Abstract

Being highly dependent on the oil sector, Azerbaijan suffered from economic downturn due to sharp fall in oil prices in 2015. However, such dependence creates development challenges for her. Simulated impact of prioritized economic reform policies—using a computable general equilibrium model (AZEORANI)—shows that, under the business-as-usual case with oil prices at 2011 level, it is projected to grow by 2.0% a year to 2030. However, consistent policy reforms enable enhanced growth by another 1.1 percentage points annually due to productivity boost and increased exports from non-oil sectors, viz., tourism and agriculture. In particular, following strategic roadmap, we consider baseline and policy shocks—10% improvement in productive efficiency, investment boost by 5% in non-mineral sector, and enhanced agricultural efficiency by 5%, and boost in tourism and transport by 10% via logistics-infrastructure, and technical progress in manufacturing over long run by 10–20% per annum. All these show that economic reforms have potentials to induce positive impact to overcome the binding constraints inhibiting growth and hence could promote economic development of Azerbaijan.

Keywords

Introduction

With its high dependence on the oil sector, the sharp fall in oil prices 2015 has led to an economic downturn in Azerbaijan. Economic growth dipped and turned negative in 2015. The drop in the oil exports also caused a large external imbalance and significant reduction in government revenue. Thanks to the government’s appropriate response, economic growth has gradually recovered in 2018 and the trade deficit has narrowed. While economic growth has returned to positive territory, with oil price not expected to return to the 2012 level, Azerbaijan will face daunting challenges ahead to bring growth to and maintain it at a higher level. With outbreak of war between Russia and Ukraine and evolving geo-politics reshaping economic relations, the oil problem has resurfaced with steep prices and fluctuations with uncertainties. No doubt, that oil sector will continue to be an important source of growth for going forward, but higher and more stable growth will require economic diversification to increase the contribution of the non-oil sector as heavy dependence on hydrocarbon-based growth causes vulnerability without alternative sources. Growth diagnostics following Hausmann, Rodrik and Velasco’s 2005 model have identified key binding constraints to investment in the non-oil sector, including short-term macroeconomic risks, lack of access to finance, high investment risks, and underdeveloped infrastructure to support external trade and tourism.

The government recognized the need to diversify the sources of growth and associated challenges that need to be addressed. The Strategic Road Map (SRM) for National Economy Perspective (henceforth, SRM/NEP, interchangeably), issued in 2016, identified sets of strategic priority areas of reforms to support higher growth medium to long term. These reforms include efforts to improve macroeconomic management, reduce business impediments, attract investments, promote efficiencies in the state-own companies (SOEs), address remaining infrastructure bottlenecks, and upgrade human resources development to foster productivity-driven growth. In terms of sectors, the SRM also targets generating a better growth environment for non-oil, non-energy sectors such as agriculture, trade and logistics, and tourism. These include short-term priorities that need to be achieved by 2020 (short-term), long-term reforms with targets to be achieved in 2025, and aspirational phases beyond 2025.

This paper attempts to quantify the potential impact of selected government structural economic reform priorities identified in the SRM on future growth and economic diversification. In particular, the paper uses a computable general equilibrium (CGE) model developed for the Azerbaijan economy (AZEORANI) that uses 2011 input-output (supply use) data. The model allows for detailed analysis of planned government structural reform policies. Our objective is three-fold: (i) to present stylized facts about historical performances of the Azerbaijan economy in the recent past, and highlighting the obstacles for growth diversification; (ii) offering an ex ante analysis via policy simulation model to perform “what if” analysis of reform scenarios; and (iii) showing that appropriate reforms enable overcoming the growth constraints. This is in keeping with the recent Asian Development Bank (ADB August 2020) study by Hampel-Milagrosa et al. (2020) where the country diagnostics study identifies the obstacles to reform, outlines achievements so far, and recommends further steps for making reform a success. Our study complements this.

Thus, our contribution lies in exploring evaluating the impacts of policy simulations. In particular, these are (a) under the business-as-usual case, with oil prices remaining at 2011 level, Azerbaijan’s economy is projected to grow by 2.0% a year to 2030; (b) implementing selected reforms improves the business climate; (c) enhancing efficiency of SOEs and increasing participation of the private sectors would enable additional 1.1 percentage points annual growth rate; and (d) improvement in productivity of both labor and capital might lead to increased exports from non-oil sectors such as tourism and agriculture.

The next section summarizes strategic SRM reforms needed to address growth constraints and to provide the basis for policy simulations to be presented. The third section outlines the structure of the Azerbaijan economy-wide model (AZEORANI) and how it is used to quantify and analyze the economy-wide effects of the selected government’s strategic reforms. The fourth section presents the economy-wide effects of proposed policy changes on economic growth, industry outputs, export diversification, and regional income distribution. The last section concludes.

Government reforms to foster economic diversification

Structural reform has been undertaken in many emerging countries in Central Asia. However, the need for speeding up of reforms for improving productivity has been felt recently to catch up (Georgiev Piroska and Plekhanov, ADB, 2017). With oil prices not expected to return to its 2011 peak, the need for diversification into non-energy exports and services is imperative. Considering the fact that followed by services (49%), 37% of the labors work in agriculture, economic diversification that include agriculture sector and agribusiness is essential to improve productivity and make growth more inclusive. With economic diversification and improved productivity, the SRM targets for more than 3% GDP growth annually, and job creation of over 450,000 by 2025 (see pg. 57, SRM).

1

According to “Global Competitiveness Report” for 2018–19 (World Economic Forum), although Azerbaijan ranked 58th among 141 nations in terms of global competitiveness, it ranked low in terms of macroeconomic stability (70th), skills (70th), infrastructure (77th), financial system (55th), and business dynamism (72nd). Several important studies—such as Mukhtarov (2018), Tiwari et al. (2018), World Bank (2016), Ibadoghlu (2018), and Rahmanov et al. (2016), to name a few—echo same concern. Thus, for diversification into non-oil and traded sectors it is necessary to go beyond the capital accumulation-led to productive-efficiency improvement via developing quality human resources, good infrastructure, access to finance, and promoting business and institutional environment (Bayramov et al., 2014; Durlauf, 2018; Estrada et al., 2017). To that end, SRM includes four strategic priorities: 1. Fiscal sustainability and robust macroeconomic policy: Macroeconomic reforms will include reforms to move to a floating exchange rate system and good fiscal management to ensure macroeconomic stability. 2. Privatization, SOE reforms, and FDI: Reforms in these areas are aimed to increase the dynamism of Azerbaijan economy by increasing efficiency in the activities currently controlled or belong to the government. Some of the SOEs, where feasible, will be privatized in the medium term. 3. Educational Quality and Labor Productivity: This reform is aimed at enhancing human resources development to foster productivity growth and meet the needs of future growth via improving labor efficiency and productivity. 4. Improving the Business Environment: This reform is key to improving the domestic business environment and enhancing the competitiveness of domestic firms. This, supported with a healthier financial-banking system and better macroeconomic environment under a floating exchange rate system, will open opportunities for expansion of access to foreign markets. This is pertinent for transition to “new economic growth” model via endogenous growth.

After the first generation of reforms post-independence (in 1995–2003) and the second oil boom (in 2004–2010), the Azerbaijan economy achieved high growth although the path was not rosy, and the economy started manifesting symptoms of “Dutch disease.” However, given the four SRM priorities, private investment and entrepreneurship remains a major hindrance. Not only that, dependence on oil could trigger a full Dutch disease unless managed well. The binding constraints underlying such dearth of investment could be categorized into several kinds, viz., macroeconomic in nature as well as micro aspect with bottom-up repercussions throughout the economy via factors, such as risks for market failure, inadequate human capital, and poor infrastructure. Origin of the constraints are both macro in nature, encompassing fiscal, monetary and financial policies, as well as micro level based on sectoral productivity, competitiveness, and efficiency. Bottlenecks in infrastructure and inadequate skills are severe. Investment in these areas is necessary for product diversity and export sophistication.

Given the evolution of the economy, Agriculture, Tourism, Logistics and Transport are, inter alia, important among 11 priority non-oil sectors of the SRM. One of the main obstacles for developing these sectors is existence of large SOEs. Underperforming SOEs have shown diminishing importance in terms of shares in GDP and employment but profitable ones like the State Oil Company of Azerbaijan Republic (SOCAR) are critical. Although the State Oil Fund of Azerbaijan Republic (SOFAZ) transfers for fiscal management are essential, too much dependence on oil revenue for fiscal deficit is not ideal. Underperforming SOEs create fiscal burden and productivity loss due to inefficiencies further worsening debt, inflation, and forex constraints. SOE reform is necessary for the micro and macroeconomic risks to be eradicated toward a favorable business climate. In addition, fiscal consolidation and prudence are necessary along with sound financial policy.

In order to augment investments in the non-oil sector, it is necessary to overcome short-term macroeconomic risks through reforms. Improving access to finance is crucial so that it is not too costly for the private sector to borrow for boosting domestic saving propensities, stabilizing exchange rate and controlling inflation for improving macroeconomic stability. Recently, Mckinsey and Company (2019-2020) studied that new reform model in 2016 and associated measures have improved significantly the business environment inducing sustainable GDP growth (from 38 billion USD to 4t billion) via non-oil exports and setting up new investment climate for businesses. Further, this will be instrumental and crucial for SDGs in 2030 in progression. Valiyev (2020) mentions about particularly inclusive sustainable growth (SDG 8) for structural reform and job-led growth. IMF (June 2021) also mentions about the precariousness especially after post-Covid-19 and the more urgent necessity of undertaking economic or structural reform program for diversifying the production and socio-economic developments by improving efficiency, governance, human capital, and reforming the state-owned enterprises.

Macroeconomic reforms

Most binding constraints for diversified economic growth are low levels of FDI, low levels of private investment and entrepreneurship in the non-oil sectors, and high levels of risk. These are related to “Business Climate Reforms” for promoting conducive business environments for investment. As short-term macroeconomic risks could emerge from the excessive dependence on oil for exports and as a source of revenues for the government budget, sharp fall in oil prices could make the country vulnerable to external fluctuations and put a burden on fiscal deficit, external balance, and balance sheets of local banks. Although the scenarios might change, growth in the non-oil sector is important for further diversification. Fiscal reform is also effective to arrest currency depreciation of “manat” without leading to high double-digit inflation (e.g., 20.8% in the past in 2008).

Typically, high cost of finance—due to low domestic savings, inappropriate international finance, underdeveloped non-bank financial institutions, bad local finance, minor role on bank-financing and high interest rates and spread—is a major obstacle for economic development for any country. Because of the high spread between lending and borrowing rates, financial intermediation is problematic. It is imperative to boost gross fixed capital formation as a percentage of GDP so that credit and investment for the businesses are not severe constraints for investment in non-oil economy, such as agriculture, energy, transport and communication, construction, manufacturing, trade and services. All these are important for minimizing high risk in the “real sector” and high inefficiency in the financial sector for inducing entrepreneurship.

Although the Central Bank resorted to currency devaluation in 2015 and adopted a managed floating exchange rate for offsetting the adverse effects of oil price reduction and decline in oil production, it increased macroeconomic risks such as high inflation, fiscal deficit, and fall in current account surplus. However, as mentioned above with appropriate responses such as restructuring of feeble financial sectors it was overcome.

SRM targets to cure these malaises in the system via establishment of a healthy, dynamic, regulated environment for a better functioning financial system, which aims to mobilize domestic and foreign savings to the non-oil sector, especially. The setting up of the Financial Market Supervisory Authority (FMSA), Credit Guarantee funds, and National Fund for Entrepreneurship Support aims to foster loans to strategic sectors, such as agriculture and other small business owners. Azerbaijan has been trying to implement reforms successfully in this direction since 2018 (see Mukhtarov (2018), Ershova (2017) and World Bank (2016) on this).

Priority reforms undertaken are (i) restrictive monetary policy and disciplined fiscal policy (fiscal consolidation) to ensure price stability; (ii) development of financial system ensuring flow of loanable funds; (iii) floating exchange rates for mitigating adverse oil price shock; (iv) transparency and protection of property rights to reduce risk in the financial sector where banking sectors suffer from oligopolistic competition; and (v) improving accountability through regulation and monitoring via some institution.

Business climate reforms

Although Azerbaijan’s ranking for “Ease of Doing Business” is at 34th, 2 the Global Competitive Index of the World Economic Forum (2018-2019) identifies some obstacles for doing businesses related not only to the issues of access to finance, inflation, exchange rate fluctuations, bank failures, foreign currency regulations, etc., but also to other drawbacks. 3

As part of the 2018 reform program, infrastructural bottlenecks and public goods constraints have been addressed. These are especially necessary to achieve targets prioritized in SRM. This is a medium-term constraint for non-oil growth. For development of agriculture and tourism with ample opportunities to diversify via technological or efficiency improvement, Azerbaijan still needs to develop efficient and cost-effective logistical networks and transport systems (roads, railroads and ports), and improve telecommunication networks beyond urban centers. As it is a water scarce country, poor infrastructure could pose a serious threat for the growth of tourism and agriculture. For agriculture, irrigation and water network infrastructure, desalination of cultivated land, investment for crop yields via technology are critical for inclusive growth via export diversification (see Das, 2007, 2017). In this context, the development of small and medium enterprises (SMEs) is priorities. One of the major focuses is developing entrepreneurship for job creation and employment growth via SMEs based on the country experiences from emerging economies as well as the developed nations. This is aimed for increasing competitiveness, efficiency and employment creation.

