Abstract

The transition to Industry 4.0 presumes the use of innovation potential which is also determined by the institutional environment, including the level of corruption and its perception. The post-communist countries of Central and Eastern Europe are characterized by a higher level of corruption and higher share of the shadow economy, which can fundamentally reduce their innovation potential and thus become the brake on the transition to Industry 4.0. The aim of this paper is thus to evaluate the effects of corruption in public administration on the size and structure of the shadow economy, and to determine whether the existence of corruption may affect the transition of a country and society to Industry 4.0. Based on an extended DSGE (Dynamic Stochastic General Equilibrium) model and using the data for the Czech Republic, the paper finds that corruption in public administration has a much more destructive and long-term effect on the capital accumulation than on the size of the workforce. In that sense, corruption can become a significant obstacle to the transition, underlining that the task of public policies is not only to support digitization, robotization, and further development of technologies, but especially to ensure a transparent non-corrupt environment of public administration.

Introduction

The transition to Industry 4.0, which is perhaps more of an evolutionary process rather than the typical—fourth in a row—industrial revolution, has started to take place in many parts of the world. Indeed, the current COVID-19 pandemic has only intensified the acceleration of this presumably natural development of the Western civilization. The transition to Industry 4.0 has an impact not only on economic foundations but also on society and the institutional environment as a key factor influencing the public policy and administration. However, even 30 years after the collapse of the communist regime in Europe, the new, post-communist members of the European Union still face problems related to the rule of law, which undoubtedly has an adverse effect on the economic changes which take place in these countries. As a result, the functioning of the EU as a whole is disrupted, which translates into recurring problems such as the approval of the Union’s budget.

As shown by Wallace and Latcheva (2006), Johnson et al. (2000), or Avdulaj et al. (2021) from most recent studies, the Central and Eastern European countries in particular are plagued by relatively high levels of corruption in public administration and its negative perceptions associated with hiding output above all. Although corruption comes in many forms and has been immanent in every society since time immemorial, its form, variations, and effects are changing insofar as the requirements imposed on public administration are responding to changes within the society and the economy. The post-communist members of the European Union, which are among the relatively advanced economies of the world, are leading candidates for the transition to Industry 4.0. This fact is magnified not only by the proximity to the most advanced European economy—Germany—and close foreign and trade orientation toward it, but also by the priorities of the European Union and its new budgetary and programing period.

The question is, however, whether the Central European partners of Germany, the country on which Industry 4.0 is based by definition, are prepared not only in economic but institutional terms in particular (see Walheer, 2021; Xu et al., 2018). As indicated by Vysochyna et al. (2020) or Gonzalez-Fernandez (2020), institutional environment, corruption, and shadow economy affect productivity, innovation potential, and technological progress, and thus may limit or even preclude the arrival of the Fourth Industrial Revolution altogether. Accordingly, the aim of this article is two-fold: (1) to evaluate the effects of corruption in public administration on the size and structure of the shadow economy; and (2) to determine whether the existence of corruption can affect the transition of a country and society to Industry 4.0.

Literature Review

This paper models the link between corruption in public administration, taxation, and the shadow economy through the dynamic stochastic general equilibrium model (DSGE model), which is based on microeconomic foundations and allows for all important sectors to be captured as a system. Namely, the DSGE model presented by Orsi et al. (2014), which already includes the shadow economy and taxes, is used. However, the model is significantly modified so as to include the tax rates structurally corresponding to the situation in the Czech Republic. As such, it captures all current types of taxes imposed on economic agents within the standard tax mix such as personal income taxes, corporate income taxes, VAT, excise taxes, and social security contributions. A comprehensive approach to the methodology of tax policy modeling can be found, for example, in Auerbach (2017). Corruption in public administration is then integrated into the model through its effect on each individual component of the effective tax rate. This is similarly described by Born and Pfeifer (2014) who state that corruption may be understood as additional taxation since its increase leads to higher tax rates, which simulates for instance the fact that there is a higher need of tax revenues. The significance of the impact of corruption nevertheless differs according to the particular types of taxes and therefore it is important to capture them separately in the model.

