Abstract

We examine how interlocking directorates influence innovation performance differentials between firms. Our study offers a new perspective of the effect of interlocking directorate ties upon innovation performance, focusing on network effects on interfirm performance. Using a sample of China’s listed companies for the period 2012–2016, we empirically examined the relationship between board interlocks and interfirm innovation performance differentials. The results demonstrate that the presence of board interlocks reduces interfirm innovation performance differentials and leads to a convergence of innovation performance between the connected companies. Furthermore, cross-level analysis found that the relationship between board interlocks and interfirm innovation performance differentials is moderated by the interfirm industry attributes and demographic characteristics of the board. This study expands the existing research in explaining the driving mechanism of enterprise innovation performance as affected by interlocking directorate ties.

Introduction

The role of networks and linkages is becoming increasingly prominent in investigations of enterprise innovation performance (Ahuja, 2000; Laursen & Salter, 2006; Scott & Brown, 1999; Zhang et al., 2019). Scholars have studied the effect of networks on innovation performance from several different perspectives, such as knowledge-sharing (Zhang et al., 2019), strategic imitation in R&D investment (Oh & Barker, 2018), firms’ external environment (H. Li & Atuahene-Gima, 2001), and external search strategies (Laursen & Salter, 2006). However, a review of the cumulative results of empirical research examining the relationship between networks and firm innovation performance has revealed inconclusive findings (Carpenter et al., 2012; Gnyawali & Park, 2011). Thus, novel theoretical explanations of networks’ influence upon firm innovation performance are needed.

Mazzola et al. (2016) called on the scientific community to investigate the role of directors’ networks on the relationship between interfirm network position and innovation performance. This article attempts to explore the relationship between social networks and corporate innovation performance from a new perspective, following Pallotti et al. (2015): “If interorganizational relations have implications for organizational performance, they should be revealed by variations in performance differentials between connected organizations” (p. 190). Following this logic, the relationship between networks and firm innovation performance could be explored by examining the influence of social networks on interorganizational performance, rather than only focusing on individual innovation performance, as most previous studies have done. The relationship between networks and corporate innovation performance can be explored from the new perspective of the variation in innovation performance differentials between paired enterprises, whether connected or not, to explain the inconsistent conclusions in previous studies. To the best of our knowledge, with the partial exception of Pallotti et al. (2015), we are not aware of any research that has attempted to explore innovation performance differentials between firms instead of individual innovation performance.

In this article, we focus on interlocking directorate ties to explore the influence of networks on interfirm innovation performance differentials. Why use interlocking directorate ties to explore the relationship between social network effects and firm innovation performance? Interlocks (see detailed description below) represent a more general social relationship, or basic tie, between firms. Moreover, interlocks have usually been treated as significant phenomena (Mizruchi, 1996). In other words, interlocks are expected to affect a firm’s behavior even if all other conditions are identical. Moreover, in China it is crucially important to study the relationship of social networks and corporate innovation performance from the perspective of directorate interlocks, because (a) the presence of concurrent directors of listed companies is a prominent phenomenon in China compared with enterprises in other countries (Y. Chen & Zheng, 2017); (b) it has been argued that in the process of institutional change in emerging economies such as China, a network-based strategy is the main way for enterprises to achieve growth (Boisot & Child, 1996; Peng, 2004); and (c) corporate governance in China is based on a two-tier board structure, similar to the situation in Germany. The two-tier board structure has a markedly different effect than the one-tier board structure on governance culture. Therefore, the Chinese example is not only suitable for the research topic of this article, but, more importantly, it is meaningful to know whether interlocks lead to the convergence of interfirm innovation performance in countries with transition economies and special governance culture, such as China. In summary, this article focuses on interfirm innovation performance differentials, explores the relationship between directorate interlocks and corporate innovation performance in the Chinese context, and aims to determine whether or not the social relationship, represented by directorate interlock ties, leads to the convergence of interfirm innovation performance differentials. To achieve this, our article takes Chinese listed companies for the period 2012–2016 as samples and uses a two-stage pair model (Fracassi, 2016) to pair all companies in each year to empirically examine the impact of directorate interlocks on interfirm innovation performance differentials. We show that the interlock network relationship can narrow interfirm innovation performance differentials at the dyadic level. Furthermore, differences in the industry of operation of the two companies and the demographic statistics of the two companies’ boards were found to have a moderating effect on the relationship between the interlock network and interfirm innovation performance differentials.

Theoretical Background

Corporate Innovation Performance and Its Influencing Factors

Following previous studies’ definitions of innovation performance (Ahuja & Katila, 2001; Laursen & Salter, 2006; Rosenbusch et al., 2019), this article holds that innovation performance is generated from the corporation’s innovative production, helping the corporation improve and upgrade its products or services, processes, new marketing methods, or new organizational methods. In this way, innovation performance can refer to both intermediate results, such as patents (Ahuja & Katila, 2001), and final outcomes, such as the introduction of new products (Laursen & Salter, 2006).

In case an enterprise innovation cannot obtain the entire required knowledge from inside, it must procure it from external organizations that have the knowledge (Lambe & Spekman, 1997). Enterprises must then reconfigure the diverse knowledge for better innovation performance, meaning that they should effectively absorb the acquired knowledge from external organizations and put it their own to use (Gilsing et al., 2008; Song et al., 2019). Therefore, the search, acquisition, absorption, and integration of innovation elements are closely related to innovation performance.

