Abstract

Previous research investigating the UK economy impacts of introducing a new Scottish CO2 Transport and Storage (T&S) industry linked to carbon capture and storage (CCS) has focussed on supply chain and funding requirements in introducing such a new sector to service proximate Scottish industrial emissions via onshore pipelines. However, Scottish plans extend to shipping CO2 from outside Scotland for storage in North Sea reservoirs by also servicing sequestration requirements from elsewhere in the UK and/or overseas. This will involve investment in greater industry capacity but could ease associated domestic funding requirements. Here, we introduce improved economy-wide structural (input-output) data reflecting how a Scottish T&S sector may emerge from current Oil and Gas industry supply chain capacity to a computable general equilibrium (CGE) model, extending to simulate emergence of an export base. Our central finding is that exploiting overseas T&S export opportunities is crucial where the policy aim is to generate greater economic activity without increasing demands on the public purse. However, any extent of real wage bargaining and consequent producer cost pressure as labour demand increases will act to dampen expansionary power, displacing export production and employment, while driving consumer price impacts that limit real income and public budget gains.

Keywords

Introduction

Following the 2019 UK Climate Change Committee’s report (CCC, 2019), the UK Parliament amended the 2008 Climate Change Act 1 so that the UK now has a fixed goal of achieving net zero by 2050. However, the climate and energy policy trajectory in enabling the required economy-wide transition in less than three decades is complex in the UK, as in other nations. This is not least in the face of post-Covid economic crises exacerbated by energy supply and security challenges and exacerbated by Russia’s invasion of Ukraine.

Thus, the CCC’s (2019) highlighting of the necessity of action on several cross-cutting climate change mitigation actions – including but not limited to the implementation of carbon capture usage and storage (CCUS) in industry, hydrogen production and power generation – gains urgency from a wider energy and public policy perspective. That is, there is a pressing need to act in enabling diversification of the energy mix in ways that extend the lives of fossil fuel power plants and ensure a more secure and affordable energy mix, alongside sustaining jobs and real incomes in currently emission-intensive industries and supply chains.

A foundation for UK policy action on CCUS in particularly was provided in the CCC’s (2019) recommendations to establish CCUS in regional industry clusters capturing at least 10 MtCO2 per annum by 2030. Government responded with a refined aim of having two clusters operational by mid-2020s, while aiming for four clusters by 2030, but with the objective of capturing up to 10 MtCO2 a year (HM Government, 2020), with a focus on industrial emissions. Two clusters, in Merseyside (the Hynet cluster) and the broader Humber/Teesside (the East Coast cluster) regions, were selected as ‘Track 1’ of the industrial CCUS ‘cluster sequencing’ rollout in 2021, followed in 2023 by two more in Humberside (Viking) and Scotland (Acorn) in the subsequent ‘Track 2’.2, 3

For Scotland, the CCC (2019) recommendations included a 2045 net zero target, introduced into law by the Scottish Parliament via the Climate Change (Emissions Reduction Targets) (Scotland) Act of 2019. 4 The closer target for Scotland reflects (among a wider low carbon resource potential) the greater capacity of the devolved nation for CO2 removal and storage compared to the rest of the UK. The Scottish CCUS cluster involves the Acorn project, 5 linking offshore storage capacity – via a terminal at St Fergus in the northeast of Scotland – to industrial activity concentrated in the east. However, the Acorn project is also designed to service sequestration demand from other UK clusters or overseas, primarily via the Peterhead Port facilities. 6 Here, servicing emissions from outside Scotland would require shipping rather than pipeline transportation, an aspect of UK CCUS capacity and capability where the UK Government has recently received recommendations to develop a strategy by 2024 (Skidmore, 2023).

This paper considers the potential economy-wide implications of the Scottish Cluster further developing its CCUS network to provide transport and storage services for CO2 captured either in other UK locations or abroad. Our specific research question is whether a new Scottish CO2 Transport and Storage (T&S) industry, capable of servicing sequestration demand beyond the Scottish cluster, could deliver greater wider economy gains – with a policy and political focus on job creation (BEIS 2021) – while relaxing domestic funding constraints involved in ensuring utilisation of invested capacity. Our key finding is that exploiting overseas T&S export opportunities may be crucial where the policy aim is to generate greater economic activity and employment opportunities without increasing direct demands on the public purse.

