Abstract

The growth of Islamic banks in Indonesia has not been followed by the availability of competence human resources that meet professional qualifications. Higher education institutions are the large provider of human resources to fulfill the needs of Islamic financial industry. The aim of this study is to formulate the accounting curriculum development in Higher Education Institution (HEI) to fulfill the needs of human resources in Indonesian Islamic banking. This study is descriptive qualitative using instrumental and pragmatic paradigm to illustrate the need of accounting profession in Islamic banks and accounting curriculum formulation for HEI. The curriculum design places more Islamic basic knowledge and Islamic accounting in addition to accounting knowledge standards. The analysis of this study is expected to be able to create a link and match between the education institutions and the Islamic financial industry so that the human resources produced by educational institutions can be optimally absorbed by the Islamic financial industry. The study focuses in the development of the accounting and auditing curriculum for Islamic banking in higher education institutions in Indonesia.

Introduction

The Islamic finance industry in Indonesia shows a significant development. Not only Islamic banking, the non-bank Islamic financial institutions (IFIs) such as Islamic insurance, Islamic mutual fund, Islamic pawnshop, and non-profit Islamic financial institutions such as zakah and waqf organization have significant growth. For the year of 2019, the number of Islamic banks reached 198 Islamic banks with total assets of 538,322 billion IDR, while the number of non-bank Islamic financial institutions reached 209 institutions with total assets of 105,612 billion IDR (FSA, 2019). For Islamic micro finance institution (IMFI) that is registered in the Indonesian Financial Service Authority (FSA) is 75 units per December 2019, however, IMFI that is registered in the ministry of cooperative and SMEs (small and medium enterprises) is more than 5,000 units.

Indonesia is also strengthening its position in the global Islamic economy and finance. Indonesia was ranked first in the Global Islamic Finance Report 2019, up five places compared to the previous year. In the scope of Islamic economy, Indonesia is ranked fifth in the State of the Global Islamic Economy Report 2019/2020, where the development of Islamic finance is one of the factors driving Indonesia’s ranking (FSA, 2020). Indonesia also occupies the second position on the 2019 Islamic Finance Development Indicator, after Malaysia, which is seen based on the number of Islamic financial education institutions and producing the most Islamic finance research papers (FSA, 2020).

The development of those IFIs has consequence to the need of a lot of human resources, especially with special competences such as Islamic economic, Islamic finance and Islamic accounting and auditing. Indonesia faces challenges related to the limitations of human resources who have competencies according to the needs of the Islamic financial industry (Amalia, 2014; Huda et al., 2016). The increasing of IFIs requires large human resource, not only in terms of numbers, but also the competencies in accordance with the needs of IFIs. The chairperson of the Indonesian Islamic Bank Association (Asbisindo), Yuslam Fauzi, said that every year the Islamic bank’s needs 11,000 human resources, while universities are only able to provide around 4,000 workers who have Islamic economic background, and therefore, the need of 7,000 people per year for working in Islamic banks can not be fulfilled (Akubank.co.id, 2019). As a result, the employees in Islamic banks are dominated by bachelor degree who are not from Islamic economics background, even the majority of the employees are transferred from conventional banks (Republika, 2016).

Considering the demand of IFIs’ human resources, some universities in Indonesia have started to insert the courses related to Islamic finance/economics/accounting or even initiate the opening of department related to those subjects into their educational curriculum. Huda et al. (2016) in their research at several Islamic universities in Indonesia find that employment absorption from these universities in the Islamic finance industry is still very low, and one of the reasons is the curriculum that still prioritizes hard skills instead soft skills. Tahir (2009) argues that basic knowledge of Islamic economics in undergraduate programs will support the students understanding in the next program (postgraduate) as well as student research. Meanwhile El Ghattis (2016) argues that the curriculum of Islamic banking subject should support the critical thinking of both the lecturers and the students. Based on the analysis above, the question that needs to be solved in this paper is how to formulate a strategy for curriculum development at the HEI level to meet the needs of human resources in Indonesian Islamic banks. Accounting is one of the knowledge that needed in Islamic banking (AlAbbad, 2016). Accounting is a branch of science which in an Islamic perspective does not merely assist management in providing financial information to limited stakeholders, such as shareholders and management, but more broadly is a form of accountability for IFI performance to wider stakeholders such as consumers and society in order to realize the value of justice and welfare. Furthermore, focusing on one particular subject will make the discussion more focused and in-depth.

The aim of this study is to formulate the accounting curriculum development in Higher Education Institution (HEI) to fulfill the needs of human resources in Indonesian Islamic banking. Some previous studies tend to discuss the prospect and challenges of IFIs in Indonesia (Effendi, 2018; Nugraheni & Muhammad, 2020), or carry out confirmative research related to the knowledge of respondents such as the society, public, consumers, and students about the intention to saving or using the products and services of IFIs (Karim & Affif, 2005; Nugraheni & Fauziah, 2019). Some scholars discuss the curriculum of Islamic economics in HEI such as Amalia and Al Arif (2013), Amalia (2014), Arif and Hak (2016), and Zakiy (2017). However, those studies only describe the subjects that should be taught in universities or college, without including a sample curriculum of courses that must be taught as a whole while students are pursuing higher education. There are still less empirical studies at the national or international level about the analysis of Islamic Economics/Finance/accounting curriculum at universities to fulfill the needs of human resources in the Islamic financial industry.

