Abstract

The resource-based view (RBV) posits that the sustainability of a firm’s success depends upon the creation, development, and implementation of a given organization’s unique resources and capabilities. Based on this theoretical framework, this article analyzes the relationship between organizational capabilities, business strategy, and profitability in the Portuguese textile industry. The strong relationship between these variables suggests that the organizational capabilities and the choice of business strategy may be the key to increase the profitability in this study context. So, the ability of the Portuguese textile organizations to change their business strategy based on their organizational capabilities affects profitability in a number of ways. Concretely, the results of this study highlight the importance of the choice of the business strategy as a partial mediator between the organizational capabilities and the profitability, a point that is crucial to understanding the success of a given organization and how resources and capabilities contribute to the process. The article concludes with a number of managerial implications and directions for future research.

Introduction

Business strategy is one of top management’s primary concerns as it is crucial for a given firm’s survival and for creating wealth in today’s highly competitive global market. Considered one of the most important aspects of management, business strategy has been the focus of considerable research. The theoretical underpinnings of business strategy are based on knowledge from several other disciplines, including classical economics, game theory, finance, psychology, and leadership or organizational culture (Leite-Teixeira, 2001). In contrast to general management, business strategy is currently in a pre-paradigmatic stage characterized by a diversity of opinions and tendencies regarding principal concepts and dimensions (Rosa & Teixeira, 2002). Nowadays, organizations are in constant competition for production factors, resources, customers, and the revenue necessary to guarantee their continued functioning. As they navigate this uncertainty, managers must make choices. Some choices are strategic, such as the selection of resources and products, the firm’s position in the market, the level of diversification, the organizational layout, and the leadership profile. These choices contribute to the success or failure of the organization (Rumelt, Schendel, & Teece, 1994). This study focuses on business strategy; specifically, the view that a given firm’s resources and capabilities are of utmost importance. Organizations differ because they possess a distinct set of tangible and intangible resources that contribute decisively to strategic advantages. However, resources alone are not sufficient to secure sustainable competitive advantages and ensure consistently superior performance. Generally, these advantages only emerge and endure if several activities and resources are complementary and the organization is able to create the type of sustainable competitive advantages that have a significant impact on profitability.

The study population is comprised of medium to large companies from northern Portugal’s industrial textile sector. This geographic region was selected because it has exhibited considerable sensitivity to the effects of the current global economic crisis and because of the growing interest in the ability of this important economic region to recover from what has been termed a setback in terms of Portugal’s economic and business weight (Associação Têxtil e Vestuário de Portugal, 2009). Recent years have seen the textile industry struggle to integrate itself into the sector’s new global context. This difficulty is particularly apparent considering that during the 2-year study period (2007-2009), the sector’s total business volume fell by 19%, whereas job creation plummeted by 10% (Associação Têxtil e Vestuário de Portugal, 2009). In the current context, textile firms play a vital role in creating jobs in northern Portugal; however, they find themselves at a precarious crossroads as they must reposition themselves and find new competitive advantages to continue in their traditional role as major contributors to national production and job creation. In addition, the paucity of studies focusing specifically on the Portuguese textile industry and the influence of firm capabilities and business strategy on profitability further justify the present study and the hypothesized model. In this vein, the purpose of this article was to investigate the relationship between firm capabilities and profitability, paying particular attention to the mediating role of business strategy.

Literature Review

The resource-based view (RBV)

The strategy concept is not new. In the 1960s appeared the first specific and structured texts analyzing the theme in an independent way and focused on business and economic issues. In this first moment, the strategy was fundamentally based on the determination of long-term goals and the ways to reach them (Drucker, 1946, 1954). The contributions of this period correspond also to what Chaffee (1985) defined as linear model of strategy. Later, strategy appears as an effort of adjusting the organizations to the external environment, which it became increasingly complex. It refers to the period from the end of seventies to the end of eighties, when new elements were added to the strategic planning process, as growth/market share matrixes or attractive market indices. It became fundamental to pay attention to the nearest environment of the organizations, namely, the bargaining power of suppliers and customers. In this context, it is important to mention Porter (1976, 1979, 1980) studies developed around the concepts of strategic positioning of the organizations and the creation of strategic groups (McGahan & Porter, 1997; McGee & Thomas, 1986). Finally, in the recent years the complexity of the environment has forced the companies to include in their strategic plans other dimensions beyond technological, financial, and market considerations (Hamel & Prahalad, 1990), with many of the studies focused on the resources and capabilities theory. This approach defends the importance of analyzing the resources and capabilities belonging to the company, how it uses them, the characteristics they have, or the new capabilities generated in the organization from the existing interactions and complementarities (Barney, 2002; Grant, 1996; Penrose, 1959; Wernerfelt, 1984). Therefore, nowadays the efforts are focused on the conjugation between external and internal aspects, trying to optimize the organizational innovation and creativity (Klein, Mahoney, McGahan, & Pitelis, 2010). Other new approaches consider the dynamic sources of the competitive advantages. Thus, they are based on the constant orientation of the company to integrate, create, and reconfigure its resources and capabilities; and, what is more important, to actualize and change its core capabilities in response to the changing environment to obtain competitive advantages (Teece, Pisano, & Shuen, 1997; Wang & Ahmed, 2007).

