Abstract

This article demonstrates, on one hand, how organizations are able to optimize their business processes to streamline their activities and, on the other hand, how performance can be enhanced by using the target cost method in a construction project. Based on the analysis of national and international literature, the authors carried out a quantitative and qualitative study based on a questionnaire containing a set of four questions aimed at highlighting the issues mentioned in the launched objectives. Business process-specific steps in a construction project are described and analyzed. The case study outlines how to optimize business processes by using Swimlane charts and how to reduce operating costs by applying the target cost method. The article concludes with our conclusions about the real benefits of optimizing business processes in a construction project by using the target cost method and increasing the performance of entities in this field.

Keywords

Introduction

In the modern business environment, organizations have been trying to identify new ways to increase their efficiency and ensure the successful execution of critical business processes, to ensure an advantageous competitive position in a given market (Abdelkafi & Täuscher, 2016; Zott et al., 2011). Ensuring a strong competitive position in a certain market depends on certain key factors, such as customer service and quality, low costs, ongoing customer relationship improvement, and maximum flexibility in meeting customer requirements and exigencies (López-Cabarcos et al., 2015).

Business processes are directly related to competitive advantages and profitability (Biloshapka et al., 2016; Massa et al., 2017). The most efficient functioning of an organization is related to the identification, monitoring, analysis, control, and improvement of business processes, as provided by business process management (BPM). The concept of BPM is built around the desired result and not the tasks required in delivering results by taking certain standardized steps to ensure the consistency and efficiency of business processes and reduce the risk of errors (DaSilva & Trkman, 2014). BPM supports the evaluation and continuous improvement of business processes, to optimize them and provide the best possible results (Demil & Lecocq, 2010; Foss & Saebi, 2018).

The theory explaining the concept of BPM has evolved from a simple focus on providing value by reducing costs and increasing efficiency in customer orientation (De Oliveira & Cortimiglia, 2017; Gassmann et al., 2014). Thus, the customer experience has become the business priority for most organizations, which is why our study aims to meet these requirements and tries to demonstrate the optimization of business processes in a construction project and increase performance (Peric et al., 2017; Yusof et al., 2014).

The implementation of BPM requires the mapping of workflows and their analysis, as well as the performance of tests to identify obstacles, which could prevent the optimal development of business processes. For decades, BPM existed only as a manual practice and technology was not a necessary requirement for its implementation. At present, however, there exist software solutions, which simplify the implementation of BPM and shift responsibilities from people to technology.

In Romania, economic entities in the construction field seek to be as competitive as possible on the market by practicing competitive advantages related to price, time, quality, and execution cost, for which they must implement a modern and efficient costing method which, through its contribution, leads to the reduction of operational costs and the practice of efficient management.

This article attempts to examine the implementation of BPM, starting with the design of business processes (determining the conditions of existence and their creation), modeling business processes, implementing the system, monitoring it, and (based on the data provided) optimizing business processes to increase performance.

Moreover, the current study has a twofold purpose. First, we demonstrate how organizations are able to improve their business processes to streamline their activities, and, second, we examine the increase of performance gained by using the target costing (TC) method in a construction project. With the knowledge that the improvement of an organization’s performance is achieved by optimizing business processes, our study tries to highlight the advantages of BPM within a company by using the target cost method.

Finally, this study contributes to the research conducted and presented so far in the identification, monitoring, analysis, control, and improvement of BPM and, through the results obtained, to succeed in resizing the existing information on its application in economic entities in the construction field. During the research activity, we found that there are few materials in the national literature related to the application of business processes within the economic entities of the construction field in Romania.

With this background, this article is structured in the following way: The second section presents the literature review and research methodology. In the third section, the empirical results and discussions are considered, in terms of optimizing business processes and the effectiveness of the target cost method in a construction project. The main conclusions of this research are provided in the final section.

Literature Review

Evolution of BPM

In recent years, the issue of increasing performance has received extensive attention (Wouters & Sandholzer, 2018). The theory suggests that organizations have been trying to identify new ways to increase their efficiency and guarantee the successful execution of critical business processes, to ensure a competitive edge in a particular market (Shafer et al., 2005). There also exist other theories which explain how BPM has evolved to give rise to new concepts such as Enterprise Resource Planning (ERP), Workflow Management (WFM), Enterprise Application Integration (EAI), and Customer Relationship Management (CRM) (Weske et al., 2004).

