Abstract

Empirical evidence, regarding the impacts of female leadership on firm’s corrupt level, is lack of studies in various research context. The objective of this study is to assess whether female managers impact negatively or positively on the corrupt behavior of family SMEs (household business) and nonfamily SMEs (Small and Medium-sized Enterprises). To do that, this paper used regressions, taken from a sample of 1,720 Vietnamese SMEs (based on the survey data of UNU-WIDER), to compare the impact of female percentage in management board in family and nonfamily businesses in reducing the level of corruption of the firms for the period 2011 to 2015.The findings indicated that first, drawing on socioemotional wealth theory and Vietnam context, family SMEs (household businesses) are more likely to engage in corruption. Second, we also found that female participant in management team can promote firms to be less involved in unethical practices such as bribe. However, the positive role of female managers in reducing corruption engagement is moderated by family control. We used upper echelon theory to suggest that female managers tend to have less managerial discretion in family-controlled organizations. This study has practical contributions, especially for policymakers and owners of household businesses.

Introduction

This study examines the relationship between female manager and corruption in SMEs (Small and Medium-sized Enterprises), and whether the role of female leadership in reducing levels of corruption can be different between family SMEs-household business and nonfamily SMEs. In the literature, family business can be defined as organizations that founding or controlling individual or families play an essential role in firms’ activities (Chua et al., 2011). To test our research questions, we concentrate on SMEs and household businesses in Vietnam. Household businesses are defined in Vietnamese legislation (Decree 43/2010/NĐ-CP) as a form of privately owned small business, with an individual who can stand up to be the owner or a family consisting of members who are Vietnamese citizens, being full 18 years old, full of have the capacity and satisfy the requirements of civil acts. Thus, household businesses can be recognized as micro-small family businesses (family SMEs) according to the definition in the study of Lussier and Sonfield (2015) because they are owned and managed by an individual or a family, and employing a small number of workers. With the usual number of employees less than 10 people, household businesses trades goods that do not require too much technology such as grocery store, food store, making salt, doing business in street vendors, and snacking. In the situation of an emerging country like Vietnam, the number of SMEs in 2018 was about 600,000 businesses, accounting for 97.6% of all firms, which contributed to approximately 50% of total employment and 40% of GDP (Phan & Archer, 2020). In SMEs, household businesses accounted for a large proportion, which contributed to approximately 80% of jobs and 31.2% of the GDP of the Delta areas in 2011 (Giang et al., 2016).

In recent year, because of the growing presence of women in top management team (TMT), many studies have focused on the question whether the representation of women in TMT increases or reduces corruption. Previous studies argued that female participant in leadership positions is associated negatively with the level of corruption in firms (Breen et al., 2017; Ponomariov & Kisunko, 2018; Trentini & Malinka, 2017). This is because women have higher ethical standards (Swamy et al., 2001), more trustworthy (Dollar et al., 2001), fewer opportunities to commit corruption (Trentini & Malinka, 2017), and more risk-adverse than men (Buchan et al., 2008; Croson & Gneezy, 2009), and therefore negatively impacts the corruption degrees in businesses.

In order to disentangle the nexus between female representation and the firms’ level of corruption, and illuminating with light on this field, we examine this relationship in SMEs and evaluate whether family business status moderates the linkage between female participant in TMT and firm corruption. Several researchers have suggested that the characteristic of female leadership in family businesses is different in nonfamily firms. Family businesses are highly likely to incorporate women into TMTs, compared to nonfamily firms to preserve the interests of the family’s control (Abdullah, 2014). However, Chadwick and Dawson (2018) argued that the leadership of women in family firms is mitigated due to its limited role and power in the firms, compared to men. They are often considered as “behind-the-scenes” emotional leader (Martinez Jimenez, 2009) and their role is usually underrated and less consideration than men’s work (Martinez Jimenez, 2009; Rodríguez-Ariza et al., 2017). Although an amount of literature identified a significant relationship between female participation and a lower degree of corruption (Breen et al., 2017; Dollar et al., 2001; Jagger & Shively, 2015; Torgler & Valev, 2006), limited studies in this field have investigated whether the nexus between female management and firm’s corruption is adjusted by family business status.

In Vietnam, although this country follows East Asian culture which tends to hold misconceptions about the role of women in society (Pham & Hoang, 2019), in recent years, Vietnamese women are participating more and more in leading and operating enterprises. The report, conducted by the General Statistics Office of Vietnam (GSO), showed that the proportion of female participant in TMT accounts for approximately 23% of all managers in the business field (Tran, 2020), whereas they also contribute up to 71% of SMEs and 23% of household businesses leaders according to the World Bank report in 2014 (Pham & Hoang, 2019). Consequently, the role of female managers in SMEs and household firms in Vietnam is an interesting topic that should be investigated.

To add to the understanding of the orientation of female managers toward corruption in SMEs and household businesses, we adopt the socioemotional wealth theory (SEW) and the upper echelon theory. The SEW perspective is derived from the lack of a theoretical perspective which is idiosyncratic to family-controlled firms. This theory suggests that major strategic decisions and management behavior in family-controlled firms depend on the preservation of “nonfinancial aspects” or “affective endowments” of family members (Berrone et al., 2012). As the preservation of SEW, family firms proactively engage to “legitimate” stakeholders, including officials (Cennamo et al., 2012). Based on SEW theory, previous studies showed that family-controlled firms tend to sustain their reputation and image as well as being less corrupt than their nonfamily counterparts (Berrone et al., 2010; Dawson et al., 2020; Ding et al., 2016). To understand the influence of female leadership on firms’ activities, the upper echelons theory (UET) is used. This theory states that there is a correlation between business’s strategic decisions and managerial background characteristics (Hambrick & Mason, 1984). Gender of managers is one of managers’ observable demographic indicators that should be concerned.

In the context of Vietnam, a transitional economics, informal payment to the government can be considered as a “must-have behavior.” Indeed, Vietnam was ranked quite low at 107 out of 180 countries according to Transparency International’s Corruption Perception Index in 2017. As noted by Rand and Tarp (2012) and Van Vu et al. (2018), 79% of Vietnamese firms usually make informal payment to tax officials. Household businesses, as well as SMEs, face the problem of corruption in Vietnam. About 20% of household businesses that had a relation with tax officials between 2009 and 2010 paid an informal payment according to Transparency Global Corruption Barometer 2010 (Giang et al., 2016). The question is: whether or not small family businesses, operating in a corrupt environment, still perform better corporate reputation or being less corrupt than other SMEs. Thus, our study contributes to the literature by researching on the corrupt behavior of SMEs and household businesses in the situation of a highly corrupt country like Vietnam.

