Abstract

This case details the evolution of the Hyperlocal Grocery Delivery Industry in India and a comparative analysis between Dunzo and Blinkit. The case describes the macro and industry level imperatives, growth drivers and competitive dynamics, and the resultant evolution of alternate business models. In an emerging economy context traditionally characterized by institutional voids, technological and infrastructural challenges, and a lack of entrepreneurial resources, the evolution, proliferation, and growth of the Hyperlocal Delivery business model makes for an intriguing story. We intend to make readers aware of the industry dynamics and allow them to use strategy, technological innovation, and the fundamentals of platform businesses frameworks from strategy, innovation, and platform businesses domains to evaluate the value proposition and offering that these firms have for consumers and the operational model to craft winning strategies in this emerging industry.

Keywords

Introduction

The quick commerce grocery industry rose to mainstream popularity during the Covid induced lockdowns of 2020 and 2021. Consumers are increasingly embracing this pandemic-induced necessity as a matter of convenience. The trend has caught the eye of the investor community, with billions flowing into the industry as existing players struggled to cope with the explosion of demand caused by lockdowns. The year 2021 saw investments to the tune of $ 14 bn (INR 1043 bn approx.) into this space. Globally, the space saw the rise of companies attempting to satisfy consumer demand within minutes (Kamel, 2022). The rush of money towards this space will impetus the players to expand and scale in the short to medium term. However, there remain long-term structural issues related to the economics of grocery delivery. The business model is still evolving. Players are looking to improve the unit economics by improving their average order value by adding higher-value products such as health and beauty products, specialty foods, seasonal products, and select non-food items. Companies are also attempting to reduce costs through direct sourcing from manufacturers, retail sourcing collaborations, and increasing the share of private-label goods.

In India, quick commerce grocery delivery services also saw a significant uptake in urban areas, particularly in the metro cities of Bengaluru, Delhi, Mumbai, and Chennai during the Covid lockdowns. The rush to satisfy consumer demand has significantly increased the competitive rivalry in the industry, with significant players Zepto, Reliance-backed Dunzo, Swiggy’s Instamart, Zomato-backed Blinkit, and Tata-backed Big Basket entering the foray (Bhalla, 2022). Swiggy entered the space in August 2020 through the launch of “Swiggy Instamart” (Swiggy Website). Zomato also announced its entry into the quick commerce space with the launch of “Zomato Instant” (Business Today, 2022). In a share-swap deal, Zomato acquired Blinkit for INR 4447.48 crores 3 months after this launch (PTI, 2022). Considering that the recent market signals indicate Dunzo edging over Blinkit, what should Dunzo do to retain this lead?

Evolution of grocery retail in India

India is home to the world’s third-largest grocery retail market, with sales of $ 410 bn (INR 30,074 bn approx.) in 2020 (Euromonitor, 2022). Traditionally, Kirana stores or the unorganized hawkers/neighborhood shops have dominated this sector. The Kirana stores account for the bulk of the market in sales (about 90%). Modern grocery retailers and e-commerce players comprise the rest of the market (Patil et al., 2021). The Indian Digital Grocery Retail Market has risen exponentially, with an annual growth rate of over 50%. The Indian Digital Grocery Retail Market size is projected to grow from $ 10 bn to $ 12 bn (INR 744 bn to INR 892 bn approx.) by 2025 from the estimated $ 2 bn to $ 3 bn (INR 147 bn to INR 220 bn approx.) in 2020 (Mckinsey & Company, 2022). The customer base is currently from mid-to-high affluent households from the top six or seven metros and is expected to make up 60% of the market (Mckinsey & Company, 2022).

Customer value proposition and evolving landscape

In terms of customer value proposition, local Kirana and brick & mortar retailers provide product sampling and personalized service, which is considered essential by a large segment of consumers, especially for high-value food items. In comparison, e-commerce players aim to satisfy the consumer demand for convenience—most large brick & mortar retailers today attempt to become omnichannel by establishing marketing channels through e-commerce. Reliance Retail is establishing its presence with JioMart and trying to build an ecosystem of Kirana stores. Discount Retailer “Avenue Supermart” has also entered the online space with an online platform named “D Mart Ready.” The platform offers grocery, baby, sanitary, and personal care products (Dmart, 2022). Future Retail’s Big Bazaar has also announced that it will provide a two-hour home delivery service starting with Mumbai, Bengaluru, and the National Capital Region (Tandon, 2021).

