Abstract

Morocco is an African country containing a very large market for e-commerce, which further expanded during the 2020–2022 COVID-19 pandemic. However, a few obstacles, like low internet penetration and lack of digital payment systems, are acting as obstacles for the local e-commerce service providers to reach potential in the country. Chari is one such B2B company whose operations changed the landscape of logistics and distribution among the FMCG businesses in Morocco. The company also exercises a B2B2C model, which it achieved through acquiring Karny.ma and Axa Credit, enabling its customers to use a lending and financial transaction tracking model. However, the industry is quite competitive, with offline retailers like TradeDepot, WaystoCap (acquired by MaxAB), and Sokowatch deciding to exploit the possibilities online. Apart from the rising competition, Chari still faces challenges in additional expansion due to the improper and inadequate infrastructure of the country. However, if it can overcome the external threats and utilize the geographical location of Morocco to its advantage, Chari has enormous potential to flourish both locally and globally.

Introduction

With a revenue of USD 1.4 billion, Morocco placed to be the 60th biggest market in e-commerce in 2021, ranking before Angola and after Slovakia. Morocco with a rise of 21%, contributed about a 15% to the growth of the global e-commerce market in the year 2021. The Moroccan e-commerce market is anticipated to grow till 2025 and has a forecasted compound annual growth rate of 8%. Huge portion of the Moroccan e-commerce sector is dominated by Electronics and Media segment with a contribution of 32% followed by Fashion segment with 26%, Furniture and Appliances segment with 17%, Toys, Hobby and DIY segment with 14%, and lastly Food and Personal Care segment with 11% (ecommerceDB, n.d.). Amid the global pandemic, the e-commerce sector of Morocco witnessed a considerable increase in 2021, where the transaction volume in Moroccan e-commerce websites climbed by 48%, and the sum of money spent rose by 30% compared to 2020, which was a result of the boost in the internet penetration of the country. The rise in internet penetration catalyzed the enlargement of Moroccan-based e-commerce websites from 300 to 1000. A rise in the demand for products from Asia mainly connected to e-commerce has also increased the demand for the distribution of large carriers that require modern infrastructure like Tanger Med Port. 1 Likewise, one of Morocco’s strongest suits is its road network which is essential for good quality roads to allow the products to be delivered quickly and allows e-commerce businesses to deliver to rural areas in the country. The strong port and road network allow Morocco to have excellent logistic capabilities (Sinclair, 2022). However, with only 17% of Moroccans above the age of 15 using the digital payment system and only 1.6% of the citizens buying products and services through the internet, the lack of internet penetration is acting as an obstacle for the industry to reach its full potential. Due to the lack of internet penetration and the prevalence of improper digital payment infrastructure, Visa partnered with Interbank Monetary Center (CMI) 2 to launch a business-to-business (B2B) digital payment system that will allow smoother cash flow between businesses with the usage of platforms like PayByMail and Android smart terminals. Apart from the digital payment system blockade, the e-commerce sector in Morocco had to deal with the “trust issues with e-commerce consumption within the Moroccan population” pre-pandemic. Moroccans were not enthusiastic about conducting online businesses, resulting in only about 2% of the retail store operating their businesses as e-commerce (Sinclair, 2022).

Fintech industry in Morocco

Morocco’s position in the fintech industry is ahead of the rest of the countries in Africa in terms of gross domestic product (GDP) and larger infrastructure advancements. Banks cover a significant portion of the country’s financial system with two major banks in Africa being Groupe Banque Populaire 3 and Attijariwafa. 4 The banks are playing significant roles in contributing to the innovation in this sector. A number of financial institutions is bringing in their own technologies to provide customers with the services similar to that of fintech and start-ups. Moreover, the traditional banks are utilizing digital technology to provide customers with fintech services like mobile banking and other digitalized platforms (Santosdiaz, 2022). Among the various subsectors in the fintech industry in Morocco, payment, point-of-sale (POS), and remittance are the most advanced. Other sectors prevalent in the fintech ecosystem in Morocco are crowd funding (process of funding an arrangement by collecting money), personal financial management, data analytics, and lending. Additionally, Morocco plans on launching banking framework. Currently, the country has a financial service industry data protection framework and a financial service industry cybersecurity framework and also has conventional consumer protection laws containing clear provisions in terms of financial services. Furthermore, since 2017, Morocco has prohibited the usage of cryptocurrencies for any sort of transaction but there is a huge fanbase of crypto among Moroccan citizens and the country is one of the most significant countries around the world to perform in crypto trading internationally (Santosdiaz, 2022)

