Abstract

Are people likely to reward politicians who support canceling student loan debt? This paper draws on original conjoint and survey experimental data to assess the effects of student debt relief proposals on voter behavior. Using data collected 3 months prior to Biden’s announcement of a specific plan for broad-based student debt relief, the paper addresses two interrelated questions: How do policy details—such as eligibility restrictions and the amount of debt canceled—shape voter support for candidates who embrace student loan cancellation? And second, will executive action by President Biden increase Democrats’ chances of winning in 2022 or 2024? We find evidence to suggest that candidates who support student debt relief plans offering generous debt cancellation while minimizing eligibility restrictions get the largest boost in support from voters, especially for key Democratic constituencies. We also find that executive action on student debt increases the likelihood that key groups would support Democratic congressional candidates in upcoming electoral contests. These results offer the first systematic evidence exploring the potential political ramifications of enacting student debt relief.

Introduction

On 25 August 2022, President Biden announced a long-anticipated plan to provide student loan debt relief to most of the approximately 46 million Americans who together owe more than 1.6 trillion dollars in federal education loans. Through a series of executive actions, Biden’s plan called for $10,000 of forgiveness for all borrowers of federal student debt with incomes below $125,000 ($250,000 for married couples), $20,000 of forgiveness for Pell Grant recipients, and changes to make income-driven repayment plans more generous (White House 2022). 1

The announcement delivered on Biden’s campaign promise to address the growing student debt crisis. It also came in the wake of a persistent effort by a coalition of progressive lawmakers, advocacy groups, and activists calling for federal action to cancel student debt. Beyond the substantive benefits for borrowers, proponents encouraged Biden to pursue debt cancellation because of its presumptive political benefits as well. They argued that enacting a policy popular with the Democratic base might help Democratic lawmakers avoid a “red wave” in the 2022 midterm election and improve the president’s flagging approval ratings. Opponents also seemed certain of the plan’s political payoff, with prominent Republicans accusing Biden of trying to buy votes with his debt relief proposal.

While ongoing legal challenges have stalled the program’s full implementation and made the fate of debt cancellation uncertain, the issue of mounting student debt remains, particularly with the 3-year pause on federal student debt payments set to expire in August. Furthermore, as the administration engages in rulemaking to enact the less controversial reforms to income-driven payment and as borrowers experience either the reality of debt cancellation or the fallout from the Supreme Court halting a popular plan that millions of borrowers expected to benefit from, it is likely this topic will remain politically salient. In this context, it is critical to understand more about the political dynamics of student debt relief.

While opinion polls have shown support for student debt forgiveness broadly construed, especially among Democratic constituencies, this study employs original conjoint and survey experimental methods to make two key contributions to our understanding of the emerging politics of student debt relief. First, it systematically explores whether support for debt relief might meaningfully translate to political action—an assumption that has been merely speculative thus far. This is especially important to probe because studies find that public support for other reforms related to debt and credit often do not translate to political action—even in the survey context (SoRelle, 2020, 2022b). We also move beyond the more general insights gleaned from opinion polls by examining how specific details of student debt forgiveness proposals—including amount and type of debt to be forgiven—shape the likely dynamics of electoral support. Overall, we find evidence to suggest that both President Biden and congressional Democrats may reap political rewards from executive action on debt relief. But we also find that increasing the amount of debt forgiven and removing restrictions on eligibility for proposed income-driven repayment reforms might yield even stronger political rewards.

Study 1: Policy details and political mobilization for debt relief

What do voters think about different plans for student debt forgiveness, and how might different policy details translate to political support? Three factors seem especially relevant in understanding how policy attributes might shape voter behavior in the case of student debt relief: evaluations of beneficiary deservingness, preferences for universal versus targeted policy design, and self-interest. Scholars have demonstrated a clear link between how people evaluate the deservingness of beneficiaries and their support for social policies (Kreitzer et al., 2022; Schneider and Ingram, 1993). In general, beneficiaries are viewed as more worthy of government assistance when they demonstrate need, are perceived as hardworking, and are perceived as not responsible for their misfortune (Van Oorschot 2000). Thus, we might expect voters to prefer (and reward politicians for enacting) student debt relief plans that target needier populations or borrowers who chose less expensive education and those aimed at borrowers who have already spent time repaying their loans.

