Abstract

Despite its growing popularity, the term business model has not been uniquely defined so far. Within the management science and practice, it has been frequently confused with other popular terms. This article aims to bring clarity into what stands behind the business model concept by providing a review of the most common themes used in defining business model elements. It also discusses the relationship between the concept of a business model, on one hand, and strategy and sustainability, on the other. A few conclusions emerge. First, although there are no generally accepted definitions for either the business model or its building blocks, academics and practitioners agree that a business model is all about value. Second, a business model is not the same as a strategy but it has an important role in strategy implementation. Third, sustainability is found to be a hot topic for business models and has been increasingly used in symbiosis with this concept. Besides being a theoretical contribution to a definition of the business model as an independent concept, the findings may be particularly helpful to managers and business practitioners seeking ways to enable their firms to deal with complex market challenges and gain competitive advantage.

Introduction

The business model concept has become very popular in terms of a company’s competitive success as well as in management science. Regarding companies, whenever a business venture is established, it either explicitly or implicitly employs a particular business model (Teece, 2010), and for a venture to become viable, a sound business model is required (Magretta, 2002). Also, business model design and innovation are of critical importance for a company’s performance and success (Kesting & Günzel-Jensen, 2015; Zott & Amit, 2007; Zott, Amit, & Massa, 2011).

These claims may sound very clear and logical, but a question arises: Do we know how to build a sound and innovative business model? Put differently, what stands behind this concept? Recently, many authors from various fields of research have been looking for appropriate answers (Arend, 2013; Casadesus-Masanell & Zhu, 2013; Chesbrough, 2007; Johnson, Christensen, & Kagermann, 2008; Kesting & Günzel-Jensen, 2015; Klang, Wallnöfer, & Hacklin, 2014; Osterwalder, Pigneur, & Tucci, 2005; Schaltegger, Hansen, & Lüdeke-Freund, 2016; Seelos & Mair, 2005; Zott & Amit, 2010, etc.) and it really seems that the business model is emerging as a new unit of analysis (Zott et al., 2011). These authors offer a variety of definitions, but a general consensus on the definition of the business model has not been reached. The term has been frequently confused with other popular terms in the management literature such as strategy, business concept, revenue model, economic model, or even business process modeling (DaSilva & Trkman, 2014; Morris, Schindehutte, & Allen, 2005).

As a generally accepted definition of the business model does not exist, it is not surprising that the constitute elements of the business model are not clearly defined too. Despite many efforts (e.g., Demil & Lecocq, 2010; Mahadevan, 2000; Morris et al., 2005; Onetti, Zucchella, Jones, & McDougall-Covin, 2012; Osterwalder & Pigneur, 2010; Richardson, 2008; Roome & Louche, 2016; Runfola, Rosati, & Guercini, 2013; Shafer, Smith, & Linder, 2005), this issue still allows for different interpretations. For that reason, aiming to make the business model concept more transparent, some authors have extensively explored extant literature and meta-science databases (DaSilva & Trkman, 2014; Ghaziani & Ventresca, 2005; Kujala, Artto, Aaltonen, & Turkulainen, 2010; Mäkinen & Seppänen, 2007; Morris et al., 2005; Onetti et al., 2012; Richardson, 2008; Wirtz, Pistoia, Ullrich, & Göttel, 2016; Zott et al., 2011). Their conclusions are quite similar; the research on business models shows a high degree of complexity and is still an underresearched topic within the management field.

This article builds on these recent works reviewing the state of the art in business model research and has two main objectives. First, it intends to provide a review of the most common themes used in defining business model elements. Second, it discusses the relationship between the concept of a business model, on one hand, and strategy and sustainability, on the other. Providing new insights into the business model notion, the findings not only contribute to the development of management theory but could be also used by the managers and business practitioners of new entrants as well as incumbent firms to design business models capable of addressing direct competitive challenges.

The article proceeds as follows. The “Literature Review” section provides a synthesized overview of the available literature, focusing on the emergence and popularity of the business model concept in academic literature as well as on business model definition. The “Method” section describes the methodology of research. The “Results” section details the results obtained regarding business model elements and two issues usually associated with business models: strategy and sustainability. The article finishes with a discussion and some concluding remarks.