In general, corruption is defined by Transparency International (2021b) as an abuse of entrusted power for private gain. Treisman (2000) defines corruption as the misuse of public office for private gain and summarizes the theoretical approaches to corruption and its causes showing that those include legal system, level of democracy, religion, political stability, or the level of economic development. All these factors given by the theory determine the higher level of corruption in post-communist Central or Eastern European countries as evidenced by Wallace and Latcheva (2006) and others, as mentioned above.

In our study, the relationship between corruption and shadow economy is essential. Buehn and Schneider (2012) claims that from a theoretical point of view, the relationship between corruption and the shadow economy is ambiguous as they can either be substitutes or complements. However, they present empirical evidence for a complementary (positive) relationship of corruption and the shadow economy. Complementarity of the variables is confirmed also by Goel and Saunoris (2014). Although Dreher et al. (2009) present analysis confirming rather substitutional relationship between the variables, in later study Dreher and Schneider (2010) explain and specify that corruption and the shadow economy are complements in countries with low income, but not in high income countries.

In our DSGE model, the shadow economy is a key factor observed. The OECD offers a definition of the shadow economy and other terms associated with it, such as the unobserved or informal economy. Formally, the shadow economy is understood as economic activities (legal and illegal), which should be reported to the tax authority according to the law, but are not, and thus the tax avoidance or tax evasion occurs. According to the OECD, the services sector (B2C services), hospitality and accommodation services, retail, and construction are most often represented in the shadow economy sector. The OECD also points to some trends in the development of the shadow economy in recent years, whereby changes in the use of cash, the emergence of new business models and forms of working hours and contracts, and cross-border activities play a major role. The OECD also offers more or less specific recommendations and strategies for combating the shadow economy, which emphasize in particular the simplicity of the tax system, reducing opportunities for tax evasion and, in general, strengthening social norms in society and the economy.

Schneider and Enste (2003) consider especially illicit work, social security fraud, illegal employment, and economic crime the most typical examples of shadow economy activities. According to Feld and Schneider (2010), the shadow economy, in its narrower definition, represents all production of goods and services (whether legal or illegal) that is not included in official estimates of gross domestic product. In a broader sense, according to these authors, it includes all economic activities and related revenues that the government authority cannot regulate, tax, or observe. In our article, we apply the definition from the concept of Feld and Schneider (2010) or Schneider and Buehn (2018). This definition includes all legal production of goods and services traded on the market, that is, hidden from government authority, whether due to the avoidance of income taxes, value added taxes, any other taxes, social security contributions, or due to efforts to avoid compliance with legal standards on the labor market (minimum wage, maximum number of hours worked, and safety requirements). However, many authors point to the importance of the relationship between the setting up of the tax system and the size of the shadow economy (Blackburn et al., 2012; Giles & Johnson, 2002; Singh et al., 2012; Spiro, 2005).

While examining the issue of the shadow economy, it should be also borne in mind that there is a number of different approaches to it, and especially to its measurement. An overview is offered by Restrepo-Echavarria (2015), Medina and Schneider (2018), or Schneider and Buehn (2018). Enste (2018) presents different approaches to identifying the extent of the shadow economy, and points to their considerable differences. The methods used to estimate the size of the shadow economy include both direct (microeconomic) approaches using questionnaire surveys and indirect (indicator) approaches having the character of macroeconomic approaches. These indirect methods are based on the use of indirect indicators, which are in some way connected with the size of the shadow economy and its development.

As Medina and Schneider (2018) point out, estimates of the size of the shadow economy based on macroeconomic approaches can usually be seen as an upper limit on the size of shadow economies, because they include illegal activities. Relatively newer, and not explicitly mentioned in previous works, is a structural approach based on dynamic stochastic models of general equilibrium. This approach, presented in Orsi et al. (2014), which we use in our model, is also based on the interconnection of observed and unobserved macroeconomic variables. However, in contrast to the MIMIC (multiple indicators, multiple causes) approach, this relationship is parameterized through logical structural relationships based on the optimization behavior of households and companies, or other economic entities.

