrose, & Scholz, 2011; Salloum et al., 2014; Tusek, 2015). In a series of efforts to improve audit committee independence, various regulations including the Sarbanes-Oxley act of 2002 (SOX), the UK Corporate Governance Code, the Code of Corporate Governance (Council, 2012) have been issued that require audit committees to be fully (or in the majority) comprised of independent or non-executive directors (NEDs)―who are not serving their companies in any executive or management position and do not have any other business relationship with those companies. However, the important thing to be considered here is whether having independent or NEDs as committee members are mere superficial regulations confirming “procedural independence” or they are actually associated with enhanced effectiveness of audit committees improving “substantive independence” (Church et al., 2018; DeZoort et al., 2002; Salehi, 2020).

For the said purpose, we examine the relationship between audit committee independence and auditor reporting by using stockholding as a measure to assess “substantive independence” of NEDs acting as audit committee members. Specifically, we examine the relationship between the stockholding of audit committee members (including their close relatives serving on board) and the likelihood that the auditor will issue a going concern report in the sample of financially distressed companies.

Earlier research suggests that stockholding of audit committee members (hereinafter referred to as “audit committee stockholding”) may impair their independence and objectivity, and urge them to increase the firm’s involvement in earnings management to present more profitable results (Al-Hadrami et al., 2020; Leung et al., 2014; Mangena & Pike, 2005; Tusek, 2015). It causes conflicts of interest in a way that committee members support rather than challenge management’s policies (Carcello & Neal, 2003; Mangena & Pike, 2005; Saeed & Riaz, 2021; Seifzadeh et al., 2021), and make committee members refrain from blocking a managerial attempt to dismiss an auditor after a going concern report (Carcello & Neal, 2003; Dalwai & Salehi, 2021; Mareque et al., 2017; Saeed et al., 2021a). Therefore, we contend that the greater the audit committee stockholding, the less the committee will act independently in supporting the auditor in their dealings with management regarding the audit report type to be issued. This effect is more pronounced for companies experiencing financial distress because companies with more instances of fraudulent financial reporting tend to have audit committees and BOD with fewer independent directors (Beasley et al., 2009; Berglund et al., 2018; Faysal et al., 2021; Seifzadeh et al., 2020). Carcello and Neal (2000) suggest that lower audit committee independence decreases the likelihood that auditors will issue going concern reports to a financially distressed company and, further, non-independent audit committees are more likely to dismiss auditors if they issue going concern reports.

Codes of corporate governance globally have gradually dispensed commendations for corporate board structures and, particularly, relating to its independent members (Crespí-Cladera & Pascual-Fuster, 2014; Mohammadi et al., 2021; Saeed et al., 2021a,b). Most regulators and academicians define a member independent if he or she has neither familial nor financial links to the firm or any other board member, and highpoint the monitoring profits of independent executives (e.g., Armstrong et al., 2014; Chen et al., 2015; Klein, 2002). Corporate governance standards show the wide mainstream plainly contains endorsements on board independence. In United states, the corporate board should consist of majority of independent members. Because it is considered that board independence increases board effectiveness, thus leading towards effectual organizational strategies and increase shareholder’s wealth (Ben-Amar et al., 2013). In developed countries such as USA and UK independent directors do not hold stock because it harms their independence which leads to less monitoring of the organizational strategies (Crespí-Cladera & Pascual-Fuster, 2014; Fan et al., 2021; Salehi et al., 2020). However, the case of developing countries like Pakistan is sharply different from developed ones. (Riaz & Saeed, 2020). This study used the data from a developing country—Pakistan because for the following reasons. Pakistani market is characterized by a relatively unsophisticated legal and regulatory framework, high ownership concentration, and weak enforcement and monitoring of regulations (Ali & Bin Nasir, 2014; Salehi et al., 2019). Regarding corporate governance regulations, the Code of Corporate Governance (hereinafter referred to as “the code”) issued by the Securities and Exchange Commission of Pakistan (SECP) in 2002 (revised 2012; amended July 2014) contains ambiguous provisions regarding the audit committee independence. The clause (XXIV) of the code requires an audit committee to completely consist of Non-Executive Directors (NEDs), one of whom is required to be an Independent Director (INED) who is also required to act as chairman of the audit committee. However, there are numerous lacunas in the code’s provisions that may impair the substantive effectiveness of the code despite apparent compliance. Contrary to the Berle and Means (1932) and Shiri et al. (2018) model of separation of ownership and control, the corporate ownership structure in Pakistan builds around concentrated family ownership. The majority of stockholders not only maintain control of a company but are also actively engaged in managing it. Pakistan’s Code of Corporate Governance ignores this fact and not offering the right remedy for the governance issues faced by a concentrated ownership structure like Pakistan. Similarly, the code is deficient in listing minimum requirements for directors to fulfill their fiduciary duties hence posing gaps that may lead to mere superficial compliance with code’s provisions while lacking the true spirit to serve the company and its stockholders including minority stockholders (Ibrahim, 2006; Khan et al., 2021).