The advent of hyperlocal grocery delivery platforms has not rendered physical stores obsolete. A Bain & Company survey showed that 93% and 89% of grocery shoppers used both channels in France and China, respectively (Kamel et al., 2022). The omnichannel players exhibit a much greater awareness and knowledge about the variety and depth of consumer needs. Hyperlocal delivery platforms currently struggle to offer the same type and depth owing to the fewer stock keeping units (SKUs) they can offer compared to a traditional omnichannel player. Omnichannel shoppers, that is, who tend to purchase both online and offline, have also been found to have a higher monthly spend and higher margin realizations compared to shoppers who buy either solely online or offline.

Supplier management is a critical area of strength for omnichannel players. Big players in the consumer-packaged goods market typically enjoy a better margin when supplying omnichannel grocers. The margin can generally be anywhere between 17 and 22% of operational earnings. This is much more than what Consumer Packaged Goods (CPGs) earn from other online distribution channels. This asymmetry in benefits leads to CPGs providing attractive terms, more competitive prices, and priority restocking to omnichannel incumbents. Despite the advantages that omnichannel incumbents have over hyperlocal grocery delivery players, it is still advisable for them to stay alert to these new players. The new players are built around the twin pillars of the unique retail experience, that is, logistics and data. The ability to leverage insights gained about consumer behavior from data can help new players become more adept at offering desired service levels to consumers. This can neutralize the advantage of consumer intimacy that incumbents enjoy. Further, the agility of new players in terms of working and infrastructure makes them a threat.

Retail business models

Broadly, retail business models can be categorized into three types: Inventory Led Model, Marketplace Led Model, and Hyperlocal Led Model. Under Inventory Led Model, the retailer procures and stores a wide range of products in bulk. Traditional retailers such as Reliance Retail, D-Mart, and Spencer’s Retail used to operate under this model. The rise of digital applications and smartphone penetration led to the rise of platform-based businesses in India and across the globe. In the retail sector, marketplace models provided a platform for third-party vendors to list and market their products. Companies like Amazon and Flipkart operate under this model in India. The marketplace model has further evolved into a Hyperlocal Model, wherein companies intend to serve customers in a small geographical area through a locally situated fulfilment center within a very short (generally less than an hour) distance. Major hyperlocal players in India are Blinkit, Dunzo, Swiggy’s Instamart, and Zepto.

Quick commerce business models

Quick Commerce Business Models are a typical result of the convergence between retail, logistics, and technology. The business models of different Quick commerce players are Standalone Quick commerce players, Restaurant Aggregators and E-Grocery Players. Standalone Quick commerce players are specialized commerce platforms where consumers are satisfied through micro fulfilment centers. Key Indian players within this segment are Blinkit, Dunzo, and Instamart, while the key global players are Gorillas and GoPuff. Restaurant Aggregators follow the marketplace model where the aggregator acts as a middleman between restaurants and customers while providing delivery services through the delivery fleet. Key Indian players within this segment are Zomato and Swiggy, while Key Global players are Doordash, Pandamart and Getir. E-Commerce Horizontals are e-tailing players operating on a delivery model with slotted deliveries and movement between first and last-mile connectivity. Key players in this segment are Amazon and Flipkart. E-Grocery Players are slotted/scheduled grocery delivery players having order processing from centralized warehouses. Total order to delivery time ranges from 2 to 6 hrs. Key Indian players within this segment are Big Basket, and Zepto, while Key Global players are Instacart and FreshDirect.

Macro environment

The Covid induced lockdowns provided a once-in-a-lifetime opportunity for hyperlocal grocery delivery companies, with consumers both reluctant and, in some instances, unable to move out of their homes for essential grocery and FMCG purchases. Hyperlocal grocery delivery players tried to rise to the challenge and focused intently on consumer and supplier problem-solving. The big question, however, remained as to whether the consumer behavior impacted by lockdowns will continue post-lockdown. The question can be primarily answered considering that the number of hyperlocal commerce shoppers is expected to reach 214 million at the end of 2022, growing at 2% (Maloo, 2022).

The Indian government has taken initiatives to ease access to credit and capital and promote digitization. Several prominent schemes have been launched to encourage innovation and promote start-ups. “Startup India Seed Fund Scheme” has been launched to provide financial support to new-age ventures for proof of concept, developing prototypes, product trials, market entry and commercialization. “Startup India” is another initiative wherein eligible companies recognized by Department for Promotion of Industry and Internal Trade (DPIIT) are provided benefits in taxation, legal compliance, and fast-tracking of patent registration. Innovation Scheme has also been launched with the intent to promote innovation. The Digital India campaign has been launched to provide affordable, quality internet connectivity across urban and rural areas. The overall political environment in recent years has supported the growth of hyperlocal delivery platforms.