Chari: An overview

Ismael Belkhayat and Sofia Alj co-founded a B2B company named Chari to provide the local Moroccan store with the option to order their required stock of products. The start-up initiated its journey with the aim of changing the landscape of logistics and distribution among the businesses in Morocco. Using Chari, the local shops owners are able to order the things that they need for their shops at reasonable prices and get it delivered for free within 24 h. Around 15,000 users have registered on their app Chari.ma in 2020 where it was found that about 5,000 users have used the app at least three times to order products. Chari used to operate using only one warehouse located in Casablanca which is used to cover the whole Rabat-El-Jadida 5 area but recently has opened another warehouse in Tangiers 6 which is used to deliver products to the northern part of the country (Berrada, 2021). The start-up is valued at USD 20 million and was successful in making Y Combinator and France Orange to invest in the company. Chari currently operates a fleet of 20 trucks which makes its operations extremely efficient. The application for Chari was developed in-house and for the technology that was available, optimization of everything including transport costs was also possible which allowed them to deliver more orders quickly Chari’s main aim is to provide a platform for the small retailers in Morocco and Tunisia where they will be able to order and acquire products from multinational and local fast-moving consumer goods (FMCGs) manufacturers (Berrada, 2021).

Business model

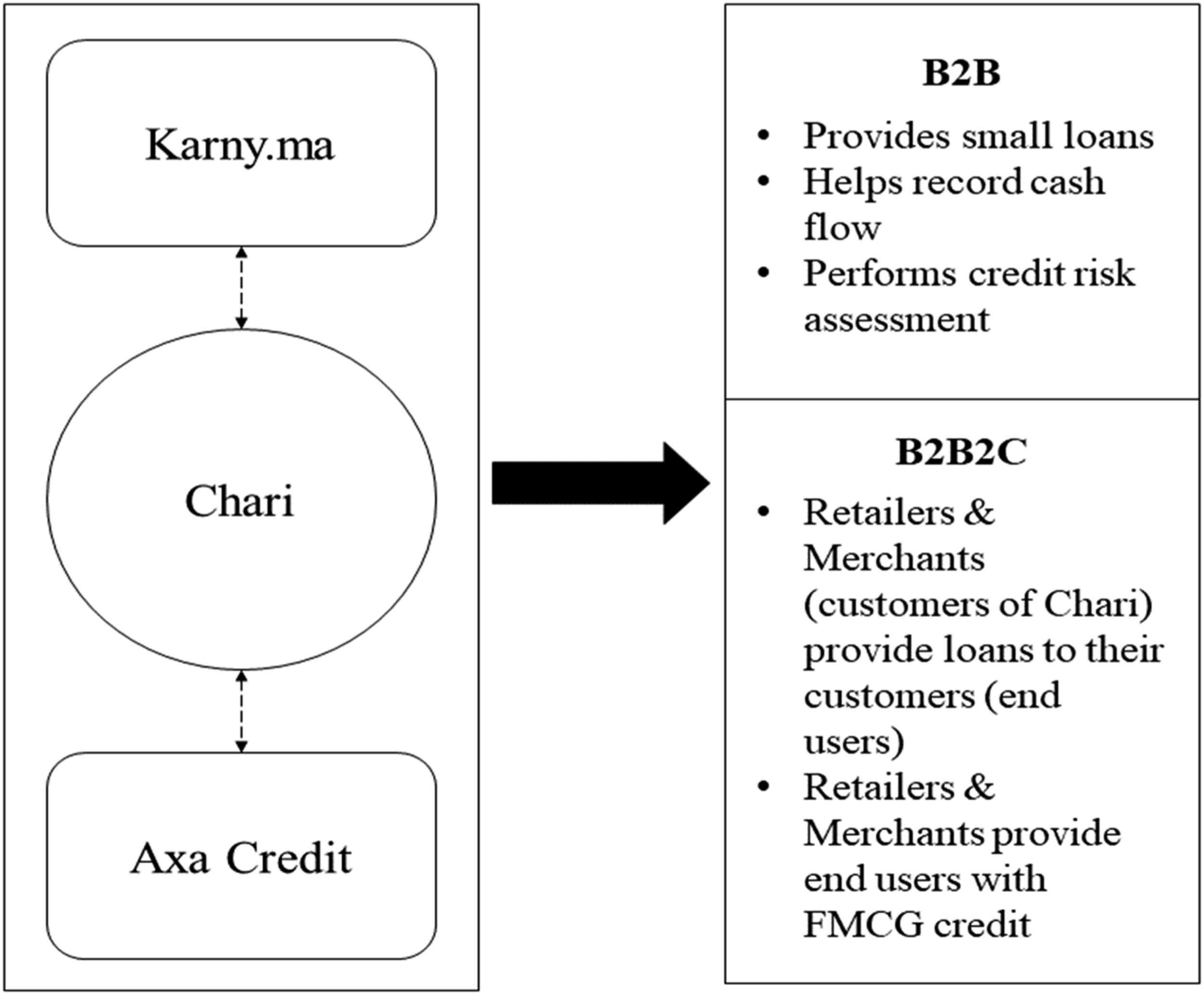

The company operates using both B2B and business-to-business-to-consumer (B2B2C) model. In 2021, Chari acquired Moroccan credit book Karny.ma 7 which allowed about 50,000 merchants to keep track of the credits they provide to their customers. Chari also acquired Axa Credit 8 which makes the company one of the few Moroccan start-ups to attain the