The results of this study support our expectations. We find a negative relation between audit committee stockholding and the likelihood that the auditor will issue a going concern report to a financially distressed company. We further find that CEO influence negatively moderates the relationship between audit committee stockholding and auditor’s propensity to issue going-concern reports to financially distressed companies. These findings are robust for multiple estimation techniques and model specifications.

This study adds to the existing body of knowledge in the following different ways. On the top, it is one of the earliest to investigate the impact of audit committee independence on auditor reporting by considering stockholding of audit committee members as a measure of committee’s independence. Prior studies conducted in this realm have mainly considered the presence of independent or non-executive directors (NEDs) as committee members for audit committees to be categorized as independent (Ali & Bin Nasir, 2014; Sharma & Kuang, 2014; Yasser et al., 2011). Secondly, we show that the effect of audit committee stockholding on auditor report type is contingent on CEO influence. In doing so, we add new evidence to the studies on the determinants of audit committee independence (Al-Najjar, 2011; Beasley et al., 2009; Bruynseels & Cardinaels, 2014; Cohen et al., 2012). Thirdly, by providing this evidence we extend the literature discussing substance versus a form of audit committee effectiveness and independence (Carcello, Hermanson, & Ye, 2011, Carcello, Neal, Palmrose, & Scholz, 2011; Church et al., 2018; Cohen et al., 2012; Lisic et al., 2016). Our results advocate that audit committee members’ independence status mere in form alone is not sufficient to ensure the substantive independence of the audit committee. Rather, audit committee stockholding and CEOs’ influence are important determinants of substantive audit committee independence. By doing so, we unfold the nexus between audit committee independence (by using stockholding as a measure to assess substantive independence) and auditor reporting for financially distressed companies in the context of an emerging market.

Literature Review and Hypotheses Development

Statutory auditors are deemed as the watchdog authority responsible to protect the public interest and report on the accuracy and transparency of the corporate sector’s financial matters (Ali & Nasir, 2018; Halbouni, 2015; Mareque et al., 2017; Tusek, 2015). If auditors are not independent of their clients, it may impair their ability to perform their functions objectively and independently. To address the concern, audit committees were introduced to protect the independence of auditors and enable them to perform their functions objectively. Church et al. (2018) suggest that audit committees supported auditors in their disputes with management and strengthened their independence.

To fulfill the responsibilities and protect auditors from any undue pressure exerted by executive management, the audit committees themselves need to be independent in the first place. Sommer (1991) observes that audit committee members may not always fulfill their responsibilities in an effective manner and the mere existence of audit committees may not warrant desired corporate governance outcomes. In this regard, the advocates of agency theory (such as Mangena & Pike, 2005) are of opinion that an audit committee with a larger proportion of independent or outside directors is more likely to work in the best interests of shareholders due to the lack of economic or personal interests of these directors in firm. Such independent audit committees are well placed to support auditors in their conflicts with management due to their unbiased approach (Krishnamoorthy & Maletta, 2012), and help auditors to issue a going concern report where warranted (Carcello & Neal, 2003; Mareque et al., 2017; Salehi et al., 2018). So, audit committee independence is regarded as the most significant factor to ensure the overall effectiveness of an audit committee and lead to better monitoring of the company’s financial reporting practices (Carcello, Neal, Palmrose, & Scholz, 2011; Riaz et al., 2022).

Procedural and Substantive Independence

In most of the studies conducted in this area, audit committee independence is measured by checking the compliance with the independence requirements posited by various government regulations like the Sarbanes-Oxley act of 2002 (SOX), the UK Corporate Governance Code, which require the presence of independent or non-executive directors (NEDs) as committee members for audit committees to be categorized as independent (Ali & Bin Nasir, 2014; Saeed et al., 2021a,b; Sharma & Kuang, 2014; Yasser et al., 2011). However, these regulations have not explicitly forbidden audit committee members, especially non-executive directors, from holding stocks in their companies which provides them with opportunities of getting benefit from their companies (Lavelle, 2002). So, this stockholding can be a potential threat to the substantive independence of these audit committee members who may falsely try to protect their companies from objective auditor reporting (Bolton, 2014) while, still, may seem to have procedural independence being non-executive directors in compliance with the requirements of relevant regulations.

There is a plethora of studies showing stockholding as an important measure to assess audit committee independence (e.g., Cardwell et al., 2011; Carcello & Neal, 2003; Mangena & Pike, 2005). The NEDs serving as audit committee members are not on the payroll of companies receiving any regular salary or performance-based compensation and the only aspect which can help these NEDs to get benefit from these companies is their stockholding. Bolton (2014) suggests that stock ownership of audit committee members is a more important measure than other independence measures and has significant effects on the overall independence of audit committee members. It was argued by Lavelle (2002) that the stockholding of independent audit committee members can render their actions to be examined as they may try to protect their investments by defending misrepresented financial results and profitability by executive management. Similarly, Carcello and Neal (2003) find that audit committee members having stockholding in their companies may purposefully refrain from supporting auditors regarding their dismissals after going concern reports issued by them. Hence, the usage of stockholding as a yardstick measure to evaluate audit committee independence and its impacts on auditor reporting quality is worth examining.