The propensity to consume is dependent on the disposable income of the households. A country’s per-capita income can be a reliable factor for measuring the disposable income of households. Currently, India is considered a lower middle-income country by World Bank. In 2020, the average per-capita income of an Indian was $ 1935 (INR 141,330 approx). As per estimates of the International Monetary Fund, the same is expected to go up to $ 3769 (INR 307,630 approx.) by 2027. World Bank considers a country with a per-capita income above $ 4000 (INR 326,480 approx.) an upper middle-income country (Rajadhyaksha, 2022). As a country’s per-capita income rises and it starts approaching middle-income and upper-middle-income levels, domestic consumption of consumer discretionary and Fast Moving Consumer Goods (FMCG) items rises faster.

There is a rising proliferation of digital applications due to enhanced smartphone penetration and improved internet connectivity. There are 692 million active internet users in India, including 351 million from rural India and 341 million from urban India. The number is expected to rise to 900 million by 2025 (Livemint, 2022). Further, the increasing usage of data analytics and machine learning to understand customer insights and manage the supply chain optimally will help low-margin businesses like hyperlocal grocery delivery to break even and reach a sustainable profit level over time. Moreover, leveraging technology becomes critical for managing an optimal delivery fleet that is efficient for business while responsive to end consumers.

Several new-age start-ups prefer employing gig workers. A gig worker is a person who works as an independent contractor or freelancer. The employment of a substantial proportion of the workforce as gig workers has consequences concerning compliance with labor laws and could attract penalties and cause financial losses. Companies should ensure fair and just treatment of gig workers to avoid penal consequences and possible harsh regulatory changes from policymakers, which will ultimately reduce operational flexibility and increase the cost of operations. Besides treating gig workers fairly, managing hygiene and safety standards is also critical. Any lapses on these fronts will negatively affect the health of the end consumers, which will ultimately attract fines and negatively impact the business' reputation. There will also be anti-competitive concerns in the industry as mergers and acquisitions occur between different hyperlocal players as the industry evolves.

There is a renewed push towards sustainable practices that minimize waste generation and have a net zero environmental impact. This can be achieved by employing electronic vehicles in a delivery fleet, biodegradable packaging, and minimizing food wastage. There is also a growing chorus among the investor community for applying non-financial: Environmental, Social and Governance (ESG) metrics to evaluate any business before investing. Thus, while ESG reporting is not mandatory as per existing laws and regulations, these metrics can impact a business’ valuation and fund-raising prospects among the investor community. Given that most players in the hyperlocal delivery business are burning cash to gain market share, they must operate in a manner that has either a net positive or the least possible negative impact on the environment.

Socio-cultural changes such as the increasing proportion of women in the workforce and the number of nuclear families are changing consumer behavior. People want grocery and essential FMCG items delivered to their homes owing to increased convenience and lack of time. Consumer behavior has also been impacted majorly due to the pandemic-induced lockdown. Women’s participation in the labor force in India is still considerably lower than that of the developed world. Further, the number of nuclear families is also expected to rise in urban and rural areas. Both trends are expected to provide tailwinds for the growth of hyperlocal delivery applications. Further, the favorable demographic profile of India, with most of the population in the working age group, would aid the growth of these applications as new-age consumers are quicker to adopt digitally convenient solutions.

The rising consumer preference towards hyperlocal delivery is owing to convenience. A Mckinsey survey on customer behavior found that almost 33% of consumers consider both affordability and cost as crucial factors while shopping for groceries. Further, the survey found that better value is a significant driver for alternate shopping preferences. Consumers increasingly rely on multiple purchase channels, including online and in-store shopping. The survey also found that more than 60% of consumers intend to continue using alternatives to in-store shopping. Consumer loyalty is also increasingly becoming fragile as consumers easily switch brands for variety, quality, and value. This shift in changing behavior is more extensive among millennial and Gen-Z consumers. There is also an increasing trend towards niche items among consumers in the form of organic foods and nutritious eating. Over half of the respondents in the survey intend to spend more on organic foods.

Critical success factors for quick commerce grocery in India

The hyperlocal grocery delivery industry is a low-margin industry. Accordingly, optimizing the cost structure and the forecasting mechanism is critical for a profitable unit economic structure. Several companies in the industry work with a dark store model to achieve this. A Dark Store location is a distribution center that is not open to visitors and is used for storing inventory and filling orders quickly and accurately. These stores are typically mini-warehouses, optimized with technology designed to serve customers optimally with the most required products by the customers residing in that locality. Some of the critical success factors are discussed below:

Effective inventory management

Since unit economics is more challenging owing to the addition of delivery costs, it is imperative to minimize inventory costs and keep the wastage of inventory to a minimum. Accordingly, it becomes critical to accurately forecast and manage the optimal level of stocks of the most desired items locally. Effective inventory management is critical to consumer experience regarding the availability of the desirable items and the variety of SKUs available to customers. Omnichannel incumbents can offer a wide range of products to customers. Thus, for hyperlocal players to become competitive, they must strike the right balance between variety, availability, and inventory costs. Considering the low-margin nature of this business, effective inventory management will be critical for the success of any hyperlocal grocery delivery player.