The paper makes empirical and practical contributions to the management literature. Our empirical results confirm the influence of female leadership on SMEs’ corruption level and this relationship is moderated by household businesses. First, because there is a lack of studies on small family firms (Bjuggren et al., 2018), this research provides evidence about Vietnamese household business, a type of small family firm and its relation with the firm’s level of corruption. Second, previous experimental studies suggested that gender-corruption nexus may depend on institutional and cultural contexts (Armantier & Boly, 2011; Frank et al., 2011). While women are less likely to involve in bribery in a strong institutional environment (Boehm, 2015), they are more likely to pay bribes in a weak institutional environment (Wellalage et al., 2020). Thus, this study make some implications to the literature by providing new investigation into the nexus between female leadership and corruption in a highly corrupt and Asian cultural country like Vietnam. Third, while there are several studies examining how female leadership role in family firms’ ethical issues (Chen et al., 2018; Cruz et al., 2019; Rodríguez-Ariza et al., 2017), we extend the literature by researching the relationship between female leadership and corruption in family SMEs. From theoretical perspective, the study adds to SEW by finding that with the negative side of SEW and a good relationship with “legitimate” stakeholder: the officials, family SMEs-household businesses impact negatively on the efficiency of female managers in reducing levels offirms’ corruption. Our finding also adds to the upper echelon theory that family-controlled firm can moderate the nexus between female leadership and firms’ behavior.

Theory and Hypotheses Development

The Socio-Emotional Wealth Theory (SEW) and Corruption in Family SMEs (Household Businesses)

A large and growing body of literature has investigated what is the difference between family firms and their nonfamily counterparts. However, the field has often been in the shortage of a theoretical perspective which is idiosyncratic to family-controlled firms because most early studies used theories borrowed from other fields such as agency theory, stewardship theory, and resource-based view (Prügl, 2019). Furthermore, the controlling family impacts on the strategic decision, governance, and decision making of family businesses (Astrachan, 2003; Chua et al., 1999), which makes them become a unique organizational form Ding et al. (2016).

In response to this difficulty, Gómez-mejía et al. (2007) suggested a new theory—SEW—which states that major strategic decisions and management behavior in family-controlled firms are derived from the protection of “nonfinancial aspects” or “affective endowments” of family members (Berrone et al., 2010). Gomez-mejia et al. (2011) also maintained that the preservation of SEW is prioritized over financial goals which conflicts with those non-economic values. In other words, the loss or gain of SEW is regarded as the most important reference point in family firms’ decision making. SEW approach can be a “theoretical cannon” which explains managerial choices, strategic decision making, corporate governance, the relation with stakeholder, and business ventures (Berrone et al., 2010; Gomez-mejia et al., 2011; Kalm & Gomez-Mejia, 2016). However, scholars argued that SEW has a twofold outlook, referring to its dark side and bright side (Rodríguez-Ariza et al., 2017). Some previous studies found that due to SEW preservation, family businesses tend to be more socially responsible (engagement in CSR activities) than their nonfamily counterparts (Cennamo et al., 2012) but, regarding to the negative side, they also can prioritize family interests to the damage of their stakeholders in order to preserve their SEW (Gedajlovic et al., 2012). To solve this concern, a boarder perspective has been adopted by Berrone et al. (2012) who defined five dimensions of SEW, called FIBER consisting of “Family control and influence,” “Family members’ identification with the firm,” “Binding social ties,” “Emotional attachment,” and “Renewal of family bonds to the firm through dynastic succession.”

In the literature review studies, comparing the ethical values of family businesses to their nonfamily counterparts, previous studies suggest that family businesses admire and prioritize ethical behavior or actions, compared with nonfamily firms. For example, Ding and Wu (2014) addressed the influence of family ownership on one of ethics-related issues: corporate misconduct to find that family businesses have lower possibility to engage in corporate misconduct than nonfamily businesses. Regarding accounting study on family firm, Wang (2006) and Ali et al. (2007) argued that family firms tend to disclose the higher quality of accounting and financial information. In term of CSR (corporate social responsibility) study, family firms tend to pursue and commit CSR activities (Chalkasra et al., 2019; Labelle et al., 2018; Yu et al., 2015). Gils et al. (2014) also pointed out that family businesses pay more attention to social problem and stakeholders than nonfamily firms. Family firms tend not to commit unethical behavior (Chua et al., 1999; Litz, 2008) and generally receive greater ethical values (Anderson & Reeb, 2003; Berrone et al., 2010). There are several reasons to explain. Most previous studies argued that SEW preservation is a key influence of family-controlled firms’ ethical behavior (Ding et al., 2016). SEW protection is the way to preserve family firm’s identity, reputation, long-term growth, and sustainability (Chalkasra et al., 2019; Ding et al., 2016; Labelle et al., 2018; Yu et al., 2015).

Corruption is one of ethical issues attracting the concern of many scholars and studies from different fields and disciplines. According to Bahoo et al. (2020, p. 2), corruption can be defined as “an illegal activity (bribery, fraud, financial crime, abuse, falsification, favoritism, nepotism, manipulation, etc.) conducted through misuse of authority or power by public (government) or private (firms) officeholders for private gain and benefit, financial or otherwise.” There are several reasons to explain why firms engage in corruption. Although this illegal activity allows firms to surpass bureaucratic processes, complex regulations (Lui, 1985) and develop networks or social capital to exceed the challenges of entering a new market (Jong et al., 2012), which promotes growth and achieves higher financial performance (Ashyrov & Akuffo, 2020; Williams & Kedir, 2016), firms may face reduced financial performance because of excessive bribe payment. Moreover, from previous empirical evidence, family firms perform a deeper concern for their image with the public and are not willing to engage in unethical activities (López-Pérez et al., 2018). Gils et al. (2014) also argued that the preservation of longevity and reputation make family firms to be more proactive in improving social issues and connections with their stakeholders than nonfamily counterparts. Household businesses are a type of family SMEs and thus, they maybe not likely to involve in corruption like bribe. .

To sum up, SEW preservation is a key characteristic of family-controlled organizations (Ding et al., 2016). As a result, any potential damage to the firm’s image and reputation is not encouraged in family firms, as it impacts negatively to SEW maintenance. Thus, we suggest the first hypothesis.

H1. Family SMEs (household businesses) are less corrupt than their nonfamily counterparts.

Upper Echelon Theory and Female Leadership

Top-level corporate managers impact on the decision to engage in bribes (Apergis & Apergis, 2017; Collins et al., 2009; Hanousek et al., 2019). Upper-echelon theory argues that the demographic characteristics of CEOs, such as age, gender, and educational level, can explain a firm’s behavior including illegal acts (Hambrick & Mason, 1984). For example, from the review of literature in the relationship between the TMT characteristics and illegal corporate activity, Daboub et al. (1995) suggested that the age, tenure, degree of functional experience, military experience, and homogeneity of TMT can neutralize or enhance the nexus. Troy et al. (2011) found that CEOs who are younger, less functionally experienced and do not hold business degree tend to accept accounting fraud. Sun et al. (2019) argued that younger, male, and lower educated CFOs are more likely to be associated with fraudulent financial reporting.

