Abstract

This study aims to examine the causal and long-term effects of domestic finance, political risks, and global risk on domestic economic risk in QISMUT countries, namely Qatar, Indonesia, Saudi Arabia, Malaysia, UAE, and Turkey, covering the period of 1997Q1 to 2015Q2. The study used the threshold cointegration test, which involves Gregory and Hansen Cointegration and Hatemi-J Cointegration tests. The tests endogenously combined possible regime shifts in the long-run relationship of the underlying variables. Our results reveal (i) the presence of cointegration among the time series variables with endogenous structural breaks. The linear Toda-Yamamoto causality and nonlinear—Diks and Panchenko and Hatemi-J—causality test shows (ii) changes in domestic financial risk significantly lead to changes in economic risk in the QISMUT countries; (iii) domestic political risk causes economic risk in Indonesia, Qatar, Saudi Arabia, UAE; (iv) global risk affects significantly on economic risk in Saudi Arabia, Turkey, and UAE. Critical policy intervention could include governors in the QISMUT countries should control financial stability indicators such as domestic and foreign debts, exchange rate, and liquidity problems to control macroeconomic dynamics in their respective markets.

Keywords

Introduction

From the post-war period up until now, the biggest challenge faced by both developed and developing markets is the global crisis of 2007 to 2008 (Cassette & Farvaque, 2014). Surprisingly, Islamic banks were less affected by the global crisis than conventional banks (Hamid et al., 2017; Hasan & Dridi, 2011. Islamic banks and generally Islamic finance have also gained the attention of scholars. Hasan and Dridi (2011) found that the asset and credit performance of the Islamic banks in the QISMUT countries, namely Qatar, Indonesia, Saudi Arabia, Malaysia, the United Arab Emirates, and Turkey, was much better relative to conventional banks during the global crisis period of 2008 to 2009. Though many economists are focusing mainly on the studies of economic development, economic growth, economic risk, and economic volatility issues, in the literature, there are very few studies conducted upon Islamic finance and especially QISMUT countries. In other words, to the best of our knowledge, no study has comprehensively investigated the effect of domestic finance, political risks, and global risks on domestic economic risk in the QISMUT countries by threshold cointegration tests and nonlinear causality tests. These countries are, selected because they are the top six Islamic countries, with remarkable rapid-growth countries (RGMs), also categorized as fast-growing countries in terms of the size of the economy, economic growth, population, and global business activities (Yildirim, 2015). Furthermore, each one of them has its own individual dynamics, such as a diversity of regulatory and supervisory responses, including Shariah-compliant government guarantees on bank exposures and payment moratoria (IFDI, 2020) to some extent. Malaysia’s Islamic banking assets, the largest Islamic financial hub in the Asia-Pacific region, account for approximately 9.6% of the total Islamic banking assets; Indonesia, within the world’s largest Muslim population, has a share of only 1.39%, Saudi Arabia, the leader in Islamic finance, has a share of 18.57%, The United Arab Emirates, located in the Gulf region, is a major player in the Islamic banking sector with its 7.36% share, Qatar, the other Gulf Arab state, has a share of 4.47%, while Turkey’s is 3.20% (Comcec, 2017).

Ernst and Young’s (2016) study has highlighted that the QISMUT countries are expected to lead the growth of Islamic finance shortly. Currently, around 80% of the total Islamic banking asset located in QISMUT countries and their competitive power in these countries have been enhanced within their rising market shares. These countries may be positioned as a forerunner of the growth cycle in the present and future markets of the region. It is widely accepted that the economies of the QISMUT countries, to some degree, deal with the harmful waves of the global crisis in the world as compared to the other emerging markets (Al-Malkawi & Pillai, 2018).

One of the underlying reasons Islamic banks are less affected is the differences between Islamic banks and conventional banks. The principal dissimilarity can be summarized as; the lower leverage and the prohibition of short selling and derivatives trading in the Islamic capital market. Also, the interest rate and excessive uncertainty are prohibited according to Islamic finance regulations. As well as equity-based financing, asset-backed securitization has a favorable influence on economic growth. Furthermore, one of Islamic finance’s visions, to divvy the risks of economic and financial processing by Islamic instruments, helps maintain the financial system’s stability. Channeling the funds to the real sector, instead of to the financial sector, to protect the economy from being over-financialization helps the economy’s growth (TKBB, 2016). The rapid rise in the transaction activities of the Islamic financial sector can be seen from the Islamic finance assets growths—from 1,761 USD Billion (2012) to 2,875 USD Billion (2019) (IFDI, 2020). The question may arise, how Islamic finance has grown so far. According to the global Islamic Finance Development Indicator, henceforth (IFDI), the indicators to be the principal drivers of progress in the sector are; Corporate Social Responsibility, Governance, Quantitative Development, Knowledge, and Awareness (IFDI, 2020). Due to the study’s limited scope, we will focus only on these indicators’ outcomes as the risk levels on global economic risks in these countries. Also, it should be taken into consideration that, within the deepening of the Islamic financial sector, numerous already excluded Muslims, due to their religious beliefs from the formal banking activities, started to take part in Islamic banking transactions (TKBB, 2016). Also, as the Islamic banking finance growths rise, questions arise about; how the financial market’s development affects Qismut countries’ economic growth and as it’s still growing, do they need reforms or policy and can their regulatory be a leading financial aid to the other developing or developed countries. The aim to try to find these answers motivates us to investigate the economic conditions in the QISMUT countries.

Despite the contribution of these countries to financial and economic stability over a decade, surprisingly, a minimal number of studies have focused on the QISMUT countries’ economies. Thus, it turns out to be essential to assess the relationship between domestic financial risk, political risk, and global risk on domestic economic risk in these countries. The distinctive contribution of this study to the literature is to fill the gap in economic literature by performing threshold cointegration tests. This econometric technique allows us to capture the long-run equation between economic risk and financial risk, political risk, and global risk. Also, the study performed linear and nonlinear causality tests to measure the possible effects of domestic risks and global risk on the economic risk of the QISMUT countries.

Our empirical outcome supports the hypothesis of Schumpeter, revealing that domestic financial risk has an impact on the economic risk, in other words, on the economic growth of the QISMUT countries. In addition, domestic political risk leads to economic problems such as economic risk in Indonesia, Qatar, Saudi Arabia, and UAE. Furthermore, another important risk, global risk, less discussed in the literature, causes prominent impacts on economic risk in Saudi Arabia, Turkey, and UAE. Overall, our results could prospectively open a new discussion on the topic in the economics literature, specifically for the QISMUT countries, which highlights remarkable implications for policymakers in these countries.