Timely and error-free delivery

Since the promise of the hyperlocal delivery model is goods being delivered within a few minutes, it becomes essential that the deliveries adhere to the expected time of arrival shown to the customers at the time of placement of the order. Further, the delivery must be not just timely but also of the expected quality level of the customer. Timely and error-free delivery will become more critical as these hyperlocal players look to expand into Tier 2 cities where the connectivity infrastructure may not be as conducive for shorter delivery time compared to Tier 1 cities. As hyperlocal players choose to grow strategically outside of the most desirable, heavily populated cities, they will also need to change their service model. The model will require tweaking, especially shorter delivery times, as these companies enter Tier 2 cities.

Optimizing fleet size and utilization

The unit economics of a hyperlocal delivery business depends significantly on the size and utilization of the delivery fleet. Optimizing fleet size and its utilization through efficient and effective route management goes a long way in ensuring optimal performance and customer satisfaction. It requires leveraging data and software to capture all constraints and provide optimal solutions. An optimal delivery fleet will also have implications for last-mile delivery, which is critical for consumer experience. In areas where hyperlocal companies have significant scale and business volume, an in-house delivery fleet and direct employment of drivers can significantly improve customer experience and operating margin. In areas where the scale of operation is not so voluminous, tie-ups and partnership models with delivery riders might be a better model economically.

Reaching an optimum average order value

An optimum Average Order Value (AoV) is essential for ensuring profitability per-order. Also, a higher AoV means that the frequency of orders may be lower. Further, order composition is also crucial for maintaining margin levels. Everyday grocery items typically have lower margins, so they need to be coupled with certain things that can support the margin at a per-order level. It is critical to note here that the online grocery channel is structurally less profitable than in-store retail. Pandemic-induced lockdowns and a flush of private equity and venture capital investments have turbocharged the channel without fixing the underlying economics. The disruptors have begun to charge fees that accurately reflect the cost of providing convenience at the consumers' doorstep. For Instance, Amazon has started charging a per-order delivery fee of $ 9.95 (INR 812 approx.) in the US at its Whole Foods Market arm. This fee is being charged over and above the $ 139 (INR 11,345 approx.) annual subscription charge for Amazon Prime. However, the overall industry model is still flawed from an economic perspective. The dark store model followed by hyperlocal grocery delivery players tends to be profitable at a contribution level (excluding costs related to customer acquisition and other indirect costs) only for large order sizes. Most quick commerce players have to offer discounts and subsidies to acquire consumers. While it is assumed that these discounts and subsidies will eventually be rolled back, the need to attract new customers and retain existing customers considering competing offers, makes a rollback infeasible.

The current cost structure, which accounts for fixed costs relating to technology development, general administration expenses, and customer service, requires the quick commerce players to increase the average order value and the order volumes per store to reach a break-even level. For instance, as per Bain’s report, European quick-commerce players need to lift average order values from € 20 to € 30 (INR 1700 to INR 2550) and increase the volume of orders received per store from the existing 300–800 to more than 1000 (Kamel et al., 2022). The model requires improvement not just in terms of the higher order value and increased order volumes but also improvements relating to better supplier terms, faster picking and delivery, dynamic pricing based on demand and supply mismatches, and better customer satisfaction through fewer delivery delays and lesser missing items (Kashyap, 2022).

While it is easier to list the critical metrics such as average order value and order volumes required to be improved, there lie real challenges in raising these metrics to the desired level. Smaller assortments make it difficult for players to increase average order values. Further, growing orders per store become difficult with competitors' presence within the same locality. Optimum fleet utilization becomes difficult considering the need to keep surplus fleet capacity to respond during demand surges. The above challenges make it seem evident that there is a limit to the number of quick commerce stores that a single locality can sustain. Further, the problem of a broken economic model is compounded by the fact that food delivery aggregators are also attempting to grab a pie out of the hyperlocal grocery market as the industry seems to fit inside their circle of competence and a natural extension to the services they are already offering—the above discussion points towards a coming consolidation in this industry segment. The extent and severity of the consolidation will depend on several factors, including the underlying growth drivers and the way hyperlocal delivery players and incumbent players respond to these changing dynamics.

