Abstract

This article explores monetization and networking strategies within the consolidating creator economy. Through a large-scale study of linking practices on YouTube, we investigate how creators seek to build their online presence across multiple platforms and widen their income streams. In particular, we build on a near-complete sample of 153,000 “elite” YouTube channels with at least 100,000 subscribers, retrieved at the end of 2019, and investigate the URLs found in 137 million video descriptions to analyze traces of these strategies. We first situate our study within relevant literature around the creator economy, the role of platforms, and issues such as social capital building and economic precarity. We then outline our data and analytical approach, followed by a presentation of our findings. The article finishes with a discussion on how monetization and networking strategies via placing URLs in video descriptions have become more important over time, but also differ substantially between channel sizes, content categories, and geographic locations. Our empirical analysis shows that YouTube, as a highly unequal platformed media system, thrives on the economic pressures it exerts on its creators.

Introduction

While the web was initially designed as a convenient and easy-to-use way to help researchers share information, the last three decades have seen successive waves of “economization,” in the sense that economic activity has become a central driver for online participation. E-commerce has changed how goods are found and sold; streaming platforms for music, movies, and tv-series have transformed remuneration schemes in these industries; and various kinds of online services have become central parts of work processes. One of the online activities that have expanded most dramatically over the last decade has been addressed with terms like “creator” or “influencer” economy. These terms, which arose from the mid-2000s emergence of web 2.0, address the increasing economization or commercialization of user-generated content in the sense that “creators” or “influencers” collect revenue through a variety of monetization schemes. While the creator economy is notoriously hard to scope, one report (Shapiro & Aneja, 2019, p. 19) claimed that an “estimated 14.8 million Americans earned income by posting their creations on Instagram, WordPress, YouTube, Tumblr and five other platforms.”

Digital platforms have indeed played a central role in this story, to the point where scholars speak of a “platformization of cultural production” (Nieborg & Poell, 2018). Social media services, in particular, provide the communicative infrastructure, set a number of ground rules, and create direct pathways for monetization, for example, through sharing advertisement revenue or so-called “creator funds” that provide remuneration based on specific inclusion criteria. 1 YouTube has been one of the key players within the online creator economy. By sharing advertisement fees with video producers almost from the beginning, YouTube has evolved from being a hoster of amateur clips into a vast ecosystem of increasingly professionalized channels that are able to broadcast to large audiences and acquire significant revenue. While still open to the “ad hoc” productions of early days, many creators are now pursuing YouTube as a full-time job, with regular update schedules and polished production. This makes YouTube one of the pillars of what Cunningham and Craig (2017, 2019a) have called “social media entertainment,” an industry that successfully attracts young viewers in particular and allows certain creators to become stars who rival actors and musicians in popularity.

In analogy to Andrew Chadwick’s (2013) concept of a hybrid media system, “built upon interactions among older and newer media logics” (p. 4), we have previously (Rieder et al., 2020) conceptualized and explored YouTube as a platformed media system, that is, as an emergent ecosystem of channels that is sufficiently large to develop high levels of economic activity and internal heterogeneity, rivaling or surpassing the traditional media systems of nation states.This ecosystem is highly unequal—we found that the top 0.4% of channels account for 62% of views—and structured along dividing lines such as language, subject area, and so forth. While YouTube sets its boundaries and governs it in different ways, content creators pursue their own production and optimization strategies relatively freely within its confines, separating it from streaming services such as Netflix where control over content is much tighter. Crucially, these creators are, at least in part, able to build viable businesses on top of the functionalities and monetization possibilities made available to them.

Despite its internal richness, YouTube is not siloed off. On the one side, videos are shared as links or embedded directly, circulating through other platforms and the open web. On the other side, creators can link elsewhere from their videos, in particular via video descriptions, which allow for up to 5000 characters of text to accompany each clip. Next to promotions or placed advertisements in the videos themselves, these links represent an opportunity for creators to reduce their dependence on YouTube, both for generating income, for example, through affiliate programs or crowdfunding, and for building social capital across other social media accounts or websites. 2

In this article, we deepen our investigation of YouTube as a platformed media system, focusing specifically on monetization and networking strategies within the consolidating creator economy. More specifically, we build on a near-complete sample of 153,000 “elite” channels with at least 100,000 subscribers, retrieved at the end of 2019, and investigate the URLs found in 137 million video descriptions to analyze traces of these strategies. We are interested in understanding how creators seek to build their online presence across multiple platforms and widen their income streams. The article is structured as follows: We first discuss relevant literature around the creator economy, the role of platforms, and issues such as social capital building and economic precarity. We then outline our data and analytical approach. The third section summarizes and presents our findings. We show how monetization and networking strategies have become more important over time, but also differ substantially between channel sizes, content categories, and geographic locations. We conclude by arguing that YouTube, as a highly unequal platformed media system, thrives on the economic pressures it exerts on its creators.

The Creator Economy in a Platformed Media System

The Creator Economy

Digital platforms have become central organizing infrastructures in many different domains of public and private life, transforming these domains in often significant ways (van Dijck, 2020). Within cultural and media industries, sites coveting user-generated content have lowered barriers of entry for large numbers of “creators.” As Poell et al. (2022) have argued, advances in computing more generally and platform mediation more specifically have lowered the costs of production, distribution, and transaction. In the case of YouTube, users can shoot a video with a cheap smartphone camera, edit it on their device, upload it for free, potentially reach a large and diverse audience, and earn income without having to search and contract with advertisers directly. Already over a decade ago, authors like Kim (2012, p. 53) noted how “smooth links between content and commercials” on YouTube fuel tendencies toward institutionalization and professionalization. This transformation of cultural production, together with the observation that “the rich get richer” dynamics at work in networked systems lead to the emergence of steep hierarchies of visibility all over the web (Hindman, 2009), seriously dampened early enthusiasm about the “democratic” potential of social media.

While platforms like YouTube, Facebook, TikTok, Instagram, and Twitter have given marginalized voices access to expression and (sometimes) visibility, terms like “user-generated content” and “participatory culture” (Jenkins, 2006) have mostly been replaced by concepts like “creator economy” that locate the ecosystems that have sprung up around these sites within the larger sphere of the cultural industries (Hesmondhalgh, 2019). Burgess and Green (2009) put a name to the “entrepreneurial vlogger” in 2009 already, but the last decade has also seen the emergence of more formalized economic actors active on YouTube, including large channels run by entire teams, multi-channel networks that further facilitate commercialization (Lobato, 2016), and “legacy” media companies that expand into these newer platforms, for example, the music and news industries. The multiplication of terms used to address these developments—next to “creator economy,” we find “influencer marketing,” “creative labor,” “platform labor,” and others—signals the difficulty to demarcate a complex and layered phenomenon.

