Abstract

In Australia, an increasing number of households face problems of access to suitable housing in the private market. In response, the Federal and State Governments share responsibility for providing housing assistance to these, mainly low-income, households. A broad range of policy instruments are used to provide and maintain housing assistance across all housing tenures, for example, assisting entry into homeownership, providing affordability assistance in the private rental market, and the provision of socially owned and managed housing options. Underlying each of these interventions is the premise that secure, affordable, and appropriate housing provides not only shelter but also a number of nonshelter benefits to individuals and their households. Although the nonshelter outcomes of housing are well acknowledged in Australia, the understanding of the nonshelter outcomes of housing assistance is less clear. This paper explores nonshelter outcomes of three of the major forms of housing assistance provided by Australian governments—low-income mortgage assistance, social housing, and private rent assistance. It is based upon analysis of a survey of 1,353 low-income recipients of housing assistance, and specifically measures the formulation of health and well-being, financial stress, and housing satisfaction outcomes across these three assistance types. We find clear evidence that health, finance, and housing satisfaction outcomes are associated with quite different factors for individuals in these three major housing assistance types.

Introduction

In Australia, an increasing number of households face problems of access to suitable housing in the private market as a result of unaffordability, discrimination, adequacy, or locational requirements (Steering Committee for the Review of Government Service Provision [SCRGSP], 2011). In response, the Commonwealth and State Governments share responsibility for providing housing assistance to these, mainly low-income, households. A broad range of policy instruments are used to provide and maintain housing assistance across all tenures, for example, assisting entry into homeownership, providing affordability assistance in the private rental market, and the provision of socially owned and managed housing options. Underlying each of these interventions is the premise that secure, affordable, and appropriate housing provides not only shelter but also a number of nonshelter benefits to individuals and their households. Such a premise is enshrined across Australian policy and practice. The current National Affordable Housing Agreement (NAHA), which defines the roles and responsibilities of all levels of Australian government with respect to housing and homelessness, is a key example; it aims to ensure “that all Australians have access to affordable, safe and sustainable housing that contributes to social and economic participation” (Objective 6, NAHA). This objective clearly assumes that, beyond mere shelter, housing assistance has other social, economic, and well-being outcomes.

Although many of the nonshelter outcomes of housing are well acknowledged in Australia, the understanding of the nonshelter outcomes of housing assistance is less clear. Apart from some notable exceptions (e.g., Bridge, Flatau, Whelan, Wood, & Yates, 2003; McDonald & Merlo, 2002; Phibbs, 2005; Phibbs & Thompson, 2011), few studies have sought to robustly investigate the longer term impacts of housing assistance. Important among the findings of these studies is the finding of Phibbs (2005; building on the earlier analysis by McDonald & Merlo, 2002) that among lower income groups, “non-shelter outcomes are likely to be sharpest at the bottom end of the market where housing conditions do work against households achieving appropriate outcomes in health, education and other areas” (p. 5). What this means is that nonshelter outcomes for low-income households are different and cannot be straightforwardly generalized from those of the broader population. In addition, because housing assistance is principally targeted to households with very low incomes and often high and complex needs, the outcomes of that assistance are likely to be even more distinct from those of the national average. To some extent, the fact that the nonshelter outcomes of housing assistance are poorly known sits at odds with the underlying objectives of such assistance programs (such as NAHA).

This paper explores nonshelter outcomes of three of the major forms of housing assistance provided by Australian governments—low-income mortgage assistance, social housing, and private rent assistance (Commonwealth Rent Assistance [CRA]). It is based upon analyses of a survey of 1,353 low-income recipients of housing assistance, and specifically measures the formulation of health and well-being, financial stress, and housing satisfaction outcomes across these three assistance types.

