Abstract

Objective

Given an increasingly aging global population, physical health challenges faced by elderly individuals have become a critical societal issue. This study investigates the influence of digital finance on the physical health of seniors and its underlying mechanisms to explore an effective technology-facilitated pathway for enhancing well-being in later life.

Methods

Using data from the China Health and Retirement Longitudinal Study, the digital finance index developed, and a two-way fixed-effects model, this study assessed the role of digital finance in shaping the physical health of older adults.

Results

We find that the development of digital finance has significantly promoted the physical health of older adults mainly by increasing income, promoting healthcare accessibility and social participation. The relaxation of liquidity constraints is not the main reason for this improvement. Heterogeneity analysis reveals that welfare improvement exhibits no noticeable differences based on their residence and education level or the region's traditional financial scale; these trends are more pronounced in the western region. In addition, innovative financial products such as digital insurance, mobile payments, and monetary funds facilitate the promotion of elderly physical health.

Conclusions

The study provides evidence of the practical value of digital finance in enhancing the physical health of the elderly. It also recommends the adoption of elderly-friendly designs and complementary social services through which digital financial tools can contribute more effectively to promoting efficient health outcomes.

Introduction

The aging population is a significant challenge faced by countries worldwide.1,2 China stepped into the aging society in 2000, and now experiences both a substantial elderly population and a fast pace of aging.3,4 According to the National Bureau of Statistics, the population aged 60 and above in China reached 297 million by the end of 2023, accounting for 21.1% of the total, while the population aged 65 and above was 216 million, or 15.4%, proving that China has matured into an aged society. 5 Given that China's declining birthrate and increasing life expectancy are set to exacerbate population aging in the next few decades, 6 the elderly physical health of older adults has emerged as a pressing societal issue. 7 As reported by the National Health Commission of China, by the end of 2023, more than 75% of individuals aged 60 and above had at least one chronic condition, with 43% suffering from multimorbidity. The long-term chronic diseases and disabilities of the elderly will not only severely undermine their quality of life but also impose significant strain on social governance and welfare. 8 Only by effectively tackling the physical health challenges faced by older adults, can China potentially reap the gains from the extended life expectancy and alleviate the latent burden on the economy and society. 9

Existing studies on elderly physical health show the profound impact, in addition to direct factors such as exercise,10,11 diets,12,13 healthcare utilization,14,15 of IT.16–18 While internet use is found to effectively promote the physical health of elderly individuals,19–21 a significant gap exists in the literature regarding the impact of other IT on their physical health, let alone the role of digital finance. Considering the mounting physical health crisis among older adults, innovative strategies are urgently needed to effectively address the evolving health demands.

Quintessentially an ideal form of inclusive finance, digital finance effectively lowers financial barriers, and can provide the elderly with more efficient and convenient financial services. 22 Research has demonstrated the role of digital finance in improving the subjective well-being of older people23,24; so, it is anticipated that digital finance could contribute to improved physical health outcomes. However, this relationship remains underexplored and lacks empirical support. This study posits that investigating the nuanced mechanisms through which digital finance influences elderly physical health can provide advanced solutions to achieving healthy aging. Additionally, it offers theoretical insights to the advancement of digital finance and public health policies.

Utilizing data from the China Health and Retirement Longitudinal Study (CHARLS) and the digital finance index developed by Peking University, 25 this study investigates the impact of digital finance on the physical health of the elderly. China was selected as the focus country for several reasons. First, compared with other countries, China is confronting an acute aging challenge, with older adults bearing a high burden of physical health issues.26,27 Second, China is at the forefront of digital finance worldwide, with widespread adoption among the elderly population. According to the 54th Statistical Report on Internet Development in China, the usage rate of mobile payments among the elderly reached 75.4% by mid-2024, highlighting the growing integration of digital finance into their daily lives. 28 This extensive adoption provides a solid data foundation for analyzing its impact on the physical health. Numerous financial institutions and platforms are promoting elderly-oriented innovations, such as designing exclusive apps or new versions to meet the demands of the elderly, further magnifying the positive effects of digital finance on their physical health.

The empirical results of our analysis using a two-way fixed effects model as the baseline, suggest that the advancement of digital finance has significantly promoted the physical health of older adults—the results remain robust even after a series of tests. This positive effect showed no significant differences among older adults in different residences and with varying educational backgrounds, or regions with different financial scales, but is notably stronger in the western region. An analysis of the mechanisms reveals that digital finance improves older adults’ physical health mainly by increasing income and promoting healthcare accessibility and social participation, while alleviating liquidity constraints is not the main reason. Digital financial products, such as digital insurance, mobile payments, and monetary funds, are also conducive to improving the physical health of the elderly individuals.

This study offers new insights into the literature in three ways. First, it investigates the influence of digital finance on the elderly at the micro level, offering a refined perspective that deepens our understanding of digital finance and its implications. Extant research shows the effects of digital finance on various outcome variables at the municipal or enterprise levels, such as urban carbon emissions29,30 and corporate green innovation.31,32 Some studies using micro-level individual data have largely focused on the effects of digital finance on consumption,33,34 but often center on households as the primary unit of analysis, neglecting the unique characteristics and needs of the elderly who are vulnerable in the digital age. The present study not only enriches the theoretical framework surrounding digital finance, but also underscores its inclusive benefits for the elderly beyond economic dimensions.

Second, this study extends the mechanism of welfare improvements in digital finance to the physical health of the elderly. A recent study highlighted the beneficial influence of digital finance on elderly individuals’ self-rated health, 35 but offers a limited analysis of the mechanisms underpinning this relationship. The present study explores the possible pathways through which digital finance can affect older adults’ physical health, such as income and liquidity constraints, healthcare accessibility, and social participation, and analyzes the role of specific digital financial products in this context. The comprehensive analysis illuminates the ways in which financial access and flexibility can alleviate the health risks associated with aging. Moreover, by focusing on specific digital financial products, it facilitates more targeted interventions to enhance the capacity of digital financing to enhance elderly physical health.