Hypotheses Development: Audit Committees of Financially Distressed Companies and Going Concern Reporting

Prior research suggests that going concern reporting for financially distressed companies is a difficult decision for auditors and they are likely to endorse the client’s position in such ambiguous situations or “gray areas” (Levitt, 2000). However, it was suggested by Bronson et al. (2009) that independent audit committees are positively associated with going concern reporting by the auditor in financially distressed companies as they help auditors to mitigate management pressure in such situations and support them to report objectively and independently.

Contrarily, if audit committee members lack economic independence they may fail to perform their functions independently. Carcello and Neal (2003) found that non-independent audit committees support management in their decisions to dismiss auditors after the issuance of going concern audit reports. Similarly, Beasley et al. (2009) suggested that companies with more instances of fraudulent financial reporting tend to have audit committees and boards with fewer independent directors. Carcello and Neal (2000) find that the greater the proportion of affiliated directors on an audit committee, the lower is the likelihood that the auditor will issue a going concern report to a financially distress company.

The aforementioned problem is expected to be more prevalent in emerging economies as they are characterized by potentially weak rule of law and window dressing of facts by companies hence requiring focus on these economies to explore such problems in detail. In the context of Pakistan, Code of Corporate Governance issued by Securities and Exchange Commission of Pakistan (SECP) in 2002 (revised 2012; amended July 2014) contains detailed provisions regarding audit committee independence. The clause (XXIV) of the code requires an audit committee to completely consist of Non-Executive Directors (NEDs), one of whom is required to be an Independent Director (INED) who is also required to act as chairman of the audit committee. Further, the code has also specifically mentioned that NEDs may or may not be independent. The clause i(b) of the code has discussed the preconditions for INEDs however, the provisions of the code regarding audit committee membership eligibility have not precisely addressed the existence of such prerequisites to ensure the independence of NEDs. Yasser et al. (2011) found that 91% of the companies listed on Karachi Stock Exchange (now Pakistan Stock Exchange (PSX)) were compliant with COCG regulations regarding audit committee independence and consisted of NEDs. Here, it is important to note that companies may follow regulations of having only NEDs as committee members just for the sake of observing superficial compliance with relevant regulations and to avoid disciplinary actions by the concerned authorities. NEDs acting as audit committee members may or may not function independently due to absence of explicit prerequisite independence regulations including any check on their stockholding. It implies that compliance with minimum requirements of the code may confirm procedural independence but it does not guarantee substantive independence of audit committees and the committee members (Berglund et al., 2018; Church et al., 2018). So, to test the assertions presented by above referenced literature & discussion, we hypothesize that:

Given his or her position at the apex of the corporate hierarchy, the Chief Executive Officer (CEO) is most likely the target of shareholders’ pressure to meet their earnings expectations. In financially distressed companies, such pressures on CEOs, potentially pose a substantial risk of misstatement of financial information in annual reports which in turn elicits auditor’s skepticism and propensity to issue a going concern reports to such companies (Cohen et al., 2012). To combat such pressure, top executives of financially distressed companies may pressurize the auditor against issuing going concern reports as it can bring various problems to such companies, for example, declining stock prices and troubles in availing debt finance (Adams & Ferreira, 2007). In such situations, audit committees also find themselves under extreme pressure in facilitating auditors to perform their functions in an independent and objective manner (Cardwell et al., 2011; Cohen et al., 2008). In fact, audit committees in financially distressed companies may find themselves in even more grave situation to perform independently and support auditors for objective reporting. Several research studies have suggested that CEO is an imperative contributor to the corporate governance assortment and it may pose a detrimental impact on the independence of audit committees even though these committees meet regulatory independence requirements (Beasley et al., 2009; Bruynseels & Cardinaels, 2014; Cohen et al., 2012).

There are numerous ways CEOs can restrict audit committees from independently performing their functions. First, causing audit committee to be less conscientious in monitoring management (Cohen et al., 2012) by not providing them sufficient amount of information or providing them with low-quality information about important issues that come under the control of executive management (Adams & Ferreira, 2007; Harris & Raviv, 2008). Second, CEOs tend to have internal controls in the company to exercise more discretion on the financial reporting process resulting in low quality of financial information (Ashbaugh-Skaife et al., 2007). Third, providing managers with opportunities to make a profit by insider dealing (Skaife et al., 2013) hence resulting in the failure of the audit committee to set its agenda independently when working with a powerful CEO (Beasley et al., 2009).