The rest of the study is structured as follows: Section 2 presents a literature review, which provides a detailed argument of the existing literature. Section 3 discussed data and methodology, while section 4 presents the empirical findings. Finally, section 5 provides concluding statements and future study suggestions.

Literature Review

Relationship Between Economic Growth and Financial Development

Schumpeter (1912) initially put it forward that financial development facilitates economic growth in the early literature. In the following years, Gurley and Shaw (1955), Goldsmith (1969), and Shaw (1973) provide significant supportive findings to the finance-led growth hypothesis. The nexus between economic growth and financial stability has gained great attention both by scholars and policymakers. This information has a great significance, especially for the monetary policymakers, to conduct strategies to maintain financial stability (Alsamara et al., 2019) in their countries.

King and Levine’s (1993) study noted that the inverse stream of causality from financial development leads to economic growth. Waqabaca (2004) examined the relationship between economic growth and financial deepening using the Granger causality test and vector autoregression in Fiji. Odhiambo (2008) used the Granger causality test to make final reports about the growth led by finance in Kenya. Zang and Kim (2007) went further to decide whether the one measured in Kenya applies to other East Asian countries; they used the Sims-Geweke causality technique to make this conclusion. Furceri and Mourougane (2012) argued that the disturbances created in the credit market, coupled with the losses of significant credit institutions, are the primary causes of the economic slowdown. Based on this, Siddiqui and Ahmed (2013) strongly believe that the confidence in financial institutions to meet their financial obligation declined drastically. The study by Cournède and Denk (2015) noted that decreasing financial risk via financial development accelerates the credibility of the loans for investors and then leads the economic growth in the long run. Madsen and Ang (2016) find a piece of supporting evidence for the finance-led growth hypothesis in 21 OECD countries. As such, this led to an upward trend in political, economic, and financial risks, and these variables experienced a high level of volatility during that period. This kind of risk has given rise to stunted economic growth and creates an environment of economic fear. Within the aim of investigating the nexus amid economic growth and financial stability, Alsamara et al. (2019) analyzed the banking sector’s stability in Qatar over the period 1980:Q1-2013:Q4, utilizing a Vector Error Correction Model (VECM) with structural breaks. The outcome reveals that economic growth negatively influences the long run but a moderately positive impact in the short run on real loan provisions. Similarly, a more recent study of Kirikkaleli (2019) investigates the causal link between financial risk and economic risk, for the case of Greece, from 1990 to 2018, using the wavelet coherence technique. The study finding supports the Schumpeter hypothesis within the risk perspective, categorically, pointed out that financial risk causes economic risk in Greece at different frequency levels. In an effort to find evidence to whether financial development stimulates economic growth or economic growth improves the development of financial markets, Chazi et al. (2020), analyzed data for 28 industries in 14 countries within dual banking systems (Islamic and conventional banks. The finding reveals that the relative size of Islamic banking, faith-based banking, has a positive influence on the growth of industry, then on the economic growth.

Relationship Between Economic Growth and Political Risk

One of the most common perceptions over the years is the argument of applying populist policies. The populist policy ideologies continue to influence the general economy; their efforts to increase their votes are reflected their ideologies on economic policies. With this view, it is interpreted that the macro performance of an economy is subject to fluctuations caused by political instability. Besides, a nation’s long-term positive economic performance is a probe sign of political stability or an important indicator to simulate local and foreign investors whether to make their investments or not; thus, these indicators are essential for the sustainability of economic growth. Olson (1963), Ades and Chua (1997), Julio and Yook (2012) are among the studies that have studied political uncertainty on economic instability. For instance, an empirical study by Olson (1963) shows that political instability is associated with diminishing economic growth. The result of this study shows that political stability is positively related to economic growth.

Similarly, Ades and Chua (1997) and Julio and Yook (2012) support the effect of political instability on economic output and underline the importance of political vulnerability on the country’s investment profile. The level of investment risk is highly dependent on the uncertainty of state conditions, and this uncertainty is reflected in the investment cost as an additional cost. The study by Tabassam et al. (2016) on Pakistan’s economy via utilizing ARCH and GARCH models included by outlining four important indicators that directly affect the country’s economy, namely terrorism, election, regime change, and strikes action- to measure political instability. The study shows that only terrorism has a significant adverse effect on the vulnerability of Pakistan’s economy. Besides the result of this study, scholars and policymakers should also show that political risk takes many forms. Political risk comes from the view from the terrorism and military coups and in the form of new national legislation, new governments, and changes in a country’s ruling party (Ramady, 2014).

Allen and Wood (2006) underlined political risk as one of the highly considered factors to determine market risk premium in the economy and an essential factor in investment decisions. This study explains the differences that exist in stock returns between different countries and light how political risk causes a decline in the level of economic growth, a rise in the level of inflation and unemployment, depreciation in the exchange rate, and a rise in domestic public debt. Allen and Wood (2006) also noted that political risk has an indirect effect on economic risk by first affecting the financial risk factors, which directly affect economic risk. The recent studies by Karnane and Quinn (2019), Abu Murad and Alshyab (2019), Sweidan (2016), Okafor (2017), and Acemoglu et al. (2019) have investigated the effects of democratization and corruption on the country economy. The study of Karnane and Quinn (2019) utilized a panel data set of 157 countries covering 1996 to 2014 to investigate the influence of ethnic fractionalization and corruption on economic growth. The evidence shows that ethnic fractionalization and corruption inversely influence economic growth. Acemoglu et al. (2019) study highlighted that democratizations increase GDP per capita by about 20% in the long run. However, this study noted that despite the positive effects of democratization has on the country’s economy. It does not influence significant political change within the different development levels of countries. This finding was solidified by evidence from Sweidan (2016), Okafor (2017), and Abu Murad and Alshyab (2019) several studies. They reported that political risk always slows down economic growth in many countries. In other words, these studies can be interpreted as economic risk is affected by political risk.

When conducting the risk analysis, one should consider the country’s risk in economic and policy risks. The political factors that give increment to certain economic policies, in other words, the interplay of economics and politics, should be considered. Also, the country’s risk is affected by monetary, fiscal, or subsidy policies and a variety of other issues like regulatory restrictions, alterations in labor laws, and requirements for national economic contents (Ramady, 2014). And several studies considered a country risk when analyzing the economic and political performance of the analyzed countries. Ahmad and Ariff (2008), Song et al. (2019), Duval et al. (2020) studies focused economic performance of OECD and G20 countries and emerging markets like China and India and other developed countries. The study suggests that diversification and portfolio management within the G20 may be the right choice for handling potential country risk. Kirikkaleli (2016) study highlighted the relevance of financial sector development by investigating the linkage between country risk indicators for seven Balkan countries. The study performed the econometric analysis of the Pedroni cointegration test, FMOLS, DOLS, and causality tests, respectively. The findings reveal a positive relationship between economic stability and financial stability in the long run.

