Abstract

The founder is the cornerstone of the establishment of a company, and plays a vital role in the decision-making and cohesion of the company, as well as the operation of the company, and thus has a positive impact on the growth and performance of the company. This study takes founder control as the starting point, analyzes the correlation between founder control, equity financing, corporate radical strategy, and corporate performance, and selects 2010 to 2019 listed companies in China as the research sample. Based on literature review and theoretical analysis, four main hypotheses of this research are put forward. After descriptive statistical analysis, correlation statistical analysis, and empirical model testing of sample data, the following research conclusions are obtained. First, there is a negative correlation between founder control and equity financing. Second, there is a negative correlation between equity financing and corporate performance. Third, a corporate radical strategy has a negative moderating effect on the relevance between founder control and corporate performance. Fourth, equity financing has an enhanced mediating effect on the relevance between founder control and corporate performance. Fifth, the degree of corporate strategy of non-state-owned enterprises has a negative moderating effect on the correlation between founder control and corporate performance. Furthermore, based on the research conclusions above, this research puts forward the following recommendations: First, according to the different stages of enterprise development, reasonably restrict the control of the founder of the enterprise. Second, focus on long-term benefits and adopt strategic changes at the right time.

Introduction

Research Background

The founder, a cornerstone to the establishment of a company, plays a vital role in the decision-making, cohesion and business operation of a company. Thus, it has a positive impact on the growth and performance of the company. As for a company, its CEO, also a founder, has accumulated invaluable expertise and practical experience that are usually converted into more inspiring stock performance (Fahlenbrach, 2009). Considering funds as a vital resource for the growth and development of a company, the company takes one of the most significant financing channels (called equity financing) that assists the company in exchanging enough liquid funds to sustain and expand its businesses (Lewis & Tan, 2016; Zhang et al., 2016). However, what is equity financing is that a founder or a holder of initial shares exchanges its part of company ownership for the funds from external sources, which, eventually, may impair the founder’s control over the company. In the event that such control elapses at the founder’s hands, the company will be whipped by uncertainty in terms of development orientation, strategy and operation mode.

Research Issue

Funds, a kind of significant corporate resources, plays a role as a rare element that is vital to expand business and produce profits. In turn, financing policies belong to far-reaching decisions of a company. Financing acts as a major channel to fulfill the ultimate goal of business activities-maximize enterprise value under the balance between risks and returns. The ways in which a company take for financing will give rise to butterfly effects on benefits of such stakeholders as shareholders, managerial staff, and creditors, let alone the financing costs that the company will have to pay. All of these factors are directly interlocked with achievements in goals of business activities. In other words, any inappropriate financing decision that a company makes will shrink stakeholders’ benefits, and thus, negative influences will land on the overall corporate value to be materialized.

As for a company, the issue above anything else is funds, also known as financing or fund raising. Generally, it refers to a kind of economic behavior in which an economic obtain funds through applicable channels or in appropriate ways. There are three ways that most companies are inclined to take: (1) Retain part of company profits; (2) Debt financing: a company obtain funds from banks or corporate bond offering; (3) stock offering. In consideration of differences in strength and weak points of various financing ways, the corporate financing theory places stress on researches aiming at motives and appropriate percentages that a company takes to make a choice among retained earnings, bonds, and stocks. Strongly and mentally as a founder is stimulated and motivated to remain control rights, the corporate development would not be materialized without capital financing. Therefore, the following questions are posed in this paper: what effect will different founder control impose upon corporate decisions on equity financing? Further, what effect will founder control bring to the development strategy and corporate performance of a company?

Research objective

Financing strategies are the lifeblood of corporate development. The equity financing shapes the capital structure of a company. Therefore, this study begins with founder controls, analyzes what financing decisions a company will make under founder control, and probes into effects that is imposed by the capital structure under such financing decision upon corporate performance. In other words, this study attempts to unveil following effects of founder control on equity financing decisions and corporate performance under radical strategies: (1) the effect of founder control on equity financing; (2) the effect of equity financing on corporate performance; (3) the moderating effect of corporate radical strategies on the relevance between fonder control and corporate performance; (4) the mediating effect of equity financing on founder control and corporate performance.

The innovation of this study lies in: (1) founder control taken as the base of financing decisions to better align the corporate capital structure in a new way; (2) a new logical framework built up to incorporate strategic choices into the effect mechanism of founder control, financing behavior and corporate performance.

Literature Review and Research Hypothesis

Theoretical Foundation

Theory of control right

Just as implied in the theory of control right that was initially imposed by Grossman and Hart (1987), shareholders could exclusively dispose of corporate assets, and in particular, corporate assets could be used for the purpose of decision rights on investment and business operation. Secondly, Grossman and Hart argued that enterprise income could be divided into control benefits and equity returns. It is elicited from the theory of private benefits of control that a majority holding shareholder exercises own financing decision rights to seek for personal benefits when preparing financing plans largely based on individual interests. Furthermore, capital structure is a determiner of the control right structure, while the theory of control right of capital structure is used to explain the effect of financing decisions on control right from the perspective of ill-prepared financing contracts.

Stakeholder theory

Stakeholders stand for all individuals and groups that could lay influences on fulfillment of goals. Without resources provided by stakeholders, business activities and sustainable development of a company will never be born. Various stakeholders serve as different channels to raise performance and value of the company. In company are embraced a constellation of stakeholders, such as investors, managerial staff, providers, shareholders, staff members, governments, and communities. While making contributions to corporate development in various respects, they are faced with all risks that follow such contributions. As far as a company’s concerned, its long-lasting business activities and sustainable development are not just founded on maximized benefits of shareholders, but determined by high-effective settlement pertinent to the relationship with stakeholders of all kinds (Freeman, 1984).