“Missing cluster” or linkage development for “new” goods is related to coordination and information failure causing market malfunctioning because of macroeconomic constraints (discussed earlier) limiting development of inputs (intermediates) and production of sophisticated goods and services. Export sophistication and product diversification are important for diversifying export baskets and reaping comparative advantage. Based on multi-country study using a global database, Das (2015) shows that the degree of enrichment of a country depends on the level (Arrow & Debreu, 1954; Meroni et al., 2015) of diversification and sophistication, which in turn hinges on overcoming constraints in quality R&D, human capital, and infrastructure. As discussed, following HRV (2005) and HHR (2007), compared to other nations at similar levels of development, Azerbaijan is lagging in terms of “Export sophistication” and “Product sophistication,” which is reflected in their low exports even in non-oil sectors. These three measures are related to evolution of inter-dependent and interlinkages with other sectors in a “product space” and determine dynamics of changes in export composition (Gillespie et al., 2014; Tomohara & Takii, 2011). Azerbaijan stands far below the comparators in terms of her position in such space, as captured by the lower value of “open forest index.” We see crude oil exports plus gas account for 91% of merchandise exports in 2016. It shows that Azerbaijan might suffer from missing linkages of clusters in priority sectors leading to severe market failure syndromes. For improving weaker ranking (63 out of 137) in “foreign market size index” and “export share of GDP” (54), easing business entry for new firms, infrastructure, and skill formation are necessary for a fertile business environment. In addition, property rights, tax policy and governance are important elements for attracting new industries. A study by Ibrahimli and Guliyev (2020) discusses the hindrances in attracting foreign investment and necessities of improving the investment climate to cure this malaise. Also, the role of government measures is emphasized. In this sort of meta-analysis paper, several things are highlighted, such as education, skilled workers, sustained macroeconomic stability, favorable natural resource endowment (resource-boon), and export platform due to geographical location. Not only that, the paper identifies constraints, such as complex business environment, and infrastructure, and discusses the necessity of further “future-oriented” product diversification via economic development strategies of the government.

Also, the role of an educated workforce and good work ethic is important for a conducive business milieu. Education and Health contribute to Human Capital, and hence, they are important for productivity enhancement. Quality-adjusted labor force is scarce and for that, education at all levels (by reducing dropout rates) and across disciplines need to be promoted for employment generation. Also, because language capability with foreign vernacular is important for tourism, this barrier of communication deters international tourists to some extent. For this, Azerbaijan needs suitably skilled travel professionals with good language skill and knowledge of the external world. This lack of human capital is a constraint for attracting tourists from across the world. One pertinent point is low economic sophistication and poor market coordination (market failure) due to missing sectors. Reform prioritizes identifying product space and promising sectors (“hippos,” not the “camels”) and developing and matching skills, for sustainable efficiency driven growth beyond capital accumulation. 4 Regarding human capital development, incentives are much less as wages and salaries in the oil sector supersedes than in non-oil sectors. For productivity-driven non-oil based diversified growth and efficiency, human capital-induced skill is essential for adoption and use of technology in sectors esp. in agriculture (Priority sector 2), heavy-industry and machinery (Priority sector 4), tourism (Priority sector 5), information and communication technologies (Priority sector 10), to name few among 11 flagman sectors (see (Camanzi et al., 2018; Das, 2007, 2015; Gillespie et al., 2014; Rahmanov et al., 2016; World Bank, 2016). This means better education systems and integrating soft skills into life-long learning through educational attainment. Given the due emphasis laid on the development of these sectors (and others), the need for interlinked or inter-industry dependence is imperative for product complexity and economic diversification. Human capital development is a long-term constraint where there is skill mismatch in the labor market with a relatively low level of tertiary educated workforce. Azerbaijan ranks 90th out of 137 (tertiary enrollment) and 58th (quality of management schools) with rooms for improvements. With low levels of infrastructure and low human capital (e.g., low PISA scores in 2015), these are impossible tasks due to coordination failure, poor coordination, low social returns to investment, and low appropriability. More reforms that are specifically related to government and market failures on this front—inadequate or insufficient hard and soft infrastructure—is related to easing business conditions for attracting new industries with backward and forward linkages and encouraging flow of high skilled workers for sophisticated production networks.

SRM Number 8 emphasizes on reforming vocational education and training systems. 5 As mentioned in the SRM, there is “lowest quality indicator” in the age group of 15–24 and qualified personnel for the 25–54 age group. The Roadmap for the national economy outlines “investments across all pillars of education to support human capital formation and development” and “encouraging uninterrupted human capacity development to increase labour productivity.” This would include investing in reforming the TVET (Technical and Vocational Education and Training) system (Priority Sector No. 8) and “bringing primary vocation and secondary special education in line with requirements of the labor market” and investments in R&D.

From the previous discussion, reform priorities typically should focus on (i) investment in transport and irrigation infrastructure for marketing of products to urban agglomeration centers and also in the global market via regional networks via highway or ports, air and railways; (ii) inducing agricultural investments for sustainable development of agriculture and horticulture sector via incentives without worsening fiscal burdens via subsidies unnecessarily; (iii) diversifying to high value-added products (major crops like cotton or wine) through development of manufacturing and processing of agricultural products, linking them to regional and global value chains; and (iv) investing in skill-specific human capital for improving efficiency in the tourism sector and in tourism-linked infrastructure like clean water, transport, foods and entertainment services.

However, as in this analysis, we are doing an ex ante policy simulation exercise to study the impact of such reforms in 2018, some of these have already been attempted or implemented. 6 We now turn to the potentials for reforms in some priority sectors in keeping with the SRM for increasing share of the slow growing sectors with high potentials for improving labor market outcomes via employment, esp. in agriculture, construction, tourism, logistics, and SOEs (a case of concern for micro and macro risks). Below, we discuss them in turn.

Agriculture reforms

Agricultural primary and processed foods via agribusiness or supply chain development is of critical importance to Azerbaijan’s medium term or long-run development. The current share of agriculture in GDP is meager 6.4% (2015–16), while it provides employment to 36.7%. Although initially during 1992–99, agricultural and farm products accounted for 15% of merchandise exports—due to cotton (1/3rd) production—between 2000 and 2016, exports (in US$ terms) declined, whereas imports swelled (almost 19% of all goods imports are accounted for), resulting in rapid growth in net imports of farm products (US$800 million in 2016). This could be attributed to fall in competitiveness during oil price slump and exchange rate depreciation, and low productivity. Currently, this could lead to Dutch disease with food processing consistently accounting for more than 25% of total manufacturing GDP. Several problems, such as high costs of finance, exchange rate fluctuations, inadequate qualified human capital, investments in better agricultural technology and its adoption, and underdeveloped infrastructure, pose as binding constraints.

The only way to overcome these constraints is to raise productivity and efficiency in this sector. Among the 11 flagman priority sectors, “Manufacture and processing of agricultural products” is one where strategic targets are designed for sequential stages over medium and long-term for transitioning from traditional to market-oriented value-added intensive farming. 7 Specifically, major targets emphasized increasing meat and milk production by 30% and 20%, respectively, increasing cotton production and processing by at least 4 times, and establishing a total of 25 small and medium businesses along the relevant value chains in each region by 2020. Other ambitious targets are facilitating access to finance worth an additional of AZN 665 million, improving water supply for agricultural producers by 20% and increasing use of mineral fertilizers by agricultural producers by 25% and seeds up to 90%. For the aspirational phase beyond 2025, emphasis has been laid on advanced agricultural technology in keeping with environmental standards, sustainable food security, and efficiently integrated into the global value chain.

For improving productivity growth and export diversification, Azerbaijan needs to invest in agricultural technology, irrigation technology. Only 45% of arable area has irrigational facilities, and more than 50% of those lands suffer from salinization and inadequate drainage. Regarding infrastructural bottlenecks, Azerbaijan used to have inferior quality rural road networks, highway routes interconnecting regions and sub-regions, cities, sea port facilities, and registering sharp fall in trade and transport of goods via railways, sea, air, pipelines, and road. Not only was that, with poor telecom services and connectivity, the prospect expensive and hard to compete with imports. However, with proper reform measures, Azerbaijan has been able to overcome such things and still needs more in this regard (see SRM).

Lower educational attainment and lack of extension services cause human capital to be poor so that inadequate R&D investment inhibits less technology adoption, and that is true even for this nation (Das, 2007, 2017). Therefore, instead of subsidizing producers or protection via tariffs it is important to invest in raising productivity via (i) government expenditure on agricultural R&D; (ii) investing on basic education and post-tertiary vocational education for developing qualified specialist; and (iii) investment in road, logistics and infrastructure for improved production and tradability of agriculture, horticulture, and other farm products.

Tourism reform

According to the WEF’s 2018 Global Competitiveness Index for tourism, Azerbaijan ranks 89 out of 136 nations in terms of tourism service infrastructure. This is lower than some comparator countries like Russia and Georgia. For non-oil growth and to gain advantage out of globalization, the tourism sector holds a lot of potential for non-oil growth as “Development of Specialized Tourism Industry” is Priority Sector 5 for the SRM’s long-run (2025) and post-2025 aspirational phase. Although net exports picked up to US$360 million in 2016, the sector faces constraints like high cost finance, access to finance, appropriately trained professionals with requisite human capital, and lack of infrastructure, telecommunications, and some transportation problems (this is also linked to Priority sector 6: “Development of logistics and trade”). 8 Lack of finance at reasonable cost inhibits development of hotels, construction, and ski resorts. Even so, the service infrastructure is not sufficient to push up growth in this sector as the country trails behind in terms of airline connectivity and available airline seat kilometers, mobile and fixed telephone penetration rate per 100 populations. Given all these hindrances, for non-oil growth investment in tourism is necessary along with adequate investments in interlinked factors, such as human capital, public health facilities, and fiscal consolidation via financial access. As tourism belongs to the “social and other services,” presence of SOEs in this sector for water supply, waste disposal and sewerage contribute to inefficiency and fiscal burden. Thus, priority reform involves catalyzing productive efficiency via more investments on human skill, infrastructure and transport networks.

Transport and logistics reform

This is Priority sector 6: “Development of logistics and trade.” According to the World Bank, 9 “Azerbaijan is trying to benefit from regional connectivity initiatives to boost transit and trade. In particular, the country is one of the sponsors of the East–West and North–South transport corridors. Construction of the Baku–Tbilisi–Kars railway line, which will connect the Caspian region with Turkey, is expected to be completed in 2017. The TransAnatolian Natural Gas Pipeline (TANAP) and TransAdriatic Pipeline (TAP) will deliver natural gas from Azerbaijan’s Shah Deniz gas field to Turkey and Europe.” As geographically Azerbaijan is located in the crossroads of trade arteries connecting “Silk Road” and North–South Corridor, transport and logistics is of crucial strategic importance, for example, as a hub for transporting commodities, raw material via, for example, Baku–Tbilisi–Ceyhan Pipeline (BTC) or South Caucasus Pipeline linking her with Turkey and Georgia, and also Silk Road Project. Recently, Donaldson (2017) has offered evidence that India’s railways achieved a considerable reduction of the trade costs and interregional price gaps while increasing interregional and international trade, and thereby real incomes of the country. (Asher & Novosad, 2018; Liu et al., 2013) point out that improved water and land transport infrastructure made a significant contribution toward economic development in the PRC. As infrastructure is crucial for trade expansion, connectivity, and transportation, streamlining trade and logistics is quite important. The aim here is to actively participate in trade and establish Baku as a regional hub for further regional integration. Azerbaijan is a member of the Central Asia Regional Economic Cooperation (CAREC) Program and hence, development of trade and logistics is crucial for export competitiveness (Bayramov et al., 2014; Wattanakuljarus & Coxhead, 2008). 10 By 2025, Azerbaijan will have a strong logistics platform backed up with the benefits of a free trade zone in its recently launched free economic zone including the territory of the new Port of Baku established in Alat settlement. As part of its post-2025 vision, Azerbaijan would have a strong logistics hub located in the territory of Baku Heydar Aliyev International Airport and free trade zone included in Baku International Sea Trade Port complex in Alat settlement (further called new Port of Baku complex). Target indicators are transportation of transit freight of 150 million tons through the “East–West Corridor” in 2015 11 although Azerbaijan’s share is small in this. 12 While Central Asia and Black Sea region trade along the corridor stood at 9.9 million tons in 2015, it is expected to grow to 13.8 million in 2020. 13 Direct impact of logistics and trade centers should be equal to 20% of the total impact from regional logistics and trade hubs. Thus, the reform priorities involve: (i) development of port and railway along a designated path; (ii) establishing Azerbaijan as a regional logistics and trade hub; and (iii) regional trade integration with Baku as hub and others as spokes.