The previously mentioned work by Schneider and Buehn (2018) presents and discusses a wide range of methods for estimating the size of the shadow economy in 143 countries between 1996 and 2014. Schneider and Enste (2000) and Schneider and Williams (2013) offer in addition to a detailed overview and discussion of existing methods also the results of empirical estimates of the size of the shadow economy. In their study, Feld and Schneider (2010) summarize the conclusions of alternative estimation approaches (direct and indirect) to estimating the size of the shadow economy. This work represents one of the first uses of the MIMIC approach to estimate the size of the shadow economy and evaluate the role of repressive tools for Germany and 21 other OECD countries. The conclusions of the empirical analyses emphasize the significant influence of tax morale. In contrast to other approaches and studies, the importance of tax policy and state regulation (the increase in which leads to the growing importance of the shadow economy) is also shown here. The observed decline in the size of the shadow economy between 1990 and 2005 is not due to the growing importance of repressive instruments, but rather to the general labor market situation associated with declining unemployment due to good economic development.

Buehn and Schneider (2016) estimate time series of the amount of tax evasion (as a share of GDP) for 38 OECD countries in the period from 1999 to 2010. The primary tool of analysis in this case is the MIMIC model, which the authors advocate for earlier in their work on the example of the French economy (Buehn & Schneider, 2008). Indirect taxes and self-employment are identified as the main drivers of tax evasion. Over the period under review, there was a declining trend in the size of the shadow economy, averaging 3.8% of official GDP (with Mexico at high of 6.8% and Turkey at 6.7%, and with the United States at 0.5% and Luxembourg with a value of 1.3%). Medina and Schneider (2018) discuss the extent of the shadow economy for 158 countries between 1991 and 2015. The average size is estimated at 31.9% of GDP, with Zimbabwe 60.6%, Austria 8.9%, and Switzerland 7.2%. The authors mainly use a hybrid approach combining CDA (currency demand approach) and MIMIC model enriched with PMM (predictive mean matching). In contrast to the standard GDP or GDP per capita growth in their model, the authors use the intensity of night lighting as an indicator variable.

Enste (2018) focused on identifying the share of the shadow economy in selected OECD countries in 2003 to 2018. His estimates range from 7.4% of GDP for the United States to 34.2% of GDP for Bulgaria. The main factors influencing the size of the shadow economy are (considering the conclusions of other studies) a high tax burden, high social security contributions, and tax morale. It has also been shown that resources not used in the official economy can be successfully used in the shadow economy to increase the overall supply of goods and services. However, all analyzed studies reported an improvement in the quality of public institutions by the government, which motivates companies not to transfer their activities to the shadow economy, as a common factor suppressing the role of the shadow economy. Repressive measures to reduce the size of the shadow economy are proving costly and ineffective. The specifics for the countries of Central and Eastern Europe are higher costs and administrative burden for entrepreneurs, low probability of tax audits, and higher acceptance of work in the shadow economy. All these elements cause a higher share of the shadow economy in official GDP. According to Enste (2018), the general recommendations are those recommendations including the reform of the social system, the simplification of the tax system, and the emphasis on the overall growth of the official economy.

Through transmission to the tax ratio, corruption also leads to an increase in the shadow economy at the expense of the official economy. Corruption affects the perception of the effective tax rate, and its influences may be understood as “additional taxation.” As Baklouti and Boujelbene (2019) pointed out, the increase of perceived corruption may lead to a higher willingness to enter into economic activities in the underground economy. Reduced tax revenues lead to introducing new or increasing existing taxes. Sanyal et al. (2000) link the increase in the size of the shadow economy with rising effort to enter corruption activities due to changes in social norms. Pappa et al. (2015) highlight the importance of tax evasion and corruption in determining the size of fiscal multipliers by formulating the DSGE model with involuntary unemployment, an informal sector, and public corruption. Corruption affects the size of tax evasion during fiscal consolidation, where increasing tax rates increases the incentives to transfer the production into the shadow sector.