Drawing on the upper echelon theory, gender is one of managers’ demographic characteristics, which can impact on firms’ decision making (Bonanno & Haworth, 1998). In the male-dominated management team, the representation of women may bring numerous benefits to the firm (Krishnan & Park, 2005). Women have a more relational self-construal than men (Gabriel & Gardner, 1999), creating empathetic style when they take the role of manager in firms (Post, 2015). They are more willing to learn from others’ experiences as their networking strategies (Gersick et al., 2000) and tend to be more collaborative, empowering, and considered of other interest and opinions than male leaders (Eagly et al., 2003; Lauterbach & Weiner, 1996), so they can make higher-quality decisions, solve opportunities, and threats in an effective way. They are also likely to have different personal and professional experience such as marital and parental, comparing to male colleagues (Krishnan & Park, 2005; Post & Byron, 2015), which brings psychological benefits to women and advances their social and management skills (Ruderman et al., 2002).

Many studies have considered the performance of female managers in the ethics-related issue. Most previous studies reported that firms managed by the higher percentage of female directors show a stronger orientation toward ethical issues than companies controlled by a higher percentage of male on board. For example, the research of Williams (2003) indicated that firms, having a higher proportion of women in their TMT, tend to involve in charitable donations to a greater extent than companies with a lower proportion of women on board. In the same vein, referring to CSR related field, studies provided evidence that the number (or proportion) of women directors is positively associated with CSR performance and disclosure (Cook & Glass, 2018; Harjoto et al., 2015; Hyun et al., 2016; Sundarasen et al., 2016; Zou et al., 2018). The representation of women on board can also help mitigate the probability of fraud (Capezio & Mavisakalyan, 2016; Cumming et al., 2015; Lenard et al., 2017).

Consequently, the question is: why female managers perform greater attention to ethical issues, compared with men? The social role theory of leadership suggests that women possess characteristics which relate to pay greater attention to ethical issues (Eagly & Carli, 2007; Eagly & Johannesen-Schmidt, 2001). According to previous psychology research, they have a lower level of overconfidence, higher possibility of risk aversion and conservation than men to maintain their security (Beu et al., 2003; Byrnes et al., 1999; Charness & Gneezy, 2012). Moreover, they are less selfish (Eckel & Grossman, 1998; Swamy et al., 2001), more sensitive about the needs of stakeholders (Bear et al., 2010; Swamy et al., 2001), more likely to comply with the rule, more communally and altruistically (Buchan et al., 2008), less competitive and aggressive (Rosener, 2011), less deceptive (Dreber & Johannesson, 2008), and tend to follow a code of ethics rather than their male counterparts (Ibrahim et al., 2009). Thus, businesses, which are managed by female managers, are less likely to involve in decisions relating to unethical behavior such as securities fraud and tax avoidance for economic goal (Chen et al., 2016; Cumming et al., 2015; Dreber & Johannesson, 2008; Lanis et al., 2015) and more likely to follow more socially responsible decisions (Alonso-almeida et al., 2015). Female directors are also generally more concerned than men with environmental problems and are willing to make decisions to reduce environmental risks (Diamantopoulos et al., 2003; Fukukawa et al., 2007; Liao et al., 2015). Ethical sensitivity and risk aversion of women make them less likely to choose to break securities regulations or to commit fraud (Charness & Gneezy, 2012; Cumming et al., 2015). Furthermore, women behave more ethically when faced with economic constraint (Hietikko, 2016), and are less likely to sacrifice organizational benefit for personal interest than man (Dollar et al., 2001).

Bribery is the ethical issue of any businesses, impacted by the decision of top managers which they treat the issue seriously or not. Studies have shown that in business, female managers are associated with less corruption than their male counterparts in general (Breen et al., 2017; Dollar et al., 2001; Rivas, 2013; Swamy et al., 2001; Trentini & Malinka, 2017). To sum up, from the reasons above, we suggest the hypothesis that

H2: SMEs with more female managers will be less likely to engage in corrupt behavior.

Female Leadership in Family Firms—Household Businesses

First, the difference between family and nonfamily businesses is the existence of family involvement (Chrisman et al., 2005). Because family impacts on firm’s strategy and decision-making process, the power of senior executives maybe diminished (Zahra, 2005). This is because upper echelons theory suggests that managers tend to have less managerial discretion if their organizations do not support them to impact on organizational outcomes (Hambrick & Finkelstein, 1987). In the context of family firms, the family can exercise their control through certain forms of corporate governance and use their power to impact on the decision making process of senior managers (Carney, 2005). Thus, although, in general, the presence of female managers in TMTs may be associated with the lower level of corruption, upper echelon theory suggests that this positive relationship can be subdued in family business context because female leaders are less freedom and powerful under the control of the family. The “decline” can also be seen in other empirical studies. For example, regarding financial performance, Nekhili et al. (2018) provided evidence that the presence of female leaders associate with positive financial outcomes in nonfamily businesses rather than family firms. Similarly, according to the study of Chadwick and Dawson (2018), the positive nexus between female managers, representing in TMT and organization’s financial performance is weaker in family firms than in nonfamily firms. The reason is that, family firms exercise its authority through corporate governance mechanisms, which can reduce the managerial discretion of female leaders and also decrease potential advantages that they can bring to the firm (Montemerlo et al., 2013). Similarly, regarding nonfinancial performance, the study of Rodríguez-Ariza et al. (2017) found that the positive nexus between the existence of women on the board and CSR performance is moderated by family ownership. To be specific, this relationship is much less so in family businesses than in nonfamily businesses.

Second, female members in family firms are usually considered to take the role of “family delegate” to maintain family control (Abdullah, 2014; Martinez Jimenez, 2009), which makes them become more dependent on other family members and align with the preferences of family business in decision-making process (Burke, 1997). Furthermore, their power have less capacity to impact on firm strategies and practices than their male counterparts because it depends on the important level of their role in the family, but they are usually not respected by other family members (Cole, 1997). From the reasons above, we suggest that the advantages that female managers can bring to the firm to enhance ethical responsibility maybe less likely in family firms due to their insignificant role in the family.

Third, in the context of Vietnam the role of Vietnamese women in families and businesses has been enhanced substantially. Gender equality is regarded as one of important social issues that a Communist country like Vietnam to follow the aim goal of the socialist ideals of citizens’ equality (Knodel et al., 2005; Nguyen et al., 2015). According to the report of Vietnam Chamber of Commerce and Industry and World Bank, in 2014, around one-fourth of all businesses are headed by women and about 71% of SMEs have female directors. However, Vietnam is a country which has been strongly impacted by Confucian gender ideologies as other East Asian cultures (Pham & Hoang, 2019), and the role of women is usually overshadowed by man. They are also limited their work at home like doing housework and taking care of their children because of the preconceived notions of gender prejudice from society (Pham & Hoang, 2019). Thus, their role in family SMEs-household businesses maybe not respected.