State-owned enterprise (SOE) reforms

While discussing the constraints for finance, fiscal burden and monetary policy we saw that financial losses (fiscal burden) and productivity loss (inefficiency) in some SOEs are matters of concern for indebtedness of the government. As SOEs compete with foreign and domestic private firms, at the micro level, there are risks for government failure in terms of resource misallocation for infrastructure, human capital, and innovation for product development via R&D for “nearby” goods with scopes for inter-industry linkages. Large monopolies exist in monopolistic or oligopolistic markets such as oil and gas (SOCAR), power (Azerishiq & Azerenerji), telecommunications (Aztelekom), postal system (Azerpost), financial and insurance activities (International Bank of Azerbaijan-IBAR), logistics (Port of Baku and Caspian Shipping), transport (Azerbaijan Natural Railways State Agency on Azerbaijan Automobile), professional and scientific technical activities (Azercosmos), as well as in non-monopolistic construction sector (Azervatoyol). The SOEs are too big to fail and deter averting risks at the micro as well as macro level. Major deficiencies of the SOEs are high debt level and exchange rate exposure to vulnerability, financial vulnerability, and fiscal burden, along with low accountability with weak governance, fragmented ownership function, lack of autonomous regulatory mechanism, arbitrary tariff setting, and slow pace of privatization with quality investment.

In order to measure performance, the ADB Azerbaijan Country Diagnostic Study (2020) evaluated 15 SOEs. Overall, favorable treatment under the government umbrella in the form of debt-write-offs, subsidies, guarantees for rescue create adverse business climate for fair competition and hence, obstructs development of efficient markets for skilled workers, new industries with innovation potentials, and export sophistication by crowding out private investments. Thus, considering these risks at the micro level without governance or transparency, in the presence of worrisome SOEs government failure reinforces market failure, furthering distance to the frontier of conducive business climate. In terms of macro risks where the interplay of fiscal, monetary, and financial policies poses constraints, fiscal prudence and consolidation are necessary. This also relates to exchange rate management and fluctuation affecting foreign currency denominated debts. For example, in case of SOCAR transfers to the SOFAZ and Central Bank, the purpose is to achieve macroeconomic stability via fiscal-tax discipline.

However, inefficient administration of large SOEs such as International Bank of Azerbaijan contributed to increase in government indebtedness as it defaulted and filed for bankruptcy. Inefficient management, faulty investment policy, low liquidity, corruption, etc. led to huge external debt, jeopardizing credibility as a business destination. Although state budget dependence on transfers from the oil fund has declined as an indicator of potential push away from heavy oil revenue dependence to tax-revenue dependence, still the budget depends on oil windfall gains. This undermines the development of the private sector with much less dependence on oil price volatility. For SOFAZ transfers, the high elasticity to oil revenues is a serious concern, as tax-based revenues are less available for welfare programs.

For the non-oil economy to be diversified with export diversification, production costs need to be lower. If production costs rise, this might lead to high inflation and would hamper exports. However, currency devaluation in 2015 has caused fueling of foreign debt for SOCAR (accounting for 34.2% of GDP) and interest payments. Thus, oil price shock affected SOCAR, IBAR and Azerbaijan Railways heavily in 2015, and the government’s attempt via SOFAZ transfers for sterilizing oil revenue reinforces the possibility of Dutch disease, slowing the non-oil economy. As SOE underperformance led to 12.56 billion manat of loss to government budget, analysis showed that improved productivity performance of SOEs directly affects GDP and also helps improvement of non-oil sector, economic diversification, improvement of Balance of Payments, employment generation, reallocation of subsidies to social sectors, agriculture, and decreasing dependence on SOFAZ or SOCAR. On the fiscal front, this productivity improvement will translate into better state budget planning, increased tax revenues with a broader tax base with less tax evasion, enduring financial viability and private sector participation and less chance of default under no guaranteed debt coverage by the government.

The preceding reform efforts are grounded in theoretical literature on structural reform (see Aksoy, 2019; Campos et al., 2017). According to the SRM (p. 10), for transition to “new” growth path “[already], the most important challenge of the new period is to ensure transition from ‘capital accumulation’ based model to ‘productivity (efficiency)’ based growth model. Therefore, it is required to further increase the quality of the institutional environment and to prepare accessible financial sources, correctly segmented and specialized business environments and, most importantly, to intensively develop highly qualified human capital.” In terms of current academic literature, this kind of “new” economic growth approach documented in the SRM has underlying rationale based on the “New Growth Theory” paradigm or, Endogenous Growth Theory.

The relatively poor non-sustained growth performance of lagging countries has been attributed to factors such as limited/dilapidated infrastructure and human capital, quality of institutional factors, limited financial depth, trade orientation, and investment, and political and social stability (McAuliffe et al., 2012). Our point is that trade and investment flows, technology via R&D investment, removal of infrastructural bottlenecks, idea flows, and its adoption will facilitate economic diversification (and export sophistication and diversification), contingent on several institutional and infrastructural factors, and will influence the growth process. In a recent paper, Franck and Galor (July 2018) has shown that long-run prosperity of developing countries are hampered by adverse effects of adoption of unskilled-intensive technologies in the early phase of industrialization which prohibits human capital formation and adoption of skilled-intensive technologies. Studying 25,000 domestic manufacturing firms in 78 LDCs, (Farole & Winkler, 2012) explores that FDI-related horizontal and vertical productivity spillovers depend on recipient firms’ human capital and skill, host’s R&D intensity, technology gap, export behavior, firm location, trade policy, access to credit/finance, business and investment climate, innovation infrastructure, etc (Kim & Park, 2017; Meroni et al., 2015). 14

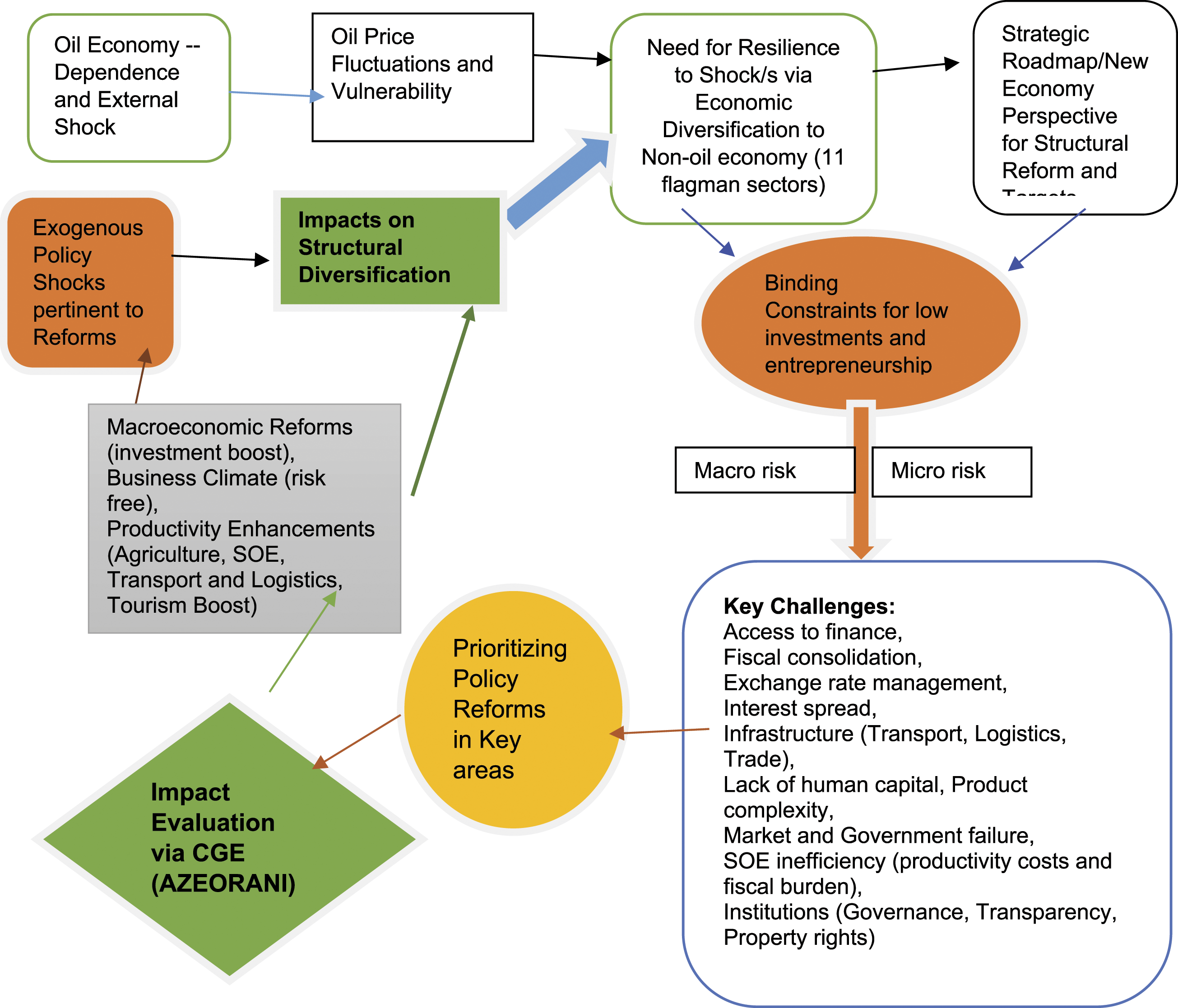

Figure 1 depicts a snapshot of the CGE impact evaluation based on the prioritized reforms. Taking the miracle “East Asian Countries” experience, we see that participation in the regional and global value chain is crucial for growth and for that, efficient trade infrastructure, and incentives are needed. Principal pathways depicting reforms and implementation via AZEORANI.

Quantifying structural reforms: The analytical framework

In order to assess impacts of reforms, a CGE model of the Azerbaijan economy—namely, AZEORANI is developed based on ORANI-genre of models, quite widely acclaimed and cited in the academic and policy research area (Dixon et al., 1982, Horridge 2000, 2013). 15 Based on Johansen class of models (1960) of multi-sectoral growth, ORANI suite of models are extensively used by the Australian Federal Government and Productivity Commission, apart from its outstanding academic outreach in policy analysis for countries like China, Indonesia, Bangladesh, Brazil, Vietnam, and many others (Burfisher, 2011; Perali & Scandizzo, 2018; Powell & Snape, 1992; Scarf, 1973 etc.). For a comprehensive overview of use of CGE models for policy reform analysis, see Arrow & Debreu (1954); Dixon & Jorgenson (2013); Dixon & Parmenter (1996); Hertel (1996). Typically, CGE models are based on neoclassical assumptions of microfoundations of consumers and producers behavior, optimizing rational agents, and perfectly or imperfectly competitive market structure (Arrow & Hahn, 1971; Asher & Novosad, 2018). Macroeconomics structure is based on such “bottoms-up” ways where government or policy makers intervene via exogenous policy shocks, which are simulated. Changes in factor supplies, scenarios for technological changes, fiscal policy, and tourism demand are important for investigating the policy impact analysis (WTO 2014/5; Shahraki and Bachmann 2018). Unlike theoretical models, integrating general equilibrium theory with “operational feasibility” is the beauty of such a genre of models. Thus, it has a practical purpose (Dixon & Rimmer, 2002). (Das, 2014) offers a compendium of studies where general perspectives on CGE model structure and several applications in different contexts are presented. 16 Few studies exist for Azerbaijan. Bayramov et al. (2014) is a simplistic 1–2–3 CGE model to study the role of WTO accession, trade-openness, and economic diversification with more focus on non-oil-based growth.

Structure of AZEORANI, Model Closure, and Calibration

AZEORANI (henceforth, “the model” interchangeably) is a comparative static, tops-down, multi-regional model. It is in the genre of Australian school of CGE approach, as best represented by ORANI model and its subsequent development and variations (see Dixon et al., 1982, Horridge 2013; Dixon and Jorgenson 2013, amongst others), with systems of linear equations involving endogenous and exogenous variables (i.e., based on closure, on which more to come subsequently). Typically, the policy reform analysis involves shocking the exogenously declared policy variables or changing the status of variables by swapping or switching between endogenous-exogenous splits. In this model, policy reforms such as efficiency-enhancements or productivity growth, as delineated in the preceding sections, will typically have ripple effects—direct and indirect in first, second, and third rounds as per the case—via intersectoral linkages and spillovers.