Competitive dynamics

Several factors impact the competitor dynamics within the Hyperlocal Grocery Delivery Industry. The businesses have high operational costs and capital outflow in its initial stages. Thus, for any company to enter the industry in a meaningful manner and acquire an initial set of customers would require a lot of marketing and operational expenditure before a minimum efficient scale is reached at which the business becomes profitable on a unit level. Regarding the merchants, it is essential to note that merchants can easily list on different platforms. Further, most merchants serve only a tiny percentage of the overall geographic area. The customer base for hyperlocal delivery platforms, at the moment, is mostly concentrated in Tier-I and selected Tier-II cities. The average order value per customer tends to be low, which needs to be increased for better operational profitability.

While Hyperlocal platforms are becoming popular, Kirana stores remain the most preferred channel for a large customer base who like to shop for their everyday grocery needs while taking an evening or morning stroll in their locality. The social experience associated with grocery purchases still lures most people towards their local Kirana and organized retail stores. Hyperlocal Players such as Blinkit, Zepto, Instamart, and Dunzo are all vying for the same consumer market. Considering that the industry is still young, their competition is expected to remain high. As time progresses, the number of players may reduce further as winners either acquire the small players, drive them out of business or restrict them to niche categories.

Company overview

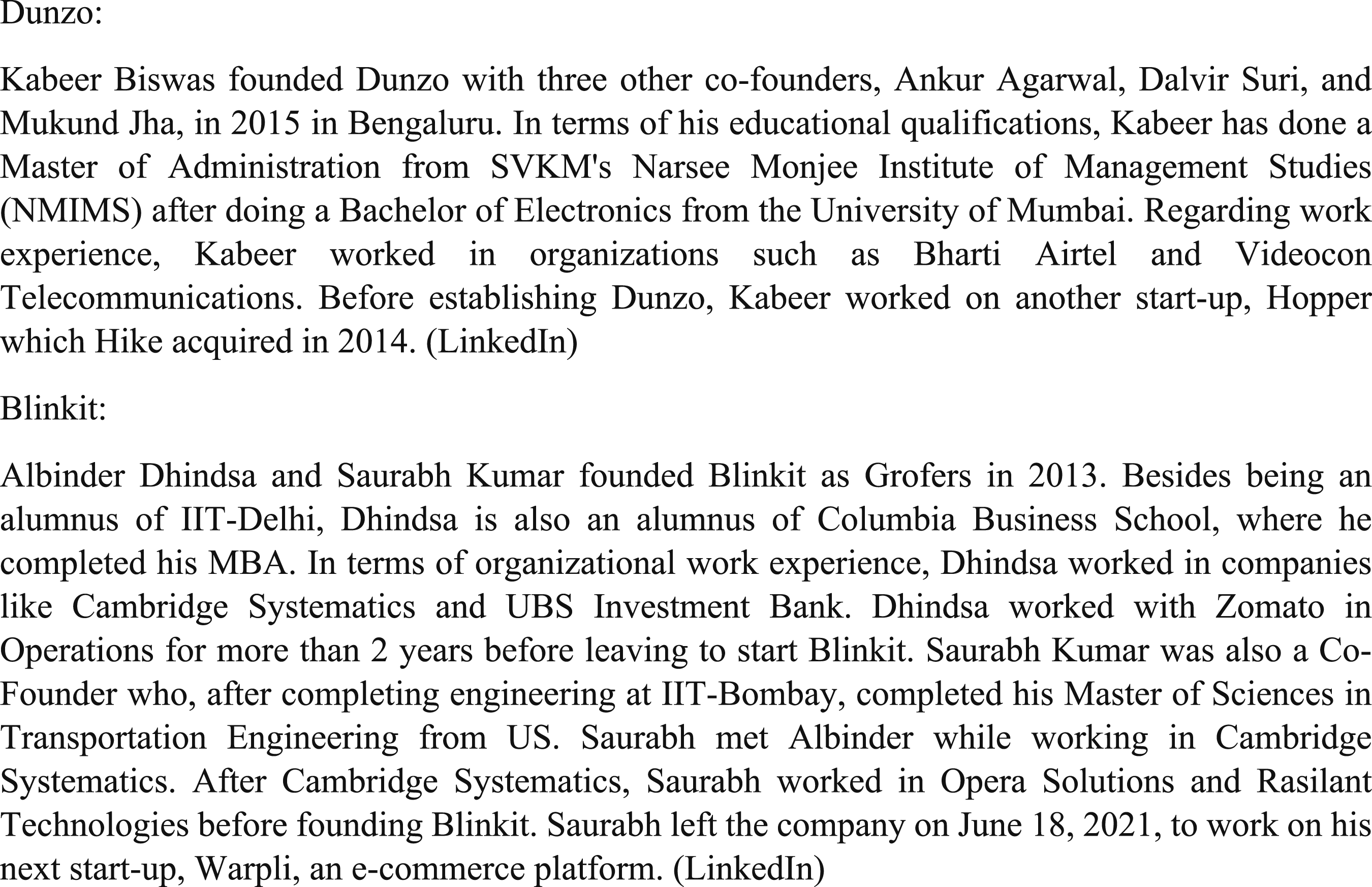

Dunzo

The genesis of the idea can be traced to Bengaluru, wherein Kabeer Biswas, while enjoying his meal, thought that it would be a great relief if one’s to-do list of chores could be outsourced to someone who could do it for you. Kabeer’s eureka moment led to the establishment of the WhatsApp version of Dunzo along with co-founders named Ankur Aggarwal, Dalvir Suri and Mukund Jha 1 . Steadily, the company began to generate around 500 orders a day in 2016. Initially, the company focused on building the application for delivery partners while taking orders from consumers on WhatsApp. By April 2017, the company decided to make a consumer version of the application. The consumer version of the application was launched by the end of 2018 when Dunzo was getting close to 80,000 orders in a month.

By this time, the company realized the need to minimize human intervention to reduce costs and maintain consistency in service. Further, the company attempted to improve consumer experience by making the application easy to use and improving efficiency in operations by better matching demand and supply, geography-specific focus and ensuring partner positioning within those geographies. Further, during its journey, the company also considered feedback from loyal and invested users and input from insights derived through data analyzed on the platform. As the platform started to grow, it became inevitable for Dunzo to hive off specific categories. For instance, alcohol delivery had to be stopped due to legal and regulatory reasons, while services like home repair had to be shut down due to lower-than-expected responses. Dunzo has also focused on partner experience and improving new partner retention. The company faces a delicate balancing task of ensuring fairness with delivery partners while at the same time maintaining control over operations and cost (Kashyap, 2020).

