Abstract

Balance of payments constrained growth model considers that if a country has a chronic external deficit, economic growth can be constrained. Initial model extended by taking into account the effects of capital flows, external debt sustainability, interest payments, budget deficit or public debt, simultaneous effect of internal and external imbalance, and the role of relative prices. We further incorporate Turkey’s high intensity of imports in the aggregate demand components and estimated the model with system estimator. The new version of the model improves significantly explaining the growth in Turkey. Our results reveal that economic growth in Turkey constrained by internal and external imbalances and relative prices play a significant role. Policies aimed at changing the structure of the imports and exports are the most effective for achieving higher growth. It is also shown that economic growth in Turkey highly depends on external demand when the strong depreciation of the domestic currency also acts as a stimulus to growth.

Keywords

Introduction

Thirlwall (1979) developed a long-run growth model consistent with the balance of payments equilibrium. The model implies that no country can grow faster than the rate consistent with the balance of payments equilibrium. The balance of payments consistent growth rate is obtained by the ratio of income elasticity of demand for exports and imports times the exogenous growth rate of world income. When countries do not respect this simple rule sooner or later, they will face a serious problem in financing the external debt and current account deficit, and in the absence of capital flows, it will be necessary to contract domestic demand and hence growth.

The law implies that growth is constrained by world demand, and if available external resources cannot finance current account deficit, it can be a serious obstacle to higher economic growth. Furthermore, Thirlwall’s model implies that income plays a significant role in the adjustment of the economy to bring back to equilibrium, not relative prices. The model has two controversial assumptions: the real exchange rate or relative prices are constant in the long run, and initially, the balance of payments is in equilibrium.

Revision of the original model comes from Thirlwall and Hussain (1982); they relaxed the initial balance of payments equilibrium assumption and allowed capital flows to finance the external deficit. Valuable contributions to the discussion of the underlying implications of the Thirlwall’s law come from, among others, McCombie and Thirlwall (1997), Elliot and Rhodd (1999), Moreno-Brid (1998–1999), Barbosa-Filho (2001), Moreno-Brid (2003), Alonso and Garcimartin (1998–1999), and Blecker (2009).

Recently, Soukiazis et al. (2012, 2014) extended the model further by considering the role of imbalances in public sector as an additional constraint on economic growth and allowing relative price play a role in adjusting external imbalances.

Imported inputs are important for domestic production, exports, and economic growth in developing countries. Use of imported inputs in manufacturing products improves the quality of products due to the use of more sophisticated inputs in the production process. This could lead to introducing higher quality products for the export market (Kugler & Verhoogen, 2009). Also, the use of imported inputs in the production process might increase productivity in the manufacturing sector (Halpern et al. 2015; Khandelwal & Topalova, 2011). Furthermore, low-cost imported inputs may increase export revenue (Bas & Struss-Kahn, 2014). All of these factors might increase the profitability of the firms, which can increase existing exports and allow the firm to bear the fixed cost of accessing new product markets (Edwards et al., 2018).

Increasing use of imported inputs might be increasing exports and contributing to economic growth, and also increases cross-country import dependence (Nordas, 2007). Imported inputs for export have potential to be the main channel for growth if it enhances capital stock and productive capacity. A country which can expand its economic activity in the high technological sector, while avoiding the expansion of medium and low technological sectors, can attain high export growth (Saygılı & Saygılı, 2011).

However, Moreno-Bind (2002), Pacheco-Lopez and Thirlwall (2004), and Blecker and Ibarra (2013) argue that the reliance on a strategy based on foreign content of export may be harmful to growth. Such a strategy may result in an increase in the income elasticity of demand for imports without a compensating effect on the income elasticity of exports. In this case, a country that relies on imported inputs may experience lower growth rates consistent with the balance of payments constrained growth (BOPCG) rates.

With trade reforms in the 1980s and the 1990s, Turkey increased its export significantly; however, this also increased import content of production and exports. In line with Muscatelli et al. (1995) and Saygılı and Saygılı (2011), we extend the Soukiazis et al. (2014) model further by incorporating Turkey’s high intensity of imports in the aggregate demand components and the production process; therefore, we extend the investment and exports functions by taking into account effects of imports.