Alternatively, people might prefer more generous, less targeted student debt relief. Studies show that universal social programs are generally more popular than means-tested programs, or those targeted only toward particular groups (Heclo 1986; Korpi and Palme 1998). In the case of student debt relief, we might expect preferences for universal programs instead of those with means testing or other eligibility requirements. Scholars have also found that individual self-interest can influence policy preferences when the potential policy benefits in question are specific, substantively meaningful, and visible (e.g., Chong et al. 2001; Haselswerdt 2020). As such, we might expect those with a clear interest in student debt relief (e.g., borrowers) to be more in favor of a student loan plan that would result in forgiveness of their loans.

Data and methods

We explore how different policy designs for student debt relief influence voter support using a conjoint experiment fielded 3 months prior to Biden’s announced debt relief and 5 months before the 2022 midterm elections. 2 A conjoint allows us to consider separately how different elements of student debt relief policies might influence people’s prospective political behavior—something that existing polling evidence does not assess. Participants were presented with six successive pairs of hypothetical student debt relief plans with information about six policy attributes featured prominently in policy debates: amount of debt to be canceled, type of debt eligible, type of institution attended, borrower income eligibility criteria, other eligibility criteria, and funding mechanism. A description of conjoint attributes and levels is in the supplemental appendix, and they are listed in the following figures. Each of the attributes was fully randomized for each policy profile, such that every possible policy profile was equally likely. After considering the policy pairings, participants were asked, “How much more or less likely would you be to vote for a candidate for Congress in 2022 if they supported each of the student debt relief plans described above?” with answer choices on a scale from one to five, where one equals “a lot less likely to vote for” and five equals “a lot more likely to vote for.”

In general, participants exhibited support for student debt relief. When asked to report whether they would “support or oppose a government program to alleviate [student loan debt],” 72 percent of respondents said they either somewhat or strongly supported such a relief program. Debt relief was particularly popular among self-identified Democrats (88 percent) and independents (67 percent). Only among Republicans did federal student debt relief fail to garner majority support (33 percent). But no study to date has moved beyond measuring generic support for student debt proposals to empirically test (1) whether and how support translates to electoral preferences or (2) how policy details influence that relationship.

Results

Figure 1 reports the findings from the conjoint, which isolates the effects of several real-world policy elements on people’s support for candidates who back the respective plans. The results reported in the following coefficient plot represent the average marginal component effects (AMCEs) estimated using OLS regression with standard errors clustered at the respondent level. In other words, the coefficients show us how each value of a specific policy attribute (relative to the baseline value listed first in Figure 1) corresponds with the average change in the reported intent to vote for a candidate who supports that plan holding all else equal. Direct effect of attributes (AMCE) on candidate support.

Candidates who support proposed plans that include at least 50 thousand dollars of cancellation (relative to only 10 thousand) received a boost in participants’ expressed intent of voting for them of between a tenth and a fifth of a point on a five-point scale. This is notable given Biden’s plan to restrict debt cancellation to 10 thousand dollars for most borrowers. By contrast, candidate backing for plans that restrict relief based on type of college attended, amount of time in repayment, or work in public service actually decreased the reported voter support by between a tenth and a half of a point on a five-point scale. Finally, restrictions based on income and level of education—two prominent features of elite rhetoric regarding debt relief that are incorporated into Biden’s proposed plan—fail to move the needle on candidate support.

All three outcomes—positive, negative, and null effects—have potential implications for voter behavior. On a five-point scale, even small changes—especially evident when clustered around the median category indicating no effect—can produce meaningful shifts in respondents’ intended support. Similarly, the fact that some key policy choices appear to have no effect on voter support suggests politicians’ assumptions about which policy details matter politically may be incorrect.

To better observe whether these shifts produce substantive effects in the change of intended candidate support, and to explore whether these overall patterns hold for different constituent groups, Figure 2 presents the marginal means (Leeper et al., 2020) for each attribute and level broken out for key sub-groups: self-identified Democrats (including leaners) versus Republicans, student loan borrowers and non-borrowers, White and non-White participants, and people above and below age 35. Marginal means account for the varying baseline levels across groups. Predicted effect of attributes on candidate rating for target groups.

Several interesting findings emerge when we explore the results for different constituencies. Among Democrats, younger respondents, and non-White respondents, supporting any plan for student debt relief corresponds with respondents being “somewhat more likely” to vote for that candidate. There are, however, some key differences that emerge across policy details. Among Democrats and young respondents there is a small, statistically significant increase in willingness to vote for candidates who embrace at least 50 thousand dollars of debt cancellation relative to those who support only 10 thousand dollars—Biden’s proposed amount. Among non-White voters, only full debt cancellation elicits a statistically significant bump in intended voter support. This is notable because Black voters bear the heaviest debt burdens, and borrowers of color are the most likely to owe a significant portion of their initial loan amount after several years of repayment.