The Nexus Between Economic Growth and Global Risk

Apart from the impact of the political and financial stability on the economic stability in many countries, very few studies have focused on the effect of global risk factor that affects the others. No matter how resilient a country’s economy may be, there will always be global risk factors that threaten to derail economic growth. Rodrik (2012) underlined that “policymakers need to guard against not just domestic shocks, but also shocks that emanate outward from financial instability elsewhere”. The empirical study by Li et al. (2012) explores the spillover effect of the 2007 to 2008 global crises on the Chinese economy. The underlined that despite the dramatic reduction in Chinese export during the global crisis, the economic growth performance of China remained more robust and above the international average. Stockhammar and Österholm (2016) paper utilized Bayesian VAR models and spectral analysis to investigate Sweden’s economy, covering 1988 to 2013. Results found that the Swedish economy was adversely affected by US policy uncertainty. Finally, the recent study by Kirikkaleli and Onyibor (2019) investigated the financial and political risks on economic risk in the Southern European countries, considering the 2008 to 2009 global financial crises as the global risk. Results show that political risk has created economic vulnerabilities in Southern European countries.

Contrary to the consideration of the Schumpeter hypothesis, Chandavarkar (1992), Rousseau and Xiao (2007), and Pradhan et al. (2013) studies find supportive evidence of the neutrality hypothesis. These studies’ results show that there is no significant causality between economic growth and financial development. Rousseau and Xiao (2007) argue that the influence of banking sector development on economic growth is much more significant than the stock market development in China for the years 1995 to 2005. Cecchetti and Kharroubi (2012) analyze the relationship between the two variables for 50 developed and underdeveloped countries and found similar results to earlier studies, concluding that financial development does not accelerate economic growth. The early studies by Rousseau and Wachtel (2002), Law and Demetriades (2006) showed that “expanding financial instruments and developing financial systems do not play a significant role in fostering economic growth” (Kirikkaleli, 2016). However, the recent study of Asteriou and Spanos (2019) offers a different perspective, such as the relationship between financial development and economic growth may change over time, especially at the pre and during the global crisis period. As evident from the literature, there is no consensus about the possible causal relationship between economic growth and financial development; therefore, this study models economic risk in the QISMUT countries is considered as the gap in the literature. The next section presents data and methodological used in this paper.

As seen in the literature review, there are plenty of studies in the empirical literature on economic growth, with or without the variables as financial development, policy risk, and country risk of a country or across many countries. However, the causal and long-term effects of domestic finance, political risks, and global risk on domestic economic risk in QISMUT countries have not received enough attention. Only a few studies have been conducted to compare the financial performance of the Islamic and conventional banks operating in the QISMUT (Faizulayev et al. (2020) and/or member of Gulf Council countries. Faizulayev et al.’s (2020) study investigate the profitability determinants and profit persistency of both banks in QISMUT countries and Bahrain, Kuwait, and Pakistan as Islamic finance-oriented countries. The findings show that (i) profit persistency of Islamic banks, henceforth, (IBs, is higher than conventional banks, henceforth, (CBs), (ii) For CBs, the bank capitalization, risk behavior have more importance, (iii) profitability determinants of both banks are distinct. Including same countries, shortly, QISMUT + 3, Probohudono et al. (2021) search the influence of corporate social responsibility on these countries’ Islamic banks’ financial performance by utilizing the Islamic Social Reporting Disclosure Index (ISRDI). The outcome demonstrates that the financial performance has positive impacts on ISRDI for the UAE, Turkey, and Kuwait. These studies generally focus on the nexus between the economic and financial development in the countries with dual banking systems but only considering partial sides of the risk components. Therefore, new variables and empirical models should be conducted to fulfill the literature gap in this area of research.