In order for the overview to be complete, it should be noted that there are also studies that clearly show that the extent of the shadow economy determines the capital-labor ratio in the official economy and also affects foreign direct investments inflow as possible source of competitiveness through knowledge, know-how, and technology transfer. Recent studies include in particular Bayar et al. (2020), Bilan et al. (2019), Walheer (2021), Vysochyna et al. (2020), or Gonzalez-Fernandez (2020), as already mentioned above.

To summarize the above, in our empirical analysis below, we assume that the high level of corruption and its perception causes an additional tax burden, which is reflected in a higher extent of the shadow economy, which can be effectively captured in our modified DSGE model (for more, see the details of the model in Němec et al., 2021). On the contrary, the extent of the shadow economy can be eliminated by higher quality of public administration as a key element of the institutional environment of public policy. However, if the institutional environment fails and high levels of corruption persist in public administration, then increasing taxation may shift some of the output from the official to the shadow economy, which also means a shift in labor and capital accumulation, which may change the capital-labor ratio to official part of the economy. This can then be a brake for Industry 4.0.

Results

Quarterly data for the Czech Republic for the period 2002 to 2019 were used to estimate the model. The time series databases from the Czech National Bank (2021), Czech Statistical Office (2021), Ministry of Finance of the Czech Republic (2021), and Transparency International (2021a) were used. A more detailed description of data sources and calibration of structural parameters and steady-state values are available in Němec et al. (2021) who provide the simulated impacts of shocks in a fully calibrated model. They are also listed below as a benchmark in the description of the results.

In this article, we present parameter estimates and resulting simulations based on real data for the Czech Republic, which is not very common in DSGE modeling aimed at shadow economy and corruption. It is the culmination of long-term work on calibrating the model and performing simulations. Although a part of the parameters and steady-state values remain calibrated (see Table 1), the model’s remaining parameters were estimated by using the Metropolis-Hastings algorithm with the use of the Dynare toolbox version 4.6.1 (Adjemian et al., 2021) in the Matlab 2020a environment. Two independent chains, 1,000,000-sample each, were generated, with 80% of the initial samples being eliminated. The resulting characteristics of posterior density were thus calculated based on a total of 400,000 samples of parameters from both chains. The convergence of each chain was verified based on the convergence diagnostics of Brooks and Gelman.

Calibrated Parameters and Steady-States.

Table 2 shows the mean values and standard deviations of the prior densities, which were chosen rather uninformatively as well as the posterior mean values and the highest posterior density intervals (HPDI). Table 3 shows that most of the parameters were identified well from the data. The average acceptance ratio was 18%.

Estimates of Structural Parameters.

Note. G = gamma distribution; B = beta distribution; HPDI = highest posterior density intervals.

Estimates of Autoregressive Parameters.

Note. B = beta distribution; HPDI = highest posterior density intervals.

The posterior estimates of parameters point to a relatively lower share of labor in the shadow economy sectors as compared to the official economy sector. The model’s estimates also made it possible to identify the relative weight of the effect of the corruption perception indicator on individual tax rates. The corporate income tax has the highest influence here, while the lowest influence can be seen in case of the excise taxes and the social security contributions.