This complexity extends to the variety of available monetization instruments, which includes not only direct revenue from advertising, but also various kinds of affiliate marketing, product placement, paid sponsorships, appearance fees, and other sources of income that are hard to measure (Gerhards, 2019; Vrontis et al., 2021). Digital media scholars describe a new class of “influencers” that is able to attract significant amounts of money from advertisers, albeit often under difficult labor conditions. Creators invest time and energy not only in creating content but also in self-branding and networking across different platforms, often exposing their private lives to establish and maintain intimacy with audiences (Bishop, 2021), in the hope of gaining popularity and reputation, that is, of increasing their social capital. 3 As Gandini (2016, p. 124) argues, “social media has come to represent a working tool that serves the curation of a professional image and the management of social relationships for purposes of professional success and career progression.” But content creators’ quest to monetize their social capital happens under great uncertainty, due to a continuously changing landscape of platforms, terms of service, pay rates, competences, and intermediaries, making the creator economy more often than not part of a larger “gig economy” that faces considerable economic instability (Duffy, 2017; Scolere et al., 2018; Vallas & Schor, 2020). In the case of YouTube, bans, demonetization, and algorithmic invisibility are constant threats (Duffy et al., 2021; Glatt, 2022; Kumar, 2019), particularly for channels that deal with sensitive topics (Caplan & Gillespie, 2020). Creators thus often entertain ambiguous relationships with platforms that provide (economic) opportunities but may also hamper or destroy years of work in an instant (Scolere et al., 2018). Similar to fields like the arts or journalism, platforms profit from the “aspirational” character 4 of much of the labor performed by users: many creators are willing to accept precarious conditions as long as the promise of “making it” remains at least somewhat believable (Duffy, 2017; Hesmondhalgh & Baker, 2011; Kuehn & Corrigan, 2013).

The YouTube Economy and the Aspirational Curve

From an economic perspective, platforms like YouTube are multi-sided markets. As Rochet and Tirole (2006) argue, such markets enable interactions between different types of end-users and obtain revenue from this intermediation. On YouTube, we can identify three different “sides”—viewers, creators, and advertisers—and the ability to balance the interests of these groups is crucial for the platform’s success (Gillespie, 2010). Viewers constitute an audience that seeks free and unlimited access to a large variety of audiovisual content. These “eyeballs” then constitute the main interest for creators and advertisers to be on the platform. In that sense, YouTube follows a business model that is similar to traditional media, which consists of attracting large audiences that can be sold as a commodity to advertisers (Smythe, 1977). What distinguishes YouTube from traditional media, then, is the fact that the platform relies on content created and uploaded by another group of users.

YouTube seeks to attract and secure the loyalty of these content creators through different economic incentives. Most importantly, the YouTube Partner Program (YPP), launched in 2007 and counting over two million members according to the company (Lyons, 2021), shares 55% of the revenue generated by ads shown on monetized videos with their creators. The program has been central in transforming a platform hosting amateur videos into one where professionally generated content more aligned with the interests of advertisers takes an always greater place (Kim, 2012). Sharing revenue with creators has also distinguished YouTube from other social media platforms and has been crucial for the development of entrepreneurial careers (Burgess & Green, 2018) that form a proto-industry of social media entertainment (Cunningham & Craig, 2019a) and fuel a platformed media system (Rieder et al., 2020). The YPP challenges the characterization of platforms as exploiters of free labor (Fuchs, 2015) but also draws a line between “partners” and other creators (Kopf, 2020).

To qualify for the YPP, creators have to be at least 18 years old and “in good standing with YouTube.” They also need at least 1,000 subscribers and more than 4,000 watch hours in the last 12 months (YouTube, n.d.-e). Meeting this basic requirement gives access to ad revenue as long as creators adhere to the guidelines for “advertiser-friendly content” that prohibit the use of inappropriate language, depiction of violence, drug use, and other things not considered suitable for advertisers (YouTube, n.d.-b). Prior to March 2021, YouTube further distinguished channel “tiers” based on subscriber count—graphite (100), opal (1,000+), bronze (10,000+), silver (100,000+), gold (1,000,000+), diamond (10,000,000+), ruby (50,000,000+), and red diamond (100,000,000+)—giving creators access to additional perks and resources as they grow their audience, such as training opportunities and direct access to partner managers. This has since been simplified to an awards system that no longer directly associates benefits with subscriber numbers. 5

Over the years, the YPP has evolved to include different ad formats and now offers a variety of monetization features inside the platform: channel memberships are a means, similar to Patreon, for viewers to support individual channels directly; Merch shelves enable creators to showcase and sell branded merchandise; Super Chats and Super Stickers allow viewers to pay for having their chat messages highlighted during live streams. Revenues from the subscription service YouTube Premium are also shared, and in February 2023, YouTube finally introduced monetization for Shorts (Southern, 2022).

Important for the purpose of this article, the YPP also accepts that creators add “product placements, sponsorships and endorsements” (YouTube, n.d.-a) to their videos with appropriate disclosure. Product placement, for example, can take the form of links in video descriptions, verbal advertisement in videos, or “visual-only” promotions where a product is merely displayed (Schwemmer & Ziewiecki, 2018, p. 11). Although the inclusion of affiliated links in video descriptions, which allows creators to obtain a commission for transactions made after viewers click on the link, is common on YouTube (Mathur et al., 2018; Ørmen & Gregersen, 2022; Schwemmer & Ziewiecki, 2018), the YPP does not explicitly recognize the practice as an official revenue stream available to creators. Affiliate links are only mentioned in YouTube’s external links policy (YouTube, n.d.-d), which states that they are allowed as long as they do not violate spam guidelines.

Despite the multiplication of monetization possibilities within YouTube, income from advertising remains the central source of revenue for the platform, growing from 8.1 billion in 2018 to 28.8 billion in 2021. To protect its business model, YouTube has had to adjust numerous times to external controversies that have challenged its economic interests. In the first years, music copyright violations were a major problem, leading the company to introduce the Content ID system to appease music companies (Burgess & Green, 2018). More recently, the need to provide a “safe” environment for advertisers has prompted it to take a more active role in content curation. This shift occurred in lockstep with moments of crisis, most clearly in 2018 when advertisers withdrew from YouTube after discovering that their ads were running on videos promoting terrorism and hate speech, what later became known as the first “adpocalypse” (Caplan & Gillespie, 2020; Kumar, 2019). YouTube’s ad policies have since continued to become stricter, the most significant move being the outright “demonetization” of certain kinds of content such as “low-quality” 6 videos, which has had major consequences for some creators (Caplan & Gillespie, 2020). These broader changes in monetization practices and, in particular, the demonetization of individual YouTube channels further illustrate the uneven power relations between the platform and creators who have limited possibilities for demanding redress and, more broadly, lack any formal recognition as stakeholders in the evolution of the platform (Cunningham & Craig, 2019b).

While YouTube’s changes to monetization policies and often erratic reaction to specific events have certainly played an important role in creators’ search for what has been called “alternative monetization strategies” (Hua et al., 2022), at least in certain sectors of the ecosystem, there are other factors to take into account. Early studies already indicated that popular content creators on YouTube have always deployed a wide array of strategies to find success (Morreale, 2014). But more fundamentally, a system animated by low barriers of entry, high aspirational attractivity, performance-based pay, and hierarchization through cumulative advantage (Hindman, 2009) is bound to produce a long-tailed income distribution where the vast majority of participants will not be able to find economic success. To illustrate this principle, we use data from our previous analysis of a large-scale sample of over 36 million YouTube channels (Rieder et al., 2020), to estimate average advertising income for channels, divided into tiers based on subscriber numbers (Table 1).

Estimation of Ad Revenue Per Subscriber Tier, Based on the Distribution of Views Reported in Rieder et al. (2020) and Google’s Disclosure of Ad Revenue of $15 Billion for 2019, of Which $8,25 Billion Were Distributed to Channels.