Remaining part of the article is organized as follows: In the “Internal and External Imbalances, and Growth in Turkey” section, we briefly explain recent developments in Turkish economy with special emphasis on the link between current account deficit, fiscal imbalances, and economic growth. The “Related literature” section gives a brief survey of Thirlwall’s model and presents an extended growth model that takes into account internal and external constraints and relaxes the assumption of relative prices being neutral. In “The Balance of Payment Constrained Growth Model With Internal and External Imbalances, Non-Neutral Relative Prices, and With Foreign Content” section, we test the extended model on the Turkish economy to identify the main determinants of its growth performance within the demand-oriented growth model. The “Scenario Analysis” section provides a scenario analysis focusing on the factors that could foster or harm economic growth in Turkey. The “Conclusion and Policy Implications” section presents the main conclusions and policy recommendations that could help the country to improve its growth performance.

Internal and External Imbalances, and Growth in Turkey

Starting from 1980, the momentum of the reform process brought a decade of rapid economic growth. However, Turkish economic growth has been very volatile in the 1990s; the average growth rate was 3.9%. During this period, the Turkish economy functioned under a mist of vulnerability, distressed by chronically high inflation and persistent fiscal imbalances.

Periods of economic expansion have followed with periods of rapid decline (see Figure 1). After a severe recession in 1994, the economy went through a boom period of above-trend growth between 1995 and 1997. The real depreciation of the Turkish lira in 1994 led to strong exports performance and contributed to the strong economic growth. In 1998, the economy severely hit by the Russian crisis and economic growth shrank over 6% in 1999.

GDP growth and public debt to GDP ratio.

Increasing macroeconomic uncertainty limited access to external financing, the government was forced to increase its reliance on domestic financing and monetization. This increased inflation and rapid accumulation of domestic debt to gross domestic product (GDP) ratio (see Figure 1).

The Turkish economy was also vulnerable to the emerging market crisis—the turmoil in Asia and the Russian default affected the economy. In the second half of 1998, Turkey faced massive capital outflows, rising real interest rates, and declining economic activity.

Policies clearly could not continue on this path for long; following elections in April 1999, the new government introduced a new economic program focusing on fiscal adjustment and deep structural reform. The government has signed a stand-by agreement with the International Monetary Fund (IMF) in late 1999 to stabilize and reform the economy (IMF, 2001; Onis, 2003).

Major institutional and structural reforms introduced after the 2001 crisis helped overcome the earlier “boom-and-bust” cycles during the 1990s, but external deficits expanded significantly. The combination of strong growth and external imbalances has characterized Turkey’s growth pattern since the beginning of the 2000s.

The development of Turkey’s current account deficit since the beginning of the 1990s plotted in Figure 2. Turkey’s current account deficit hovered around 1% of GDP during much of the 1990s. A more sizable external imbalance started to emerge only after the financial crisis of 2001, when Turkey experienced strong growth, thanks to important reforms to strengthen its macroeconomic policy framework and financial sector. The current account deficit to GDP ratio steadily increased between the 2003 and 2007 periods. The impact of the global crisis was severe on the Turkish economy, the growth rate was significantly negative, and the current account deficit decreased sharply in line with the economic slowdown in during 2008 and 2009. In 2010, domestic demand recovered swiftly and the economy returned to rapid growth reached 9.2% in 2010 and 8.5% in 2011 and the current account deficit widened again relative to its pre-crisis levels. The deterioration of the current account has worsened worryingly in the first quarter of 2011 which reached the unsustainable level.

Real GDP growth and current account deficit to GDP ratio.

After a vigorous recovery from the global financial crisis, Turkey went into a period of below potential growth in recent years. However, consumer price inflation is far above the inflation target, and the current account deficit is much too high for comfort. Economic growth was encouraging given the very adverse circumstances in 2015 and 2016. Current account deficit to GDP ratio in the same periods was still high. Turkish economic growth is highly dependent on domestic demand and capital inflows, which mainly come in the form of short-term debt-creating flows.

Spells of current account deterioration have been characterized by strong credit-financed domestic demand-driven growth, sizable capital inflows, real exchange rate appreciation, and increasing import penetration.

In summary, Turkish growth is constrained mainly by the fiscal imbalances during the 1990s and external imbalances after the year 2000. Considering all these developments, we aim to use an alternative approach that takes into account internal and external imbalances on the economic performance of Turkey.

Related Literature

Thirlwall (1979) developed the BOPCG theory by focusing on the relative growth rate adjustments required to balance trade at given relative prices. The model designed to understand long-run differences in growth performance. Since then, several contributions have been made. Thirlwall (2012) comprehensively review recent theoretical and empirical contributions to the BOPCG models.