Literature Review

Emergence of the Business Model Concept in Literature

The term business model has been present in academic literature for more than 60 years now. According to Markides (2013), its first use in the literature can be traced to Lang (1947), while Osterwalder et al. (2005) found that it appeared for the first time in an academic paper in 1957 (in the context of business games for training purposes; Bellman, Clark, Malcolm, Craft, & Ricciardi, 1957) and in the title and abstract of a paper in 1960 (how college students from the business field should be trained and how technologies should be introduced to them; Jones, 1960). In the beginning, however, the term was used in a very unspecific manner, reflecting a simplification and simulation of reality aimed at educating future managers on technology (DaSilva & Trkman, 2014). Since the 1970s, the business model has been associated regularly within the context of information technology and mainly used in the sense of business modeling (see Wirtz et al., 2016). This highlighted its operational and functional aspects necessary for system modeling. Still, until the 1990s, the term had been used only sporadically. The advent of the Internet in the business world gave a boost to the usage of the term business model (see Amit & Zott, 2001; Magretta, 2002), with so-called dot-com firms pitching business models to attract funding (Shafer et al., 2005). In parallel, academics searched for more generic approaches in their researches, and the business model has developed into an overall presentation of the company organization contributing to managerial decision-making process (Wirtz et al., 2016).

During the “new economy” era (Morris et al., 2005), that is, the 1990s, we witnessed an explosion of the use of the term in both nonacademic and academic literature. Only in the last decade, at least five special issues were devoted to business models (e.g., the Long Range Planning in 2010, the Journal of Cleaner Production in 2013, the Strategic Entrepreneurship Journal in 2015, and the Sustainability and the Organization & Environment in 2016).

The rise to prominence of the term was also confirmed by many authors who have extensively explored extant literature, by searching the term business model in the title, abstract, or full text of the articles (DaSilva & Trkman, 2014; Ghaziani & Ventresca, 2005; Klang et al., 2014; Kujala et al., 2010; Mäkinen & Seppänen, 2007; Morris et al., 2005; Nenonen & Storbacka, 2010; Onetti et al., 2012; Osterwalder et al., 2005; Richardson, 2008; Shafer et al., 2005; Wirtz et al., 2016; Zott et al., 2011). Their findings suggest that, in peer-reviewed journals, the number of articles has grown from a single-digit number per year to more than several 100 articles per year in the last 50 years. The rapid growth of references to the business model in the literature has certainly contributed to the efforts to theoretically and operationally define this concept. Despite the fact that research in business models has matured over the years, the literature on business models is divergent and heterogeneous.

Business Model Definitions

Analyzing the evolution of the business model concept, Osterwalder et al. (2005) concluded that this evolution has entered its final phase, with the business model concept being applied in management and information systems (IS) applications. This implies that the previous four phases (definition and classification of business models, listing business model components, describing business model components, and modeling business model components) have all been finished. However, just from a short glance at Table 1, which presents a synopsis of available perspectives regarding business model definitions, one can see that it is still quite an interesting topic for academics.

Business Model Definitions.

Also, it seems that the term is not clearly and unambiguously defined. The business model has been referred to as a statement, a description, a representation, an architecture, a conceptual tool or model, a plan, an assumption, a structural template, a method, a framework, a pattern, and a set (see also Morris et al., 2005; Zott et al., 2011).

Morris et al. (2005), Zott et al. (2011), and Wirtz et al. (2016) tried to bring some order to the various perspectives in the gathered definitions. Summarizing their findings, several general approaches, perspectives, and/or categories of definitions could be distinguished: technological, economic, operational, and strategic. The technologically oriented business model articles were very dominant during the earlier stages of business model evolution. It was at the turn of the new millennium that many articles were published in the context of electronic business (Chen, 2003; Dai & Kauffman, 2002; Lam & Harrison-Walker, 2003; Rayman-Bacchus & Molina, 2001; Timmers, 1998, to list only a few). Afterward, the business model concept became more generic, that is, more universally applicable to other types of firm. The economic approach is concerned with the logic of profit generation, that is, how to make money and sustain its profit stream over time (Abdelkafi, Makhotin, & Posselt, 2013; Shafer et al., 2005; Stewart & Zhao, 2000; Teece, 2010). The operational perspective embraces architectural configuration that enables the firm to create value (Morris et al., 2005). This architectural approach further involves firms’ internal processes, resources, and their organization (Amit & Zott, 2001, 2015; Johnson et al., 2008; Osterwalder et al., 2005; Timmers, 1998; Voelpel, Leibold, Tekie, & von Krogh, 2005; Wells, 2016). Finally, definitions also emphasize firms’ strategies, with particular interest on market positioning, organizational boundaries, stakeholder identification and networks, competitive advantage, and sustainability (Baden-Fuller & Haefliger, 2013; Casadesus-Masanell & Ricart, 2010; Casadesus-Masanell & Zhu, 2013; Cavalcante, Kesting, & Ulhøi, 2011; Chesbrough & Rosenbloom, 2002; Shafer et al., 2005; Voelpel et al., 2005). Furthermore, the strengths of the more strategy-oriented articles lie in efforts to understand business by decomposing strategy into a system of interrelated decisions, relationships, and organizational boundaries (Onetti et al., 2012).