The theoretical framework for this study focuses on the importance of a given organization’s resources and capabilities. One of the premises of this perspective is that firms differ in multiple ways as each firm possesses a unique set of tangible and intangible resources (Collis & Montgomery, 1998). It is precisely this heterogeneity that permits the development of competitive advantages (Barney, 1991, 2001a). As Barney (1991) noted, several empirical studies have been based on Porter’s framework, focusing on the relationship between environment and performance, but giving little importance to the impact of a given firm’s idiosyncratic attributes. In contrast to the preceding structure–conduct–performance paradigm from which the market-based view emerged, this new format posits a logic based on resources–conduct–performance, wherein the success of a firm depends on the resources it possesses (Kühn & Grünig, 2000). In recent years, several authors have further developed these concepts, creating what is today known as the RBV (Barney, 2001a, 2001b, 2002; Collis & Montgomery, 1998; Grant, 1991, 1996; Peteraf, 1993; Peteraf & Barney, 2003; Rumelt, 1991; Wernerfelt, 1984). While the importance of the RBV continues to be discussed at the theoretical level (Barney, 2001a; Hoopes, Madsen, & Walker, 2003; Priem & Butler, 2001) and the perspective continues to evolve (Barney & Mackey, 2005), many empirical RBV studies can be found in the business strategy literature (Byrd, Pitts, Adrian, & Davidson, 2008; Newbert, 2008; Tanriverdi, 2005; Zhu & Kraemer, 2002). Some authors have pointed out several limitations in the application of RBV, for example, the difficulty to measure in case of intangibility (Godfrey & Hill, 1995; Priem & Butler, 2001) or the static perspective of this approach (Priem & Butler, 2001). According to Armstrong and Shimizu (2007), the variety of empirical methodologies used and the multiple forms to study the RBV have not facilitated the integration of the results and the conclusions of the previous studies. Based on these facts, the authors identify the most important aspects that the researchers must attend, as the proper identification and operationalization of the resources, the sustainability concern, and the control of the cofounder factors. However, these limitations have been overcome and diminished, with this perspective in the last years being a dynamic source of important studies. Thus, the RBV has been the base of important empiric studies considering the intangibility of the resources (Newbert, 2008); the technological, marketing, or regulation capabilities and their influence on performance measures (De Carolis, 2003); the interaction between quality, innovation, or cost-leadership capabilities and the organizational context (Wang & Ang, 2004); or the importance of the resources and capabilities to obtain competitive advantages in public organizations (Symaniec-Micka, 2014).

So, numerous authors have directly or indirectly invoked principles derived from RBV perspective. In this sense, several authors have presented extensive listings of resources and capabilities that are likely to lead to the creation of competitive advantages for organizations (Amit & Schoemaker, 1993; Grant, 1991). Building on contributions by Penrose (1959) and Rubin (1973), Wernerfelt (1984) developed a perspective from the business strategy point of view (Porter, 1996). In his 1984 article, Wernerfelt set out to develop some simple economic tools to analyze organizations at the resource level and verify the strategic alternatives that emerged from the study. The results show the relationship between profitability, performance, and resources, and the impact on long-term resource management. Barney (1991) considered as resources all assets, capabilities, organizational processes, attributes, information, and knowledge controlled by the organization that allow it to implement more effective and efficient business strategies. The author posits that a firm has a competitive advantage when it executes a value creator business strategy that is not simultaneously implemented by an actual or potential competitor. The resulting advantage will be sustainable when other firms cannot duplicate the strategy’s benefits. Grant (1991) also stresses the importance of resources, noting that they guarantee a direction and form the basis of a given firm’s profitability.