With enormous effects given by this theory upon corporate performance enhancement, participation and investment of a stakeholder in corporate development seem as a powerful force that could never be neglected to expand a company. In pursuit of own maximized benefits, a shareholder is advised to take into account restraints from other stakeholders, rather than aim at own benefits regardless of rights enjoyed by other stakeholders. Otherwise, all provisions under contracts will collapse, and in turn, new stakeholders will come into being when they sign updated contracts after the company is reorganized.

Literature Review

According to the theory of company control right, the financing structure of a company controls benefit flows after the company receives earnings, and it also determines the transfer and assignment of company control right. Of all researches on control right and equity financing, first of all, Du and Dai (2010) take data of nine companies in different countries to investigate into the relationship between the ultimate control right and capital structure, from which it is elicited that a company with bigger bias data about cash flow right and control right would be apt to high leverage. Among experts who, in the early time, analyzed equity financing preferences, Wang et al. (2012) pose their viewpoint that ill-developed equity structure of Chinese listed companies is behind inordinate equity concentration, while equity arrangements are featured by insider control in the circumstance of destitution of state-owned shares, and secondary equity offering becomes a major financing way that a listed company adopts, due to preferences of managers and non-public shareholders. Zhang (2003) makes a study on equity financing, in which benefit expropriation by Substantial Shareholder is further examined in three aspects-investment efficiency, resource expropriation by substantial Shareholders, and value effects on unfair related-party transactions. In research results, it is disclosed that secondary equity offering strongly motivates substantial shareholders with super control to clandestinely fight for private benefits in various ways for the purpose of quickened capital gains, which, in nature, deprives minority shareholders of their benefits. Xiao (2012) argues that conflicts between controlling shareholders and minority shareholders, rather than between managerial staff and shareholders, have predominated agency collisions in the event that ownership is centralized and separated from control right. In studies, Ni et al. (2015) point out that the equity financing that a listed company takes is never immune from benefit expropriation committed by controlling shareholders. Furthermore, the financing scale is a significant indicator that defines its tunneling, with separation from needs for equity financing- investment-based financing adopted for high returns, while money-based financing taken for low returns.

With regard to relevance between equity financing and corporate performance, on the other hand, Brown and Petersen (2009) propose their view in studies that the flourishing stock market could lower down costs of equity financing to enhance profitability of a company. Hovakimian (2011) contend through studies that when faced with difficulties in obtaining external financing and expenditures on agency costs, a managerial staff of a company is required to allocate funds to more promising investment opportunities, which will, in fact, ameliorates corporate performance. The finding from studies made by Lewis and Tan (2016) tells that company’s choices and anticipation-related optimal financing structure could effectively bring more profits. Thus, equity financing ought to enjoy a higher percentage of corporate financing if the company witnesses its growth in favorable anticipation. Zhang et al. (2015) argues that an innovation-based company in pursuit of equity financing is advised to draw attention of investors to prospective high returns generated by new technologies and products. As the company’s desire for innovation funds projects both high returns and high risks on shoulders of investors, an innovation-based company, more often than not, will acquire necessary liquid funds from equity financing to sustain and expand its businesses for the purpose of corporate performance enhancement. However, from own studies based on small and medium-sized enterprises in Switzerland, Yazdanfar and Oehman (2015) conclude the finding that long-standing debts will intensify agency conflicts and even trigger bankruptcy of a company. Liu (2014) elicits that equity financing significantly imposes negative effects on corporate performance after he applies multiple linear regression into his empirical studies on Chinese listed companies in the field of non-ferrous metals.

Stimulated by frequent fight for control rights in recent years, more case studies on control rights have spout out in terms of researches pertaining the control right theory and financing structure. Some experts hold that fights for control rights could help to streamline the capital structure of a company, while some of other experts infer from own studies that such fights do harm to optimization of corporate governance structure, with a plenty of negative effects upon corporate performance. As the spotlight in the academic community, a great number of researches on financing’s effects upon corporate performance have been made by experts from home and abroad in various dimensions and fields. What could be inferred from the literature review is that effects of external financing ways upon listed companies vary with different fields. Notwithstanding, equity financing could boost the improvement in corporate performance of a listed company in the field in which the company engages.

Research Hypothesis

Effect of founder control on equity financing

In the case that a founder of a company is the largest shareholder, equity financing will weaken the ultimate control right, but debt financing will not (Du & Dai, 2010). What’s more, the founder shareholder will make use of its information advantages to hold back the corporate equity financing more bitterly (Ni et al., 2015). Finally, the ultimate controlling shareholder troubled by the larger sum of debts will have no choice but to spend more free cash flow in reducing agency conflicts between such shareholders and minority shareholders (Frank & Goyal, 2007; Xiao, 2012). With more founder controls, debt financing will become a preferred way of financing. As a result, Hypothesis 1 is put forth in this paper as below:

Hypothesis 1: Founder control imposes negative effects on equity financing.

Effect of equity financing on corporate performance

For a company, there is the inevitable correlation between financing structure and corporate governance (Mao, 2016): on one hand, the stock issuance for financing will lay negative influences upon a company, for such a financing way would send a signal of overestimated corporate value to external investors; equity financing would result in over-investment by operators of listed companies through reducing financing costs, and thus, the efficiency of fund utilization would be lowered down (Gilson & Schizer, 2003; Yazdanfar & Oehman,2015). With the swelling percentage of equity financing, on the other, the agency costs incurred by agency issues will go up (Liu, 2014; Zeitun & Tian, 2007), imposing negative effects on corporate performance. To be specific, it is signified by the ensuing corporate performance shrinkage that information asymmetry would result from the consequence that the company operator is no longer the full owner of a company since equity financing decentralizes ownership, control right, and income right of a company. With pursuing maximal own benefits, the operator is predicted to make decisions that damages benefits of the owner. In other words, moral risks strike entrusted agency. Therefore, a company is required to formulate stern and well-developed governance systems for restraint of operator’s behaviors. However, it will not just raise costs of supervision and business activities, but will inevitably generate other negative effects. Therefore, Hypothesis 2 is contrived on the basis of this analysis.