While this calculation has a number of limitations, 7 it provides an order of magnitude for channel income across YouTube. Taking the highly uneven distribution of views as a stand-in for revenue, we see that only a small fraction of channels can expect to earn a living wage from advertising income. The vast majority of creators are stuck on the lower rungs of what we call the “aspirational curve,” that is, the emergent distribution of success in a market where large numbers of participants are willing to perform “hope labor,” a “future-oriented investment” (Kuehn & Corrigan, 2013, p. 10) that is likely to never pan out. Our numbers indeed show a steep income pyramid where the lower tiers are basically working for free. Given their relatively low contribution to overall view numbers—the 153,000 channels on the top account for 62% of all views—it could be argued that these smaller channels are simply irrelevant to YouTube. But they play an important role as an “innovation department” that invests time, assumes risk, gains experience, and creates fresh content to attract viewers. They are a standing reserve of content and labor, and the “natural” replacement when channels from the top cease their activity or move to other platforms. Crucially, they put pressure on the whole system, forcing even top creators to keep uploading if they want to remain successful. In such a setting, there are strong incentives to develop alternative monetization pathways, even without any threat of demonetization. In the following section, we explain how we investigate these pathways in more detail.

Studying Monetization and Optimization Practices on YouTube at Scale

Previous Work on URLs as Indicators for Monetization Practices

Several studies have used links in video descriptions to study monetization practices on YouTube, differing in terms of subject focus, data sampling, and analytical methodology. A study of 139,475 videos posted by the top 100 German channels (Schwemmer & Ziewiecki, 2018) manually coded domains “related to product promotion” from the 50 most common domains in the data set, which accounted for 83.32% of all links in the sample. The authors found that there were on average more than two such links in the sampled videos, and they were particularly concerned with the increasing difficulty for users to distinguish between commercial and non-commercial content. Another study (Mathur et al., 2018) working with 515,999 videos selected through prefix sampling—a method for creating random video identifiers—followed a similar research interest, focusing on (the lack of) mandatory disclosures when using affiliate links. The researchers applied frequency analysis to discover linking patterns associated with affiliate marketing and compiled a list of “57 unique affiliate URL patterns from 33 different affiliate marketing companies” (Mathur et al., 2018, p. 9) that were then used to parse collected links to detect monetization and disclosures. Based on their research, the authors estimated that more than 7% of YouTube videos contain affiliate links. Closest to our own research interest and methodology, a recent study by Hua et al. (2022) relied on the YouNiverse data set which “covers around 25% of the top 100k most popular YouTube channels and around 35% of the top 10k most popular” (p. 6) to investigate “alternative monetization strategies.” Using a combination of manual coding and automated analysis, they classified all of the URLs in the sample, including crypto addresses for donations, but were limited to English-language content. They found that 61% of the channels in their sample included links to external monetization sites in their videos at least once, which led them to conclude that “alternative” monetization practices via linking URLs are “extremely prevalent among popular channels on the platform” (p. 22).

Our study differs from these efforts in a number of ways, particularly in terms of subject focus, where we inquire not only into monetization in a strict sense, but also into the broader process of professionalization, which includes building social capital beyond YouTube. Using a near-complete data set, we also provide the first overall picture of monetization and networking practices by “elite” channels on YouTube at scale and over time, and inquire how these practices differ between channel size, thematic focus, and geographic location. In the following two sections, we outline our methodology.

Data and Initial Overview

This article is based on a large-scale sample of over 36 million channels that was gathered at the end of 2019. A detailed description of the data collection method can be found in Rieder et al. (2020). In short, we used a crawling strategy that followed featured channel and subscription links. For this study, we zoom in on the 153,770 channels 8 with at least 100,000 subscribers, for which we were able to retrieve the (almost) 9 full video lists and collected metadata for 136,909,228 videos published between 1 January 2007 and 1 December 2019. While our crawling method has its own limitations and caveats, we are confident that our sample contains virtually all channels in the Silver tier and above (see Table 1). Compared with the studies by Schwemmer and Ziewiecki (2018) and Hua et al. (2022), we are thus not limited to German- or English-language content. At the same time, in contrast to the prefix sampling method used by Mathur et al. (2018), our sample is not representative of the overall video population on YouTube but focuses on those channels that have already been successful in accumulating a substantial number of subscribers. While a sample that includes videos from channels with fewer describers has its own merits, it would include many videos that were never uploaded with the intention of reaching a large audience or engaging in forms of monetization.

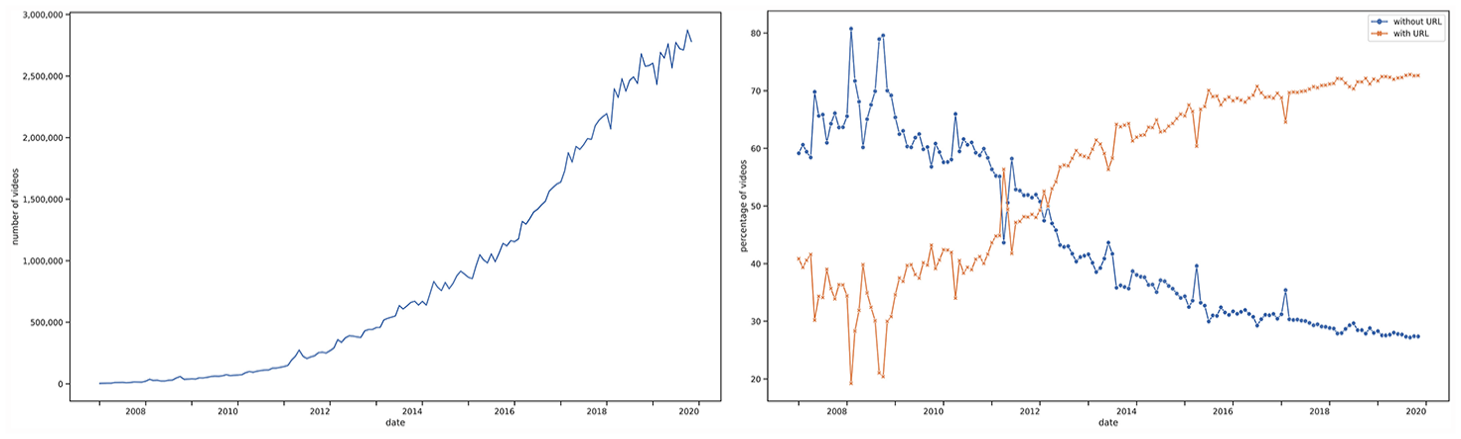

To analyze linking practices, we extracted all correctly formatted URLs from roughly 137 million videos, yielding 570,996,385 individual links from the 93,186,712 video descriptions that actually contained links (68%). Since many of the resulting URLs were using a shortening service like Bitly, we followed all links to their end point, finding that 0.82% could not be resolved and 3.66% failed to return a valid response, similar to what Mathur et al. (2018) reported. In our analysis, we did not limit ourselves to only recent videos, for several reasons. First, since the volume of videos has grown significantly over time, there is already a heavy skew toward the present. The videos published from January 2017 to November 2019, for example, amount to 59.8% of our sample (compare with Figure 1). Second, older videos may still attract viewers. This also points to a limitation affecting analyses over time, namely that video descriptions may have been edited after a video was published, a common practice, especially for channels that are able to attract viewers to their older videos and want to monetize them.

Monthly change of video volume and percentage of videos with and without URLs.

With these caveats in mind, Figure 1 shows how linking practices in our sample have evolved over time. While the majority of older videos do not contain links, this trend reversed in 2012 and has since stabilized at around 75% of videos containing at least one link.