The relationship between firm capabilities and business strategy

One of the main premises of RBV is that firms must base their strategic decisions on a strong set of resources that can generate complex capabilities and lead to superior performance (Amit & Schoemaker, 1993; Peteraf, 1993). Therefore, a given firm’s strategy is developed and advanced based on the resources that organization possesses, how it applies them, their characteristics, and the capabilities generated (Ray, Barney, & Muhanna, 2004; Smith, 2008). The impact of capabilities on competitive advantage corresponds to a given firm’s ability to develop its capabilities while implementing a better and more complex strategy (Amit & Schoemaker, 1993; Liu, Baskaran, & Li, 2009). Although there is some theoretical consensus regarding the notion that both tangible and intangible resources are necessary for a firm to gain a competitive advantage (Arenas & Lavanderos, 2008; Barney, 1991; Morgan, Kaleka, & Katsikeas, 2004; Piercy, Kaleka, & Katsikeas, 1998), to date only a few empirical studies have explored this relationship. This presumed effect is supported by some studies that have examined the vital role of firm capabilities in securing competitive advantages (Cater & Cater, 2009; Hitt, Bierman, Shimizu, & Kochhar, 2001; Lages, Silva, & Styles, 2009; Spanos & Lioukas, 2001). Therefore, the following hypothesis is proposed:

The relationship between business strategy and profitability

The direct effect of a firm’s business strategy on its performance has been the topic of several studies (Deitz, Tokman, Richey, & Morgan, 2010; Kotha & Nair, 1995; S. Lee & Lee, 2008). Research in this domain has generally confirmed a positive relationship between competitive advantage and performance (Kotha & Nair, 1995; Kroll, Wright, & Heiens, 1999; Morgan et al., 2004; Pertusa-Ortega, Molina-Azorín, & Claver-Cortés, 2009; Piercy et al., 1998; Rivard, Raymond, & Verreault, 2005). However, some researchers have found that competitive advantage does not always affect performance as at least some of the benefits are appropriated by stakeholders (Coff, 1999; Coyne, 1986). Although several researchers have examined the marketing dimension of performance by assessing parameters such as market share (Baker & Sinkula, 1999; Dussauge, Garrette, & Mitchell, 2000), in the present study performance was assessed in terms of profitability, a more clearly defined and objective measure. In this sense, other authors have also measured performance in terms of firm profitability (Dess & Robinson, 1984; Powell & Dent-Micallef, 1997). Therefore, the following hypothesis is proposed:

The relationship between firm capabilities and profitability

A sustainable competitive advantage depends on the firm’s ability to obtain, integrate, and reconfigure its resources to respond to the growing demands of its customers and the market. Therefore, differences in performance are derived from the heterogeneity of the resources and capabilities possessed by different firms (Teece et al., 1997), wherein possessing a superior set of capabilities has a positive impact on a given organization’s performance. It is well established that the more an organization accumulates capabilities to the exclusion of its competitors, the more its performance improves relative to those competitors (Gong, Law, Chang, & Xin, 2009; Urbano & Yordanova, 2008). Capabilities have been considered antecedents to performance since the theoretical and empirical development of RBV (Penrose, 1959; Wernerfelt, 1984). The relationship has been studied extensively, with results consistently indicating the positive influence of resources and capabilities on performance (Fandel, Backes-Gellner, Schlüter, & Staufenbiel, 2004; Levinthal & Wu, 2010; Richey, Tokman, & Dalela, 2010; Tayles, Pike, & Sofian, 2007). Piercy et al. (1998) analyzed the importance of the competitive resources that magnify export capabilities, highlighting their effect on performance. Other authors have examined profitability as a dependent variable, making the important contribution of identifying information and communication technologies as capabilities (Bharadwaj, 2000; Makadok, 1999). Richey and his colleagues (2010) explored the collaborative and technological resources used in supply chain management at several organizations in the food retailing sector, verifying that profitability is linked to a given firm’s ability to develop and implement collaborative technologies between different partners. Based on the existing literature, the following hypothesis is proposed:

Business strategy as mediator between capabilities and profitability

An organization’s success depends not only on its strategic position in the market but also on the sustainability of that success in terms of being able to continually create and develop unique capabilities (Peteraf & Barney, 2003; Winter, 2003; Zollo & Winter, 2002). The question that remains is whether a firm’s capabilities alone are enough to enhance performance or if the effect is only fully realized after implementing a particular business strategy. That is, what is the effect of a firm’s capabilities on its performance through the mediation effect of the competitive advantage? This relationship represents the confluence of the different effects on performance that derive from the firm’s ability to alter its business strategy based on its capabilities (Edelman, Brush, & Manolova, 2005; Lages et al., 2009; López-Cabrales, Pérez-Luño, & Valle-Cabrera, 2009). Based on their analysis of several small firms, Edelman and colleagues (2005) examined how business strategy mediates the alignment of resources and performance. Their results indicate that organizational and human resources, in combination with quality and customer-oriented business strategies, can enhance a given firm’s performance. Similarly, Chrisman (1999) explored the success associated with creating new firms, underscoring the fact that the mediating effect of business strategy is crucial to understanding an organization’s success and the role of resources and capabilities in the process. Considering the importance and implications of these variables to the textile industry, the following hypothesis is proposed:

Method

Participants

The sample comprised of medium and large organizations from northern Portugal’s industrial textile sector. The population of this study included 521 industrial textile organizations with more than 50 employees; data were obtained from the National Institute of Statistics (Instituto Nacional de Estatística, 2008). At the end of the data collection process, responses had been obtained from 153 organizations, or 29% of the study universe, which is in line with similar research in the field (Cater & Cater, 2009; Rivard et al., 2005).

The sample characteristics reflect those of the population. Private limited companies were the most common legal form (64.5%), followed by public limited companies (33.6%). Regarding size, 57% of the firms had fewer than 100 employees, while 39% had between 100 and 249 employees; only 4% of the firms in this study had 250 or more employees. Firm age ranged from 1 to 84 years, with a median of approximately 20 years (Standard deviation (SD) = 13.74).

Procedure

Data were collected between February and September 2009. The methodology involved sending a questionnaire to the managers of all organizations included in the study. Questionnaires were accompanied by a small set of instructions, a cover letter that summarized the reasons for the study, a request that the managers complete and return the questionnaire, a formal declaration of confidentiality in data processing, and a brief explanation of the importance of participating in the study. The data and hypothesized relationships were analyzed using the structural equation modeling (SEM) technique with SPSS 17.0 package. This is a statistical methodology that represents causal processes that generate observations on multiple variables (Bentler, 1988). The hypothesized model created with SEM could then be tested statistically using a simultaneous analysis of the entire system of variables to determine the extent to which it was consistent with the data. By using SEM procedures, it was possible to incorporate unobserved and observed variables, and there were no widely and easily applied alternative methods for modeling multivariate relations (Byrne, 2009).

Instruments

This section provides a description of the instruments utilized in this study. For the Firm Capabilities scale, we have followed Spanos and Lioukas (2001). This scale has been supported by other authors (Dess & Davis, 1984; Fandel et al., 2004; Rivard et al., 2005; Teece et al., 1997). Respondents were asked to indicate in a Likert-type 5-point scale (1 means a lot less than the competitors and 5 means a lot more than the competitors) in which measure their capabilities can be considered a strength relative to their competitors. Fourteen items were considered in total. Examples of included items are “managerial competencies,” “market knowledge,” and “efficient and effective production department.”

For generic business strategies, we have followed Spanos and Lioukas (2001) too, which has been supported by other researchers (Dess & Davis, 1984; Pertusa-Ortega et al., 2009; Porter, 1980, 1985; Rivard et al., 2005). This 5-point Likert-type scale (1 means weaker than competitors and 5 means stronger than competitors) examines the extent to which differentiation or cost-leadership actions are taken. Examples of included items are “R&D expenditures for product development,” “innovation in marketing techniques,” and “modernization and automation of production processes.” A second-order multidimensional construct was used in this study (Ambrose & Schminke, 2009) for Firm Capabilities and Business Strategy scales as capabilities include lower level indicators of organizational (seven items), marketing (four items), and technical capabilities (three items); and strategy includes lower level indicators of innovation-differentiation strategy (three items), marketing-differentiation strategy (four items), and cost-leadership strategy (three items). To demonstrate the appropriateness and validity of the second-order constructs, the process defined by Johnson, Rosen, and Chang (2011) was followed.