We build on an earlier study by Turner et al. (2021) published in this journal, using a UK computable general equilibrium (CGE) model to examine the potential wider economy impacts of establishing a Scottish T&S industry. As in that earlier work, use of a UK-wide model is motivated by policy action on the CCUS rollout being reserved to Westminster Government, including responsibility for providing funding, with specific focus here on the need to ensure demand for utilisation of the capacity created in relatively infrastructure-intensive activity. We also follow Turner et al. (2021) in using the supply chain structure of the existing UK Oil and Gas (O&G) industry as a benchmark for the nascent T&S sector but update the CGE model’s social accounting matrix (SAM) to incorporate more recent and detailed information on the input mix of that benchmark. This leads to an additional key finding regarding the importance of initial assumptions, particularly in terms of the likely capital intensity of a nascent industry like T&S, and how this impacts the value of output supported and the extent of wider economy expansion triggered.

We also extend previous analytical and policy focus by considering different specifications of, and scenarios for, the Scottish T&S industry. This incorporates the Turner et al., (2021) focus on a case where the transportation of captured CO2 is done exclusively through domestic pipelines (in only when servicing Scottish sequestration requirements). However, we introduce consideration of cases where transport involves a combination of pipelines and shipping, with the latter enabling other UK or overseas demand for T&S to be serviced. Here, the consensus of industrial stakeholders associated with the Scottish ACORN CCS project is that, at least initially, international rather than domestic (UK) marine transportation services are likely to be used in transporting CO2 captured outside of Scotland. 7

We contribute to a growing literature considering the economy-wide impacts both of CCS (e.g. see Le Treut et al., 2021; Vennemo et al., 2014) and the introduction of new industry activity (e.g. Mukhopadhyay and Thomassin, 2011; Phimister and Roberts, 2017). Moreover, in extending focus and scope to consider expansion of T&S industry capacity – and fuller utilisation offshore CO2 storage capacity – we add a novel dimension to input-output and CGE modelling literatures on the implications of new industry development involving an export base (e.g. Ha and Swales, 2012; Zhou and Latorre, 2014) and the emerging literature on issues and challenges around nascent industries required for the net zero transition (e.g. Bonsu, 2020; Pollitt and Chyong, 2021).

The remainder of the paper is structured as follows. The Methods section sets out our CGE methodology and details our simulation strategy. In the Results and analysis section, we present and discuss the key findings from our analyses, followed by a Sensitivity analysis section. The Conclusions section summarises our key conclusions and makes suggestions on future research.

Methods

The UKENVI CGE model

We follow Turner et al. (2021) in using the UKENVI model of the UK. Here we update UKENVI using more recent and sectorally detailed industry-by-industry input-output data (reported by the UK Office for National Statistics, ONS 8 ) to develop the 2018 SAM used in calibration, which is assumed to representing the real economy with no other changes in our base year of 2022. 9 One key feature of the update is that the existing O&G industry, which we follow (Turner et al., 2021) in using as a benchmark for CO2 T&S activity, is now separately identified in the 2018 data. 10 The key implication is that the Scottish T&S sector introduced here – where we identify two variants of the Scottish T&S industry to reflect the different transportation approaches considered – is more capital and less labour-intensive than the one studied by Turner et al. (2021). That is, a similar capacity created generates a smaller output and, thus, value of demand, and direct employment is lower (see Result and analysis section).

We provide a high-level description of the key features of UKENVI for the application presented here, with more detailed descriptions provided by Turner et al. (2022a, 2022b).

Production and investment

There are 34 producers and commodities, including the new T&S sector, which we disaggregate from O&G at a base (pre-simulation) scale of 0.2% of the original O&G industry. The base year value of imported and domestic intermediate, and labour and capital inputs to each production sector is provided by the SAM.

Sectoral capital stocks are adjusted on a year-by-year basis, using a recursive dynamic process. Investment is endogenous, covering depreciation and a fraction between the actual and desired capital stock. The only exception is the T&S sector where investment is exogenously determined to model the initial oversizing required prior to the sector becoming operational. In the long-run equilibrium, the actual matches the desired capital stock in all sectors, with any further investment simply offsetting depreciation.

Labour market

We assume a fixed labour supply, with an initial pool of unemployed workers where producers can source additional labour. Data are not available to model any sector-specific skills, so there is free movement of workers between industries. However, we do attempt to capture the impacts of the UK labour market constraints by modelling a real wage bargaining process (Blanchflower and Oswald, 2009).

The base year (full-time equivalent, FTE) unemployment rate, 4.1%, is given by ONS data for 2018. Workers have greater bargaining power as the unemployment rate falls and vice versa. The effect of unemployment rate on the real wage rate is determined by ε, the elasticity of wages relative to the unemployment rate. The central value of ε is 0.113 (Layard et al., 1991), with sensitivity analyses (see Sensitivity analysis section) considering cases where we set a low (0.05) and a high (0.2) value to consider the impact of variations in the bargaining power of workers. We also explore the importance of how real wages are determined on the potential outcomes, by adopting an alternative labour market closure where we fix the real wage rate.

