Abstract

This article surveys the effects of state hydrocarbon rents—defined as government income from oil and natural gas—on authoritarian survival and the onset of democracy. We also examine the association of changing state hydrocarbon rents with state spending and taxation based on a new collection of historical data, the Global State Revenues and Expenditures dataset. Using these novel data, we provide evidence that increasing state rents from oil and gas hinder democratization by reducing citizens’ tax burden. However, an increase in the oil and gas income flowing directly into state coffers does not appear to lower the average risk of ouster by rival authoritarian elites. We have found no evidence of the systematic distributional effects of state hydrocarbon income on regime survival.

Keywords

Introduction

Research on the (re)distributional foundations of rare political events depends heavily on the availability, quality, and consistency of historical state budget data. In this context, the literature addressing the impact of oil and natural gas income on the onset of democracy and the survival of authoritarian regimes is a telling example (Andersen and Ross, 2014; Haber and Menaldo, 2011; Herb, 2005; Morrison, 2009; Ross, 2001; Smith, 2004, 2015; Wright et al., 2015). Conceptually, this field of study assumes that hydrocarbon income generates greater independence from society for rulers, for two major reasons (Mahdavy, 1970: 466–467): 1 first, oil and gas income releases governments from taxing citizens, which in turn leads to lower demands for political representation; second, oil and gas income increases rulers’ capacity to spend resources on co-opting, bribing, or coercing pressure groups.

These core assumptions of rentier state theory have so far not undergone extensive empirical tests. One reason for this is the absence and inconsistency of budget data. The Global State Revenues and Expenditures dataset (GSRE) attempts to partially address this gap. In this article we introduce this new dataset and demonstrate some of its advantages compared to previously used sources. We further exploit this novel data, thereby contributing to the ongoing debates on the nexus of taxation, government spending, and state hydrocarbon revenues. Our findings supplement the existing literature on oil and gas income and regime type in three ways: first, the GSRE data provide suggestive evidence that increasing state rents from oil and gas hinder democratization, but may not impede autocracy-to-autocracy transitions; second, higher hydrocarbon rents appear to decrease the burden of direct taxation for citizens and businesses; third, the new data provide no evidence to support the claim that distributional strategies impact the survival of authoritarian rule.

We introduce the GSRE dataset in the next section of this article, highlighting its added value. We subsequently use the GSRE data to reassess and complement a recently published contribution on the nexus of oil and authoritarian survival by Wright et al. (2015). Our findings point to different relationships between authoritarian regimes’ state hydrocarbon rents and the likelihood of authoritarian survival and democratic transition. We conclude the article by discussing the impact of these findings for further research.

The Global State Revenues and Expenditures dataset

The GSRE dataset is based on recently released historical documents from the International Monetary Fund (IMF), and improves the coverage and accuracy of state budget data for many authoritarian regimes since the end of World War II. The GSRE dataset includes 39 unique indicators covering major aspects of state finance for 161 countries between 1946 and 2006. 2

The IMF Articles of Agreement 3 require member countries to provide information on various macroeconomic developments. Since the beginning of each country’s membership and on the basis of these obligations, staff missions from IMF regional departments have visited countries and prepared annual reports for presentation to the IMF Executive Board, which served as the source for developing the GSRE dataset. In the past, these reports were kept confidential and were for internal use only. In 2009, as part of the IMF’s effort to promote openness and transparency, these documents were made publicly available at the IMF Archives.

We have extracted all relevant historical state budget data from the available reports—which increase the data availability for non-democratic countries in particular—to build this time-series cross-section dataset covering the period 1946–2006. In general, the GSRE improves the coverage and validity of data on state hydrocarbon revenues, tax revenues, and state spending. The two subsequent sections explain the advantages and added value of the GSRE dataset in more details.

Data on oil and gas income as part of GSRE

In the literature on authoritarian rule and democratic transition, three main indicators are used to measure the impact of hydrocarbon income: first, data on hydrocarbon rents; second, hydrocarbon export values as a percentage of GDP; and third, data on per capita income from hydrocarbon production. None of them measures the true amount of oil and gas income controlled by governments. This is a shortcoming, which we have aimed to solve with the GSRE dataset.