Revenue streams

Dunzo generates revenues mainly from commissions earned from Merchants and Delivery orders 2 . This commission accounts for around 95% of the company’s total revenues. The commission earned from merchants is on a per-order basis from vendors who are registered on the platform. This accounts for more than 50% of the total revenues. Commission from delivery riders is also per-order, depending on the distance covered while delivering orders. This commission accounts for around 45% of the total revenues. The company also makes money by running brand campaigns. However, this segment constitutes only about 3% of its total revenues.

Cost streams

The most significant expenditure for Dunzo concerns employee benefit expenditure in the form of salaries and Employee Stock Options (ESOPs) payments. This expenditure head accounts for roughly 34% of the total costs. Delivery fleet expenses incurred for maintenance of the delivery fleet constitute another significant expense for the company. This expenditure head accounts for roughly 19% of the total costs. Information Technology and Communication expenses are another significant expenditure incurred on maintaining and improving partner and consumer applications. Currently, this expenditure head accounts for roughly 16% of the total costs. Marketing expenditure to attract new customers to the platform is also significant and accounts for 4% of the total expenses. Other Operating and Administration costs concerning general overheads and operational maintenance expenses are also significant. Currently, the expense head accounts for more than 25% of total costs (Vardhan and Tyagi, 2021; Manchanda and Ashrafi, 2022).

Blinkit

The company started as “Onnumber” as an on-demand delivery service from neighborhood shops to customers in 2013. Later, the company was rebranded to Grofers as a 90-minute delivery service in the Delhi-NCR region. In 2014, the company received seed funding of $ 500,000 (INR 4,25,18,000) from Sequoia Capital. Next year, it expanded operations to Bengaluru, Jaipur, Ahmedabad, Chennai, and Hyderabad, with a team size reaching 3000 plus individuals. Around this time, the company acquired a B2B logistics player named Townrush. The company crossed 100 crores in Gross Merchandise Value (GMV) by January 2018. In 2018, it also forayed into the FMCG segment with seven brands. By 2019, the company had expanded its operation into 27 cities, hired 5000 employees to cater to rising demand, and added 700 Kirana shops to the network. In 2021, Zomato initiated the regulatory process to acquire a 9.3% stake by approaching the Competition Commission of India. With Zomato’s investment of $ 100 million (INR 9 bn approx.), the company entered the unicorn club. During this year, the company also introduced 10-minute grocery delivery in 10 cities. In 2022, Zomato signed a term sheet with the company for a merger alongside providing a $ 150 million (INR 13 bn approx.) loan. Zomato acquired the remaining stake in the company for $ 567.78 million (INR 44 bn approx.) (Maloo, 2022).