Research on corporate innovation through the social relationship lens emphasizes the impact of embeddedness on innovation activities and performance (Ahuja, 2000; Owen-Smith & Powell, 2004; Powell et al., 1996), and some scholars even believe that the social relationship is a prerequisite for innovation (Cowan et al., 2007; Imai & Baba, 1989; Powell, 1998; Whittaker & Bower, 1994). Indeed, the social relationship brings great benefits to companies’ innovation. For example, it helps the company obtain outside information and resources (Gulati et al., 2000), facilitates the flow of knowledge and information among enterprises (Howard et al., 2017), and realizes resource sharing (Wei et al., 2000). In addition, some scholars focus on the network of enterprise alliances (Gilsing et al., 2008; Schilling & Phelps, 2007; Zhang et al., 2019) and board interlocks (Howard et al., 2017; Oh & Barker, 2018) to study the impact of these special networks on the innovation performance of enterprises.

Existing research indicates that the resources and capabilities owned by enterprises themselves, as well as their ability to obtain external resources based on networks and connections, are the main factors influencing their innovation performance. However, with a growing trend of complexity and uncertainty in innovation activities, investigation into how differences in networks and linkages give rise to performance heterogeneity has been at the forefront of innovation research (Rosenbusch et al., 2019). In addition, few current studies on enterprise innovation mechanisms are cross-level, and most of them focus on analyzing the role of variables only at a single level (Gupta et al., 2007; Tan et al., 2015).

Board Interlocks and Corporate Innovation Performance

A board interlock is created between firms when an executive or director of one firm joins the board of another (Burt et al., 1980; Mizruchi, 1996), which embeds enterprises into a system for the dissemination of business experience and practice. Boards can be utilized as important boundary spanners while forming links with the external environment and achieve interfirm linkages, such as the appointment of outside directors and board interlocks, which can be used to manage environmental contingencies (Obigbemi et al., 2016). Previous studies have focused on the relationship between board interlocks and corporate innovation (Davis et al., 2003; Echols & Tsai, 2005; Mazzola et al., 2016; Mizruchi, 1996; Oh & Barker, 2018). For example, Wincent et al. (2010) showed how high levels of board interlocking directorates have positive effects on innovation performance related to new product development. From a theoretical perspective, our review of the existing studies on board interlocks and enterprise innovation found that social network theory, resource dependence theory, and organizational learning theory are the main theoretical bases used in current research.

Social network theory (Gulati & Gargiulo, 1999) is a theoretical perspective often used to understand interlocking directorates. Social network theory argues that corporate actions are influenced by the embedded social network, and its patterns of connectedness and relationships have an impact on the behavior of network participants (Granovetter, 1985). Research supports the influence of social embeddedness on organizational innovation performance and interlock studies establish the role and importance of interlocks in the process of embeddedness (Echols & Tsai, 2005; Mizruchi, 1996). The fact that interfirm linkages promote capabilities for learning adaptive responses (Kraatz, 1998) and forming board-level schema for decision-making (Westphal et al., 2001) makes the interlocking directorate network an information network filled with abundant resources.

Organizational learning theory (Levitt & March, 1988) is traditionally used to study board interlocks, with a focus on imitation. Relevant studies believe that board interlocks are an important channel for interfirm strategy imitation from the perspective of organizational learning theory. For example, Westphal et al. (2001) studied how board ties lead to the adoption of a similar strategic decision-making process. Moreover, Oh and Barker (2018), using panel data from large American manufacturing companies, found that CEOs imitated their outside boards in their own companies’ R&D decisions.

Resource dependence theory regards board members as boundary spanners who access resources from outside (Pfeffer, 1972). To help the corporation deal with the complex environment, the directors make practical suggestions through scanning the business environment (Rindova, 1999; Useem, 1984), basing their recommendations on experience gained from other company boards (Davis et al., 2003; Richardson, 1987). Therefore, according to the resource dependence theory, it can be predicted that the more outside directors there are, the more helpful they are in bringing resources and information needed for innovation, and the better the company’s innovation performance will be.

Innovation Spillovers Across Firms

Firms’ innovative ideas may spill over to other firms, thus affecting firms’ innovation behavior and other outputs (see Cardamone, 2010; Norman & Pepall, 2004; Owen-Smith & Powell, 2004; Pӧschl et al., 2016; Trajtenberg & Henderson, 1993). A large literature base has accumulated from empirical studies analyzing innovation spillovers across firms, mainly technology, R&D, and knowledge spillovers. Most of these studies agree that propinquity, including geographical proximity and closeness of the relationship (e.g., Almeida et al., 2003), is commonly linked to a variety of information spillovers.

Innovation emerges essentially by the combining and recombining of knowledge elements (Schumpeter, 1934). Spillover of innovation requires a focus on knowledge-related spillover. An external knowledge spillover occurs when the positive impact of knowledge occurs between individuals without or outside of a production organization (e.g., Norman & Pepall, 2004). Recent research on innovation spillover from the network perspective has shown that not only individuals in the organization, such as researchers, use ties to share knowledge across organizational boundaries (e.g., Bouty, 2000), but also formal collaborative ties between firms increase the innovation output (e.g., Baum et al., 2000).

Thus, research on innovation spillover across firms commonly focuses on the spillover of knowledge and emphasizes the influence of proximity on innovation spillover; however, it usually does not offer evidence on whether innovation spillovers contribute to the consistency of innovation performance among enterprises, which is lacking even from the network perspective.

In summary, existing research finds that board interlocks have an impact on corporate innovation performance through outside information acquisition, information transmission, and decision-making imitation. The following section will integrate social network theory, organizational learning, and resource dependence theory to form a theoretical basis for formulating hypotheses.

Hypotheses Development

Board Connections and Interfirm Innovation Performance Differentials

An early study on the use of science in industrial innovation revealed that more than one third of key innovation knowledge comes from outside (Gibbons & Johnston, 1974). Thus, the interfirm network, as an effective channel for knowledge transmission, can affect corporate innovation performance (Lynn et al., 2000). Increased breadth of information sources is associated with high innovation success rates (Leiponen & Helfat, 2010). Social interactions mean frequent and wider breadth of the information-and-knowledge exchange. In this case this knowledge-sharing mechanism is constantly strengthened, which encourages enterprises not only to acquire and internalize explicit knowledge, but also to absorb tacit knowledge (J. L. Lin et al., 2009). According to the above logic, two companies with board linkages will have much more efficient knowledge transfer, information transmission, and resource sharing, because the communication between the interlocking directors and the other directors of the two enterprises is not only frequent, but also full and comprehensive with respect to information sharing.