Using a multifaceted methodological research approach for the quantitative and qualitative collection and analysis of data from approximately 350 senior administrative and IT officers, ECAR conducted a study based on a comprehensive presentation and analysis of information based on business process innovation in higher education. The results of the study illustrated that there exist several common practices in optimizing business processes. The key to success is to establish an institution’s objectives from the beginning, following the project management practices during execution, and assisting and relating to users throughout the implementation process (Pirani & ECAR, 2005).

Organizations can achieve sustainable and efficient improvement of business processes by combining project management and the Six Sigma methodology, which leads to the identification of several opportunities and strategic changes. In other words, it is essential for organizations to combine project management, Six Sigma, and business process optimization to achieve process gains and ensure faster, better, and cheaper products and services while maintaining a high level of market quality (Meyer, 2006).

In an attempt to define BPM, some authors have embedded different visions of BPM into organizations, using technologies and techniques as tools (Antunes & Mourão, 2011; Feng et al., 2019) or technological assessment and capabilities to change existing business processes (Pyon et al., 2011); while other authors have emphasized the synergistic effects created by combining technology and human aspects to redefine existing methods (García-Unanue et al., 2015; zur Muehlen & Indulska, 2010).

Most specialists agree with the idea that BPM is a set of tools and techniques needed to manage business processes efficiently (Huang et al., 2011; Lindsay et al., 2003). Through its use, BPM focuses on two main axes: the first axis is related to the identification, design, implementation, and execution of business processes in an organization (Guinot et al., 2016; Ursic et al., 2005), whereas the second axis is related to the interaction, control, analysis, and optimization of business processes in an organization (Smith, 2003; Vidalakis et al., 2013). As organizations grow more and more, business processes have been becoming more and more complex, and it has become necessary for organizations to focus their attention and efforts to make them more efficient (Rohloff, 2011; Wang & Wang, 2006).

Evolution of TC

Studies on the application of the TC method have been carried out on a global scale. In the United States, specialists have highlighted a very close link between supply management and design function in TC practice (Feng et al., 2018; Hibbets et al., 2003), as well as the involvement of research and development (R&D), supply management, and suppliers in the primary milestones of the target cost method, including the impact of the strategy and the competitive environment (Ellram, 2006).

In Asia, a number of specialists are of the opinion that cost reduction and cost control must be concentrated from the early stages of the product life cycle (Kato, 1993; Sandelin, 2008), involving the engineering function (Gong & Janssen, 2012; Tani, 1995; Tani et al., 1994), while some specialists have supported the strong involvement of managers in planning, development, detailed design, production engineering, product acquisition and sales, absence of financial accounting, simultaneous engineering application, and/or target cost management (Anderson et al., 2004; Huh et al., 2008). In Australia, a vast majority of specialists have discovered poor adoption of the target cost method and its benefits, the impact on the size of firms, culture, and the Australian business environment (Ali & Elazouni, 2009; Chenhall & Langfield-Smith, 1998).

In Europe, specialist studies on the TC method have been expanded since 2000. There are a few aspects which are similar to those found by American or Asian specialists, in terms of cost reduction, early product introduction and customer satisfaction goals, involvement in product development and the creation of design departments, and lack of involvement of the accounting department (Dekker & Smidt, 2003; Rosenfeld, 2009). Compared with Australia, a positive relationship has also been found between adopting the target cost method and competitive intensity, which has the effect of moderating the perceived environmental uncertainty in a negative sense (Ax et al., 2008; Weske et al., 2004). Furthermore, a positive relationship has been found between the adoption of the target cost method and its adaptation to the Romanian accounts plan (Ripoll & Urquidi, 2010).

Method

The adopted research methodology is quantitative and qualitative exploratory research, which was carried out among specialists in the construction field, namely, managers and specialists from 36 state-owned and private companies in Romania. The first category consisted of specialists in the field of managerial accounting (i.e., management accountants) and the second category consisted of company managers (i.e., department heads and senior management).

The method of investigation used was a telephone interview that was conducted by recording the answers to a questionnaire composed of the following four questions: (a) “Does business process management contribute to the efficiency of your company’s activities?”; (b) “What are the benefits of using business process management in your company?”; (c) “What modern costing method do you use within your company?”; and (d) “What are the benefits of the method used to determine costs and achieve performance within your company?”