Third, this study innovatively incorporates digital finance into the elderly health research lens, adding novel insights to the discourse on older adults’ well-being and social policies. Extant research has predominantly focused on the factors directly influencing elderly physical health, such as daily lifestyle36,37 and healthcare utilization.38,39 Our contribution lies in emphasizing the significant potential of digital finance in advancing the physical health of older adults, offering a transformative perspective on promoting health through technology-driven solutions. The multidimensional variables used to measure elderly physical health status allow for a more thorough assessment of how digital finance influences health outcomes. The findings also provide valuable policy implications for leveraging the latest IT to enhance older adults’ well-being and social inclusion.

Theoretical analysis

Health demand theory conceptualizes physical health as a durable capital stock that individuals produce and maintain through investment behaviors. 40 With advancing age, the rate of depreciation of health capital accelerates, heightening the need for sustained and strategic health investments to mitigate functional decline and safeguard overall well-being. By offering accessible, efficient, and inclusive financial services, digital finance can facilitate investments in health capital among older adults. Specifically, by lowering transaction costs, improving payment convenience, and enhancing the efficiency of resource allocation, the elderly can make timely health-related expenditures, access healthcare services more easily, and better manage the financial risks associated with illness. These advantages jointly contribute to the accumulation and maintenance of health capital, promoting improved physical health outcomes later in life. Studies grounded in health demand theory have demonstrated that digital technologies can effectively enhance individuals’ health capital and health status.41,42

This theory underscores that an individual's physical health status is determined by their capacity as well as incentives to invest in health capital, which are shaped by economic resources, the accessibility and price of healthcare services. 40 Bolin et al. 43 further pointed out that social participation is also a crucial determinant of health capital. Based on this, we construct a theoretical framework to analyze how digital finance influences the physical health of older adults, which comprises five mechanisms such as income, liquidity constraints, digital insurance, healthcare accessibility, and social participation, explained next.

First, economic resources are manifested through income improvement and increased liquidity stimulated by digital finance, which enhances older adults’ capacity to afford health-preserving goods and services. Second, the facilitation of healthcare service utilization through digital finance platforms alleviates the spatial and informational barriers to medical treatment. Third, digital insurance reduces the effective price of healthcare by lowering out-of-pocket expenses and uncertainty associated with illness, further encouraging timely medical interventions. Fourth, digital finance promotes older adults’ social participation by providing more convenient payment methods and a wider range of activity recommendations, thereby stimulating healthier lifestyles. Through these interconnected channels, digital finance is expected to enhance older adults’ abilities and willingness to invest in their health, ultimately contributing to sustained physical health outcomes. Several recent studies have provided empirical evidence of the health-promoting effects of digital finance. Liao and Du 44 found that digital finance enhances physical health by increasing household expenditure on fitness and extending the duration of physical exercise. Yan et al. 45 focused on the migrant population and showed that digital finance contributes to improved health outcomes by facilitating the expansion of healthcare institutions and mitigating environmental pollution. Based on the above discussion, we propose the following hypothesis:

H1: Digital finance is conducive to enhancing the physical health of the elderly.

Digital finance has been widely recognized for its significant contribution to promoting income and reducing poverty. 46 For urban residents, digital finance can improve income by fostering their entrepreneurial spirit and increasing their participation in financial markets. 47 For rural residents, digital finance can help increase agricultural productivity and foster non-agricultural employment, raising income levels and alleviating the vulnerability of rural households. 48

Digital finance has direct and indirect effects on income. Regarding the direct impacts, digital finance expands investment channels—residents can invest small through digital finance platforms, such as Yu’E Bao, thus promoting the growth of wealth. 49 As for indirect effects, digital finance contributes to increasing employment and entrepreneurship. Lee et al. 50 investigated whether rural households could reduce poverty by using mobile banking and found that people who frequently used mobile banking were more likely to receive additional job offers. Zhang et al. 51 stated that digital finance helps increase household income by promoting entrepreneurship, and households with fewer physical and social assets benefit relatively more.

A substantial body of research indicates that increases in income are positively correlated with enhancements in individuals’ physical health.52,53 Miglino et al. 54 evaluated the impact of a permanent income increase on the physical health of elderly individuals using Chile's pension plan as a case study; the results showed that the probability of death among elderly pension recipients decreased by 2.7%. Similar conclusions have been drawn from studies focusing on elderly individuals in China. By comprehensively examining indicators such as activities of daily living (ADL), instrumental activities of daily living (IADL), and physical illnesses, Mitra et al. 55 showed that higher income levels can significantly enhance the physical health of older adults. More importantly, income and health can mutually reinforce each other; higher-income individuals can afford comfortable and clean living conditions and high-quality health investments, which help maintain better physical health status and work performance. Consequently, their income may increase.56,57 Based on the above, the following hypothesis is proposed.

H2: Digital finance improves the physical health of the elderly by promoting income growth.

The liquidity sensitivity of healthcare consumption indicates that liquidity constraint is an important factor in delaying or preventing patients from seeking medical attention.58,59 Gross et al. 60 stated that individuals constrained by budgets consume healthcare only when they have cash, instead of when they need it. Their physical health improves significantly if they obtain transfer payments or exogenous sources of income. Apouey and Clark 61 showed that liquidity brought that lottery prizes have a positive impact on mental health. Kim and Koh 62 also found that lottery prizes can promote physical health. Most studies indicate that alleviating liquidity constraints is beneficial in promoting residents’ utilization of healthcare, thereby improving their physical health status.63,64 Belchior and Gomes 65 investigated whether cash transfers like emergency aid (EA) could mitigate delays in healthcare utilization among individuals facing financial constraints and limited access to credit. Their findings suggest that EA effectively shortened the time to seek medical attention and contributed to a notable decline in the number of new daily infections.