The process of enterprise innovation is the process of constantly producing new knowledge and applying it to business practice. Previous research has shown that new knowledge is created by the novel reconfiguration of existing knowledge (Fleming, 2001). More and more studies have indicated that corporate social networks and relational properties have an impact on knowledge creation and innovation performance, by affecting effective knowledge searching, acquisition, and transfer of node enterprises (Galunic & Rodan, 1998; Nahapiet & Ghoshal, 1998). The corporate social network works in many forms with board ties being only one of them. However, the board tie is much more potent and effective in scanning the business environment and acquiring outside information and resources, as the interlocking directors can make the information more real and effective through their own experience of participating in the decision-making of other companies. Moreover, some studies have shown that those enterprises that have mastered advanced technology will consciously spread it to other board-connected companies that have not, to realize the sharing of knowledge and technology, and that external directors have a positive impact on the company’s innovation performance (Balsmeier et al., 2014).

Mutual imitation related to innovation among board-connected enterprises will eventually lead to the narrowing of the innovation performance gap. An enterprise innovation decision is the optimal decision based on limited information and an uncertain environment. To reduce the risk of limited information and uncertainty, the interlocking directors apply their prior cases as a basis, resulting in similar information between board-connected companies, which leads to the imitation of R&D investment among enterprises (Oh & Barker, 2018).

Interlocking directors may promote the establishment of strategic alliance partnerships between enterprises. For example, Gulati and Westphal (1999a) found that board-connected enterprises are more inclined to establish strategic alliance partnerships, where interlocking directors have a good cooperative relationship with the CEO in strategic decision-making and show higher coordination and communication and less desire to control. An alliance network is the channel of knowledge and information flow among partners (Sampson, 2007). Alliance knowledge-sharing is expected to enhance the similarity of new knowledge cognition and innovation action, subsequently leading to the narrowing of innovation performance differentials.

Knowledge spillover may be an additional driver for the convergence of interfirm innovation performance of interlocking directorates. Audretsch and Lehmann (2006) argue that board directors with academic backgrounds can promote the access to, and absorption of, external knowledge spillover. In this vein, innovative knowledge from universities and research institutes can spill over into firms through the appointment of their employees as directors of firms’ boards (Baptista, 2000). Interlocking firms with interlocking academic directors from universities and/or research institutes receive and absorb the knowledge spillover from the same source. This eventually leads to a narrowing of the innovation performance differentials between them.

Notably, the study of indirect directorship interlocks has gained more attention by scholars in recent years (Abdelbadie & Salama, 2019; Ahuja, 2000; Owen-Smith & Powell, 2004; Salman & Saives, 2005). Indirect interlocks occur “when directors from two companies are affiliated with and/or sit on the board of a third organisation” (Abdelbadie & Salama, 2019, p. 85). Granovetter (1973) considered indirect interlocks to be weak ties, but a source of diversified information. Existing studies have found that the indirect relationship between enterprises is also an important variable affecting innovation performance (Ahuja, 2000; Owen-Smith & Powell, 2004; Salman & Saives, 2005). For example, in a longitudinal study about the international chemical industry operating in Western Europe, Japan and the United States, Ahuja (2000) reported that indirect interlocks among companies play a significant positive role in developing patents. Indirect connections are one of the sources of enterprise information and the channel of information exchange between enterprises; indirect connections can also be used as tools to monitor external environments for complementary knowledge and new opportunities. For all indirectly connected enterprises, the long-term equilibrium results in the convergence of their innovation performance due to mutual access to information and tools for acquiring complementary knowledge and new opportunities.

In summary, we can propose the hypotheses as follows:

Strength of Board Interlock Ties and Interfirm Innovation Performance Differentials

Tie strength is defined as a “combination of the amount of time, the emotional intensity, the intimacy (mutual confiding), and the reciprocal services which characterize the tie” (Granovetter, 1973, p. 1361). The existing literature proposes a range of methods for measuring tie strength (Carpenter et al., 2012). In addition to Granovetter’s (1973) classical classification of strong ties and weak ties, N. Lin et al. (1978) further indicated that tie strength is defined not only by the type of relationship, based on Granovetter (1973), but also by the frequency of contact, as there is no consensus on whether weak ties or strong ties are better for technological innovation, and clearly, both strong ties and weak ties are beneficial for technological innovation (Heller & Fujimoto, 2004; Miyazoe, 2006). In view of above, as this article emphasizes the influence of the linkage intensity of interlocking directorate ties on innovation performance, we discuss the relationship between strength of board interlock ties and interfirm innovation performance differentials in two groups, namely, we consider the strength of direct interlocking directorate ties and indirect interlocking directorate ties, respectively.

Different board linkages with various strengths appear in interactions among different companies, affecting knowledge creation, acquisition, and transmission. Direct interlocking directorate ties (strong ties) are conducive to exploitative innovation because they can transmit high-quality information and tacit knowledge, whereas indirect interlocking directorate ties (weak ties) are conducive to exploratory innovation because they can provide heterogeneous knowledge. However, in the face of an uncertain environment, whether direct ties or indirect ties are present, greater linkage intensity of board interlocks, indicated by the number of interlocking directorate ties, can provide more stable information and knowledge flows for enterprise innovation.

Moreover, whether interlocks are direct or indirect, an increase in the number of common interlocking directors between enterprises will strengthen the relationship between enterprises, and continuously enhance the degree of interfirm trust, creating a situation that is more conducive to the transmission of complex knowledge or secret information. Therefore, as strongly connected enterprises know each other well and have similar knowledge structure and background experience, the innovation performance of strongly connected enterprises will be consistent.