To measure performance, the choice taken in the current study was the use of the performance’s perception measure in a dimension designated as profitability (three items; Dess & Robinson, 1984; Powell & Dent-Micallef, 1997). This scale was supported by other researchers (Choi & Lee, 2003; H. Lee & Choi, 2003; Venkatraman & Ramanujam, 1986, 1987). Therefore, a 5-point Likert-type scale was used (1 means far below average and 5 means far above average). Examples of included items are “profit margin” and “return on own capital.” All of these items were measured in relative terms to competitors (Dess & Robinson, 1984; Rivard et al., 2005; Venkatraman & Ramanujam, 1987; Woo & Willard, 1983). To avoid data distortion from contextual fluctuations and with the aim of getting closer to the notion of sustainable performance, answers reflected a 3-year period (Arend, 2006).

In the questionnaire, the variables number of employees, firm tenure, and legal form were included as control variables.

Results

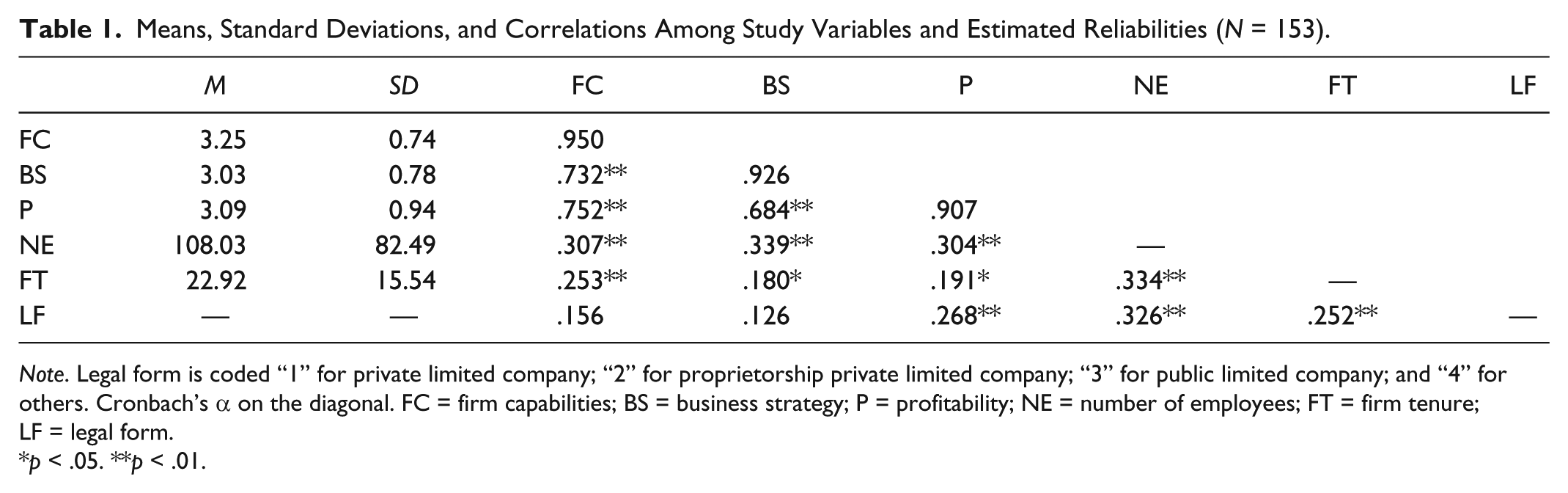

The means, standard deviations, simple correlations, and estimated reliabilities (Cronbach’s α) of the variables used in this study are presented in Table 1. The number of employees, date of incorporation, and legal form were significantly correlated with firm capabilities, business strategy, and profitability. Thus, these three variables were controlled for when testing the model (Shi, Chen, & Zhou, 2011). Firm capabilities were positively correlated with business strategy and profitability, and business strategy was positively correlated with profitability.

Means, Standard Deviations, and Correlations Among Study Variables and Estimated Reliabilities (N = 153).

Note. Legal form is coded “1” for private limited company; “2” for proprietorship private limited company; “3” for public limited company; and “4” for others. Cronbach’s α on the diagonal. FC = firm capabilities; BS = business strategy; P = profitability; NE = number of employees; FT = firm tenure; LF = legal form.

p < .05. **p < .01.