Data and Methodology

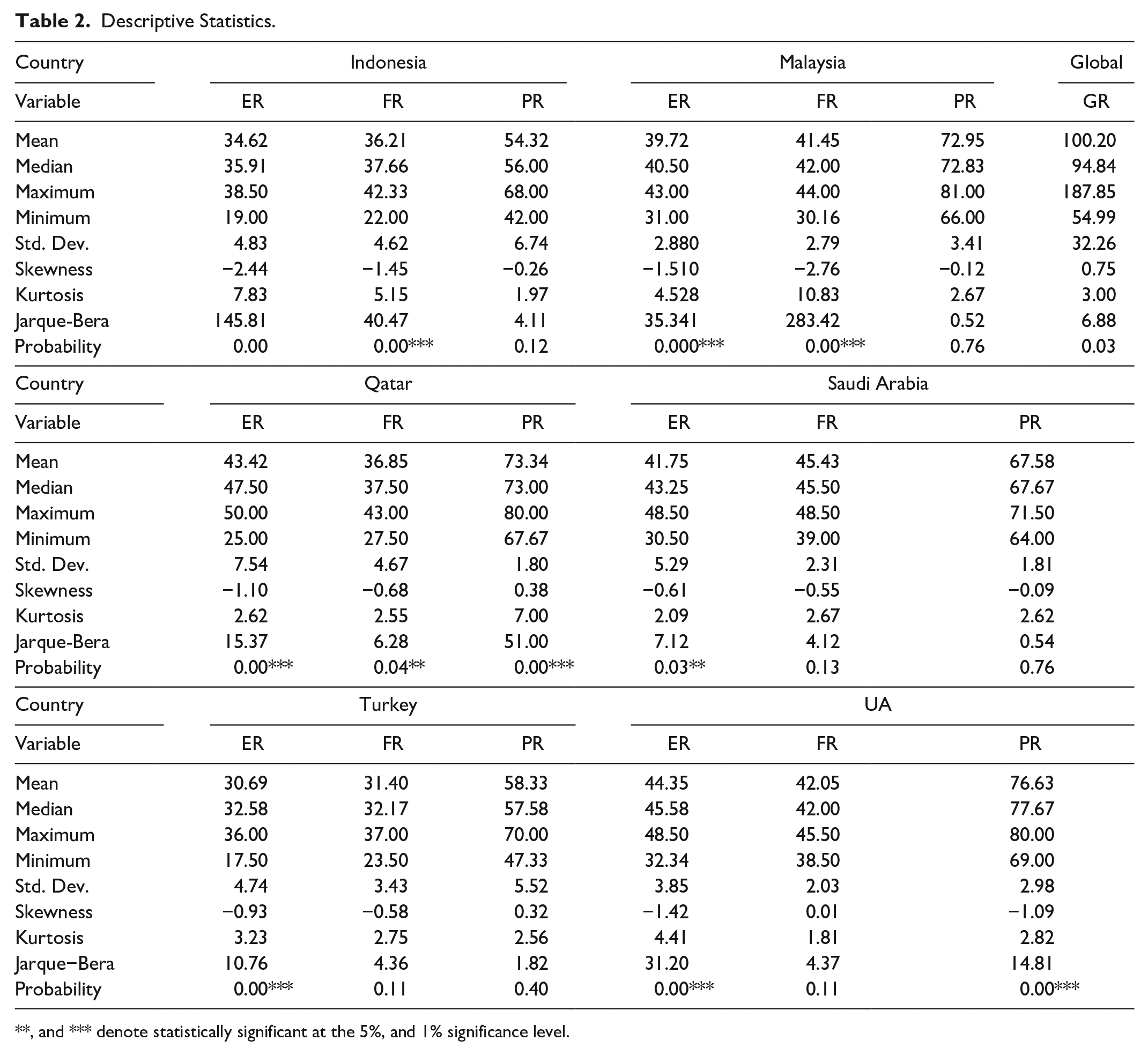

For this paper, we apply nonlinear cointegration tests to examine the effect of economic risk in the QISMUT Countries covering the period 1997Q1 to 2015Q2. Table 2 presents descriptive statistics of variables employed. These variables include economic risk (ER), financial risk (FR), political risk (PR), and global risk (GR). We collect ER, FR, and PR from the Political Risk Services (PRS) Group (see, http://www.prsgroup.com), while the global economic policy uncertainty index (see, http://www.policyuncertainty.com) is gathered from Economic Policy Uncertainty (EPU) and used as a proxy for global risk in this study. Since the present study employs a risk-based dataset, we used a non-seasonal adjusted dataset (see, Table 1).

Definition and Explanation of Variables.

Descriptive Statistics.

**, and *** denote statistically significant at the 5%, and 1% significance level.

The present study uses Global Economic Policy Uncertainty as a proxy for global risk. “The index is a GDP-weighted average of national EPU indices for 21 countries: Australia, Brazil, Canada, Chile, China, Colombia, France, Germany, Greece, India, Ireland, Italy, Japan, Mexico, the Netherlands, Russia, South Korea, Spain, Sweden, the United Kingdom, and the United States. Each national EPU index reflects the relative frequency of own-country newspaper articles that contain a trio of terms pertaining to the economy (E), policy (P), and uncertainty (U). In other words, each monthly national EPU index value is proportional to the share of own-country newspaper articles that discuss economic policy uncertainty in that month.”

Figure 1 shows the economic risk index of QISMUT countries. The pattern of these countries in Figure 1 supports their sound economic and financial performances in the last two decades. Although the QISMUT countries found themselves in a position of very high risk to moderate risk in 1997, in 2015, the economic environment of these countries ranged between low risk and slight risk. According to the PRS Group dataset analyzed in this study, the economic environment of Malaysia, Saudi Arabia, Turkey, and UAE are negatively affected by the 2007 to 2008 global crises in the short run.

Economic Risk Index in the QISMUT countries.

As an initial approach, we employ the BDS test of Broock et al. (1996) to detect the nonlinearity in the time series variables. As a next step, the unit roots of the ER, FR, PR, and GR variables are captured in the QISMUT countries by using the Zivot and Andrews (2002) unit root test. Traditional unit root tests suffer from capturing possible structural breaks that are known to plague most financial and economic time series. In addition to Zivot and Andrews (2002) unit root test, the present employs the Fourier ADF unit root test (developed by Enders & Lee, 2012) which is more powerful under the unknown number of breaks while considering nonlinearity.

Since the time series variables have the same order of integration, I (1), we checked the cointegration relationship as a next step. Conventional cointegration methodologies assume that the cointegrating relationship remains constant during the selected period of the study by ignoring the existence of structural breaks in long time-series data. Economic crises, external shocks, policy changes, and technological shocks can be given as an example for structural breaks, which can change the long-run relationship among the variables, so it should be taken into consideration for the reliability of the analysis (Ghosh & Kanjilal, 2016). One of the cointegration tests that sensitive for the structural break is developed by Gregory and Hansen (1996), who allows for the possibility of regime shifts because of one endogenous structural break. In other words, Gregory and Hansen’s test allows structural changes in the parameters of the cointegrating relationship under three alternative hypotheses: The first one is; a shift in the intercept (represented in equation (1)), second one: a shift in the intercept and the trend (represented in equation (2)) and last one is: a shift in the intercept and the slope coefficient relationship (represented in equation (3)) (Caporale et al., 2015). The first model shown below involves a shift in the intercept as follows;

The second form of the Gregory and Hansen’s cointegration test accommodating a trend in the data also limits shifts to changes in level with the trend can be expressed as;

The most popular model of the Gregory and Hansen’s cointegration test is the one that allows for changes in both the intercept and slope of the slope coefficient relationship as follows;

In the model, the structural changes are determined by the dummy variable which, is represented as

Where (0, 1) is a symbol of the relative timing of the change point. According to Andrews (1993), the trimming interval generally is taken to be (0.15n, 0.08n). The models are performed with a structural break over the interval s (0.15n, 0.08n) in equations (1)–(3). Gregory and Hansen (1996) used three error-based tests: the ADF test and Za, Zt tests to estimate the hypothesis of no cointegration for its regression errors. They underlined that using these tests to the regression residuals is likely to cause the misspecification of cointegration if the time series variable contains unknown structural breaks. Therefore, Gregory and Hansen (1996) developed bias-corrected modified ADF, Za, and Zt tests for estimating the cointegrating equation among the time series variables. More recently, Hatemi-J introduced a test which counts in two possible endogenous regime shifts in the cointegrating relationship. Both Gregory and Hansen Cointegration and Hatemi-J Cointegration tests are known as threshold cointegration tests. Hatemi J’s (2008) test is an extension of Gregory and Hansen’s (1996) test (Ghosh & Kanjilal, 2016), therefore while capturing the cointegration equation between economic risk and financial risk, political risks and global risk in QISMUT countries, both tests are employed in the present study.

The present study aims to capture the causal effects of domestic financial and political risks and global risk on domestic economic risk in QISMUT countries. Based on this aim, linear—Toda and Yamamoto—causality and nonlinear—Diks and Panchenko and Hatemi-J—causality tests are employed. In a pioneer study, Granger (1969) developed a traditional causality test called the Granger causality test to investigate the short-term causal linkage among the time series variables. The idea is that X t does Granger cause Y t , if and only if the variable X t can be explained better by using the past values of both Y t and Xt, rather than just by using the historical values of X t . In essence, this test allows us to investigate whether the past values of Y t can improve the prediction of X t or not. Despite some shortcomings of the Granger causality criterion, it has been a popular tool in empirical investigates. The general equations of the traditional Granger casualty test for the X and Y variables are shown below;

Where n denotes the number of lags in the models, and the SIC information criterion is used to select the number of lags of the models. In equation (5) and (6) β1–2, α1–2, and m1–2 indicate parameters for estimation, whereas et is an error term of the models.