Finkelstein (1992) posits that an important factor giving power to CEO is his stockholding in the company which increases his power and reduces the influence of directors. This study posits that influential CEOs impact auditor’s propensity to issue going-concern reports to financially distressed companies because influential CEOs have a substantial effect on decision making and organizational actions, including audit quality. Furthermore, influential CEOs are more prone to employ their discretion in audit reporting, specifically where audit reports can create harm for the firm (Walls & Berrone, 2017). Influential CEOs are considered to own greater discretion over organizational matters and they are more likely to engage in self-interested activities such as manipulation of firm financial performance for personal benefits (Alhadab & Clacher, 2018). Walls and Berrone (2017) argue that the formal, as well as informal power of CEOs, is the catalyst for maneuvering the organizational performance in their best interest. CEO can obtain formal power within the board members and committees. Members of the board and committees enable the CEO to build direct links with other stakeholders within in outside the firm such as audit team members. CEOs establish a mutual relationship among them through their regular meetings and interactions (Westphal, 1999). In addition, influential CEOs are characterized by strong social capital, which is reflected in his/her personal relationship with other influential board members, assists as an additional foundation of resistance for auditors to issue going-concern reports. Social links are characterized by loyalty, trustworthiness, and closeness, which makes members share relevant information, pursue necessary advice and gain support from their links (Engelberg et al., 2012). In our case, we state that influential CEOs has more solid social links with other members, particularly those who have skills and competence in finance and accounting related actions of firms such as with members of the audit committee which enables CEOs to negatively moderates the negative relationship between audit committee stockholding and auditor’s propensity to issue going-concern reports to financially distressed companies. Besides that, influential CEOs can shape the hiring of the audit firm. When the audit firm is hired by the choice of the CEO, it facilitates the earning management and window dressing by the firm (Alhadab & Clacher, 2018) because auditors are under strong pressure of CEOs in this situation leads to less likeliness of issuance of the going-concern report. Hence, it is of significant importance to examine that how CEO influence measured by stockholding of CEO may adversely affect the independence of directors serving as audit committee members, hence, impairing the substantive independence of audit committee and objectivity of auditor reporting. So, based on the above discussion, we hypothesize that:

Data and Research Design

Data

To test our proposed hypotheses, we use companies experiencing financial distress, in the years 2011 to 2019, from a population frame of all non-financial companies listed on the Pakistan Stock Exchange (PSX). A particular focus is placed on financially distressed companies as they have virtually more chances to receive going concern reports than normally operating companies and prior research also shows that auditors almost never issue going concern reports to companies not experiencing financial distress (Berglund et al., 2018).

We consider only those companies which have financial distress levels high enough to enhance auditor’s propensity to issue going concern reports to these companies. Previous research in this area indicates that auditors are more likely to issue a going concern report when the probability of failure of a company exceeds 28% as calculated by Zmijewski’s (1984) financial distress prediction model (Krishnan & Krishnan, 1996). This financial distress threshold is also used in earlier studies conducted in Pakistan such as Jahanzeb et al. (2016). So, we also follow a similar financial distress prediction model in our study.

Thus, the sample for this study includes non-financial companies listed on Pakistan Stock Exchange (PSX) with a probability of failure above .28 as calculated by Zmijewski’s financial distress index (Carcello & Neal, 2003) and that had not filed for bankruptcy. According to the estimations made by applying Zmijewski’s financial distress index, there were 109 financially distressed companies as of the year 2011. After excluding companies with data unavailability (11 companies), and companies that declared bankruptcy during this period (8), we were left with a sample of 86 companies with 774 firm-year observations during the period 2011 to 2019. There are two important reasons to start our sample from 2011. First is the availability of data as the company information is richer for recent years, while, firm information beyond 5 to 6 years is very limited. This is particularly true in the case of information regarding corporate governance variables. Second, starting our sample from 2011 eliminates the possibilities of having downturn effects of the 2008 financial crisis in our sample period.

The corporate governance data used in this study is hand-collected from published financial statements of sample companies, available on their respective websites and/or Pakistan Stock Exchange (PSX), for the years 2011 to 2019. Further, financial statements’ analyses of non-financial companies listed on the Pakistan Stock Exchange (PSX), available on the website of State Bank of Pakistan (SBP), are also used along with published annual reports of sample companies.

Estimation Model

We investigate the relation between audit committee stockholding (as a proxy for audit committee independence) and auditor reporting for financially distressed companies and how this relation is affected by CEO influence. The following logistic regression model is used to test the hypotheses developed for this study:

Variable Measurement

Our dependent variable is the type of audit report issued on the company’s financial statements for the years 2011 to 2019. Following Cardwell et al. (2011) and Carcello and Neal (2000), it is measured as a dummy variable (REPORT) that takes the value of 1 if going concern-modified report is issued and 0 when unmodified or modified for a consistency exception report is issued. Our main variable of interest is the percentage of audit committee stockholding (STHAC) including their close relatives serving on boards following Cardwell et al. (2011), Mangena and Pike (2005), and Carcello and Neal (2003). It is measured as a percentage of the company’s stock (including stock options) owned by directors serving as audit committee members along with their close relatives serving on board, based on the pattern of shareholding given in published financial statements of sample companies. Next, CEO influence (CEOINF) is measured by stockholding of CEO taken as a percentage of the company’s stock (including stock options) owned by the CEO (Finkelstein, 1992).