local branch of a global bank. A significant percentage of the population in Morocco are either “unbanked, underbanked or unable to prove recurring income” and as a result they are not being able to get loans as some form of financial stability to needs to be shown which is quite impossible without proper bank accounts. So, Chari wants to serve this segment of the population with the help of Karny through which the start-up will provide the small retailers with loans by using the platform Karny to record cash flow in and out of their businesses (Kene-Okafor, 2022).

Incorporation of fintech technology

With the acquisition of Axa Credit, Chari offers its FMCG B2B clients with loans which can also be used by them to lend money to their customers which make the company operate under a B2B2C (as shown in Figure 1) lending model as well. Chari is confident that it knows about the consumption habits of its clients which allow them to perform the credit risk assessment which a standard bank is unable to do. Besides providing loans, the retailers and merchants can also provide the customers with FMCG on credit. As a result of offering the loans and products on credit, the merchants act as branches and provide the same services to their end customers which allows the underbanked population to “play on a level field” with the ones with bank accounts. The merchants on the Chari platform are provided with free credit line and the costs are allocated through FMCG suppliers as high distribution margins. In exchange for that the suppliers are provided with data about the Stock-Keeping Units (SKU) that they are selling to the individual stores. Higher credits lines are provided to retailers who provide loans to the end consumers. As a result, Chari shares the data collected through Karny about end consumers’ purchasing behavior with the FMCG companies paying for the higher loans (Kene-Okafor, 2022). Dual business model through acquisition Source: Authors’ own creation.

