Abstract

The article poses a dual research question: What are the determining factors of the type of audit opinion in a stressed economic environment and do these factors differ between family and nonfamily firms? Our results show that auditor tenure and return on assets (ROA) raise the probability of receiving a favorable opinion. On the contrary, losses during the previous year, high financial leverage, and hiring a “Big 4” firm increase the probability of receiving an unfavorable opinion. Although the sign and the statistical significance are similar, the size of such effects differs between family and nonfamily firms. Finally, the probability of receiving a report with a favorable opinion increases as the economic situation improves.

Introduction

Audit reports are the main tool used by auditors to confirm the veracity and reliability of the information given in financial statements. The type of audit opinion issued by an auditor not only indicates whether the organization is complying with accounting standards and is concerned about its financial management, but it is also an important factor for preventing fraudulent activities (Bell & Zimmerman, 2007). According to agency theory, auditing plays an essential role, because it aims to reduce the agency costs arising from the separation between the owners (shareholders, creditors, and suppliers) and those in control (managers and directors). Managers will therefore demand external audits to confer greater credibility on their accounting information (Jensen & Meckling, 1976). Furthermore, the recent global financial crisis has boosted the interest in audit opinions (European Commission, 2010). It is in turbulent times that auditors are most needed, because they must state the future viability of entities in their reports (Pedrosa & López-Corrales, 2018).

Although most of previous research on the determinants of audit opinions does not distinguish between family and nonfamily firms, the particularities concerning the governance and accountability of the latter make studying the differences between groups relevant. However, this is in contrast with the fact that family businesses are one of the most important economic engines for economies, being the most numerous institutions worldwide (Chua, Chrisman, & Steier, 2003; Gersick, Davis, Hampton, & Lansberg, 1997; Upton & Petty, 2010).

Hence, our article aims at filling this research gap focusing on two main questions. First, what are the determining factors of the type of audit opinion in a stressed economic environment, such as the so-called “Great Recession”? Second, do these factors differ between family and nonfamily firms? To answer both questions, we focus on both financial variables and auditor’s characteristics, and we rely on a sample of 9,873 private Spanish firms, of which 5,819 are family firms and 4,054 are nonfamily firms. The sample covers years 2011 to 2015, including both a recession and a period of recovery.

The contribution of this article is threefold: (a) It expands the academic literature by providing empirical evidence on the factors that determine the type of opinion issued by auditors for nonlisted firms, because most of the existing studies have focused on listed firms. (b) It covers both a crisis period and a period of economic recovery. Vanstraelen and Schelleman (2017) pointed out that there is limited empirical evidence on auditor behavior when issuing opinions in times of financial crisis, particularly for nonlisted firms. (c) It sheds additional light on the relatively unexplored topic of the audit opinion in family firms by classifying firms as family and nonfamily firms. 1

Our results involve several practical and relevant implications. First, both longer auditor tenures and higher return on assets (ROA) values raise the probability of receiving a favorable opinion. Second, the opposite effect is produced by a higher financial leverage (FINL), losses during the previous financial year, and the fact of hiring one of the Big 4 auditing firms. Third, the probability of receiving favorable opinions is pro-cyclical: It is positively correlated with gross domestic product (GDP) growth rates. Finally, the effect of both ROA and FINL is stronger in the case of family firms, but the impact of losses and auditor tenure is weaker.

This article is organized as follows. Section “Auditing and Family Businesses: The Spanish case” explains the relevance of the Spanish case. Section “Literature Review and Hypothesis Development” reviews the related literature and presents the hypotheses. Section “Research Method” describes the research method as well as the sample selection, data collection, variables applied in the analysis, and econometric methodology. Section “Empirical Results” presents the results along with the summary statistics and regression results. Finally, section “ Conclusion and Discussion” concludes with implications, limitations, and suggestions for future research.