To sum up, we propose the negative nexus between female appearance in TMT and firm’s corruption level to be moderated by the business type being a family SME-household business or not.

H3: The negative relationship between the percentage of female managers and the level of corruption is weaker in family-owned SMEs than in nonfamily ones.

Data and Methododology

Data Collection

The study data were selected from the database undertaken by the coordination of the Development Economics Research Group (University of Copenhagen), United Nations University, Central Institute for Economic Management (Vietnam), and the Institute of Labour Science and Social Affairs (Vietnam). This database can be used and downloaded from UNU-WIDER. Our sample consists of non-state manufacturing SMEs (below 300 employees) collected in this database, which we followed for a period of 3 years (2011, 2013, and 2015). These firms operate in nine provinces of Vietnam: Hanoi, Phu Tho, Hai Phong, Nghe An, Quang Nam, Khanh Hoa, Lam Dong, Ho Chi Minh, and Long An. The method of data collection bases on a survey question and face to face interview designed to capture information about firm and manager/owner background characteristics. Specifics of sampling methodology can be seen from https://www.wider.unu.edu/database/viet-nam-sme-database. Data covers to important firm’s characteristics such as financial performance, sales, bribes, and manager teams’ characteristics. The study sample is strongly balanced (data were available for all SMEs for the whole research period), with 5,160 firm-year observations (1,720 firms). These firms are from various industries, classified by VSIC code (Vietnam economic sector system; Table 1). Industries that account for a large proportion of the sample are Food production and processing (30.06%), producing products from prefabricated metal (17.64%), and Wood processing and production of products from wood, bamboo (10.56%).

Sample Description.

Regression Model

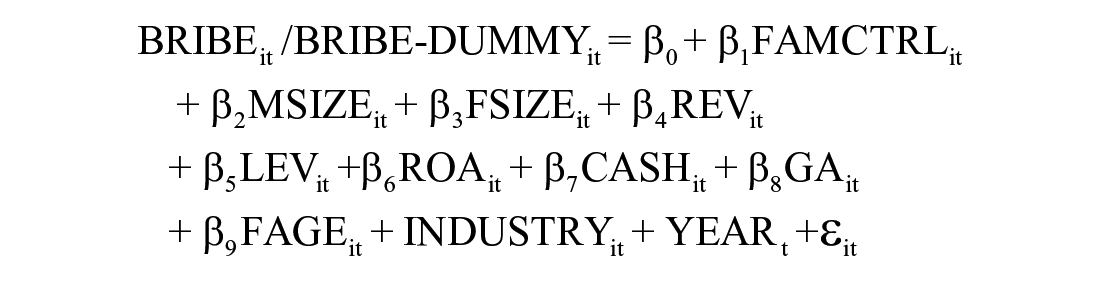

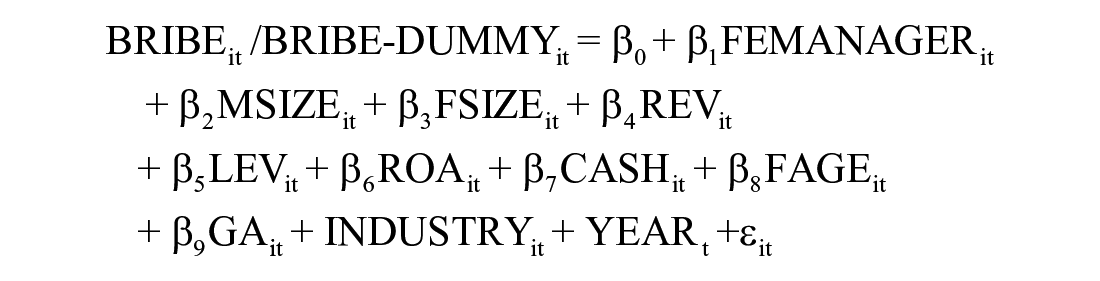

In this research, we use two regression models. The first model tests hypothesis 1 that family SMEs correlate significantly and negatively to the firms’ corruption level. This model applies for all firms in the sample. The second model tests hypothesis 2 and 3 that female leadership will have a negative effect on the level of bribery and the difference between family and nonfamily SMEs. This model applies for family/nonfamily firms.

Model 1 for all firms (test H1):

Model 2 for family and nonfamily firms (test H2 and H3):

Where:

Dependent variables

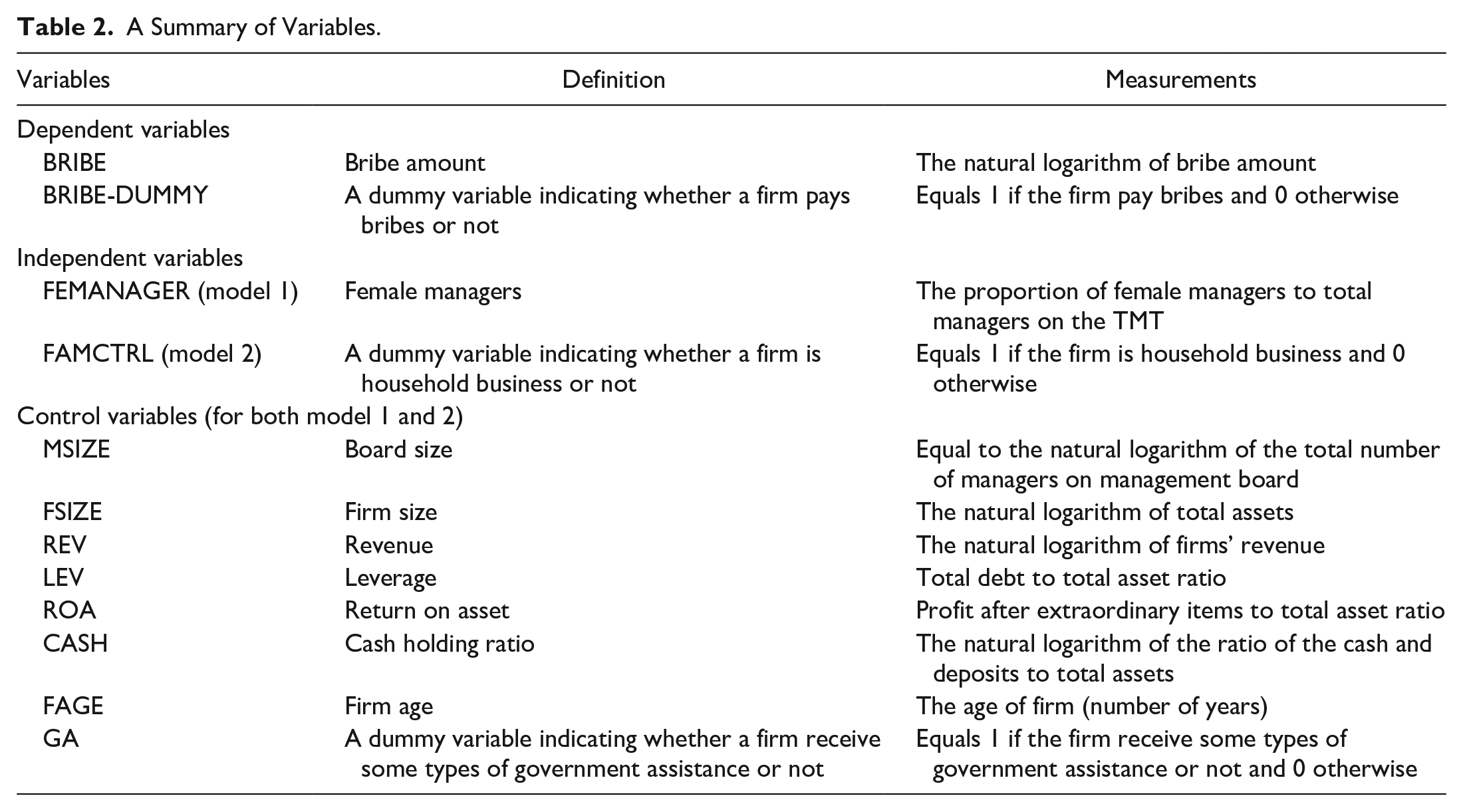

Corruption is difficult to measure because of its various forms (Hietikko, 2016). Most previous studies often consider bribe amount as the underlying phenomenon of corruption. In this study, the information of bribe amount is directly collected by questions in the survey. Because bribe amount varies widely between SMEs, the natural logarithm of bribe amount is used as a dependent variable (BRIBE) in this study. With the case that firms do not bribe, which the value of bribe amount is 0, we assign the value “0” to variable BRIBE (because the natural logarithm of 0 does not exist).

The difference between non-bribing and bribing firm problem is solved in robustness test with dummy variable (BRIBE-DUMMY; Equals 1 if the firm pay bribes and 0 otherwise). Moreover, the minimum value of bribe amount by bribing firm is 98, which means that the natural logarithm value of it is 4.585. This value is still higher than 0 and also guarantee that after changing from bribe amount to its natural logarithm, the value of BRIBE variable of bribing firms is still higher than its value of non-bribing firms.

Both dependent variables BRIBE and BRIBE-DUMMY are used in model 1 and 2.

Independent variables

The percentage of female managers in TMT (FEMANAGER) is measured by the percentage of female managers in TMT. This is the independent variable of model 1

A firm is household business (family SME) or not, presented by FAMCTRL variable. It equals to 1 if the firm is household business and 0 otherwise. This is the independent variable of model 2

Control variables

As reviewed by Phan and Archer (2020), we choose a set of control variables consisting of assets (log.; ASSET) and revenue (log.; REV) in the regression model. Because there is a relationship between corruption and firm financial performance according to the study of Van Vu et al. (2018), we include ROA (return on asset) and leverage as control variables. Thakur and Kannadhasan (2019) found that cash holdings are positively associated to the level of corruption, so we use cash holdings as the natural logarithm of ratio of cash and deposits to total assets. Since corruption relates to informal payment paid by firms to officials, we include a dummy variable: government assistance (GA) to indicate whether a firm receive some sort of government assistance or not. Another control variable is the natural logarithm of the total number of managers in the TMT (MSIZE). The measurement units of this database is 1,000 Vietnam dong. We use the same control variables for both model 1 and 2.

All variables used are shown in Table 2.

A Summary of Variables.

Results

Descriptive Statistics

Table 2 displays descriptive statistics for variables. Our sample has a total of 5,160 observations including 3,440 family SMEs-household businesses, which 66.67% of them is controlled by families, for the period 2011 to 2015. About 41.085% of total observations illustrate that they used to pay bribes, whereas the mean of bribe amount is 3,341.124 (million VND) and the mean of the natural logarithm of bribe amount is 3.2762. Our sample has 66.667% of total firms which are controlled by family. This means that household businesses account for approximately one third of the total number of observations. The percentage of women held a position in management board is on average 38.085%, indicating that the number of male managers surpasses their counterparts in most SMEs. The logarithm of total management team members is 0.3917, while the logarithm of total assets reaches 20.64098. In term of revenue variable, the mean is at 13.9192, and the range is from 8.5172 to 22.8357. The average value of LEV is 0.0802, with a standard deviation of 0.1984. The mean of variable ROA is 0.2927, whereas the average CASH has a range from −15.3872 to −6.9518 in logs. Firm age (FAGE) ranges from 2 to 61 years with the mean is 16.0689 year. The mean of the dummy variable (GA) is 0.1143, which demonstrates that 11.434% of total firm—year observations used to receive some types of government assistance (Table 3).

Descriptive Statistics for Variables of All Firms.