Digital finance is extremely inclusive in providing financial support. On one hand, it helps overcome geographical barriers by facilitating the matching between fund providers and demanders, residents from any location have the potential to obtain loans. 33 On the other hand, digital finance institutions or platforms can access data on a broader scale, altering the traditional credit service model with fewer restrictions and lower thresholds for financial service applicants. 66 In the traditional financial system, a large share of the elderly population lacked collateral and was unable to accumulate credit records via credit cards. The advancement of digital finance has transformed this pattern, allowing individuals to accumulate credit through routine transactions conducted via platforms like WeChat and Alipay. These records are now used by digital financial platforms for loan approval. 67 With the increasing use of mobile payments among the elderly, they are more likely to access loans, thereby significantly alleviating their liquidity constraints. Based on the above, we propose the following hypothesis:

H3: Digital finance improves the physical health of the elderly by alleviating liquidity constraints.

Insurance is intricately linked to physical health, as it can effectively reduce the financial burden of medical expenses, thereby facilitating timely access to healthcare when needed, and supporting the maintenance of overall health. 68 Specifically, social insurance programs, exemplified by the New Rural Cooperative Medical Scheme and long-term care insurance, enhance individuals’ utilization of primary medical care, thereby fostering substantial improvements in their physical health. 69 In addition to social insurance, private health insurance can complement social health insurance by addressing residents’ diverse and high-intensity healthcare needs and encouraging greater engagement in preventive healthcare services, including routine health examinations. It also contributes to improvements in residents’ physical well-being.70,71

As a key function of digital finance, digital insurance refers to insurance services provided through digital technology and online platforms, this model typically involves purchasing insurance and filing claims through mobile applications, websites, or other digital channels. 72 Digital insurance can overcome the spatial constraints of the traditional offline mode to improve accessibility of insurance. 73 It effectively reduces information asymmetry between applicants and insurance companies, allowing residents to directly access introduction and price of insurance products through mobile terminals and choose suitable products. 74 More importantly, digital insurance significantly enhances the convenience and efficiency of claims; applicants only need to upload relevant documents to the online platform, and the insurance company can complete the claims process in a relatively short time through a dedicated claims channel, thereby avoiding cumbersome procedures and extended evidence-gathering time in offline commercial insurance. 75 Studies indicate that the expansion of digital finance stimulated residents to purchase digital insurance, leading to pronounced enhancement of physical health outcomes among older adults.33,76 Based on the above, the following hypothesis is proposed.

H4: Digital insurance services enhance the physical health of the elderly.

The application of digital finance in the healthcare sector plays an essential role in enhancing older adults’ accessibility to medical services. Digital finance platforms streamline the process of offline medical visits by facilitating appointment scheduling, real-time payments, and the retrieval of test results, leading to shorter waiting times and reduced physical and mental burden commonly associated with traditional healthcare procedures. 77 By integrating telemedicine and online pharmacy services, it enables older adults to consult physicians remotely, access professional advice, and obtain prescriptions online, thereby extending the spatial and temporal availability of medical care in a manner particularly beneficial for those living in underserved or rural areas. 78 Improvements in healthcare accessibility driven by digital finance empower older adults to obtain timely diagnoses, adhere to treatment regimens, and participate in preventive care practices. These elements are vital for controlling chronic diseases and curbing progressive physical health decline, ultimately contributing to maintaining their physical capability and the promotion of long-term well-being. Based on this discussion, we propose the following hypothesis.

H5: Digital finance promotes the physical health of the elderly by enhancing healthcare accessibility.

Social participation is widely recognized as a crucial determinant of physical health among older adults. Engaging in community activities, volunteer services, or group-based leisure events often requires regular mobility and interaction, which encourage physical activity and help maintain functional capacity. 79 Moreover, active involvement in social networks can promote adherence to healthy behaviors such as maintaining a balanced diet, engaging in regular exercise, and undergoing preventive health checkups, largely through peer influence and the dissemination of health-related knowledge. 80 Studies have shown that higher levels of social engagement are associated with a lower risk of chronic diseases, reduced functional decline, and better self-rated physical health later in life. 81 Therefore, promoting social participation is an effective strategy for enhancing the physical well-being of the elderly.

Digital finance holds significant potential for enhancing older adults’ social participation by lowering barriers to social engagement and expanding opportunities for interpersonal interactions. First, digital financial services provide streamlined payment methods outside homes, allowing older adults to engage in community life and social interactions more conveniently and with greater autonomy. 82 Second, by providing user-friendly platforms and personalized recommendations, digital finance facilitates seniors’ involvement in various consumption activities such as group travel and recreational gatherings. 83 Third, the integration of digital finance with social media can indirectly strengthen elderly individuals’ connections with their peers and communities, thereby fostering a stronger sense of belonging and inclusion. 84 Through these pathways, digital finance contributes to reducing social isolation and promoting active participation in social networks among older adults. Therefore, we propose the final hypothesis.

H6: Digital finance enhances the physical health of the elderly by promoting social participation.

Method

Data

Data used in this study were obtained from the CHARLS, related to physical health status, insurance coverage, daily routine, lifestyle, and demographic characteristics. We utilize data from the 2013, 2015, and 2018 waves. Although the latest wave released to date is from the year 2020, substantial changes in the questionnaire design have resulted in the absence of data on certain key variables required for this analysis, such as liquidity constraints. Therefore, the 2020 wave is not included in this study.

The Digital Finance index developed by Peking University was employed to measure the development of digital finance. 25 This aggregate index is compiled using big data from Ant Group and covers three aspects: breadth of coverage, depth of usage, and degree of support for digital services. This index comprises three levels—province, municipality, and county—reflecting the utilization of various digital financial services, such as mobile payments, digital insurance, monetary funds, online loans, and Internet investments. This study focuses on the aggregate index at the municipal level in the same years as the CHARLS. In addition to the micro data, macro data, such as the year-end balances of financial institution loans and per capita GDP at the municipal level, were primarily employed as control variables.

Variables

Physical health status among the elderly is evaluated based on their performance in ADL and IADL,85,86 comprising 12 indicators, such as dressing, bathing, eating, getting up, using the toilet, controlling bowel and bladder movements, doing housework, cooking, shopping, making phone calls, taking medication, and financing. Each ability is classified into four levels: “no difficulty,” “difficulty but can still complete,” “difficulty, requires assistance,” and “unable to complete.” Correspondingly, scores from 4 to 1 are assigned, where a higher score indicates better functional ability. Final scores ranged from 12 to 48 points. Self-rated health is utilized as an alternative dependent variable to capture their physical health status; however, owing to subjective bias in this indicator, it was only used in robustness checks. Considering the research subjects of this paper, samples aged 60 and above were retained.