The variety of perspectives become more comprehensible as one progressively moves from the technological and economic across the operational to the strategic levels (Morris et al., 2005). However, the boundaries between basic theories become blurred (Wirtz et al., 2016; Zott et al., 2011), and it would be very hard to draw a line between these dimensions as the majority of definitions encompass at least two or three categories. In recent articles, authors mostly refer to the fundamental works and aspects of multiple basic perspectives (e.g., Johnson et al., 2008; Kesting & Günzel-Jensen, 2015; Tikkanen, Lamberg, Parvinen, & Kallunki, 2005; Wirtz, Schilke, & Ullrich, 2010; Zott & Amit, 2010; Wells, 2016).

These broad definitions and approaches are sometimes detailed through the identification of the components of the business model. Indeed, after the definition phase, listing and describing business model elements (or components or unique building blocks or constitute attributes) are the next logical steps in the evolution of the business model concept (Osterwalder et al., 2005). In fact, definitions of a business model quite often focus on structural aspects regarding its contents (e.g., Johnson et al., 2008; Tikkanen et al., 2005; Voelpel et al., 2005).

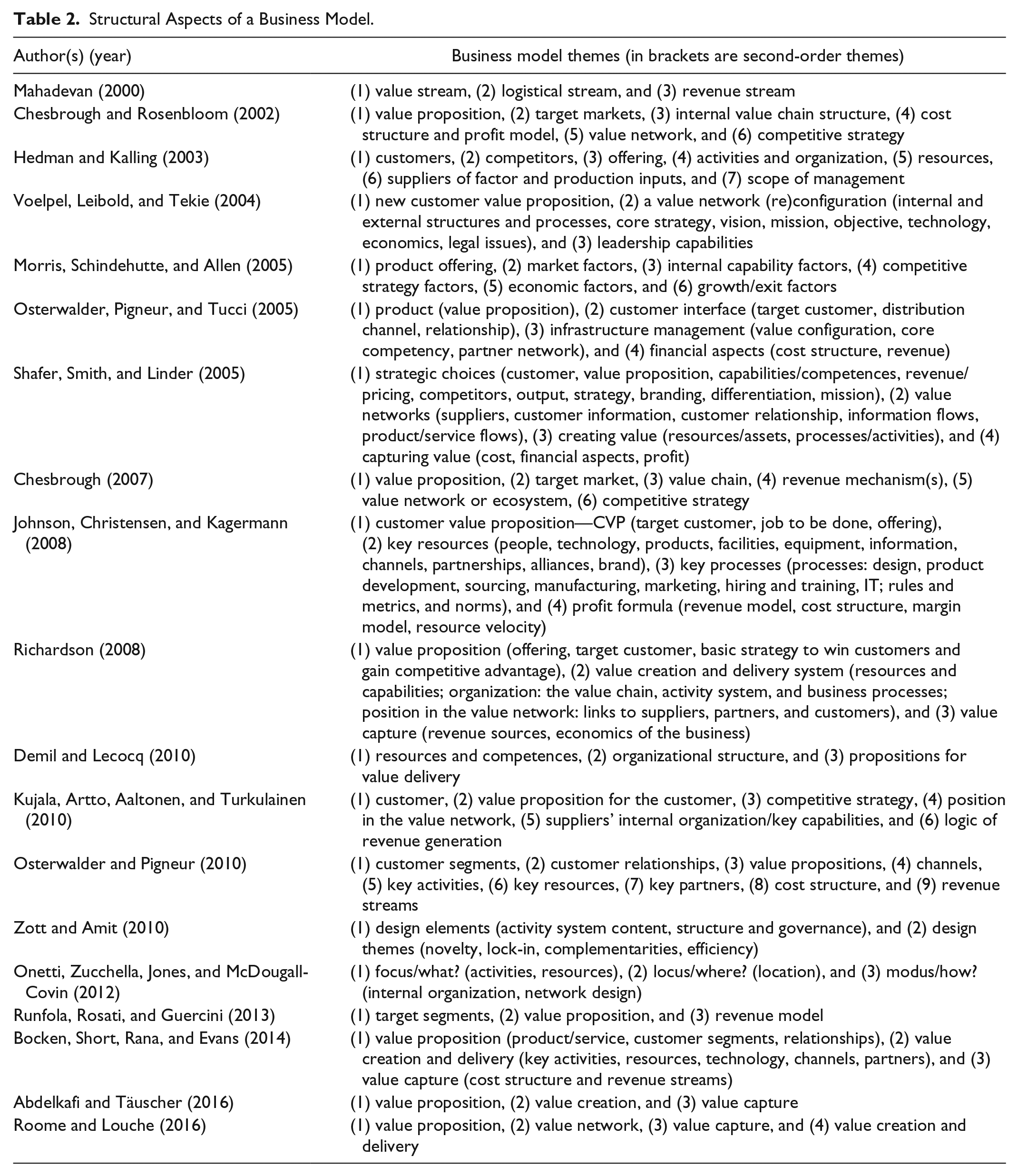

Regarding the content-related structural aspects of a business model, extant literature indicates a separate development and expansion of business model elements within these two distinctive phases of listing and describing. For instance, Morris et al. (2005) analyzed key words in definitions and found 24 different items that are mentioned as possible elements, with 15 receiving multiple mentions. At the same time, Shaffer et al. (2005) and Osterwalder et al. (2005) found more than 40 different items each. Recently, academics have been continually trying to gather and analyze the up-to-date state of the research (Nenonen & Storbacka, 2010; Onetti et al., 2012; Wirtz et al., 2016; Zott et al., 2011, to list only a few) and proposing their own theoretical conceptualizations on what constitutes a business model (see Table 2).

Structural Aspects of a Business Model.

The review in Table 2 indicates that most authors distinguish between first- and second-order themes within the structure of a business model. Many elements overlap and/or have very similar names. Also, they have been alternately classified into both categories. Hence, there are numerous differences in the definitions of elements implying the need for clearer distinction.

Method

In this article, a comprehensive review and critical analysis of previous research on business models and their elements were conducted in February and March 2016 as a part of the research design. In conducting the analysis, a multistep process was used.

For the analysis to be scientifically traceable, this study searched for articles that contain the term business model in the title or keywords published in leading academic and practitioner-oriented management journals (Academy of Management Journal [AMJ], Academy of Management Review [AMR], Academy of Management Perspectives [AMP], Administrative Science Quarterly [ASQ], Journal of Management [JOM], Journal of Management Studies [JMS], Management Science [MS], MIS Quarterly, Organization Science [OS], Strategic Management Journal [SMJ], California Management Review [CMR], Harvard Business Review [HBR], and MIT Sloan Management Review [MSM]). This search revealed 277 articles on business models from the early publishing dates to December 2015, of which only 21 had been published in academic journals, while 256 had appeared in practitioner-oriented journals (i.e., CMR, HBR, and MSM).