Auditing and Family Businesses: The Spanish Case

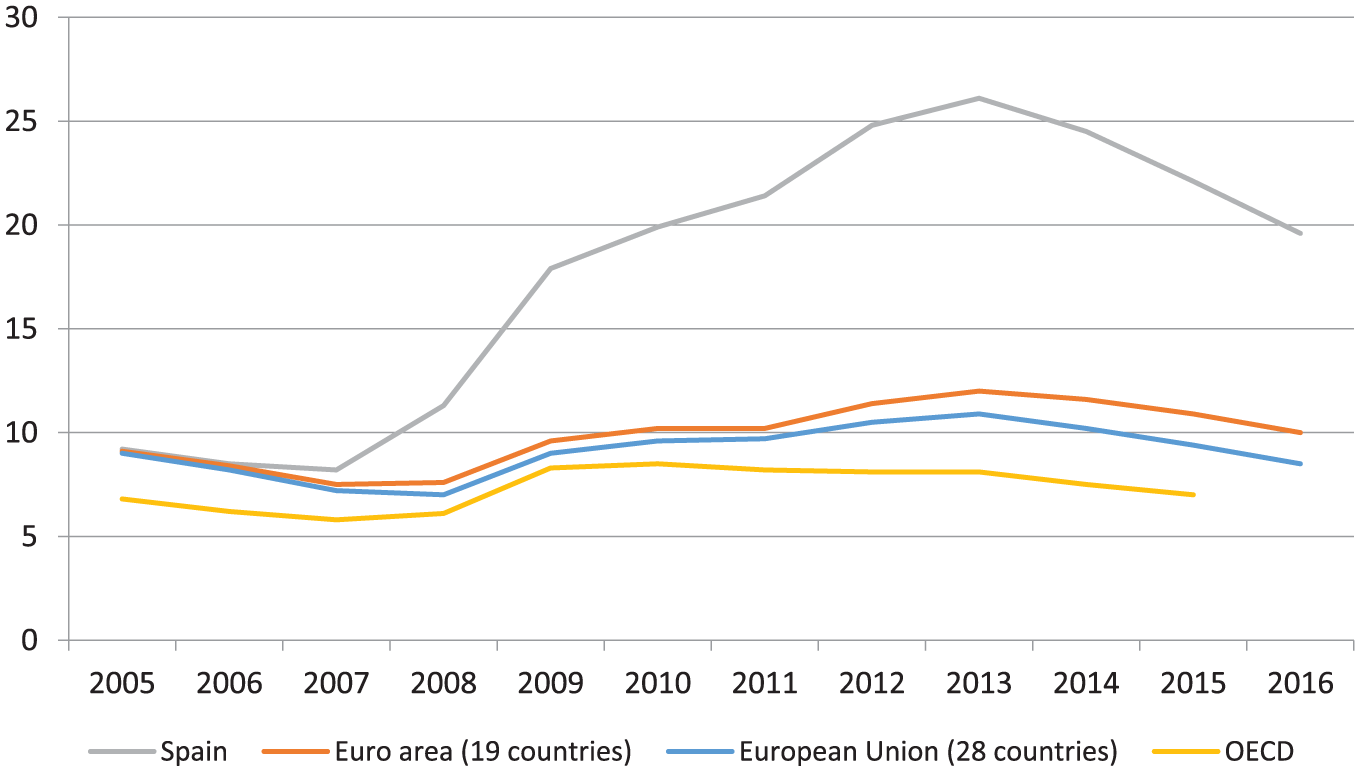

The “Great Recession” shocked the world economy as a whole but asymmetrically. Some countries faced the worst economic scenario in decades. Among the largest economies in the Organisation for Economic Co-operation and Development (OECD), Spain provides a particularly interesting case for a study of the causes and consequences of this recession as it is one of the countries that the crisis has affected most, in terms of both GDP (Figure 1) and employment (Figure 2). The unemployment rate rose above 25% (2012), the highest level of all developed economies (Álvarez-Díaz, Caballero, Manzano, & Martín-Moreno, 2015).

Annual growth rates of GDP in Spain, UE28, Eurozone19, and OECD34 (2005-2016).

Evolution of the rate of unemployment in Spain, Eurozone19, EU28, and OECD34 (2005-2016).

Family Businesses in Spain

In the EU25 in 2015, there were 17 million family businesses, which generated 100 million jobs. Family businesses account for 60% of all the institutions in the European Union (EU) and employ between 40% and 50% of all workers (European Economic and Social Committee, 2016). In the United States, family businesses represent 80% of the business network and 50% of private employment. In Spain, those figures are larger. There are 1.1 million family businesses (89% of the total companies). Their special features make this type of companies the largest generator of domestic employment (67% of private employment with 6.6 million jobs). They are also responsible for 57% of the GDP in the domestic private sector (European Family Business, 2015).

Casillas, Barbero, and Moreno (2013) analyze the differential behavior of Spanish family businesses in turbulent times. They argue that the familiar character of the company can exert as much a positive influence as negative in relation to the intensity and the sense of the processes of restructuring to deal with negative results. The family nature can favor the rapid development of readjustment or change of direction strategies, insofar as these companies have shown a greater entrepreneurial orientation (Casillas, Moreno, & Barbero, 2010; Nordqvist & Melin, 2010). This entrepreneurial orientation not only allows this type of company to identify and exploit new business opportunities but also provides them with greater capacity to react to unsatisfactory results through disinvestment processes or reallocation of resources. However, family owners tend to show a greater commitment to the family business, as evidenced by the stewardship approach (Eddleston & Kellermanns, 2007). This approach shows that family businesses present a greater orientation to the stewardship that is reflected in a stronger focus on the long term, toward its employees and its clients (Miller, Le Breton-Miller, & Scholnick, 2008). It prevents making drastic decisions that may affect the organization, trying to maintain the traditional jobs, products, and strategies of the company.

Auditing in Spain

For unlisted companies, the Spanish legislation establishes that companies have an obligation to be audited when, for two consecutive years and at the close of one of them, they meet at least two of the following three circumstances: (a) total assets in excess of €2,850,000, (b) a net annual turnover in excess of €5,700,000, and (iii) an average number of employees during the year in excess of 50.

Current regulations in Spain on the types of opinion to be issued in the audit report were modified in 2010 with the aim of adapting them to the International Standard on Auditing (ISA). The current regulations, applicable to the audit reports issued as of January 1, 2011, are published by the Spanish regulatory body (Institute of Accounting and Audit of Accounts) and regulated by ISA-ES 700 and 705. According to this legislation, two types of opinion can be issued. In the case of unmodified opinions (favorable opinions), the auditor concludes that the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. By contrast, in the case of modified opinions (unfavorable opinions), the financial statements as a whole are not free from material misstatement or there is not sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement. In both cases, the auditor modifies the opinion in the auditor’s report in accordance with ISA 705. This ISA establishes three types of modified opinions, namely a qualified opinion, an adverse opinion, and a disclaimer of opinion.

On the other contrary, it is important to highlight the importance of the auditor pronouncing himself in the report on the going concern problems of a company that had special notoriety in the writing of the audit reports during the recent financial crisis. ISA 570 establishes the types of opinion to be issued in the report when there is material uncertainty regarding going concern problems, taking into account whether the company’s management adequately reveals these problems in the financial statements. In this sense, the opinions to be issued could be a favorable opinion with a paragraph on material uncertainty regarding going concern problems, a qualified opinion, or an adverse opinion.