The core explanatory variable is the municipal level digital finance index, representing the level of digital finance development across different regions.87,88 Micro-level control variables primarily related to personal information of the respondents, such as residence, age, marital status, medical insurance, pension, education level, physical exercise, and family hygiene.89,90 Physical exercise was represented by the survey question: “Do you usually participate in any of the following activities for at least 10 minutes per week? This includes vigorous physical activities that are physically demanding (such as fast cycling), moderate-intensity physical activities (such as practicing Tai Chi), and light physical activities (such as walking).” A response of “yes” to any of these activities was recorded as 1, while responses of “no” to all activities were recorded as 0. Family hygiene was based on the investigator's evaluation of the household cleanliness. Level of cleanliness was classified into five options: “untidy,” “ordinary,” “clean,” “very clean,” and “extremely clean,” to which values from 1 to 5 were assigned, respectively (1 representing “untidy”).

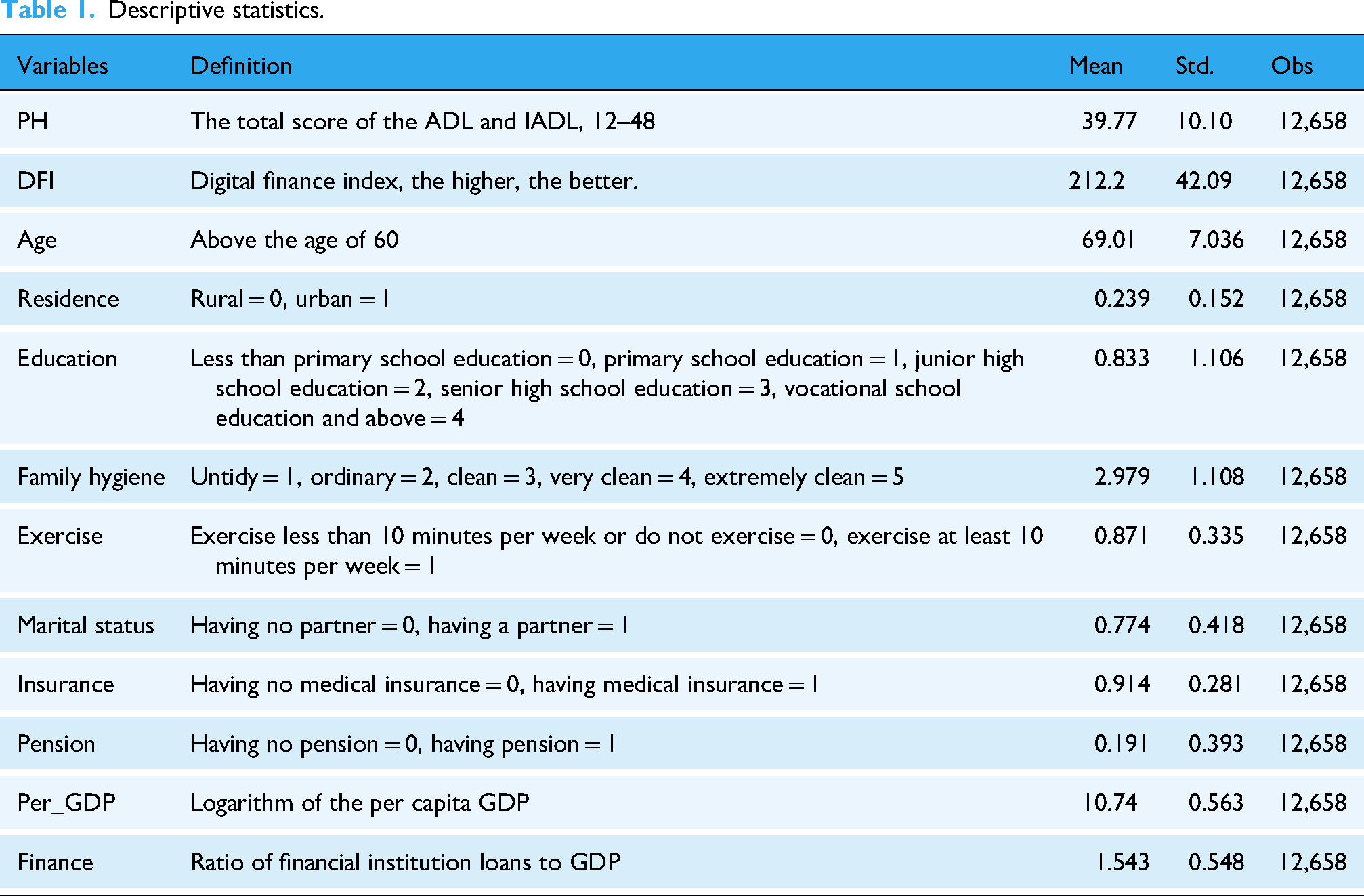

Macro-level control variables include the logarithm of the per capita gross domestic product (GDP), and scale of traditional finance, represented by the ratio of financial institution loans to GDP. The descriptive statistics for all variables are presented in Table 1.

Descriptive statistics.

Empirical results

Model

Based on our theoretical analysis, we used a two-way fixed-effects model to investigate the effects of digital finance on the physical health of elderly individuals. Individual fixed effects address the unobserved variations among older adults, such as personal characteristics and baseline health conditions, which may influence health outcomes. Time-fixed effects control for factors that vary over time, but affect all individuals equally, such as macroeconomic conditions or changes in healthcare policies. By incorporating both individual and time-fixed effects, we obtain more accurate estimates of the causality between digital finance and physical health in the elderly, isolating the influence of digital finance from other confounding variables. This model, also widely used in research related to digital finance,91,92 is outlined as follows:

In equation (1),

Regression results

Table 2 reports the baseline regression outcomes. In column (1), only the core dependent and independent variables are included, Column (2) shows the regression results containing micro control variables, and Column (3) displays the results of the two-way fixed effects regression containing both micro and macro control variables. The estimated coefficient of

Baseline regression results.