Based on earlier studies, we include various control variables in regression analysis to account for their potential influences on auditor reporting. It was found by Chen and Church (1992) that debt default (DEFAULT) ultimately increases the chances that the auditor will issue a going concern report to the company. In this regard, they suggested different instances which express that a company is experiencing going concern problems in case of: (1) missed debt principal or interest payments, (2) covenant violations, or (3) restructuring of existing debt. It is expected that default will enhance the likelihood that auditor will issue a going concern report to the company. For this purpose, a dummy variable is used to measure whether the company is in default before the issuance of the audit report (1 = debt default and 0 = other). Next control variable is firm size (SIZE). Prior studies suggest that large companies are less prone to failure and the auditor may also hesitate to issue a going concern report to a large client as it may result in losing the significant fees generated by the large clients (Carcello & Neal, 2003; Mutchler et al., 1997). Therefore, a negative association between client size and auditor’s propensity to issue a going concern report is expected. The size is measured as the natural log of total sales (in thousands of PKR).

Audit committee size (SIZEAUDCOM) is the natural log of total number of audit committee members. Archambeault and DeZoort (2001) relate audit committee size with strong monitoring and suggest a positive relationship between the size of audit committee and the receipt of a going-concern report for a financially distressed company. Lastly, previous research focusing on audit committees has suggested that number of meetings of audit committee and board of directors enables effective monitoring (Tusek, 2015). A positive relation is expected between number of meetings of audit committee and the receipt of a going concern report for a financially distressed company. The number of meetings of audit committees (NOMTG) is measured as the natural log of total number of audit committee meetings in a given year. Industry and time fixed effects are used. All variables are winsorize at the 1% and 99% levels to minimize the potential effect of outliers.

Empirical Results

Descriptive Statistics

Table 1 presents the descriptive statistics of the variables included in our research model. The statistics show that the average audit committee stockholding (STHAC) in companies getting going concern report is 13.54% as compared to 37.9% in those companies getting a clean report. Similarly, average CEO influence (CEOINF) is also reported at a lower level, 7.81%, in companies getting going concern report than 22.8% in those companies getting a clean report. It emphasizes that stockholdings of audit committee members and CEO are weaker in those companies getting going concern reports than those getting clean reports. It may indicate that these stockholdings of audit committee members and CEO are playing their roles and helping those financially distressed companies in getting clean reports from auditors where the financial conditions of those companies warrant auditors to report otherwise.

Descriptive Statistics for Variables Used in the Analyses.

Note. In this table, variables are STHAC (audit committee stockholding), CEOINF (CEO influence), DEFAULT (missed debt/interest repayments, debt restructuring, and covenant violations), SIZE (measured as natural logarithm of total sales), SIZEAUDCOM (natural log of number of audit committee members), and NOMTG (natural log of number of audit committee meetings).

As expected, companies getting clean reports are larger in size (SIZE) 20.35 and have a lower default (DEFAULT) percentage of 32% than size of 18.55 and default percentage of 79%, respectively, of those companies getting going concern reports. It shows that auditors may find it difficult to issue going concern reports to larger companies. Further, size of audit committee (SIZEAUDCOM) and number of audit committee meetings (NOMTG) are almost similar in both categories of companies. We may infer that companies maintain size of audit committees and number of their meetings only for compliance purposes whereas making no real contribution to improve the objectivity and independence of auditor reporting.

Table 2 presents correlations among all the variables included in our research model. Audit committee stockholding and CEO stockholding have shown negative and highly significant association with audit report type. Some of the variables included therein have shown correlations above .50 which may indicate the presence of multicollinearity among some variables included in the research model, however, most of the correlations are below than more typical cut-off limit of .8 (Berry & Feldman, 1985). To overcome the problem of multicollinearity, z-standardization (subtracting mean of the variable from its original values and then dividing by standard deviation) of the explanatory variables was performed for all variables facing higher multicollinearity. Similar technique is used by earlier studies (Echambadi & Hess, 2007; Lacobucci, 2016) encountering multicollinearity.

Correlation Matrix.

***, **, and * indicate the coefficient is significant at 1%, 5%, and 10%, respectively.

Regression Results

Table 3 presents the results of logistic regression model used to analyze the relationship between audit committee stockholding (STHAC) and auditor reporting behavior for financially distressed companies. The overall model is highly significant as per generalized Wald test of explanatory variables following χ2 distribution. The results of Wald test reported Wald χ2 (7) = 34.43 with 7 degrees of freedom which is highly significant (p > χ2 = .000) and affirms the goodness of fit of the model.

Logistic Regression Results.

***, **, and * indicate the coefficient is significant at 1%, 5%, and 10%, respectively.

As predicted, the greater the percentage of audit committee stockholding, the less likely the auditor is to issue going concern report (p < .01). This finding conforms to our first hypothesis. Further, the interaction term (STHAC × CEOINF) between CEO influence (CEOINF) and audit committee stockholding reduces the likelihood for going concern report (p < .01) which conforms to our second hypothesis that CEO influence negatively moderates the relationship between audit committee stockholding and audit report type, that is, it exacerbates the relationship reported in first hypothesis.