Identifying the right courses in universities’ curriculum is needed to improve student competencies to meet the needs of human resources in Islamic financial industry. Although every IFIs already has a training and development program to its employees, but the existence of higher education to produce the quality graduates for the need of business industry is important. Therefore, one focus of this research is to fill the empirical literature in the field of Islamic Economics and Financial education. It is expected that this study can provide some contributions: first, Indonesia has a major contribution in the development of Islamic finance at the global level. Therefore, all efforts to maintain and enhance Indonesia’s role in the world need to be carried out, by preparing the necessary infrastructure, including competent and professional human resources in the field of Islamic accounting. Second, this study uses an instrumental and pragmatic paradigm. Instrumental paradigm is useful to identify the need of the accounting profession in Islamic banks, while pragmatic paradigm is used to illustrate the accounting curriculum based on identification of accounting profession needed in Islamic banks. Third, increasing the role of higher education and academicians in formulating educational program to produce the quality graduates who can meet the needs of Islamic financial industry, especially Islamic banking that having most rapid, popular and massive development. Forth, this research is expected to be able to create a link and match between the education institutions and the Islamic financial industry so that the human resources produced by educational institutions can be optimally absorbed by the Islamic financial industry.

The study will be divided into several sections, first, the literature review discusses the development of Islamic financial industry and the competency that should be had by the employees of Islamic banks. Second, research methodology will describe the method used in this study and third, the discussion about the development of accounting curriculum to increase the competency of HEI graduates. Mapping the accounting profession in Islamic banks and the competency that needed by the university graduates to work in Islamic financial industry are important to increase the quality of HEI graduates.

Literature Review

Development of the Islamic Financial Industry

Islamic financial industry began after several Muslim countries gained independence from the colonialism in the 1950s until the 1960s. In 1963, a social movement activist, Ahmad-al-Najjar founded a financial institution that promoted a social welfare institution called Mit Ghamr Local Saving Bank (1963–1967) with a mechanism of financial institutions that actually uses Islamic Sharia principles. Ahmad (2000) explain that after Mit Ghamr no longer existed, in Egypt the Islamic financial institution Nasr Social Bank was re-established in 1971 to help some of the weak and disadvantaged society. Furthermore, other countries such as Malaysia and Dubai also introduced financial institutions based on Sharia principles, namely Lembaga Tabung Haji in Malaysia in 1963 and the Dubai Islamic Bank in 1975. Recently, those countries and Bahrain are known as centers of international Islamic financial industry development due to the enormous government support and high interest in Islamic financial business in the region.

Askari et al. (2009) notes that the Islamic financial industry began to receive international attention from the early 1990s until the early 2000s by starting to establish Islamic financial institutions in various countries even in capitalist and socialist countries. This happens because of two main factors, first, during 30 years of their existence, there is no Islamic banks that failed systemically, even during the financial crisis, those banks has increased the efficiency and profit compared to conventional banking. Second, Islamic financial system shows better stability than the conventional system (Khan & Bhatti, 2008).

The international academicians have also begun to develop not only in Muslim countries but also in non-Muslim countries that have mature academic culture. Askari et al. (2009) states that reputable educational institutions such as Harvard University (USA), Durham University (UK), and Loughborough University (UK) periodically held international seminars and conferences, establish departments from undergraduate to postgraduate, and certification courses in Islamic Economics and Finance. Even prominent publishers such as Euromoney, John Wiley, and Edward Elgar also productively publish books on theoretical and practical studies in the field of Islamic Economics and Finance. Those prove that the Islamic financial industry has been recognized academically and has received high attention by economists and conventional financial practitioners as one of the main alternative systems to offset the dominance of the Neo-classical economic system.

The Competency of Human Resource in Islamic Financial Institutions

Islamic Financial Institutions (IFIs) become alternative for Muslim customers who want their economic activities to remain in accordance with Islamic principles. The good development of IFIs apparently raises other challenges that must be considered. Customers will still consider the performance and quality of services provided by Islamic banks, and one of the several factors that are considered by customers is employee’s competency (Dusuki & Abdullah, 2007). However, the availability of the good quality of human resources is not balanced with the development of IFIs (Djayusman, 2017). This is one of the challenges that needs to be formulated as a solution so that the quality of human resources in the Islamic finance industry can meet the expectations of the community.

Activities of IFIs that are different from other organizations generally require resources that have appropriate knowledge according to the characteristics of IFIs. Ideally, all employees at all levels of IFIs have understanding not only about the knowledge of business but also knowledge of Islamic principles although in different levels. According to Rozalinda (2016), the qualifications and competencies of human resources should be adjusted to the needs of IFIs so that they can improve the performance of the institution. Meanwhile Musa et al. (2020) state that the problems of human resources in IFIs were lack of sharia background and sharia training. Previous studies identify the kind of knowledge that IFIs’ employees usually have. For example, Nor et al. (2012) state that the competency of Islamic bank employees is more dominated by general knowledge such as accounting, finance, economics, management and banking knowledge so that banks must provide training on sharia aspects. Some training centers set up by Islamic banks in Middle East and GCC focused on the employee understanding of technical aspects including transactions and dealing in accordance with Islamic principles (Nor et al., 2012).