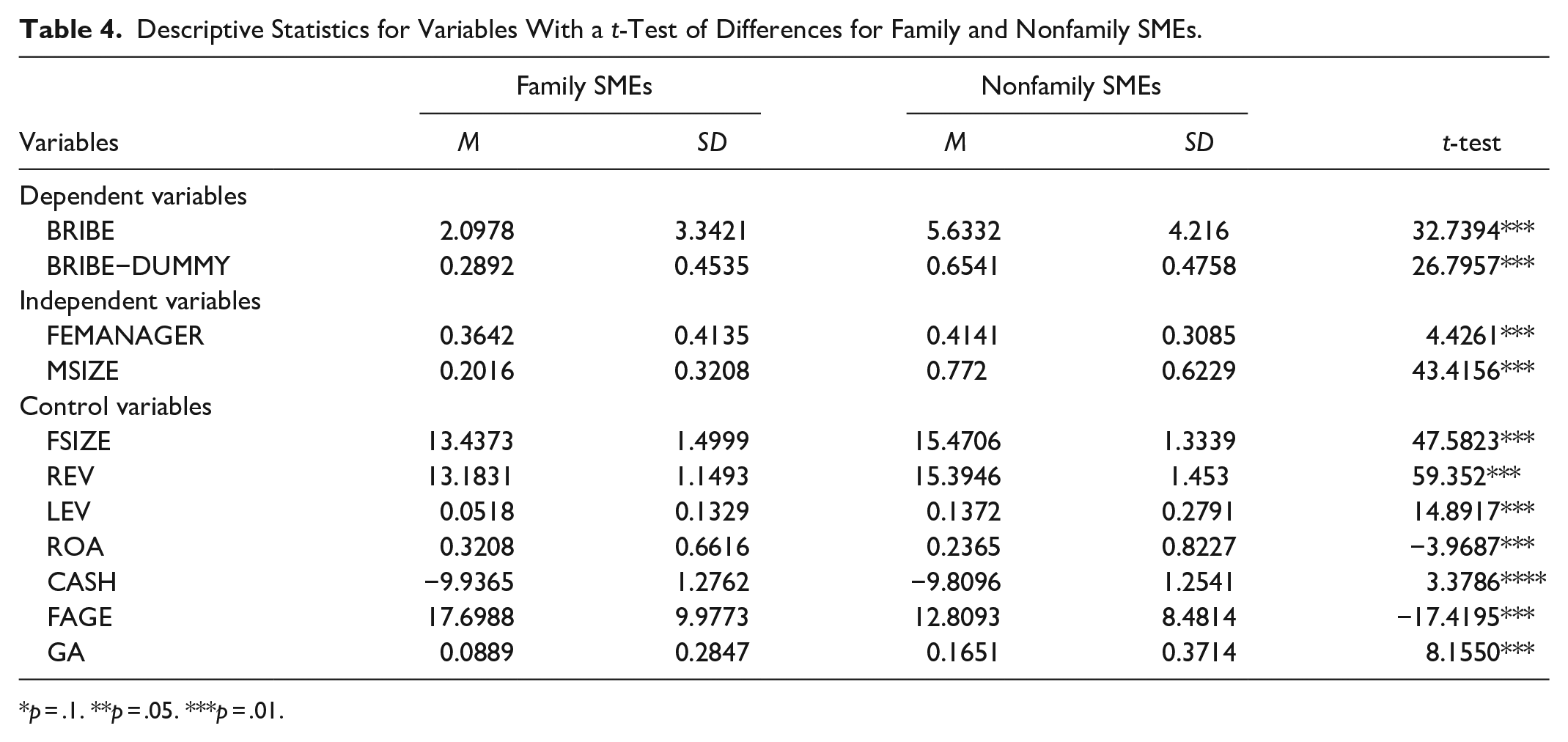

Table 4 presents a comparison of family SMEs and nonfamily SMEs and shows that there are significant differences between them in terms of variables. For example, nonfamily SMEs are more likely than family SMEs to bribe (65.41% compared with 28.92%). Female involvement in management is higher in nonfamily SMEs (41.41% compared with 36.42%). On average, the natural logarithm of the TMT size is larger in nonfamily SMEs than family SMEs. The return on asset (ROA) is higher in family SMEs than nonfamily SMEs (0.3208 and 0.2365). Family SMEs also show a higher firm age than nonfamily SMEs (17.6988 and 12.8093).

Descriptive Statistics for Variables With a t-Test of Differences for Family and Nonfamily SMEs.

p = .1. **p = .05. ***p = .01.

In this part, we present correlations between explanatory variables. Table 5 shows the correlation matrix and multicollinearity for our key variables in the sample of family SMEs. The VIF of all explanatory variable is below 5, which indicates the absence of multicollinearity in our regression models (Isidro & Sobral, 2015). Similarly, Table 6 shows the correlation matrix and multicollinearity for our explanatory variables in the sample of nonfamily SMEs. The problem of multicollinearity is absent because the VIF of all explanatory variable is below 5.

Correlation Matrix: Family SMEs.

p = .1. **p = .05. ***p = .01.

Correlation Matrix: Nonfamily SMEs.

p = .1. **p = .05. ***p = .01.

Estimation Methods

To estimate the regression models, ordinary least squares (OLS), random effects (RE), and fixed effects (FE) model were conducted in this study. In term of the first model for all firms. To test whether heteroscedasticity and serial correlation problem exist in the model, the Breusch–Pagan/Cook–Weisberg test and Wooldridge test (Wooldridge, 2002) were used (Tables 4 and 5). The statistical results of two tests indicated that the data have the heteroscedasticity problem (Ho is rejected at p < .01) and autocorrelation (Ho is rejected at p < .01). Similarly, in term of the second model for family and nonfamily firms, tests indicated that FE model should be chosen instead of RE and OLS model. The statistical results of Breusch–Pagan/Cook–Weisberg test and Wooldridge test show the problem of heteroscedasticity (family firms) and autocorrelation (nonfamily firms). Thus, the FE model applied the robust standard error to address the problem of heteroscedasticity and serial correlation (Tables 7 and 8).

Heteroscedasticity Statistics.

Test Result for Autocorrelation.

Regarding the result from Table 9, in term of FAMCTRL variable, the result shows that the coefficient on this variable is negative and insignificant (coef = −.2609, p > .1), proving that family SMEs—household businesses are not less likely to commit corruption. Thus, the first hypothesis is rejected. From Table 10, the regression results show that the participant of female managers in the TMT correlated positively and insignificantly with corruption level (coef = .1329, p > .1) in family SMEs. By contrast, from Table 11, the percentage of female managers on management board (FEMANAGER) in nonfamily SMEs is significantly and negatively associated to the degree of corruption (p < .01), which supports for our second hypothesis. This finding supports that hypothesis 2: “SMEs with more female managers will be less likely to engage in corrupt behavior” is only proven to be true in nonfamily SMEs and not in family SMEs. Thus, the results also support H3: “The negative relationship between female manager and the degree of corruption is much less so in family businesses.” In other words, the negative relationship between female managers and degree of corruption in SMEs is only proven to be true in nonfamily SMEs. In family SMEs, this relationship is insignificant.

Regression Results (Model 1 for All Firms).

Note. Standard error is presented in parentheses.

p = .1. **p = .05. ***p = .01.

Regression Results (Model 2 for Family SMEs).

Note. Standard error is showed in parentheses.

p = .1. **p = .05. ***p = .01.

Regression Results (Model 2 for Nonfamily SMEs).

Note. Standard error is showed in parentheses.

p = .1. **p = .05. ***p = .01.

Endogeneity Concerns

According to Wintoki et al. (2012), board characteristics can be endogenous variables because they are chosen by firms to adapt to their operations and business environment, which implies causality. Causal phenomena can be explained by two ways—meaning either that TMT characteristics leads to lower possibility of engaging to bribery, or these low—bribery engaging likelihood firms are more likely to choose a more female manager board. To address the potential endogeneity of the variables TMT gender diversity and the likelihood of engaging in bribery, two-stage least-square (2SLS) estimation was applied in the model of nonfamily firms. It also checks the robustness of the supporting result for hypothesis 2.

Endogeneous test is shown in Table 12. As performed in this table, because the result of the Hausman test of endogeneity is insignificant (p = .0234 < .05), which indicates that the null hypothesis: the percentage of women on management board is exogenous explanatory variable is not rejected. This result indicated that FEMANAGER is an exogenous variable and does not have causal effect with dependent variable BRIBE in the sample of nonfamily firms. It can be explained that the higher or lower degree of bribe amount is not likely lead to an increasing or decreasing of employing female managers or vice versa. In reality, for SMEs, these companies are concerned with more important issues such as financial outcome. Thus, bribe may not be an issue for them to consider when considering changes in TMT.

Endogeneity Test.