Note: Robust standard errors clustered at the municipal level are shown in parentheses.

*p < 0.1, **p < 0.05, and ***p < 0.01.

Endogeneity analysis

Although the probability of reverse causality between digital finance and physical health in the elderly is extremely high, endogeneity problems may still be triggered by measurement errors or omitted variables. Therefore, we employed Internet penetration rate as the IV for

The IV must satisfy the principles of relevance and exclusivity. On one hand, the expansion of digital finance is deeply rooted in Internet technology; higher Internet penetration rates indicate a more developed Internet infrastructure and mature technology in the region, thereby providing a robust foundation for continuous advancement of digital finance. The IV satisfy the relevance requirements. On the other hand, the physical health level is a personal state that is not directly influenced by the internet penetration rate. Thus, Internet penetration rate is a suitable IV for digital finance.

Column (1) of Table 3 presents the first-stage regression results. The coefficient of the IV is statistically significant and positive, indicating that the development of digital finance is closely associated with Internet penetration rates, which aligns with expectations. The F-value in the first-stage regression is 16.59, which is greater than 10, suggesting no weak IV problem. The second-stage regression results are reported in column (2) of Table 3. In line with the baseline analysis, the coefficient of

Instrument variable estimation results.

Note: Robust standard errors clustered at the municipal level are shown in parentheses.

*p < 0.1, **p < 0.05, and ***p < 0.01.

Robustness checks

A range of robustness checks has been performed to confirm the reliability of the baseline regression; the results are showed in Table 4. First, we modified the model. Considering that the dependent variable

Robustness checks.

Note: Robust standard errors clustered at the municipal level are shown in parentheses.

*p < 0.1, **p < 0.05, and ***p < 0.01.

We then change the dependent variable. In addition to ADL and IADL, the CHARLS survey also included questions related to physical mobility, including nine activities such as yoga, long-distance and short-distance walking, standing up after prolonged sitting, climbing stairs, squatting, stretching arms, lifting heavy objects, and picking up coins. Each ability is classified into four levels: “no difficulty,” “difficulty but can still complete,” “difficulty, requires assistance,” and “unable to complete.” Scores from 4 to 1 are assigned, where a higher score indicates better physical mobility. We calculated the scores based on respondents’ answers, and then summed the scores with the existing dependent variable, creating a new dependent variable named “Health_New.” Additionally, we used self-reported health measures to assess the physical health of the elderly. Self-reported health includes five options: “very bad,” “bad,” “fair,” “good,” and “very good”—with higher values indicating better health status. Both Columns (2) and (3) of Table 4 present that digital finance significantly facilitates physical health among the elderly.

In the third step, elderly people from Beijing, Shanghai, Guangzhou, Shenzhen, and Hangzhou were excluded. Alipay, as a symbol of digital finance, was first launched in Hangzhou and placed the city at the vanguard of this field. Beijing, Shanghai, Guangzhou, and Shenzhen are first-tier cities in China, where IT is growing more rapidly than in other cities; thus, these cities rank among the leading areas of digital finance development across the country. After eliminating samples from cities with obvious comparative advantages, the regression results can more accurately reflect the influence of digital finance on the physical health of the elderly. In Column (4) of Table 4, the coefficient remains significantly positive. A series of tests demonstrated that the conclusions of this study are relatively reliable.

Heterogeneity analysis

To identify heterogeneous effects, an interaction-term approach is adopted by incorporating interaction terms between the core explanatory variable and subgroup identifiers into the regression model. Due to large discrepancies in sample sizes between groups in this study, the traditional approach of subgroup regressions poses significant limitations, differences in significance of estimated coefficients across groups may not truly reflect heterogeneous effects but rather stem from inconsistent sample structures and distributions of control variables. By estimating the interaction terms in the full sample, this method maintains consistent controls and model specifications across groups. It effectively avoids the structural biases introduced by sample splitting and ensures greater comparability of results. The interaction coefficients offer a clearer and more robust identification of heterogeneous effects, making this approach more suitable for examining how digital finance affects the health of older adults across different populations.

Table 5 presents the heterogeneity analysis results differentiated by urban and rural residency, education, traditional financial scale, and regions. First, China's bifurcated urban–rural economic system endogenously determines the potential heterogeneity in the impact of digital finance. However, the results in Column (1) of Table 5 reveal an insignificant coefficient on the interaction term, implying that digital finance exerts a comparable positive impact on the physical health of older adults in both urban and rural settings. This finding can be largely explained by the promotion of the digital rural initiative, through which China has substantially advanced the development of digital infrastructure in rural communities, and promoted the deep integration of digital finance with agriculture, rural areas, and farmers. Rural elderly individuals can also benefit from the increasing prevalence of digital finance.

Heterogeneous influence analysis.

Note: Robust standard errors clustered at the municipal level are shown in parentheses.

*p < 0.1, **p < 0.05, and ***p < 0.01.

Second, given that the elderly individuals in the sample were generally undereducated, we set junior high school education as the cutoff point. Samples were recorded as 0 if the individual's education level was below junior high school, and as 1 if they had completed junior high school or higher. The coefficient of the interaction term in Column (2) of Table 5 is not significant, reflecting that digital finance has positive influence on elderly individuals with different educational backgrounds. This finding indicates the inclusion of digital finance. Elderly individuals with lower educational levels often have lower financial literacy and are easily excluded from traditional financial services. The emergence of digital finance has significantly reduced barriers to accessing financial services such as loans and financial management. Additionally, many digital finance applications have introduced elderly oriented features, enabling elderly individuals with lower educational levels to use these financial tools.

Third, samples were categorized based on whether the traditional financial scale of their region was below or above the median, with 0 indicating the former and 1 indicating the latter. In Column (3) of Table 5, the non-significant coefficient of the interaction term indicating that the positive effect of digital finance on the physical health of the elderly does not vary significantly across regions with different traditional financial scales. This further highlights the inclusion nature of digital finance as it transcends the geographical limits institutions by conducting financial transactions directly through online platforms. This greatly expands the channels for elderly individuals in regions with underdeveloped traditional financing to access financial resources, thereby overcoming the endemic constraints of offline financing.