Background

Australia is a relatively well-housed nation, with good quality stock by international standards. For many decades, the “Great Australian Dream” of homeownership was attainable by average-income working families, and the homeownership rate was stable at just under 70% of the population. For those households that could not afford to, or choose not to, own their own homes, a private rental market and a small social housing system provided alternative housing options (representing on average around 25% and 5%, respectively, of the market). Although these three housing tenures still house similar proportions of Australians, much has changed in recent years. Alongside a severe (and increasing) supply shortage (Commonwealth of Australia National Housing Supply Council, 2011) and demographic change, which has increased the number of separate households and hence housing demand (Flood & Baker, 2010), Australia has become one of the most unaffordable housing markets in the world. Recent work by Demographia (2010) rates most Australian housing markets as being less affordable than those in Canada, the United Kingdom, and the United States. As a result of such changes (described in greater detail in Beer, Baker, Wood, & Raftery, 2011), increasing proportions of the population, especially the low-income population, are not able to afford appropriate, adequate, or secure housing, and in response, Australian governments provide various forms of housing assistance.

Alongside a number of untargeted measures, such as First Home Owner Grants, and tax benefits to private landlords, three main forms of targeted housing assistance are provided specifically to low-income households. They are public rental housing, rental subsidies for privately owned rental properties, and homeownership assistance. Public housing is funded and managed by the Federal and State governments. Fulfilling a welfare role, entry to houses of this sector is limited to tenants on very low incomes, often with multiple and complex needs. Although varying slightly between states, rents in public housing are capped at around 30% of household income, to make them affordable. The relatively small size of this sector, and increasing welfare demand, has meant that obtaining public housing is difficult, and many individuals spend up to a decade or more on waiting lists to enter the tenure. The second major form of assistance is aimed at renters in the private market—CRA. This rent assistance is paid to low-income households who would be eligible for entry into public rental housing, but who reside in the private rental sector. Although it provides some assistance with housing costs, this welfare payment is aimed at reducing the cost, rather than making private rental affordable, and even with this assistance type, many private renters experience extreme housing unaffordability. The third major form of housing assistance aimed at low-income households is mortgage assistance. In Australia, two state and one territory governments provide mortgage assistance to households whose income would otherwise make them ineligible for a housing loan. The structure of this assistance may be in two forms, either a structured repayment schedule that distributes payments more evenly across the term of the loan, or by providing loans to households who may not be eligible in the private market.

While each of these housing assistance types provides obvious shelter benefits to recipients, little is known of the other, less direct ways in which such interventions may benefit these households. This paper examines three of these potential benefits—health, financial stress, and housing satisfaction.

Housing Assistance, Health, Financial Stress, and Housing Satisfaction

Housing is well documented to be a key determinant of the health and well-being of individuals and households (e.g., Braubach, 2011; Marmot, Friel, Bell, Houweling, Taylor, 2008; Shaw, 2004). Varied housing assistance programs exist across all postindustrial countries, and an existing body of research has shown that such programs have similarly varied impacts across and beyond housing quality (Comey, Popkin, & Franks, 2012), education (Phibbs, 2005), employment (Bridge et al., 2003), and welfare reception (Newman, Holupka, & Harkness, 2009). This study compares, across the three major housing assistance types, the component population and housing characteristics associated with health, financial stress, and housing satisfaction.

Housing costs (either rent or mortgage payments) are on average the largest category of expenditure for Australian households, accounting for around 20% of all household expenditure (United Nations Statistics Division, 2008), and therefore, the effect of housing assistance on the financial stress experienced by households is crucial. Moreover, many housing assistance programs aim to address affordability alone in order that other nonshelter benefits may follow. Although we know little of the direct effects of housing assistance type on housing satisfaction, we know from the established literature on housing choice and preferences that there is a “natural preference” for homeownership (Saunders, 1990) and that housing assistance that enables homeownership is most likely to be associated with better housing satisfaction.

Interest in health as a benefit of housing assistance is increasingly recognized by researchers and policy makers. Health has been shown in a growing number of studies to be an outcome of affordable (Bentley, Baker, Mason, Subramanian, & Kavanagh, 2011), secure (Mallett et al., 2011), well-located (Wright & Kloos, 2007), and good quality (Wells & Harris, 2007) housing. Important to an examination of different tenure-based forms of housing assistance, health effects have been shown to be tenure dependent across a number of studies. Positive health effects have been attributed to homeownership across a number of studies (e.g., Gibson et al., 2011), through “autonomy and prestige” (as described by Hiscock, Macintyre, Kearns, & Ellaway, 2003). Interestingly though, a number of studies have reflected on negative health effects attributed to the “burden of debt” (Gibson et al., 2011, p. 178) experienced by some home owners. Similarly, Smith, Easterlow, and Munro (2004) suggest that homeownership may be health limiting for individuals with existing illnesses, poor health, or other vulnerabilities. This is because the costs of maintaining housing or mortgage payments may be unsustainable, or the low incomes of these individuals may not allow the purchase of dwellings of sufficient quality or the location to be health promoting. One of the few Australian studies to specifically examine the health outcomes of housing assistance among individuals entering public housing found that health improved via a number of pathways, such as improved access to medical resources, improved housing quality and security of tenure, and importantly, improved financial resources (Phibbs, 2005).