Literature Review and Hypothesis Development

Literature Review

Most of the existing literature has focused on the variables that may explain or affect the opinion issued by auditors in their reports. Gosman (1973) obtained statistically significant relationships between the probability of receiving a report with certain types of reserves and the size of both the firm and the auditing company. Subsequently, Warren (1980) studied the characteristics of firms that received qualified reports, providing significant results for the size of the audited firm, its sector, and the type of auditor. Krishnan, Krishnan, and Stephens (1996) searched for a link between the probability of receiving a qualified report and a change in the auditor. Their results indicated that firms that receive a qualified opinion have a less stable financial situation, and their systematic risk (measured by the beta), customer/assets ratio, inventory/assets ratio, and ROA are lower than those of firms receiving a favorable opinion are. Furthermore, firms that change their type of auditor are smaller. Laitinen and Laitinen (1998) conducted a study to develop a model for Finnish limited liability companies based on their financial statement information to identify qualified audit reports. Univariate analysis showed that the qualification of an audit report is mainly associated with low profitability, high indebtedness, and low (negative) growth.

None of these studies distinguishes between family and nonfamily firms. However, family businesses have different characteristics regarding management, long-term orientation, the combination of financial and nonfinancial objectives, the perception of environmental opportunities and threats, the entrepreneurial activities undertaken, and so on. A family firm is interested in passing on its legacy down the generations, so it presents greater risk aversion (Hiebl, 2012). Furthermore, in most family businesses, ownership is concentrated in the hands of few shareholders, which allows decisions to be made quickly, reducing agency costs. When this happens, a better performance is achieved for family firms than for nonfamily firms (Cai, Luo, & Wan, 2012; Minichilli, Brogi, & Calabrò, 2016). If such differences exist in management and corporate governance, then they might also exist in accounting, financial information, and auditing. For instance, Low and Majid (2008) concluded that the relation between family businesses and modified audit opinions is negative, implying that family-controlled firms are less likely to receive modified audit opinions than nonfamily firms, with the same result if the CEO is also the Chair of the Board of Directors in family businesses. It seems, therefore, that a family business is more likely to receive a favorable opinion, especially if power is concentrated (which results in lower agency costs).

Hypothesis Development

Audit opinions and the result of the previous financial year

Tsipouridou and Spathis (2014) analyzed Greek listed companies and distinguished between audit opinions that are qualified according to the going concern principle and those that are qualified for other reasons. They concluded that firms with a low financial performance during the financial year audited or with losses in the previous year and small firms are more likely to receive a going concern opinion. In the same vein, F. Chen, Peng, Xue, Ynag, and Ye (2016) found that listed Chinese companies with accounting losses are more likely to receive modified (unfavorable) opinions. The auditor is more likely to issue a report with a modified audit opinion in an attempt to limit his responsibility. However, the long-term focus of family firms makes short-run financial results less important for auditors as signals of structural problems. Hence, we pose the following hypothesis:

Audit opinions and Big 4 auditors

Several studies have related audit opinions to the auditor issuing them. Some studies have found differences between the various firms existing in the audit market and the probability of an unfavorable opinion and shown that international firms, which are associated with the best reputation, are more likely to issue unfavorable opinions than smaller firms (DeFond, Raghunandan, & Subramanyam, 2002; Lennox, 2000; Warren, 1980). Large audit firms are less prepared to accept problematic accounting practices and more likely to point out errors and irregularities (Duréndez & Maté, 2012). Habib (2013) performed a meta-analysis of 73 empirical studies published in high-impact auditing and accounting journals over the period 1982-2011 and observed that the Big 4 are positively associated with a modified audit opinion. Small audit firms, on the contrary, have less capacity for finding errors or are reluctant to report any errors that they find (Wang, Wong, & Xia, 2008).

Previous studies have indicated that the large international auditing firms, now called the Big 4 (Deloitte, PriceWaterhouseCoopers, KPMG, and Ernst & Young), have a distinctive reputation derived from the existence of a recognized brand name, providing higher quality audits than other companies (DeAngelo, 1982). Specific studies on family businesses have shown that such firms are less likely to take on the services of the Big 4, probably because of lower agency costs (Niskanen, Karjalainen, & Niskanen, 2010). However, once a family firm chooses to hire a Big 4 auditor, professionalism, brand image, and reputation maintenance should ensure that the treatment received would be similar to a nonfamily company. In view of the above, our second hypothesis is as follows:

Audit opinions and the ROA

The ROA is a measure of the financial risk to which the company is subject. If it is too low, it may indicate economic management problems. Previous studies have observed that ROA is a key factor in the early detection of problems in a business (Jones, 1996). Firms with low financial performance are more likely to manage earnings upward, which increases the likelihood that they will receive a modified audit opinion (Chan, Lin, & Mo, 2006; C. J. P. Chen, Chen, & Su, 2001). Gallizo and Saladrigues (2016) observed that the lower economic return obtained made it more likely that the auditor issued an audit report modified by going concern opinion; consequently, they confirmed their presumption that low profitability was a factor for the early detection of a modified audit opinion. In any case, their long-term vision plays again in favor of family businesses: We expect that a higher ROA will have a higher reward for family firms.