Linear causality test is used to examine the dynamic relation between domestic financial and political risks and global risk on domestic economic risk in QISMUT countries. In this paper, we apply the Toda and Yamamoto causality test, which is proposed by Toda and Yamamoto (1995). When working with data that are not stationary, the usual Wald test becomes invalid. Therefore, the test statistic under the null hypothesis does not have its usual asymptotic Chi-square distribution. However, Toda and Yamamoto (1995) procedure can be applied for the nonstationary time series variables (Rahimi et al., 2016). Besides, Toda and Yamamoto’s approach can overcome the singularity problem, which occurs in the traditional causality test by augmenting the VAR model with the maximum integration degree of the variables.

Moreover, the Toda and Yamamoto procedure does not need to test cointegration relationships and estimate the vector correction model. The Toda and Yamamoto causality test is robust to the data’s unit root and cointegration properties (Nazlioglu, 2011). In the classic analysis, a VAR (p) model estimation, where p is the optimal lag length(s), is required. Nevertheless, in the Toda and Yamamoto approach, estimation is required for the VAR (p + d) model, where d is the maximum integration degree of the variables (Nazlioglu, 2011). It can be express as in equation (7).

Where yt is a vector of time series variables, v is a vector of intercepts; A is the matrix of parameters, and mt is a vector of error terms.

From the perspective of nonlinearity, we perform the nonlinear causality tests to examine the effect of domestic financial and political risks and global risk on domestic economic risk in QISMUT countries. Precisely, we employ Diks and Panchenko causality tests proposed by Diks and Panchenko (2006) and Hatemi-J causality (proposed by Hatemi-J (2012). The nonlinear Diks and Panchenko causality test is the developed version of nonlinear Granger causality proposed by Hiemstra and Jones (1994). Diks and Panchenko (2006) developed a new test statistic to avoid spurious rejection of the null hypothesis, which is one of the main weaknesses of the nonlinear causality test of Hiemstra and Jones (1994). As a last causality technique, the Hatemi-J causality test is used; the causality test is developed asymmetric causality testing and dealt with variables that are integrated of the first degree without any deterministic trend parts (Hatemi-J & El-Khatib, 2016). As clearly detailed by Hatemi-J (2012), in reality, asymmetric casual impacts can be expected because of the number of potential reasons (Hatemi-J & El-Khatib, 2016). It is also well-known that if the absolute magnitude of the positive and negative shock is the same, people and economic agents react differently to a negative shock than a positive one. (Hatemi-J, 2011). Besides, people react more to negative changes (in price, etc.) than to positive ones. The magnitude of a causal impact of a negative charge can be different from a positive change. It means we should take into consideration the sign of the variations while implementing causality tests. By using the Hatemi-J causality test, we could distinguish the causal effects of positive changes from the negative ones. Hatemi-J’s test uses the modified Wald (MWALD) test statistics in the VAR model. Hatemi-J’s (2012) causality test generates critical values that are robust to non-normality and time-varying volatility.