Household consumption

We identify an aggregate representative household, with income mainly composed of earnings from employment, capital income and government transfers (fixed in real terms) and consumption is determined by total income net of taxes and savings and responsive to changes in income and relative prices.

Trade

In our single nation model, the UK trades with a single external rest of the world (ROW) region. The prices of the ROW goods and services are fixed, with the volume of imports and exports affected by the relative price changes between domestic and external goods and services (Armington, 1969).

Government

The government budget (GB) is given by

GY corresponds to the government revenue, where income tax is the largest component. The government also receives revenue from other taxes (e.g. the indirect business tax), capital revenue and foreign remittances at a fixed exchange rate. GEXP reflects the government expenditure following

GQ is the real government spending on goods and services (including T&S), which is fixed and exogenously determined and nominally adjusting for changes in the government price index Pg. Government transfers to households (TRG hh ) and firms (TRG firms ) are also fixed in real terms, with government spending adjusting in line with the consumer price index (CPI). We do not impose a balanced budget; hence, the impact of supporting Scottish T&S is reflected on the value of GB.

Scenario simulation strategy

We simulate the introduction of a T&S industry to service, at a minimum, clustered Scottish industry CO2 sequestration requirements, but with potential to also service demand from the rest of the UK (RUK) or overseas (ROW). Our simulations involve introducing the necessary T&S industry infrastructure over a 4-year period (2023-2926) before the sector becomes operational in year 5 (2027). Capital requirements and demand levels vary by scenario, drawing on estimates provided by Calvillo et al. (2022), depending on emissions levels sequestered and associated transportation requirements.

A common assumption across scenarios is that the UK Government must cover the costs of guaranteeing utilisation of capacity where emissions generated within the UK emissions are sequestered by Scottish T&S for storage in North Sea reservoirs. We assume that this involves deficit funding, abstracting from any potential options to balance the budget and/or recover the cost of T&S services, motivated by the need to isolate and identify fundamental impacts on the public budget.

We consider three separate scenarios depending on which sectors are serviced and how: • Scenario 1: Scottish T&S industry services Scottish cluster demand only (3.83 Mt CO2 per year), involving domestic pipeline transportation, where the UK Government guarantees demand for utilisation of all the capacity created from 2027. This is in line with current plans to repurpose the main Feeder 10 onshore pipeline infrastructure and use the Goldeneye field in the Scottish North Sea for storage. • Scenario 2: Scottish T&S industry services Scottish cluster plus some other UK cluster demand (6.38 Mt CO2 per year), involving the use the services of the international ‘Marine Transportation’ (shipping) services to transport the additional 2.55 Mt from RUK industry clusters, expanding North Sea storage capacity beyond Goldeneye. The UK Government guarantees demand for full utilisation of capacity created. • Scenario 3: Scottish T&S industry services Scottish cluster plus overseas export demand (6.38 Mt CO2 per year), also with the use of international shipping services and expansion of Scottish North Sea storage capacity to sequester the additional 2.55 Mt, now from overseas industry clusters. Here the UK Government only needs to guarantee demand for capacity created to sequester the 3.83 Mt of CO2 generated in the Scottish cluster.

Our sensitivity analyses centre on the importance of labour market responses, with focus on Scenario 3. First, we vary the elasticity between real wages and the unemployment rate in equation (1) above. This allows to capture how the potential outcomes vary depending on the power of workers to bargain real wage rates. A high elasticity is representative of greater bargaining power (unemployed workers will require a higher real wage rate offer to move back into the labour supply), while the opposite is true for a low elasticity. Second, we consider how outcomes compare to one of extreme real wage rigidity. Here, assuming a fixed real wage across the UK labour market means that, even in the presence of a persisting labour supply constraint, nominal wage costs faced by all producers only change in line with the CPI.