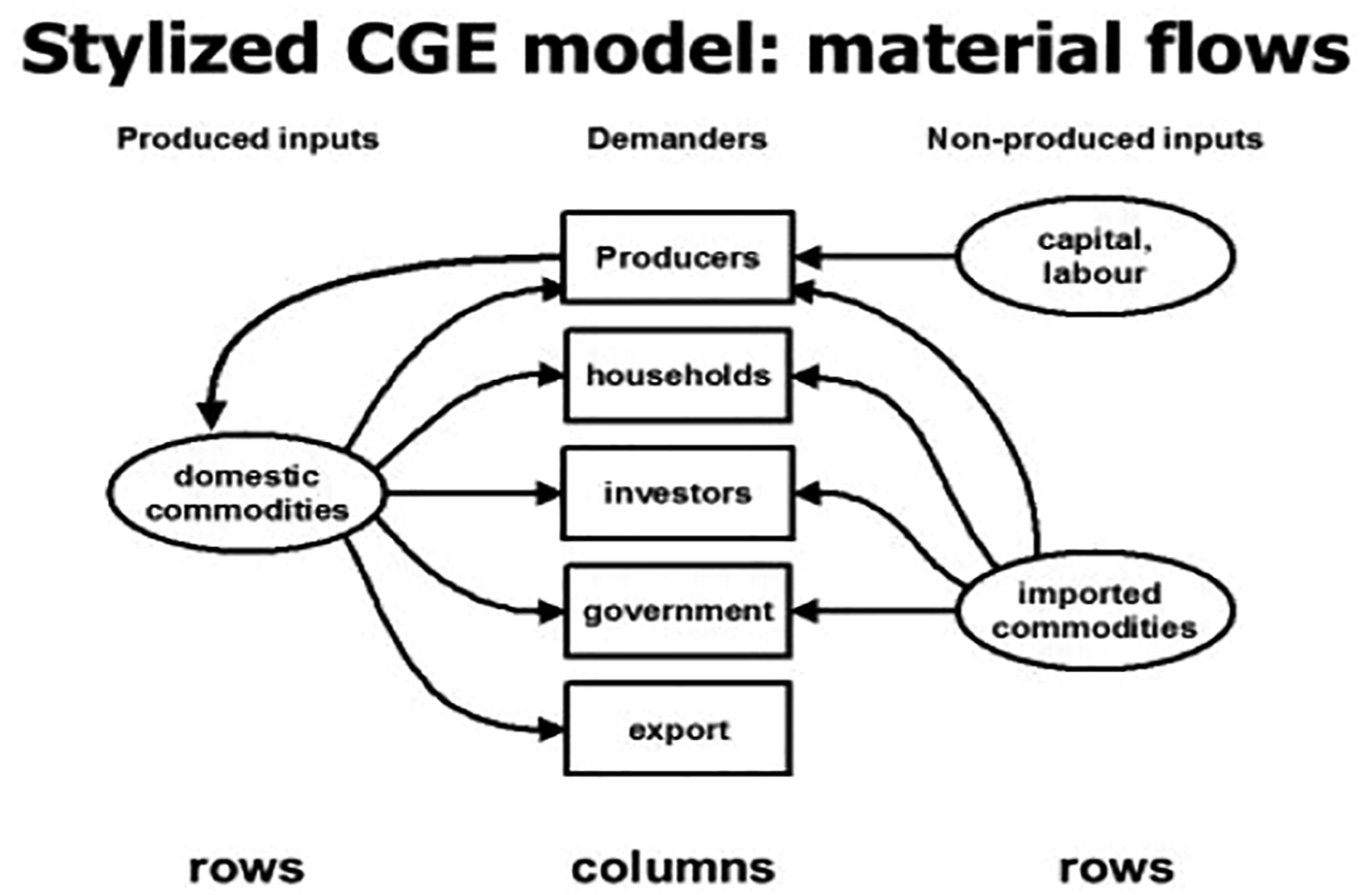

Each agent, in a perfectly competitive economic environment, is a price-taker. Being a small open economy, the assumption of such “atomistic” behavior is realistic. The flowchart (Figure 2) captures the interactions between producers (sectors/firms) and the consumers (households) and the corresponding flows of commodities. Stylized CGE model: Material flows as in the ORANI model (Dixon et al., 1982).

As depicted, producers use primary factor inputs with intermediate inputs to add value. Final commodities have two end-uses: consumption demand and intermediate demand. Households are consumers while producers demand commodities for further production, and investors demand goods and services for producing capital goods and hard infrastructure used for future production. Public consumption is meant for providing basic infrastructure, administrative services, and social welfare facilities. Beyond the border, as a small, open, economy commodities are exported to foreigners to meet their demands (elastic foreign demand), while commodities produced abroad are imported for local consumption. Thus, the categories of agents and their interactions, domestically or internationally, are captured through sets of equations in each block representing material flows. As in the ORANI model, it consists of several equation blocks for production, consumption, and macroeconomic identities (Horridge 2013; Dixon and Jorgenson 2013). Theoretical structure is schematically presented in Supplemental Appendix A (Figure). In the model, producers maximize profits and zero pure-profits condition is satisfied in the long run. There is no joint production and hence, the absence of multi-product firms. Production structure is nested with CES technology while at the top level, production function is Leontief with Constant Returns to Scale (CRTS) in primary inputs, and intermediates. Labor differs across skill types with imperfect substitution among them but are CES—combined to form a composite one. In the case of AZE, we have two occupational labor types—skilled and unskilled. Elasticities of substitution differ across nesting (see below). The production takes place using intermediate goods—imported as well as domestically sourced—with value-added composite of primary inputs in a Leontief top-nest. Then, via the CET function, the final goods are destined for local and foreign markets. Households demand goods for private consumption and each representative consumer is assumed rational and maximizes utility subject to budget constraint. The utility function is based on linear expenditure systems. 17

Consumption by agents are distributed on commodities differentiated by source viz., domestic and imported/foreign. Typically, exports represent foreign demand for home goods and services while imports represent local demand for commodities produced abroad. There are consumption functions for each commodity and source. The substitution between domestic and imported commodities depends on their relative prices. Consumption is constrained by budget availability. The price equations determine “domestic” prices from input-output relationships and from world prices and exchange rates. The price equations are ensuring zero-profit conditions in production and relating domestic prices with international prices via the exchange rate. The market-clearing equations ensure the equality between demand and supply in both factor and goods markets. Investors use Goods & Services for developing new infrastructure and capital goods for further production in the long run.

Important thing of this kind of policy modeling is to “close” the model, by declaring the categories of variables in exogenous (policy shocks as in case of reforms analysis) and endogenous variables which are perturbed by those reform-led impacts. That is precisely called the model “Closure” (more on it is in Supplemental Appendix A). In the current context, we analyze the impact of policies by 2030 and hence a long-run closure is adopted. In this closure, ex post capital reallocations to more productive sectors move the economy in new equilibrium with changes in capital stock in the subsequent periods following the impingement of shocks. With the closure, the validity of the model and the consistency of the model with the database and parameters are checked via performing: (i) real and nominal homogeneity test by shocking the numeraire of the model, viz., the exchange rate (local currency/dollar); and (ii) checking GDP from income and expenditure side to match. Both tests confirm initial data balance and consistency prior to running simulations—baseline and policy shocks (see below in Supplemental Appendix B: Table A2). 18

AZEORANI database and parameters for calibration

AZEORANI Calibration is done using supply-use tables for the economy for year 2011 (in million MANATs) as obtained from the Statistics committee of Azerbaijan, comprising 81 sectors (81 industries and 81 products with no multiple or joint products).

19

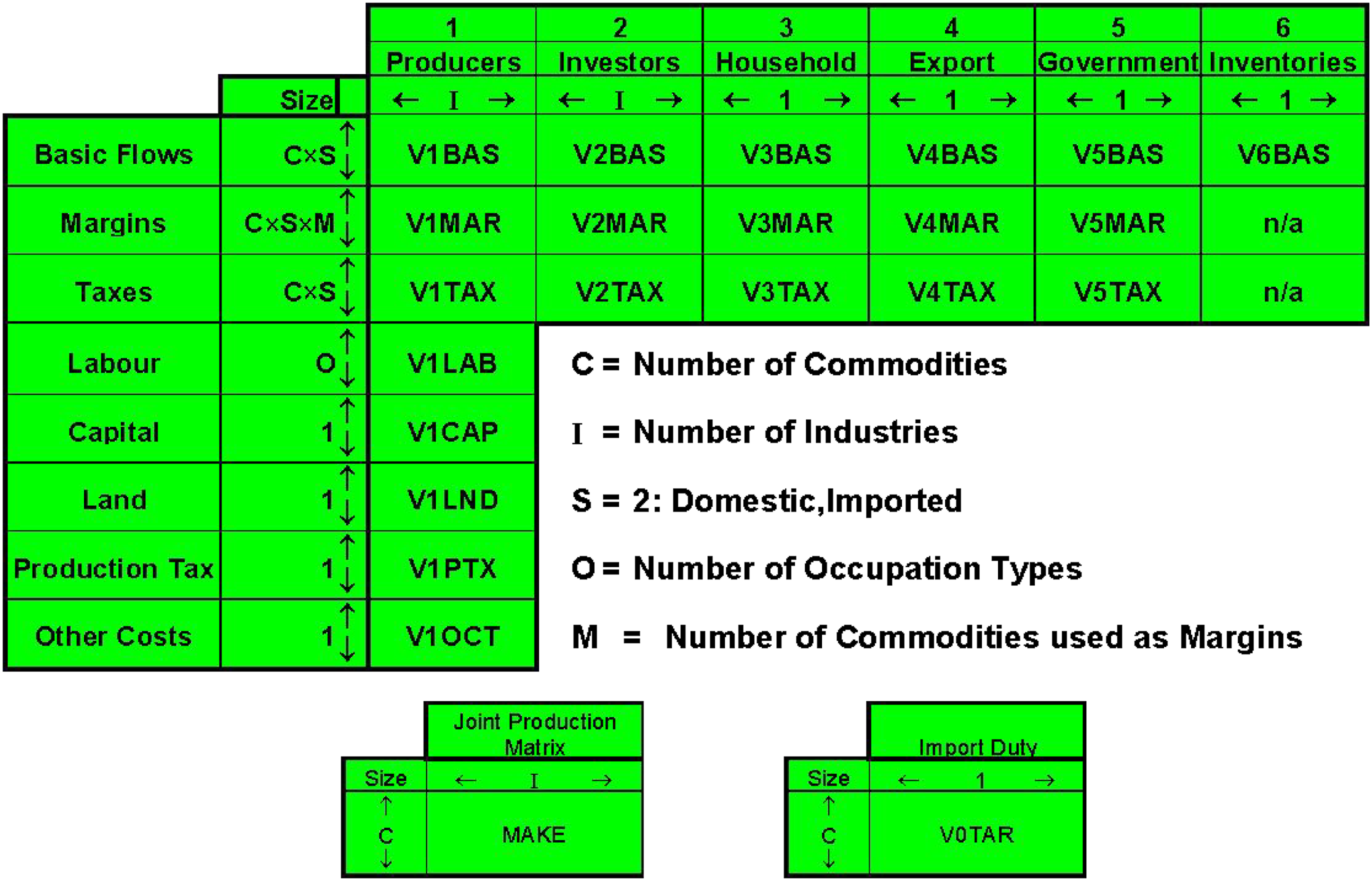

It has all taxes, tariffs and margins and losses. GDP from income, expenditure, and value-added match each other confirming accuracy. Figure 3 depicts the base year database derived by reorganizing the input-output database into several submatrices corresponding to different blocks. Each cell is a submatrix of the model database with the dimensions specified in Row-Column headings. There are 4 mining sectors in the aggregated lower-dimensional database, while in the detailed one there are 7. Structure of model database as in the ORANI model (Dixon et al., 1982).

Row wise, for the 1st row gives total basic values of 81 commodities demanded by all users represented by 6 columns with headings. Second row “margins” represents total values of trade and transport margins or logistics for transfer of commodities—sourced domestically or imported—from producers to users. Not all sectors are used as Margin commodities (i.e., subsets of all sectors). For each sector, rows are split into two—Trade and transport—margins added to domestic sales of commodities, and further divided into four different margins categories, viz., Wholesale trade, Retail trade and Motor repair, and Transport activities, distinguished into land, water, or air. Domestic taxes on goods are recorded in the third row. In AZEORANI, Total labor payments are included in the fourth row with subdivision into different occupational skill categories while the 5th and 6th rows include rental values of land and capital (user cost) paid by producers. Row 7 includes production taxes and subsidies faced by producers. “Other cost tickets” in the last row are costs not recorded in the above rows. “Make matrix” is of dimension “’81 × 81,” and equivalent to the supply-use table and gives the production of commodities by domestic producers. For column headings representing sales structures, we have 5 key demanders, while the 6th column is the inventories (accumulation) at the end of the base year for unsold part of current GDP. There are intermediate and investment demands for each industry. For the producers’ column, the rows 1–3 represent the cost structure of production, including the costs of the intermediates, margins, and taxes.