Coding Monetization and Networking Via Domain Names

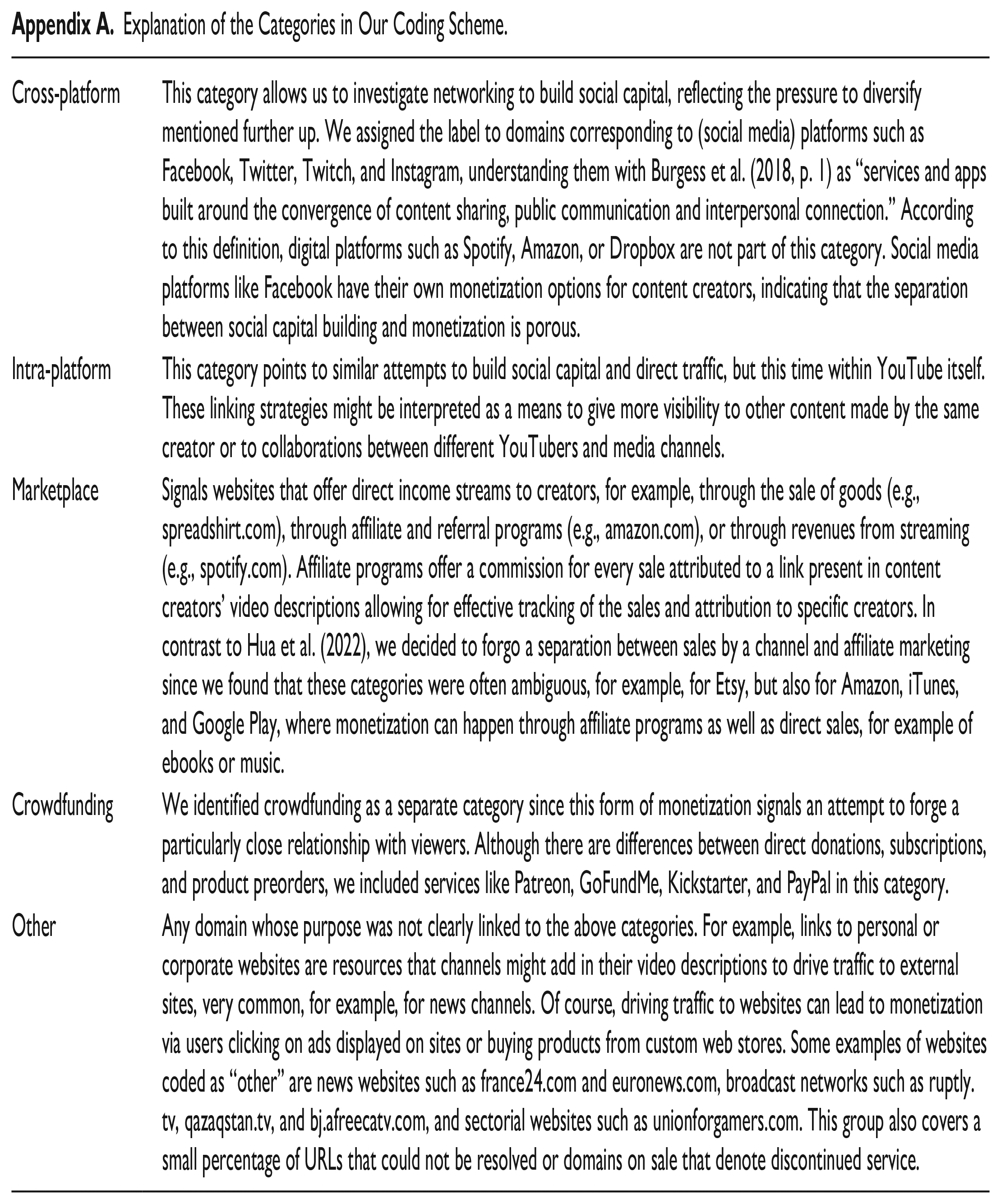

In an effort to get a more detailed account of monetization and networking strategies on YouTube, we manually coded the top 1,000 domains present in the video descriptions of our sample of 571 million URLs. 10 Together, these 1,000 domains cover 86.42% of all links. The distribution has a very long tail with 865,488 unique domains overall, showing considerable diversity when it comes to connecting with the web. In an iterative grounded coding approach, three coders independently classified the list of domains. Following the first iteration, the coders agreed on five categories. In line with our broader research interest, our classification considered “value generation mechanisms” in less granular fashion than other studies, distinguishing between cross-platform (links to other social media platforms), intra-platform (links to YouTube content and channels), marketplace (links to websites that offer direct income streams to creators), crowdfunding (links to services like Patreon, GoFundMe, Kickstarter, and PayPal), and other domains. Since a website or platform may offer more than one revenue stream to creators, we assigned more than one label to certain domains instead of resorting to fully exclusive categories. We remained on the level of the domain and did not include specific URL patterns in our classification. We also cross-referenced our list with both Mathur et al. (2018) and Hua et al. (2022). In a second iteration, all coders assigned the above codes to domain names independently once more. After this second iteration, the coders discussed their differences and came to an agreement. Appendix A explains our categories in more detail.

Findings

Basic Findings

Looking at the full sample of videos, we found that 68% of video descriptions contain at least one link and, respectively, 44.2% for intra-platform, 49% for cross-platform, 13.4% for marketplace, and 2.55% for crowdfunding links. If we consider marketplace and crowdfunding together as “alternative” monetization links, we find that 14.79% of YouTube videos make use of at least one of these revenue sources. This is higher than the 7% in Mathur et al.’s (2018) random sample, which can be explained by our inclusion of music streaming sites and stronger skew toward popular channels, but it is lower than the 18% found in the English-language sample in Hua et al. (2022). Figure 2 adds detail by tracking the evolution of linking practices over time. Intra-platform and cross-platform links grew at a fast pace, slowing down somewhat around 2016. Monetization through marketplace links also stabilized around that time at around 16%–17% of all videos. Crowdfunding comes in at a much lower level and stabilization occurs a little later, around 2018. Interestingly, links that are part of our “other” category or not classified are steadily going down. One possible explanation of this finding might be that having one’s own domain in video descriptions is becoming less important in a moment of “platformization” (Helmond, 2015) where a few proprietary platforms increasingly dominate the internet.