Hypothesis 2: Equity financing imposes negative effects on corporate performance.

Moderating effect of corporate radical strategy on founder control and corporate performance

Owning to the preference given to founder control, the founder of a company is reluctantly to choose corporate decisions of higher risks; consequently, a great number of opportunities for the corporate development will be doom to sneak (Zhu & Wang, 2012). For instance, the founder is more apt to choose debt financing rather than equity financing while making financing decisions (Lewis & Tan, 2016). On the contrary, shareholders, with the hope that the company would choose more equity financing, will adopt radical strategies that acts as a uncertain factor to the long-term development of a company, but also as a aider to the growth of corporate performance in the long run (Larrain & Urzúa, 2013; Zheng et al., 2016). In this paper, therefore, radical strategies would help to improve corporate performance, that is, radical strategies could, to a certain extent, hold up conservative financing ways under founder control to mitigate negative effects of founder control on corporate performance. The analysis above catalyzes Hypothesis 3 in this paper.

Hypothesis 3: Corporate radical strategy has a moderating effect to suppress the relevance between founder control and corporate performance.

Mediating effect of equity financing on founder control and corporate performance

A founder would pick out a financing way to maximize own benefits for the benefits of control (Hart, 2003). As the restriction ratio of competitive shareholders is elevated by the streamlined allocation of control right, financing structure will take on changes that bring modified structure of corporate governance (Flannery & Rangan, 2006; Xiao, 2012). Furthermore, costs and risks of financing will be adjusted to changes in financing structure, from which the corporate performance will be under impacts (Liu, 2016). In a certain sense, the corporate equity financing could be seen as the intermediate variable of the effect that the founder’s preference of control right imposes on the corporate performance. Finally, Hypothesis 4 comes out in this paper.

Hypothesis 4: Corporate equity financing has a mediating effect on the founder control preference and corporate performance.

Research Design

Sample selection

For this study, 2010 to 2019 listed companies in The Shanghai Stock Exchange and The Shenzhen Stock Exchange are selected as research samples to verify the correlation between founder control, equity financing, corporate radical strategy, and corporate performance. All data are sourced from CSMAR database. Sample data are filtered and acquired through: (1) eliminating ST and *ST samples; (2) eliminating samples in sectors of finance and insurance; (3) eliminating samples with incomplete fiscal data. Finally, 8,093 sample companies are used as research samples after acquired sample data are sorted and analyzed with tools of EXCEL and STATA12.

Definition of Variables

Dependent variable-corporate performance

In this study, corporate performance is seen as the explained variable to truly project business outcomes and financial standings of a company. As an indicator that vividly describes asset operation, cost reimbursement, and risk control of a company, corporate performance could be used to mirror the selection and implementation of corporate strategies in an indirect way (Huang et al., 2011). In this paper, return on asset (ROA) serves as an indicator for corporate performance to be measured. ROA shows the ratio between net profits and average total assets, equivalent to net profits from each unit of assets.

Independent variable-founder control

A founder is the person who establishes a company, the ownership of which, however, belongs to the person(s) who has(have) the contractual relationship with the company (namely, company owner and shareholders). In this sense, it is found in this study that the founder will still hold the control right if the found keeps the right of management (Feng, 2010; Li, 2015). According to the annual report of the company, the POWER value (founder control) in this study is 1 if the founder continues to hold the control right over business operation of the company; and otherwise, it is 0, which means the company founder loses the control right.

Moderator variable-radical strategy

The corporate strategy mentioned in this paper refers to adjustment and changes that a company makes in allocation of key strategic resources. With reference to measuring methods taken by such experts as Zhang (2003), and Barton and Gordon (2010), together with data accessibility, the corporate strategy is measured in six dimensions for the reasons as below: (1) all of six dimensions are under the control of senior executives; (2) they play a vital role in corporate performance; (3) they are complementary. Each of them focuses on a significant and particular corporate strategy; (4) they could be modified for data collection, and relatively comparable across different companies in the same sector. Six dimensions include market investment (M1 = selling expense/operation revenue), research input (M2 = development expense/operation revenue), corporate growth=(M3 = growth rate of operation revenue), expenditure (M4 = management expense/operation revenue), work efficiency (M5 = staff quantity/operation revenue), and capital intensity (M6 = fixed asset/total assets). For the indicator in each of six dimensions, its moving mean at the interval of 5 years is calculated as the ultimate value. The strategic value MARK = M1 + M2 + M3 + M4 + M5 + M6. This value is used to measure the intensity of strategy radicalization. Highly radical strategy means the company has adopted more radical strategies in that year, while the lower one stands for conservative strategies the company has adopted in that year.

Mediator variable-equity financing

Equity financing refers to such financing ways as public offering and private equity, that is, original shareholders of a company are willing to transfer parts of the company ownership through capital increase for the purpose of demanded funds. With reference to researches made by Larrain & Urzúa (2013), and Li and Xu (2015), this paper takes this indicator to measure the equity financing of listed real estate companies, probing into the effect of changes in the equity financing rate (SFR) on corporate performance of listed companies.

Control variable

The following variables are used as control variables, together with industry and year taken as control variables: company size (SIZE), company ownership (STATE), size of board of directors (BOARDS), shareholding ratio of board of directors (BSTOCK), separation extent of ownership and control right (TP), financial leverage (LEV), and stock at TOP 10 shareholders (Table 1).

Description of Each Variable.

Model Building

For the sake of Hypothesis 1verification, the multiple linear regression is adopted on the basis of previous literature (Huang et al., 2011; Larrain & Urzúa, 2013; Li & Xu, 2015) to build a random effect model that is used to test the effect of founder control on equity financing. In Model 1, the coefficient α1 represents the relevance between founder control and equity financing.