Empirical Findings

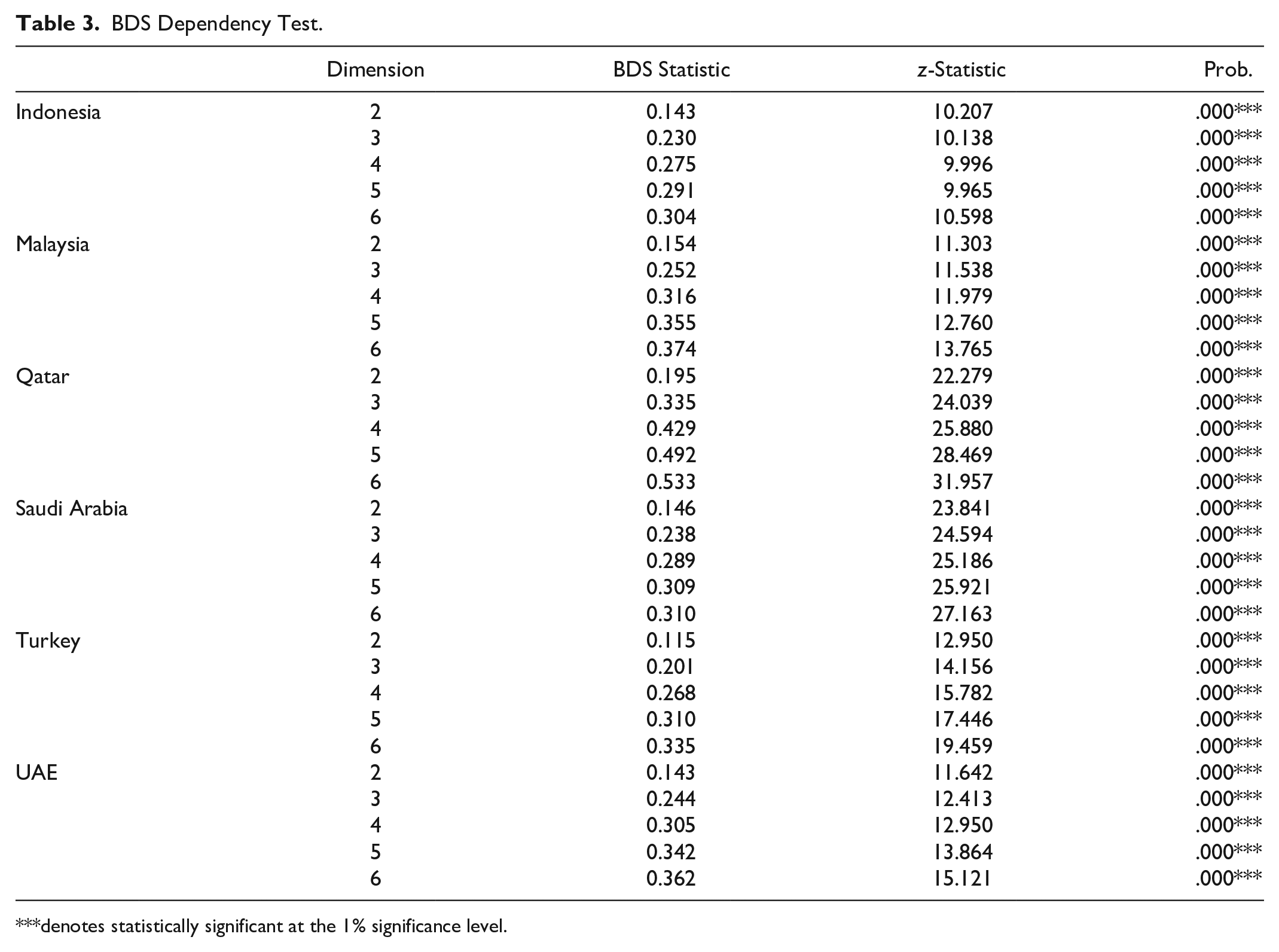

As we have outlined the methodological approach abovementioned, as an initial technique, in this study, the BDS test of Broock et al. (1996) is employed to detect nonlinearity in the time series variables. The outcomes of the BDS test for the variables of ER, FR, PR, and GR in the QISMUT countries are reported in Table 3. The results provide empirical evidence that the data is independent, identically distributed (i.i.d). The assumption was rejected at a 5% significance level for the QISMUT countries. This result indicates that the threshold cointegration test that allows structural breaks and nonlinear causality tests are valid to estimate the long term and causal effects of domestic financial and political risks and global risk on domestic economic risk in QISMUT countries, and the optimal lag for each model is selected using the Schwarz information criterion.

BDS Dependency Test.

denotes statistically significant at the 1% significance level.

As a next step, Zivot and Andrews (ZA) 2002 unit root tests with a single structural break is employed to identify the order of integration of the variables. The results of the Zivot-Andrews test are illustrated in Table 4, which shows that for all countries, ER, FR, PR, and GR are integrated with the of order I (1). This is due to the higher value of calculated estimated test statistics than the critical values of the test at a 5% significance level. The Fourier ADF unit root test is also employed in this study since many breaks known or unknown in a series can be captured by using a small number of low-frequency components from a Fourier approximation. Table 5 provides results from the Fourier ADF test which is developed by Enders and Lee (2012). The outcomes support the findings of the ZA unit root test.

ZA Unit Root Test.

Note. Δ symbol indicates the first difference of the variables. *, **, and *** denote statistically significant at the 10%, 5%, and 1% significance level, respectively, while SB denotes structural break. The 1%, 5%, and 10% critical values of the ZA unit root test are −5.34, −4.93, and −4.58, respectively. The decisions are taken based on a 5% significance level.

Fourier ADF Unit Root Test.

Note. Δ symbol indicates the first difference of the variables. *, **, and *** denote statistically significant at the 10%, 5%, and 1% significance levels, respectively. The decisions are taken based on a 5% significance level.

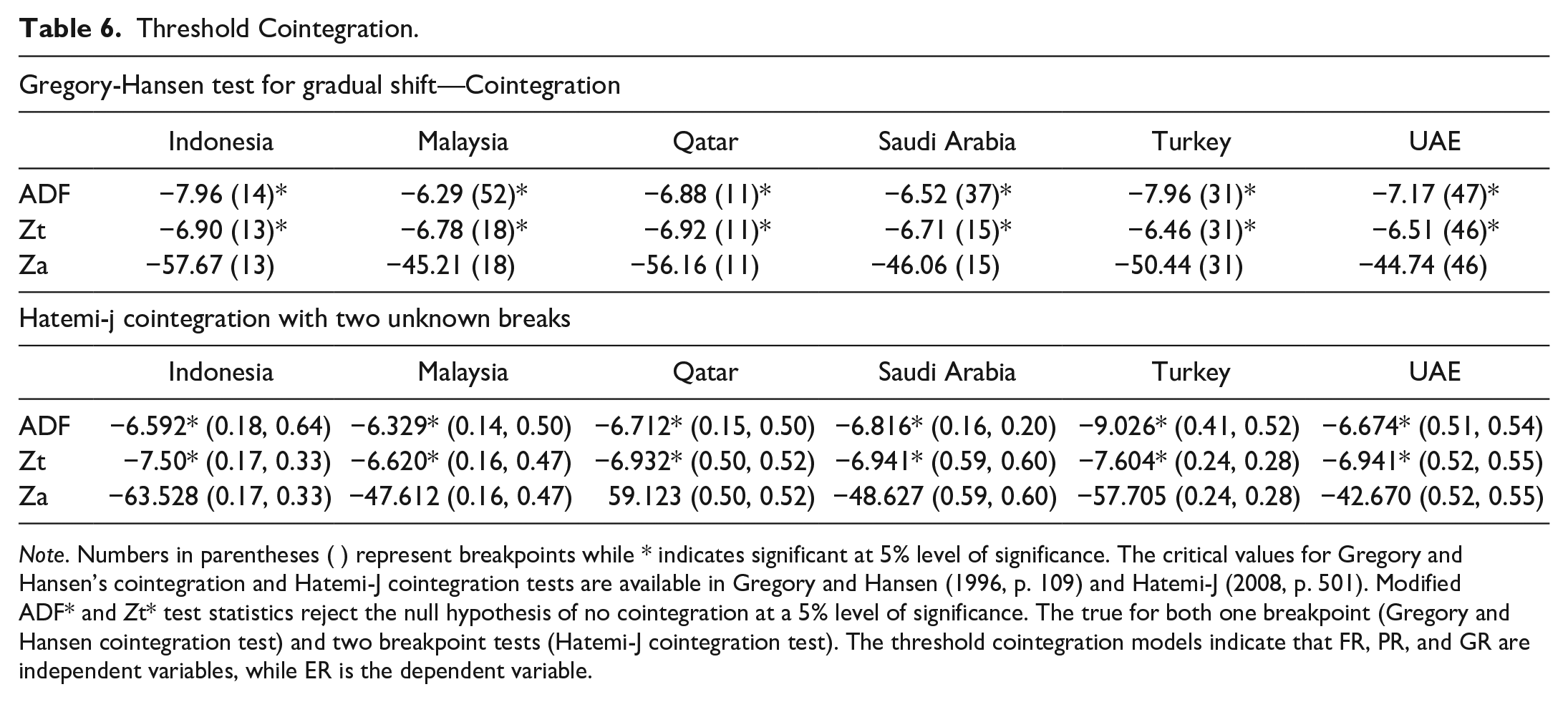

After detecting the linearity and order of integration of the time series variables, the threshold cointegration approach is applied in the present study in order to investigate the presence of cointegration among the variables of ER, FR, PR, and GR in the QISMUT countries. As suggested by Gregory and Hansen (1996) and Hatemi-J (2012), since the long-run relationship can witness one or two regime shifts in the same period, conventional cointegration tests may result in misleading results. In other words, structural breaks in a long-term series can change the cointegrating relationship. Thus, we employ Gregory and Hansen cointegration and Hatemi-J cointegration tests in order not to end in misleading or inconclusive results (Bondia et al., 2016). The outcomes of the threshold cointegration test for the time series variables are reported in Table 6. The results provide empirical evidence that the i.i.d assumption of no cointegration is rejected at a 5% significance level for each country, indicating the existence of a long-run relationship among the variables in the QISMUT countries. In other words, the time series variables move together in the long run. It is worthy of mentioning that the outcomes of the Hatemi-J cointegration test are consistent with the outcomes of Gregory and Hansen’s cointegration test for all estimated models.