Measurement Model

Following the two-step procedure recommended by Anderson and Gerbing (1988), the measurement model employed the maximum-likelihood estimation and used the bootstrapping technique to correct for any deviation from the conditions of multivariate normality (Batista-Foguet & Coenders, 2000) and to enhance the statistical power to facilitate the detection of mediating effects (Wood, Goodman, Beckmann, & Cook, 2008).

The convergent validity analysis showed that the loadings of all indicators on their corresponding factors were significant (p < .001) and substantial (λ > .5). Moreover, two additional indicators—the composite reliability index and average variance extracted (AVE)—were calculated to assess the reliability of the scale. Both indicators exceeded the recommended minimum values of .7 and .5, respectively (Fornell & Larcker, 1981; see Table 2), confirming the scale’s reliability. Discriminant validity was evaluated by comparing the AVE with the squared correlations between constructs (Hair, Black, Babin, & Anderson, 2010); in all cases, the AVE was greater than the squared correlation estimates. The goodness-of-fit indices (GFIs) for the model were acceptable: χ2 (df) = 611.564 (340), p < .001, GFI = 0.775, root mean square error of approximation (RMSEA) = 0.072, Tucker–Lewis index (TLI) = 0.914, comparative fit index (CFI) = 0.923, χ2 / df = 1.799.

Standardized Measurement Coefficients, Composite Reliability, and AVE.

Note. AVE = average variance extracted.

p < .001.

Structural Model

The theoretical model (Model 1) was tested, and the effects of the number of employees, date of incorporation, and legal form on all of the variables included in the study were estimated. Based on the results, the model fit was acceptable: χ2 (df) = 755.803 (420), p < .001, GFI = 0.758, RMSEA = 0.0073, TLI = 0.897, CFI = 0.907, χ2 / df = 1.8. In sharp contrast to the number of employees, firm tenure and legal form were not significantly related to business strategy. Also in contrast to legal form, the number of employees and firm tenure were not related to profitability. The structural paths between capabilities and business strategy (β = .773, p < .001), business strategy and profitability (β = .368, p < .01), and capabilities and profitability (β = .528, p < .001) were significant, thus confirming H1, H2, and H3.

In view of these results, H4—business strategy partially mediates the relationship between capabilities and profitability—was supported. Baron and Kenny’s (1986) framework for mediation analysis was used to fully confirm this hypothesis. This framework advocates that a full mediating relationship is established if the following criteria are met: (a) a significant association between the exogenous variable (firm capabilities) and the mediator (business strategy) exists, (b) a significant relationship between the mediator (business strategy) and the endogenous variable (profitability) exists, and (c) a significant association between the exogenous (firm capabilities) and the endogenous (profitability) variable exists, which then disappears once the mediator (business strategy) has been taken into consideration. So, two additional models were tested. The first one (Model 2) was similar to Model 1 except for the exclusion of a direct path from firm capabilities to profitability. The second additional model (Model 3) included a direct path between firm capabilities and profitability, whereas the mediating paths were set to 0.

Table 3 presents the model-fit statistics and the path coefficients of the three models. The relationship between firm capabilities and profitability is significant in Model 3 (direct effects), and it does not disappear once business strategy is taken into consideration (Model 1). The paths from firm capabilities to business strategy and from business strategy to profitability remain significant in both models (partial and full mediation). The chi-square of Model 1 (partial mediation; χ2 = 755.803, df = 420) was lower than the chi-square of Model 2 (full mediation; χ2 = 773.837, df = 421), and the chi-square of Model 3 (direct relation; χ2 = 873.049, df = 422) was significantly different (Δχ2 = 18.034, Δdf = 1; Δχ2 = 117.246, Δdf = 2), respectively. The three hypotheses tested, joined by the best fit of Model 1, resulting in this model being accepted as a better choice. Based on these results, business strategy partially mediates the relationship between firm capabilities and profitability, supporting H4. In addition, the Sobel (1982) test was performed to assess the significance of the indirect effects of firm capabilities on profitability as mediated by business strategy, with the results highlighting the importance of business strategy as a mediator (z = 2.89; p < .01). Figure 1 summarizes the results of the hypothesis testing.

Structural Equation Path Coefficients and Fit Results for Structural Equation Models.

Note. Model 1: partial mediation; Model 2: full mediation; Model 3: direct effects. RMSEA = root mean square error approximation; CFI = comparative fit index; GFI = goodness-of-fit index; TLI = Tucker–Lewis index.

p < .01. ***p < .001.