In model 1, it contains the explained variable—SFR (corporate equity financing), and control variables (also explanatory variables) like founder control (POWER), company size (SIZE), company ownership (STATE), shareholding ratio of board of directors (BSTOCK), stock at TOP 10 shareholders; INDU refers to the control over a company for shield against industrial influences, and YEAR stands for the control over a company for shield against years.

For the sake of Hypothesis 2 verification, the multiple linear regression is adopted on the basis of previous literature to build a random effect model that is used to test the effect of equity financing on corporate performance. In Model 2, the coefficient α1 represents the relevance between equity financing and corporate performance.

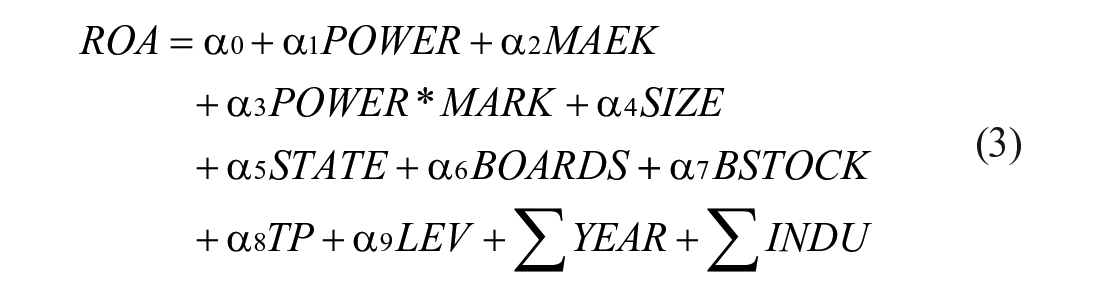

In model 2, it contains the explained variable—ROA (corporate performance), and control variables (also explanatory variables) like SFR (corporate equity financing), company size (SIZE), company ownership (STATE), size of board of directors (BOARDS), shareholding ratio of board of directors (BSTOCK), separation extent of ownership and control right (TP), financial leverage (LEV); INDU refers to the control over a company for shield against industrial influences, and YEAR stands for the control over a company for shield against years.

For the sake of Hypothesis 3 verification, the stepwise regression (Bansal & Thenmozhi, 2020) is adopted on the basis of previous literature to build three random effect models that is used to test the moderating effect of radical strategies on founder control and corporate performance, including Model 3 for the first-step regression to verify the effect of founder control on corporate performance; Model 4 for the second step to verify the effect of founder control and radical strategies on corporate performance, and Model 6 to verify the moderating effect of radical strategies on founder control and corporate performance. Just as described in the verification criteria of moderating effects, the factor α3 in the interaction term in Model 6 appears significant if the factor α1 in Model 3, and α1 and α2 in Model 4 show significant. In turn, the moderating effect of radical strategies on founder control and corporate performance are proved.

In Model 3, 4, and 5 mentioned above, the explained variable ROA refers to corporate performance, and the explanatory variable is POWER which stands for founder control. Control variables also serve as moderator variables including: MARK (extent of radical corporate strategies), SIZE (company size), STATE (company ownership), BOARDS (size of board of directors), BSTOCK (shareholding ratio of board of directors), TP (separation extent of ownership and control right), LEV (financial leverage); INDU refers to the control over a company for shield against industrial influences, and YEAR stands for the control over a company for shield against years.

For the sake of Hypothesis 4 verification, the stepwise regression is adopted on the basis of previous literature to build three random effect models that is used to test the mediating effect of equity financing on founder control and corporate performance. Just as described in the verification principle of mediating effects, the first step is to verify the relevance between independent variable X and dependent variable Y, Y = cX + ε. It is called Model (3) for this study on effects of founder control on corporate performance. The second step is to verify the relevance between independent variable X and mediator variable M, M = aX + ε. It is called Model (1) for this study on effects of equity financing on founder control. The third step is to verify the relationships among independent variable X, mediator variable M and dependent variable Y, Y = c’X + bM + ε. Accordingly, Model 6 is built. If α1 in Model 2, and α1 and α2 in Model 6 appear significant, the mediator variable is significant once they are regression coefficients.

In Model 6, the explained variable ROA stands for corporate performance, and the explanatory variable POWER refers to founder control. Model 6 contains control variables like SFR (the mediator variable, corporate equity financing), company size (SIZE), company ownership (STATE), size of board of directors (BOARDS), shareholding ratio of board of directors (BSTOCK), separation extent of ownership and control right (TP), financial leverage (LEV); INDU refers to the control over a company for shield against industrial influences, and YEAR stands for the control over a company for shield against years.

Empirical Result

This paper, beginning with founder control, analyzes the relevance among founder control, equity financing, radical corporate strategies, and corporate performance. Such approaches as descriptive statistics, relevance analysis, and multiple linear regression analysis are applied to the empirical analysis for verification of research hypotheses.

Descriptive Analysis and Correlation Analysis

As indicated in results of descriptive statistical analysis for all variables, Table 2 shows that the explained variable (corporate performance, ROA) sees the minimum at −0.19, with the mean at 0.04. Its maximum is 0.21, with standard deviation at 0.05. Based on this analysis, the corporate performance witnesses big differences among sampled companies, and experiences a certain of fluctuation. Highly discrete corporate performance results from a wide range of factors that influence corporate performance. As for founder control-an explained variable, the mean POWER value is 0.17, with standard deviation at 0.38 and 1,394 samples at POWER > 0. This is to say that sampled companies take up a low percentage of those companies still controlled by founders. The moderator variable MARK unveils how radical a corporate strategy is. For MARK, its mean is 0.69, with standard deviation at 0.86, minimum at −0.12, and maximum at 8.51. Only 2,388 samples get the MARK value greater than the mean 0.69, accounting for 29.51% of total samples, which discloses that sampled companies are more inclined to adopt conservative strategies (few of companies choose aggressive ones). The mediator variable-equity financing (SFR) shows its mean at 0.36, with standard deviation at 0.24, the minimum 0.03, and the maximum 1.59. Its analysis and comparison with debt financing tells that equity financing overweighs debt financing for 56% of sampled companies. Thus, from the perspective of financing structure, sampled companies prefer equity financing. Higher maximum of equity financing signifies more notable fluctuation. The maximum LEV 3.5343 refers to 3.5343 times as many as reights and interests held by the owner of the company with the most debts in research samples. The mean TP value is 5.0072 with its maximum 29.3613, which tells that the majority of sampled companies witness the large extent of separation between their control rights and ownership. The mean value of stocks at TOP 10 shareholders amounts to 0.2300 with the maximum 14.6500, which implies that there are huge differences in stocks held by TOP 10 shareholders among research samples, and its mean value is 0.2300%, with the maximum 14.6500%.