Depending on the estimated relevance in relation to the research topic, a convenience sample was chosen, consisting of 421 people (385 specialists and 36 managers), according to Table 1.

Centralized Response to Respondents.

Source. Authors’ processing.

The selection of companies was made, according to the following criteria: country/county of origin, field of activity, size of turnover, size of profit/loss, and number of employees.

Results

Description and Analysis of Business Processes

The results indicated that the business process was represented by the set of structured and related tasks, which contribute to the manufacture of a product, the execution of a work, or the provision of a specific service, responding to the need of a particular customer (or customers) in general. As specified by the answers to the first question of the questionnaire, 93.76% of the total number of specialists and 94.45% of the managers of construction companies indicated that BPM contributed to the efficiency of the company’s activities.

At the same time, the centralized answers related to Question 2 of the questionnaire indicated the following advantages of using BPM within the companies: efficiency and flexibility (84.93% specialists and 77.78% company managers), achievement of customer requirements (92.98% specialists and 88.89% company managers), and the development of sustainable solutions (83.37% specialists and 81.25% company managers).

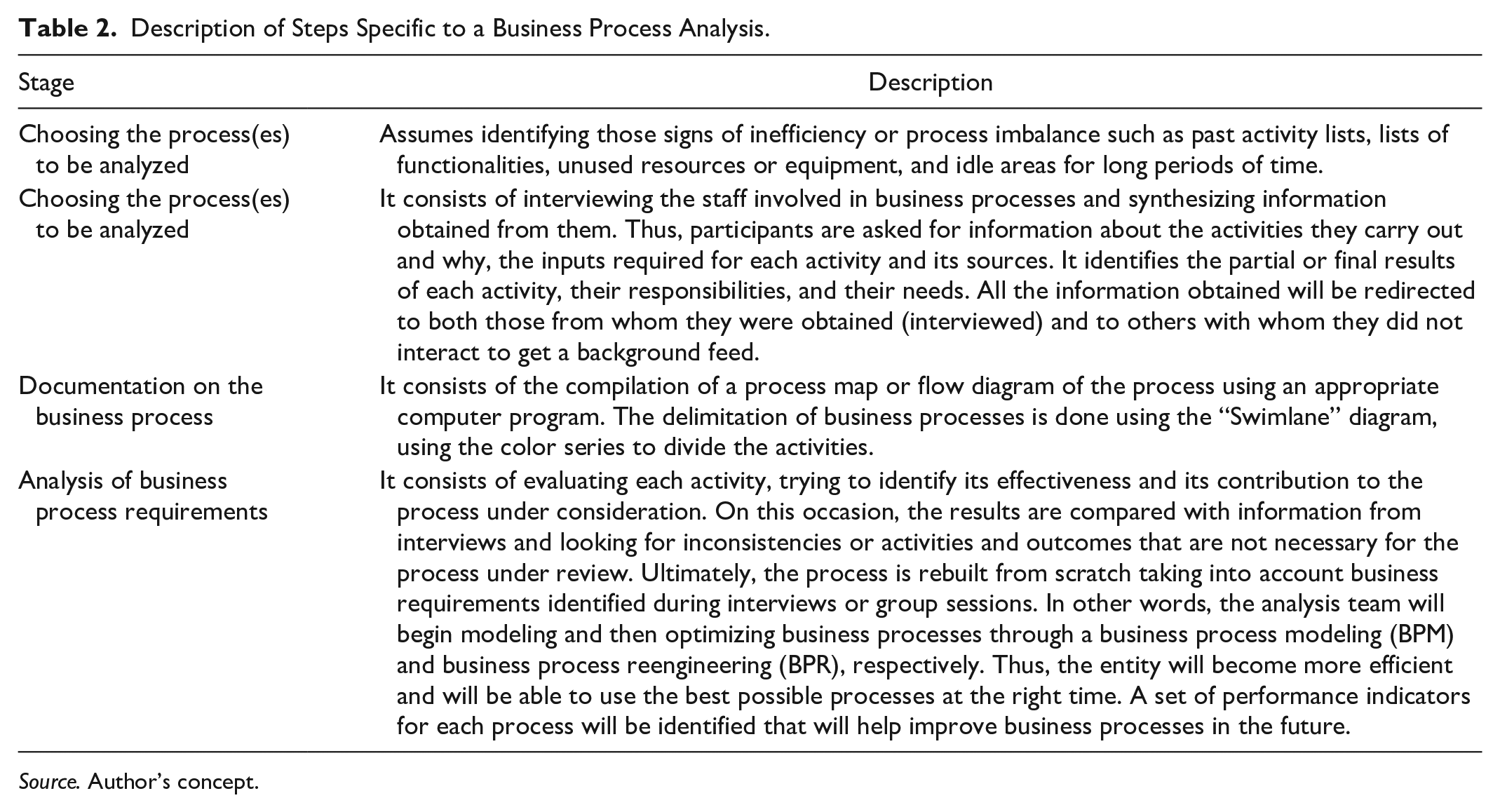

On the contrary, the high degree of competitiveness of an entity depends fundamentally on the degree of structuring, optimization, and the relationship between its processes. If the entity’s management wants lower production costs, lower delivery times, and high-quality work, it