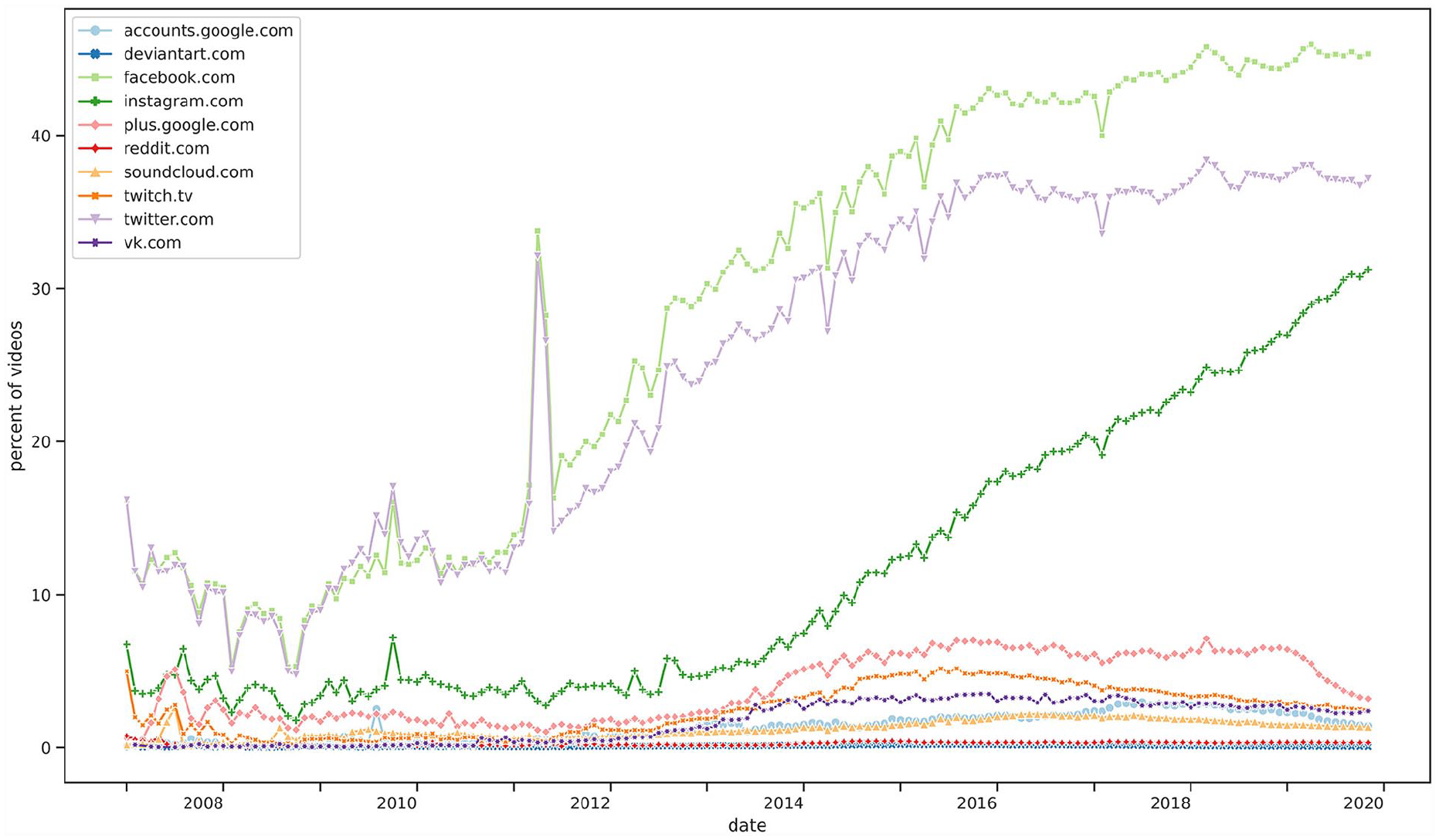

Evolution of URL categories over time.

When looking at the most linked domain names (Table 2), we instantly recognize the familiar pattern that a small number of heavily linked sites dominate. YouTube itself accounts for over a third of all links and, on further investigation, we discovered that 59% are links to channels, 20% to playlists, 18% to videos, and 3% could not be parsed. This shows how creators seek to direct viewers to their own channels and videos, but also to other creators.

The Top 20 Most Linked Domains.

Facebook, Twitter, and Instagram are the pillars of cross-platform linking (Figure 3), with over half of the channels under observation linking to each of these platforms at least once. This shows how these services have become central to the quest for gaining visibility, accumulating social capital, and constructing “a platform-independent brand with the freedom to leave YouTube if conditions become unsatisfactory” (Ørmen & Gregersen, 2022, p. 15). The now defunct Google+ already comes in at much lower numbers and continues to lose ground; more topic- or country-specific services like Twitch, VK, Pinterest, and Discord—although important in specific content categories like Gaming or Howto&Style—are nowhere near as popular as these “general-purpose” social platforms.

The 10 top cross-platform domains over time.

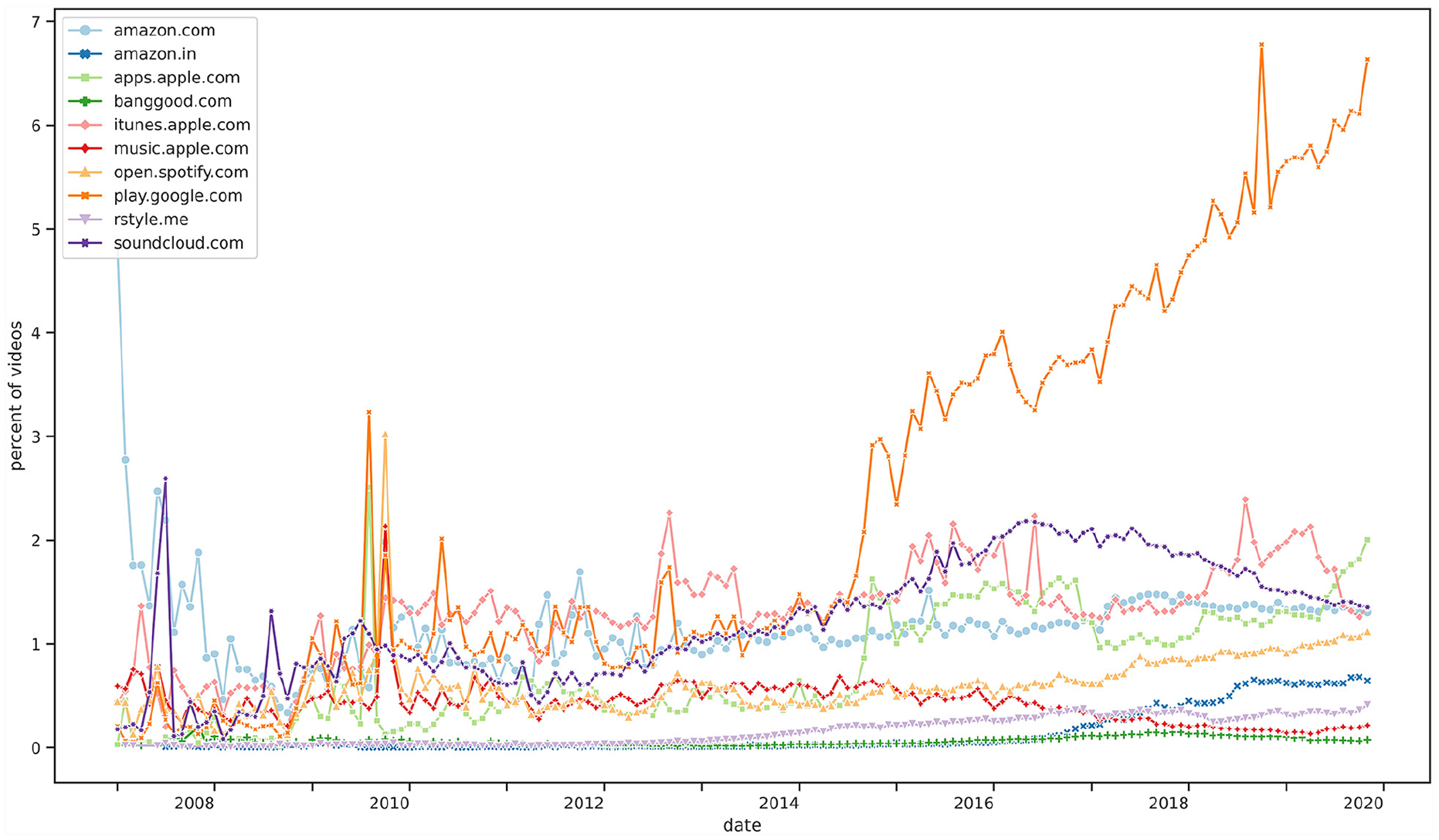

When it comes to our broad marketplace category (Figure 4), Google Play and the different Apple stores are the most common domains. Many of the links in our sample point toward download pages for apps, for example, Zee5, a popular Indian video on demand service. Music services like SoundCloud, iTunes, and Spotify indicate another pathway to direct monetization as these services provide income through sales or streaming. The videos linking to these services generally have a higher view count as music videos are often watched more than once. The various Amazon country domains clearly dominate the affiliate sales monetization space. What we notice, here, is that these links often appear in clusters (the average number of links in a video that has at least one link to amazon.com is 3.48), possibly the result of creators linking to their video equipment in every video they make and similar practices.