The research was further extended to the ABI/INFORM database. Examining databases was confirmed as an appropriate method for exploring extant literature on business models (DaSilva & Trkman, 2014; Ghaziani & Ventresca, 2005; Mäkinen & Seppänen, 2007; Wirtz et al., 2016; Zott et al., 2011, etc.) while international coverage makes the ABI/INFORM database one of the most complete sources on business studies. The search was focused on academic articles containing the term business model in the title or abstract, published in peer-reviewed scholarly journals in the English language from January 1960 to December 2015. In total, 4,028 articles were obtained. As 16 of the newly found articles were already present in the initial sample of 277 articles, our overall sample contained 4,289 articles.

As an initial cursory analysis of these 4,289 publications revealed that many of the selected publications would not be useful for further analysis, three additional criteria were introduced to identify articles relevant for this study: (a) an article must deal with the business model concept in a nontrivial and nonmarginal way, (b) an article also must refer to the business model as a concept related to business firms (as opposed to economic cycles or models, for example), and (c) an article must directly refer to the constitute elements or components of a business model. As a result, 102 articles fit the suggested criteria. Through careful reading of these publications, a few additional publications on business models were found that appeared relevant for this review, primarily books and working papers. The final sample, therefore, contained 108 publications.

Frequency of appearance of business model elements was searched within the selected publications. Special attention was devoted to searching for business model elements that are related to strategy and sustainability to analyze the relationship between business models, on one hand, and strategy and sustainability, on the other.

Results

Domains Addressed in a Business Model

Across these 108 publications, 387 different business model elements or unique building blocks are found. A brief review of these adjacent literatures is presented in Table 3. It seems that some of the elements are seen time and time again in the definitions. For instance, four elements (value proposition, customer, product, and resources) are mentioned in more than 20 publications, and another 56 out of 387 elements are mentioned at least 4 times. In addition, 16 elements are mentioned 3 times, 49 elements 2 times, and 262 elements are mentioned only once.

Frequency of Appearance of Business Model Elements.

Elements related to sustainability.

Elements related to strategy.

Regardless of the large number of perspectives provided when business model elements are concerned, something consistently recognized was that definitions often included those elements that comprise the concept of value. More precisely, value proposition is convincingly the most often mentioned element of a business model (in one third of analyzed publications). However, many other elements also overlap each other while referring to value proposition. For instance, value, value offering, (customer) value proposition, or even product or service all refer to value that is first proposed and then delivered to a customer. In other words, value proposition is typically concerned with the product and service offering, that is, the value embedded in the offerings of the firm (see also Afuah & Tucci, 2003; Osterwalder et al., 2005; Voelpel, Leibold, & Tekie, 2004).