Study Design and Description of the Populations

This analysis is based on the results of a postal survey administered in 2008 to 4,051 low-to-moderate-income South Australian households. Surveys were sent to households recorded as being in receipt of housing assistance between 2003/2004 and 2008/2009. Three housing assistance groups were targeted:

homeownership assistance (this group had entered homeownership via a state government mortgage provider),

public housing (this group had public rental housing tenants), and

private rent assistance (this group had private tenants in receipt of the Australian Government’s rental assistance payment—CRA).

The postal survey comprised approximately 100 questions, including standardized measures of physical and mental health, 1 questions about employment, perceptions of the impact of housing assistance, and demographic, economic, and locational accessibility. Along with structured response questions, a number of the questions were open ended, allowing respondents to provide more in-depth responses on the effects and influence of housing assistance. In total, 1,353 surveys were returned from households in receipt of housing assistance representing a response rate of over 33%. Importantly, for each assistance group, a statistically representative sample was achieved.

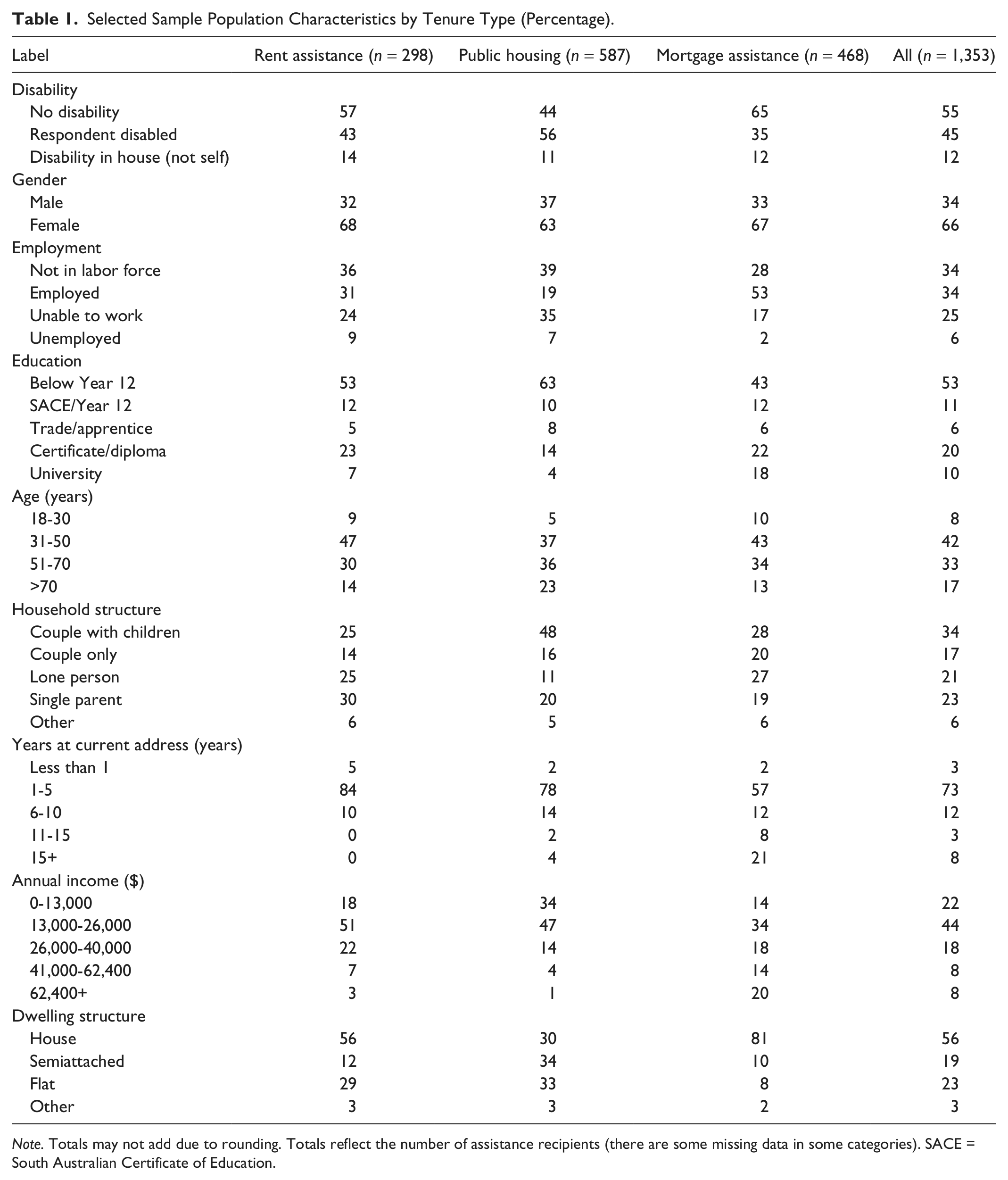

As shown in Table 1, the population characteristics across the three intervention groups are different. The public housing group was more concentrated in the older age cohorts, while the rent assistance and mortgage assistance groups tended to be more concentrated in the working ages. A very high proportion of public renter respondents had a disability (57%), followed by 44% of rent assistance respondents, and a much smaller 35% of mortgage assistance respondents. Unsurprisingly, more than half of all mortgage assistance respondents were employed compared with less than 20% of public housing respondents. Correspondingly, very few (2%) respondents from the mortgage assistance group were unemployed, though about 17% were “unable to work.” The three assistance groups were also different in terms of their household structure, with single-parent households dominating the rent assistance group, and lone-person households dominating both the public housing and mortgage assistance groups.

Selected Sample Population Characteristics by Tenure Type (Percentage).

Note. Totals may not add due to rounding. Totals reflect the number of assistance recipients (there are some missing data in some categories). SACE = South Australian Certificate of Education.