The 10 top marketplace domains over time.

In the crowdfunding category (Figure 5), Patreon and PayPal are most prominent, and other sites such as GoFundMe, Kickstarter, and Tipeee also appear within the top 10 ranking. DonationAlerts/DonatePay (subsidiaries of VK) and APOIA.se specialize in two particularly active YouTube countries: 27% of all 5,061 Russian channels in our sample link to the former at least once, and 6% of the 9,907 Brazilian channels to the latter.

The 10 top crowdfunding domains over time.

Overall, we notice the importance of cross-platform linking, which confirms the hypothesis that creators are investing heavily in social capital and brand building. Marketplace and crowdfunding URLs are found much less frequently, despite the fact that each has dominant actors that reach across content categories and geographies, accompanied by websites that specialize in specific content categories or geographies, indicating a “tiered” system of linking.

Investigating Channels

YouTube channels remain the most pertinent unit of analysis when it comes to studying monetization and networking practices because they structure production and output on YouTube. One of the characteristics of YouTube as a platformed media system is channel diversity (Ørmen & Gregersen, 2022; Rieder et al., 2020). This means that, while we could calculate values for domains found in an “average” channel, it would hardly represent the important differences between large and small channels in terms of subscriber or viewer numbers, between channels active in different content categories, and between channels based in different locales.

When looking at the distribution of linking activities over our channel collection (Figure 6), two extremes come into view. The peaks at both ends of the histogram indicate that there are channels that pay scrupulous attention to placing links in a large majority of their videos—87,455 channels (56.9%) have links in at least 80% of their videos—while another group invests little in linking (29,665 channels, 19.3%, have links in less than 20% of their videos). Indeed, 10,460 channels (6.8%) in our sample have videos listed, but without even a single link in any of them. These channels generally have lower subscriber, video, and channel view counts, but an almost three times higher average view count per video. Looking at these channels’ self-chosen country flags, Asia (India, Indonesia, Thailand), Latin America (Brazil, Mexico), and the Middle East (Egypt, Turkey) are overrepresented compared with the channels that do link, but almost half (43.5%) have no country selected, indicating lower attention to metadata optimization than the linkers, where only 21.5% miss that information. In terms of content, these channels often feature music videos and content targeting kids, which explains the high per video view numbers, as well as TV shows and movie-related content. Three observations can explain the lack of linking here. First, large parts of this content may be bootlegged and shared without the intention to create a professional YouTube presence or brand. Second, the infrastructure for alternative monetization in many non-Western countries remains limited, making linking less relevant. For example, we could not find specialized crowdfunding sites for India, 11 while we did for Russia (DonationAlerts) and Brazil (APOIA.se). Third, countries like India are generally “mobile first” 12 and linking into the open web may simply be less important. While this may seem counterintuitive, we also found that channels with a denser posting schedule link and monetize slightly less. This may be an effect of high-volume channels such as news stations that often post many videos per day with relatively little invested in YouTube/internet-native practices. Video duration does also not correlate with linking behavior.

Percentage of videos with links distributed across the channel population.

On the other extreme, we find channels that are heavily invested in networking within YouTube and beyond. Looking more deeply into the relationship between linking practices and other channel behaviors, we find, unsurprisingly, that channels that link a lot also promote or feature other channels in their YouTube profiles more (0.15 correlation). One explanation for this finding is that channels that want to succeed economically on YouTube will either have more than one channel or promote other channels to network and potentially gain visibility. Another set of insights into professionalization comes from indicators that connect with community building and audience interaction. Relying on metrics we developed in the context of our previous publication (Rieder et al., 2020)—intensity (the relationship between views and more “active” reactions such as liking, disliking, and commenting) and likeratio (the relationship between like and dislikes)—we find that channels with higher average intensity and a more positive likeratio tend to link more (0.109/0.104 correlation) overall and particularly to other platforms (0.188/0.158 correlation). These channels may be more explicit in asking for audience reactions (“leave a like”) or audience feedback (“let me know in the comments”), seeking to boost both algorithmic visibility and community parasociality. They also monetize more heavily, both with regard to marketplace and crowdfunding.

Channels that want to gain social capital on YouTube do so largely via intra- and cross-platform links, which account for the largest number of links overall. When it comes to the most obvious “alternative” sources of revenue (crowdfunding and marketplace), however, we find that most channels in our sample do not monetize heavily outside of YouTube, at least not through URLs. About 53,256 (34.6%) do not use marketplace links even once and 115,904 (75.37%) in fewer than 20% of their videos. Only 10,221 (6.6%) have such links in 80% or more of their videos. For crowdfunding, the numbers are even lower: 127,805 (83.1%) channels do not use crowdfunding links even once and 144,521 (94%) use them in fewer than 20% of their videos. Only 2,675 (1.74%) add crowdfunding links in 80% of their videos or more. These findings nuance previous claims around affiliate links and crowdfunding sites being common revenue sources for YouTubers wanting to professionalize (e.g., Cunningham & Craig, 2019a; Hua et al., 2022; Ørmen & Gregersen, 2022).

Subscriber Tiers

Considering the great differences in terms of subscriber and view numbers between channels, one question is how monetization and networking practices change between subscriber tiers. Following YouTube’s now defunct nomenclature, Table 3 shows the relative percentages of linking categories for silver (100k-1M), gold (1M-10M), and diamond (10M+) channels. We notice that crowdfunding, in particular, grows as we move down the hierarchy, with marketplace going into the opposite direction.

Channel Statistics Split by Subscriber Tier.

Table 3 shows that the tiers are progressively differentiated in terms of channel age (“days active”) as well as number of videos. Diamond channels are older, on average, and have posted almost six times as many videos as Silver channels. This connects to what Gregersen and Ørmen (2023) have called the “output imperative,” but also to geographic particularities: an important number of highly subscribed Asian channels, like T-Series or SET India, have published tens of thousands of music clips or television programming, following a different publication rhythm as “typical” Western channels. Diamond channels are less community-oriented, however: they rely less on crowdfunding and their videos solicit less intense reactions (see “average intensity” column in Table 3). In that sense, they resemble TV channels more than what one would imagine as “traditional” YouTube channels. Their high use of marketplace links again shows that the link between “alternative” forms of monetization and the waves of adpocalypse may be exaggerated. These channels are mostly safe from demonetization and simply seek to maximize revenue like other businesses in a capitalist economy.

Countries

As we have previously noted, monetization and networking practices are distributed unequally with respect to geographies. Using the creator-chosen country flags for channels as indicators, we can explore this distribution in more detail. As Figure 7 shows, URLs in video descriptions are most heavily present in Western countries with Japan, Russia, and Vietnam constituting notable exceptions. Latin America mostly sits in the middle, although we notice that limiting ourselves to countries with at least 100 channels excludes smaller countries on that continent as well as much of Africa. Linking practices to marketplace sites (Figure 8) show an even more accentuated pattern, with German and Austrian channels standing out as monetizing particularly heavily and the Global South showing much lower use overall.

Percentage of videos with links for countries with at least 100 channels in our sample.

Percentage of videos linking to marketplaces for countries with at least 100 channels in our sample.

Figure 9 indicates that Ireland, Australia, Canada, Austria, and the United Kingdom are the channel geographies most strongly relying on crowdfunding—all smaller countries that are part of a larger language sphere. Russia has comparatively high levels of crowdfunding (given that marketplace links are not very prominent), which can be explained by the availability of specialized sites like DonationAlerts, by the international sanctions in place since the invasion of Crimea in 2014 making monetization through advertisement more difficult, and by the country’s prominence in the Gaming content category, which is particularly active in that regard.