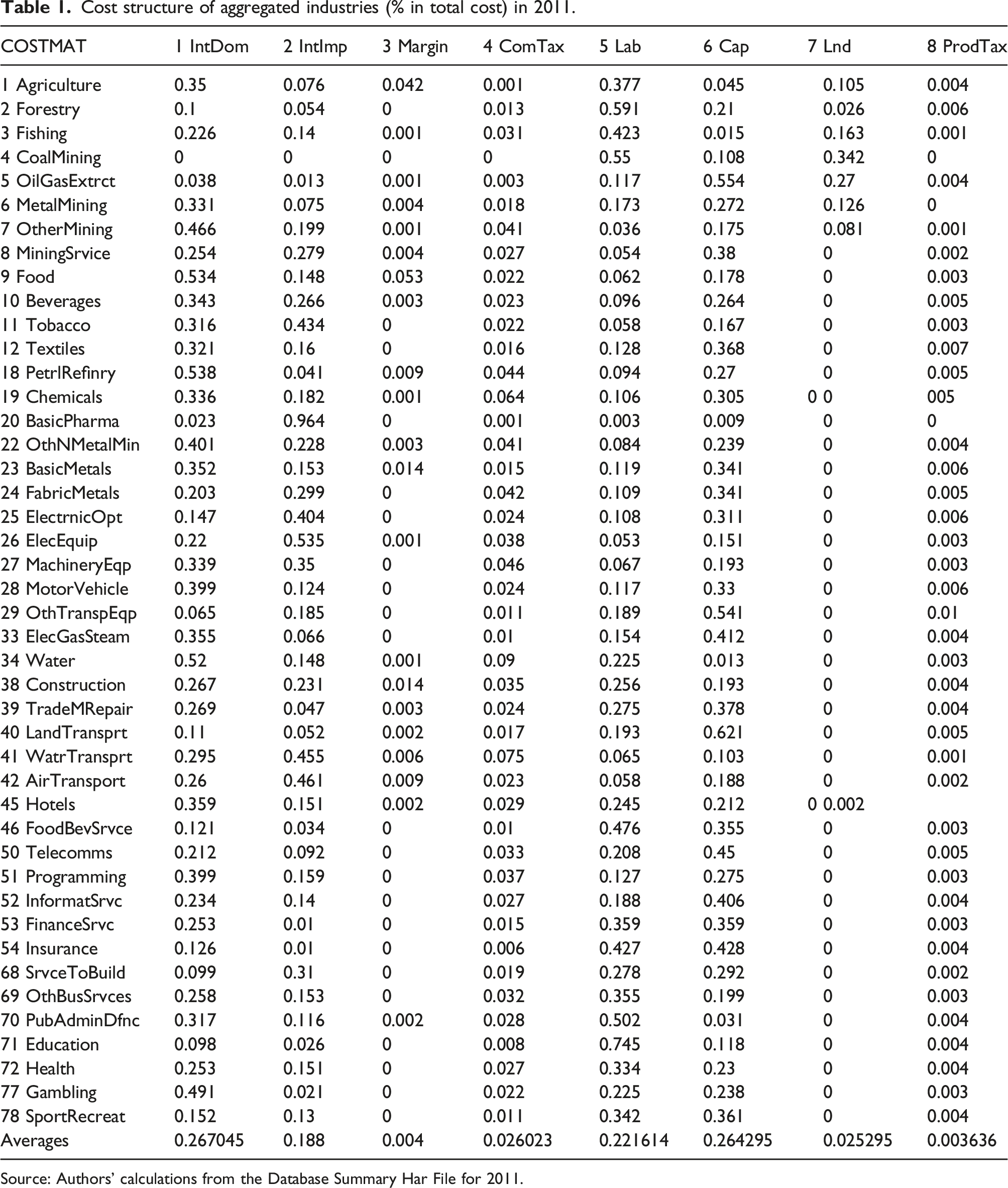

Cost structure of aggregated industries (% in total cost) in 2011.

Source: Authors' calculations from the Database Summary Har File for 2011.

Manufacturing (light and heavy), trade and transport, logistics, services, as well as mining (oil, gas, and extract) are capital intensive. Agriculture, forestry and fishing are labor and land-intensive with the presumption that it is included in the capital by treating land ownership as part of it. Most of the priority manufacturing sectors such as the machinery equipment, motor vehicles, construction, chemicals, mining, electrical equipment, as well as the transport and services have intersectoral linkages via domestic intermediate inputs usage (i.e., backward linkages). Agriculture, food, construction, trade, and transport uses “margins” in their production processes.

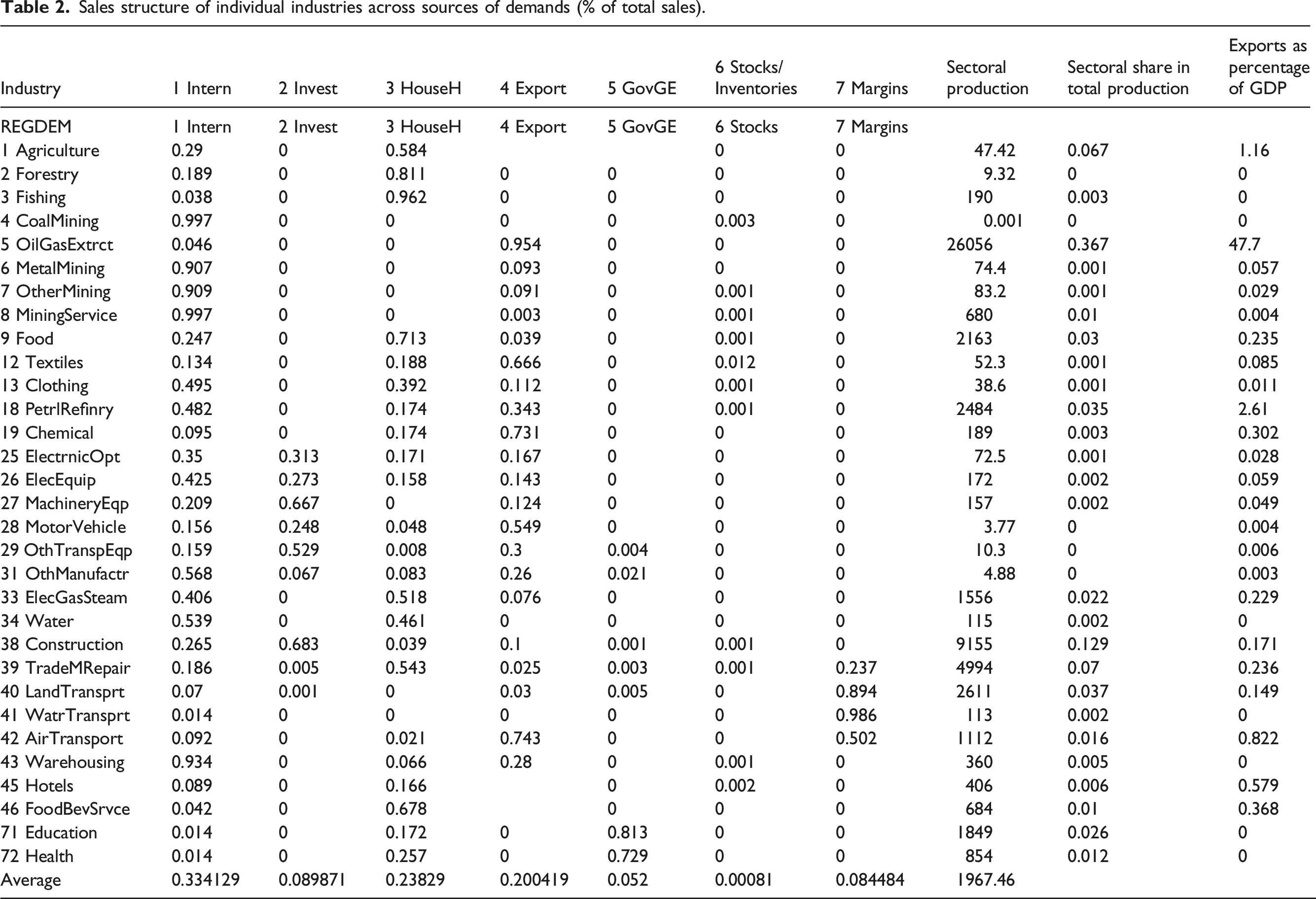

Sales structure of individual industries across sources of demands (% of total sales).

In order to see the export-orientedness, we look at the 5th column of the Table 2 that for oil and gas extractive industries, more than 95% of oil and gas output is exported, followed by chemicals (73%), hotels (74%), textiles (67%), basic metals (54.6%), motor vehicles (55%), tobacco (40%), petrol and refinery (34%), machinery equipment (12.4%), electronic, computer and optical products (17%), mining (9%), agriculture (8.9%), telecoms (4.8%), to mention a few. Except air transport (38.5%), construction, trade and logistics has less share (about 3%). Agriculture, forestry, fishing, beverages, legal services, and government services are used mainly by households and government.

Enumerating policy reforms impacts

Building scenarios and simulations

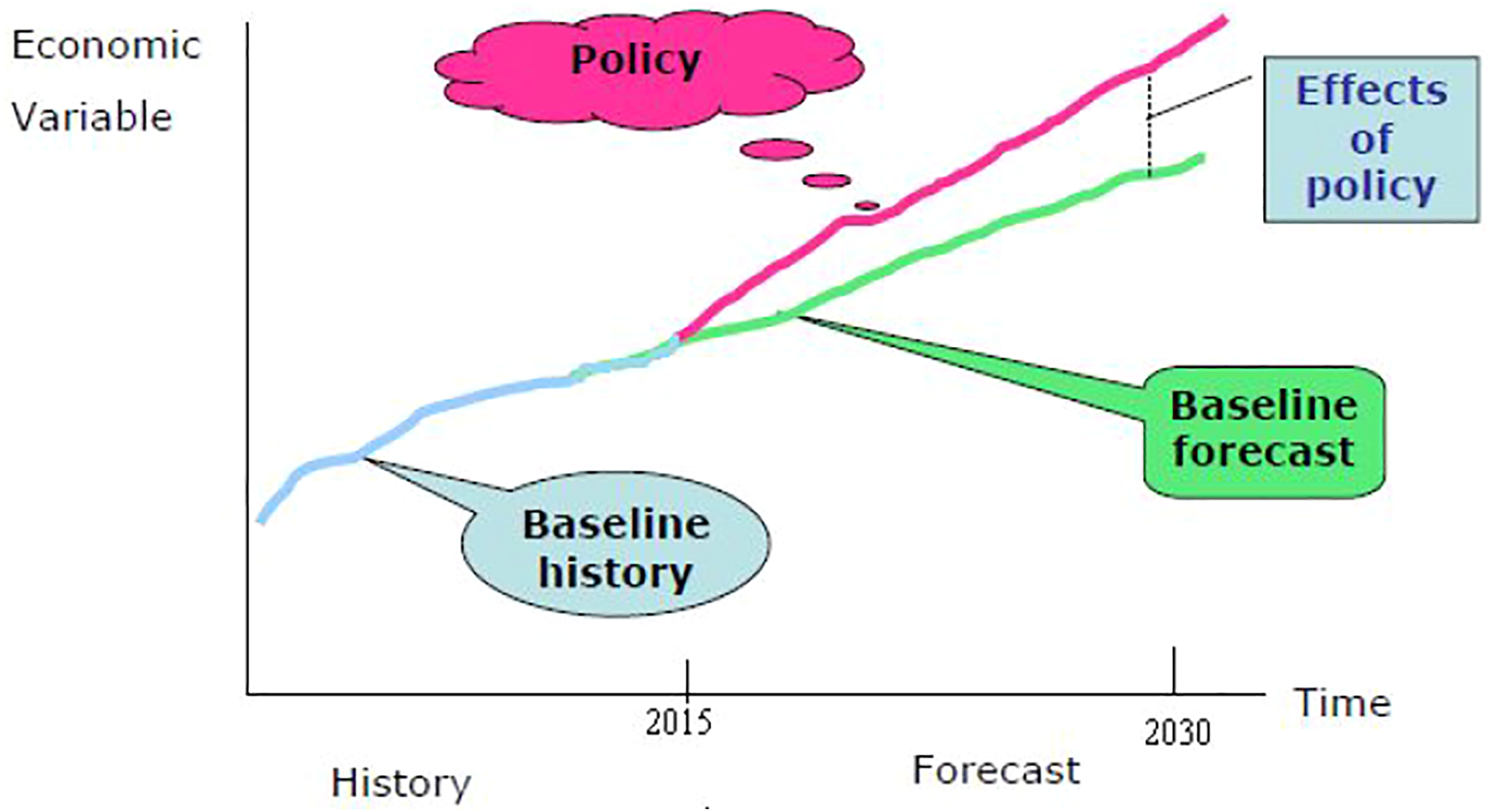

In this section, in a broader perspective we describe—based on SRMs summarized in the Macroeconomic Reforms section and the Business Climate Reforms section—the possible “nature” of simulated impacts in the CGE model. Three “growth visions” are mentioned: (i) Short-run Strategic Visions for 2020; (ii) Long-term Vision for 2025; and (iii) Futuristic Post-2025 Aspirational vision. Consistent with the ORANI-G based models for policy analysis (Horridge, 2014; Dixon et al., 2013), we consider conceptually two kinds of perturbations into the model viz., the baseline scenario as well as policy-induced exogenous shocks. For quantifying economy-wide and sectoral effects of ensuing policy reform-led changes, as described above, we consider two-stages of simulated impact: (a) Baseline where the economy naturally evolves over 2011–30 under certain “normal” dynamic adjustment with the passage of 19 years, such that a new equilibrium database is generated. It captures no policy reforms; (b) Policy reform simulations entailing policy changes after the economy adjusted from one base (2011) to new base (2030). This captures prospective policy repercussions on the economy as the economy moves to a new equilibrium in 2030, but this time at a particular point of time, that is, 2030. The difference between these two changes of the concerned “endogenous” variables captures the pure policy-induced impacts traced between 2011 and 2030 as per reform-led initiatives (see Figure 4). Dynamic and comparative static interpretation of results.

We conduct baseline simulations with no-reforms in practice. Strategic Road Map and NEP gives IMF Forecasts in “basic scenario’ for the economy in 2018, 2019, and 2020 as 2.3%, 2.9%, and 2.5%, respectively (see ibid. p. 43). For the oil sector, growth is going to be 1% compared to 3% in 2018 while for the non-oil sector these are 1.8% in 2018 and 3.4% in 2020.