Descriptive Statistic Data of Each Variable.

In Table 3 are listed the results of correlation statistical analysis for each variable. There is a significantly negative relationship between POWER and SFR, by which Hypothesis 1 is proved preliminarily. There is a significantly negative relationship between ROA and SFR, by which Hypothesis 2 is proved preliminarily. Furthermore, the absolute value of correlation among each variable is lower than 0.50, indicating no serious multicollinearity among each dependent variable.

Pearson Correlation Analysis of Each Variable.

The correlation is significant at .05.

The correlation is significant at .01.

Effect of Founder Control on Equity Financing

In Table 4, PANEL_A is used to verify the correlation between founder control (POWER) and equity financing (SFR). Random Effect Model 1 gets goodness of fit (R2) 0.38 that shows its satisfactory goodness of fit. This is to say this model is statistically meaningful. Its testing value F is 197.90, appearing significant at the 1% significance level. Therefore, Model 1 is proved to pass the significance testing, and in other word, there is the effect of founder control on equity financing. In the economic sense, the regression coefficient of the model discloses that POWER has the correlation coefficient at −.01, with testing value T −1.81 and p < .10. This is the projection of the significantly negative correlation between SFR and POWER at the 10% confidence level, which unveils the negative correlation between founder control and equity financing, that is to say, bigger founder control results in less equity financing. Consequently, Hypothesis 1 in this paper is proved.

Regression of Founder Control to Equity Financing and Corporate Performance.

Note. T Value is parenthesized.

, **, and * respectively stand for the 1%, 5%, and 10% significance level.

As indicated in above mentioned regression results, founders will avoid equity financing methods that could dilute their control rights. To be specific, those founders with deeper control rights will be more apt to take advantage of their strength in information and rights for the purpose of more challengeable obstructions on equity financing that will, in turn, avert the eye of a company to debt financing.

Effect of Equity Financing on Corporate Performance

In Table 4, PANEL_B is used to verify the correlation between equity financing (SFR) and corporate performance (ROA). Random Effect Model 2 gets goodness of fit (R2) 0.20 that shows its satisfactory goodness of fit. This is to say this model is statistically meaningful. Its testing value F is 76.21, appearing significant at the 1% significance level. Therefore, Model 2 is proved to pass the significance testing, and in other word, there is the effect of equity financing on corporate performance. In the economic sense, the regression coefficient of the model discloses that SFR has the correlation coefficient at −0.07, with testing value T 22.12 and p < 0.01. This is the projection of the significantly negative correlation between SFR and ROA at the 1% confidence level. In other words, more equity financing that a company adopts will lead to worse corporate performance. Consequently, Hypothesis 1 in this paper is proved.

As shown in the regression coefficient of the model, there is the negative correlation between SFR and ROA at the 1% confidence level, which indicates that equity financing will catalyze rising agency costs. Based on this, Hypothesis 2 in this paper is proved that there is a negative correlation between equity financing and corporate performance.

Moderating Effect of Radical Strategy on Founder Control and Corporate Performance

The three-step regression is essential to verify the moderating effect of corporate strategy (MARK) on founder control (POWER) and corporate performance (ROA). Step 1: verify the correlation between ROA and POWER in Model 3. According to results in Table 5, the correlation between ROA and POWER has the coefficient −.01, with testing value T −2.87 and p < .01. This projects the significantly negative correlation between ROA and POWER at the 1% confidence level. In other words, deeper founder control will bring worse corporate performance. Thus, the first step of moderating effects is proved: founder control will impose influences corporate performance.

Moderating Effect of Corporate Radical Strategy on Founder Control and Corporate Performance.

Note. T Value is parenthesized.

, **, and * respectively stand for the 1%, 5%, and 10% significance level.

Step 2: Add MARK onto the results after Step 1 is done (namely, Model 4). According to results in Table 5, the correlation between ROA and POWER has the coefficient −.01, with testing value T −2.36 and p < .01. This projects the significantly negative correlation between ROA and POWER at the 1% confidence level. However, MARK has the correlation coefficient .01, with testing value T 5.84 and p < .01. This projects the significantly positive correlation between MARK and ROA at the 1% level, which implies that the larger extent of radical corporate strategies will generate more favorable corporate performance. That is to say, the second step of moderating effects is proved.

Step 3: verify the significance of interaction terms in Model 3. First, Model 1 gets goodness of fit (R2) 0.38 that shows its satisfactory goodness of fit. This is to say this model is statistically meaningful. Its testing value F is 197.90, appearing significant at the 1% significance level. Therefore, Model 1 is proved to pass the significance testing, and in other word, there is the effect of founder control on equity financing.

Based on the analysis from the perspective of economic significance, the interaction term of full sample–MARK * POWER get the coefficient .01 with testing value T 3.27 and p < .01, that is, MARK*POWER is significantly and positively correlated with ROA at the 1% confidence level. Furthermore, there is the negative correlation between POWER and ROA; in other words, deeper founder control will more significantly weaken corporate performance. Since radical corporate strategies could stimulate corporate performance, they will, in turn, mitigate negative influences of founder control upon corporate performance. Consequently, Hypothesis 3 in this paper is proved: corporate strategies impose the negative moderating effect on relevance between founder control and corporate performance.