These findings are in line with the previous literature that audit committee stockholding adversely affects the audit committee independence (Mangena & Pike, 2005) and objectivity of auditor reporting, hence, making them refrain from supporting auditors to perform their functions independently and objectively especially in case of financially distressed companies (Berglund et al., 2018; Saeed et al., 2021a,b). Due to lack of support from audit committee members, the auditors may not find them in a position to face the pressure of management and issue going concern reports to financially distressed companies when the financial condition of these companies warrants to do so. The situation becomes even more severe when there is involved CEO influence. If the CEO of a financially distressed company possesses stockholding in the company then it will aggravate the situation and auditor will be even lesser willing to issue the going concern report to such financially distressed company despite of bad financial situation of the company. All these inferences made by using research model specified for this study are in line with previous literature and support our hypotheses.

Control variables also show important findings. The likelihood of going concern report increases with Default (DEFAULT) (p < .01) which shows that if a company finds it difficult to pay back its liabilities then it may persuade auditor to issue going concern report to such company. On the other hand, size of the company (SIZE), size of the audit committee (SIZEAUDCOM), and number of meetings (NOMTG) held by committee have no significant effect on the likelihood of going concern report.

Procedural independence compared with substantive independence

As discussed earlier, most of the previous research studies related to audit committee independence have focused upon procedural independence, that is, whether the independence requirements posited by government regulations are complied with or not (Ali & Bin Nasir, 2014; Church et al., 2018; Sharma & Kuang, 2014; Xie et al., 2021). In Pakistan, the code of corporate governance requires an audit committee to completely consist of Non-Executive Directors (NEDs), one of whom is required to be an Independent Director (INED) who is also required to act as chairman of the audit committee. So, we incorporate a compliance variable (NED) to assess whether code’s regulations of audit committee independence are followed and check whether it has a relation with auditor reporting behavior for financially distressed companies. In our model, we replace the earlier used substantive independence measure (STHAC) with procedural independence measure (NED) and run the regression.

The results provided in Table 4 show that the compliance variable (NED) is not significant (p > .1) in explaining the auditor reporting behavior. Further, the interaction term (NED × CEOINF) between CEO influence (CEOINF) and compliance variable is also not significant in moderating the relationship between compliance variable and audit report type.

Audit Committee Procedural Independence.

***, **, and * indicate the coefficient is significant at 1%, 5%, and 10%, respectively.

As per our assertion, it shows that mere confirming procedural independence by checking compliance with regulations may not help understanding how audit committee independence can affect auditor reporting. On the other hand, as per the results presented in Table 4, it is ascertained that the greater the percentage of audit committee stockholding, the less likely the auditor is to issue going concern report (p < .01). These findings emphasize that substantive independence of audit committees is a crucial aspect, alongside procedural independence, to examine the association between overall audit committee independence and auditor reporting.