First, World Bank data on hydrocarbon rents, as used for instance by Aslaksen (2010), are based on a calculation of average world prices minus average country-specific production costs (plus a normal return to capital) multiplied by the annual country-specific amounts of oil or gas production (Hamilton and Clemens, 1999: 339; The World Bank, 2015). These data, which have been available since the late 1990s, come with a number of more general problems: first, production costs for oil and natural gas are estimated only at average and not at marginal levels; second, production costs are often calculated at one fixed point in time; third, for many countries the average and fixed costs of neighboring countries are used; fourth, some countries sell hydrocarbons on domestic markets below world prices and therefore obtain comparatively less income. Overall, the World Bank data tend to overestimate the level of state rents for countries with higher-than-average production costs or high levels of internal usage, while they underestimate state rents for countries where production costs are below average. It is therefore hard to say how the data on rents are biased without knowing the country- or location-specific marginal production costs and the price levels on domestic markets.

Second, relying on the share of hydrocarbon exports as a percentage of GDP (hydrocarbon dependence), as most of the earlier literature in the field does (e.g. Herb, 2005: 20; Ross, 2001; Smith, 2004), creates additional problems. Hydrocarbon dependence very likely overestimates the influence of oil and gas in poorer and more conflict-prone countries (Ross, 2015: 242), since these societies are less able to absorb fuel production due to lower demand and the absence of refining capacity. From a conceptual point of view, it seems that hydrocarbon dependence is inadequate for measuring what the original rentier state theory proposed with regard to state–society relations: the idea that government-controlled resource rents free the government from societal pressure by permitting it to avoid taxation and/or feed citizens (or social groups) is an argument essentially based on individual preferences or calculations (Smith 2015). Therefore, indicators based on per capita values are conceptually more suitable to test for these relationships. 4

Third, Haber and Menaldo’s (2011) and also Ross’s (2012) data on oil and natural gas income are calculated by multiplying the volume of oil and gas production in each country-year by the respective unit value (Haber and Menaldo, 2010: 14–20). These data, often used in recent contributions (e.g. Andersen and Ross, 2014; Wright et al., 2015), systematically overestimate the true amount of hydrocarbon rents available to governments’ budgets since no country-specific or production-site-specific production costs are deducted.

Apart from the operationalization issue, all historical data on oil and gas income based on production or export levels suffer from an additional validity problem if they are used as a proxy for state hydrocarbon rents. They do not adequately cope with the most significant structural change on international oil markets. Between the late 1960s and the late 1970s almost all oil producers nationalized the oil companies operating within their borders (Andersen and Ross, 2014: 1000–1003; Ross, 2012). Previously, transnationally operating and vertically integrated companies had extracted the majority of rents. As a result of the new policies, national governments became the main recipients of massively increased oil and gas revenues. Data on oil and gas income based on the volume of production or exports does not adequately depict this shift.

Haber and Menaldo, however, do provide a more direct measurement of natural resource rents within government budgets. Their indicator of fiscal reliance—the percentage of government revenues from oil, gas, or minerals—includes taxes, royalties, dividend payments, or direct transfers paid by the resource sector to the government (Haber and Menaldo, 2010: 3). As they themselves admit, data on fiscal reliance is limited to only 16 major oil producers and is available only as a percentage of total government revenues.