Agustianto (2015) argues that employees of Islamic financial industry should have several competencies such as Arabic and English, Islamic economic knowledge such as fiqh muamalah, and the implementation of fiqh muamalah in the IFIs’ activities. Hidayat et al. (2020) in their research in Russia state that the level of awareness of the IFIs’ employees toward Islamic finance is still low despite having a good level of education. The reason may come from the small number of Muslims and the geographical location of Russia that is far from Islamic financial development countries. Therefore, in formulating an Islamic financial education curriculum further, it is necessary to devise a strategy that is appropriate and relevant to these conditions. This is in line with the argument of Ki-Yoon and Ken (2002) that in carrying out curriculum design, stages are required to obtain data and record information related to jobs in accordance with their functions within the company organization, the capabilities and competencies needed, and who is eligible to do it. Then a job analysis is needed to find out the functions and specifications.

IFIs and Human Resources in Indonesia

Indonesia is not a new country in recognizing the Islamic financial industry. The idea of establishing Islamic bank has emerged since the 1970s during the National Seminar on Indonesia-Middle East Relations in 1974 (Muhammad, 2019). However, only in the year of 1992 the Indonesian government issued Law Number 7 of 1992 concerning Banking which giving opportunity for banking industry to provide profit sharing system. Currently, Indonesia has become part of the development of the Islamic financial industry both practically and academically with the establishment of Islamic Economics and Financial institutions and department or college in the state and private universities.

Indonesia with the largest Muslim population in the world is the development target of the Islamic financial industry in the world after the Middle East and several countries in Europe such as Britain, France and Germany (Nair & Richter, 2010). It also motivated by the development of Islamic financial industry in Malaysia which became one of the two strongest Islamic financial countries in the world after Bahrain (Askari et al., 2009). The seriousness of the regulator to support the development of the Islamic financial industry in Indonesia is seen in 2019 where Indonesia won the first rank for the global sharia financial market from the Global Islamic Finance Report (GFRI) in 2019 after the previous year only have ranked sixth (Edbiz Consulting, 2020). The bright future in the global financial industry indicates good employment opportunities also for the human resources who want to have career in this industry.

Table 1 describes the total number of employees in Indonesian Islamic banks. Although there is a fluctuation of the number of employees, but the last data of December 2019 shows the highest number of employees of Islamic banks.

The Number of Employees of Indonesian Islamic Banks.

Furthermore, the fluctuation is not followed by the fluctuation of human resources cost because every year the cost is increased, including for training for the employees. Table 2 shows human resource cost for Islamic commercial banks and Islamic business units.

The Amount of Human Resources Cost for Islamic Commercial Banks and Islamic Business Unit (in Billion IDR).

FSA (2017) publishes a roadmap to develop Islamic finance in Indonesia, and one of the programs are to increase the quality of human resources including: (a) forming a working group for Indonesian Rector Forum to prepare the curriculum of Islamic finance, (b) organizing training for trainers of Islamic finance, (c) developing program of certification and continuing professional education, and (d) cooperating with higher education institutions to create reliable human resources.

Higher education institutions are the large provider of human resources to fulfill the needs of Islamic financial industry. However, the lack of Islamic economics competency of their graduates makes IFIs’ often spend a lot of money to educate their employees. Another way is to hire employees who come from conventional institutions who at least have the business knowledge so that training costs are cheaper. The large number of university graduates in Indonesia is not guarantee that they have the skills needed by the industry, including in Islamic financial industry. This is not only a problem for the Islamic financial industry, but also a challenge for universities to graduate human resources who are ready to work in this industry. Some experts state the importance of practical lectures for students to know the real IFIs operational activities. However, theoretical knowledge remains important as a basis for the application of practical knowledge.

Von Konsky et al. (2016) explain that curriculum should be designed by good collaboration between academics and industry practitioners as stakeholders as well as prospective users who would utilize college graduates. Industry practitioners are expected to provide input in the form of relevant competencies that are currently needed in the workplace. It means that the educational program should teach certain competencies to accommodate the skill needed by the business industry. Therefore, it is important to consider the involvement of practitioners of the Islamic financial industry more intensively in the activities of formulating learning objectives, compilation of courses, implementation, and the process of periodic evaluation of the curriculum in higher education.

The Model of Islamic Economics and Financial Education

Chapra (1995) stresses the need for moral values in education because conventional education that currently exists is less successful in forming individuals who have the morality of both science and commitment and integrity to their respective professions. This can be shown by the fraud both in the business industry and government management. Therefore, the Islamic financial industry, which has characteristics of Islamic values in its business transactions needs to be part of the solution by encouraging fair and honest practices in carrying out its activities in the global business environment.

Khan (2015) mentions several factors related to problems in Islamic economic education such as the availability of books, non-standard curriculum, and the limited number of institutions that provide training in Islamic economics and finance, both formal and informal institutions. Huda et al. (2016) states that one of the main problems faced by the Islamic financial industry is the lack of quantity and quality of human resources who understand economics and finance with sufficient Islamic knowledge. What currently exists usually individual who only has the knowledge of economics and finance and some others only have the knowledge in Islamic subjects. In fact, developing human resources for the Islamic financial industry does not only have the conventional knowledge but also should be based on the adequate Islamic knowledge. Djayusman (2017) also states that the rapid growth of the Islamic financial industry is not matched by the presence of human resources who had sufficient competency because formal education institutions are slow to respond to this development. Consequently, non-formal educational institutions emerge and conduct short courses to meet the need of human resources quickly although they are not inadequate in terms of curriculum.