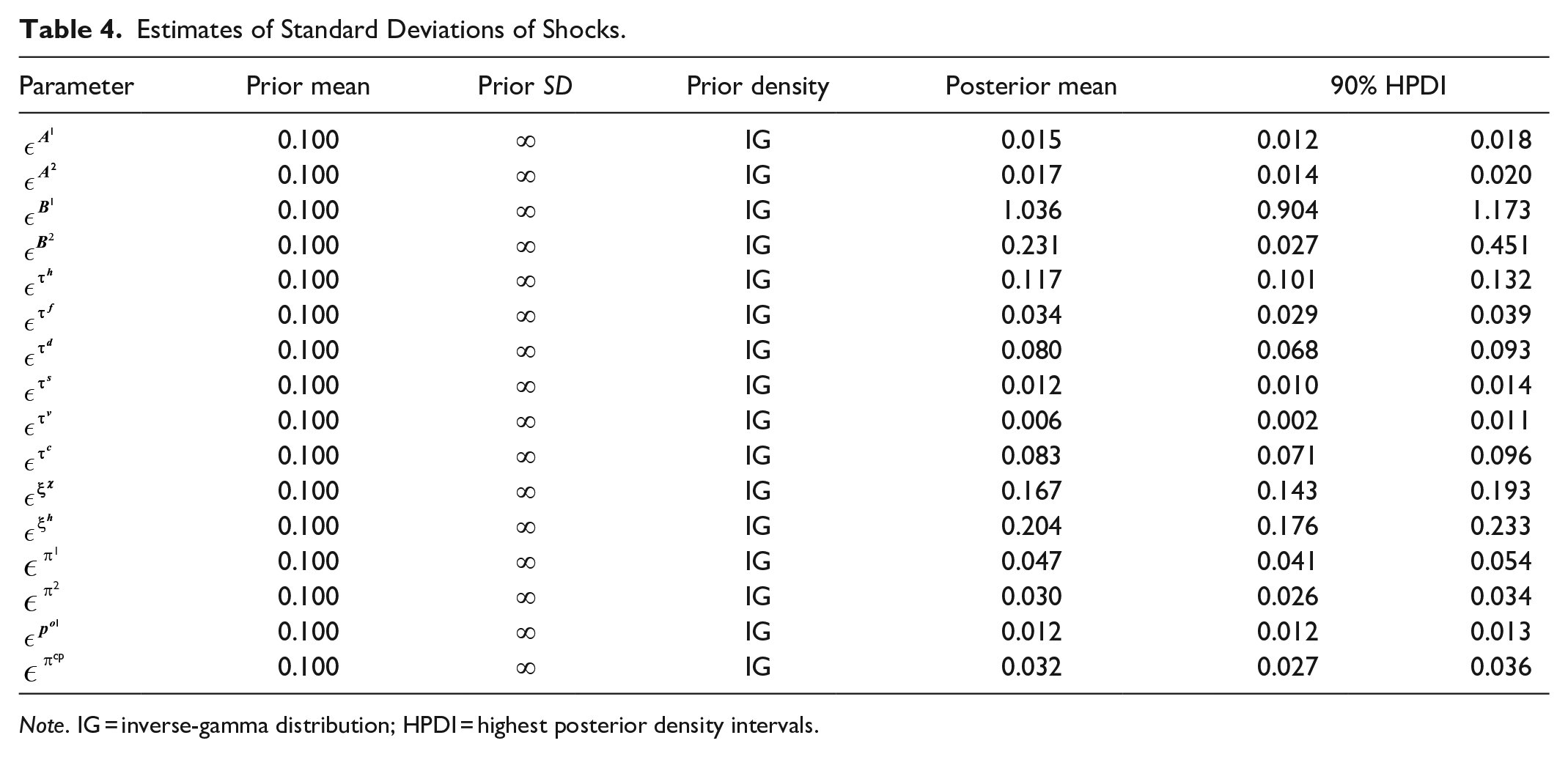

Table 3 shows the relatively high persistence in most exogenous shocks. The only exception is the persistence in corruption perception. Estimates of standard deviations of shocks are contained in Table 4. The high volatility of technology shocks is due to the relatively low shares of steady states of labor and capital in the shadow economy (compared to analogous values of steady states in the official part of the economy), and a large part of production transmission to the shadow economy is then explained in the model as increased productivity of production factors.

Estimates of Standard Deviations of Shocks.

Note. IG = inverse-gamma distribution; HPDI = highest posterior density intervals.

Figure 1 shows the effects of various persistent shocks in corruption on the key characteristics of the shadow economy, which lead to an increase in economic activity in this sector to varying degrees. As a benchmark, also the simulation results from the calibrated model are present.

Effects of shocks in corruption: simulations and real-data estimations.