The economy is assumed to (a) continue following the past strategy, viz., dependence on growth driven by oil and gas (energy sector and exports therefrom) while prices in these sectors remain the same or rise marginally (as per projections from some studies), if not decline further; (b) population growth remains at the same rate; (c) growth rates of other variables (TFP, capital stock, industry growth, labor, land, capital, etc.) and shares remain the same as in the base case; and (d) export growth and import growth depends on projection on the world economy’s trajectory. In particular, under the baseline (BL, henceforth) we assume that the Azerbaijan economy undertakes the business-as-usual (BAU) path.

The baseline shocks are (i) a one-shot forecast approximating annual 2% balanced growth during 2011–2030; (ii) employment increases by 1% per annum, and number of households also by 1% based on population growth rate; (iii) labor productivity augments by 1% per annum uniformly across non-mineral sectors, (iv) capital stock grows in mineral sector by uniform 5%, and (v) oil and gasoline prices fall by 45%, respectively. This moves the economy along the baseline path to 2030 without policy shocks that were administered in 2011 with the updated database of baseline simulations.

As discussed, in keeping with the constraints and prioritized reform, the policy shocks enlisted are as follows: (i) SOE Reform: 10% improvement in productive efficiency in the SOEs. (ii) Investment Boost: Increase in Capital Stock by Foreign Investment induced via increase in rate of return outside mining by 5% (in non-mineral sector). (iii) Enhancing Agricultural Efficiency: Additional 20% annual technological progress in agriculture showing 2030 full repercussions, along with 5% increase in agricultural land due to reclamation of unused land for increasing crop yield (a la NEP/SRM). (iv) Tourism and Transport Boost: Additional improvement in logistics, transport, and infrastructure by 20% per annum, conjointly with increase in tourism export demand by 100. (v) Efficiency in Manufacturing via Technical Progress: Increase in productivity in selected manufacturing by 20% per annum.

Analysis of results 20

Baseline simulations: Macroeconomic impacts

Under this scenario of no reform, as mentioned above, the dynamic evolution of the economy is assumed as uniform productivity escalation and investment. The basis for the assumptions is rooted in history as total factor productivity improvement occurred due to reduction in factor-usage per unit of production. Also, the level of employment and households are assumed to increase by 1% per annum. In this case, the economy is assumed to grow by 2% a year till 2030.

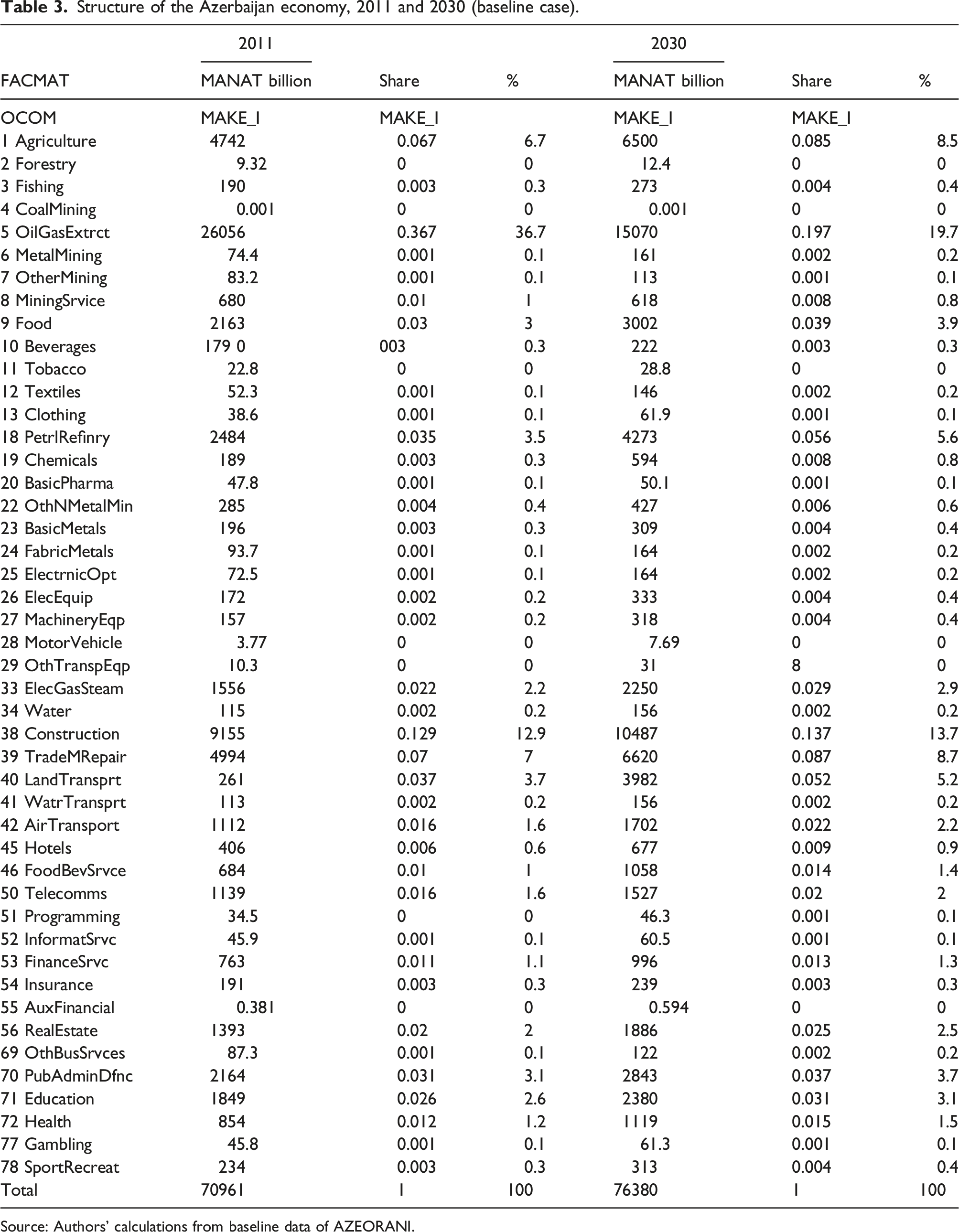

Structure of the Azerbaijan economy, 2011 and 2030 (baseline case).

Source: Authors’ calculations from baseline data of AZEORANI.

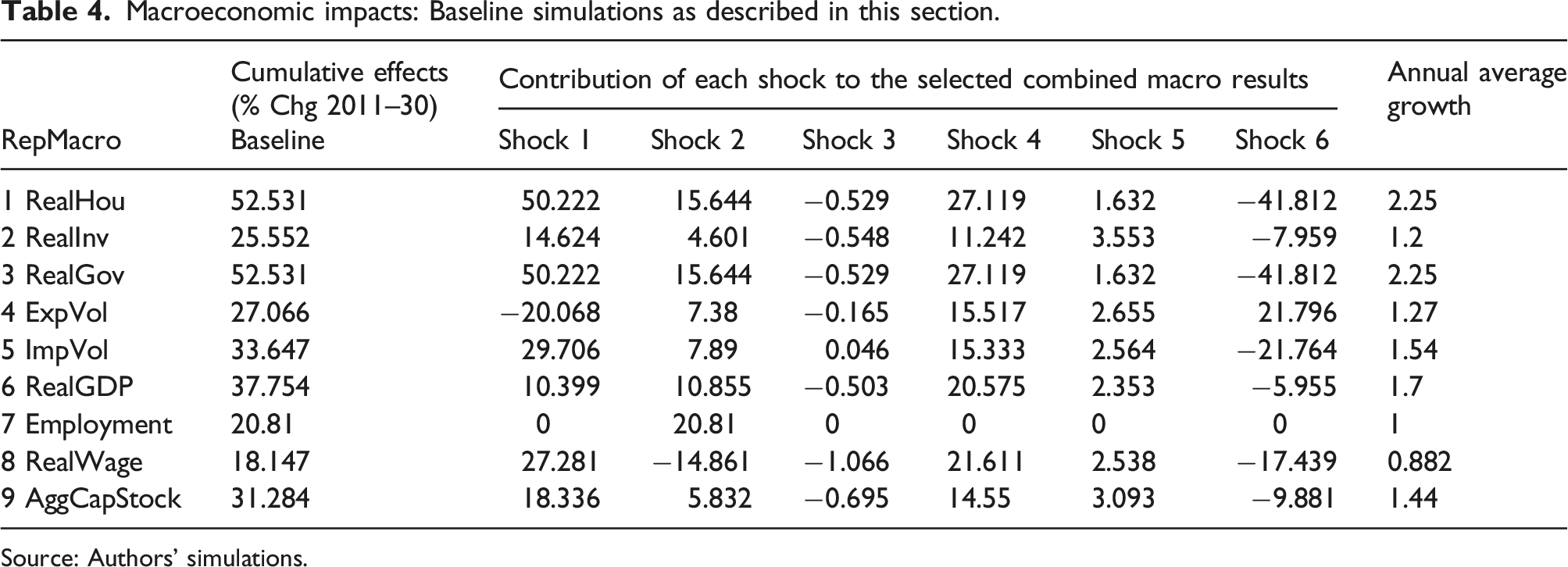

Macroeconomic impacts: Baseline simulations as described in this section.

Source: Authors’ simulations.

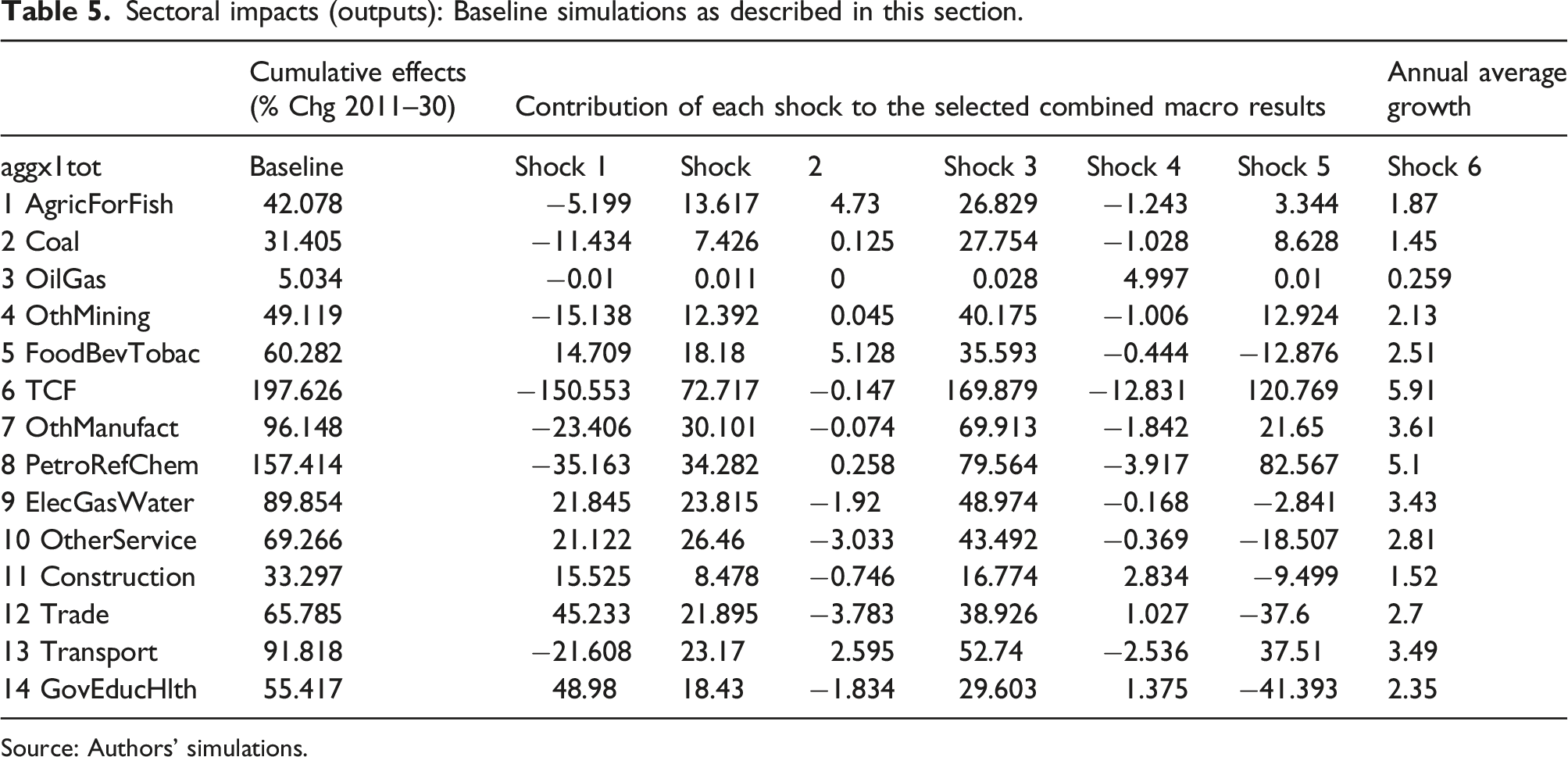

Sectoral impacts (outputs): Baseline simulations as described in this section.

Source: Authors’ simulations.