The original formulation of Thirlwall’s law assumes that only the export revenues finance imports. However, if a country can attract capital inflows, this assumption is too restrictive. Thus, Thirlwall and Hussain (1982) revised Thirlwall’s law by taking into account the capital flows. In the modified model, changes in the export prices also affect the economic growth of countries by way of the real value of net capital inflows. This extended model allows for a continuously rising ratio of net borrowing; therefore, a country’s level of indebtedness relative to GDP can increase continuously. McCombie and Thirlwall (1997) modified the Thirlwall and Hussain (1982) model to make sure that the long-run economic growth is consistent with a sustainable path of foreign borrowing. Theoretical result of the modified model showed that capital inflows cannot permit a country to increase its growth rate above that given by Thirlwall’s law for a long period. Elliot and Rhodd (1999) further modified the Thirlwall and Hussain (1982) model by including the effect of debt servicing. Moreno-Brid (1998–1999) also extended the Thirlwall and Hussain (1982) BOPCG model by incorporating the constraint that the current account deficit to GDP ratio is constant in long-run equilibrium. Barbosa-Filho (2001) extends the balance of payments (BP)-constrained growth model to allow for a sustainable accumulation of foreign debt, taking into account both the potential instability of such a constraint and the impact of interest payments on debt accumulation. Moreno-Brid (2003) develops a version of the BOPCG model adapted from Thirlwall and Hussain (1982) that explicitly considers interest payments and generates a sustainable path of external debt accumulation.

In many BOPCG models, there are no relative price effects. However, according to some empirical studies, the impact of relative prices or the real exchange rate on economic growth is mixed. Prices may change in response to productivity growth and that change in relative prices may have a significant impact on export growth. Recently, Soukiazis et al. (2012, 2014) extended the BOPCG model further by considering the role of imbalances in public sector as an additional constraint on economic growth and allowing relative price not neutral in adjusting external imbalances. The similar model has been applied to Italy (Soukiazis et al., 2014), Portugal (Soukiazis, Cerqueira, & Antunes, 2013), Romania (Soukiazis et al., 2015), Slovakia (Soukiazis, Muchova, & Lisy, 2013), Greece (Soukiazis et al., 2018), and Nigeria (Panshak et al., 2019), and the result revealed that it is very coherent in identifying the most important determinants of growth.

Thirlwall’s original model previously tested for Turkey by Halicioglu (2012) by estimating the export and import functions for the 1980–2008 period. His results show that the average predicted growth rate is close to the average actual growth rate. However, he also finds that during the high inflationary periods (1992–2003), the actual and predicted growth rates are significantly different. Gokce and Cankal (2013) also tested the model indirectly for 1968–2011 period. They found a co-integrating relationship between output and export, and claimed that Thirlwall law is supported by the data. The vast majority of studies support the BOPCG hypothesis.

The Balance of Payment Constrained Growth Model With Internal and External Imbalances, Non-Neutral Relative Prices, and With Foreign Content

Soukiazis et al. (2014) model incorporates both internal and external disequilibria and hypothesized that relative prices are relevant factors. In this section, we extend the Soukiazis et al. (2014) model further by incorporating Turkey’s high intensity of imports in the aggregate demand components. The full derivation of the model is given in Appendix C (see Supplemental Material).

The Import Demand Function

Import demand is explained by the components of domestic income, contrasting the traditional model that relies on real aggregate GDP. Furthermore, it is assumed that relative prices play a significant role in determining import demand and that in the long run can have an effect on long-run economic growth. The import demand function with the above assumption is specified in growth rates as follows:

The above function shows that the growth rate in demand for imports

The Export Demand Function

The Turkish economy relies significantly on the importation of critical raw and intermediate goods, and equipment and machinery for export growth. Therefore, we extend the SCA export model in line with Muscatelli et al. (1995), and Saygılı and Saygılı (2011) by adding the import growth. Specification of the export growth equation in dynamic form is as follows:

The growth rate of export

Private Consumption and Investment Functions

Conventionally, long-run aggregate consumption depends mainly on total disposable income (earnings from holding public bonds and assets inclusive). We will presume that consumption growth is a function of all disposable income growth:

where

The private investment model is derived from the Keynes accelerator theory, postulating that the growth of gross investment

Here,

The Government Sector

The government budget is expressed in nominal values as given by the below identity:

Here, nominal government spending is represented by Gn, public debt owned by home bondholders is accounted for by BH, while BF represents public debt owned by foreign bondholders, real domestic income is captured by Y, P denotes the domestic price level, D is the public deficit, nominal interest rates compensation given to domestic and overseas public debt investors are captured by i and i*, respectively, e represents the nominal exchange rate, and t is the tax rate on nominal income. According to this expression, we are in the state of a public deficit when total current spending surpasses the tax revenues from domestic nominal income, that is, when

From the above expression, budget deficit ratio is represented by

The Balance-of-Payments Condition

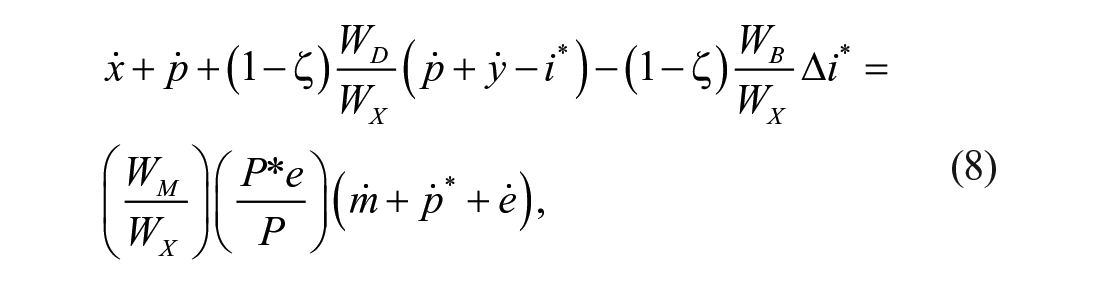

In the concluding part of the model specification, we model the external equilibrium condition by the below identity:

The left-hand side component of the equilibrium condition indicates the amount of monetary resources that will be used to finance imports (export revenues plus the amount of public deficit financed by foreign capital flows minus the interest payments to foreign bondholders).

The final identity can be represented as

where

Domestic Income Growth

Following in the dimension of Soukiazis et al. (2014) and imports in investment and export functions, the growth rate of domestic income can be obtained as 2

where

Domestic income growth model comprehensively specified above shows inter alia that the growth of real GDP is a function of both internal and external imbalances as well as relative prices. Precisely, the Numerator A is disintegrated in various components: the first term captures the shock of foreign demand on real GDP (i.e., domestic growth), the second term reveals the effect of substitution through the adjustments or changes of relative prices, the third term tells us how the trade volume affects domestic growth, and the last component of the numerator terms captures the impact of internal imbalances on domestic growth. The denominator measures the role and effect of the disaggregated import elasticities of the components of demand on domestic growth. We shall employ Equation 9 in explaining growth for Turkey.

Estimation and Application of Extended SCA Model for the Turkish Economy

We extended the Soukiazis et al. (2014) model further by incorporating Turkey’s high intensity of imports in the aggregate demand components. We estimate and test the model for Turkey and provide some assessment on the expected economic performance of Turkey, in a sense identifying policy options for higher economic growth for Turkey.

As we have seen in the overview of the Turkish economy in the “Internal and External Imbalances, and Growth in Turkey” section, the country faced with both fiscal imbalances in the 1990s and external imbalances after 2001. We test and verify the extended growth model in line with SCA that takes into account internal and external constraints and relaxes the assumption of relative prices being neutral for Turkey. The initial stage entails the estimation of all the four-system equation simultaneously. Therefore, import demand equation (1), the export demand equation (2), the private consumption (3), and investment equation (4) are estimated simultaneously to get the needed elasticity coefficients essential to compute the reduced form of domestic income growth as specified in Equation 9. As earlier indicated, this article uses growth rates of all the variables spanning 1990Q1–2016Q2 to estimate the derived four-system equation. The definition of the variables and the data sources are given in Appendix A. We used dummy variables for crisis periods, 1994, 2001, and 2009. We estimated our four-equation system by three-stage least squares (3SLS), which is more efficient for controlling the endogeneity of regressors and cross-equation error correlation. Table 1 gives 3SLS estimation results where endogeneity of the variables in the models and cross-correlation of the residuals across equations are taken into account. Exports, imports, consumption, and investment at growth terms as well as the growth rates of domestic income, government final expenditures, domestic disposable income, real effective exchange rate, and real domestic interest rate are assumed to be endogenous variables. The article assumes that other variables in the system as exogenous, including the lagged values of some of the variables (see Table 1). To check the robustness of our 3SLS estimation results, we estimated our four equations individually by two-stage least squares (2SLS) with using the same set of instruments. The Sargan test for over-identification reveals that the instruments used are valid and uncorrelated with error terms. It also demonstrates that the excluded instruments are correctly excluded from the estimated equation. The Breusch–Godfrey test for serial correlation results shows that the null hypothesis of no serial correlation cannot be rejected at the 5% significance level. The autoregressive conditional heteroskedasticity (ARCH) test results conform homoscedasticity of the residuals.3