Results and analysis

Introducing the Scottish CO2 T&S industry

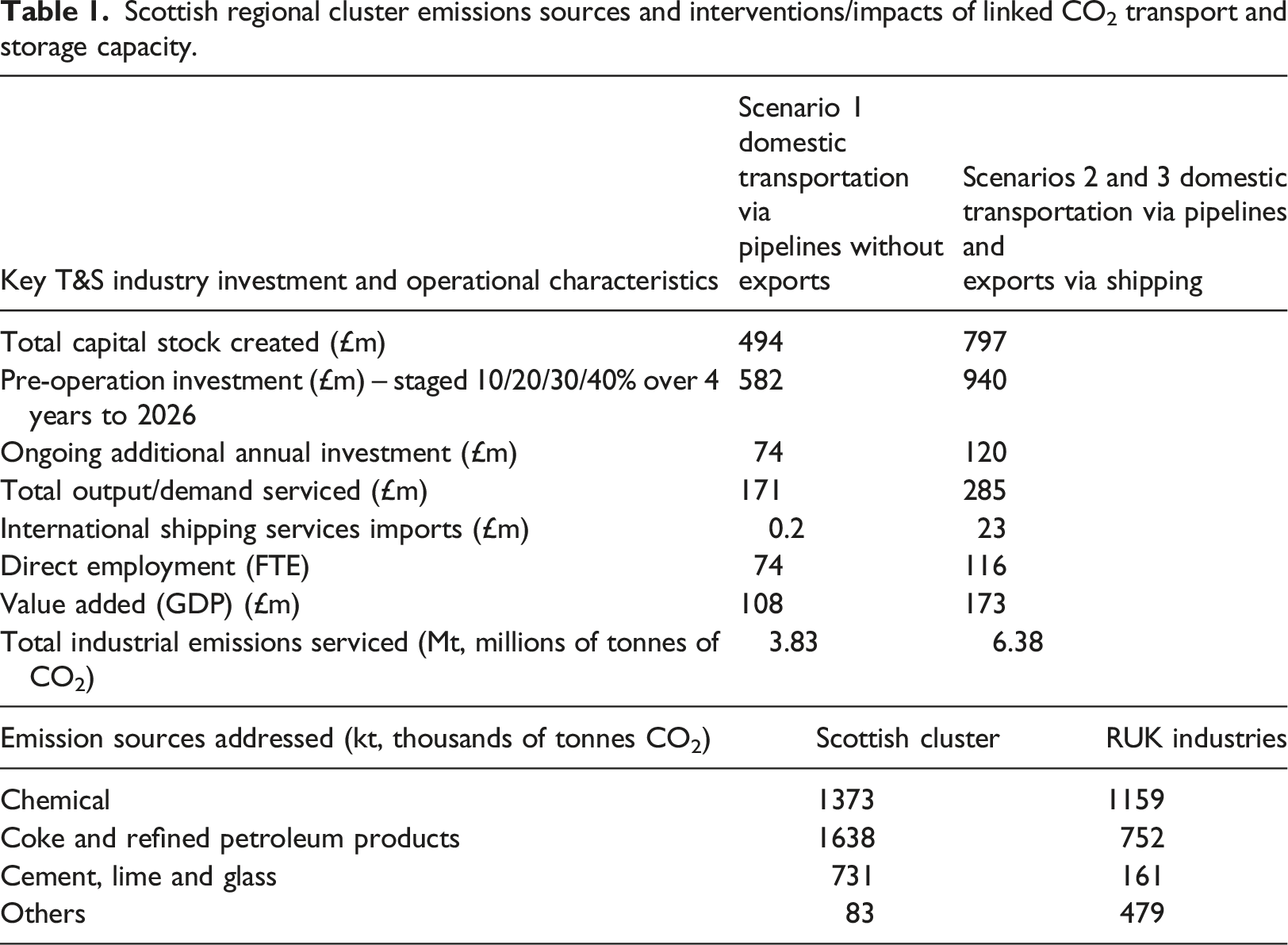

Scottish regional cluster emissions sources and interventions/impacts of linked CO2 transport and storage capacity.

Full operation of the capacity created supports £171m in annual output to sequester the 3.8 Mt (millions or mega tonnes) of CO2 captured across the Scottish cluster. This is associated with direct T&S industry employment and value-added/GDP (payments/income to labour and capital providers) gains of 74 FTE workers and £108m per annum, respectively. Subsequent annual T&S investment (£74m per annum) simply comprises maintenance, repairs and offsetting depreciation. 11

The capital intensity of the new industry is reduced if capacity is increased to service demand for Scottish T&S services from capture activity beyond the Scottish industrial cluster. Rather than expanding the pipeline infrastructure proportionately with the growth in capacity, this involves drawing on (imports of) international shipping services to bring in CO2 for storage via the Peterhead port. 12 The figures in the second data column of Table 1 align with a scenario suggested by colleagues associated with the Acorn CCS Project, 13 which involves a potential industry picture where 40% of the total industry capacity involves sequestration of CO2 shipped in from outside of Scotland. This could be from elsewhere in the UK (Scenario 2) or from overseas (Scenario 3).