Looking at the sectoral impacts in Table 5, we observe that in the base case, there is not enough growth in services, transport, and logistics—see the last rows of the table—and also, in agriculture and other manufacturing. As ex post sales structure does not change much from the initial database, we see that there are rooms for sectoral diversification. Thus, it highlights the necessity of structural shifts and economic diversification via product complexity.

Policy reforms: Macro and sectoral impacts 21

As typical of an oil-dependent economies, where resources lead extractive industries, these sectors contribute highly for GDP, production activities, and total exports. These attract FDI into the sector and lead to growth via investment and revenue generated out of these activities via forward linkages as well as backward linkages. Governing these extractive resources is as important as the necessity of structural diversification (Bebbington et al., July 2018).

This is necessary because external adverse shocks might perturb the economy, and with over-dependence the vulnerability becomes apparent. With the booming oil sector and escalation of oil prices, there is a possibility of the presence of Dutch disease. The resultant flows in FDI and foreign exchange might cause exports to fall and hence, contraction of non-oil traded sectors coupled with expansion of non-oil non-traded sectors. This could be the case for Azerbaijan due to the unfolding of global financial meltdown spanning from 2008 to 2011, with contagion effects following thereafter. The decline in GDP growth in 2011 is an indication of this phenomenon. Like other economies such as Kazakhstan, external imbalances and other adversities moved the economy out from the previously established growth trajectories. Diversification into non-oil traded sectors as well as some non-traded sectors—for example agriculture, manufacturing, and services—would help cure the malaise. Tables 2 and 3 show that oil and gas exports and mineral sectors still occupy a significant portion of GDP and exports.

The unsustainability of too much oil-dependence is evident from the fall in GDP in the recent past. Several external forces—shale gas extraction, new fracking technologies, and biofuel replacing fossil-fuels (Das, 2017)—worked against the sustenance of growth in GDP. As per ADB’s ADO (2018), the economy after experiencing fall in GDP growth rate by 3.1% in 2016, has registered 1.7% growth in GDP (and per capita GDP is 0.6%) in 2018—lowest among all the comparator Central Asian nations—and the projected growth rates for GDP and per capita GDP for 2019 are 2% and 0.7%, respectively. According to the World Bank’s GEP (2018), the forecast for annual percentage changes for GDP at market prices are 3.8% (in 2019) and 3.2% (in 2020). 22 As per the IMF forecast, the oil and gas exporters in the Caucasus and Central Asia projections for AAGR of real GDP is 3.7% (2018), and 3.8% (2019). In particular, for Azerbaijan, the non-oil GDP growth is projected to be 3.2% in 2019. 23 In its flagship publication, IMF forecasts for annual percentage changes GDP (at constant prices) are 2.03 (in 2018), 3.86 (in 2019), 3.623 (in 2020), 2.74 (in 2021), 2.71 (in 2022), and 2.61 (in 2023). 24 However, despite external demand for agricultural products and other non-oil exports the recovery after a sharp downturn in 2016 was modest due to OPEC-led cuts in oil production, oil exports slowed down (Global Economic Prospects of the World Bank, 2018). 25 Therefore, we consider scenarios of government supports for policy reform measures with focus on non-oils, viz., productive efficiency and reclamation of land for agriculture sector, total factor productivity (TFP) augmentation, removal of bottlenecks in the State-Owned Enterprises (SOE) to make them efficient for making the business environment “better,” and boost in logistics and tourism for trade and transport.

First, in keeping with the government’s initiative in reforming the SOEs in the medium to long-term (see the sections Quantifying Structural Reforms: The Analytical Framework and Enumerating Policy Reforms Impacts), for improving the soundness and efficiency of the services, the focus is on improving transparency, reducing financial vulnerability, low accountability, and fragmented ownership function. We introduce a 10% increase in productive efficiency by 10% by 2030. These will facilitate functioning and performance of manufacturing and other sectors such as logistics and improve the business environment.

Second, we consider an increase in investment in the non-mining sector with a fixed (exogenous) rate of return outside mining to increase by 5% annually.

Third, we discuss the impact of productivity improvement in agriculture (in the 14-sector aggregated version as well as for the disaggregated 81 sector version). Quite expectedly, this kind of measures would increase growth in agricultural production and exports as agricultural innovation via new practice or even new ideas embedded in new seeds, fertilizers, or irrigation systems, would enable better practices and adoption of such practices would lead to rise in production. This is true for any developing country (see Ogundari and Bolarinwa (2018) for African case studies). Proxying the government’s initiative for such a target under SRM, we introduce a primary factor productivity shock of 20% (cumulative total till 2030). Also, in keeping with the government program of reclaiming cropland for increasing crop yield, we shocked a 5% increase in the stock of agricultural land.

Fourth, in the case of government’s strategic objective of developing external demand and boosting external sector for trade and transport (i.e., indirectly affecting logistics via forward linkages), we introduce a 20% improvement in efficiency of tourism sectors (viz., food, beverages, hotels, and travel agency) by 2030, as well as resultant increase in export demand schedule via rightward shift by 100% over 2011–2030.

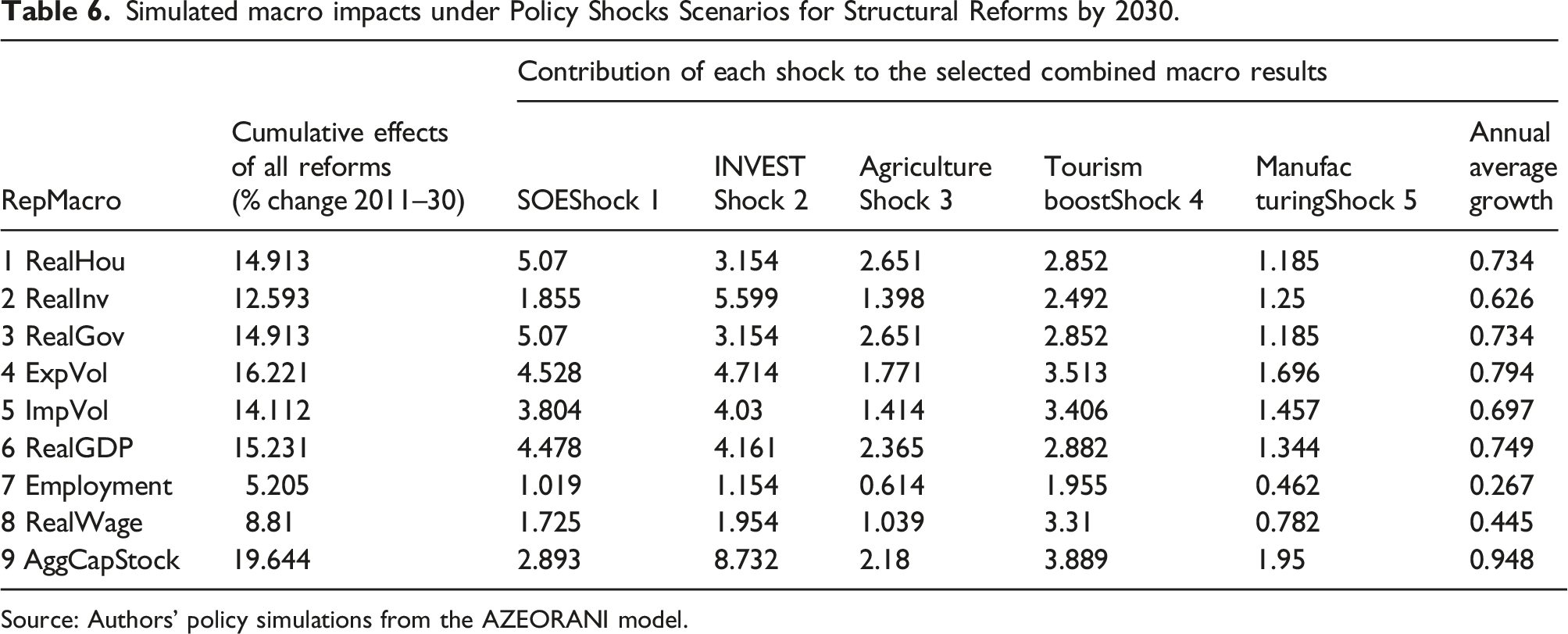

Simulated macro impacts under Policy Shocks Scenarios for Structural Reforms by 2030.

Source: Authors’ policy simulations from the AZEORANI model.

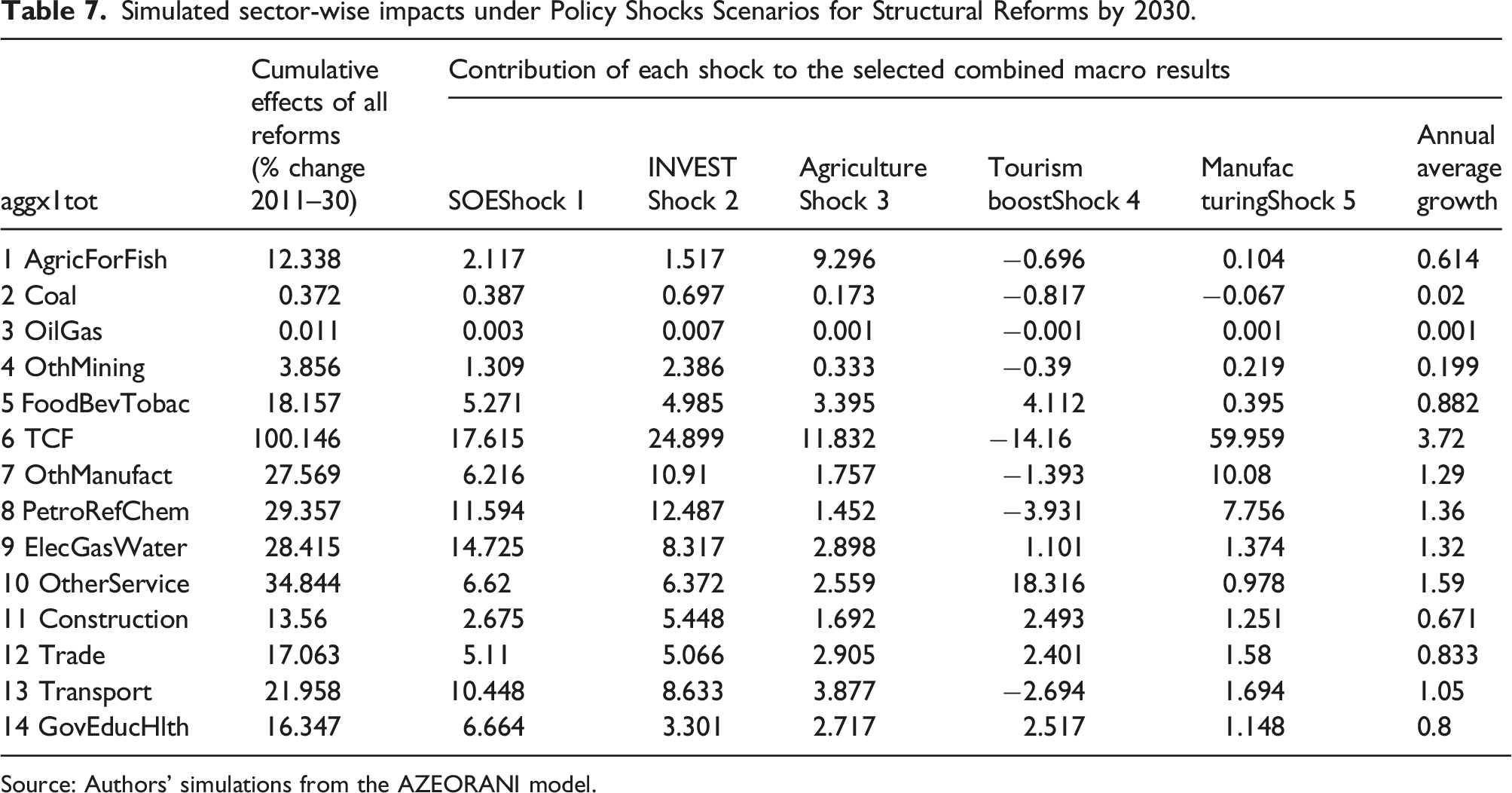

Simulated sector-wise impacts under Policy Shocks Scenarios for Structural Reforms by 2030.

Source: Authors’ simulations from the AZEORANI model.

Similarly, for every sector, we can calculate percentage point contribution/s to each policy shock’s annual average growth rate effects from component-wise cumulative effects, thus, resulting in total percentage changes over a 19 years span of policy-induced impacts. This will enable us to identify productivity-spillover effects via forward linkages, except for a few sectors. From 5.6 and 5.7, for example, we can infer that sectors undergoing reforms have recorded higher growth. However, reforms in say, tourism, investment in non-mineral sectors, or manufacturing make indirect contributions to Petrol and Refinery, Other Manufacturing, Other services. We see that tourism boosts impact positively on construction, other services such as hotels, food and beverages, and postal manufacturing sectors, such as transport equipment, electricals, and electronics, TCF benefit mostly from direct productivity spurts, as well as from shocks pertaining to investment boom, reforms in SOEs as a whole, and quite minutely from agricultural sectors. Overall, the deviations of these CGE estimates from the strategic targets or the projections by the IMF and World Bank can be attributed to implementation of selective reforms in selected fronts, rather than covering “all” of the broad-spectrum of reforms in the SRM for “Aspirational Plan.”