In addition, the long-term mutually beneficial relationship between the direct or indirect connected enterprises makes both sides willing to strengthen their input into technological innovation and form a cooperation mode to solve problems together (Larson, 1992; Uzzi, 1997); this will increase as the number of joint directors between connected enterprises increases. Furthermore, enterprises are often willing to take higher risks to provide resources needed for the highly uncertain innovation of strongly linked enterprises, thus forming a bond of innovation interests with the linked enterprises. Therefore, innovation cooperation relationships form easily among strongly connected enterprises, thus promoting the development of innovation performance consistency among them.

Thus, the hypotheses can be proposed as follows:

Moderating Effect of Industrial Differences on the Relationship Between Board Interlock Ties and Interfirm Innovation Performance Differentials

Innovation activities not only have a high degree of professional characteristics, but also carry the risks and benefits of intertemporal and significant information asymmetry, thus leading to innovation decision-making in the context of significant uncertainty. Indeed, the uncertainty context of decision-making is the major reason for imitation (Lieberman & Asaba, 2006). Lieberman and Asaba (2006) argue that mutual imitation is a common means of competition, when companies with similar resource endowments and market positions compete with each other. Competing companies imitate each other to maintain their relative positions or to offset the aggressive behavior of competitors. Compared with enterprises in different industries, enterprises in the same industry have more similar resource endowments and closer market positioning, so they are more competitive with each other. When faced with innovative choices, they often choose to adopt a similar or homogeneous strategy that matches the behavior of competitors to mitigate the intensity of competition or reduce risks.

The content of the interfirm connections is most relevant during the process of advancing technological innovation. For example, M. Li (2019) shows that the industrial diversity of interlocked firms will positively influence the technological innovation of the focal firm because of knowledge diversity. Furthermore, a firm’s external board members from the same industry are less able to contribute valuable information because its senior management has similar industry experiences to theirs (Srinivasan et al., 2018). Thus, interlocking directorate ties (whether direct or indirect) in the same industry do not lead to a widening of innovation performance differentials between firms because interlocking directors from the same industry will play a small role in innovation performance. Furthermore, from the perspective of absorptive capacity theory (W. M. Cohen & Levinthal, 1989, 1990), a firm’s knowledge base plays a major role in determining its ability to identify the value of new knowledge, absorb it, and apply it to the realization of organizational goals. Generally speaking, enterprises in the same industry have a similar knowledge base. This means that interlocked firms (whether directly or indirectly) in the same industry easily recognize and absorb each other’s knowledge, ultimately leading to innovation performance convergence. In addition, industry-level factors, such as technology opportunities (the potential for technological advancement), the applicability of innovation returns, and customer demand for new products, may influence the motivation of innovation, and the likelihood and extent of innovation success, leading to similar innovation performance of companies in the same general industry. Meanwhile, an organization’s ability to learn from a partner increases as the knowledge bases of the partners become more similar and complementary (Hamel, 1991).

In summary, regarding industrial differences, the relationship between boards and corporate innovation performance differentials can be proposed as follows:

Moderating Effect of the Directors’ Demographic Characteristics on the Relationship Between Board Interlock Ties and Interfirm Innovation Performance Differentials

The board of directors (BoD), as the link between the shareholders and the manager, is not only an important part of the corporate governance mechanism (Abdelbadie & Salama, 2019; Hamdan, 2018), but also a central institution that influences the strategic decision-making of the enterprise. Considering that top management team (TMT) studies have shown that the demographic characteristics of TMTs have a significant impact on corporate performance, due to their involvement in various key business decisions (Papadakis & Barwise, 2002), we specifically chose to investigate two key demographic variables, “age” and “education level.” These two variables were chosen because they are important demographic characteristics of the board in relation to innovation performance, not only with respect to their risk attitude but also with respect to their acceptance of new knowledge. Therefore, we focus on the impact of age and educational level of the BoD on the difference in innovation performance between enterprises in innovation decision-making and innovation execution.

The directors’ age reflects the general life and work experience of the executive team members, where decision makers of different ages frame and interpret information in different ways (Hambrick & Mason, 1984; Marcel, 2009). Therefore, from the perspective of the innovation process, the directors’ age will affect the two innovation-related activities: enterprise innovation decision-making and postdecision management (innovation execution). Generally speaking, in corporate innovation decision-making, the average older board generally dislikes risks and is often reluctant to be adventurous for innovation, whereas the average younger board is more prone to making innovative decisions as it is more able to learn and integrate information in the decision-making process, and its information resources are more novel. However, things change. When the average younger board makes innovative decisions, the information channel of the directors’ linkage may make the average older board think that companies that may have made innovative decisions are better informed about the innovation prospects, and they may simulate the innovative decisions based on “information cascades” (Bikhchandani et al., 1992, 1998), because innovation-related decisions are highly uncertain and ambiguous, and those in charge easily accept information implied in others’ actions. Although incomplete, information cascades have a profound impact on the board’s thoughts and decision-making process, as proposed by the information cascade, “when it is optimal for an individual, having observed the actions of those ahead of him, to follow the behavior of the preceding individual without regard to his own information” (Bikhchandani et al., 1992, p. 994).

Nevertheless, when companies with linkages clarify innovation decisions and begin to enter postdecision management (i.e., supervision of innovation execution), perhaps, the average younger board considers that the average older board has a better source of information, and then relies on the information channel of the board interlocks to imitate innovation management activities, as the average older board has richer experience in innovation management.