3SLS Estimation of the Structural Growth Model: Turkey 1990–2016.

Note. Endogenous variables:

Exogenous variables:

3SLS = three-stage least squares.

10% significance level. **5% significance level. ***1% significance level.

When we look at the 3SLS estimation resuts in Table 1, we can assert that the parameter estimates are largely in conformity with the underlying theoretical postulation. Generally, elasticities demonstrate their expected signs and significance. Relative price elasticity in both import and export equations is highly significant with correct signs. Relative price elasticity of imports higher than that of exports in absolute value indicates that imports are more sensitive to relative price changes. Further comparing with the value of income elasticities, relative price elasticities are lower; this finding is in line with the literature confirming that the trade is more sensitive to income than relative price changes. In the import demand function, all the variables have correct signs and statistically significant at the 1% significance level, and government expenditure is significant at the 10% significance level. Import elasticity of investment and export are 0.328 and 0.318, respectively, while the consumption elasticity is 1.251, which indicates that imports increase more than proportionally with respect to the consumption increase.

Estimation results in Table 1 also show that income elasticity of consumption and investment are high, 1.034 and 2.370, respectively; the latter is confirming the accelerator principle in the investment function. Interest rate elasticity of investment is −0.163, which is significant but low relative to the other variables. In our specification of the investment equation, we added import growth as a new variable because with the liberalization of external account in Turkey, production structure changed by employing the significant amount of imported inputs, machinery, and equipment. Import elasticity of investment is .370 and statistically significant.

Estimation results of the export equation show that world income elasticity of the exports is 1.721, which implies that export is highly sensitive to foreign demand. This high sensitivity of exports to foreign demand should be a case of concern in the period of slowdown in foreign income and lose access to foreign markets. A contribution and novelty on the applicability SCA model for Turkey is the inclusion of imports in the export demand function.

The result shows that import growth positively stimulates the export growth of Turkey, and imports elasticity of exports is 0.312. This owes to the change in the production structure of the economy after external account liberalization and the large capital inflows resulting overvaluation of the domestic currency.

After estimating the core parameters of the structural model, we can compute the growth rate of domestic income in Turkey compatible with external and internal constraints as given in Equation 9. Table 2 reports the values necessary to compute the growth rate of domestic income in Turkey. Greek letters

Computation of the Growth Rates of Domestic Income in Turkey, 1990Q1-2016Q2.

Note. Actual growth rate

The aggregate import elasticity with respect to domestic income growth is obtained as 2.004.

When we embark on a comparative analysis of the actual average growth rate of domestic income for the period 1990Q1–2016Q2 (4.092%), the below bold conjectures could be outlined:

The growth predicted by original Thirlwall’s law is 3.727% using the aggregate income elasticity of imports (2.004), which is below the actual growth rate of 4.092%. The Turkish economy grew at a higher rate (0.365% per annum) than that allowed by the balance of payments equilibrium. Recall that Thirlwall’s law assumes that the balance of payments is in equilibrium, relative prices are neutral in the sense that does not play any significant role on growth, and capital flows and internal imbalances are not considered in the model.

The growth predicted by the Soukiazis et al. (2014) model where relative prices are not neutral and with internal and external imbalances is 5.868% per annum higher average growth rate (1.776) compared with the actual growth rate.

Finally, growth obtained by the extended model which takes into account external and internal imbalances and relative prices is not neutral, and import content of aggregate demand component is 4.836%. This growth rate is very close to the actual growth rate but slightly over predicts realized growth rate in Turkey. The difference between actual and the predicted growth rate, in this case, is 0.744% per annum. These results imply that Turkey could grow at a higher rate than it actually did without exacerbating external and internal imbalances.