Revenue streams

More than 90% of Blinkit’s revenue is generated from the sales of goods. The company also collects commissions from sellers on its platform to facilitate transactions. This commission accounts for around 4% of operating revenue. Blinkit also earns from advertising charges from FMCG brands and sellers for promoting products on Blinkit’s platform. This fee accounts for more than 2% of operating revenue. Blinkit offers shipping and delivery services for FMCG products to third-party sellers, accounting for roughly 2% of operating revenue. (Tyagi and Vardhan, 2022)

Cost structure

The purchase of goods is a significant expenditure accounting for greater than 70% of the total expenses of Blinkit. Employee benefits expense in the form of salary and ESOPs is the second highest, accounting for around 11% of the total expenditure. Other Operating and Administrative expenses and Freight and Packaging expenses account for around 4% of each expense head. Other expenditures in technology, rent, repair, etc., account for 9% of the total expenses.

What lies ahead?

The explosive growth of the global hyperlocal delivery industry and the mad rush of investment in the sector have created opportunities and challenges. Several companies are competing for the same set of consumers with comparable offerings. While the industry is growing, consolidation seems inevitable in the long run. The economic structure and fulfillment model must be worked out to ensure that investment in the sector remains viable. Further, the treatment of delivery partners considering introducing ultra-fast delivery services would be under media and public scrutiny. Thus, players must balance customer responsiveness, fleet optimization, and cost control while providing fair and just treatment to delivery partners. Moreover, a fundamental challenge for the industry is to have a sustainable operating model which is profitable at a unit economic level. The interplay of unit economics and customer experience will determine the future of this industry.