An additional and stark cohort difference was residential mobility/stability. Less than 1% of the private rent assistance group had lived in their home for more than 10 years, compared with the homeownership group, where 29% had lived in their home for more than 10 years. Overall, the public housing group had a similar pattern of high mobility to that seen in the renter group. Although the public housing group was most likely to have low incomes, the income distribution was again most similar to the renter group. Finally, the table shows that the dwelling types occupied by these three sample groups were often different. More than 80% of mortgage assistance recipients lived in detached houses, compared with around half of private renter households, and under a third of public renters.

In addition to the findings shown in Table 1, an earlier analysis of this survey data (Beer et al., 2011) also showed that not only were there descriptive cohort differences between the groups, but also, individuals within each group on average regarded the impact of their housing on their health differently. Overall, when asked to rate the impact of their current housing (on a scale from very positive to very negative) on various elements of their health and well-being, there was a clear pattern of response. In each case, those in the homeownership assistance group were most likely to regard their housing’s effect as positive, followed by a smaller proportion in the public housing group, and finally, a much smaller proportion of rent assistance recipients regarding their housing’s impact as positive.

Method

In this analysis, three survey questions are examined, reflecting self-assessed health, financial stress, and housing satisfaction. Self-assessed general health is measured using the Short Form (SF-1) question from the SF-36 Quality of Life survey instrument. This instrument is one of the most widely used self-completion measures of health status (Coons, Roa, & Keininger, 2000), and the SF-1 question has been validated across a number of Australian studies (e.g., Gill, Broderick, Avery, Dal Grande, & Taylor, 2009). This question asked the following: “In general, would you say your health is excellent, very good, good, fair, or poor?” Individual housing satisfaction was assessed using a similar question that sought responses on a five-point scale: “How well would you say your current home meets the needs of you (and your family)?—very well, well, satisfactorily, slightly, not at all.” Self-assessed financial stress was measured using the survey question,

In the last 12 months, have any of these things happened to you because you were short of money? Could not pay electricity, gas, or telephone bills on time; pawned or sold something; went without meals; unable to heat or cool your home; asked for assistance from family, friends or community organisations; none of the above.