Competition

The landscape that Chari is operating in is highly competitive. Companies like TradeDepot, WaystoCap (acquired by MaxAB), and Sokowatch were offline retailers who decided to exploit the online opportunities and bring their businesses to the online platform. MaxAB is an Egyptian B2B e-commerce company that entered the Moroccan e-commerce industry by acquiring a local company named WaystoCap. MaxAB is a platform that enables users to buy food and grocery. The company was looking for ways to expand into the Middle Eastern and African regions, where it came across WaystoCap. WaystoCap is a cross-border trade platform that enables goods to be transacted within Africa. The company took its cross-border services to the Ivory Coast and Togo regions in West Africa, which allowed it to process transactions worth $3 million every quarter. Since the business model of WaystoCap and MaxAB coincided, the latter decided to acquire them and expand into Africa (Kene-Okafor, 2021). Additionally, TradeDepot is an FMCG platform based in Lagos. The company provides B2B products and services through its mobile platform that helps the retailers in developing markets and economies connect directly to the consumers good brands which, as a result, enables them to order their desired products and get it delivered. TradeDepot differentiates itself by allowing the suppliers to save up to 25% of the costs in their delivery logistics which the traditional route-to-market companies tend to do. This allows the company to provide the small retailers with reliable products needed to run their businesses at the best prices available in the market (Digest Africa, n.d.). Furthermore, Sokowatch is another B2B company operating in the Africa e-commerce industry. The business model of the company put focus on what the larger portion of the African consumers tend to buy. The local family-run retailers face difficulties when the supply runs out in the last minute and ordering through the traditional offline methods takes ample amount of time which restricts the retailers to cater to the customer’s demands. To bridge the gap, Sokowatch orders on behalf of the retailers while also financing their purchase and providing the retailers with delivery on the very same day. However, their category of products is not vast and only offers the required staple products (Whitehouse, 2021).

Setbacks and challenges

One of the biggest problems that Chari faces is its potential value expansion. The Moroccan infrastructure is not set up that enables the country’s e-commerce segments to operate at their full potential, which is visible with the lack of digital payment systems and payment practices in the country. The World Bank reports that only a handful of 17% of the population above 15 utilizes digital payment systems. Additionally, it is also noted that only 1.6% of the entire population buys products and services online. The data only portrays the vast gap that is present in the market and the potential for growth in penetration in the e-commerce sector that Morocco can tap into (Sinclair, 2022). Even though Morocco has taken initiatives to build up a digital payment infrastructure in the country that will enable its population to have several payment options, a significant portion of the Moroccan population needs to be reached as the internet penetration is not that high. Most e-commerce sellers still prefer cash-on-delivery as a viable payment option. But there are other issues that Moroccan e-commerce companies are facing as well. Customers purchasing through the online platform have a history of trust issues when shopping digitally. Before the pandemic, this was one of the reasons Moroccans used to think conducting business online was “too risky and not advisable.” The attitude among the population is very clearly seen, with only 1.6% of the population adapting and using the digital medium to shop. Currently, this number only increased to 2%. With the whole world adapting to e-shopping, such a low percentage shows how much behind the country is with its technology (Sinclair, 2022).

Future

One of the strongest suits of Moroccan geography is its robust access to ports and a good network of roads within Africa. One of the most vital things for e-commerce is a good road network, as it enables businesses to deliver goods faster within the country and gives access to remote locations like small villages. The strong port access of 40 African ports connected through Tanger Med port enables Morocco to gain complete access to different points in Africa. Chari can exploit the geographic setting of Morocco to serve its customer better and increase its brand value which will, as a result, enable them to build more vital trust by living up to its promises (Sinclair, 2022). The three essential foundations in building strong e-trade are “a modern, reliable and affordable telecommunications infrastructure, an open, transparent and predictable business environment, and the availability of high-skilled human resources.” The Moroccan government’s allocation of funds for improving digital infrastructure by enhancing internet penetration can help the country exploit the high-potential e-commerce sector. Moreover, businesses operating in the e-commerce industry need to maintain transparency with their customers, which can help build the trust that is lacking among them. Moreover, providing adequate training to the population who can utilize their skills to cater to the market needs is also vital for Morocco and its e-commerce businesses like Chari to flourish in the country and compete globally (International Finance Corporation, 2019).

Suggested discussion questions

1.In your view, how well developed is the Fintech industry and markets in Morocco today? 2.What are the ways in which Chari delivers its services? 3.Explain the competitive environment in which Chari is operating in. 4.How can the company overcome some of its challenges? 5.What can other economies learn from the Moroccan experience?

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project received financial support from InterResearch, Bashundhara, Dhaka, Bangladesh.