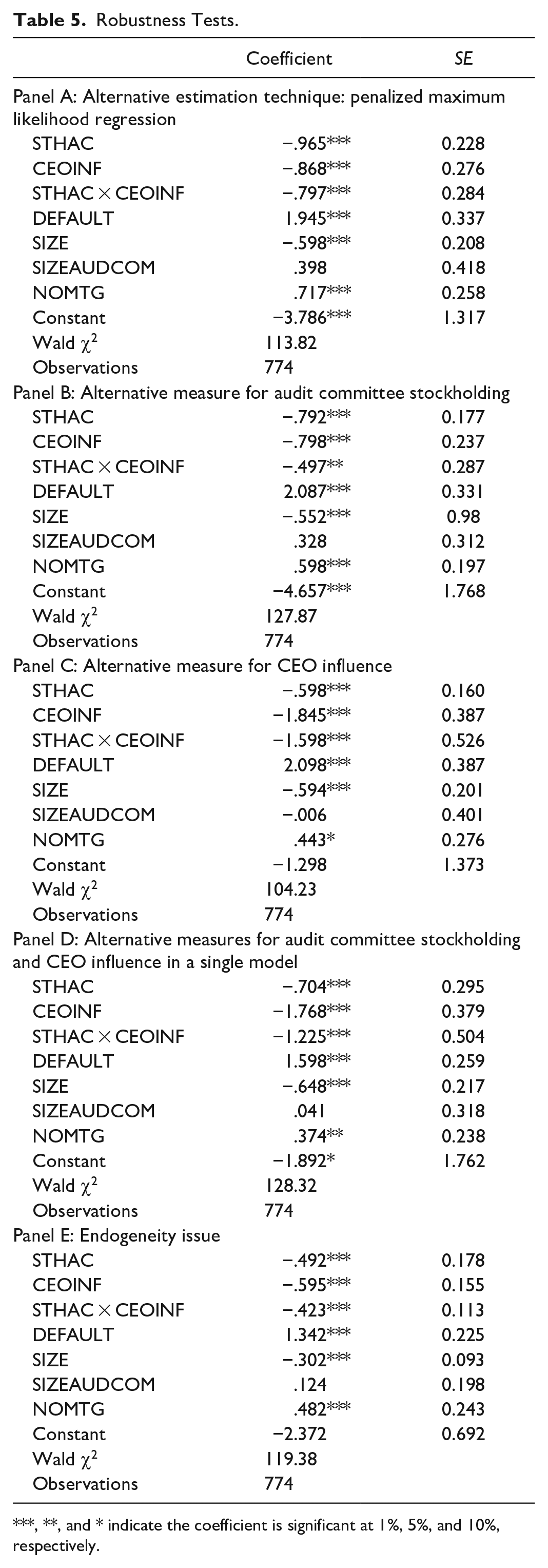

Robustness Tests

Alternative estimation technique: Penalized maximum likelihood

To check the robustness of our findings, we re-estimate our results using an alternative estimation technique, that is, penalized maximum likelihood (Firth logistic regression). Firth’s penalized maximum likelihood method produces finite parameter estimates by addressing the problems of rare events, sparseness, and small sample bias in panel data (Greenland & Mansournia, 2015). The results presented in panel A of Table 5, obtained by applying penalized maximum likelihood, show that the greater the percentage of audit committee stockholding, the less likely the auditor is to issue going concern report (p < .01). Further, the interaction term (STHAC × CEOINF) between CEO influence (CEOINF) and audit committee stockholding reduces the likelihood for going concern report (p < .01) which shows that CEO influence negatively moderates the relationship between audit committee stockholding and audit report type.

Robustness Tests.

***, **, and * indicate the coefficient is significant at 1%, 5%, and 10%, respectively.

These results collectively support the previous findings provided by conventional logistic regression, hence, affirming that our findings are not materially affected by the choice of estimation technique.

Alternative measure for audit committee stockholding

As discussed earlier, audit committee stockholding causes committee members to refrain from supporting auditors in their disputes with management where auditors think that financial situation of a company warrants them to issue going concern report. Bolton (2014) argues that if these committee members have close relatives serving on BOD which have stock holdings in these companies, it enhances the odds that committee members will be less supportive to auditors in their disputes with management where auditors think that financial condition of a company permits them to issue a going concern report. So, there is a possibility that our results are driven by the holdings of close friends and relatives. To address this concern, we use an alternative proxy for audit committee stockholding by including the stockholding of only audit committee members (excluding the stockholding of close relatives of audit committee members).

The results presented in panel B of Table 5 confirm previous findings of main logistic regression. The greater the percentage of ex-close relatives audit committee stockholding (STHAC), the less likely the auditor is to issue going concern report (p < .01). Further, the interaction term (STHAC × CEOINF) between CEO influence (CEOINF) and audit committee stockholding reduces the likelihood for going concern report (p < .05) showing that CEO influence negatively moderates the relationship between ex-close relatives audit committee stockholding and audit report type. These results affirm that overall findings of the main logistic regression are robust.

An alternative measure for CEO influence

To further test the robustness of results, we used CEO duality instead of stockholding of CEO as a source of power for CEO. Earlier studies suggest that CEO duality weakens the monitoring role of the board over executive management which may adversely affect the corporate performance and shareholders’ interests (Bliss et al., 2011; Nicholson & Kiel, 2007).

The inferences made in panel C of Table 5 are in support of the earlier findings from the main logistic regression. The greater the percentage of audit committee stockholding (STHAC), the less likely the auditor is to issue going concern report (p < .01). Further, the interaction term (STHAC×CEOINF) reduces the likelihood for going concern report (p < .05) showing that CEO duality negatively moderates the relationship between audit committee stockholding and audit report type. These results affirm the robustness of findings provided by the main logistic regression.

Additionally, we employed the alternative proxies for audit committee stockholding and CEO influence in a single model to check the robustness of previous findings. The results provided in panel D of Table 5 are in support of the previous findings from the main logistic regression.

Endogeneity issue

Panel data is often subject to the problem of endogeneity where an independent variable correlates with the error term of the model hence causing the covariance of independent variable and error term not to be zero resulting in the reported estimations being inaccurate and biased (Woolridge, 2002). So, to test for endogeneity, we employed a control function estimator or instrumental variable approach known as probit model with continuous endogenous regressors which is a widely used technique to assess the problem of endogeneity in binary response models.

For employing a probit model with continuous endogenous regressors, an instrumental variable is needed which is highly correlated with endogenous variable and is independent of error term. For that purpose, we used stockholding of executive directors (STHE × Dir) as an instrumental variable and applied a probit model with continuous endogenous regressors to test the presence of endogeneity. The underlying rationale to use stockholding of executive directors as an instrumental variable is that it can often highly affect the independence of audit committee members (non-executive directors). According to Code of Corporate Governance (2012) issued by SECP, various matters regarding committee members’ nomination, salary, etc. are decided by executive directors serving on board which can cause those executive directors to exert influence on audit committee members. Further, there may be built close associations and relations between these executive and non-executive directors (O’Sullivan & Wong, 1999) which can affect the performance of these non-executive directors. However, the stockholding of these executive directors may not directly affect the audit report type as executive directors do not directly work with auditor and they can exert their influence on auditor only through audit committee members. So, it is presumably safe to use stockholding of executive directors as an instrumental variable.