The dependent variables in the following regression models are self-rated ordered responses. There is meaning assigned to the ranking of choice, but it is not assumed that the measures are interval metrics. Thus, general health and financial stress are modeled as five-point scales. In the regression analysis, we use a generalization of the binary choice framework: the ordered logit estimation technique. In this latent-variable approach, the dependent variable (y*) is estimated as a linear function of the set of independent (explanatory and control) variables (Xs) and a set of threshold values (τ = 1…m). 2 The model estimates the coefficients (β) and threshold points; an error term (ϵ; assumed to be logistically distributed) is added to the structural model representation. Multinomial or ordinal choice models assume that the individuals are faced with a number of choices and that the choice they make is a function of their characteristics. Thus, we estimate a model that allows prediction of the (conditional) probability that individuals make specific choices:

where i indexes individuals and k the explanatory variables. Ordered outcomes are assumed to take place sequentially as the latent variable, y*, crosses the progressively higher threshold values (τ). The sign of the coefficient can be interpreted by determining whether the latent variable increases with each X: For a positive β, an increase in X can be interpreted as a decrease in the probability of being in the lowest category (y i = 1) and an increase in the probability of being in the highest category (yi = m).

Therefore, the probability of observing outcome j corresponds to the (conditional) probability that the estimated linear function (plus error) is within the range of the estimated threshold values:

A well-known feature of the ordinal logit is that it is only possible to make unambiguous statements about being in the lowest or highest group in the ordered dependent variable, and there is ambiguity about the other groups, that is, in these models, it is not clear what would happen to the groups/categories between the highest and lowest (it is not possible to overcome this feature of this model). 3

As the interpretation of the estimated coefficients is not intuitive (they represent the log-odds 4 ), they are converted to odds ratios (ORs) where OR = eβ. An OR of 1 means that the odds of an event is the same in both the “treatment” and “control” group; for example, an OR of 2 means that, all other things equal, the OR is twice as high in one group versus the reference group whereas an OR of say 0.5 says that one group has half the odds of the reference group—The odds of financial stress are about 50% lower (all other things equal). Therefore, when interpreting an OR, it is helpful to look at how much it deviates from 1. So, for example, an OR of 0.75 means that in one group, the outcome is 25% less likely; an OR of 1.33 means that in one group, the outcome is 33% more likely (Cameron & Trivedi, 2005).

Three strategies are suggested for model construction: forward selection, backward elimination, and a stepwise process (Le, 1998). The econometrics literature is clear and unambiguous; general to specific is superior (given a sufficient sample size; Gilbert, 1986; Greene, 2003; Hendry, 1995). Theoretically, the econometrically derived general-to-specific specification is a parsimonious model that removes irrelevant variables, avoids large Type I errors, and reduces the likelihood of multicollinearity, which would reduce the validity of the estimates and of the statistics used to measure individual and model goodness of fit (Cameron & Trivedi, 2005). To balance overfitting 5 and underfitting, and in recognition of the small sample size, 6 in the econometric analysis, variables are retained in models from the general-to-specific method at least at the 20% level of significance.

For analysis of the influence of tenure type, preliminary models are estimated using pooled data (i.e., we include tenure type as a set of dummy variables and model the full sample). In all cases, preliminary results indicate that aggregation is inappropriate and that individuals cannot be treated as a homogeneous group: across forms of housing assistance, groups are heterogeneous. Final results strongly support this view. Modeling at the disaggregate tenure type level has the disadvantage that samples become relatively small—and in some cases a potential explanatory variable must be excluded due to small cell numbers, 7 but this disadvantage is overwhelmed by the model results that lead conclusively to the view that individuals in various forms of tenure type cannot be aggregated as if homogeneous.