Audit opinions and FINL

The literature has related the amount of leverage to the financial risk, because high levels of debt may lead to liquidity problems. Authors such as DeFond et al. (2002) have observed that the probability of receiving a modified (unfavorable) audit opinion is greater when firms have high degrees of leverage. Later, Carey, Simnett, and Tanewski (2000) showed that, in an unregulated environment, the demand for external auditing in family firms is positively correlated with agency conflicts and with the level of firm debt. However, we have not a clear prediction on the difference between family and nonfamily firms. We therefore pose the following hypothesis:

Audit opinions and Auditor tenure

The effects of tenure on auditor independence have mostly been addressed through the study of going concern modified opinions (GCMOs) in financially distressed firms. The evidence obtained is mixed. Carcello and Neal (2000) did not find negative effects of tenure on the likelihood of GCMOs being issued to financially distressed firms in the United States. However, recent research has provided somewhat contradictory results. Although Lim and Tan (2010) reported a positive effect of tenure on audit quality in the United States, Gul, Basioudis, and Ng (2012) in the United States and Firth, Oliver, and Wu (2012) in China concluded that auditors are willing to forgo independence by issuing fewer GCMOs in longer tenures. This is in line with results by Lennox (2000), who observed that the probability of changing auditor increases after a qualified report is received. Khalil and Mazboudi (2016) offered research focused on the possible peculiarities of the relationship between auditors and family firms. They found that audit firms are less likely to resign in family firms. If family firms accept qualified reports better than nonfamily firms, independence of auditors should be greater and the effect of tenure should be weaker. We thus formulate the following hypothesis:

Audit opinions and the economic cycle

A macro financial crisis leads many companies to have liquidity problems and significant losses, thus increasing their level of risk. They fail to comply with the conditions specified in their debt contracts, often having to carry out refinancing operations on their loans. The whole functioning of companies is affected and then the likelihood of receiving an unfavorable opinion in its audit report is greater (Geiger, Raghunandan, & Riccardi, 2014; Mareque, López-Corrales, & Pedrosa, 2017; Tsipouridou & Spathis, 2014; Xu, Carson, Fargher, & Jiang, 2013; Xu, Jiang, Fargher, & Carson, 2011). Furthermore, in turbulent times, auditors face greater possibilities of being sued if their clients go bankrupt or if they have extremely high losses (Rittenberg, Johnstone, & Gramling, 2012). It involves that auditors tend to increase their propensity to issue GCMOs to protect themselves from the risk of litigation (Thoman, 1996; Xu et al., 2013). Finally, family businesses support financial crises better than nonfamily companies. Zhou, He, and Wang (2017) find that family firms outperformed nonfamily firms during the crisis. They also find that during the global financial crisis, founder firms invested significantly less and had better access to the credit market than nonfamily firms. They suggest that the superior performance of founder firms is largely caused by their lower incentive to overinvest to boost short-term earnings.

Based on the above, and bearing in mind that the period analyzed corresponds to the last years of the Great Recession (2011-2013) and the beginning of the subsequent expansion (2014-2015), we pose the following hypothesis:

Research Method

Sample Selection and Data Collection

The procedure used to build the database was taken from prior studies by Arosa, Iturralde, and Maseda (2010), among others, and from information obtained in the field by the Network of Family Business Chairs in Spain. The requirements for firms were as follows: limited companies (Sociedad Anónima [SA]) or limited liability companies (Sociedad de Responsabilidad Limitada [SL]), active in 2015, sales in excess of €2 million a year, or 10 or more employees during 1 of the 3 years from 2011 to 2013. Finally, taking this database of 118,932 firms (classified as family and nonfamily firms), we used the SABI database to select those that had received an audit opinion during the five financial years analyzed, 2011-2015.

To distinguish between family and nonfamily firms, we used the official definition of family firms agreed in 2008 in Brussels by the Groupement Européen des Entreprises Familiales (GEEF) and in Milan by the Board of the Family Business Network (FBN), the two main international bodies representing family businesses. The report of the Commission’s group of experts on family businesses recommended the adoption of the following definition of family businesses: (a) the majority of decision-making rights is in the possession of the natural person(s) who established the firm or who has (have) acquired the share capital of the firm or in the possession of their spouses, parents, children, or children’s direct heirs; (b) the majority of decision-making rights are indirect or direct; (c) at least one representative of the family or kin is formally involved in the governance of the firm; and (d) listed companies meet the definition of a family enterprise if the person who established or acquired the firm (share capital) or his or her families or descendants possess 25% of the decision-making rights mandated by their share capital.

The final sample comprises a total of 9,873 firms, 5,819 family firms and 4,054 nonfamily firms, according to the classification established by the European Family Business (2015). The study period is 2011-2015. The year 2011 was chosen as the starting point because the regulations on types of audit opinion in Spain were changed in 2010 to adapt them to international auditing standards. The main difference with regard to the previous regulations was that previously any uncertainty or doubts about a firm’s capacity to continue as a going concern necessarily led to an unfavorable opinion. Hence, in the same circumstances, an opinion would not necessarily be the same before and after this change in regulation and, obviously, the database used (SABI) gives the audit opinion issued according to the standards applicable at the time.

Variable Design and Measurement

Dependent variable

The dependent variable OPINION is a dichotomous variable taking the value 1 if the type of audit opinion is modified (unfavorable), and 0 otherwise.

Independent variables

LOSS was included in the model to analyze firms’ operational risk (DeFond et al., 2002). A firm that reports continued losses is more likely to receive an unfavorable report, so the relation between the two variables is positive. As in previous studies (Ghosh & Tang, 2015), this variable is dichotomous, taking the value 1 when the firm obtains negative ordinary income during the previous year and 0 otherwise.