With reference to MARK, the samples are divided into two groups—radical strategy and conservative strategy. It is found that the coefficient of the interaction term MARK*POWER is significantly and positively correlated with ROA at the 1% confidence level in the former group, while in the latter group, no significant correlation between the coefficient of the interaction term MARK*POWER and ROA is detected. Further, corporate radical strategy could positively influence corporate performance, and even suppress the negative effect of founder control on corporate performance. Therefore, Hypothesis 3 in this paper is proved.

Mediating Effect of Equity Financing on Founder Control and Corporate Performance

The verification rules for the mediating effect are used for: step 1, verify the correlation between independent variable X and dependent variable Y, Y = cX + ε. Step 2, verify the correlation between independent variable X and mediator variable M, M = aX + ε. Step 3, verify the relationship among independent variable X, mediator variable M and dependent variable Y, Y = c’X + bM + ε, and if a, b, and c’ are significant regression coefficients, mediator variable M will appear significant.

The three-step regression is essential to verify the mediating effect of equity financing (DEBT) on founder control (POWER) and corporate performance (ROA).

Step 1: verify the correlation between ROA and POWER. The correlation between ROA and POWER has the coefficient −.01, with testing value T −2.87 and p < .01. This projects the significantly negative correlation between ROA and POWER at the 1% confidence level. That is to say, deeper founder control is followed by worse corporate performance. Thus, the first step of the mediating effect is proved: founder control will impose effects on corporate performance.

Step 2: Based on the regression in Model 1, the correlation between POWER and SFR has the coefficient −.01, with testing value T −1.81 and p < .10. This projects the significantly negative correlation between SFR and POWER at the 10% confidence level. That is to say, deeper founder control decreases corporate equity financing. Thus, the second step of the mediating effect is proved: founder control will impose effects on equity financing.

Step 3: verify the mediating effect with Model 4. According to results in Table 6, Model 4 gets goodness of fit (R2) 0.38 that is in line with satisfaction. This is to say this model is statistically meaningful. Its testing value F is 73.99, appearing significant at the 1% significance level. Therefore, Model 4 is proved to pass the significance testing.

Mediating Effect of Equity Financing on Founder Control and Corporate Performance.

Note. T Value is parenthesized.

, **, and * respectively stand for the 1%, 5%, and 10% significance level.

As shown in the regression coefficient of the model, POWER has the correlation coefficient −.01, with testing value T −3.37 and p < .01. Furthermore, SFR coefficient is −.07, with testing value T −22.19 and p < .01. Therefore, both SFR and POWER are significantly positive correlated with ROA at the 1% significance level. That is to say, deeper founder control decreases corporate equity financing. In turn, worse corporate performance will happen to a company. Founders, therefore, would make use of own control rights in combination with equities to choose debt financing while lessening equity financing. For the corporate performance is exacerbated by rising costs and risks of financing due to such as financing structure, equity financing imposes an enhanced mediating effect on relevance between founder control and corporate performance. In other words, Hypothesis 4 in this paper is proved.

To further analyze its mediating effect, equity financing is divided into two groups for regression: large percentage and small percentage. Based on the comparison and analysis of regression results in the table, it is detected that for those companies with large percentages of equity financing, there is no significant correlation between founder control (POWER) and corporate performance after SFR is added. In other word, equity financing has the full mediating effect on founder control and corporate performance, that is, founders with bigger rights would control financing structure to maximize own benefits. For companies with a great deal of equity financing, the negative effect of founder control on corporate performance will be fully controlled by equity financing. Those companies with small percentages of equity financing are facing the partial mediating effect.

Further Research and Robustness Test

Further Analysis

Analysis of moderating effect of state-owned enterprises and non-state-owned enterprises

The samples are divided into two groups—state-owned enterprises and non-stated-owned enterprise which, then, are substituted into Model 3 for regression to verify the moderating effect of corporate strategies on corporate performance (ROA) and each subitem under founder control (POWER). In the former group, the model gets goodness of fit (R2) 0.18 that is in line with satisfaction. This is to say this model is statistically meaningful. In the group of non-state-owned enterprises, the model gets goodness of fit (R2) 0.17 that is in line with satisfaction. This is to say this model is statistically meaningful.

According to the model regression results shown in Table 7, the group of state-owned enterprises has the correlation coefficient −0.02 for the interaction term POWER*MARK, with testing value T −0.39. In other word, there is no significantly positive relevance between ROA and the interaction term POWER*MARK.

Respective Moderating Effect of State-Owned Enterprises and Non-State-Owned Enterprises.

Note. T Value is parenthesized.

, **, and * respectively stand for the 1%, 5%, and 10% significance level.

In the other group, its interaction term has correlation coefficient 0.01, with testing value T 2.59 and p < .05. In other word, there is the significantly positive relevance between ROA and the interaction term POWER*MARK at the 5% confidence level.

Judging from the above-mentioned results, corporate strategies of state-owned enterprises doesn’t impose the significant moderating effect on founder control and corporate performance, while for non-state-owned enterprises, corporate radical strategies could suppress the negative effect of founder control on corporate performance. That is to say, those non-state-owned enterprise with radical strategies could, to some extent, hold up the negative effect of founder control on corporate performance; in other words, there is a negative moderating effect of corporate strategies on the relevance between founder control and corporate performance. For a non-state-owned company, that is to say, deeper founder control is followed by worse corporate performance. However, radical corporate strategies could abate negative effects of founder control on corporate performance: a more radical corporate strategy will generate more favorable corporate performance.