Standardized path coefficients in the partial mediation model.

Discussion

In this study, three types of relationships were analyzed using data from industrial textile firms in northern Portugal. All the hypotheses proposed were supported, so organizational capabilities have a direct and positive influence on profitability and an indirect influence through business strategy. The study first examined the effect of possessing a set of capabilities on a given firm’s profitability. This research concluded that the more a firm concentrates on these capabilities relative to its competitors, the more its profitability increases. Thus, H3 was supported. As postulated, the direct impact of possessing a certain and superior set of capabilities on a firm’s profitability has been shown to be significant. These results are in line with previous studies that examined different types of capabilities with results largely coinciding with the classification proposed in the present study (Piercy et al., 1998; Tayles et al., 2007). In the current study, this strong connection indicates that the capabilities of Portuguese textile firms—rooted in a strong set of resources—continue to be crucial for increasing profitability. These results suggest that textile organizations that invest in the development of their capabilities over time generally enjoy improved performance relative to competitors that do not develop their capabilities.

Second, the relationship between a firm’s capabilities and its competitive advantage was analyzed considering a given firm’s ability to implement a better business strategy (Cater & Cater, 2009; Hitt et al., 2001; Rivard et al., 2005). This relationship was also shown to be significant as supported by organizational theory, which argues that tangible and intangible resources are essential to attaining sustainable competitive advantages (Amit & Schoemaker, 1993; Arenas & Lavanderos, 2008; Barney, 1991; Morgan et al., 2004; Piercy et al., 1998; Spanos & Lioukas, 2001). So, H1 was supported. Future studies should further explore and confirm this relationship. The takeaway for managers in northern Portugal’s industrial textile sector is that organizations must develop long-term strategies and strong and sustainable competitive advantages. So, textile firms must make a considerable investment in their resources as well as their technical, marketing, and organizational capabilities. As an example, they could explore their positioning in the market in a more robust way and act more effectively, considering the new competition derived from the increasingly globalized market. Strategies along these lines are likely to help these organizations increase their profitability.

Finally, the direct effect of a firm’s strategy on its profitability was also examined and shown to be significant, supporting H2. As expected, the results obtained are consistent with the aforementioned studies (Morgan et al., 2004; Piercy et al. 1998; Spanos & Lioukas, 2001). Therefore, the significant effect of strategy on performance corroborates the impact for the textile organizations studied; thus, the theoretical and empirical implications are that an organization must explore and develop its strategic positioning, developing a pool of available resources that are crucial to the formulation of its business strategy (Grant, 1991; Rumelt, 1991). In addition, the results indicate that organizations should explore the resources at their disposal and develop new capabilities that allow them to adopt competitive strategies that lead to superior performance. Portugal’s industrial textile organizations—even those that have developed strong competitive advantages—have found difficult to increase their sales and market shares, and therefore, their profitability. This difficulty is clearly related to growing international competition and the arrival of new organizations with a marked competitive aggressiveness, particularly in terms of price. Based on the results of this analysis of northern Portugal’s textile industry, it is very important that these organizations implement strong and well-outlined strategic decisions, as new competitors—mainly from emerging countries—have well-developed characteristics that ensure their strong strategic positioning in the market.

Finally, the effects of the mediating variable, business strategy, were examined to better understand the relationships proposed in the theoretical model (Baron & Kenny, 1986; Preacher & Hayes, 2004). This was accomplished by analyzing the impact of a given firm’s capabilities on its profitability and considering whether that effect appeared to be reinforced by the business strategy. In this article, the influence of capabilities on profitability was analyzed in terms of the mediation role of competitive advantage; and the results reflect the confluence of effects on profitability, which derive from the ability of an organization to alter its strategy relative to its capabilities (Edelman et al., 2005; Lages et al., 2009; López-Cabrales et al., 2009). So, the business strategy of the firms studied partially mediates the relationship between their capabilities and their profitability (Chrisman, 1999; Edelman et al., 2005; Ramaswami, Srivastava, & Bhargava, 2009). So, H4 was also supported. In contrast, Reimann, Schilke, and Thomas (2010) studied the relationship between technological resources and firm performance, finding that this relationship was not partially but fully mediated by cost-leadership and differentiation strategies.