Existing studies generally believe that the higher the overall educational level of directors, the more conducive they are to enterprise innovation (e.g., Bantel & Jackson, 1989; Datta & Rajagopalan, 1998; Wally & Baum, 1994). First, highly educated directors have stronger research ability and knowledge related to innovation management, which is conducive to improving the quality of innovation-related decisions (Datta & Rajagopalan, 1998), because of the complexity and difficulty of innovation decision-making due to the uncertainty and risk of innovation-related activities tests the cognitive ability and information processing ability of decision makers. Second, a BoD with a high level of education can pay more attention to innovation activities and treat the uncertainty of innovation with an open attitude (Bantel & Jackson, 1989; Hillman & Dalziel, 2003). Therefore, they can find more innovation opportunities and make more rational and efficient decisions related to innovation. Finally, a board with a higher education level values innovation more, has a higher tolerance for uncertainty, and is more receptive to new ideas (Wally & Baum, 1994).

From the perspective of the entire process of innovation decision-making, the greater the age and education level differentials of the board, the higher the potential for consistency of innovation performance. Thus, Hypothesis 4 can be proposed as follows:

Method

Sample and Data

To test our hypotheses, we used a sample of A-share listed Chinese companies, which refer to shares traded in Renminbi, the local currency in mainland China, on the Shanghai Stock Exchange (SHSE) and Shenzhen Stock Exchange (SZSE) for the period 2012–2016. We began collecting data on interlocks and other key firm- and industry-level controls in 2012 to ensure the consistency of the research samples in the macroeconomic environment, because Xi Jinping took over as China’s national leader since 2012. Using a 1-year lag between the independent and dependent variables, the data are collected only until 2016 because the data of patent application from China’s State Intellectual Property Office (SIPO) have so far been updated only to 2017.

We employed multiple data sources to construct our data set. The basic information and financial data of the listed companies such as official name, size, age, return on assets (ROA) were retrieved from the Wind database which is provided by Wind Information Co., a leading financial data firm in China, and the information about listed companies’ board directors was taken from the China Stock Market & Accounting Research (CSMAR) database which is developed by Guo Tai An Information Technology Company. The Wind database and CSMAR database are used by many researchers on China (e.g., Haveman et al., 2017). In addition, we secured information about patent applications during the period 2013–2017 from SIPO. Under Chinese corporate law, all listed companies must have a two-tier board structure where the BoD is regarded as a “decision-making” unit and the supervisory board as a mechanism that monitors the activities of the BoD. Therefore, the interlocking board discussed in this article includes not only the corporate relationship formed by the interlocking supervisors but also the corporate relationship formed by the interlocking directors.

The final data set was constructed in three stages. First, we secured sample firms and their information about A-share listed Chinese companies on SHSE and SZSE during 2012–2016 from the Wind database, eliminating the companies labeled ST (Special Treatment) or that had missing data for the sample period. Second, we obtained personal information about the board members from CSMAR, then compared whether directors with the same name are the same person, and gave each director a unique code. Third, we matched the information about the sample firms’ official names with the firms’ information collected from the Wind database, their board directors’ information from SMAR, and the patent application information from SIPO.

We compiled the 9,357 company-year observations (i.e., sample size) for the sample period 2012–2016. The annual data of the sample (Table 1) demonstrate that the proportion of enterprises with director linkage relationships is very high, and there is an increasing trend from year to year.

Interlocking Directorate Ties in A-Share Listed Enterprises in China (2012–2016).

Variables

Dependent variable

Following the research method of Fracassi (2016), we measured the innovation performance differentials between the connected firms using a paired model as follows:

First, we accounted for as much of a company’s innovation performance as possible using common control variables. Specifically, we began by regressing Company i’s innovation performance

This article uses the total number of enterprise patents applied for each year to measure corporate innovation performance

Equation 1 follows prior studies (V. Z. Chen et al., 2014; Choi et al., 2011; Heidenreich, 2009; Köhler et al., 2012; Sorensen & Start, 2000) and introduces the following control variables: (a) main business rate of growth; (b) firm size, measured by the natural log of total assets; (c) ROA to control the sample firm’s past performance; (d) ownership, using a dummy variable, where state-owned and non-state-owned enterprises are expressed as 1 and 0, respectively; (e) firm age, measured by the natural logarithm of the number of years since the company was founded; (f) organizational slack, measured by the average of the debt to equity ratio and the current ratio.

The residual

Finally, we used the log of the innovation performance differential measure as the dependent variable.

Independent variables

There are two main independent variables, board connections and the strength of the board connections, which are added separately to the different models.

Board connections

Board connections in this study were measured and analyzed directly and indirectly. (a) Direct board connections. Assign the variable a value of 1 if a direct board connection exists, otherwise, 0. (b) Indirect board connections. The indirect-board-connection path should not be too long; otherwise, we would obtain information of a poor quality and a defective empirical analysis. Therefore, this study only considers indirect board connections with a path length of 2 (as in Gulati & Westphal, 1999b). That is, if the two paired companies do not have a direct board connection, but both are directly connected with a third company, then the two companies have an indirect board connection. Assign the variable a value of 1 if indirect board connections exist, otherwise 0.

Strength of board connections

The strength of the direct board connection is determined by the number of direct interlocking directors, whereas the strength of the indirect board connection is determined by the number of indirect interlocking directors. The specific measurement method is shown in Figure 1. The higher the value, the greater is the strength of the board connection between the paired companies.

Illustration of board connections.

Moderating variables

Two types of moderating variables were tested in this article. One is industry of operation difference and the other is board demographic difference between the paired companies, in particular, the average age difference and education-level difference of directors. If the paired companies are in the same industry, we assign the industry variable a value of 1, otherwise 0. The level of education ranges from technical secondary school to honorary doctorates, coded in order from 1 to 6. The average age difference and education-level difference of directors between the paired companies’ boards is used to measure the board demographic difference.