Munthe (cited in Zakiy, 2017) identifies five challenges in developing human resources in Indonesian HEI: (1) the lack of Islamic economics expert, (2) the lack of Islamic-based curriculum, (3) the lack of textbook about Islamic economics, especially in Indonesian language that make it difficult for readers to understand the books, (4) the weak collaboration between IFI and HEI, and (5) the lack of research about Islamic economics because of the limited funding.

Nasution (2009) states that:

The need for a large number of human resources can be met if the material for teaching Islamic economics is formalized as teaching material in educational institutions. In addition, Islamic economic education not only addresses the needs of human resources quantitatively, but also qualitatively.

This means that the formation of human resources for the Islamic financial industry cannot actually be achieved in a short time. It needs the planning of adequate curriculum related to the material concept and focus on certain professional fields. Thus, the education model for creating human resources for Islamic financial industry needs to be formulated by using deductive and inductive approach.

The deductive approach emphasizes the existence of normative elements derived from the values of the Qur’an and Sunnah. This approach is used by Al Alwani (1995) to implement Islamization of knowledge by building scientific paradigms based on methodologies related to the Qur’an and Sunnah. The methodology is used to evaluate and review conventional knowledge so that it can be known which is appropriate and which is not in accordance with the Islamic principles. This approach will be more practical when combined with the approach of Khalil (1995) who tries to build scientific methodology from the theoretical side to the practical level. This approach seems to be in line with the expectation of providing human resources for Islamic financial industry which have strong basic of Islamic knowledge and are able to evaluate and elaborate conventional economics and finance to develop Islamic finance.

The second approach is an inductive approach that emphasizes the practical aspects and needs of the Islamic financial industry which form the basis of curriculum development. Islamic financial business practices are sometimes distorted by conventional views based on secular and capitalist values. These things need to be filtered with sufficient Islamic knowledge to assess the halal (lawful) and haram (forbidden) of a transaction, not only limited in the name that contains Islamic aspects such as murabahah, ijarah, and mudharabah. Al-Faruqi (1988) introduces the methodology of Islamization of knowledge by mastering modern (conventional) sciences, followed by good mastery of Islamic heritage so that a Muslim intellectual was able to synthesize Islamic heritage that is relevant to the development of modern science. This is reinforced by the approach of Sulaiman (1989) who tries to pair up the scientific position that comes from human reasoning with God’s revelation as outlined in the holy book of the Qur’an. Therefore, the human is not free of value because there are limits that need to be obeyed so that the knowledge developed is beneficial for the benefit of society (Adibah, 2013).

Kusuma (2006) proposes a number of strategies for developing the Islamic Economics curriculum in higher education: first, Islamic economics as a stand-alone course and consists of several subjects. Second, the material of Islamic economics is not independent, but is included in a variety of existing economic courses. However, for universities that have not been able to implement a broad Islamic economics curriculum, at least they can incorporate norms, Islamic ethics in certain subject topics, such as; Introduction to Microeconomics, Introduction to Macroeconomics, Economic Systems, Monetary and Fiscal Economics, Introduction to Management, Introduction to Entrepreneurship, and so forth.

Previous studies show several challenges that still have to be faced in creating quality human resources for IFIs, including the importance of strengthening Islamic knowledge in addition to general knowledge related to business. Various strategies have also been described how to improve the quality of human resources in Indonesian Islamic bank. It may still take a long time to create ideal human resources of Islamic banks, even though some challenges have been started to be solved. For example, HEI specifically offers Islamic economics study programs, or special courses related to Islamic banking knowledge. This study focuses on one of the challenges, namely creating an ideal human resource who has basic and Islamic knowledge through the accounting curriculum at HEI.

Research Methodology

This paper will try to describe the curriculum of higher education institution related to Islamic economics, finance or accounting. The research method used is descriptive qualitative by analyzing the problem using previous studies that discuss related topics. Descriptive method is useful in sharpening the analysis of data to obtain information about the direction and the potential development of Islamic finance and banking education in the level of universities. This method is also used by Khan (2015) who discusses the competency and performance of human resources in Islamic banks using a literature review analysis.

In addition, Visscher-Voerman et al. (1999) divided four paradigms in curriculum compilation, among others: (a) instrumental paradigm; (b) communicative paradigm; (c) pragmatic paradigm; and (d) artistic paradigm. Instrumental paradigm is an approach in curriculum design by starting to plan with clear objectives as a reference used in the preparation of the next curriculum instruments. This paradigm is the most widely used in the world of education. Meanwhile, the communicative paradigm emphasizes stakeholder participation in curriculum design. Pragmatic paradigm emphasizes practicality in design by using a prototype that can at any time be evaluated with the functions felt by its users. Finally, artistic paradigm is the idealism of the curriculum compilers according to their subjective considerations based on reasons they consider rational.

This paper will combine the instrumental paradigm and pragmatic paradigm with the consideration that: first, the formulation of the curriculum has the aim to prepare graduates to have competencies according to analysis of the needs in Islamic bank organizations. Second, the formulation of the curriculum ends by preparing a prototype of the design of the courses offered with the possibility of evaluation and improvement in accordance with stakeholder needs. Third, the preparation of this prototype does not involve stakeholders in the Islamic banking industry and still uses the writer’s subjectivity.