The ROA is defined as the quotient between the operating income for the financial year (EBIT) and the total assets (Cascino, Pugliese, Mussolino, & Sansone, 2010; Ghosh & Tang, 2015; Niskanen et al., 2010). The relation between this variable and the opinion is expected to be negative, because the lower the ROA, the greater the probability that a modified (unfavorable) opinion will be received.

FINL seeks to capture the risk of default. It is defined as the quotient between the debt and the total assets (Cascino et al., 2010; Niskanen et al., 2010), and the relation between the FINL and the opinion is expected to be positive.

BIG 4 aims to analyze the probability that the size of the audit firm may influence the probability of receiving an unfavorable opinion. It is defined as a dichotomous variable taking the value 1 if the firm is audited by one of the Big 4 (Deloitte, PriceWaterhouseCoopers, KPMG, and Ernst & Young) and 0 otherwise (Niskanen et al., 2010).

TENURE is calculated as the number of consecutive years in which the same auditor audits the firm (Ghosh & Tang, 2015). Although the evidence is mixed, a negative relation is expected between this variable and the opinion; that is, the longer the auditor’s tenure in a firm, the less likely it is that the opinion will be modified (unfavorable).

The variable FAMILY identifies the subgroup of family firms within the sample. It is a dummy variable coded 1 for family firms and 0 otherwise.

Concerning the period effects capturing changes in the endogenous variable explained by the dynamics of the economic cycle, a set of period dummy variables is included in the specification. The year 2011 is the benchmark for coefficients.

Apart from the above variables, initially another three were included: the ZFC index, auditor change, and the liquidity ratio. The ZFC index measures the degree of financial tension in a firm with the aim of predicting business failure. As the results obtained in the estimates were similar using either the ZFC index or the ROA and the debt ratio (FINL), we decided to use the latter two, which we noted were the most widely used in prior studies on family businesses. When the auditor change variable was included in the model together with the TENURE variable, we found problems of multicollinearity, so we decided to use only the latter. Finally, the liquidity ratio showed a very low level of significance in the preliminary estimates, so we considered it to be irrelevant and decided to exclude it.

Summary Statistics

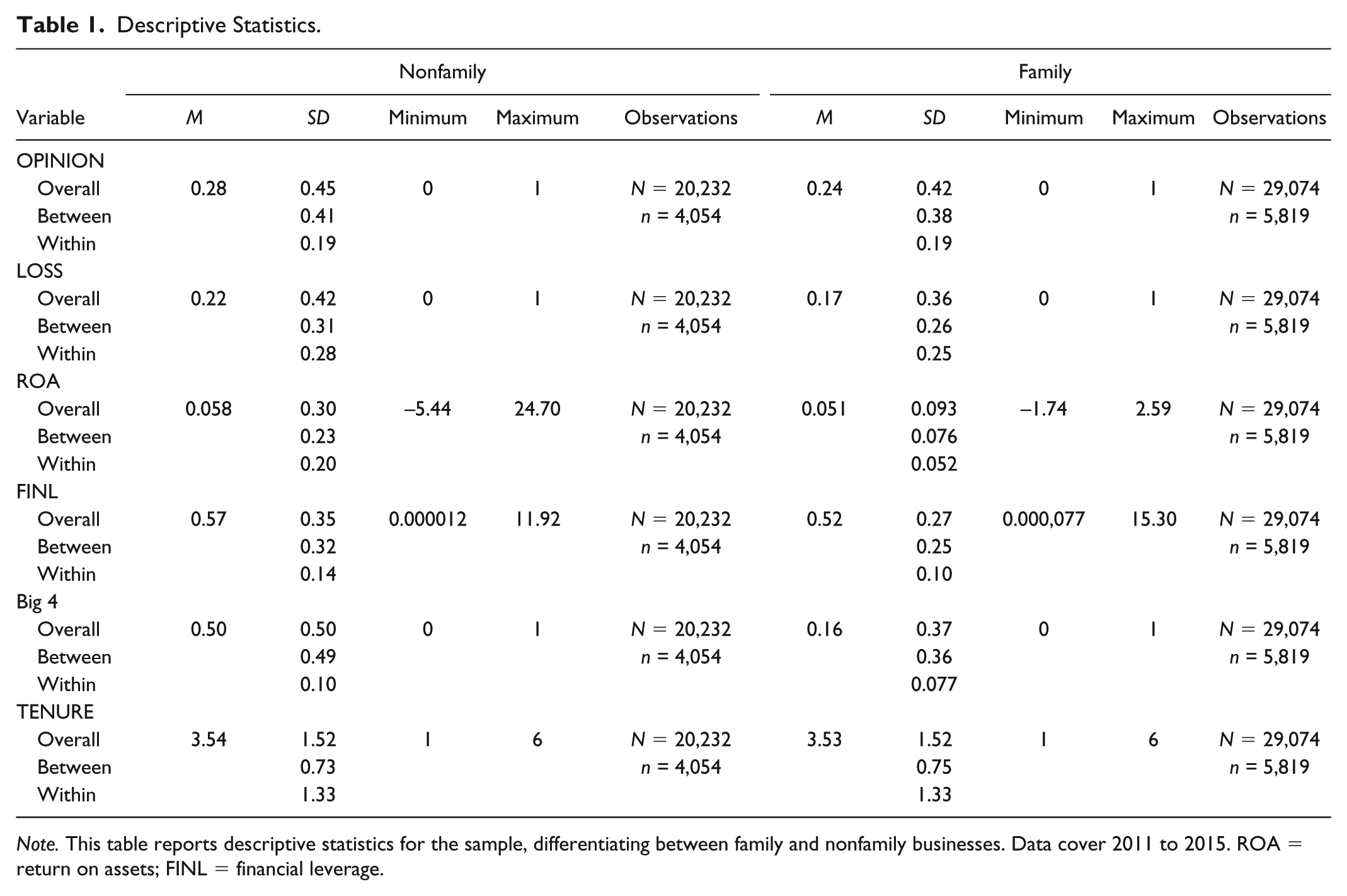

Table 1 presents the descriptive statistics for the dependent variable and for the independent variables, distinguishing between family and nonfamily firms, with family firms representing 58.96% of the total sample. An average of 28% of the nonfamily firms received a modified (unfavorable) opinion, as opposed to 24% of the family firms.