However, in this paper, we focus on the effects resulting from the estimations performed on the real data for the Czech economy in the period 2002 to 2019. Our simulations are based on the model dynamics (represented by the impulse response functions) evaluated at the mean values of the estimated posterior densities of the parameters. As it is evident from the Figure 1, corruption with no or low persistence has positive effect on labor and capital stock in the shadow economy, which is however almost negligible and fades away slowly. But in case the corruption reaches the level of high persistence, the situation dramatically changes. The workforce declines temporarily in the shadow economy due to the shock of corruption, which is, nevertheless, followed by a rapid increase in several quarters. After less than 2 years, we observe a return to the original level and a further increase in the workforce, which persists in the shadow economy. The situation is similar in the case of the capital stock, where, however, the increase is immediate after the shock of corruption. Even in this case, the growth reaches its peak after less than 2 years and persist in the shadow economy. As for the intensity of these changes, it is clear that they are much more significant in the case of the capital stock, which is reflected in the change in the capital-labor ratio in the shadow economy.

Discussion

The industrial revolution and the transition to Industry 4.0 are leading to a change in the relative ratio of capital and labor. This ratio is increasing, and capital is becoming relatively more significant in the digital and smart economy. Corruption, according to the performed analyses and simulations, leads to a transfer of activities to the shadow economy. This applies to both capital and labor. The development of these variables, however, is different not only when analyzing the intensity of the changes, but primarily when analyzing the temporal aspect of their changes.

First, it is necessary to discuss the situation in which the impact of corruption on the size of the workforce is modeled. If there is a very low persistence of corruption that is not reflected in future periods, that is, in a situation in which corruption and its perception is not a systemic phenomenon and is either a random phenomenon or a case in which its negative perception or historical memory of society is very short, then corruption has a positive effect on the size of the workforce in the shadow economy. Such type of corrupt practices will lead to a slight increase in the workforce activities, which will immediately begin to fade slowly away.

The situation is different if the effects of corruption are examined on the size of capital accumulation in the shadow economy. Capital accumulation in the shadow economy also grows and, similarly to the workforce, this increase slowly fades away. In terms of the intensity of the capital accumulation increase, however, the increase may be about 10 times higher. Thus, there is a significant increase in the capital-labor ratio in the shadow economy, which may be interpreted as a drastic, relative transfer of capital resources from the official to the shadow economy. If the transition to Industry 4.0 is understood in a simplified form as an increase in the capital-labor ratio, corruption then has a negative effect, and the transition to Industry 4.0 in the official economy slows down as the sources of economic growth in the official economy shift to the shadow economy.

In the event that corruption reaches such an intensity that private interests significantly influence the government’s decision-making processes and corruption becomes systemic, we speak of the so-called state capture. Although this phenomenon is predominantly used in some developing economies, it is still significantly present in relative comparisons within the European Union, especially in certain post-communist countries. Reference is made to Bulgaria, Hungary, or Poland in connection with the Government of the “Law and Justice” party. Given the current tense situation, which also led to the fall of the previous government and significant problems at the level of justice components and police forces, a high level of corruption approaching the phenomenon of state capture is present in Slovakia as well. In the analysis of Czech Republic, in our opinion, systemic political corruption does not reach the same intensity as in the above-mentioned countries, though with regard to the conflicts of interest of the Prime Minister and other representatives of political power, it might be hidden and even more perilous.

In all these cases, there is already a certain persistence and inertia in corrupt practices, which become immanent. The situation of the so-called low persistence cannot be described as state capture yet, though it is modeled herein that the subsiding of corruption is slower, and its perception decreases approximately by 50% each period. In the Czech Republic, a typical case is that of Vladimír Kremlík, former Minister of Transport (overpriced contract for electronic vignettes). He resigned at the beginning of 2020 and now (after about 1 year) the said corruption case is less present in terms of corruption perception.

In the case of a low persistence of corruption, workforce growth in the shadow economy is about 20% higher than in the case of zero persistence. The growth of capital accumulation in the shadow economy is then higher by about 25%. The impact on the overall capital-labor ratio in the shadow economy is therefore more pronounced than if corruption was a random, non-inertial phenomenon. The arrival of Industry 4.0 then slows down even more.