Our GSRE dataset contains unique indicators of state rents from the production, export, and sale of oil or natural gas. State rents—defined as payments into the fiscal coffers of the state above the sum of unit production costs and a return to capital—are found at different places throughout government budgets. Many state rents are budgeted under non-tax revenues. For instance, oil royalties—either a fixed amount or a fixed share of income from the sale of each barrel of oil—are usually budgeted under this category. Also, revenues from transporting oil or natural gas, such as transport or pipeline royalties, are often added here. An exclusive focus on non-tax revenues, however, ignores the fact that primary-commodity-exporting companies—regardless of whether they are privately or state-owned—pay large amounts of taxes. This corporate taxation is most often budgeted under direct tax revenues. In some cases special export taxation on selected primary commodities exists; this is then budgeted under taxation from international trade. The GSRE state hydrocarbon rent indicators attempt to gather all of these different payments emanating from the production and export of oil and natural gas into a single annual amount. While this indicator tries to capture the official amounts of hydrocarbon rents, it potentially underestimates the amounts of rents available to governments, since it omits off-budget accounts (Ross, 2012: 59–62). 5 Strictly speaking, the GSRE data captures the minimum amount of hydrocarbon income a regime has at its disposal. We leave further discussions on more refined measurements using budget rent data and production rent data to future research.

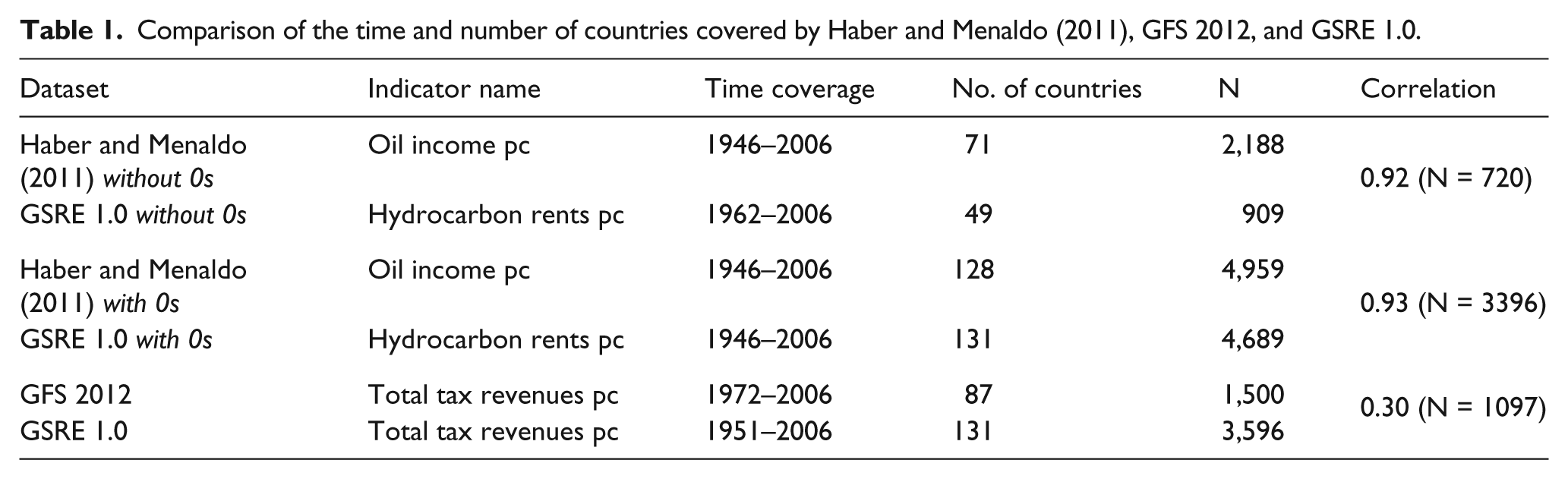

In Table 1 we compare the coverage of the oil income data from Haber and Menaldo (2011) with data on hydrocarbon rents from GSRE. In order to increase its coverage we add zeros to the GSRE data if two conditions are fulfilled: first, Haber and Menaldo’s data on oil and gas income signal that there was zero production of oil and gas in a given year and, second, no data for this year is available in the GSRE dataset. 6 Figures A-1 and A-2 in Appendix A provide a visual comparison of the two indicators with and without zero values.

Comparison of the time and number of countries covered by Haber and Menaldo (2011), GFS 2012, and GSRE 1.0.