Descriptive Statistics.

Note. This table reports descriptive statistics for the sample, differentiating between family and nonfamily businesses. Data cover 2011 to 2015. ROA = return on assets; FINL = financial leverage.

An average of 22% of the nonfamily firms reported losses during the year (LOSS), as opposed to 17% of the family firms. The ROA and FINL amounted, respectively, to an average of 5.8% and 57% in nonfamily firms and 5.1% and 52% in family firms. One of the Big 4 audited 50% of the nonfamily firms, as opposed to 16% of the family firms. Finally, auditor tenure was similar in family and nonfamily firms, about 3.5 years.

Specifications and Econometrics

A number of preliminary estimates were performed to select the specifications and choose the most appropriate econometric methodology. The need to include both individual and time or period effects was clearly supported by Wald tests applied to panel least squares (PLS). A Hausman test showed a high and significant correlation between random effects and explanatory variables, so the fixed-effects option was required. This solution makes it unnecessary to include time-invariant control variables (such as sector, region, and variable FAMILY in levels) or variables that are mostly invariant in the short run (size). Their effect on the endogenous variables would already be captured by the individual effect. The autocorrelation fades once both individual and period fixed effects are included: the estimated AR(1) coefficients on the PLS residuals in Tables 2 and 3 are between 0.11 and 0.14 in all cases.

Estimates of Specifications (1) and (2).

Note. Ordinary t-statistics in parenthesis and robust PCSE statistics in brackets. Computations performed using Stata 14. All regressions include individual fixed effects. ROA = return on assets; FINL = financial leverage; PLS = panel least squares; PCSE = panel corrected standard error.

Significant at the 10% level, two-tailed. **Significant at the 5% level, two-tailed. ***Significant at the 1% level, two-tailed.