As with the full sample, these groups report slightly diminished (but still positive) willingness to vote for candidates who support restrictions on debt cancellation based on the type of institution attended, time in repayment, and work in public service. Income restrictions continue not to influence candidate support. Finally, Democrats become slightly less supportive of (though still positively inclined toward) candidates who want to limit forgiveness to undergraduate debt, while that makes little difference for young and non-White respondents—a notable finding given Biden’s proposal to restrict new income-driven repayment benefits to undergraduate debt.

Among Republicans, supporting any plan for debt relief makes respondents “somewhat less likely” to vote for the candidate. Interestingly, however, policy details do not generate statistically significant differences in the magnitude of opposition, except for candidates who want to restrict debt relief to students who attended historically Black or minority serving colleges. Older voters’ reported willingness to support a candidate is largely uninfluenced by most details of loan forgiveness the candidate supports; however, they are slightly more willing to vote for a candidate who supports a plan without restrictions on type of institution attended, time in repayment, or work in public service. A similar pattern emerges for White respondents with one notable difference: White voters become more willing to support a candidate who embraces cancellation of 50 thousand dollars or more relative to 10 thousand dollars.

Finally, we look at the effects for respondents who are student loan borrowers. In general, the patterns between borrowers and non-borrowers are quite similar, but there are a few notable differences. As for other groups, borrowers are more willing to vote for a candidate who supports canceling 50 thousand dollars or more relative to 10 thousand dollars. Interestingly, however, borrowers are similarly supportive of candidates who support no restriction on type of college attended or would restrict loan forgiveness to those with debt from public colleges, a distinct pattern relative to other groups.

Overall, these findings suggest several interesting implications about what does and does not matter to voters in the case of student debt relief. A key argument among opponents (and, indeed, some proponents) is that wealthier borrowers with graduate degrees are less deserving of help. In our experiment, however, neither income eligibility caps nor restricting benefits to undergraduate debt appeared to matter for voters’ support (and in the case of the latter, they actually diminished support among Democrats). Furthermore, limiting relief based on the type of college attended generally lowered support for candidates endorsing those plans. Thus, plans designed to target benefits to people deemed more deserving—whether due to greater financial need, time in repayment, or choice of less expensive education—did not generally translate to the largest electoral rewards, and in some cases weakened them. Results also imply that while self-interest may be a factor, most sub-groups report remarkably similar patterns of candidate support across attributes. Perhaps most clearly, universalism and generosity appear to drive voter intentions, with respondents significantly more supportive of candidates who embrace generous, less restricted student debt relief. These results suggest that candidates who back robust student debt relief are poised to benefit most at the ballot box among Democratic leaning voters.

Study 2: Political benefits of executive action on debt relief

While the first study tested how policy details influence candidate support, a second study focuses more narrowly on the electoral payoff of executive action on debt cancellation with plans of varying generosity in 2022 and 2024. Scholars have found a clear correlation between policy benefits and political engagement (e.g., Campbell 2002), especially when the electorate can link policymaking to a particular governmental actor. The ability to attribute responsibility for policy action is particularly important for consumer lending (SoRelle 2022a), and perhaps especially for student loans, where government’s role has historically been hidden from the public (Mettler 2011). Yet, government’s responsibility for student loan policy was substantially revealed to the public during the highly visible blanket pause on payments and interest during Covid. Furthermore, Biden’s executive actions clearly link him to debt cancellation. If voters attribute student debt relief to action by the Democratic President, we expect this could have a mobilizing effect for Democrats in 2022 and for Biden himself in 2024.

Data and methods

We employed an information experiment—conducted as part of the larger survey described in Study One—to explore this question. Participants were told “President Biden is considering several options to cancel some or all federal student loan debt for existing borrowers. He has indicated that he will make a final decision this summer.” They were then asked, “If President Biden decides to [take a randomized action], how likely would you be to do each of the following?”: Vote in the 2022 midterm election in November, vote for a Democratic candidate for Congress in the 2022 midterm election, and vote to reelect President Biden in 2024. 3 Participants were randomly assigned one of five actions reflecting common plans for student debt relief: (1) take no action, (2) extend the repayment pause, (3) forgive $10,000 of student debt, (4) forgive $50,000 of student debt, or (5) forgive all student debt.