Two final issues are considered. First, one potential issue for econometric models of health outcomes is endogeneity (due to reverse causality 8 or a feedback process from an unobserved attribute). To control for the potential influence of tenure type on general health, in this model, we included only those sample members who have resided at their current address for more than 1 year. Thus, any change in the tenure type preceded the current health status by 1 year. 9

Second, consideration of results below demonstrates that some explanatory variables are statistically significant for all tenure types and it may be interesting to know if these coefficients are statistically different across tenure types, for example, does an OR of 0.197 differ from 0.243 for the impact of disability on general health? We do not test this relationship at the individual coefficients level, but at the model level, the hypothesis of equal common coefficients is consistently rejected.

Results and Discussion

Tables 2 to 4 show the general-to-specific ordered logistic regression models for the three forms of tenure type (rent assistance, public housing, and mortgage assistance). The exogenous explanatory (or control) variables are given in column 1, the reference category in column 2, and estimated coefficients reported as ORs in the other columns of tables. 10

Self-Rated General Health.

Note. OR = odds ratio. OR < 1 = more likely to be very satisfied; OR > 1 = more likely to be slight/not satisfied.

Categories included overcrowding, lack of storage space, lack of adequate heating or cooling facilities, structural problems, serious disrepair, damp and mold, lack of private outdoor space, or other respondent-specified problems.

p < .10. **p < .05. ***p < .01; only significant results are shown; unmarked are significant at p < .20.

Financial Stress OR.

Note. OR = odds ratio; p/wk = per week. OR < 1 = more likely to be very satisfied; OR > 1 = more likely to be slight/not satisfied.

Categories included overcrowding, lack of storage space, lack of adequate heating or cooling facilities, structural problems, serious disrepair, damp and mold, lack of private outdoor space, or other respondent-specified problems.

p < .10. **p < .05. ***p < .01; only significant results are shown; unmarked are significant at p < .20.