Resource-based view (RBV) of the firm (e.g., see Amit & Zott, 2001; Seppänen & Mäkinen, 2007; Morris et al., 2005; Seppänen, 2009) also proved to be relevant for the business model concept. Besides the term resources (found in one fifth of publications), elements such as key resources, strategic resources, assets, competencies, information, or even technology or brand all indicate the tangible or intangible substance of a firm and its business model. On the contrary, Morris et al. (2005) argued that activity sets support each element of a business model. Furthermore, Zott et al. (2011) found that the received literature on business models mostly supports an activity system perspective, that is, a set of interdependent organizational activities centered on a focal firm. Indeed, this research found that managerial, organizational, manufacturing, marketing, and especially networking processes are frequently mentioned within the business model framework. As a link connecting a firm’s infrastructure and customers, these activities are required to create and deliver the value proposition to the targeted customer.

The last domain addressed is about considering how the company creates value for itself. Elements such as revenue model or revenue stream, value capture, cost, price, and profit formula (all these elements are mentioned at least 5 times in publications) reveal the financial aspect of a business model. When considered in relation to other domains and elements, a business model is a specific combination of resources and transactions which generate value for both customers and the organization.

Business Model Versus Strategy

Transformation of resources into valuable products and services, and delivery of those to customers, occurs in a specific strategic context. The previous review indicated that the strategy literature stream has an essential influence on business model development and that strategic elements are mentioned very often in the context of business models. Strategy or some other elements related to strategy like mission, competitors, organization, or structure have often been incorporated in definitions (see again Casadesus-Masanell & Ricart, 2010; Chesbrough & Rosenbloom, 2002; Shafer et al., 2005; Smith, Binns, & Tushman, 2010; Voelpel et al., 2005). This is also reflected in the various approaches used when defining the main elements of a business model (see Tables 2 and 3).

Many authors argue that strategy is essential when considering elements of a business model. For instance, Hamel (2000) considered the core strategy as a central (first-order) element of a business model. Also, a group of authors refer to competitive strategy (Chesbrough, 2007; Chesbrough & Rosenbloom, 2002; Kujala et al., 2010; Morris et al., 2005). They all agree it must delineate how the firm will gain and hold advantage over rivals. Richardson (2008) mostly agreed but, from his point of view, basic strategy to win customers and gain competitive advantage is a second-order theme and belongs to value proposition. Shafer et al. (2005) argued that strategy is all about making choices (regarding customers, value proposition, pricing, competitors, branding, etc.), and strategic choices are therefore considered as a separate element of a business model. Voelpel et al. (2004) and Tikkanen et al. (2005) see strategy as a second-order theme. According to Voelpel et al. (2004), strategy, vision, mission, and objectives are a part of a value network (re)configuration which has to provide value for customers. Tikkanen et al. (2005) explained that the business model of the firm is based on how the material aspects of the business model interact with managerial belief systems. Within material aspects, they find strategic intent (long-term organizational commitment), the strategy process managed by a firm’s managers, and the content of strategy as part of the material aspects of a business model.

On the contrary, there are authors who do not explicitly embed the term strategy within the business model framework. For some of them, Onetti et al. (2012) for instance, the terms are more clearly explained when strategy is excluded from the defining elements of the business model. Therefore, Onetti et al. (2012) deliberately excluded concepts such as mission and strategy (together with the components of value proposition, competition, differentiation, customer target market, and pricing) from the defining elements of the business model.

According to Wirtz et al. (2016), such a lack of consensus with regard to the area of strategy as a building block of business model could be explained by the fact that some authors usually integrate the implications of corporate strategy through a strategy model within the business model. Indeed, the literature points to the importance of business models for a firm’s strategy and definitions of a business model at a strategic level. However, a business model and a strategy are not the same thing, and the two should not be confused. In fact, literature tries to portray the business model as an independent concept but related to a number of other established managerial concepts such as strategy, organizational structure, or business planning (e.g., Casadesus-Masanell & Ricart, 2010; DaSilva & Trkman, 2014).