Control variables

In theory, any further control variables should not be needed in the following data analysis, because any determinant of company innovation performance should be controlled for in the process of obtaining data on the innovation performance differential, as specified in Equation 1. However, when we use innovation performance differentials as dependent variables in a regression equation, it is important to control for possible heteroscedasticity in the second moments of the innovation performance variable across some variables that can influence and bias the results of the data analyses (Fracassi, 2016). An F test was used to analyze the heteroscedasticity of these control variables in this study. Thus, we added several control variables: First, we add an industry dummy that was assigned a value of 1 if the paired companies are in the same industry, otherwise, 0, because enterprises in different industries have great differences in innovation performance. Second, we also add the average number, age, and educational level of directors for each firm pair to control for the fact that larger, older, and more highly educated boards tend to have more similar innovation performance. Furthermore, we also controlled for the average of company-listing-year and concentration of equity, as we found that firms with longer listing age and higher ownership concentration have similar innovation performance. Moreover, we added the difference in number, age, and education level of directors, and difference in company-listing-year and concentration of equity between the paired firms to rule out the effect of similarity in the values of these variables on similarity in innovation performance. Finally, we controlled for R&D investment between the paired firms using both the average values and the difference between them. Although R&D investment has an impact on innovation performance, we controlled for it in the second moments for possible heteroscedasticity rather than in Equation 1. This is because enterprises with higher R&D investment submit more patent applications, whereas enterprises with the same R&D investment submit similar numbers of patent applications, in general.

All of above independent variables, moderating variables and control variables were lagged by 1 y. To eliminate the influence of extrema, all continuous variables were winsorized at the 1% and 99% levels.

Analyses

To test our hypotheses, we took the fixed-effect panel models using the Hausman test to demonstrate the rationality of adopting fixed-effect analysis. Specifically, we used a year-industry, double-fixed-effect regression to control the year and industry factors, with the year dummy to control the idiosyncratic differences across years and industry dummy for each industry.

In the empirical analysis, we adopted the following strategies to control for endogeneity. First, in our model, all the independent variables and control variables lag the dependent variables by 1 year to eliminate concerns of contemporaneous endogenous effects. Second, we used the year-industry fixed effect and double-fixed-effect regression which may prevent endogeneity caused by missing variables to some extent. Finally, following Salas (2010) and Fracassi (2016), we use deaths of directors as exogenous shocks to test the effect of interlocking directorates on interfirm innovation performance differentials. Our results show that there is no potential endogeneity in our study. We used each pair of companies as an analysis object, and given 9,357 company-year observations, there were a total of 8,878,253 unique firm pairs (pairings were made annually). As the dependent variable was measured as the difference between the residuals in Equation 1, we could expect the coefficient to be small. The value of R2 should also be small for the same reason; related papers using the same method (e.g., Fracassi, 2016) also reported small values of R2.

While analyzing board interlocking network Wong et al. (2015) used a sample of 725 large U.S.-based public companies and for dealing with the independence assumption of network effects in tie formation they employed the exponential random graph modeling (ERGM) for social networks. Our data set does not enable the employment of this technique as the network structure comprises too few bilateral and triangular links. However, as our analysis compiles a large sample size of 9,357 company-year observations and this sample comprises most of the studied population as shown in Table 1, the reliability of statistical inferences in this study is considered to be relatively high (J. Cohen, 1988).

Results

Descriptive statistics for the study variables in the regression models for innovation performance differentials are presented in Table 2. This table shows that the mean of the innovation performance differential between paired companies is 0.4012, with a standard deviation of 0.2621. This result suggests a large difference in interfirm innovation performance.

Descriptive Statistics in All Regression Models on Innovation Performance Differential Between Paired Firms (N = 8,878,253).

Note. Correlations are statistically significant (at

Results of the regression models of the main effects are presented in Table 3 (Models 1–4). Models 1 and 2, in which the independent variables are direct board connection and indirect board connection, respectively, test Hypotheses 1a and 1b. That is, a direct (or indirect) board connection between the paired companies is significantly negatively related to their innovation performance differential within 1%, with the coefficients: β = −0.0213 and β = −0.0117, respectively. This means that the presence of direct (or indirect) interlocking directorate ties between two companies reduces interfirm innovation performance differentials, supporting Hypotheses 1a and 1b.

Regression Model Results: Innovation Performance Differential (N = 8,878,253).

Note. The OLS coefficients are reported, with t statistics in parentheses. OLS = ordinary least squares.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Models 3 and 4 in Table 3, in which the independent variables are strength of direct board interlocks and indirect board interlocks, respectively, test Hypotheses 2a and 2b. That is, the strength of direct (or indirect) board interlocks between the paired companies is significantly negatively correlated to their innovation performance differential within 1%, with the coefficients: β = −0.0298 and β = −0.0151, respectively. This suggests that stronger direct (or indirect) interlocking directorate ties will be associated with smaller differences in their innovation performance, supporting Hypotheses 2a and 2b.