This study aims to discuss the accounting curriculum development in Higher Education Institution (HEI) to fulfill the needs of human resources in Indonesian Islamic banking. According to Salehi et al. (2013), the first step that universities must take to be able to prepare graduates who are suitable for the job market is to identify the labor market needs and then create a planning (curriculum) related to the expertise and skills needed. Therefore, some steps conducted in this study based on the previous studies including: (1) Identification the challenges of creating HR in Islamic banks, (2) doing analysis of HEI readiness in Indonesia, (3) identify the accounting profession in Islamic banks by looking at the organizational structure of one of the Islamic banks, and (4) based on the competencies required by the accounting profession in Islamic banks, this study designs accounting curriculum to improve the required competencies.

Analysis and Discussion

The Challenges of Creating Human Resource (HR) for IFIs

Some previous studies have been stated the challenges of fulfilling the need of human resources for Islamic financial industry. This study identifies the main problems that currently emerge in creating quality human resources for Islamic banking: First, there is low synergy between the HEI and Islamic business practitioners in Indonesia to develop an education program for students that fulfill the needs of Islamic financial industry (Huda et al., 2016; Zakiy, 2017). It is undeniable that there has been some collaboration between educational institutions and Islamic financial institutions, but this phenomenon is only limited to sporadic actions by individual institutions and has not long-term vision. Second, in contrast to other countries that conduct top-down approach, which the strategies to develop Islamic financial industry are come from the government, Indonesia tend to implement Bottom-Up Approach where there are freedom for the society to contribute to the development of Islamic finance and it impacts on the more strong commitment base.

Third, more HEIs in Indonesia have now established the department of Islamic economics, Islamic Finance, and Islamic Accounting as a response to the rapid growth of IFIs and high demand of human resources for IFIs. However, HEI needs to consider not only producing a large number but also enhancing the quality of the graduates that having competencies and qualifications that are in line with the needs of Islamic financial industry (Zakiy, 2021). If not, the Islamic financial industry needs to pay more to grade up the graduates. This is one form of inefficiency that leads to a decrease in competitiveness as a result of the high cost of training and human resource development.

Analysis of Higher Education Institution Readiness in Indonesia

Higher education institutions in Indonesia have actually offered and developed departments related to Islamic Economics, Management, Finance, and Accounting in accordance with the capabilities of their institutions respectively. Initially, these universities were limited to offer a number of courses such as Islamic Economics, the Basics of Islamic Banking, and Islamic Accounting. Those institutions also held Islamic Banking Training/Short Course as commitment to increase the knowledge of graduates from various educational backgrounds who are interested in developing Islamic financial industry. Finally, a more serious step from these matters is to establish a new department with a focus on Islamic Economics and Finance.

Based on data from the National Accreditation Board-Higher Education Institutions (BAN-PT) in 2020, some HEIs have organized educational program of Islamic economics and finance which has accreditation as described in Table 3.

Higher Education Institutions Which Organizing the Departments of Islamic Economics, Finance, and Accounting.

Source. National Accreditation Board-Higher Education (18 April 2020).

The table 3 shows that the number of program study in Islamic economics and finance (including Islamic banking) in Indonesia. However, there are several things that can be noted, among others: first, the Ministry of Education does not seem to have a clear scale of needs related to human resources in Islamic financial institutions because the study program granted permission to operate does not specifically describe the profession that will be needed in institutional practice of Islamic finance. Second, the study program still illustrates general knowledge in the field of Islamic economics and finance that might reduce the confidence of prospective users of graduates related to their competencies. Third, study programs that have special competencies such as Islamic accounting have not been popularly offered because of the narrow market in the eyes of prospective students.

Huda et al. (2016) reveal that many universities in Indonesia initially offer subjects of concentration and research interest in the field of Islamic economics, finance, and Islamic accounting. However, in general, these initiatives are still partial and not standardized so that the level of curriculum variation offered is very high between the universities. Amalia (2014) states that the curriculum of Islamic finance subject in many universities in Indonesia has its own characteristics, depends on their policy on the curriculum and learning material. According to Amalia and Al Arif (2013), the curriculum should include the vision and mission and educational goals of the related department, including the expected results from the department to their students such as the competencies for the future.

Therefore, this paper also highlights the tendency that educational providers who provide human resources in Islamic financial institutions do not have a clear orientation in preparing their graduates to be ready to enter the workforce in Islamic financial institutions. The obstacles faced by the education providers include: first, the lack of synergy between the ministries of education, the business world, and academics in the formulation of an appropriate curriculum. Second, the ability of academics to formulate curriculum and teaching materials that are rarely updated so that there is a gap between the world of education and the reality of work. Third, students are less equipped to study independently and tend to rely on teaching materials provided by lecturers.

Identify Accounting Profession in Islamic Banks

This study aims to discuss the accounting curriculum development in HEI to fulfill the needs of human resources in Indonesian Islamic banking. Accounting is one of the knowledge that should be owned by the employees of Islamic banks (Nor et al., 2012). Accounting is a branch of study that studies how an entity, both business and the public or non-profit sector, records its business transactions and reports on its economic activities to stakeholders. At present, accounting has evolved not only to study technical reporting but also to discuss various issues related to report several aspects including social responsibility, environmental stewardship, the impact of financial statements on corporate decision making, and even the importance of accountant ethics that can influence financial reports (Haniffa & Hudaib, 2007; Maali et al., 2006).

Rahman (2010) states that accounting in an Islamic perspective has very clear objectives as expressed in the Qur’an implicitly and explicitly (Al Anbiya’: 47 and Al-Baqarah: 282), that accounting goals should ensure honesty and justice in transactions made between the parties. Accounting is a form of accountability to God so that the information generated should be able to reflect the responsibility of human actions to God who also meets the need for financial information, social activities, and other information for its stakeholders. Accounting in Islamic perspective has users that are not only limited to shareholders and management, but more broadly are Muslims and society.