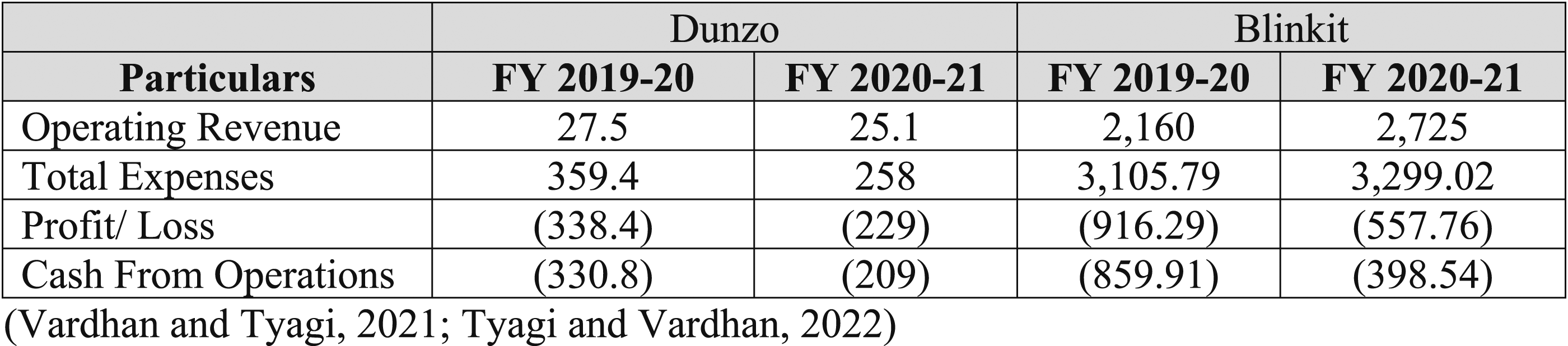

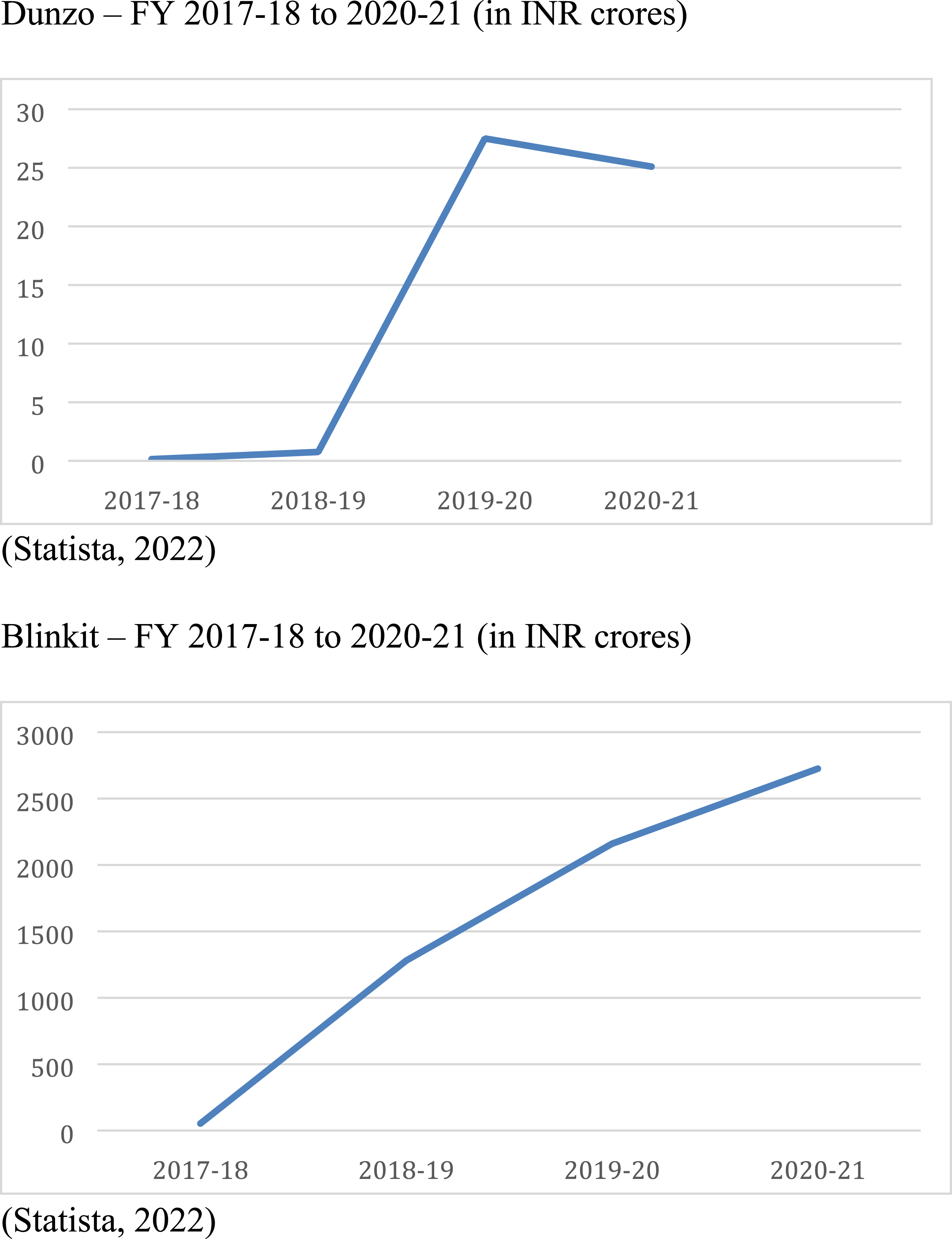

Regarding its scale of operations, Blinkit is a more prominent player in terms of its operating revenues. While comparing different consumer metrics, we find that Dunzo is doing better compared to Blinkit across several vital consumer factors. These include perception of delivery speed, offers and discounts, the conduct of delivery partners, and customer service. It is critical to note that delivery speed, variety of listed products, and offers/discounts significantly impact customer satisfaction. Accordingly, hyperlocal players attempting to gain market share over their competitors would need to pay specific attention to improve their business metrics in these areas. What should Dunzo and Blinkit do to win in this emerging industry? Founders. Latest Financial Statements (Amount in INR crores). Operating Revenue Trends (Past 5 years).

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author note

This case was prepared by Prof. Krishna, Nirmit, and Prof. Vivek from published sources. This case is developed solely for the purpose of class-discussion. It is not intended to serve as source of information on the company or any endorsement of (in) effective handling of situation(s).

Target audience

This case is aimed at B-School post-graduate and executive education participants.

Target courses

This case is best suited for courses focused on Technology, Innovation, and Strategy.

Target teaching modules/concepts

Following modules/concepts can be taught using this case: macro and industry environment analysis; internal environment analysis; business model canvas and business model innovation; and critically evaluating the customer value proposition and the business model changes.

Disclaimer

Like other cases written solely based on secondary sources, this one also has standard disclaimers such as,

1. The case cannot be used as a source of information on the company.

2. The information/facts/statements/mentioned in the case has been taken from secondary sources and is not endorsed by the company, its founders, partners, and other stakeholders.

3. The case is not intended to serve as an endorsement of (in) effective handling of situation(s).

4. Authors acknowledge that the brand names and trademarks used/mentioned in the cases are owned by respective title holders.

5. All errors are the responsibility of the authors. Upon being notified, the authors will undertake all reasonable efforts to rectify the errors.