Our results show that if we consider internal and external imbalances and non-neutrality of the relative prices and import content of aggregate demand component, the model predicts a slightly lower growth rate than the SCA model.

Turkey’s import sensitivity of the demand components is quite high, especially that of consumption

At the aggregate level, income elasticity of imports demand is high,

Many countries import too many raw materials and intermediate goods to produce exportable and domestic goods as well as final consumer goods; what is important here in the final goods that form products should contain high domestic value added. In international markets, most of the produced goods and exports contain a substantial share of imported components, but in terms of gains, the value added in exports embodying imported components must be much higher.

Turkey produced (and exported) low value-added domestic goods despite the move from low to medium or medium–high technology exports in recent years (Turkstat, 2018). On the contrary, the share of the general service sector including construction in the overall economy was about 45% at the beginning of the 1990s and has risen significantly representing 61% of the gross value added in 2016 against 20% in industry and 5% in agriculture (Turkstat, 2018). There was a significant drop in the share of industrial and agricultural sectors. Most of the service sector consists of a high number of micro enterprises with a substantial proportion of non-tradables and high informality. Therefore, to improve the external balance and growth performance of the country shift to more tradable sectors, decreasing informality in the economy will improve internal balance and hence can contribute to economic growth.

Scenario Analysis

Here, we carefully designed some possible and executable policy scenarios to enable us to identify the most suitable policies that will assist in positioning Turkey on the path of rapid and sustainable growth. This analysis is carried out in the dimension of the extended SCA model. The scenario analysis we apply focuses on attaining external equilibrium.

The model used here assumes that relative prices are not neutral. We check the effect of the depreciation of the domestic currency by assuming that the average value of growth rate of real relative prices for the whole period changes from

Alternative policy option could be to reduce import sensitivity of exports from

The growth rate of Turkey is also sensitive to import contents of the consumption and investment. Reducing imports sensitivity of consumption from

Reducing the imports to income ratio by 5% (from 0.238 to 0.226) will increase the predicted growth rate from 4.8364 to 6.3575; alternatively increasing exports to income ratio by 5% will result in 6.2336 growth rate. Furthermore, if we assume that the imports share is equal to the exports share

An increase in the foreign income elasticity of exports demand from

An increase in the foreign growth rate from 0.02 to 0.25 will increase growth rate from 4.8364 to 5.1171

An increase in the foreign holding of debt (reduction of domestic holding from 0.65 to 0.4) will increase the predicted growth from 4.8364 to 5.5287. The non-resident flows into the government debt securities market may lower the cost and smooth the cyclicality of domestic funding/savings over the years. Therefore, capital inflows are also very important for growth in Turkey.

Fiscal policy toward reducing income taxation: We observe that average income tax during 1991–2016 period is about 20%, if this tax rate reduces from t = 20% to t =10% (everything else constant), predicted growth rate by the model is

Government budget deficit policy toward reducing the public deficit and debt ratio: The period average of the budget deficit and debt to GDP ratio in Turkey is relatively low:

The period average of the domestic interest rates is relatively high in Turkey. Assuming a more favorable monetary policy of the Central Bank aiming at reducing the cost of financing of the economy by 20% (implied Δi = −0.0094) could help the economy to grow 5% which is much higher than the actual and the predicted growth rate. On the contrary, if foreign interest rates rise from period average of 4.3% to 5% (implied Δi* = 0.00723), the predicted growth rate falls significantly to 3.205%. If this increase reaches to 7% (with Δi* = 0.02723), growth rate will be 2.205%.

These exercises have shown that growth in Turkey is very sensitive to changes in the domestic and foreign interest rates, both due to domestic and foreign debt. Therefore, financing the domestic economy with lower interest rates is a considerable stimulus to growth. This implies that Turkey to grow faster should reduce the cost of financing.

The most effective policies to achieve faster growth in Turkey are related to the external sector; Turkey should implement structural reforms aiming at reducing chronic current account imbalances. Lowering imports to income ratio or increasing exports to income ratios will produce higher growth rates. Depreciation of the domestic currency also acts as a stimulus to growth.

Conclusion and Policy Implications

We extended the Soukiazis et al. (2014) model further by incorporating Turkey’s high intensity of imports in the aggregate demand components. We estimated the model for Turkey and provided some assessment on the expected economic performance, in a sense identifying policy options for higher economic growth for Turkey.