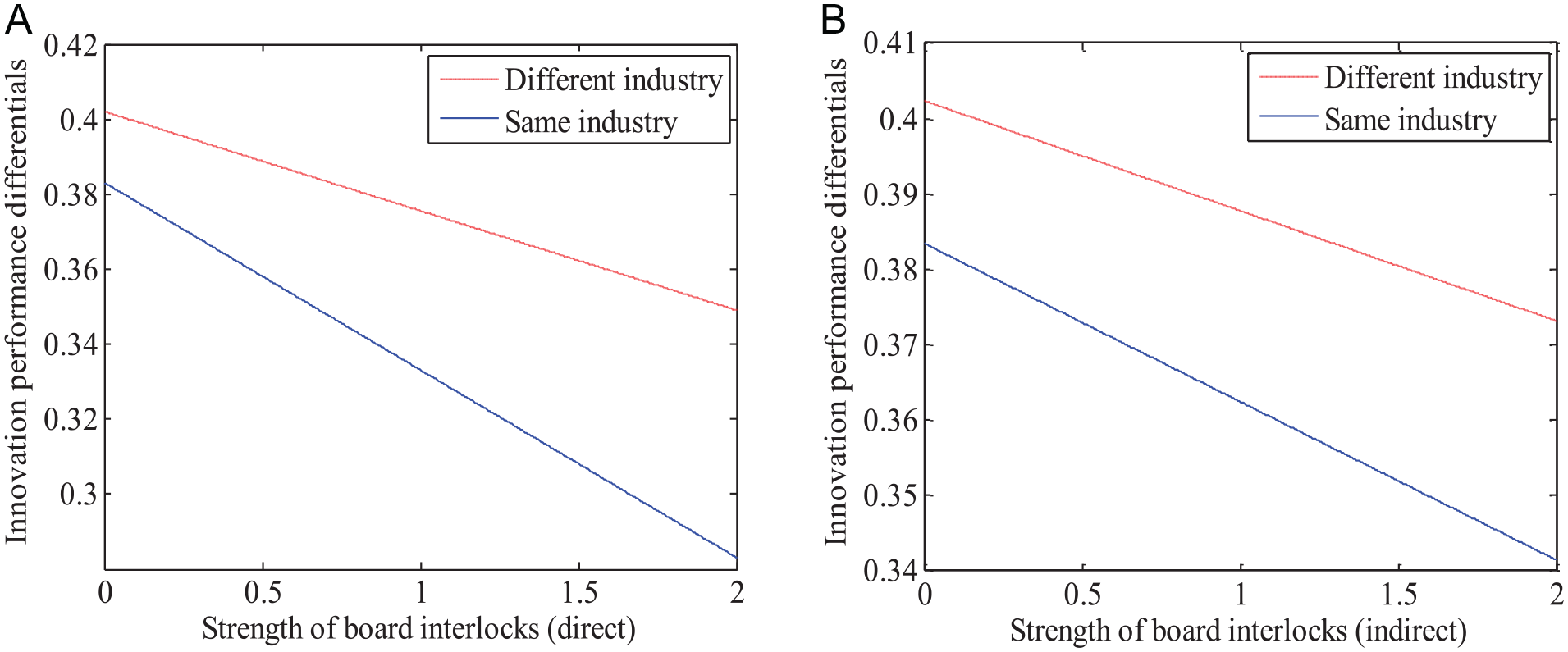

Hypotheses 3a and 3b suggest that direct (or indirect) interlocking directorate ties between paired companies in the same industry have a more positive effect on reducing their innovation performance differentials than those between paired companies in different industries. To test this hypothesis, we ran two regression models, respectively, adding the interaction terms “same industry (Y/N) × direct (or indirect) board connections” and “same industry (Y/N) × strength of direct (or indirect) board connections,” after controlling for the main effects predicted by Hypotheses 1a, 1b, 2a, and 2b. The results of these regression models (Models 5–8) are presented in Table 4. All the correlation coefficients of the interaction terms in Models 5 to 8 were significantly negative within 1%, with the following respective coefficients: β = −0.0173, β = −0.0075, β = −0.0235, and β = −0.0064. This indicates that when paired companies are in the same industry, the impact of board interlocks will be enhanced, that is, their innovation performance differentials will be narrower. Therefore, Hypotheses 3a and 3b are verified. Figure 2A and B further depicts how the relationship between the strength of board interlocks and their innovation performance differentials increases when they are in the same industry.

Regression Model Results: Moderating Effect of Industrial Differences (N = 8,878,253).

Note. The OLS coefficients are reported, with t statistics in parentheses. OLS = ordinary least squares.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Analysis of significant interactions. (A) Same Industry (Y/N) × Strength of Board Interlocks (Direct) and (B) Same Industry (Y/N) × Strength of Board Interlocks (Indirect).

The results of the regression models of the moderating effect of the difference in average age of directors are presented in Table 5 (Models 9–12). Models 9 and 11, in which the interaction terms are “Difference in Average Age of Directors × Direct Board Connections” and “Difference in Average Age of Directors × Strength of Board Connections (Direct),” test Hypothesis 4a; Models 10 and 12, in which interaction terms are “Difference in Average Age of Directors × Indirect Board Connections” and “Difference in Average Age of Directors × Strength of Board Connections (Indirect),” test Hypothesis 4b. The correlation coefficient of the cross-term is significantly negative within 1% in Models 9 and 11, whereas it is significantly negative within 10% in Model 12 but not significant in Model 10 (Table 5). It shows that the greater the difference in average age of directors in paired firms, the narrower the differentials in innovation performance, caused by both the strength of direct and indirect interlocking directorate ties. Moreover, this is true for both the connection alone and also its strength when the interlocking directorate ties are direct. Therefore, Hypothesis 4a is supported, but Hypothesis 4b is not. Figure 3A and B further depicts how the relationship between the strength of board interlocks and their innovation performance differentials increases when the difference in average age of directors between paired companies increases.

Regression Model Results: Moderating Effect of the Age of the Board (N = 8,878,253).

Note. The OLS coefficients are reported, with t statistics in parentheses. OLS = ordinary least squares.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Analysis of significant interactions. (A) Difference in Average Age of Directors × Strength of Board Interlocks (Direct). (B) Difference in Average Age of Directors × Strength of Board Interlocks (Indirect).

The results of the regression models of the moderating effect of the difference in average education level of directors are presented in Table 6 (Models 13–16). Models 13 and 15, in which the interaction terms are “Difference in Average Education of Directors × Direct Board Connections” and “Difference in Average Education of Directors × Strength of Board Connections (Direct),” test Hypothesis 5a; Models 14 and 16, in which interaction terms are “Difference in Average Education of Directors × Indirect Board Connections” and “Difference in Average Education of Directors × Strength of Board Connections (Indirect),” test Hypothesis 5b. The correlation coefficient of the cross-term is not significant in Models 13 to 16 (Table 6). This shows that there is no moderating effect of difference in average education level of directors; therefore, Hypotheses 5a and 5b are not supported.