In this respect, much has been discussed about differentiating between business models and strategy (Casadesus-Masanell & Ricart, 2010; Chesbrough & Rosenbloom, 2002; DaSilva & Trkman, 2014; Klang et al., 2014; Magretta, 2002; Morris et al., 2005; Osterwalder et al., 2005; Richardson, 2008; Teece, 2010; Tikkanen et al., 2005; Wikström et al., 2010; Zott et al., 2011). For Chesbrough and Rosenbloom (2002), the business model is “more of a proto-strategy, an initial hypothesis for how to deliver value to the customer . . .” (p. 550). It describes the organization’s activities and how to create and deliver value to the customer but does not consider competition as a critical dimension of performance (Magretta, 2002). Hence, the business model is focused on value proposition and emphasizes the role of the customer (Zott et al., 2011). On the contrary, the strategy is concerned more with value capturing and its sustainability than with value creation (Chesbrough & Rosenbloom, 2002; Mäkinen & Seppänen, 2007). This means strategy gives meaning and direction on how the business model is utilized depending on contingencies that might occur in a competitive environment (Casadesus-Masanell & Ricart, 2010; Tikkanen et al., 2005), and in such a way, strategy stresses the need for positioning (Magretta, 2002). Hence, strategy is all about making choices while a business model reflects the strategic choices that have been made and their operating implications (Shafer et al., 2005). However, Casadesus-Masanell and Ricart (2010) argued that strategy is not just the mere selection of a business model (making some choices and suffering the consequences of these choices) because every organization has some business model, but not every organization has a strategy. Some academics have even questioned whether it would be possible to have more than one business model at the same time (Arend, 2013; Casadesus-Masanell & Ricart, 2010; Hedman & Kalling, 2003; Kim & Min, 2015; Malone et al., 2006; Markides & Charitou, 2004) or to alter business models within one strategy (DaSilva & Trkman, 2014).

Business Models and Sustainability

Another theme that is becoming more and more present within the context of business models is sustainability. Although sustainability is almost always seen in terms of three dimensions that must be in harmony, namely, social, economic, and environmental (Kates, Parris, & Leiserowitz, 2005; Strange & Bayley, 2008), when it comes to business models, the harmony of these dimensions was not always the case. At first, sustainability was mentioned only from an economic perspective. Besides creating and delivering value, the core of a business model was to create a sustainable competitive advantage in defined markets (Morris et al., 2005) and to generate profitable and sustainable revenue streams that ensure the satisfaction of relevant stakeholders within a firm (Brousseau & Penard, 2007; Osterwalder et al., 2005; Voelpel et al., 2005). The focus was on how a firm can sustain itself, that is, how to be self-sustainable on the basis of the income it generates (DaSilva & Trkman, 2014; Shafer et al., 2005; Teece, 2010). As previously mentioned, many elements of a business model (e.g., revenue model, revenue stream, value capture, profit formula) reflect this approach. Objectives and interests of the environment and community, as external stakeholders, were less relevant. For instance, environment is considered as an element of business model only twice (see Hoque, 2002; Nair, Paulose, Palacios, & Tafur, 2013) and has the meaning of a turbulent and competitive business setting that impacts firms’ survival.

Meanwhile, the overall competitive landscape has changed in favor of the environment and wider community. In 2008, Stubbs and Cocklin (2008) discussed how sustainability concepts (all three dimensions) should shape the driving force of the firm and its decision making. They coined the term sustainability business model (SBM)—a model where a firm treats sustainability as a business strategy in itself, rather than as an add-on. For firms, sustainability is not only the right thing to do but also the smart thing to do (Stubbs & Cocklin, 2008) because becoming environment-friendly lowers costs, creates new businesses, and generates additional revenues from better products (Nidumolu, Prahalad, & Rangaswami, 2009). In this way, sustainable organizations need profits to exist (i.e., survive) and to achieve sustainable outcomes but they do not just exist to make a profit (Stubbs & Cocklin, 2008).

The concept of a SBM was well accepted by other academics and practitioners under slightly changed names—sustainable business model or business model for sustainability (BMfS; Abdelkafi & Täuscher, 2016; Bocken, Rana, & Short, 2015; Bocken, Short, Rana, & Evans, 2013, 2014; Boons & Lüdeke-Freund, 2013; Boons, Montalvo, Quist, & Wagner, 2013; Jabłoński, 2016; Roome & Louche, 2016; Schaltegger et al., 2016; Schaltegger, Lüdeke-Freund, & Hansen, 2012; Wells, 2016). However, all SBM or BMfS understandings agree on the integration of a triple bottom line approach and consider a wide range of stakeholder interests. SBM is based on the principles of balancing the business from a number of perspectives, and it is a kind of holistic and hybrid model (Jabłoński, 2016). It generates therefore shared value creation for all stakeholders—it captures economic value for itself, while distributing value beyond its organizational boundaries by maintaining or regenerating natural, social, and economic capital (Bocken et al., 2015; Bocken et al., 2014; Boons et al., 2013; Schaltegger et al., 2016; Schaltegger et al., 2012).