Finally, we divided the samples into three regions, east, central, and west, based on the provinces of residence. Elderly individuals were classified according to their region of residence: 0 for the western region, 1 for the eastern region, and 2 for the central region. In Column (4) of Table 5, Reg1 represents a comparison between the eastern and western regions, whereas Reg2 represents a comparison between the central and western regions. The two negative coefficients imply that digital finance has a stronger promotive effect on the physical health of older adults in the western region. This finding can be better understood in light of the economic and social background of the west, which faces persistent challenges such as lower levels of economic development, inadequate financial services, and restricted accessibility to high-quality medical resources. In addition, the relatively late development of IT in this region has resulted in weak digital foundations and limited exposure to digital services. These constraints make the elderly in this region more vulnerable to health risks and more dependent on external support systems. In such under-resourced settings, the introduction of digital finance can help overcome the shortcomings of traditional financial and healthcare support systems, thereby generating stronger marginal benefits. By contrast, in the central and eastern regions, where digital technologies are already deeply embedded in daily life, the incremental gains from digital finance tend to be less pronounced.

Mechanism results

This part investigates the underlying channels linking digital finance to improvements in elderly physical health. Table 6 presents the mechanistic analysis results.

Mechanism analysis.

Note: Robust standard errors clustered at the municipal level are shown in parentheses.

*p < 0.1, **p < 0.05, and ***p < 0.01.

Income

Column (1) of Table 6 shows the effect of digital finance development on elderly income. Incomes are the sum of wages, pensions, and other subsidies. Theoretical analysis indicates that digital finance contributes to increasing income directly or indirectly, thereby promoting physical health of the elderly. The positive and statistically significant coefficient of

Liquidity constraints

In Column (2) of Table 6, we investigate whether mitigating liquidity constraints through digital finance serves as a channel for enhancing the physical health of older adults. The liquidity constraints of the elderly were measured using their personal debt ratio (debt/assets). As few studies have analyzed the impact of liquidity brought about by online loans on physical health, an interaction term between the personal debt ratio and the digital finance index is added to further examine this mechanism. Theoretical analysis indicates that digital finance enhances the physical health of older adults by alleviating their liquidity limitations, which means that the physical health of those facing higher liquidity constraints should improve further, and that the coefficient of the interaction term should be statistically significant and positive. The results show that the interaction coefficient between digital finance and the personal debt ratio is not significant, implying that the mitigation of liquidity barriers through digital finance did not lead to a notable enhancement in their physical health. Thus, H3 was not supported.

Digital insurance

Column (3) of Table 6 lists the influence of digital insurance on the physical health of older adults. Digital insurance is measured by the digital insurance subindex. According to our theoretical analysis, digital insurance can reduce uncertainty, offer financial assistance for the healthcare of the elderly, and meet their preventive or therapeutic medical needs, thus elevating their physical health status. The positive and significant coefficient of digital insurance demonstrates a beneficial effect of digital insurance on older adults’ physical health. Digital insurance offers a variety of products at relatively low prices and provides convenient and quick claims services, better ensuring the medical needs of the elderly and enhancing their physical health levels. 75 Thus, H4 is supported.

Healthcare accessibility

Column (4) in Table 6 shows the impact of digital finance on healthcare accessibility. Due to the lack of data on telemedicine in the CHARLS, healthcare accessibility was measured by whether the respondent had undergone a physical examination in the past year. Theoretical analysis indicates digital finance facilitates older adults’ utilization of healthcare services by streamlining medical procedures and reducing information asymmetry between patients and healthcare institutions, thereby contributing to improved physical health. The results show that the coefficient of digital finance is significant and positive, demonstrating its important role in enhancing healthcare access. Improved access to healthcare enables earlier detection of health problems, ensures timely medical interventions, and supports regular health monitoring. Such advancements are crucial for reinforcing physiological resilience and decelerating the trajectory of functional decline later in life. 95 Thus, H5 is supported.

Social participation

Column (5) of Table 6 presents the effects of digital finance on older adults’ social participation, which was measured based on whether the respondent engaged in any of the following 11 types of activities over the past month: interacting with friends; playing mahjong, chess, cards, or visiting a community club; helping non-cohabiting family members, friends, or neighbors; attending sports, social, or other clubs; participating in community-related organizations; volunteering or engaging in charity work; caring for a sick or disabled non-cohabiting adult; enrolling in educational or training courses; investing in stocks; using the Internet; and other activities. Elderly individuals who engaged in at least one of these activities were recorded as 1; otherwise, they were recorded as 0. Theoretical analysis indicates digital finance promotes social participation by enhancing payment convenience and broadening channels for social interaction, which in turn contributes to better physical health.

The results show that the coefficient of digital finance is significantly positive, indicating that digital finance effectively promotes older adults’ engagement in social activities, supporting H6. Greater social participation contributes to improved physical health by fostering more active lifestyles and enabling the timely exchange of practical health-related information. Collectively, these factors help mitigate physical decline and foster the maintenance of functional capacity among older adults. 79

Further analysis

The preceding analysis focused on mechanisms directly and intricately linked to the physical health of older adults. Considering the wide range of innovative financial services that digital finance includes, this study further investigates these additional components to offer a more holistic evaluation of the influence of digital finance.

Mobile payment refers to the method of payment using mobile devices; residents can complete financial transactions such as shopping, transferring money, and paying bills through mobile payment applications such as Alipay. 96 Column (1) of Table 7 shows this coefficient to be significantly positive, indicating that mobile payments have a positive effect on elderly physical health. Mobile payment is the most influential and well-developed product in China, with high coverage even among the elderly. 28 It is not only used for daily consumption but has spawned other services as well, such as internet hospitals.77,97 Older adults and their family members can directly make appointments, pay bills, and consult doctors through mobile payment platforms. This significantly enhances the convenience of healthcare and improves the accessibility of high-quality medical resources, allowing the elderly to make full use of healthcare services to maintain their health. Research has found that the mobile payments usage has greatly enhanced the convenience of accessing medical care. This study builds on the foundational work by directly investigating the impact of mobile payments on physical health outcomes, showing that mobile payments hold considerable promise for fostering the well-being of the elderly, thereby broadening the conceptual and empirical horizons of this research domain.