Robustness of Results

Additional robustness check has been conducted by taking variable BRIBE-DUMMY as a dummy dependent variable to assess the reliability of the research. Due to the logarithm of bribe amount chosen as a dependent variable and evidence in previous research (Phan & Archer, 2020), a logistic model is used for the robustness check. This robustness test fulfill the problem of natural logarithm with firms that do not bribe by doing logistic regression with dependent variable (bribe or not). The BRIBE-DUMMY variable equals to 1 if the firm pay bribes; otherwise, the variable equals to 0. The logistic regression analysis has been conducted, using clustered standard errors. Regarding H2 and H3, the results support the results of regressions reported in Tables 10 and 11. In term of H1, the result is different with the finding in Table 9, which supports for this hypothesis instead of rejecting. We will explain this contrary finding in the discussion part. Overall, the results in Tables 13 to 15 support or partly support our hypothesis 3 and 12. The summarize of findings is shown in Table 16.

Regression Results With BRIBE-DUMMY Dependent Variable (Model 1 for All Firms).

Note. Standard error is performed in parentheses.

.01 Sig. **.05 Sig. *.1 Sig.

Regression Results With BRIBE-DUMMY Dependent Variable (Model 2 for Family SMEs).

Note. Standard error is showed in parentheses.

p = .1. **p = .05. ***p = .01.

Regression Results With BRIBE-DUMMY Dependent Variable (Model 2 for Nonfamily SMEs).

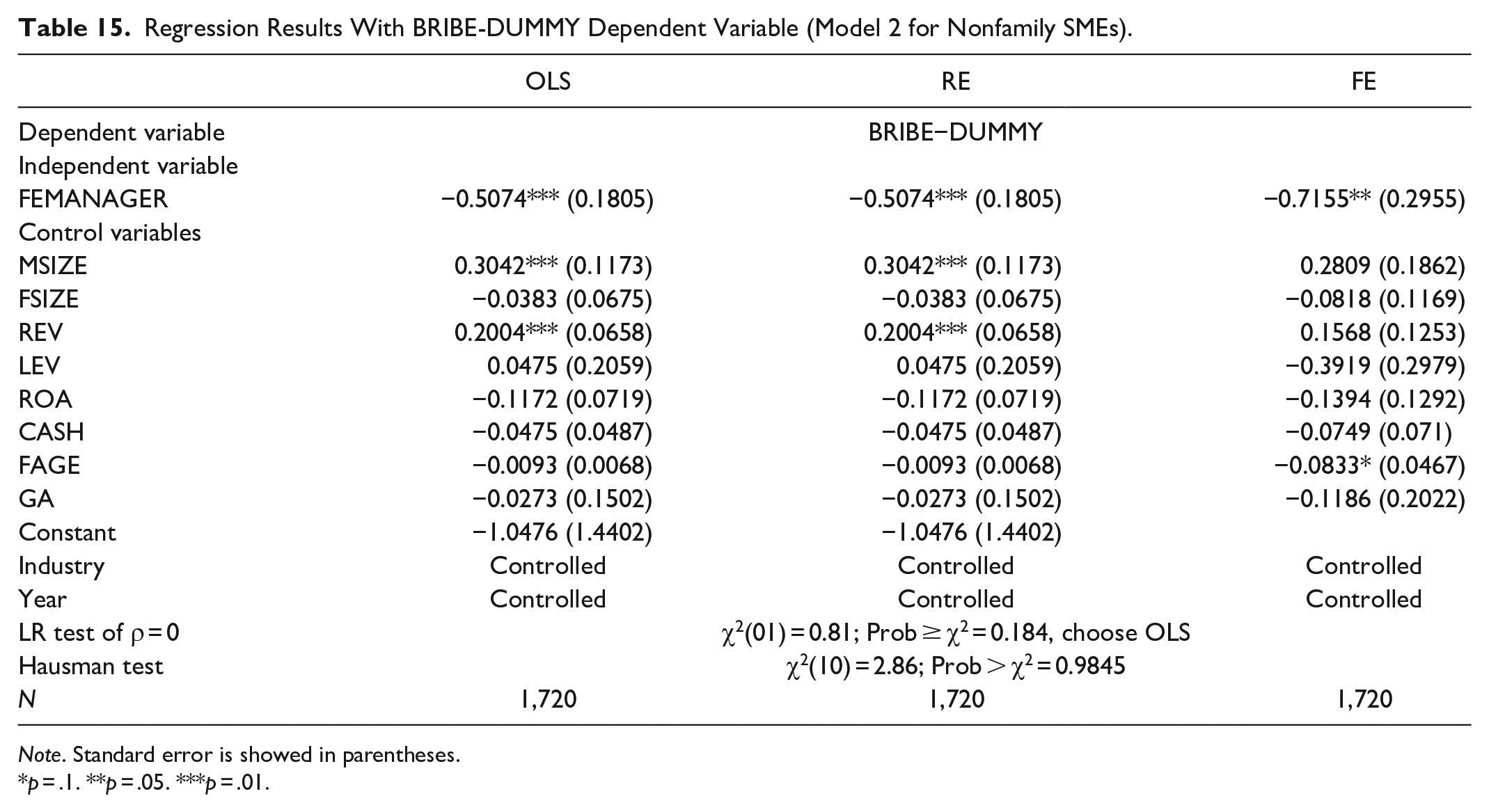

Note. Standard error is showed in parentheses.

p = .1. **p = .05. ***p = .01.

The Summary of Results.

Discussion and Implication

The main objective of this study is to investigate the performance shown by female managers in whether or not the firm pay bribes, and to analyze the moderating factor of family SMEs-household business. More specifically, we analyze the impact of board gender diversity on the possibility of SMEs’ involving in bribery and analyze the role of female managers in household and non-household businesses in SMEs’ corruption behavior, using a panel data of 1,720 SMEs, for 3 years: 2011, 2013, and 2015. Our main contribution is that the negative influence of the representation of women on the TMT in reducing corruption commitment is less so in family SMEs than in nonfamily SMEs-.

Turning to family SMEs, descriptive statistics show that there is a difference between family and nonfamily-businesses concerning the level of bribery. By contrast with our prediction, the linkage between family SMEs and the degree of corruption is negative and insignificant. However, when considering the situation that firm bribe or not, our results support for hypothesis 1 .This contrary finding is inconsistent with some previous findings which support the hypothesis that the level of family ownership is positive associated with more favorable reputation and socially responsible (Cruz et al., 2014; Deephouse & Jaskiewicz, 2013; Dyer & Whetten, 2006; Sageder et al., 2018) and negatively related with misconduct (Ding et al., 2016; Ding & Wu, 2014) in general. We consider a possible cause maybe that although, based on SEW preservation theory, family firms tend to be more concerned about their reputation and image than that of nonfamily firms, family SMEs-household businesses operate in a highly corrupt country, where bribery is “must-do activity” in doing business and considering “legitimate” stakeholders is necessary. Indeed, in the study undertaken by Pasquier-doumer et al. (2018), the experience of corruption in the form of bribes for officials or police was reported by Vietnamese household businesses at different levels. Because of administrative procedures understanding shortage and the benefit of convenience, they tend to engage in corruption such as paying bribes. Paying bribes is to gain authorization from administrative bodies to run the business or to replace fines because the firm is overdue in tax payment. Vietnam Provincial Competitiveness Index (PCI) also showed that 41% of firms consider that negotiating with tax agency is a necessary factor to run a business, so collusion and extortion are well entrenched (Malesky, 2013). Consequently, regarding household businesses, paying bribes to officials who are “legitimate stakeholder”, is fundamental to preserve the survival, growing and continuity of the businesses. Moreover, household firms are small firms, which usually suffers financial shortage, so they are they easily fall victim to illegal activities. National culture can also contribute to the degree of corruption (Achim, 2016). Vietnam is a culture that respect a high collectivistic society, being different from western countries. This type of society can involve in a higher level of corruption because people are willing to break the regulation for the interest of their own group, drawing from loyalty (Achim, 2016). To sum up, we suggest that two offsetting effects of SEW preservation and “must to do” unethical behavior is the cause of this contrary finding for hypothesis 1.