In view of these results, it is very important that Portuguese textile organizations develop strong and intense capabilities as they affect not only performance but also business strategy. Organizational, marketing, and technical capabilities are crucial to enable Portuguese textile companies to choose successful strategies (Richey et al., 2010). On one hand, organizational capabilities are important to help the companies assure a qualified management structure and to understand their complex environment. This type of capabilities is related to management and organizational processes, the manager competences and the employees’ knowledge and skills, the efficient organizational structure, the organizational culture, the existing mechanism of coordination, the strategic planning procedures, and the ability to attract creative employees (Galbreath, 2005; Teece et al., 1997). However, technical capabilities help the companies to reach the operational efficacy and efficiency, ensuring the exigent levels of competitiveness required by the market. These capabilities are related to the efficiency of the productive process and the technological capabilities, and, in terms of supporting infrastructures, they are also related to the scale economies and the technical experience (Leonard-Barton, 1995; Spanos & Lioukas, 2001). Finally, the marketing capabilities, which are the weakest of the Portuguese textile industry, are fundamental to communicate their products to customers, trying to get their loyalty. These capabilities are also related to the creation of strong and confident relationships with customers and suppliers, the knowledge of the markets, and the control of the distribution channels (Lado, Boyd, & Wright, 1992; Spanos & Lioukas, 2001). Based on these three types of capabilities, organizations will be able to build strong strategies focus on innovation and marketing-differentiation strategies, considering these perspectives the most correct ones to enable Portuguese textile companies to obtain competitive advantages (Fandel et al., 2004; Tayles et al., 2007). In this sense, the companies will be ready to build their brands and compete for more demanding customers. It is not recommended that the Portuguese textile companies focus only on cost-leadership strategies because they will have more difficulty to develop strong and profitable strategies.

In sum, Portuguese textile managers who are able to develop strategies in line with these strong capabilities can achieve greater competitive advantages, and ultimately, improve their organization’s performance. Textile organizations should also focus on three important lines of orientation: (a) managing an efficient and effective production department that is open to product and processes innovation, (b) developing knowledge and technical expertise by exploring economies of scale, and (c) investing in equipment and technological capabilities. In this way, textile firms can more easily ground their actions in strong business strategies that guarantee sustainable competitive advantages. In addition to selecting the best business strategy, having the resources necessary to develop their specific and singular capabilities will likely lead to improve performance, which will undoubtedly increase the profitability of northern Portugal’s textile organizations (see Figure 2).

Conceptual framework resulting from the findings.

Research Limitations and Future Research

This study has certain limitations. The principal limitation is that data were collected from a single setting using self-report measures. Several procedures were employed to minimize these limitations, which are common to social studies. First, the study relied on scales previously tested and confirmed by other researchers to eliminate ambiguity (Podsakoff, Mackenzie, Podsakoff, & Lee, 2003). Second, managers were informed that their responses to the questionnaire would be anonymous to encourage them to provide honest answers. Third, the dependent variables of the study were located after the independent ones, thus minimizing the influence of consistency artifacts (Salancik & Pfeffer, 1977). According to Podsakoff and his colleagues (2003), the above procedures should ensure that participants do not feel that they are being judged personally, encouraging them to provide honest answers free of speculation regarding the study’s objectives. Finally, Harman’s (1967) single factor test was used to evaluate the common method variance bias, carrying out an exploratory factor analysis on all of the study variables (27) to identify any single factor that might be responsible for most of the variance (Christmann, 2000). The factor analysis identified four factors with eigenvalues greater than 1, which explained 70.46% of the total variance; the first factor explained 14.02% of the total variance. These results indicate that the bias associated with the common method variance was not a significant concern for this study.

This study examined the relationship between firm capabilities, business strategy, and profitability in northern Portugal’s textile industry. Future studies could consider other specific constructs, such as knowledge management. It would be very interesting to analyze the interplay between tacit and explicit knowledge in creating different types of organizational capabilities, and their direct and interaction effects on firm performance. Moreover, it would be interesting to analyze the moderating role of different types of capabilities in the relationship between knowledge and firm performance. Also, organizational capability being a broad theoretical construct, future studies could examine the impact of different types of organizational capabilities on strategy and firm performance. Future studies can also be positioned in other industries, as well as in other geographical areas to offer more general results applicable to different regions and industries. This is particularly important because the specific characteristics of each industry in each country make hardly generalize the results obtained.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.