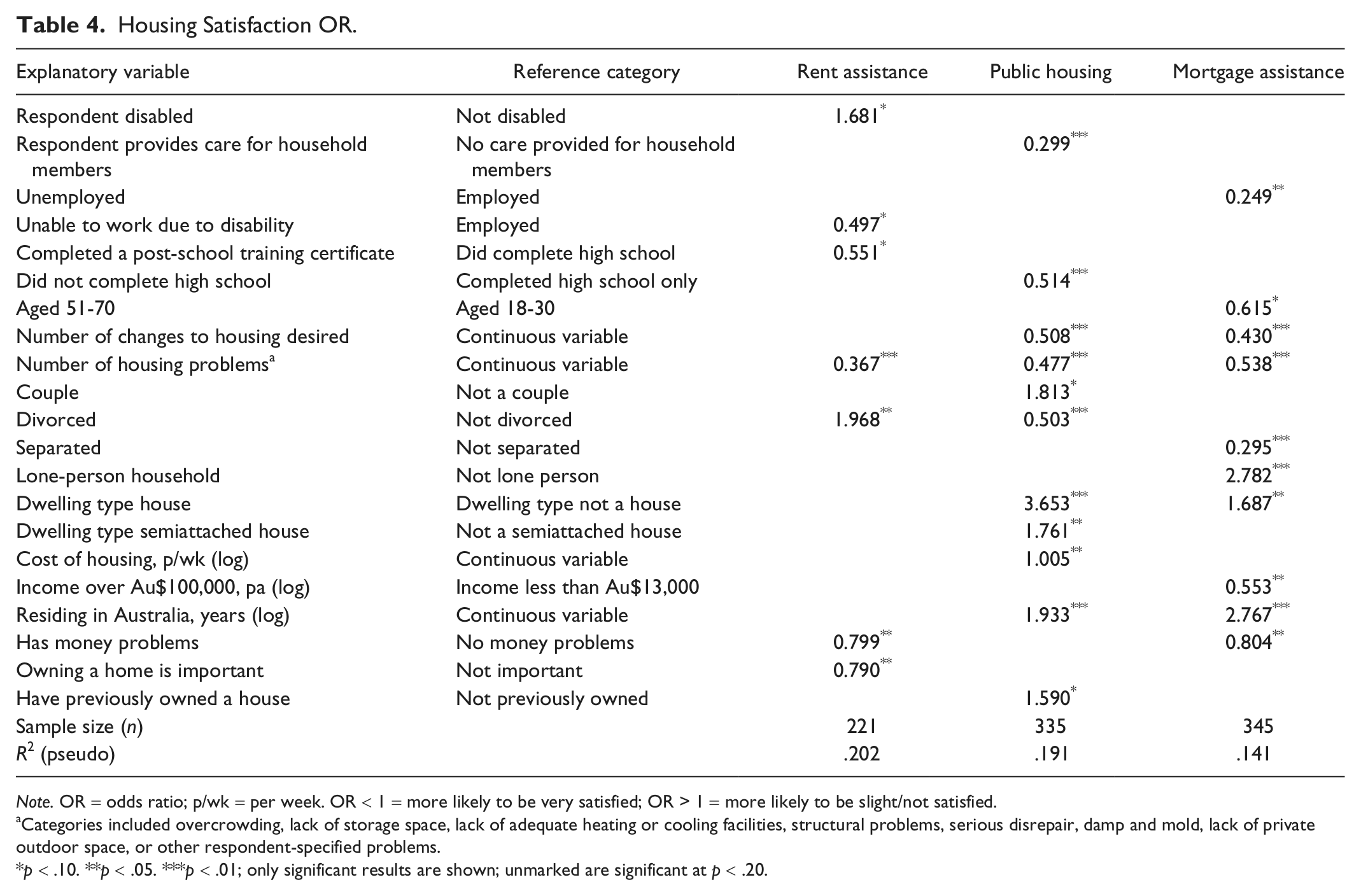

Housing Satisfaction OR.

Note. OR = odds ratio; p/wk = per week. OR < 1 = more likely to be very satisfied; OR > 1 = more likely to be slight/not satisfied.

Categories included overcrowding, lack of storage space, lack of adequate heating or cooling facilities, structural problems, serious disrepair, damp and mold, lack of private outdoor space, or other respondent-specified problems.

p < .10. **p < .05. ***p < .01; only significant results are shown; unmarked are significant at p < .20.

Using Table 2 as a guild to interpreting the tables, across each of the three housing assistance populations (rent assistance, public housing, mortgage assistance), average self-rated health can be explained by different combinations of population characteristics (explanatory variables, for example, respondent disabled). The relative effect of each explanatory variable in explaining differences in self-rated health is compared with a reference category (in this case, not disabled) and expressed as an OR (e.g., 0.210), representing the size of the effect. ORs center on 1, with lower numbers relating to higher self-rated health and higher numbers relating to lower self-rated health. In this example, an OR of 0.210*** indicates that in explaining self-rated health (for recipients of rent assistance) compared with respondents without a disability, those with a disability have lower self-rated health (*** indicates that this finding is highly statistically significant).

As noted above, explanatory coefficients are retained at the 20% level of significance: p values of .01 (***), .05 (**), and .10 (*) are indicated. Below the 20% significance level, explanatory variables are rejected from the model as they add no explanatory power.

General Health

Table 2 highlights some similarities and some substantial differences across the tenure types. In terms of commonalities across the three groups, the inability to work and the presence of disability in the household stand out as strong and significant probable influences on self-rated health. Across each assistance type, the presence of a disability in the household appears as a key indicator of poorer general health. Employment was associated with substantially higher health for public housing recipients and mortgage assistance recipients, and correspondingly, the inability to work was associated with lower self-rated heath across all three assistance types.

Overall though, the results show more differences between the groups than similarities. For recipients of private rent assistance, the characteristics most strongly associated with poorer health were the completion of high school only, unemployment and the inability to work, disability, and age. For publicly housed respondents, such a strong association with poor health was only seen in the case of disability. For the mortgage assistance group, the strongest effects were seen across disability, employment, and education. Interestingly, unemployment only appears to be relevant to health among the rent assistance group. The level of education did not appear relevant to health outcomes in the public housing group, but among rent assistance recipients, having completed high school was associated with a much higher level of health. Similarly, in the mortgage assistance group, having completed a university degree was also associated with a much higher level of health. Finally, income was only relevant to health for the rent assistance cohort, where a relatively higher income was generally related to better health.