Accounting and Auditing for Islamic Financial Institutions (AAOIFI) reveals clearly that IFI especially Islamic Banking is an Islamic entity that has dual functions, namely economic and social functions, so that the accounting also needs to involve non-financial aspects that affect the condition of the business environment. Accounting for Islamic Banking has its own uniqueness compared to conventional accounting, and therefore, The Chartered of Indonesian Accountants (IAI) issued Statement of Financial Accounting Standards (SFAS) Number 59 concerning Accounting for Islamic Banking in 2003 which was later updated with Islamic SFAS in 2007 (Muhammad, 2019).

On the other hand, the curriculum of accounting department in general has covered various technical aspects in financial management and operational activities such as management accounting, internal control systems, accounting information systems, management information systems, auditing and financial control, as well as various other aspects that are very close as a effort to manage good and healthy entities. Therefore, the paper argues that the accounting and auditing fields have a significant role in the process of managing entities both business and the public sector. Specifically, the discussion of the professions in Islamic Banking will focus on a number of professions that have close links with the field of accounting and auditing.

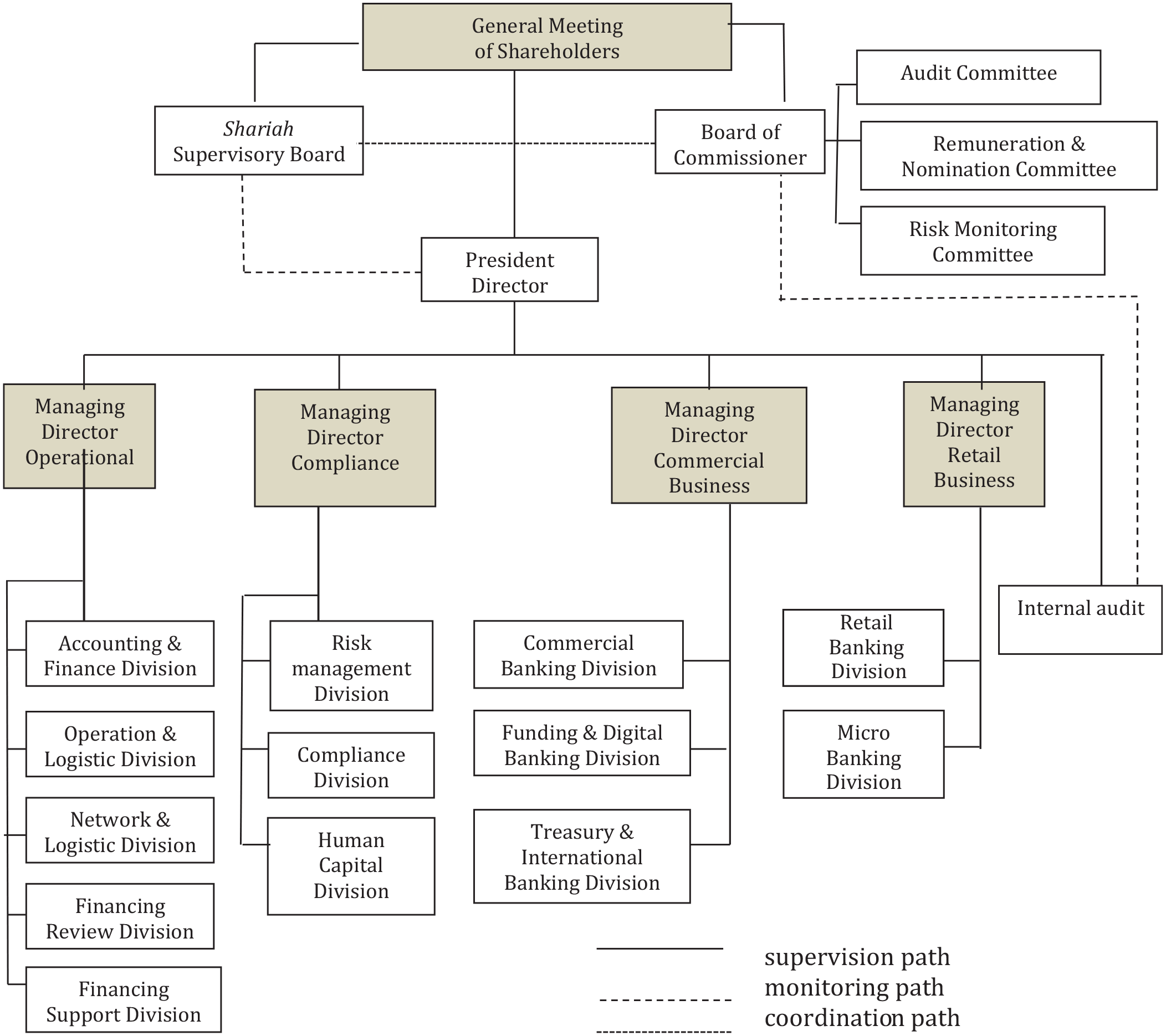

Figure 1 shows the example of organizational structure of the head office of one of the Islamic bank in Indonesia (BRI Syariah) for the year of 2019. However, the organizational structure may vary between Islamic banks because it depends on the need and the environment of organization both the internal and external condition.