Our results show that Thirlwall’s Law predicts the average growth rate of the Turkish economy. Thirlwall’s Law assumes that external trade is balanced, public finances are at equilibrium, and relative prices are neutral.

The SCA model, which allows external sector and public sector imbalances and relative prices, is not neutral; the predicted growth rate is significantly higher than the actual average growth rate under investigation. This is mainly consistent with the external trade disequilibrium that the country has been accumulating over the years and further significant public sector imbalances during the 1990s in Turkey.

The extended SCA model, which considers internal and external imbalances and non-neutrality of the relative prices and import content of aggregate demand component, predicts slightly lower growth rate than the SCA model. The model estimated here is more complete one because it incorporates the foreign content of aggregate demand components. We can think of this extended SCA model as more realistic in terms of predicting the sustainable growth of the economy.

Our scenario analysis clearly shows that the most effective policies to achieve faster growth in Turkey is related to the external sector; Turkey should put every effort to obtain a positive net trade balance. Long waiting structural reforms should be implemented to ease the external constraints on the economic growth in Turkey. Lowering imports to income ratio or increasing exports to income ratio will produce higher growth rates. It is also shown that economic growth in Turkey highly depends on external demand when the strong depreciation of the domestic currency also acts as a stimulus to growth.

It should be noted that this article estimates the aggregate import function in line with the SCA-BOPCG framework. Therefore, in terms of the future direction of the research, it is necessary to estimate the disaggregated import function, specifically intermediate, capital, and final goods, to determine their precise implications on the Turkish economy.

Supplemental Material

SGO919493_Supplement_Material – Supplemental material for Effects of Internal and External Imbalances and the Role of Relative Prices on Economic Growth: Evidence From Turkey

Supplemental material, SGO919493_Supplement_Material for Effects of Internal and External Imbalances and the Role of Relative Prices on Economic Growth: Evidence From Turkey by Irfan Civcir and M. Emir Yücel in SAGE Open

Footnotes

Appendix A

Appendix B

2SLS Estimation of the Structural Growth Model: Turkey 1990–2016.

| Variables | Coefficient | SE | t statistics | p value | Sargan test | ARCH test | BG LM test |

|---|---|---|---|---|---|---|---|

| Imports growth | |||||||

| Constant | −1.614415 | 1.292585 | −1.25 | .212 | χ2(14) = 18.978 | χ2(1) = 0.7686 | χ2(2) = 4.9681 |

| Consumption, | 1.251216*** | 0.3871477 | 3.23 | .001 | p = .165 | p = .3807 | p = .0834 |

| Investment, | 0.3048663*** | 0.1134483 | 2.69 | .007 | |||

| Government expenditure, ġ | 0.1023899 | 0.65 | .519 | ||||

| Exports, ẋ | 0.0947727 | 2.57 | .010 | ||||

| Relative price, ṗ* + ė – ṗ | 0.0763201 | 7.21 | .000 | ||||

| R2 = .9200 | |||||||

| Consumption growth | |||||||

| Constant | −0.301939 | 0.2757247 | −1.10 | .273 | χ2(37) = 46.4095 | χ2(1) = 0.7885 | χ2(2) = 5.8621 |

| Disposable income, |

0.0426294 | 24.14 | .000 | p = .1359 | p = .3745 | p = .0531 | |

| R2 = .8741 | |||||||

| Investment growth | |||||||

| Constant | −7.95584*** | 0.9979547 | −7.97 | .0000 | χ2(15) = 16.6607 | χ2(1) = 0.0147 | χ2(2) = 4.8425 |

| Domestic income, |

0.2889553 | 8.21 | .0000 | p = .3396 | p = .9035 | p = .0888 | |

| Real interest rate. |

0.0843541 | 0.19 | .849 | ||||

| Inv. req. of imports, |

0.0820099 | 4.46 | .000 | ||||

| R2 = .8775 | |||||||

| Exports growth | |||||||

| Constant | 0.8828349 | 0.9527386 | 0.93 | .354 | χ2(13) = 16.1541 | χ2(1) = 0.1797 | χ2(1) = 5.0508 |

| World income, |

0.4362284 | 3.96 | .000 | p = .2409 | p = .6717 | p = .0800 | |

| Relative price, |

0.1034828 | −3.75 | .000 | ||||

| Export req. of imports, |

0.064276 | 4.84 | .000 | ||||

| R2 = .6293 | |||||||

Note. Endogenous variables:

**5% significance level. ***1% significance level.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.