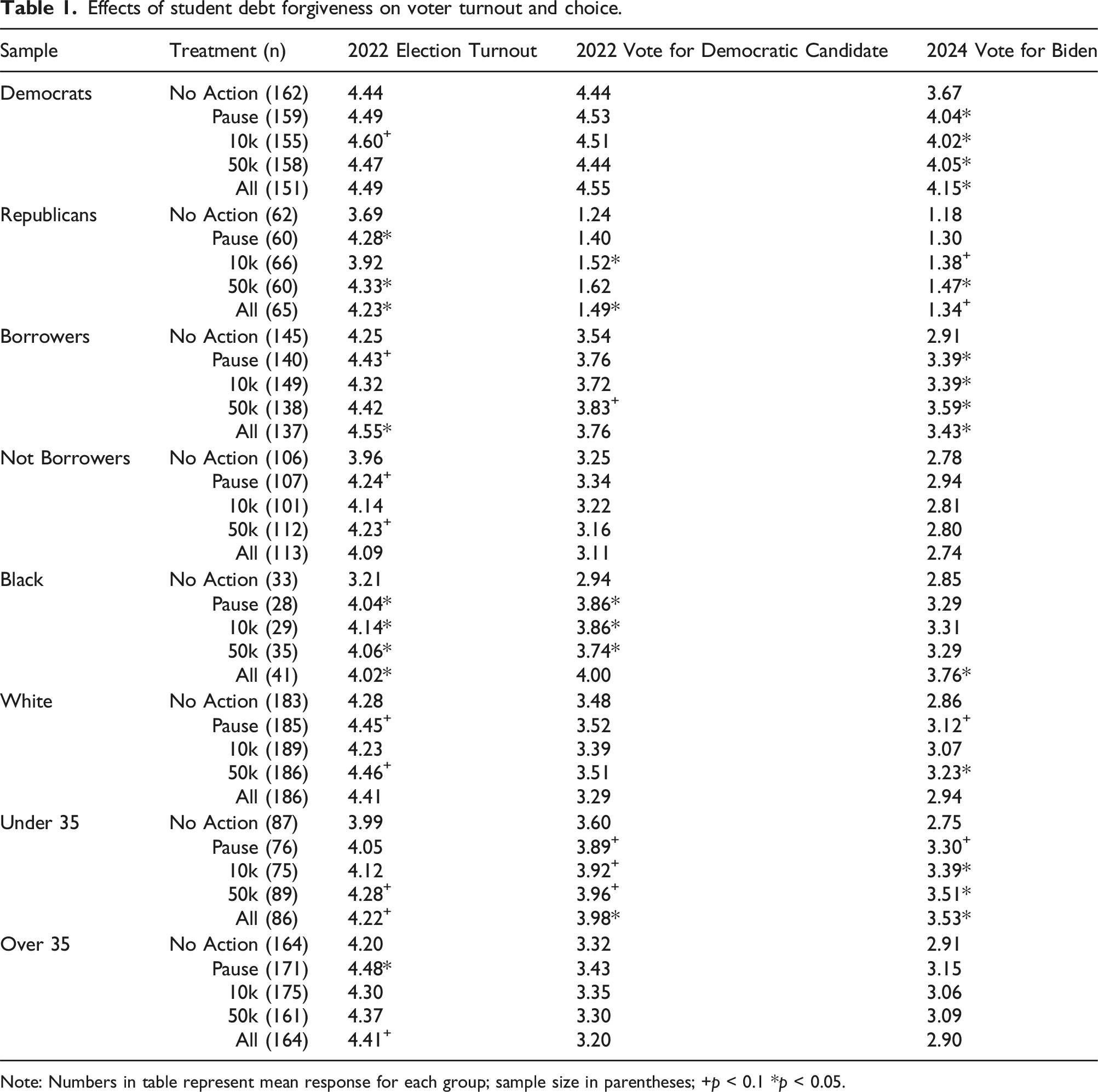

Effects of student debt forgiveness on voter turnout and choice.

Note: Numbers in table represent mean response for each group; sample size in parentheses; +p < 0.1 *p < 0.05.

Vote choice, however, is a different story. While Democrats in the control already reported very high intent to vote for Democratic congressional candidates in 2022, both young voters and Black voters indicated increased likelihood of supporting a Democratic congressional candidate in the midterm if Biden enacted any form of debt relief. Black voters become a full point more likely to support a Democratic candidate in the midterms when told Biden would cancel all outstanding student debt—moving from ambivalence to support—a substantively meaningful shift. Interestingly, while their level of support remains low, Republicans also reported a small but statistically significant increase in willingness to vote for Democratic congressional candidates in response to Biden canceling 10 thousand dollars of debt or more. Borrowers did not show an increased willingness to support congressional Democrats, but their baseline support was already high.