Percentage of videos linking to crowdfunding sites for countries with at least 100 channels in our sample.

Monetization and Networking Per Video Category

Video categories are another useful unit of analysis to investigate structural fault lines in YouTube’s platformed media system. Unlike channel categories, which are automatically attributed by YouTube, video categories such as Gaming and News&Politics are set by video creators for each of their videos. YouTube itself refers to these categories as “verticals” (Patel, 2021), indicating both their importance for organizing content and the substantial differences between them.

Figure 10 shows that cross-platform and intra-platform linking practices are important across content categories, which aligns with the general findings described in the previous sections. The “big three” (Facebook, Instagram, and Twitter) dominate across all content categories, indicating that these “general-purpose” platforms have become unavoidable promotion tools for YouTube content creators. A level below, however, we find more specific relations between content categories and social media domains. Twitch and Discord are strongly associated with gaming, and Pinterest is prominent across categories, but particularly present in Howto&Style and Pets&Animals.

Relationship between video categories and types of linking (number of videos in brackets).

When zooming into direct monetization tactics (linking practices to marketplace and crowdsourcing sites), we see significant differences between verticals. As we found previously (Rieder et al., 2020), Gaming is a particularly competitive category, where many channels are trying to “make it” and where the concept of “hope labor” (Kuehn & Corrigan, 2013) applies most clearly. The category has the highest percentage of links across all our classification categories, that is, intra- and cross-platforms as well as marketplace and crowd monetization links. This somewhat contradicts the findings by Schwemmer and Ziewiecki (2018) and Mathur et al. (2018), who found that Technology and Howto&Style had the most affiliate marketing. These two categories are among the highest in our data as well—for example, Asian gadget websites such as Gearbest and Banggood are prominent in Science&Technology—but significantly behind Gaming. We also find that Music links to marketplace domains at a high level, although this is certainly due to our choice to include streaming services.

When it comes to crowdfunding specifically, Gaming again stands out, in line with the community focus that also manifests in the highest intensity level (Rieder et al., 2020), which may also be connected to the high prevalence of live streams. But we also find relatively high levels of crowdfunding in Science&Technology, Comedy, and Pets&Animals. News&Politics and Sports are particularly low on both crowd and marketplace percentages suggesting that videos in these categories may come in large parts from “non-native” channels such as TV news, which have not yet fully invested in YouTube economics or may even be funded by public institutions.

Interestingly, Nonprofits&Activism channels show the highest use of links in our “other” category, indicating a certain resistance to platformization, although even here, we see a heavy drop-off over time (Appendix B).

Discussion and Conclusion

The first and most general observation we can make is that, at least for the elite channels that we have analyzed, linking from video descriptions is a very common practice that has steadily increased over the years. On average, there are 4.17 URLs in the almost 137 million videos in our sample. About one third of those links connect within the platform and two thirds point elsewhere. While we have described YouTube as a platformed media system that hosts a large and heterogeneous population of content creators, it is “porous” in the sense that incoming and outgoing connections abound, and a considerable part of social and economic activities “leak” elsewhere. Since native ads, as we have estimated in Table 1, only generate substantial revenue for a limited number of channels, there is pressure to look for other forms of income. The largest part of linking practices is, however, not directed toward direct monetization opportunities, but toward other social media platforms for the purpose of social capital accumulation, which may in turn drive back traffic and serve as a (limited) fallback in case of trouble with YouTube. Even channels with few or no traces of direct monetization (marketplace and crowdfunding) in their video descriptions make sure that links to other “socials” are in place, confirming Gandini’s (2016) hypothesis that content creators are investing heavily in social capital and brand building.

Concretely, this means that Facebook, Twitter, and Instagram form the first rung of a highly skewed linking hierarchy, with 42% of all external URLs pointing to one of these three. All other social media sites are far behind in terms of numbers, even if their presence can be considerable in certain topic areas (e.g., Twitch and Discord for Gaming) or geographies (VK for Russia). A similar hierarchy emerges with regard to specific forms of monetization: Amazon dominates affiliate programs, Patreon is by far the most common (external) crowdfunding service, and Apple and Spotify control the music market outside of YouTube itself. The fact that both Apple’s and Google’s online stores combine the sale of all kinds of products with affiliate programs complicates further differentiation concerning the precise economic activities their domains are indicators of.

The clear overall trend toward platformization is further confirmed by the steady reduction of sites we have classified as “other”: while they made up roughly 15%–20% of the overall linking volume until 2013, this has since declined to around 5%. This does not preclude that smaller actors can play important roles in certain niches or geographies, but the ongoing process of “ingestion” of online activity into a limited number of platforms and services complements the progressive rise of linking on YouTube.

While linking is overall popular, our analyses have identified two very different extremes when it comes to linking behavior, even within our sample of highly successful channels. While there are many channels that pay scrupulous attention to placing links in a large majority of their videos (48,6% of channels have links in at least 90% of their videos), a second group invests little or no effort in linking (15,6% have links in fewer than 10% of their videos). Overall, almost 32% of videos have no links at all. While this part of YouTube includes channels and videos from countries that have less developed alternative monetization infrastructures and “mobile first” habits that deemphasize linking, these findings also point to remnants of the “old” YouTube, where contents can be non-commercial, artistic, weird, or blatantly illegal, and still find a large audience. For example, the channel with the largest number of uploads in our sample, Webdriver Torso with over 600,000 videos listed, automatically generates videos with abstract shapes and beeps that YouTube apparently uses for performance testing and the occasional joke. Some of the non-linking channels thus fall into the “avoidance” category identified by Ørmen and Gregersen (2022), as they “actively avoid or passively ignore monetization on the platform” (p. 15) for various reasons, while others may in fact follow a “conformity” strategy that “relies solely on YouTube-native monetization options” (p. 13) and does not bother to connect directly to other websites. In the absence of easy techniques to detect whether a video is monetized on YouTube or not, it is hard to distinguish these categories automatically.

The same limitation applies to attempts to distinguish channels that monetize solely off-platform from those that profit from YouTube-native income streams as well. Overall, monetization through linking remains relatively rare in our sample of popular channels. About 75.37% of channels have marketplace links in fewer than 20% of their videos and only 6.6% in 80% or more. For crowdfunding, the numbers are even lower with 94% in fewer than 20% of videos and 1.74% in 80% or more. This does not include paid product placements or other forms of “non-linked” income, but it does show that this rather accessible pillar of monetization—both affiliate programs and crowdfunding platforms are relatively low effort—is not as common as often hypothesized. We also do not see an uptick in the prevalence of such links during the various “adpocalypses” that started in 2018 (Caplan & Gillespie, 2020). If anything, their growth starts to slow down around 2016.