must necessarily change its business processes. All issues related to this are centralized and analyzed by the business analyst, who will draw up two business process situations for the entity: the current situation and a desired future situation. The business analyst’s responsibility also includes facilitating, aggregating, and monitoring business processes, while the management’s responsibility is only to provide the information necessary to guarantee the entire process. Ensuring success on the line of optimizing business processes can translate into permanently optimized internal processes (i.e., procurement and distribution processes) or through a continuous improvement methodology. In detail, the analysis of business processes is carried out in four stages, as shown in Table 2.

Description of Steps Specific to a Business Process Analysis.

Source. Author’s concept.

For the analyzed entity, the following three business processes were analyzed: (a) Bidding–assignment of construction projects, (b) Budgeting the costs of the construction project, and (c) Execution of the construction project.

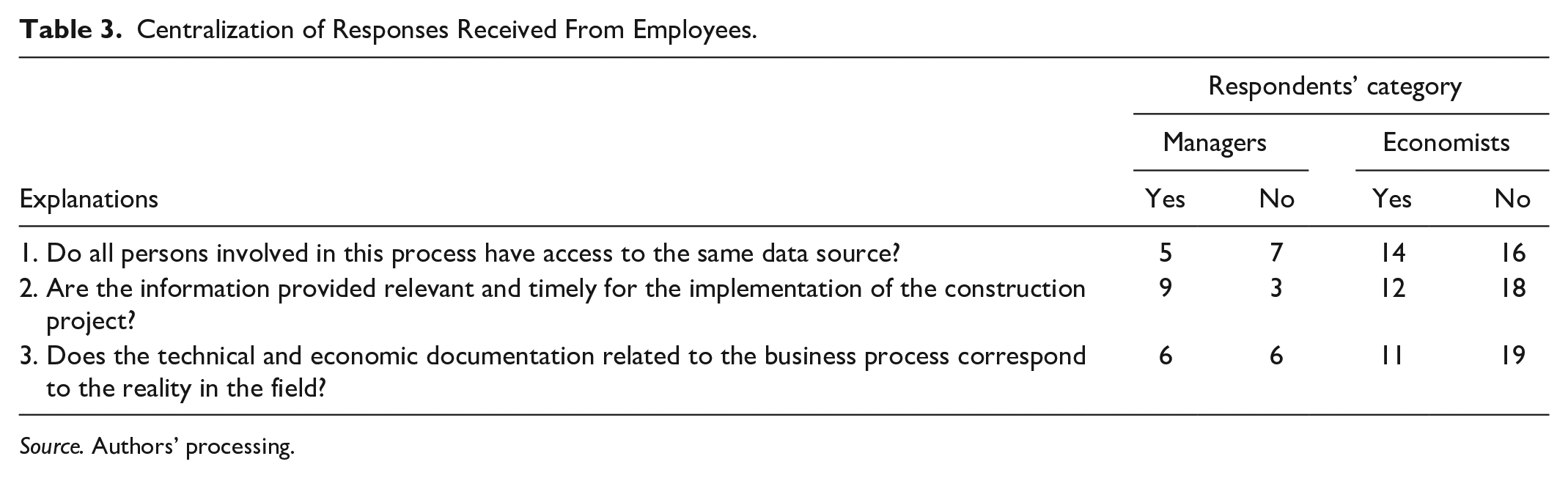

To improve the entity’s performance and improve its business processes, it was considered necessary to thoroughly analyze the business process called “Building Costs of the Construction Project.” This is due to the detection of inefficiencies related to (a) the lack of coordination between the entity’s technical and commercial parts; (b) inefficient selection of employees, not respecting certain purchasing principles; and (c) lack of cost-effective cost management. The centralized responses of the 42 employees (12 managers and 30 economists) who were interviewed by a series of three questions are presented in Table 3.