In term of the role of women in positions of influence in reducing SME’s corruption behavior, most previous scholars in ethics field have found that firms with a higher percentage of female managers are less likely to involve in fraud and unethical attitude like paying bribes (Lenard et al., 2017; Liao et al., 2019; Luo et al., 2020). Our findings support the prediction of our hypothesis: the proportion of female managers is negatively related to bribery involvement. This finding maybe explained by female orientation, which is more ethical sensitive (Eagly & Carli, 2007; Eagly & Johannesen-Schmidt, 2001; Hietikko, 2016; Ibrahim et al., 2009), socially responsible (Alonso-almeida et al., 2015), and less likely to engage in fraud (Charness & Gneezy, 2012; Cumming et al., 2015) than their male counterparts. Moreover, in male dominated TMTs, upper echelon theory posits that female managers are “unusual” and are likely to bring unique cognitive value to firms (Carpenter et al., 2004; Hambrick & Mason, 1984). The unique value can be their empathetic, collaborative, and empowering style (Eagly et al., 2003; Lauterbach & Weiner, 1996; Post, 2015) when they take a position of manager in firms, which enhance their quality of decision making. In addition, this finding also show that in a weak institutional environment like Vietnam, female managers still play a role in reducing corrupt behavior in business.

Nevertheless, this relationship depends on the moderator that represents household business. In other words, the negative relationship between female managers and the possibility of bribery engagement bases on the behavior of household members toward such practices. A possible explanation is that, first, female managers are more likely to be reliant on the preference of family’s firm in the decision-making process (Burke, 1997). Second, they are invisible in family firms and only considered as family delegate (Abdullah, 2014; Martinez Jimenez, 2009). Furthermore, women’s contributions maybe not assessed appropriately and remain in the background due to their intermediary role for male managers (Hollander & Bukowitz, 1990; Mitchell, 1984). Third, based on upper echelon theory, because family impacts significantly on senior executives’ decision making (Villalonga & Amit, 2006, 2009), their level of managerial discretion is weakened (Zahra, 2005). This research also confirms the finding of Chadwick and Dawson (2018) that upper echelon theory is declined in family-controlled firms because the degree of senior managers’ managerial independence is diminished. Thus, the degree of female leaders’ managerial independence in family firms is weaker than in nonfamily firms. Fourth, in the context of Vietnam where Confucian ideology has influenced every aspect of life, the responsibility of women is usually referred to household chores, and they are overshadowed by men in business and society (Pham & Hoang, 2019). Vietnamese women also suffer gender prejudice and their career development in business is much limited than men (Tu, 2017). Moreover, in Vietnamese families, the man is always considered to have more power than the woman. Hence, the managerial role of them in household business is weakened or obscured by men. To sum up, this would result in weakening the efficiency of female leadership in reducing corruption level in family businesses.

Conclusion and Limitation

Drawing from socioemotional wealth theory and upper echelon theory, we test the relationship between household businesses, as controlled by families, as well as female leadership, as represented by the proportion of women in senior executive positions, and the level of firms’ corruption, as represented by paying bribes. We also examine whether household business moderates the influence of women managers on firm’s degree of corruption.

First, we found that SMEs, which are family SMEs-household firms exhibit a negative and insignificant relationship with the firm’s corruption. This finding indicate that based on SEW, family SMEs-household firms tend to concern more about reputation but, operating in a highly corrupt business environment as Vietnam can make them become less ethical. We also found that the percentage of female manager in TMT is significantly positive with the firm’s corruption. This is in line with the suggestion of upper echelon theory and social role theory which state that the representation of women in management board can enhance firm’s image and reputation. In addition, our findings suggest that family ownership adjusts the influence of female managers on firm’s corruption level. According to upper echelon theory, this suggests that the managerial discretion of female managers in family-controlled firms can be less powerful than nonfamily counterparts. This finding also supports the previous studies of Chadwick and Dawson (2018). There are several practical contributions can be taken from this study. First, regarding SMEs, the appearance of female managers on management board is necessary to diminish the risk of engaging in corruption. Second, household businesses are highly impacted by the influence of corrupt business environment in Vietnam, which require Vietnamese policymakers to consider this problem. Third, household firms should promote the role of female leadership by giving them more managerial independence, which brings unique cognitive frames to the firms.

This study and its finding can also contribute to the study of corrupt behavior and female leadership in the context of other Asian developing countries. Similar with Vietnam, in these countries, the society of masculinity, more collectivistic and Confucius culture can impact on the degree of corruption level and the role of women in family business. By contrast, developed western countries such as USA, UK, and Australia follow a more individualistic and gender equality society (Achim, 2016), which can change the findings if a similar study is conducted. Thus, we suggest future studies in developing and developed countries to check the robustness of this research findings.

This study also has some limitations. First, corrupt behavior is a sensitive topic and some respondents may feel “uncomfortable” when being asked about this topic. Thus, although we mitigated this problem by taking the natural logarithm of bribe amount and keeping the confidentiality of respondents, incorrect information from the answer of them may change the findings. Future research should also use the Corruption Perception Index (CPI) calculated by Transparency International to measure the corruption to improve the accuracy of dependent variable. Second, regression method, applied in this study, is pooled OLS, REM, FEM, and 2SLS (two stages least square). However, as stated by Wintoki et al. (2012), the dynamic panel GMM estimator is the most appropriate method to solve endogeneity concerns in corporate governance study. We suggest that this econometric method should be used in future studies. Future research should also consider other types of female leadership (female CEO, female owner, female CEO-owner (duality)) to test the relationship. In addition, this study applies for SMEs in Vietnam but the findings can change when applying for larger and listed family firms because of different characteristics. Thus, we suggest that future studies should investigate the corrupt behavior of larger and listed family firms as well as the role of female leadership in the corruption level of these firms.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by National Economics University, Hanoi, Vietnam.