One of the reasons for this cognitive mismatch is that YouTube is a much larger and much less Western-dominated platform than the English-language literature, which often focuses on political issues pertaining to Western countries, leads us to expect. Since our sample is internationally diverse and topically agnostic, a more comprehensive picture emerges. One of the key findings of our project, which already became visible during our initial exploration of the same data set (Rieder et al., 2020), are the important differences between geographies when it comes to monetization and networking practices. The creator economy in countries like India, the biggest video producer in our sample, looks substantially different from what we see in the Western world. There, we find very large channels producing very large numbers of music videos, tv shows, and even full-length feature films without investing as heavily in linking or “alternative” forms of monetization. The mobile phone as the primary consumption device may be one explanatory factor, the lack of easy access to a monetization infrastructure another, but there may also be less “demonetization pressure” to contend with. As the Francis Haugen (Rev, 2021) hearings revealed, platforms—in this case Facebook, but there is little reason to believe that the situation with YouTube would be substantially different—invest much more heavily in Western language spheres when it comes to content moderation, and this may spill over into areas like demonetization. Countries like Brazil (APOIA.se), Russia (DonationAlerts), and others are nevertheless big enough to support a nascent infrastructure of companies that provide possibilities for alternative monetization adapted to local circumstances. This is not simply a story of the West vs. the rest, but national and language spheres developing at different speeds and in different directions within the larger fold of a platformed media system. Exploring these particularities is one of several directions for further research that comes out of our work. Suffice to say, we should be careful when transposing experiences from Western countries to the other parts of the world: YouTube, seen as a platformed media system, is “localized” in many different ways. That said, US platforms globally dominate the social media services YouTube creators link to.

The sheer size of YouTube also means that the channels putting marketplace or crowdfunding links into at least 80% of their videos still amount to 10,221 and 2,675 channels, respectively, a sizable number given our sample of 153,770 channels. And there are another 4.26 million channels in our sample that have between 1,000 and 100,000 subscribers, which we have not analyzed. While these channels would have a hard time earning a living wage outside of particularly profitable niches, they add substantially to the overall economy on the platform. We have indeed found that marketplace linking diminishes as we go down the subscriber rungs, whereas crowdfunding increases. With this and the finding that channels that often link to crowdfunding sites are geared toward community building, we can argue that smaller channels are emphasizing monetization schemes that reward closer relationships with viewers (crowdfunding), whereas larger channels emphasize monetization schemes that benefit from scale. This also shows that there is no upper bound to income aspirations: very large channels that are highly unlikely to be demonetized are the heaviest users of affiliate links.

We also found considerable differences between topic areas or “verticals.” Gaming, as so often, stands out as the domain where all types of links are used the most heavily, with Howto&Style, Music, and Science&Technology overrepresented for marketplace links. With the exception of Music, where links to streaming services dominate, these categories are the classic “vlogger” domains, where we find “let’s play” videos, technology reviews, beauty tips, and similar YouTube-native content. These are the areas where the pressure from the aspirational character of the work is particularly high: as we previously found (Rieder et al., 2020), Gaming channels are trying the hardest to “make it” and the heavy use of monetization links further confirms this finding.

This leads us back to an argument we started to develop with our rough estimate of average channel income. Given the lack of visibility of the “adpocalypse” in our data, we argue that demonetization may add to the pressure to diversify income streams, but the aspirational curve itself—the fact that there are thousands or millions of creators hoping to develop their channels into viable businesses—is already turning the platform into a pressure cooker for creators. To boil the story down to its most bare-bones expression: there is an abundant supply of people hoping to turn playing video games into a career. This does not mean that the often capricious governance of YouTube is irrelevant, but that the organization of the platform as a porous market recreates the competition and uncertainty dynamics we know all too well from other artistic/media sectors. The precarity we find on YouTube is thus not simply due to being “platformed” but also to being a “media system.” What platformization changes, here, is that the barriers of entry are even lower and some level of income is generated relatively early, furthering creators’ hope that this could become a profession somewhere down the line. Much like in other media industries, the aspirational labor creators perform on YouTube is constantly fueled by new entrants seeking to make it on the platform. YouTube has the same lack of labor rights as Uber or Deliveroo, but young people are dreaming of becoming influencers, not delivery drivers, and this means that they are willing, at least for some time, to work for less than little.

YouTube has no incentives to change this, on the contrary. While the top channels are providing the bulk of views and advertising income, the (still) fundamental openness of the platform—which we can see in the considerable heterogeneity in our findings—means that the company can delegate innovation and the risks that come with it to its creators. This extends to monetization. While advertising and paid promotions in videos are governed by a number of explicit rules, linking is largely unregulated, which may actually be a perk from YouTube’s perspective: instead of prohibiting links that move economic activity off-site, the company is able to see what “works” and can replicate these features within its own interface. Channel subscriptions and various forms of tipping emulate Patreon and PayPal, merch shelves and shopping features move certain kinds of sales in-house, and so forth. And even value that is not captured in this way is useful to the company as it sustains the creation of even more content. Instead of trying to emulate Netflix and other streaming services by pouring money into original content, a strategy YouTube tried out and abandoned, the aspirational curve wins the battle for efficiency as creators struggle for success. The role of ranking and recommendation systems in this context is not only to help users find content that they “like,” but to sharpen the contrast between winners and losers. The result is not a singular dominant mainstream, but a form of managed heterogeneity that allows for both variety and popularity to coexist.

While linking allows us to study one of the three pillars of monetization, YouTube-native income streams and non-linked alternative monetization such as product placements remain hard if not impossible to study at scale. Future work could combine large-scale approaches as ours as a basis for sampling to apply manual or automatic modes of content analysis or ad detection. As YouTube grows at a steady pace, we need to understand the platformed media system it instantiates much better to further scrutinize its role as the truly globalized content behemoth it has become.

Footnotes

Appendix

Explanation of the Categories in Our Coding Scheme.

| Cross-platform | This category allows us to investigate networking to build social capital, reflecting the pressure to diversify mentioned further up. We assigned the label to domains corresponding to (social media) platforms such as Facebook, Twitter, Twitch, and Instagram, understanding them with Burgess et al. (2018, p. 1) as “services and apps built around the convergence of content sharing, public communication and interpersonal connection.” According to this definition, digital platforms such as Spotify, Amazon, or Dropbox are not part of this category. Social media platforms like Facebook have their own monetization options for content creators, indicating that the separation between social capital building and monetization is porous. |

| Intra-platform | This category points to similar attempts to build social capital and direct traffic, but this time within YouTube itself. These linking strategies might be interpreted as a means to give more visibility to other content made by the same creator or to collaborations between different YouTubers and media channels. |

| Marketplace | Signals websites that offer direct income streams to creators, for example, through the sale of goods (e.g., spreadshirt.com), through affiliate and referral programs (e.g., amazon.com), or through revenues from streaming (e.g., spotify.com). Affiliate programs offer a commission for every sale attributed to a link present in content creators’ video descriptions allowing for effective tracking of the sales and attribution to specific creators. In contrast to Hua et al. (2022), we decided to forgo a separation between sales by a channel and affiliate marketing since we found that these categories were often ambiguous, for example, for Etsy, but also for Amazon, iTunes, and Google Play, where monetization can happen through affiliate programs as well as direct sales, for example of ebooks or music. |

| Crowdfunding | We identified crowdfunding as a separate category since this form of monetization signals an attempt to forge a particularly close relationship with viewers. Although there are differences between direct donations, subscriptions, and product preorders, we included services like Patreon, GoFundMe, Kickstarter, and PayPal in this category. |

| Other | Any domain whose purpose was not clearly linked to the above categories. For example, links to personal or corporate websites are resources that channels might add in their video descriptions to drive traffic to external sites, very common, for example, for news channels. Of course, driving traffic to websites can lead to monetization via users clicking on ads displayed on sites or buying products from custom web stores. Some examples of websites coded as “other” are news websites such as france24.com and euronews.com, broadcast networks such as ruptly.tv, qazaqstan.tv, and bj.afreecatv.com, and sectorial websites such as unionforgamers.com. This group also covers a small percentage of URLs that could not be resolved or domains on sale that denote discontinued service. |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work has been supported by the Platform Digitale Infrastructuur Social Science and Humanities (PDI-SSH).