Financial Stress

The models of financial stress (Table 3) have even less commonality across the assistance types. For recipients of rent assistance, the likelihood of being in financial stress was highest in the presence of unemployment, the inability to work because of disability, and residential instability. In this group, age also appears to provide protection from financial stress. For public housing tenants, the presence of disability in the household and caring for someone outside the home were among the strongest correlates of financial stress. Interestingly, within this group, those from a non-English speaking background were less vulnerable. Finally, in the mortgage assistance group, employment appeared less important in the vulnerability to financial stress, but disability in the household and household structure (with couple households being less vulnerable and divorced households more vulnerable) stood out in their strength of importance.

To some extent, public housing tenants showed more similarity in their pattern of vulnerability to financial stress to mortgage assistance recipients than the other renting group—private renters. Both the public housing and mortgage assistance groups were especially vulnerable to financial stress when a member of their household had a disability, although all groups were to some extent vulnerable to financial stress if they were unable to work because of a disability. Furthermore, being unemployed appears to affect the probability of being in financial stress for rent assistance recipients most of all, whereas for the mortgage assistance group, unemployment did not significantly influence the odds of being in financial stress. This finding probably does not truly reflect the importance of unemployment in the group with mortgages; in the sample, very few with mortgages are unemployed, perhaps because of the need to actively make home loan repayments. That is, individuals of this group probably spend less time in unemployment, even if they temporarily took imperfect employment.

Housing Satisfaction

Table 4 presents results for housing satisfaction. It shows, unsurprisingly, that the number of perceived housing problems is closely associated with lower housing satisfaction. This was found relatively uniformly across each of the three housing assistance types. Among public renters and mortgage holders, residence in a detached house was a strong predictor of housing satisfaction. Interestingly, this dwelling type was not significantly associated with housing satisfaction among the population in receipt of rent assistance. Household structure was also related to increased odds of housing satisfaction, though it varied across the assistance types. For public renters, being in a couple household was associated with greater odds of housing satisfaction, and being divorced, was associated with lower housing satisfaction. Interestingly, being divorced was associated with higher housing satisfaction for recipients of rent assistance. Among mortgage assistance recipients, being separated was associated with lower housing satisfaction, and living alone with much higher housing satisfaction.

Conclusion

Overall, this analysis has highlighted a breadth of difference across the three Australian housing assistance cohorts. Health, financial stress, and housing satisfaction are experienced very differently by each group, showing that this low-income population is far from homogeneous. Obviously, these differences are compositional as well as, most probably, causal, meaning that it is likely to be both the characteristics of those allowed (or encouraged) entry to each housing assistance type and the effects of gaining access to that housing intervention that is measured in this analysis. This small study has highlighted the very real differences across assistance type cohorts, in the way they are composed, as well as the way that they are likely to respond to housing assistance. Because these three groups are clearly not homogeneous, it follows that housing assistance policies need to better acknowledge these differences. Such findings support the need for varied housing assistance responses, such as the three examined in this study, and hint at refinements that may improve outcomes for recipients (e.g., addressing the significant financial disadvantage experienced by individuals receiving homeownership assistance who have a disability, or directly targeting employment assistance to low-income households receiving rent assistance). The analysis also highlights the ways in which failure in other domains of policy bleed into housing assistance and housing outcomes across Australia. Lower levels of educational attainment, unemployment, and the presence of a disability in the household were strongly associated with adverse housing outcomes regardless of tenure. Recent initiatives by the Australian Government have overtly acknowledged such shortcomings, with the introduction of a National Disability Insurance Scheme (SCRGSP, 2011), the reform of school funding (Gonski, 2011), and an ongoing reform in employment assistance. Housing is likely to generate a more powerful set of nonshelter benefits when other causes of disadvantage—such as low incomes associated with the presence of a disability—are less acute.

Footnotes

Acknowledgements

We thank the two anonymous reviewers as well as participants at the Asia Pacific Network for Housing Research Conference for their useful suggestions.

Authors’ Note

An earlier version of the analysis was presented at the Asia Pacific Network for Housing Research Conference.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research and/or authorship of this article: This paper emerges from a study of the relationship between housing and health funded by the Australian Research Council (ARC Linkage Project LP0776660 and ARC Discovery Project DP120102974).