Further analysis.

Note: Robust standard errors clustered at the municipal level are shown in parentheses.

*p < 0.1, **p < 0.05, and ***p < 0.01.

Monetary funds are innovative, low-risk investment options with a low investment threshold and reduced risk, such as Yu’E Bao owned by the Ant Financial Services Group, and provide higher returns than traditional savings accounts, while maintaining high levels of security and flexibility for the invested capital. 98 Column (2) of Table 7 shows this coefficient to be significant and positive, revealing that monetary funds also effectively promote the physical health of the elderly. Yu’E Bao is a low-risk investment channel that allows people to invest in small funds and is suitable for the elderly with lower risk tolerance. It has been found to be an effective instrument to financially empower the elderly and other vulnerable groups, directly boosting their income.99,100 Considering the positive effect of income on physical health, the long-term and stable income obtained from using Yu’E Bao should promote the physical health of the elderly. This result not only supports the findings of our analysis of the income mechanism, but also enriches the discussion on the welfare effects of monetary funds.

Internet investment refers to the use of digital finance platforms to allocate funds to relatively higher-risk financial assets, such as stocks. This enables individuals to engage in investment activities without relying on traditional offline financial institutions or intermediaries. 101 The results in Column (3) of Table 7 show that the coefficient is not significant, suggesting that the impact of Internet investment on elderly physical health of the is limited. This may be because most older adults are risk-averse; they seldom engage in stock trading and tend to choose conservative investment tools to mitigate any form of risk, 102 thus, they are rarely influenced by internet investments. This finding suggests that the investment preferences of older adults remain unaffected by the mode of investment, further substantiating the conclusion that the elderly generally exhibit pronounced aversion to risk.

Online loans refer to the method of applying for loans through digital finance platforms, lending institutions assess the applicant's line of credit based on their daily social media activities, online consumption records, and other data, applicants can obtain loans only through a simple online approval process. 103 Column (4) of Table 7 presents the effects of online loans on older adults’ physical health, showing a significantly negative coefficient, which indicates such loans are detrimental to the physical health of the elderly. This further supports the conclusion of liquidity constraints in the mechanism analysis. Existing research has found that elderly individuals often have a pessimistic attitude towards debt, so that debt can potentially lead to serious conditions such as heart disease.104–106 However, studies on this topic primarily rely on data from elderly populations in the United States or European countries and concentrate on borrowing from traditional financial institutions, without addressing the role of online loans. By contrast, we explored the impact of online loans, which have gained prominence in the digital age, on the elderly physical health in China and demonstrate the relevance and applicability of the conclusion that indebtedness can negatively affect them.

This study further assesses the potential long-term effects of digital finance on elderly physical health by incorporating a two-period lag of the digital finance index for regression. The coefficient in Column (5) of Table 7 is significant and positive, indicating that the earlier development of digital finance continues to exert a promotive effect on the current physical health status of older adults. This finding suggests that the health benefits of digital finance are not merely short-lived but may accumulate over time, highlighting its sustained role in supporting healthy aging. The persistent association between earlier exposure to digital financial services and improved later-life health outcomes provides empirical support for the view that digital finance can be an effective long-term instrument for enhancing elderly physical well-being.

The long-term positive impact of digital finance on elderly physical health can also be further elucidated in the context of varying socio-economic conditions. Its scalability and adaptability render it applicable across a broad spectrum of regional development levels. In less developed areas, where traditional financial infrastructure and public health resources are often limited, digital finance serves as a compensatory tool by facilitating access to health-related expenditures, improving financial resilience, and reducing barriers to timely medical care. Meanwhile, in more developed regions with better baseline conditions, digital finance may further optimize health-related behaviors by enhancing convenience, enabling more flexible resource allocation, and supporting personalized health management. This capacity to meet diverse regional and demographic needs underscores the role of digital finance in fostering more equitable and sustainable health outcomes among older adults.

Conclusions and implications

Discussion

With the role of IT in improving elderly health gaining in prominence, this study investigated the influence of digital finance on the physical health of older people, consequently supplementing the literature. First, it demonstrates that digital finance significantly improves the physical health of older adults, which reinforces existing research that has identified the health benefits of digital finance, such as improved self-reported health.44,45 The strengthened empirical evidence can be attributed to the more rigorous measurement of health status, namely ADL and IADL. These indicators, which capture the self-care abilities and functional independence of the elderly, are less susceptible to subjective bias than self-reported health. In doing so, this study provides reliable and robust support for the role of digital finance in enhancing daily functions and sustaining the independence of older adults.

Second, this study demonstrates that digital finance promotes older adults’ physical health by improving their income. This finding adopts a different analytical perspective from existing research and serves as a valuable complement. Previous research relying on macrolevel data from statistical yearbooks has shown that digital finance contributes to reducing the proportion of the impoverished population. 107 Building on this, this study shifts focus to the micro level by directly examining individual income, providing additional evidence of the income-enhancing welfare effects of digital finance from a more granular perspective.

Third, this study shows that the relaxation of liquidity constraints brought about by digital finance does not improve physical health in older adults, which differs from existing findings.62,65 A possible reason is that the studies that explore scenarios in which alleviating liquidity constraints promotes physical health mainly involve residents receiving lottery prizes or government subsidies, which directly increase cash flow. However, debt increases when elderly individuals obtain funds through digital finance platforms. The pressure of repayment potentially offsets the positive effects of liquidity constraint alleviation on physical health. 106

Fourth, this study revealed that digital insurance is positively associated with better physical health outcomes among older adults. Unlike previous research, which primarily focused on the role of traditional offline insurance models,68,70 this study emphasizes the health-promoting potential inherent in the digital transformation of insurance. This effect may be attributed to improved accessibility, operational efficiency, and user experience, which lowers participation thresholds and enhances the timeliness of financial protection in medical processes, especially for individuals less likely to benefit from the delivery of conventional insurance products.