Accordingly, designing sustainability-oriented business models requires a long-term focus at both the organizational and socioeconomic levels (Stubbs & Cocklin, 2008) and the adoption of a systemic approach that seeks to integrate considerations of the three dimensions of sustainability (Bocken et al., 2015). Indeed, environment and community are acknowledged as true stakeholders. When it comes to attributing to natural or ecological capital, Abdelkafi and Täuscher (2016) discussed environmental value proposition, which represents not the actual impact but the intended impact of a business model on the environment, and how to integrate it into a BMfS. When it comes to the community perspective, Stubbs and Cocklin (2008) even mentioned community as a subelement of a business model (together with customers, employees, suppliers, and management). In addition, some authors used the business model framework to explain how to create social businesses able to enhance social welfare (e.g., Seelos & Mair, 2005; Yunus, Moingeon, & Lehmann-Ortega, 2010). According to Yunus et al. (2010), a social business model defines the desired social profits through a comprehensive ecosystem view. This will result in a social profit equation (one constitute element of a social business model) while an economic profit equation (another element) targets only full recovery of cost and of capital, and not financial profit maximization. Despite the growing importance of these issues (i.e., environment, environmental value proposition, community, and social profit equation) in contemporary business, this research showed that they are rarely mentioned as elements of a business model. An explanation for this can be found in the core definition of the SBM—sustainability (involving also environment and society) is treated as a business strategy in itself and there is no need for it to be asserted as separate elements.

Hence, the quest for sustainability forces companies to change the way they think about products, technologies, processes, and business models. Smart organizations now treat sustainability as innovation’s new frontier (Nidumolu et al., 2009). Designing SBMs explicitly depicts how value is created and appropriated by all involved. Thus, the creation and further development of businesses toward sustainability is challenged by the cocreation of societal and economic profits (Boons & Lüdeke-Freund, 2013), leaving plenty of space for further research.

Discussion and Conclusion

This overview has revealed that many practitioners and scholars treat the business model as a promising concept. On the contrary, the validity of the business model concept and its long-term implications has been questioned over time. This apparently popular concept receives intense criticism, which is quite paradoxical (Klang et al., 2014). It was argued that the business model is defined vaguely, that there is confusion in terminology, and that the business model, as an approach to management, becomes an invitation for faulty thinking and self-delusion (Morris et al., 2005; Porter, 2001; Zott et al., 2011). Several conclusions, which are to a large extent coherent with these inferences, can be drawn from this overview.

First, although more than half a century has passed since the first appearance of the term business model in the literature, this overview shows that its popularity is a relatively young phenomenon (see also Wirtz et al., 2016; Zott et al., 2011). The business model concept began to be increasingly used only during the 1990s, in parallel with the development and intensive evolution of e-commerce. Since then, research in business models has matured over the years, and numerous definitions of business model and elements have appeared. The e-business and technology stream dominated the early stage of business model evolution, after which time a more generic approach emerged, focused on the strategic and operational dimensions of a firm and seeking to define the concept as a more generalized representation of a firm. The economic stream, emphasizing the logic of profit generation, is a constant throughout the whole period. This, therefore, is in line with some of the previous arguments (George & Bock, 2011; Morris et al., 2005; Onetti et al., 2012; Wirtz et al., 2016; Zott et al., 2011) that the literature on business models is fragmented and dispersed in several streams with very loose boundaries between each other.

The heterogeneous nature of the extant literature gives support to other two conclusions—there are no generally accepted definitions for either the business model or its building blocks. According to Shafer et al. (2005), the lacking consensus on business model definition may be in part attributed to interdisciplinary scholarly perspectives (e.g., technology, IS, strategy, organizational theory, etc.). Despite the broadness and differences in definitions over the last two or three decades, one thing the academics and practitioners agree upon is that, when business models are concerned, it is all about value (Abdelkafi et al., 2013; Amit & Zott, 2001; Chesbrough & Rosenbloom, 2002; Osterwalder et al., 2005; Santos, Spector, & Van der Heyden, 2009; Shafer et al., 2005; Smith, Binns, & Tushman, 2010; Teece, 2010; Voelpel et al., 2005; Wirtz et al., 2010). What can be read out as a common theme in the authors’ views is that a business model is a conceptual tool and an abstract representation of a company’s core logic that describes how it creates, delivers, and captures value. To make this abstraction simpler, a business model is often expounded through the identification of its elements. The most frequently cited are a firm’s value proposition, customers, products (and services), resources, value creation, value capture, revenues, technology, processes, and partners. Still, there is no congruency—different items are used for similar concepts and their meanings sometimes overlap. What product or service is to one author, value proposition is to another. Within a number of elements, it looks like these elements are crucial when business models are concerned, and that value (i.e., a firm’s value proposition, value creation, and value capture), as claimed by Johnson et al. (2008) and Nenonen and Storbacka (2010), makes the core of a business model.