The most interesting appears to be the situation of the so-called state capture, which certain post-communist members of the European Union may already be approaching. In the case of such high persistence of corruption, the transfer of labor and capital resources to the shadow economy is very drastic. After an initial decline in labor activities, which subsides very quickly and which may be attributed to the temporary incentive effect to replace lost tax revenues or effectively unrealized expenditures, there is a significant increase in labor activities in the shadow economy. In quantitative terms, the peak of these activities is almost threefold than in the case of zero persistence. The increase in capital accumulation in the shadow economy develops in a similar way, which is even 4.5 times higher compared to the same situation with zero persistence of corruption. The overall increase in the capital-labor ratio in the shadow economy is very significant, which further reduces the resources available in the official economy and exacerbates the negative effects on Industry 4.0.

From the above, it is beyond doubt that corruption approaching state capture leads to a massive increase in the capital-labor ratio in the shadow economy. This relationship is in accordance with Sanyal et al. (2000), Pappa et al. (2015), or Baklouti and Boujelbene (2019). Our approach emphasizes the impact of corruption on increase in the shadow economy at the expense of the official economy through transmission to the tax ratio. Corruption affects the perception of the effective tax rate, and its influences may be understood as “additional taxation. Dreher and Schneider (2010) pointed out that the relationship between corruption and the shadow economy depends on the income of the country. They conclude that in high-income countries, the shadow economy reduces corruption and in low-income countries, the shadow economy increases corruption. Our conclusion about the positive relationship between corruption and the shadow economy may thus result from the fact that we are concerned with the opposite causal effects, that is, the effect of corruption on the shadow economy. Given that the shadow economy, by its very nature, limits the introduction of cutting-edge technologies and can be based more on unskilled labor, this fact also acts as significant deceleration in relation to Industry 4.0.

Conclusion

The Fourth Industrial Revolution is becoming reality. The transition to smart factories and the replacement of unskilled labor leads to significant socio-economic changes. Structural changes in the world economy are being made, and the wage competitive advantage of some countries are being eliminated. The return of factories to developed countries will accelerate. There are also changes in the structure of national economies, not only on the matter of individual sectors but also on the proportions of the official and the shadow economies. The institutional environment, whose propensity to engage in corrupt practices in public administration being an important part, may then significantly determine the ability to take on the challenges of the transition to Industry 4.0. Corruption has been shown to have a different effect on two key factors of production, the ratio of which determines the progress in the transition to Industry 4.0. Corruption in public administration has a much more destructive and long-term effect on capital accumulation than on the size of the workforce. A corrupt environment that becomes more systemic and immanent and that approaches the so-called state capture significantly increases the capital-labor ratio in the shadow economy and slows down the transition to Industry 4.0. Corruption may thus become one of the possible obstacles to the industrial revolution, and if it became so systemic to be high persistent, its influence would have devastating effects.

In the transition to Industry 4.0, the task for public policies is therefore not only to support digitization, robotization, and further development of technologies through various types of subsidy instruments and incentives, but especially to ensure a transparent non-corruption environment of public administration, which will reduce the size of the shadow economy and increase the capital-labor ratio in the official economy.

In further research, it would be interesting to focus on potential changes in the tax mix, which will necessarily have to undergo significant changes in the future in connection with Industry 4.0. It will be necessary to introduce new types of taxes, such as the robot tax or the digital tax, which will replace shortfalls in the collection of taxes on labor. Furthermore, it is possible to consider that if corruption in public administration is perceived as additional taxation, which can lead to poorer tax morale and lower efficiency of tax collection, the scope for introducing new taxes is very limited, not only from economic but also from for political reasons. And all this is further aggravated in a situation where part of production is moving to the shadow economy, which further complicates tax collection. All this can be a challenge for the public policy of the future as well as future research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the European Association Comenius within the project EACO/RP08/2016, and by funding for specific research at the Masaryk University, Faculty of Economics and Administration, project MUNI/A/1451/2020.