Analysis of mediating effect of state-owned enterprises and non-state-owned enterprises

The samples are divided into two groups—state-owned enterprises and non-stated-owned enterprise which, then, are substituted into Model 4 for regression to verify the mediating effect of equity financing (SFR) on corporate performance (ROA) and each subitem under founder control (POWER). In the former group, the model gets goodness of fit (R2) 0.22, that is, in line with satisfaction. This is to say this model is statistically meaningful. In the group of non-state-owned enterprises, the model gets goodness of fit (R2) 0.18, that is, in line with satisfaction. This is to say this model is statistically meaningful.

According to the model regression results shown in Table 8, the group of state-owned enterprises has the POWER correlation coefficient −0.03, with testing value T −2.18 and p < .05. In other word, there is the significantly negative correlation between ROA and POWER at the 5% confidence level. The SFR correlation coefficient −.07, with testing value T −12.51 and p < .01. In other word, there is the significantly negative correlation between ROA and SFR at the 1% confidence level.

Respective Mediating Effect of State-Owned Enterprises and Non-State-Owned Enterprises.

Note. T Value is parenthesized.

, **, and * respectively stand for the 1%, 5%, and 10% significance level.

In the other group, its POWER correlation coefficient is −0.01, with testing value T −2.88 and p < .01. In other word, there is the significantly negative correlation between ROA and POWER at the 1% confidence level. The SFR correlation coefficient is −0.08, with testing value T −17.53 and p < 0.01. In other word, there is the significantly negative correlation between ROA and SFR at the 1% confidence level.

As implied in the results above, no difference is detected between state-owned enterprises and non-state-owned enterprises in terms of the mediating effect of equity financing on founder control and corporate performance. The founder of a company with control rights in hand would decrease corporate equity financing. Accordingly, the company will witness its shrinking performance caused by higher costs and risks of financing arising from such a financing way.

Robustness Test

In this paper, the way to measure uppermost variables is substituted to verify robustness of the research conclusion: ROA is replaced by ROE for the explained variable in this paper—corporate performance. The way that is most broadly adopted is used to measure the explanatory variable-founder control. It is to assess the control right with reference to the statement in the annual report whether or not the founder of a company is also the president or the general manager of this company: if the founder also acts as the president or the general manager, POWER* = 1, and otherwise, POWER* = 0.

According to robustness test results of 4 hypotheses shown in Table 9, founder control is negatively correlated with equity financing that has the negative correlation with corporate performance, while radical strategies would suppress the negative effect of founder control on corporate performance. Equity financing imposes a mediating effect on relevance between founder control and corporate performance. Robustness tests match with the four hypotheses in this paper.

Robustness Regression.

Note. T Value is parenthesized.

, **, and * respectively stand for the 1%, 5%, and 10% significance level.

Discussion and Conclusion

Research Results

This paper analyzes the correlation between founder control, equity financing, corporate radical strategy and corporate performance by selecting 2010–2019 listed companies in China as the research sample. Based on literature review and theoretical analysis, four main hypotheses are put forward in this paper. After descriptive statistical analysis, correlation statistical analysis, and empirical model testing of sample data, the following research conclusions are obtained.

First, there is a negative correlation between founder control and equity financing. Second, there is a negative correlation between equity financing and corporate performance. Third, a corporate radical strategy has a negative moderating effect on the relevance between founder control and corporate performance. Fourth, equity financing has an enhanced mediating effect on the relevance between founder control and corporate performance. Fifth, the degree of corporate strategy of non-state-owned enterprises has a negative moderating effect on the correlation between founder control and corporate performance.

Research contribution: This paper is the first-time study that investigates the relevance amongth founder control, equity financing, radical corporate strategies, and corporate performace. In turn, the corporate governance theory is enriched. In previous studies concerning these issues, both mediating effects of equity financing and moderating effects of radical corporate strategies have never been taken into consideration. This papers analyzes effects of equity financing upon corporate performance under different strategies, as it builds S-C-P chain effect mechanism (namely, founder control-coporate strategy-corporate performance) while holistically taking into account the effects of corporate strategies and their role as a moderator upon corporate performance. Furthermore, it proposes S-C-P chain effect mechanism (namely, founder control-equity financing-corporate performance), while holistically taking into account the effects of equity financing and its role as a mediator upon corporate performance. Accordingly, the theory of relevance between financing structure and corporate performance of a listed company is, to some extent, enriched and improved.

Research Recommendations

The following recommendations are provided in this paper on the basis of the research conclusions above.

First, according to the different stages of enterprise development, the control rights of company founders are suggested to be reasonably restricted. It is found in this research that bigger founder control imposes more negative effects on corporate performance. For the purpose of the corporate sustainable development in a long run, the founder of a company could abdicate business control rights to seek for professional managerial staff, or could effectively supervise the chief executive offer via the board of directors, with a view to boosting the corporate development.

Second, focus on long-term benefits and adopt strategic changes at the right time. In this research, it is elicited that a corporate radical strategy is positively correlated with corporate performance, and what’s more, the degree of such a strategy could weaken the negative effect of founder control on corporate performance. As for a company, the key to its continuous growth and unceasing acquisition of competitive advantages in the furious market competition is its adamant implementation of strategic reformation. That is to say more radical corporate strategies will instill more courage into a company to take risks and make innovation. With innovative products, in turn, a company would be enabled to quickly take up biggest market shares. Furthermore, a company with radical strategies is driven by the market to create values for customers and elevate corporate competitiveness for positive effects on corporate performance.

From the perspective of financing, moreover, the study reliability will, to some extent, be discounted if only equity financing is discussed without attention paid to debt financing, for the reason that as constituents of corporate financing, debt financing and equity financing are supposed to present more negative correlation. Asset = debt + shareholder equity. When assets remain the same, there will be a fully negative correlation between debt and shareholder equity. Therefore, the following studies are required to further analyze the relevance between debt financing and such effects as the effect of equity financing on corporate performance and the one of founder control on preferences of equity financing.