Organizational structure of Islamic commercial banks.

Based on the organizational structure of Islamic banks, Table 4 tries to formulate several professions in Islamic Banking. The professions in Table 4 are divided into two groups, namely accounting and auditing. The auditing sector focuses on the process of supervision and examination of the preparation of financial statements or other activities that are involved in Islamic banking activities. Auditing has also been included in the field of compliance monitoring on Sharia in AAOIFI since 2002.

Illustration of Profession in Accounting and Auditing for Islamic Banking.

The table 4 shows that there are some levels of employees in the field of accounting and auditing. This is inline with Zakiy (2017) who mentions that jobs in Islamic banks can be divided into operational and managerial levels. The different positions may influence the level of knowledge that must be possessed. For example, knowledge of auditing, fiqh muamalah and Islamic banking is important knowledge for auditors in Islamic banks (Mohd Ali et al., 2020).

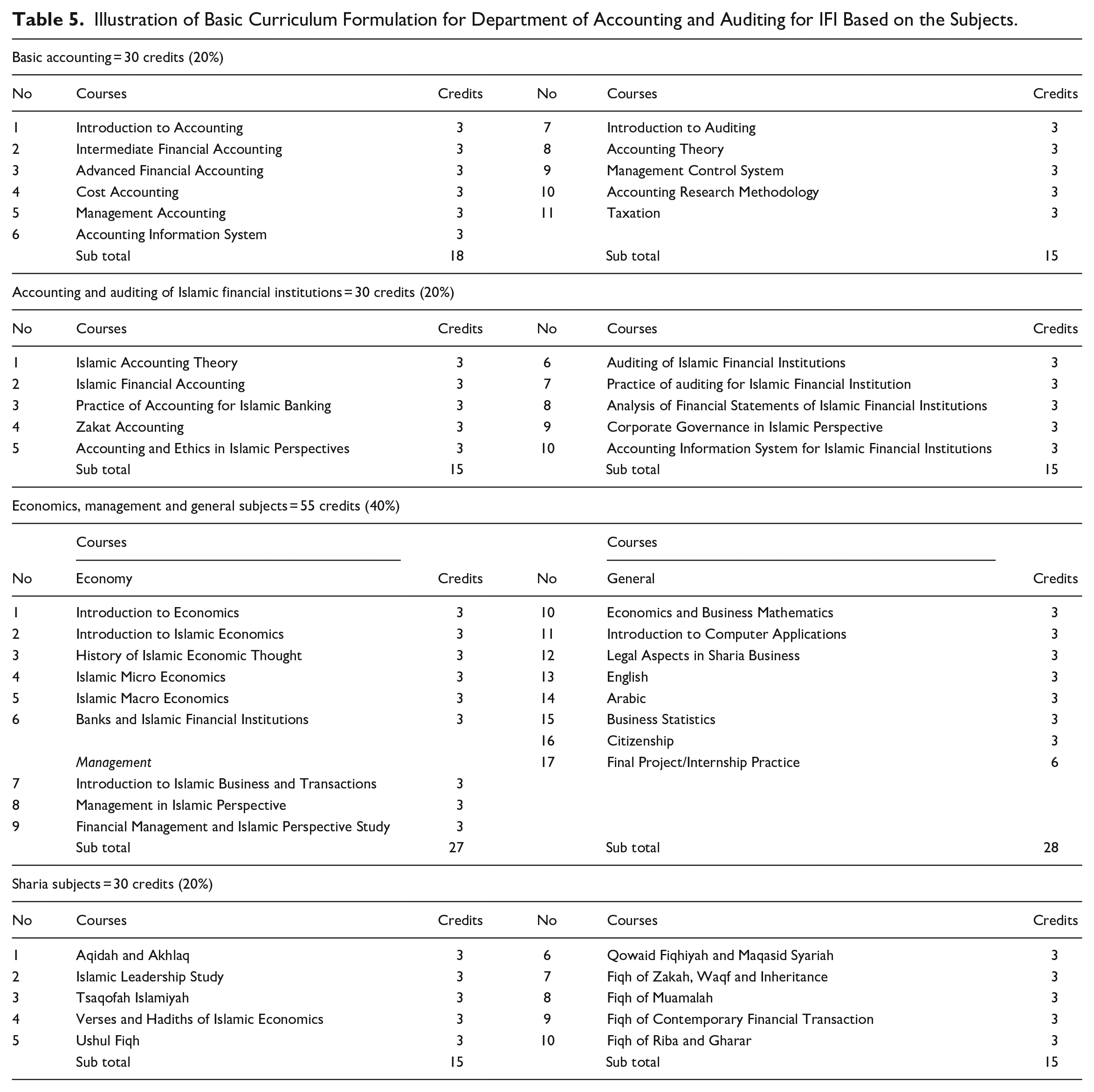

Illustration of the Curriculum Formulation of HEI (Case Study of Islamic Accounting Department)

Kessels (1999) defines curriculum design is an effort to combine various abilities and competencies that exist in the daily work environment delivered to students who join in an education program. Therefore, based on those professions on the Tables 4 and 5 provides an illustration of the curriculum of the Islamic Accounting Department. Several supporting courses that have potential contribution to the development of these professions also are included in that illustration.

Illustration of Basic Curriculum Formulation for Department of Accounting and Auditing for IFI Based on the Subjects.