Centralization of Responses Received From Employees.

Source. Authors’ processing.

After conducting the survey and communicating the results, a brainstorming session was also carried out, which helped explain to economists aspects such as: (a) identifying access to the database, (b) the relevance and updating of the data provided to managerial accounting and management control, and (c) identifying weaknesses in the elaboration of technical and economic documentation related to managerial accounting and management control. All information and findings were communicated both to the participants of the interview and to the project implementation team using the target cost method. The bidding–awarding process for construction projects is composed of two main activities: tender and management. The flow diagram of this process is shown in Figure 1.

Activities diagram of the business process: Assignment-offering construction project.

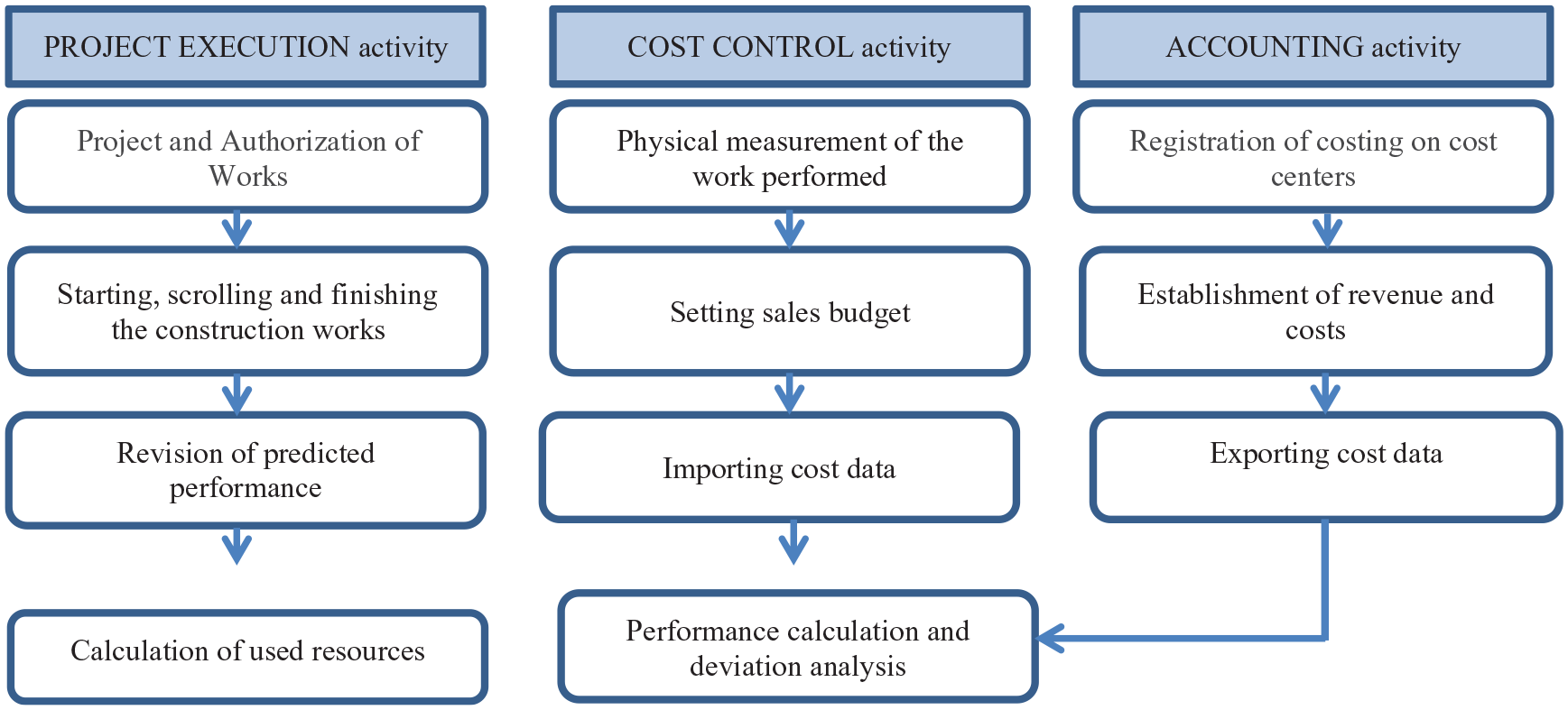

In the cost budgeting of the construction project process, three activities are carried out: budgeting itself, cost control, and accounting. The flow diagram of the cost budgeting in a construction project process is presented in Figure 2. The specific operations of the budgeting activity include progress of control over the basic program, calculating the remaining time, revising the predicted performance, calculating the resources used, and approving the processed data. The specific cost control operations are as follows: physical measurement of the work performed, establishing the sales budget, importing cost data, calculating performance based on data, analyzing deviations, estimating the actual work, and calculating final bends.

Activities diagram of business process: Costs budgeting of the construction project.

The construction project execution process consists of three activities: project execution, cost control, and accounting. Among the project-specific operations shown in Figure 3, we mention the project and authorization of the works; the start, run, and finish construction works; revision of the predicted performance; and calculation of the resources used. The following operations can be delimited in the accounting activity: the costing of cost centers, determining income and costs, and exporting cost data.

Activities diagram of the business process: Execution of the construction project.

On the basis of the business process chart, two operations have been identified that have proved to be ineffective in carrying out the whole process: approving the processed data, and processing and interpreting the data. After analyzing the two operations, the business process analysis team decided to eliminate them, and the new chart of the business process activities is presented in Figure 4:

Activities diagram of the business process: Costs budgeting of the construction project after the analysis carried out on it.