Further Discussion

Research on the correlation between founder control and equity financing

Based on a review of previous literature, Xu et al. (2018) argue that there is a clear preference for equity financing among Chinese listed companies, which is manifested by an extremely strong urge to seek an initial public offering of shares before IPO, and preference in choosing equity financing methods after IPO such as share placement or additional issue in the choice of refinancing methods. However, Erb (2020) use the embedded payoff rate calculated by using the discounted residual income model as the cost of equity financing for listed companies and compare it with the cost of debt financing taking into account the tax shield effect, arguing against the conclusion that the cost of equity financing is low and thus equity financing is preferred. Motoyama and Hui (2015) analyze 3,268 private SMEs in China and shared through a questionnaire that about 72% of business owners do not want to obtain funds through equity financing and that the share of founders tends to increase over time relative to other investors. Huang and Ritter (2009) extend the LLSV model by introducing equity financing decisions and conducted a regression analysis of the size of 1,118 public new issues of 1,803 A-share listed companies in China from 2007 to 2013. It adopts the Tobit model with restricted dependent variables, and found that the equity financing needs of listed companies show a separation phenomenon: investment-based financing is implemented when the returns are high, and captive financing is implemented when the returns are low. Based on the inconsistency between founder control and equity financing preferences, the current study questions the relationship between founder control and equity financing. The empirical analysis of this study by constructing a random effects model finds that equity financing is lower for firms in which the founder still holds control of the firm. This is due to the fact that equity financing causes dilution of ultimate control when the founder is the largest shareholder of the firm, while debt financing does not dilute ultimate control, and therefore founder shareholders will use their information advantage to make it more difficult to raise equity financing for the firm.

Research on the correlation between equity financing and firm performance

Based on a review of previous studies, Wang et al. (2018) construct a model of optimal equity structure based on the perspective of Principal-Agent Theory and Game Theory, which theoretically proved the existence of optimal equity structure. The theoretical analysis is consistent with the empirical evidence: firm value has an inverted “U” shaped relationship with equity concentration, and firm value also has an inverted “U” shaped relationship with the proportion of non-controlling majority shareholders’ equity; firm value has a significant negative relationship with equity checks and balances. Using the data of Chinese A-share listed companies from 2008 to 2012, Avcin and Balcioglu (2017)analyze the impact of corporate equity structure on corporate performance in the main board, small and medium-sized board, and venture capital board sectors. It concludes that the impact of state-owned shareholders on corporate performance was significantly positive in the main board companies; the impact of corporate shares on corporate performance was significantly positive in the small and medium-sized board companies. Beladi et al. (2018) conduct an empirical study on Chinese listed companies in non-ferrous metal sector from 2006 to 2010, and contended that commercial credit financing rate in the financing structure of listed companies in the non-ferrous metals sector, short-term bank credit financing rate, and equity financing rate had a significant negative effect on business performance. The current study aims to investigate the relationship between equity financing and firm performance despite the controversy about the research on the correlation between equity financing and firm performance. Through the empirical analysis of random effects model, this study finds that the higher the equity financing, the worse the firm performance. This is due to the fact that through equity financing, the ownership, control, and income of the enterprise are dispersed, and the business operator is no longer the full owner of the enterprise, which leads to the problem of information asymmetry, and the operator will make decisions that cause losses to the owner’s interests in order to maximize his own interests, that is, the moral hazard in principal-agent. In order to prevent this risk, enterprises must strictly establish a standardized governance system to restrain the behavior of operators, which will not only increase the cost of supervision and operation, but also have a negative impact on their business performance and reduce corporate performance.

Research on the moderating effect of corporate strategy on founder control and firm performance

First, a review of previous research literature reveals that few scholars have analyzed the moderating effect of the degree of aggressiveness of corporate strategy on founder control and firm performance, Wu and Barnes (2010) analyzed the case of Electrical Appliance’s control struggle and found that as founders were reluctant to choose riskier business decisions due to their preference for corporate control, this inevitably led to many missed growth opportunities and affected corporate performance. However, Kergus et al. (2019) explore partner system and the choice of control arrangement model for the entrepreneurial team, and find that an aggressive strategic approach is beneficial to the development of firm performance in the long run. Therefore, the current study decides to examine whether there is a correlation between founder control, the degree of aggressive corporate strategy and corporate performance, and utilized a stepwise regression research method to find that aggressive corporate strategy reduced the adverse effects of founder control on corporate performance to some extent by constructing three random effects models for analysis. The empirical test finds that aggressive strategic choices are beneficial to corporate performance, that is, the degree of aggressiveness of strategy can, to some extent, inhibit the conservative financing approach under founder control, thus reducing the negative impact of founder control on corporate performance.

Research on the mediating effect of equity financing on founder control and firm performance

A review of previous research literature reveals that few scholars have analyzed the mediating effect of equity financing on founder control and firm performance. However, Peng and Jiang (2010) select A-share listed companies as the study subjects to test whether major shareholders received implicit gains from equity refinancing. The study establishes a model to analyze the equity refinancing behavior of listed companies and examines the predatory behavior of large shareholders from three aspects: investment efficiency, resource appropriation by large shareholders, and the value effect of non-fair connected transactions. The study finds that the cause of equity refinancing preference is that large shareholders can obtain hidden benefits that small and medium shareholders cannot get through “tunneling behavior.” Meanwhile, hypothesis 2 of this study has verified that the higher the equity financing, the worse the firm performance. Therefore, this study decides to investigate how founder control, equity financing, and firm performance were related to each other. Through the analysis of Chinese listed companies, it is found that the equity financing of a firm can be considered as an intermediate variable that affects the founder’s control preference on firm performance, indicating that the greater the founder’s control, the less the equity financing of the firm. Furthermore, this financing structure, which increases the cost and risk of corporate financing, will decrease the firm performance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by Social Science Planning Youth Project in Anhui Province of China (No. AHSKQ2021D34).

Ethical Approval

The present study was carried out in accordance with the ethics standards of the institutional and/or national research committee and with the 1964 Helsinki declaration and its later amendments or compare ethics committee