The illustration in Table 5 covers several groups of subjects, namely the group of basic accounting, accounting and auditing for Islamic financial Institutions, economics, management and general subjects, and the Sharia subjects. The purpose of accounting education is to prepare students with technical competencies and business competencies to become professional accountants (Mcvay et al., 2008). Therefore, the accounting curriculum must be developed following the current professional practice (Al-Shehabet al., 2021).

This table 5 uses an illustration of credits for bachelor program. This composition in percentages can be replicated for the diploma level so that it is able to reflect the competency needs in the Islamic finance and banking industry. The composition of the basic accounting and sharia subjects’ groups of 20% each indicates that basic accounting and sharia skills are an important part of providing a basic understanding of accounting knowledge as well as sharia knowledge that equips students with basic Islamic skills. These basic Islamic skills include character education and basic knowledge of Islamic law as a basis for product development and practice in the Islamic finance industry. Bhatti (2011) states that it is important for employees of Islamic banks to understand the operational activities of Islamic banks activities because their transactions have big differences with conventional banks. Therefore, courses related to Islamic banking and banking products, Islamic accounting and Islamic finance need to be strengthened so that undergraduate students have stronger Islamic knowledge competencies (Zakiy, 2021).

Meanwhile, technical skills and main competencies have a portion of 60% consisting of knowledge competencies in managerial, legal, economic, and supporting technology (40%) and accounting and auditing of Islamic financial institutions are given a portion of 20%. The knowledge is expected to support the improvement of human resources’ quality such as foreign language skills (English and Arabic), oral and written communication skills, research skills, information technology and other abilities relevant to the work field. Amalia and Al Arif (2013) argue that the education of integrative Islamic economics should contain (a) Arabic and English; (b) Basic Sharia Knowledge; (c) General Economics; (d) Islamic Economics; and (e) Research Methodology.

Providing a larger portion of these competencies is certainly relevant to the needs in the world of Islamic financial industry practices, which have a higher transaction complexity than in the conventional financial industry. Provision of technical skills and knowledge of sharia compliance are added value for graduates of Islamic economics and finance education.

Pata et al. (2013) suggested that to avoid misunderstanding for stakeholders, curriculum design should be communicated with many parties to increase relevance in producing graduate output. Thus, this structure of courses should be discussed with other parties such as practitioners as end users and regulators by considering the conformity with the development of laws and regulations. The objective is to produce a curriculum that has a high level of suitability with the work field. Even some universities periodically do an evaluation of their curriculum so that it is always in line with the development of the business world. This is in line with Kessels (1999) who proposed a relational approach in curriculum design to involve stakeholders in the process of curriculum development and implementation.

Furthermore, this structure of courses should be completed with the learning outcome as mentioned by Pata et al. (2013). They said that learning outcome will be the basis for making decisions related to the preparation of curriculum tools such as instructional instruction, course series, assessment models, staff development, etc. The curriculum is a collection of tools such as learning materials, learning experiences, objectives, and assessments. While courses are part of the curriculum which usually starts by determining competencies that are appropriate to the end of the lecture.

Conclusion and the Way Forward

Islamic banking and financial industry in Indonesia has developed very rapidly along with the increasing interest of the Indonesian people to obtain banking services and other financial transactions that providing better value in terms of economic and social. The growth of Islamic banking and financial institutions from micro to large scale reflects the high response of the public and business world to this industry. However, this industry faces serious problems related to the availability of competence human resources that meets professional qualifications. Therefore, it is usual for industries to take shortcuts by recruiting graduates with high GPA but do not have a background in Islamic Economics and Finance.

Higher education institutions are the large provider of human resources to fulfill the needs of Islamic financial industry. Some challenges for HEI to produce the graduates who meet the needs of human resources for the banking industry and Islamic finance are the lack of cooperation between HEI and practitioners, the limited number of experts in Islamic economics and finance as well as there is no curriculum standardization either issued by the Indonesian Ministry of National Education or the Ministry of Religion.

This study identifies the accounting profession in Islamic banking such as financing analysis, financing manager, and auditor. Based on the profession, the study provides an illustration of the curriculum of the Islamic accounting department that divided into several groups of subjects, namely the group of basic accounting, accounting and auditing for Islamic financial Institutions, economics, management and general subjects, and the Sharia subjects. This study is expected to contribute in the increasing role of the higher education institution in Indonesia in formulating educational program to produce the good quality accounting graduates who can meet the needs of Islamic banking.

The implications of this study for the development of curriculum design at HEI provide a breakthrough in flexibility using a hybrid approach by taking the advantages of the paradigm that has been developed by Visscher-Voerman et al. (1999). The four paradigms developed have advantages such as a combination of instrumental and pragmatic paradigms that are able to produce curriculum designs that are expected to be more in line with industry needs. Further, curriculum development can also use other combinations such as the communicative paradigm and artistic paradigm to obtain curriculum designs that have aspects of idealism from experts in certain fields and communicated with stakeholders to get more practical input in order to obtain curriculum designs that always follow the expectations of the stakeholders.

This study is expected to have an impact on the development of the industrial world, especially the Islamic banking and finance sector in term of preparing human resources who are ready to work with adequate competencies. Curriculum design that involves relevant stakeholders is to provides opportunities for industry to not only provide input but also be involved in the design process and curriculum implementation. The involvement of industries can be in various forms of collaboration such as internship programs for students, involvement of lecturers from practitioners, and real case-based collaborative projects study that will certainly provide added value for students who are actively involved in it.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.