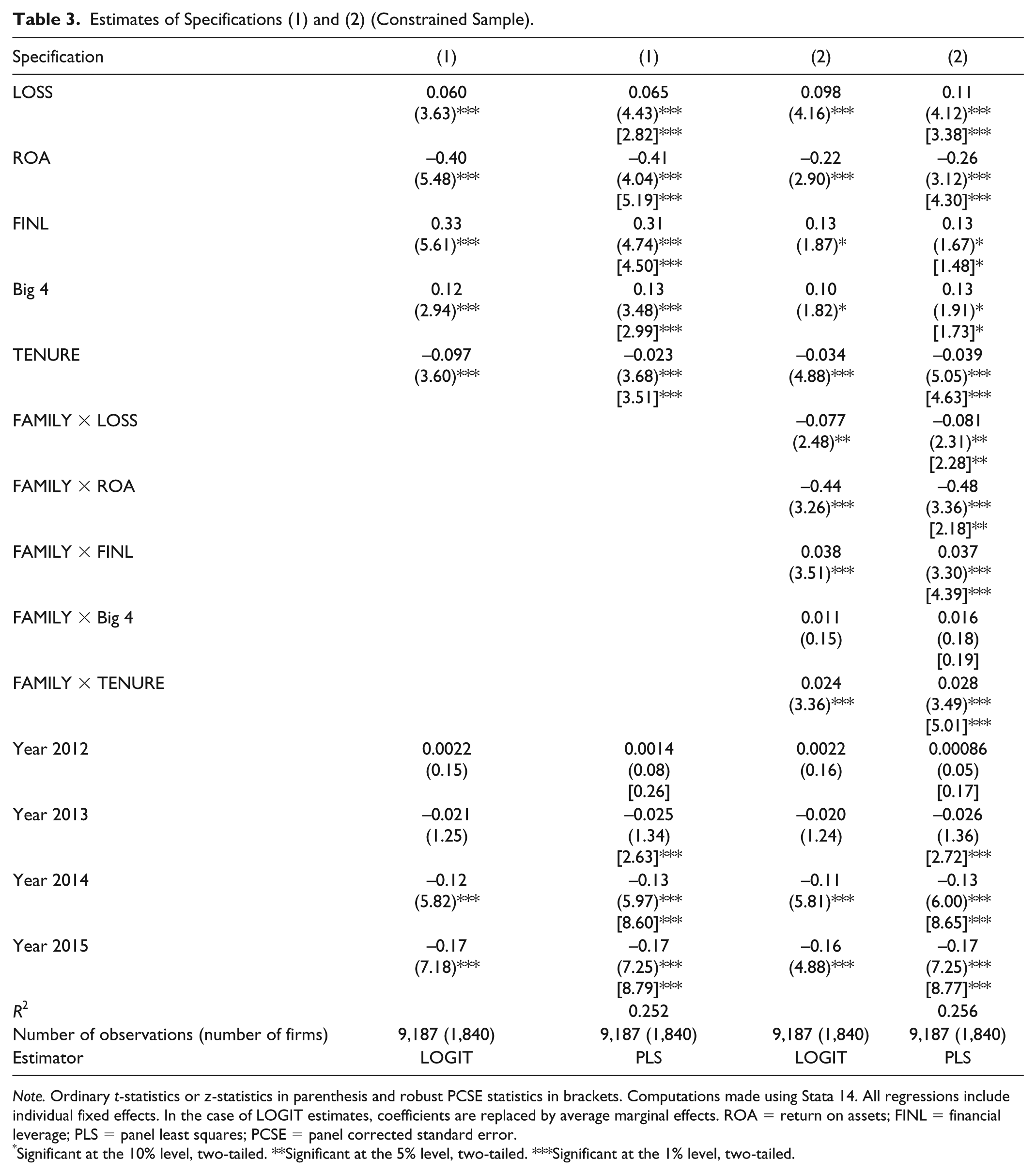

Estimates of Specifications (1) and (2) (Constrained Sample).

Note. Ordinary t-statistics or z-statistics in parenthesis and robust PCSE statistics in brackets. Computations made using Stata 14. All regressions include individual fixed effects. In the case of LOGIT estimates, coefficients are replaced by average marginal effects. ROA = return on assets; FINL = financial leverage; PLS = panel least squares; PCSE = panel corrected standard error.

Significant at the 10% level, two-tailed. **Significant at the 5% level, two-tailed. ***Significant at the 1% level, two-tailed.

To check the sensitivity of the results to both cross-contemporaneous correlation and cross-sectional heteroscedasticity, robust panel corrected standard errors (PCSEs; Beck & Katz, 1995) were also computed in the PLS estimates and are reported in Table 2. Multicollinearity is not a serious concern. The bivariate linear correlation coefficients among regressors are below 0.22 in all cases.

As discussed above, PLS provide the flexibility to deal with dynamic issues in panel data and test for different kinds of potential problems. To test the robustness of the results, conditional fixed-effect logistic regression, which is particularly suitable for dealing with dependent binary variables, was also used to estimate (1) and (2) in Table 3. However, relying on the logistic regression involves a dramatic reduction in observations, because all groups with all positive or all negative outcomes over the period 2011-2015 (8,033 firms in our case) were dropped. 2 Hence, Table 3 reports the results from the subsample of firms with at least one change in OPINION. To make the comparison easier, the regression coefficients were replaced with the average marginal effects (in the case of LOGIT estimates).

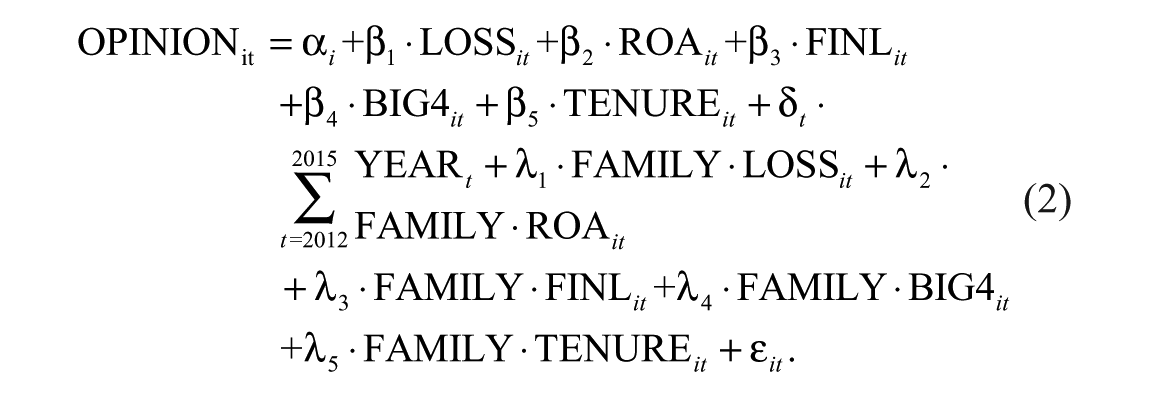

In sum, the following two specifications were estimated by both PLS and LOGIT, including individual fixed effects in both cases:

In Equation 1, both family and nonfamily firms are merged and common coefficients are imposed. In contrast, specification (2) is more flexible and estimates different slopes for each group. Insofar as the FAMILY variable is a dummy variable coded 1 for family firms and 0 otherwise, the coefficient for each variable would be β for nonfamily firms and β + λ for family firms. Of course, if λ is not significant at the 10% level or less, we conclude that the coefficient β would be the same for both groups. For instance, the LOSS coefficient would be β1 for nonfamily firms and β1 + λ1 for family firms.

Empirical Results

Regression Results

Econometric results are reported in Tables 2 and 3 and are robust to both the econometric methodology and the sample. The signs are as expected. The statistical significance for most variables is very similar across both tables. Finally, the coefficients are mostly the same for both PLS and LOGIT but are different when the tables are compared. Bear in mind that Table 2 includes observations for all firms and Table 3 only those for firms with at least one change in OPINION.