Regression Model Results: Moderating Effect of the Education of the Board (N = 8,878,253).

Note. The OLS coefficients are reported, with t statistics in parentheses. OLS = ordinary least squares.

, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Robustness Checks

To check the robustness of our results, we conducted a sensitivity analysis by replicating all models above using the same measurements but changing the lag period for all of the independent variables, moderating variables, and control variables to 2 y. The results from the robustness analysis confirm our main findings.

Discussion

While research on the relationship between social networks and enterprise innovation performance has garnered much attention from scholars for many years, empirical evidence on the relationship has remained inconclusive (Carpenter et al., 2012; Gnyawali & Park, 2011). Here we have used a different approach that explores the network–performance relationship using variation in interfirm innovation performance differentials instead of individual innovation performance. This approach is similar to the research approach of Pallotti et al. (2015), except that our study adopts a two-stage econometric model (Fracassi, 2016) and different measurement methods of performance differences.

This evidence complements recent findings in the corporate performance literature that emphasize (a) the narrowing of the difference in interfirm innovation performance by interlocking directorate relationships (b) and the strengthening of the network-performance relationship by the interplay between interlocking directorates and differences in firms’ individual attributes—namely, different industries of operation of the two companies or differences in average age of the directors of their boards. This finding is in line with the prevalent perception in the field of network–performance relationships that network relations reduce interorganizational performance differentials (Pallotti et al., 2015), and connections between enterprises in the same industry will enhance the reduction of innovation performance differentials (Laursen & Salter, 2006). Although scholars agree that innovation should be understood on at least two levels (Gupta et al., 2007), there have been few in-depth cross-level mechanistic analyses of enterprise innovation in recent years, especially with respect to those that combine network theory with a cross-level perspective, except for the study by Zhang et al. (2019). The present study shows how cross-level interplay can alter innovation performance, but differs from Zhang et al. (2019) by focusing on interfirm innovation performance differentials at the dyadic level rather than innovation performance at the individual level.

Conclusion

Our econometric evidence from A-listed Chinese companies shows that not only the interlocking directorate relationship but also the strength of this relationship narrows interfirm innovation performance differentials. When we further explore the impact of multi-level factors on innovation performance differentials, we find that the relationship between the strength of board interlocks and their innovation performance differentials between two companies is strengthened when (a) they are in the same industry, or (b) they differ in the average age of their directors.

Contributions

First, given that some previous research on the impact of social networks on corporate innovation performance mainly focused on the impact of social networks on individual innovation performance (Ahuja, 2000; Laursen & Salter, 2006; Zhang et al., 2019), this study emphasizes the impact of social networks on interfirm innovation performance differentials. As it is difficult to draw a clear conclusion about the relationship between social networks and corporate innovation performance through studies on individual innovation performance, this article has explored the network–performance relationship from the new perspective of the variation in interfirm innovation performance differentials. Thus, this study demonstrates that social networks can narrow the differentials of interfirm innovation performance, expanding the study of the individual effect of the network to the interfirm effect.

Second, few current studies on enterprise innovation mechanism are cross-level, and most of them focus on analyzing the role of variables only at a single level, so the driving mechanism of enterprise innovation performance cannot be fully understood (Gupta et al., 2007; Tan et al., 2015). However, the present study closes this gap. It studies the impacts of such variables on interfirm innovation performance differentials at both the dyadic level of the interlocking directorate network and at the interface between the individual levels of enterprise attributes and the dyadic level of the network. It turns out that interlocking directorate relationships reduce interfirm innovation performance differentials, moderated by the different industries of operation of the two companies and the demographic composition of the two companies’ boards. Gupta et al. (2007) believe that every innovation phenomenon should be understood at least at two levels, with one level being the actor and the other being the environment embedded by the actor. Thus, our empirical analysis of the interaction of different levels of factors on innovation performance not only promotes the research depth of enterprise innovation performance, but also helps to comprehensively explain the driving mechanism of enterprise innovation performance.

Finally, our study enriches the literature on innovation spillover by analyzing the relationship between interlocks and interfirm innovation performance differentials. Unlike existing research on innovation spillovers which emphasize the influence of proximity and the movements of employees on spillovers, our study from the network perspective stresses the role of interlocking directors on outward knowledge spillover, as employees in research institutes, and on inward spillover, as board directors, and the influence of knowledge spillover on the consistency of innovation performance of chain enterprises.

Managerial Implications

For practitioners in China and elsewhere, this article calls for more attention to be paid to the relationship between interlocking directorate ties and innovation performance differentials between connected firms. We find that interlocks do lead to the convergence of interfirm innovation performance, which are moderated by the differences in the industry characteristics and board characteristics. The present findings emphasize the importance of firms’ choices of who should form interlocking board ties for the firms’ innovative performance. It means that enterprises with better innovation performance should be selected to build board ties, and the differences in industrial and board characteristics should be considered.

Limitations and Future Research Directions

Some noteworthy limitations of the present study might well provide motivation for future research. This study focused on the interplay between the individual level and the dyadic level on innovation performance, leaving out the cross-level interaction between multiple networks, for example, R&D alliance networks between firms and universities and other research institutions.

In addition, our conclusions are based on evidence from Chinese firms. As discussed above, social networks play particularly important roles in Chinese firms’ operation under an economic transition (Peng, 2004). Similarly, future studies can extend single-country research by testing our theoretical assumptions with evidence from other countries with transition economies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was partially supported by the National Natural Science Foundation of China (Grant 71572027) and by the Sichuan Science and Technology Program (Grant 2020JDR0062).