Data on taxation and state spending as part of GSRE

So far, the IMF’s Government Finance Statistics (GFS) have been the exclusive source for the comparative analysis of taxation and state spending. Based on annual surveys completed by member states, the statistical department of the IMF collects data for GFS. In contrast, data from IMF staff reports, on which the GSRE dataset relies, are directly compiled by IMF regional departments during their annual country field trips. During these trips, IMF staff members visit the ministries and statistical departments of member states, discussing and negotiating economic and budget data with the responsible state officials. They therefore most likely gain a much better sense of the true value of the relevant economic and budget data. 7 We therefore believe that GSRE data based on historical annual staff reports are potentially more valid than data from GFS, though one could possibly argue that the different regional departments in charge of preparing the country reports could lead to inconsistencies in the data due to the slightly different application of accounting definitions in each regional department. Also, the GSRE covers a longer time span, as the GFS data start only in the early 1970s and no alternative source exists that goes back to the end of World War II.

Table 1 compares the same indicator (total tax revenues) from the 2012 version of the GFS (International Monetary Fund, 2012) and the GSRE dataset. The number of countries covered by GSRE is much higher and the new dataset extends over a much longer period of time. Figure A-3 in the Appendix provides a direct comparison of the number of observations for the indicator from the two different datasets.

Empirical application using the new GSRE data

In this section, we examine the influence of state hydrocarbon rents on authoritarian survival and the onset of democracy using the GSRE data. We first investigate the direct effects of oil income and state rents within state budgets on the likelihood of regime breakdown, replicating a recent study by Wright et al. (2015). In a second step, we test whether state rents from oil and gas have reduced taxation revenues or have led to higher average state spending on wages, social welfare, and military expenditures.

Effects of oil and gas rents on authoritarian survival and the onset of democracy

Do state rents from oil and gas impact the persistence of authoritarian regimes? Wright et al.’s (2015) study is the first to disentangle the effects of oil and gas using more fine-grained measures of political regime transitions. Based on their previously published data on authoritarian breakdowns (Geddes et al., 2014), the authors distinguish between autocracy-to-autocracy transitions (authoritarian transition) and autocracy-to-democracy transitions (democratic transition) and aggregate both types of transitions in the variable all regime failures. To measure the impact of oil and gas, Wright et al. (2015) rely on Haber and Menaldo’s data on oil and gas income per capita (2011). In the following section, we replicate their main specification and then substitute the Haber and Menaldo data with data on state hydrocarbon rents from GSRE.

In their empirical analysis, Wright et al. (2015) use a logistic regression model by allowing the intercept to vary by country and also control for both between-country and within-country effects. Equation (1) in Appendix B presents the functional form of this approach and describes its elements.

The main independent variable is total oil and gas income per capita from Haber and Menaldo (2011). As an alternative we apply the GSRE indicator of state hydrocarbon rents. The correlation between the two rents’ indicators is very high, with 0.97 for the respective means and 0.82 for the deviations from these means. Since GSRE original data are collected at current levels in local currencies, the data are divided by current GDP in local currencies and then multiplied by GDP per capita in 1990 international dollars per capita from the Maddison data project (Bolt and van Zanden, 2014).

As for our controls, we use the same indicators as those used by Wright et al. (2015), which are GDP per capita from the actual version of the Maddison project, a binary variable for civil war based on the most recent version of the UCDP/PRIO data (Gleditsch et al., 2002), and a variable of democratic transitions in neighboring countries in a given year. 8 All independent variables and controls are decomposed in a between- and within-country effect with the exception of the time periods, civil war, and democratic transitions. The GDP data, the oil income, and the state hydrocarbon rents variables are calculated as natural log.