Fifth, this study shows that digital finance promotes physical health among older adults by enhancing access to healthcare services, an important pathway largely overlooked in studies focusing on other age groups. Extant research emphasizes how digital finance supports health through increased access to online shopping. 44 In contrast, healthcare accessibility is particularly crucial for older adults whose need for chronic disease management and timely treatment increases with age. By integrating services such as online appointments and telemedicine, digital finance helps alleviate common barriers faced by the elderly in offline healthcare settings, including mobility limitations and procedural complexities. Compared to consumption-based mechanisms, this healthcare access pathway better reflects the unique value of digital finance in supporting the physical well-being of the aging population.

Sixthly, this study demonstrates that digital finance enhances physical health among older adults by facilitating their engagement in social activities. Unlike existing studies that primarily examine how general Internet use fosters social participation,108,109 this study provides a more nuanced perspective by focusing on digital finance, a specific application of the internet in the financial sector. As a targeted and functionally integrated tool, digital finance encourages social interaction among the elderly by providing more inclusive financial services and diversifying available activity choices. These unique features make digital finance particularly effective in promoting sustained social engagement, which in turn contributes to better physical health outcomes later in life.

Policy implications

This study proposes policy implications from two perspectives: the design of digital finance and the provision of social services aimed at enabling more elderly individuals to utilize digital finance and reap its benefits.

First, it is crucial to develop financial products tailored to the elderly, such as low-risk investment products and health insurance. Personalized financial services and advice should be offered, taking into account their consumption habits, health status, and financial situation to help them better manage their wealth. To encourage greater involvement from financial institutions in this area, government authorities can implement incentive schemes, including tax reductions, targeted subsidies, and preferential treatment in public–private partnership programs to stimulate product innovation and service adaptation. Establishing formal recognition mechanisms, such as certification systems or government-endorsed excellence awards, can enhance institutional reputation and competitiveness, further motivating the development of elderly-friendly financial services. Second, digital financing should be integrated with digital health services, offering online health consultations, medication purchases, and medical appointment scheduling to further improve the convenience of healthcare access. Third, dedicated customer service and support channels, such as phone hotlines and online customer support, should be established for the elderly. This ensures that older adults receive timely assistance and answers while utilizing digital financial tools. Finally, the security of such platforms must be enhanced with stricter identity verification and transaction-protection measures specifically designed for the elderly. These measures will help alleviate security concerns and increase their confidence in the use of these platforms.

In terms of social services, the need to accelerate the equalization of the digital infrastructure is urgent. Although our research reveals that the health benefits of digital finance show no significant differences between urban and rural elderly populations, a significant gap exists due to the relatively weak Internet infrastructure in rural areas. Efforts should be made to expedite the development of digital infrastructure in less developed and rural regions and provide stronger hardware support for advancing of digital finance.

Second, community-based education initiatives should be strategically developed to enhance the acceptance and use of digital finance among older adults. Community organizations can collaborate with financial institutions to offer digital finance training programs that focus on practical skills such as using mobile payments, managing digital accounts, and recognizing online fraud. These programs should be delivered through familiar and accessible channels, including community centers, senior universities, and residential committees, using interactive formats that encourage hands-on practice. Additionally, engaging younger volunteers or family members as digital finance ambassadors helps foster intergenerational learning and build trust. By embedding digital finance education in community life, these initiatives can alleviate anxiety about technology use and improve digital literacy.

Third, an integrated support network that mobilizes the participation of various sectors of society should be established to address the broader service needs of older adults in this digital era. Under the guidance of government policies, enterprises, communities, and non-governmental organizations can collaborate to provide tailored assistance, such as dedicated digital finance service counters and peer support programs. Leveraging local community centers as hubs for both social engagement and ongoing digital assistance ensure that older adults receive timely, human-centered support in adapting to digital finance platforms. A coordinated social service framework strengthens the long-term inclusiveness and resilience of digital finance adoption among aging populations.

Limitations and future directions

This study has a few limitations. First, owing to data constraints, the most recent wave used in this study was from 2018, which may not fully reflect current dynamics. Future research could incorporate more recent longitudinal data and explore additional mechanisms included in the new waves through which digital finance may affect the health of older adults, thereby offering a more comprehensive and timely understanding of its impact. Second, this study focuses solely on physical health; future research could extend the analysis to other dimensions of health, such as mental health and quality of life, to develop a more comprehensive understanding of how digital finance shapes overall health outcomes.

Conclusions

Using data from CHARLS and the digital finance index at the municipal level, this study provides an empirical analysis of how the development of digital finance influences the physical health of the elderly. The results demonstrate that digital finance significantly promotes older adults’ physical health. In terms of heterogeneity, the positive effects of digital finance are more pronounced in the western regions, with no notable differences observed across locations, education, or the region's traditional financing scale. The mechanistic analysis revealed that digital finance development enhances physical health status by increasing income and promoting healthcare accessibility and social participation, with a significant role of digital insurance, mobile payments, and monetary funds.

Footnotes

Acknowledgements

The authors would like to sincerely thank the China Health and Retirement Longitudinal Study (CHARLS) Team and Institute of Digital Finance of Peking University.

Ethical considerations

The de-identified, publicly available human samples used in this study were obtained from the China Health and Retirement Longitudinal Study (CHARLS) database. The CHARLS project was reviewed and approved by the Institutional Review Board of Peking University Health Science Center (IRB00001052-11015).

Author contributions

Haoyi Zeng: conceptualization, methodology, writing—original draft preparation. Chuanfeng Han: conceptualization, writing—review & editing, funding acquisition. Pihui Liu: methodology, writing—review & editing, funding acquisition. Lingpeng Meng: conceptualization, writing—review & editing, funding acquisition.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was partially supported by the National Natural Science Foundation of China (grant numbers 72474128, 71974122, and 71874123), the National Social Science Fund Project of China (Key Program) (grant numbers 23AZD073), and the Natural Science Foundation of Shandong Province, China (grant number ZR2023QG066).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Guarantor

Prof. Lingpeng Meng.