Firstly, as per results given in panel E of Table 5, the values of Wald test of exogeneity, χ2 (1) = 2.21, p > χ2 = .1370 show that we cannot reject the null hypothesis of exogeneity, that is, there exists no endogeneity in variables. It shows that variables used in logistic regression model are exogenous and are not affected by the problem of endogeneity (Chang & Park, 2010).

Secondly, the results confirm our previous findings from the main logistic regression. The greater the percentage of audit committee stockholding (STHAC), the less likely the auditor is to issue going concern report (p < .01). Further, the interaction term (STHAC × CEOINF) between CEO influence (CEOINF) and audit committee stockholding reduces the likelihood for going concern report (p < .01) showing that CEO influence negatively moderates the relationship between audit committee stockholding and audit report type. The overall probit model is highly significant as per generalized Wald test of explanatory variables following χ2 distribution. The results of Wald test reported Wald χ2 (7) = 131.97 with 7 degrees of freedom which is highly significant (p > χ2 = .000) and affirms the goodness of fit of the model.

Discussion and Conclusion

This study provides significant insights regarding the association between audit committee independence and auditor reporting for financially distressed companies. The stockholding of audit committee members along with their close relatives serving on board is used to assess its impact on audit committee independence and, ultimately, on auditor reporting behavior. Alongside, this study also emphasizes the importance of interactions between different corporate governance components by examining that how CEO influence can interact with stockholding of audit committee members to affect the objectivity of auditing process for financially distressed companies.

The results of this study support our predictions and are also in line with extant literature. The results report a negative and highly significant relationship between audit committee stockholding and auditor’s propensity to issue going concern reports to financially distressed companies showing that stockholding of audit committee members is a crucial factor that affects their independence and persuades them to adversely affect the auditing process in financially distressed companies (Berglund et al., 2018; Carcello & Neal, 2000). Furthermore, the results show that CEO influence gives power to executive management to exert its impact on audit committee independence (Finkelstein, 1992) and, hence, exacerbates the relationship between stockholding of audit committee members and auditor reporting behavior in financially distressed companies.

Like any other research, this study is subject to limitations. We have focused on stockholding as the key criterion to assess how it impairs the independence of audit committee members persuading them to refrain from supporting auditors in performing their functions objectively. There are other ways to measure the independence of committee members such as compliance with relevant regulations, social ties with management, and political affiliations (Bliss et al., 2011). Future research studies may employ these criteria to assess the independence of audit committee members and its impact on auditor reporting behavior. Similarly, we have used stockholding as a source of power for CEO causing executive management to exert its influence on audit committees and the auditing process. It would be interesting to use other potential sources of power for CEO, for example, educational background, financial expertise, industry expertise, political affiliations, etc., and evaluate their effects on audit committee independence and auditing process.

Further, while we have applied various robustness tests using alternative variables and estimation techniques, we may not have successfully identified and used all the possible variables affecting audit committee independence and auditor reporting behavior. So, future studies in this research area may consider incorporating further relevant variables along with applying different robustness tests that may help to improve the quality of research. In addition, the future studies may consider other proxies of audit committee effectiveness used in the prior studies such as audit committee chair’s ability, audit committee fees, non-audit service fees, and Big four audit firms (Al-Shaer & Zaman, 2018; Ghafran & O’Sullivan, 2013; Khemakhem & Fontaine, 2019; Zaman et al., 2011). Lastly, the scope, context, and regulatory setting of this study is focused on companies listed on Pakistan Stock Exchange (PSX) hence narrowing its focus on Pakistan only. Researchers may consider widening the scope of this study by incorporating companies from other countries as well and corroborate the results across countries to explore important insights.

Notwithstanding the limitations discussed above, our research study has many significant implications. Our results contribute to the growing body of literature regarding different corporate governance mechanisms and their impacts on the transparency of financial reporting and auditing processes. The results of this study emphasize the importance of substantive independence rather than procedural independence of audit committees. It implies that it may not sufficient to observe superficial compliance with regulations to ensure audit committee independence but there is a need to focus on more practical factors, for example, stockholding to assess how these may affect audit committee independence. It also provides vital information for shareholders and investors to understand the relations between different corporate governance mechanisms when making investment decisions. It provides important insights for professionals, policymakers, and regulators that there are many other factors that need to be addressed by increased regulations to ensure audit committee independence and objectivity of auditor reporting. Specifically, there may be needed regulations to monitor and control stockholding of audit committee members and their close relatives serving on boards as it can adversely affect the independence of these audit committee members and, ultimately, the auditing process. The results also suggest the need for regulations that can control the negative impact of CEO influence on audit committee independence which impairs the overall auditing process. Improved regulations regarding these corporate governance areas may not only improve the substantive independence of audit committees but also enhance the efficiency of the auditing process.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.