Table 2 presents the regression results. The model specifications 1, 4, and 7 directly replicate the results presented in Wright et al.’s Table 1 (2015: 297). However, our results—which are based on the same sample and use the new GSRE oil and gas rents indicator in specifications 2, 5, and 8—challenge parts of Wright et al.’s findings. In line with their original results we find that for all regime failures, both the within-country and between-country effects indicate that state rents from oil and gas decrease the likelihood of breakdown (specification 2 of Table 2). Using oil and gas rents that flowed directly into state coffers, our estimations signify no statistically significant influence on autocracy-to-autocracy transitions (specification 5), whereas higher income from state hydrocarbon rents within as well as between dictatorships decreases the likelihood of democratization significantly (specification 8). Since GSRE data on hydrocarbon rents have a lower coverage, in specifications 3, 6, and 9 we again use the Haber and Menaldo data on oil income to rerun regressions based on samples estimated with GSRE data in order to rule out the possibility that our results relate to the smaller sample size. It is clear from our results that using the new GSRE data at least in some specifications yield to findings that challenge Wright et al. (2015). While it remains unclear from the specifications estimated in this paper whether our non-finding for autocratic transition (specification 5) depends on the advanced measurement of state rents or the shrunken sample size, we can plausibly assume that the negative significant relationship between GSRE hydrocarbon rents and the onset of democratic transition relates back to the new GSRE data on hydrocarbon rents. Estimations using rent indicators without zero values confirm this finding, even though the number of transition periods is then drastically reduced. Finally, repeating all estimations by using linear probability models does not change our major findings as presented in Table 2. 9

State hydrocarbon rents, authoritarian survival and the onset of democracy.

p-values in parentheses: + p<0.10; * p<0.05; ** p<0.01.

Notes: Logistic regression with standard errors clustered in countries in parentheses. Model 2 is estimated based on the sample of Model 1. Model 3 is estimated based on the sample of Model 2. The same logic applies for authoritarian (models 4 to 6) and democratic transitions (models 7 to 9). All models include time dependence polynominals, calendar time trends, and the following controls: civil war, democratic transition in neighboring countries, and GDP pc ln. The latter is decomposed in a between- and within-country effect. Complete results are shown in Appendix B: Table B-3.

Effects of oil and gas rents on state spending and taxation

How do oil and gas rents prevent democratization? One way to answer this question is to analyze how changes in state rents may affect tax revenues and state spending. Following the conventional empirical strategies used in the literature (e.g. Morrison, 2009; Wright et al., 2015), we analyze, in a second step, which of the two major mechanisms might be relevant in reducing the likelihood of democratization—that is, whether higher hydrocarbon revenues lead to lower taxation, which could then be interpreted as having reduced demands for political representation, or whether higher oil and gas rents lead to increased state spending to co-opt, bribe, or coerce pressure groups. Using fixed-effects error-correction models, we test how changes in hydrocarbon state rents influence the level of (1) total, (2) direct, (3) income, (4) corporate, and (5) indirect tax revenues. 10 We also test whether higher oil and gas rents lead to higher total expenditures (6), more expenditures for security (7) and public wages (8), or increased welfare spending (9). Equation (2) in Appendix C presents the functional form of our estimations and adds some explanations to its elements.

Wright et al.’s analysis again serves as the best practice for our estimations. In particular, we use the following similar variables: 11 our dependent variables are the first-difference values of the respective logged spending and revenues indicators in per capita values from the GSRE dataset. We also control for the one-year lagged and logged value of the dependent variable on the right-hand side. Our indicator for oil and gas rents from GSRE is the same as that used before. As controls, we include data on civil and interstate war from the most recent version of the UCDP/PRIO data (Gleditsch et al., 2002) and three additional controls: democratic transitions in neighboring countries, GDP per capita, and regime duration. In all specifications a general and a quadratic time trend is interacted with country-fixed effects.

Table 3 presents the estimation results. Specifications 1 to 5 report on the changes in taxation, and specifications 6 to 9 look at changes in relevant state expenditures. Across the different estimations, only three short-term changes and one long-term change in state hydrocarbon rents can be significantly associated with the first-difference change in the dependent variables. All of these associations relate negatively to forms of direct taxation. This means that per capita increases in state hydrocarbon rents from one year to the next have led to a short-term decrease in the per capita amounts of direct (specification 2), income (specification 4), and corporate taxation (specification 5). These effects are significant at least at the 90% level and their size is relevant. If the logged first-difference per capita values of state hydrocarbon rents increase by one standard deviation of the estimated sample, the respective logged per capita amounts decrease by 11.89% for direct taxation, by 9.35% for income taxation and by 14.15% for corporate taxation. The negative long-term effect of 18.26% for corporate taxation in specification 5 highlights the relevance of the overall negative association between state hydrocarbon rents and per capita values of direct taxation. State hydrocarbon rents do not significantly impact spending for security when the new GSRE dataset is used.