Threshold Cointegration.

Note. Numbers in parentheses ( ) represent breakpoints while * indicates significant at 5% level of significance. The critical values for Gregory and Hansen’s cointegration and Hatemi-J cointegration tests are available in Gregory and Hansen (1996, p. 109) and Hatemi-J (2008, p. 501). Modified ADF* and Zt* test statistics reject the null hypothesis of no cointegration at a 5% level of significance. The true for both one breakpoint (Gregory and Hansen cointegration test) and two breakpoint tests (Hatemi-J cointegration test). The threshold cointegration models indicate that FR, PR, and GR are independent variables, while ER is the dependent variable.

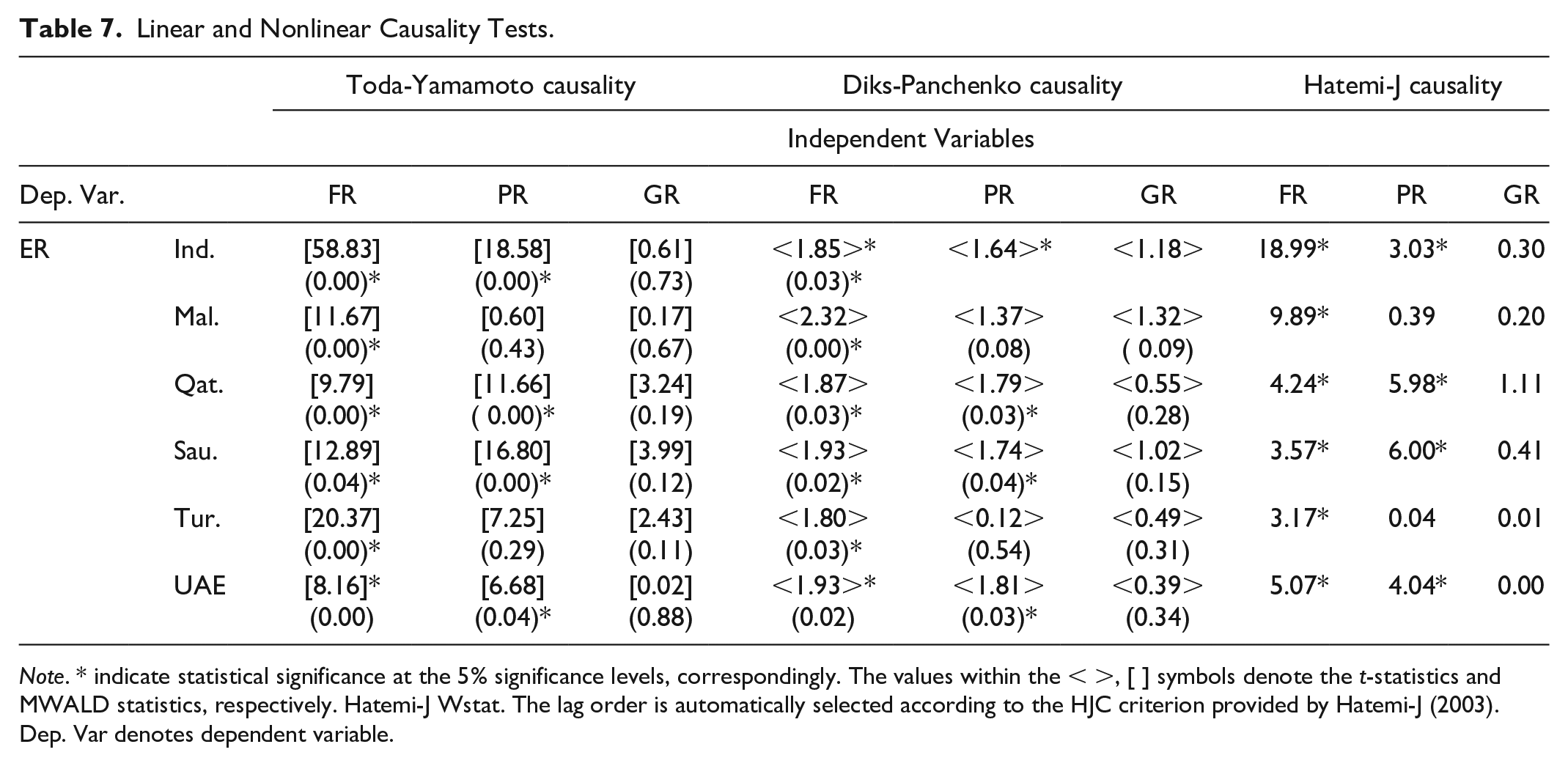

Table 7 shows the results of the linear—Toda-Yamamoto—causality and nonlinear—Diks and Panchenko and Hatemi-J—causality tests for the QISMUT countries. In the linear causality test, the results show that the null hypothesis that FR does not cause ER can be rejected in the QISMUT countries, meaning that the financial risk is a significantly important variable over the economic risk. This finding is consistent with Schumpeter (1912) and confirms the validity of the finance-led growth hypothesis within the risk perspective. This finding underlines how financial stability is essential for predicting economic stability. Governors in the QISMUT countries should control domestic and foreign debt as a percentage of GDP, their exchange rates, and liquidity level in order to control economic risk. Table 7 also shows that in Indonesia, Qatar, Saudi Arabia, and UAE, the linear causality runs from political risk to economic risk, implying that changes in political risk significantly led to changes in economic risk in these countries. These empirical results support the theoretical and empirical findings of Olson (1963), Ades and Chua (1997), and Julio and Yook (2012). Surprisingly, the findings in Table 7 also reveal that changes in global risk do not significantly lead to a change in economic risk in QISMUT countries. This finding can support the findings of—Parashar (2010), Mobarek and Kalonov (2014), Olson and Zoubi (2017)—since their findings underlined the better performance of Islamic banks relative to that of conventional banks during the global financial crisis. Consistently, the results for the nonlinear causality tests support the direct Toda-Yamamoto causality test results at a 5% significance level.

Linear and Nonlinear Causality Tests.