Although consensus among the authors regarding the dimensions of value as components of a business model exists to some extent, there is little or no agreement with regard to the area of strategy. This review implies that there is both a relationship and distinction between business models and strategy. A strong relationship between business models and strategy is manifested in two ways: Business models are often defined from a strategic point of view while strategic issues are pointed out as important business model elements. Although there is a strong relationship between the two, the next conclusion is that a business model and a strategy are not the same thing. The majority of the extant literature portrays the business model as an independent concept (Casadesus-Masanell & Ricart, 2010; DaSilva & Trkman, 2014; Magretta, 2002; Shafer et al., 2005), and a clear distinction should be made between strategy and business model. When a business venture is concerned, strategy can be understood more as a kind of guide (Wirtz et al., 2016). On the contrary, business models include a number of strategy elements but build more on the creation of value for customers, and from a strategic view, the business model can be a source of competitive advantage (Teece, 2010; Zott et al., 2011). This implies that a business model is typically developed from a more narrow perspective than a strategy (see Wikström et al., 2010). It seeks to integrate sustainable value creation with capturing and appropriation while emphasizing the role of the customer which appears to be less pronounced elsewhere in the strategy literature. In Addition, an organization’s business model framework is usually approached from a short-term perspective as the reflection of its realized strategy (see also Casadesus-Masanell & Ricart, 2010; Dahan, Doh, Oetzel, & Yaziji, 2010), providing a link between strategy and operations and between strategy formulation and implementation. From this point of view, this conclusion is in line with previous findings (e.g., Mäkinen & Seppänen, 2007; Richardson, 2008) that found that business models facilitate operations, that is, the implementation of selected strategy. Consequently, strategy reflects the long-term perspective, that is, what a company aims to become, while a business model is a description of a state, that is, what a company really is at a given time (Dahan et al., 2010; DaSilva & Trkman, 2014). For sure, business model and strategy are more complements than substitutes.

Moreover, sustainability is found to be a hot topic for business models. Besides economic sustainability (DaSilva & Trkman, 2014; Shafer et al., 2005; Teece, 2010, etc.), increased interest in research is devoted to the social and environmental dimensions of sustainability. As a result, a new stream of literature on sustainable business models has emerged (Abdelkafi & Täuscher, 2016; Bocken et al., 2015; Bocken et al., 2014; Boons et al., 2013; Roome & Louche, 2016; Schalteggeret al., 2012; Stubbs & Cocklin, 2008). According to this approach, value is distributed to all stakeholders, including those within a firm as well as those beyond the firm’s organizational boundaries.

To summarize, this article reviewed the relevant literature on business models to try gain a better understanding of the business model concept and its content-related structural aspects. It looks like 20 years of intensive development were not enough for academics to agree on what a business model is and what its constitute elements are. Still, progress is evident in other fields. Particular attention was therefore dedicated to the structural aspects of a business model and interrelationship of business models, on one hand, and strategy and sustainability, on the other. This article stipulates that the business model has an important role in the implementation of a firm’s strategy. Although its elements are focused on value proposed to customers, the business model has increasingly been used in symbiosis with the sustainability concept.

The contribution of this article is twofold. From a conceptual viewpoint, more clarity is given to the definition of a business model as an independent concept which has general validity. This overview would therefore facilitate research into the theoretical foundations of the business model. From a practical viewpoint, this overview may be particularly helpful to practitioners whose firms are seeking how to deal with complex market challenges and gain competitive advantage. Without a doubt, the design and management of business models, especially within the sustainability context, leaves gaps for further research. Cocreation of environmental, societal, and economic profits within and beyond the boundaries of a business model is surely a challenge for both practitioners and academics. In this regard, more work regarding business model terminology may certainly provide insights into making business models more efficient.

Despite the attempts to rigorously and objectively analyze the selected literature on business models, this article comes with several limitations. Besides strategy and sustainability, business models have other, emerging common themes that should be looked into. For instance, future overviews on business models should seek to overcome this limitation by focusing on business model types (see Kujala et al., 2010; McGrath, 2010; Wirtz et al., 2010), business model innovation (Cavalcante et al., 2011; Mitchell & Coles, 2004; Zott et al., 2011), and the impact of adopted business models on firm performance (Cucculelli & Bettinelli, 2015; Markides & Sosa, 2013; Zott et al., 2011). The research scope of future studies should also focus on particular industries to build the theory and compare the overall conclusions. More empirical findings (i.e., case studies) will help both practitioners and academics to put all the pieces together and design competitive business models.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Croatian Science Foundation [grant number UIP-2014-09-1214].