Hydrocarbon rents, tax revenues and government expenditures.

p-values: + p<0.10; * p<0.05; ** p<0.01.

Notes: OLS with robust standard errors clustered by country in parentheses. All models include Δ regime duration, regime duration t-1, and a general and a squared time trend interacted with country-fixed effects.

Overall, these results sow doubts about Wright et al.’s findings that oil bolsters autocratic survival through the co-optation of “challengers in the officer corps by buying new weapons, raising military wages, and providing other benefits” (Wright et al., 2015: 301). In Appendix C: Table C-1 we present results from additional estimations. If GSRE hydrocarbon rents are estimated with COW data for military expenditures, which is what Wright et al. used, only a limited significant relationship exists for the sample used in specification 7 of Table 3 in the long-term equilibrium. When we regress COW data on all available hydrocarbon rents from GSRE, no statistically significant influence at the 10% level can be identified. In addition, our estimations in Table 3 do not support alternative mechanisms of material co-optation through, for instance, the provision of social welfare or employment in the public sector, which previous studies on the redistributional strategies of authoritarian regimes (e.g. Bank et al., 2014; Morrison, 2009) have identified.

Conclusion

This article has introduced the GSRE dataset, which offers researchers unique and detailed data on hydrocarbon state rents, disaggregated tax revenues, and state spending items for 161 political regimes between 1946 and 2006. The main contributions of our data collection are, first, greater data availability and coverage for non-democratic countries and, second, a refined measurement of oil and natural-gas income. Therefore, this new dataset enables us to examine the impact of state hydrocarbon rents on autocratic survival more closely. The application of this new data in this paper at the nexus of oil and gas income and regime change has yielded several interesting conclusions:

First and foremost, our analysis provides evidence that state hydrocarbon rents controlled by dictators help prevent authoritarian regimes from the onset of democracy because petro-autocracies systematically rely on lower direct taxation of their citizens. No representation without taxation, one of the buzz phrases of early rentier state theory, appears indeed to be among the prevalent mechanisms explaining the absence of democratic onsets among resource-rich authoritarian states. As our separate estimations for revenues from income and corporate taxation indicate, this seems to be relevant for citizens through income taxation and for companies by way of corporate taxation.

Second, more analysis of the supply side of rentier state theory and what state spending means for authoritarian survival needs to be undertaken. Whether dictators reduce their vulnerability through the use of oil and gas wealth—assuming that it flows into state coffers—by, for instance, co-opting, bribing, or repressing societal pressure groups appears to be more questionable than recent studies such as Wright et al. (2015) suggest. Our analyses using the novel GSRE data casts doubt on these claims, and it is possible that authoritarian supply strategies vary in important ways across regime type, time, and region.

Key to all future analyses is valid and reliable data on state budget items. The new GSRE dataset contributes in this respect by addressing some of the existing gaps in the available data. It is, however, only the first step on a longer road to better understanding the (re)distributional foundations of rare political events.

Footnotes

Acknowledgements

We highly appreciate very helpful comments and suggestions by two anonymous reviewers and Kristian Gleditsch. We further thank Joseph Wright, Erica Frantz and Barbara Geddes for sharing their data with us.

Author’s note

Declaration of conflicting interest

The authors declare that there is no conflict of interest.

Funding

We gratefully acknowledge the generous financial support by the German Research Foundation/Deutsche Forschungsgemeinschaft (DFG) with a grant (RI-2023/2-1) for generating the GSRE 1.0 dataset.

Supplementary material

Notes

Carnegie Corporation of New York Grant

The open access article processing charge (APC) for this article was waived due to a grant awarded to Research & Politics from Carnegie Corporation of New York under its ‘Bridging the Gap’ initiative. The statements made and views expressed are solely the responsibility of the author.