Note. * indicate statistical significance at the 5% significance levels, correspondingly. The values within the < >, [ ] symbols denote the t-statistics and MWALD statistics, respectively. Hatemi-J Wstat. The lag order is automatically selected according to the HJC criterion provided by Hatemi-J (2003). Dep. Var denotes dependent variable.

Discussion

The study employed Gregory and Hansen for Gradual Shift Cointegration and Hatemi-J cointegration breaks tests, linear—Toda-Yamamoto—causality and nonlinear—Diks and Panchenko and Hatemi-J—causality tests, respectively. Results of the threshold cointegration test exhibit that there is a long-run equation among the time series variables. The result implied that the time series variables of QISMUT countries move together in the long run. The empirical analysis of both linear and nonlinear causality estimations produces robust causality results.

The results show strong evidence that financial risk causes economic risk in QISMUT countries. These results are in line and supportive of earlier evidence by Levine (1999), Chowdhury (2002), Liu and Hsu (2006), Montes and Tiberto (2012). These studies conclude that financial market development could help to accelerate long-run economic growth while political risk would plunge the country’s economy into recession. Also, to develop and benefit from Islamic finance’s led to economic growth benefit, financial sector regulations such as; liquidity management, bankruptcy resolution, taxation, support for asset-backed financing, more risk-sharing financial products and services, and new organizational formats needed. Also, as a recommendation for the Islamic countries that suffer from low economic growth, proper legislation, and regulation should be developed (TKBB, 2016).

Also, our outcome supports the findings of Karnane and Quinn (2019), Roe and Siegel (2011), and Alesina and Perotti (1996) in that they underline that political instability lowered the amount of investment and then it inevitably worsened economic growth. From the risk perspective, this finding also supports Kirikkaleli (2020) and Kirikkaleli and Onyibor (2019) outcomes. These outcomes highlight the importance of sound political stability in developing and developed countries, especially for the growing Islamic finance-based countries, as the government has an active role in the Islamic economy by entering the market acting the regulatory of economic activities (TKBB, 2016). Also, by taking a closer look into the analysis of the QISMUT countries, we can see that changes in political risk significantly led to changes in economic risk in Indonesia, Qatar, Saudi Arabia, and UAE. These results are in line with the outcome of country risk’ analysis by Ramady (2014) The results of the analysis declare that (i) both financial and economic risks have a strong impact on political risk in Qatar, (ii) political risk is highly related to corruption, democratic accountability, bureaucratic quality, and investment profile in Qatar. In Qatar’s case, although there’s a strong bureaucracy and a rise in political risk during the 2011 Arab spring events, political risk is comparatively low in the Gulf Cooperation Council (GCC), with high GDP per capita, generous subsidies, and low unemployment rate in the Gulf area. Also, with the help of the 2022 World Cup, bureaucratic reforms have been accelerated, which will positively impact economic and political stability. The government actions or imperfections by means of legislative or judicial institutions nourish the political risk, and it has negative impacts on the investment decisions, and especially international ones, in the country. Then, like a domino effect, economic growth is affected by the net investment value. As bureaucracy quality is positively correlated with investment profile, sustaining government stability has a very important role in economic stability. As an oil-dependent economy, Saudi Arabia, being one of the best-performing economies of G20, by the average rate of real GDP growth during 2008 to 2012, has overcome the negative impacts of Arab Spring with the oversubscription of mega Sukuk, most of them are government-backed. Saudi Arabia, as a monarchy based on Islamic Shariah, due to the absence of accountability, needs to overcome bureaucratic inefficiency as having bureaucracy problems comparatively to the other Gulf countries. Besides, law and order must be regulated in Saudi Arabia because it is the most significant variable that causes political risk. Thereafter, comes the internal conflict and corruption problems, as to be resolved to sustain political stability. For the political stability of the high government effectiveness-based country, UAE, government stability should be sustained as it is the most correlated problem with the political risk in UAE. Compared to Qatar, the investment profile has not strong effect on political risk due to the inward foreign direct investments from emerging economies and the MENA region. In addition, expatriated labor force can be a crucial risk factor to be managed in the future. However, politically motivated demonstrations from time to time come about throughout Indonesia. The World Bank’s ranks for the political risk in Indonesia is from low to moderate. As to sustain economic stability, the political risk factors in that region, such as; religious-based and student violence, must be controlled.

In the meantime, the political risk of these countries stands as a vital factor for predicting the economic risk; changes in global economic uncertainty will significantly lead to a change in economic risk. This cans correctly being seeing in variability in the data of Saudi Arabia, Turkey, and UAE.

Conclusions

Despite the sound economic and financial performance of the QISMUT countries in the last two decades, surprisingly, a minimal number of studies have focused on the QISMUT countries to the economy. This paper sheds light on the causal effects of domestic financial and political risks and global risk on domestic economic risk in QISMUT countries, covering the dataset from 1997Q1 to 2015Q2. As a summary, the outcomes of the present study shows (i) changes in domestic financial risk significantly lead to changes in economic risk in the QISMUT countries; (ii) domestic political risk causes economic risk in Indonesia, Qatar, Saudi Arabia, UAE; (iii) global risk affects significantly on economic risk in Saudi Arabia, Turkey, and UAE. The study’s outcome reveals how policymakers can take lessons and new precautions. At the individual country level, the impact of political risk on economic stability comes in sight far more pervasive in Indonesia, Qatar, Saudi Arabia, and UAE than in the rest of QISMUT countries. This result adds to the growing literature on the role of political risk and its impact on economic risk, particularly in the context of the country with the highest GDP in the Gulf Area (Saudi Arabia), highest Muslim population with the Islamic finance appliance (Indonesia), oil-dependent country (Qatar), and highly government effectiveness-based country (UAE) from the QISMUT countries. Also, this outcome raises the attention to these countries. To conclude, there is some political risk exposure in these countries that is different from any exposure in the remaining QISMUT countries (Malaysia and Turkey) during the analysis’s covering period.

Also, by supporting Schumpeter’s finance-led growth, the results of the study add to the extant literature. Although QISMUT countries have overcome the global financial crisis, financial precautions and regulations should be taken by each QISMUT country. Besides financial risk, global economic uncertainty also has negative effects on Saudi Arabia, Turkey, and UAE. Critical policy intervention could include, policymakers in the QISMUT countries should control financial stability indicators, including domestic and foreign debts, exchange rate, and liquidity problems, in order to control macroeconomic dynamics in their markets. Moreover, policymakers in the QISMUT countries should control political tension in order to achieve sustainable growth and obtain sound macroeconomic indicators. Perhaps, this empirical finding will prospectively open new discussions among policymakers in these countries. New researches should be performed in different regions of the world, and also including more control variables and forthcoming new empirical techniques is welcoming.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.