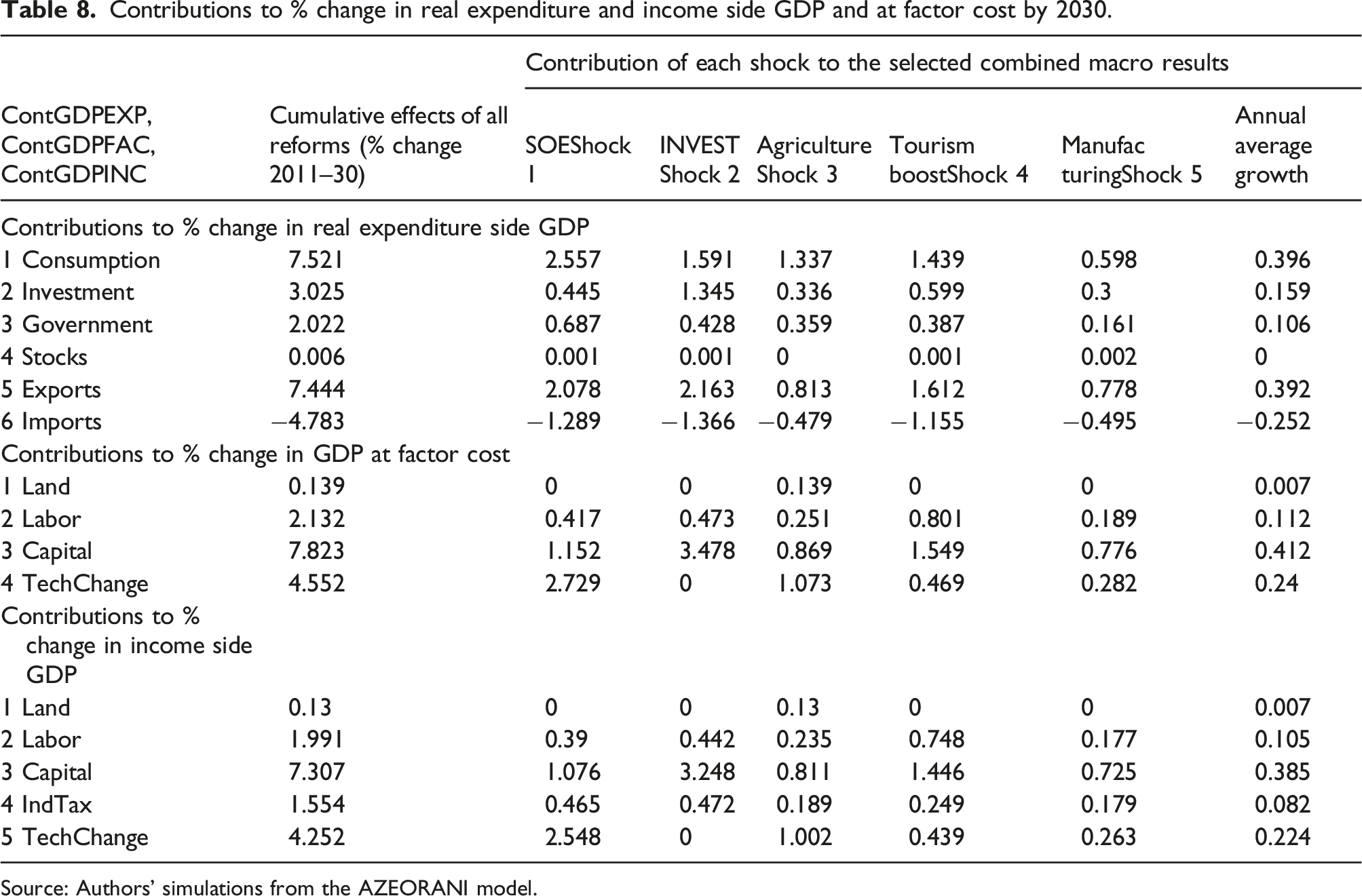

Contributions to % change in real expenditure and income side GDP and at factor cost by 2030.

Source: Authors’ simulations from the AZEORANI model.

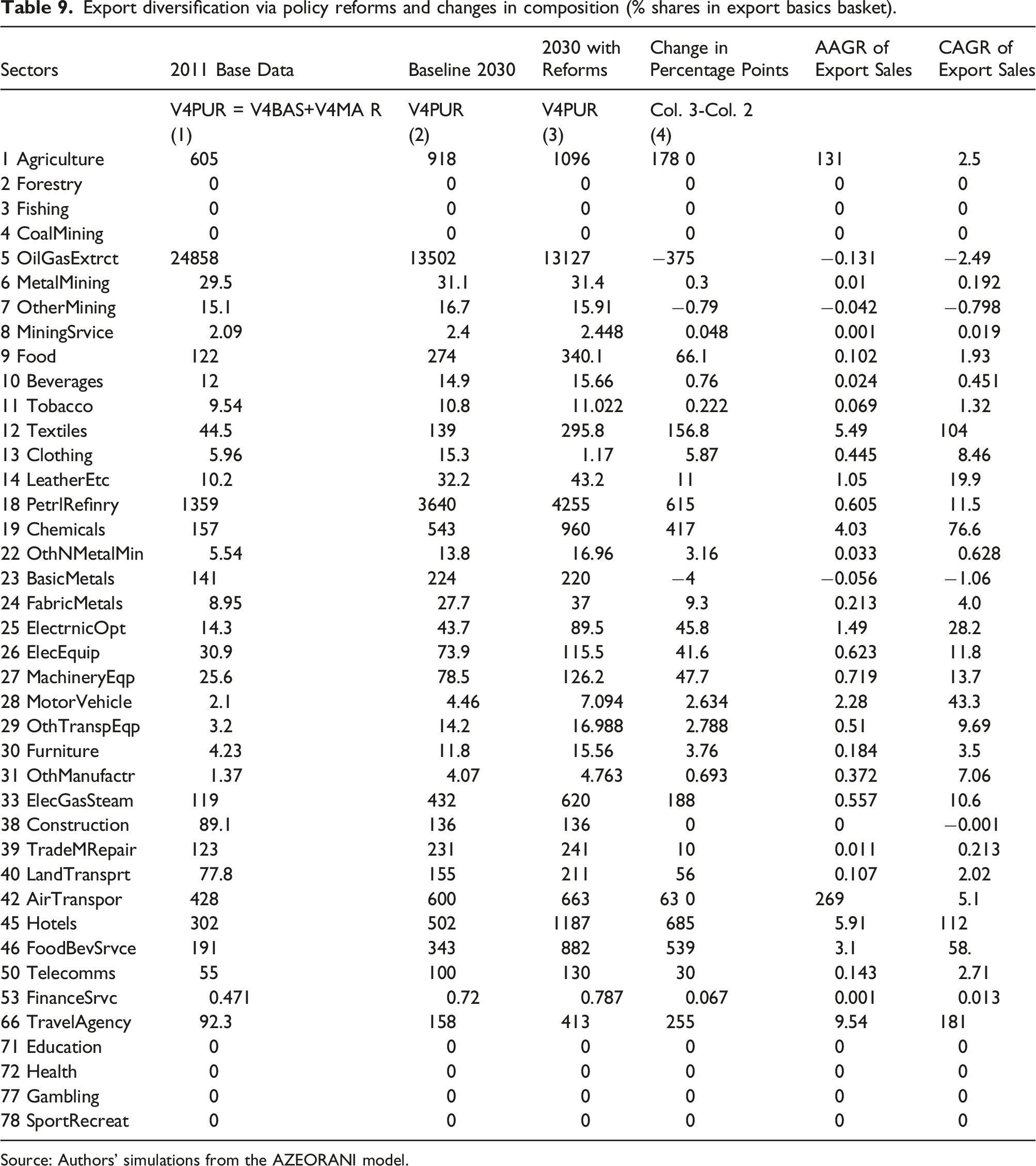

Export diversification via policy reforms and changes in composition (% shares in export basics basket).

Source: Authors’ simulations from the AZEORANI model.

In what follows, we discuss how the proposed reforms enable Azerbaijan economy to diversify the production, resulting in more exports. 26 Breakdown among shock components in Table 8 shows that the main drivers behind cumulative growth effects have been the shocks pertaining to the reforms for increase in investment in non-mineral sectors, SOE reforms, boost in manufacturing productivity, followed by agriculture, and tourism boost. Given the dependence on oil, this kind of diversification (under our current conservative policy shocks with just 1% and 1.5%) is conducive for becoming non-susceptible to external vulnerability. In the same vein, looking at Table 9, we can see that there have been compositional changes in export baskets as envisaged in percentage changes in shares in export basket from base case to baseline simulations to policy reform scenarios. From Table 9, exports rise has been mainly driven by increase in investment in non-mineral sectors, followed by efficiency improvement in services (and SOEs), tourism and manufacturing while imports shrank, which enables Azerbaijan to register improvement in trade balance.

On the trade front, we see from Table 6 (rows 4 and 5) that volumes of aggregate exports increase by more than that in aggregate imports and most importantly component-wise except tourism boost all other reforms have more pronounced effects on export volumes than the import volumes (columns for rows 4 and 5). Contribution of trade balance (BOT) is 2.7% (cumulative) and 0.14% (AAGR). However, due to implementation of reforms these sectors, especially the agriculture, chemicals, manufacturing, transport, hotels, and food and beverages under tourism expands, while exports of oil and gas contracts by miniscule percentage points. The changes have been modest, as we do not implement full-fledged reforms in all the sectors at present. However, the result is pointer to the fact that reducing dependency on oil via diversification of production and achieving efficiency via improvement of business environment facilitate such transition to stable growth and employment. Tourism boost clearly contributes mostly to external demands for hotels, foods and beverages, and travel agencies. But, for all other four reform scenarios. The impacts are substantial for percentage changes in demand for export basics. 27

Because of concern about inclusiveness or shared prosperity, the impact at the regional level needs attention. Regional differences in impacts in the light of the Strategic Road Maps is crucial as prosperity offers scope of cooperation and regional integration for economic development and other initiatives through institution building. In fact, the government has goals and sub goals for improving regional business climate improvement, infrastructure, agricultural development via irrigation, and socio-economic development. This is crucial for inclusiveness and shared growth.28 This implies that boons of structural reform-led growth should spread across the regions. Given paucity of data, we refrain from such analysis; however, the direction of potential impacts obtained from CGE simulations makes us to conjecture that perceived benefits from such reforms could augur well for sustained inclusive growth.

Concluding remarks

In this section, we summarize the policy results in the context of economic reform measures in Azerbaijan in the light of experiences of other nations—cases of miracle or debacle—to identify, if any, role models. For example, cases of Venezuela and Nigeria—being trapped in paradoxes of plenty—as opposed to other comparator countries avoiding the Dutch disease cases, such as Norway or USA, could be a lesson for policy formulation (Bjørnland et al., 2018). While these two African nations could not avoid the curse of too much oil-dependence, Norway has been able to avoid the resource-trap via resource reallocation effect of revenue generated via oil. In the case of Ghana registering around 8.9% growth—with major oil off-shore deposits—apart from oil, cocoa and gold exports is another source of growth, while trying to diversify the economy into manufacturing, education, agriculture, for job-oriented sustainable growth objectives via strategic channelizing of oil revenue.29 IMF country reports (September 2016) projects that GDP (at constant prices) will grow at 2.9% in 2019/20, and the policy reforms that we analyze in this report closely matched that projection.

Economic diversification into non-oil sources of growth should be part of the Azerbaijan reform agenda but not its core. We have seen that macroeconomic risks and high cost of finance are two areas that need immediate attention and prioritization from policy makers. In addition, several small-scale and large-scale reforms are needed to augment infrastructure and human capital, which serve as fundamental blocks of economic development. SOEs need to be made more efficient and favorable regulatory business environments need to be crafted to create space for private entrepreneurship. However, this is not enough. Beyond investments, the creation of frameworks that provide strategic directions to reforms is critical. Case in point is infrastructure policy, state ownership policy, and market development policy that still needs to be developed. The planning and coordination among a multitude of institutions to push the reform agenda forward is as important. The objective, regular and transparent measurement of successes as well as failures in the reform process is critical for policy maneuvering. Finally, ensuring that Azerbaijan is undergoing an inclusive economic transformation through its ongoing reform should be at the forefront of the government agenda.

Supplemental Material

Supplemental Material - Key binding constraints, structural reform, and growth potential of Azerbaijan via economic diversification: A computable general equilibrium policy impact analysis

Supplemental Material for Key binding constraints, structural reform, and growth potential of Azerbaijan via economic diversification: A computable general equilibrium policy impact analysis by Gouranga Das, Edimon Ginting, Aimee HampelHampel and Mark Horridge in Journal of Eurasian Studies

Footnotes

Acknowledgments

The authors acknowledge ADB for funding this work and for its generous support. The paper benefited from discussions with various government stakeholders in Azerbaijan. The authors gratefully acknowledge extremely valuable comments and useful suggestions from two anonymous reviewers of this journal. Usual caveat applies.

Author’s Note

This paper is derived from the Azerbaijan Country Diagnostic Study of the Economic Research and Regional Cooperation Department of the Asian Development Bank.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Asian Development Bank.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.