BPM is a management approach centered on adapting an entity’s activities to the growing needs and diversification of customers (Chan et al., 2011). This approach is based on the flexibility and integration of computer applications which help to increase the efficiency of the economic entity, leaving a free horizon for innovation. The most important aspect is that of helping to reduce operational costs by automating operations with the help of software programs, by attracting information from a process to understand, streamline, and remove intermediaries from it (Moselhi & Hassanein, 2003; Yilmaz & Baral, 2010).

Using the Cost Target Method to Continually Reduce Operational Costs

As part of the cost management function, the target cost method tracks the lifetime cost. Once the cost is established, it must be met—meeting the customer’s requirements by using cost-cutting methods. Entities often resort to changes in product design or structure that allow them to flexibly adapt to customer requirements while optimizing their business processes. By optimizing business processes to reduce operational costs in a construction project, there is an increase in performance, as evidenced by the target cost method.

To achieve the two objectives under consideration, a construction entity was chosen to carry out construction works; namely, building a bridge over a river linking two cities. As an additional check, centralized answers to the third question in this study indicated the target cost method as the most-used method among those mentioned (77.14% specialists and 83.34% company managers). Even so, the answers to the fourth question suggested the following benefits of the accounting method used: reduction of operating costs (96.10% specialists and 83.34% company managers), profit maximization (84.41% specialists and 94.45% company managers), and obtaining reliable information (87.27% specialists and 75% company managers).

According to the data gathered, the construction work received all necessary approvals and its development was planned in three phases: launch (start), growth (extension), and maturity (finalization). During these three phases, the constructor sought to obtain profit margins based on the turnover set at each phase of the construction project. Based on the data obtained from the economic entity analyzed, the information is presented as follows (Tables 4–6).

The Situation of the Target Turnover, the Target Cost, and the Target Profit Margin.

Unit Cost Targeting by Components and Phases.

Cost Status (Actual and Target) by Components and Phases.

Discussion

In an uncertain economic environment with strong competition, cost control is a crucial component of the strategies of Romanian entities. The main objective of this study was to investigate how, in a construction project, the Romanian economic entities in the construction field, with the help of the target cost method, can ensure and determine the operative processing of data, information on the cost of the construction project, and the establishment of optimal information indicators necessary to substantiate decisions for the efficient management of activity in the construction field—in other words, to optimize the business processes to streamline their activities.