Biden received even greater benefits, consistent with the notion that being able to identify the responsible policymaker generates electoral rewards. Democrats, borrowers, and young voters all reported an increased willingness to reelect Biden in 2024 should he act on debt relief, and the magnitude of the effect was generally greatest when canceling 50 thousand dollars or more. The shift is substantively meaningful, particularly among borrowers and young people, who move from ambivalence, or even disinclination, toward Biden’s reelection in the control to reporting they are likely to vote for his reelection in each treatment group. Black voters similarly rewarded the president, moving nearly a full point from leaning unlikely to somewhat likely to vote for Biden in 2024, but only in response to full debt cancellation.

Collectively, this data suggests that both congressional Democrats and President Biden could benefit politically from enacting student debt cancellation, though the rewards may have been even greater for canceling at least 50 thousand dollars of student loan debt. For Black and young voters as well as borrowers—all groups implicated in Biden’s debt relief plan—the substantive effects of being told that Biden is taking action to relieve student debt are electorally meaningful: they correspond with an increase in intended support that, in many cases, moves respondents from being disinclined or ambivalent about Democratic candidates to reporting they are likely to vote for them.

Discussion and conclusion

While student loans have enabled generations of Americans to get an education, the resulting debt—exacerbated by declines in full-time employment and stagnating wages—has been tied to delays in marriage, childbearing, and homeownership among younger borrowers (Velez et al., 2019). Moreover, ballooning debt has expanded the racial wealth gap (Seamster and Charron-Chénier 2017). Thus, the substantive stakes of debt cancellation are tremendous. But so too are the political ramifications.

Our study offers both theoretical and practical implications for these emerging politics. First, we find experimental evidence that candidates' embrace of expansive student debt cancellation with few eligibility restrictions generates greater support among relevant constituent groups. From a theoretical perspective, this suggests that voter preferences and electoral rewards for student debt relief reflect a logic of universalism rather than targeted policy interventions for those deemed most deserving. Practically, this indicates that policymakers’ emphasis on preventing benefits from accruing unfairly to wealthier borrowers, and subsequent choices to tailor debt relief to those deemed most in need, are at best politically neutral choices for policymakers who seek political rewards from enacting debt cancellation.

Second, our results suggest that Biden’s executive action may be politically beneficial for Democrats. The practical implications of this are straightforward, but the theoretical implications suggest that visible student debt relief may spawn policy feedback effects that shape beneficiaries’ political engagement. While one might reasonably ask whether these results translate outside of the survey context, the midterm elections provided a real-world trial of our findings. While we cannot parse out precisely how much Biden’s proposal influenced the outcome (especially given the salience of abortion), at very least, the midterm results do not run counter to our findings. Furthermore, exit polling on student debt support and higher than expected Democratic and youth turnout in key races are consistent with the findings in this study—that debt relief may have helped curb the predicted midterm “red wave.”

Beyond the recent election, our results shed light on how the politics of student debt relief may unfold moving forward. While the fate of Biden’s current cancellation policy is in legal limbo, his other efforts to alleviate burdens through changes to the repayment process are ongoing. Our findings suggest how we might expect those regulatory efforts to translate to future political mobilization. If the court overturns Biden’s highly visible effort to cancel debt, we might expect the resumption of student loan payments to spark renewed demands for debt relief. In this circumstance, our findings offer direction for future policymaking on the issue, with generous, universal plans most likely to reap political benefits. If Biden’s cancellation policy remains in place, our findings imply he will not only have achieved a policy victory, but a political win as well—one that might boost his own reelection prospects while serving as a potential roadmap for the expansion of debt relief efforts to other emerging areas such as medical debt.

Supplemental Material

Supplemental Material - The political benefits of student loan debt relief

Supplemental Material for The political benefits of student loan debt relief by Mallory E SoRelle, Serena Laws in Research & Politics

Footnotes

Acknowledgments

We thank Abigail Williamson, Nicholas Carnes, Kristin Goss, and the anonymous reviewers for their generous feedback on this article. We also thank Trinity College and Duke University for providing faculty research funds for the study.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Correction (June 2025):

Supplemental Material

Supplemental material for this article is available online.

The files can be found at https://dataverse.harvard.edu/dataset.xhtml?persistentId=doi:10.7910/DVN/U6NNSY&version=DRAFT.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.