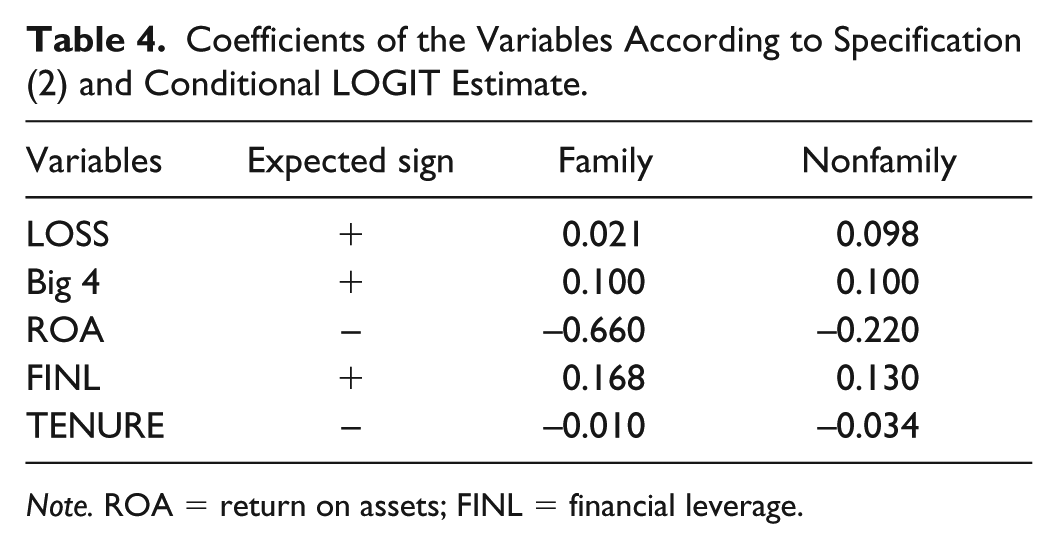

Concerning the coefficients, the reference that we chose is the effect of the variables in Table 4, in which the focus is on the firms with a change in status in the dependent variable. The direct effect of this exclusion is that the coefficients tend to be higher in absolute values, and, as there is a very substantial reduction in the number of observations, the difference is considerable.

Coefficients of the Variables According to Specification (2) and Conditional LOGIT Estimate.

Note. ROA = return on assets; FINL = financial leverage.

The results of the model suggest that the probability of receiving a modified (unfavorable) opinion is greater if the firm reported losses during the previous financial year. This evidence supports Hypothesis 1; furthermore, the coefficient for nonfamily firms (β1 = 0.098) is observed to be greater than that for family firms (β1 + λ1 =0.021) (see Table 4).

Hypothesis 2 is also accepted. The variable Big 4 is significant for the sample as a whole. Moreover, there are no significant differences between family and nonfamily firms; that is, the Big 4 do not systematically treat family and nonfamily firms differently.

Regarding the ROA variable, Hypothesis 3 is confirmed; that is, the greater the profitability ratio, the lower the probability of receiving a modified (unfavorable) opinion. As expected, the coefficient for nonfamily firms (β1 = −0.22) is lower than that for family firms (β1 + λ1 = −0.66).

Hypothesis 4 is also confirmed. The larger the FINL, the greater the probability of receiving a modified (unfavorable) opinion. The coefficient for nonfamily firms (β1 = 0.13) is slightly lower than that for family firms (β1 + λ1 = 0.168).

Concerning Hypothesis 5, we show that the longer the auditor’s tenure, the lower the probability of receiving a modified (unfavorable) opinion. Again, as expected, the effect for nonfamily firms (β1 = −0.034) is stronger than that for family firms (β1 + λ1 = −0.01).

Finally, the coefficients and statistical significance of the time dummies show that the probability of receiving a report with a favorable opinion increased as the economic situation improved in Spain, especially from 2014.

Conclusion and Discussion

Implications for Research and Practice

The aim of this article was to analyze the determining factors for the type of audit opinion and to ascertain whether they differ between family and nonfamily firms. Based on the prior literature, we examined the influence on the audit opinion of losses during the previous financial year, the type of auditor, the ROA, the level of FINL, and the auditor tenure.

Our results suggest that the auditor tenure and ROA raise the likelihood of receiving a favorable report. In contrast, reporting losses in the previous year, high FINL, and hiring one of the Big 4 all increase the probability of receiving a modified (unfavorable) opinion.

Results are slightly different when we compare family with nonfamily firms. Although signs are the same, the size of coefficients on all variables differs, except in the case of Big 4 where the symmetry is not rejected by data. In particular, the effect of LOSS and TENURE is much less intense, the influence of ROA is much stronger, and the impact of FINL is slightly stronger. Further research is required to disentangle the reasons of those differences.

Concerning the incidence of the business cycle, we observe that firms are less likely to receive an unfavorable opinion in good times than in turbulent times. Auditors increased their propensity to issue reports with a modified audit opinion at the beginning of the deep crisis because of the increased regulatory scrutiny, the increased risk of audit error, and a potential increase in reputational damage and litigation risk.

Although the results obtained may be of interest to both researchers and external and internal users of audit reports, we believe that they will be of most importance to business managers, enabling them to improve the way in which they manage and control their firms.

Limitations and Future Research

This study acknowledges some limitations. First, it uses a single-country sample. For future work, it would be interesting to extend the analysis to other countries with different institutional frameworks to compare the outcomes. Second, the use of the SABI database meant that we could not include audit variables (such as an audit report lag, audit fees, nonaudit fees, the existence of material uncertainty regarding going concern problems, the gender of the auditor, and so on), which have been considered to be relevant in other research. Finally, we only studied the family effect, considering all family firms to be homogeneous. An interesting avenue for future research would be to investigate the factors by classifying family firms into subgroups according to variables such as generation, family involvement, percentage of ownership, and so on. Additional aspects that might be of interest after the recent crisis are audit fees and going concern problems.

Footnotes

Acknowledgements

We thank Alejandro Domínguez and Fernanda Martínez for superb research assistance. The authors acknowledge financial support from the Chair of family business (University of Vigo).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article has been developped with the support of the Chair of Family Business of the University of Vigo.