Unsurprisingly, taking our results into consideration, managers are generally preoccupied by constant issues such as understanding the future and managing the activities of others. Indeed, to understand the future, managerial accounting is tasked with identifying the connections between the goals pursued and the resources engaged to obtain them.

Nevertheless, the business process can be visualized using a flow diagram to represent the business activities, which includes decision nodes, thus helping to improve them based on the definition of how an entity adopts an activity. As a consequence of this, the activities of a selected entity can be divided into processes and, based on this, a process map can be compiled. As a result, business process analysis addresses several objectives, such as: (a) understanding the way business processes work together, (b) understanding the needs of intermediate or final user groups, (c) determination of the purpose and objectives specific to each business process, (d) identifying the occurrence of process-specific problems and their causes, and (e) identifying those optimal conditions for improving business processes and their application.

In relation to activities, the findings also demonstrate that managerial accounting must provide the manager with the information which is absolutely necessary to help them understand the phenomena and the processes taking place in the economic entity, that is, the real information based on which the manager can make pertinent decisions, can foresee the consequences of their decisions, and have, at their disposal, the levers needed to exert constant and efficient control.

This study shows that cost–production–profit analysis is one of the most important instruments available to managers. This analysis helps them to understand the connections between costs, production volumes, and profits in the company they are managing, based on the interactions between variable unit costs, fixed costs, product costs, and the volume of activity.

Based on these findings, it can be reflected that highlighting the performance of an analyzed entity is done using a scorecard centered on profit, cost, and income indicators. Accordingly, the entity records a profit margin in each of the three construction steps, although the actual target costs exceeded the estimated target costs. These deviations were due to increased costs for some unanticipated works and minor delays in completing them.

Compared with other current research (Alavipour & Arditi, 2019; Chatzipetrou, 2018), the originality of our study consists in combining several different points of view and analyzing them from the perspective of improving business processes by using Swimlane graphics in their design. This improvement of business processes through Swimlane graphics helps organizations to reduce operating costs by practicing the target cost method (based on Kaizen Costing or continuous cost reduction) and increasing its financial performance. Through this contribution, we consider that the two objectives set for the purpose of our research have been met.

Conclusion

It can be said that the analysis of business processes can sometimes be technical, but only in the exclusive responsibility of the management of the economic entity and of the business analyst. Thus, the analysis of business processes helps to identify inefficiencies and establish the necessary corrections, which can help to reduce costs and improve the quality of process results.

In particular, this article shows that BPM is continually improving and optimizing to deliver high performance and flexibility in gaining competitive advantage. By using the TC approach in the continuous reduction of costs, it can be ensured that one can achieve high performance and gain a competitive advantage in a particular market or market segment. Entities are free to choose those tools that can bring added benefits and help them to permanently adapt their offer to customer needs.

According to the results of this study, both specialists and business managers (in a very large proportion) agree that BPM contributes to streamlining their activities by using modern managerial accounting methods and benefiting from the advantages offered in the long run.

From a practical point of view, the results of this research translate into the effects on the efficient implementation of the target cost method in a construction project based on the data provided—in other words, the optimization of business processes to increase performance.

From a theoretical perspective, this research has demonstrated the importance of modeling and optimizing business processes through the BPM technique, such that a company can become more efficient and use the best possible processes at the right time.

We have also attempted to understand how the complexity of the economic life under market economic–competitive requirements has determined the increasing role of information in decision-making processes. The quality of current and long-term decisions and, implicitly, the results obtained depend on the quality of the information.

Our contribution serves to provoke new attempts to adopt or implement the TC method and, thus, opens up new perspectives for future research. This study remains open to future theoretical and empirical research, as well as additions made by the target cost principles and their hybridization with other management accounting methods. The identification of viable and sustainable solutions depends only on the degree of involvement of specialists and managers in identifying empirical practices at an institutional level, thus guaranteeing the efficiency of the implementation of the target cost method. Developing partnerships between academia and interested business organizations and collecting necessary information can help to expand the theoretical–empirical framework of the target cost method and identify robust solutions for implementing and guaranteeing success in business environments.

In conclusion, it can be said that the analysis of business processes is sometimes technical; however, it is not the sole responsibility of the management of the economic entity (e.g., in the construction field) but also of the business analyst. Business process analysis helps to identify inefficiencies and to establish the necessary corrections, which can help in reducing costs and improving the quality of process results in a construction project.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.