In either case, the capital stock increases to £797m, which requires a pre-operational total investment of £940m. This is again introduced incrementally in 10%/20%/30%/40% shares over the 4 years between 2023 and 2026. Delivery of the increased annual T&S industry output – £285m, associated with storage capacity of 6.38 Mt of CO2 – now involves importing £23m of international marine transportation services. Direct industry employment rises to 116 FTE workers, and other value-added/GDP generated per annum rises to £173m.

Scenario 1: Scottish T&S industry servicing Scottish industry only

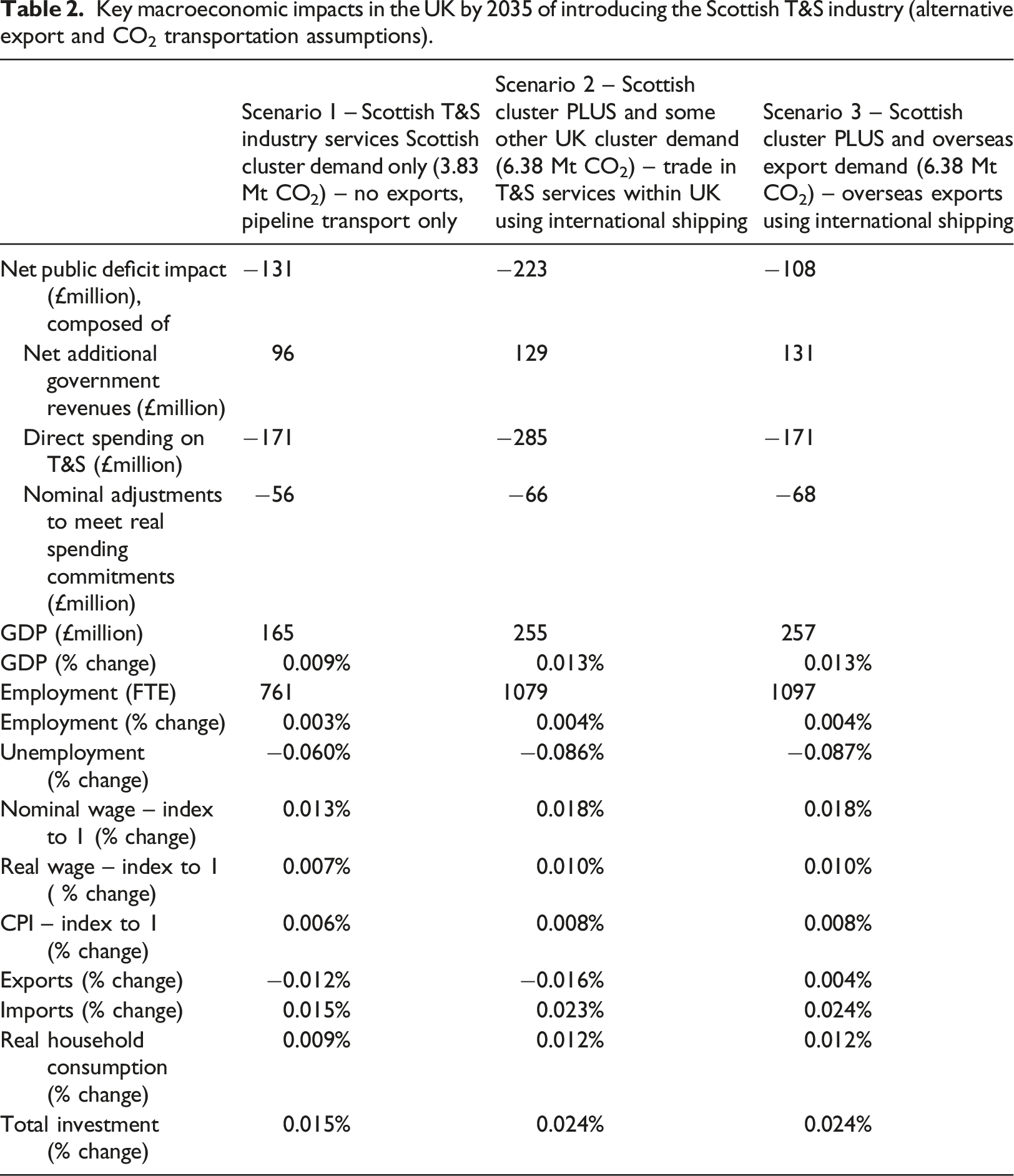

Key macroeconomic impacts in the UK by 2035 of introducing the Scottish T&S industry (alternative export and CO2 transportation assumptions).

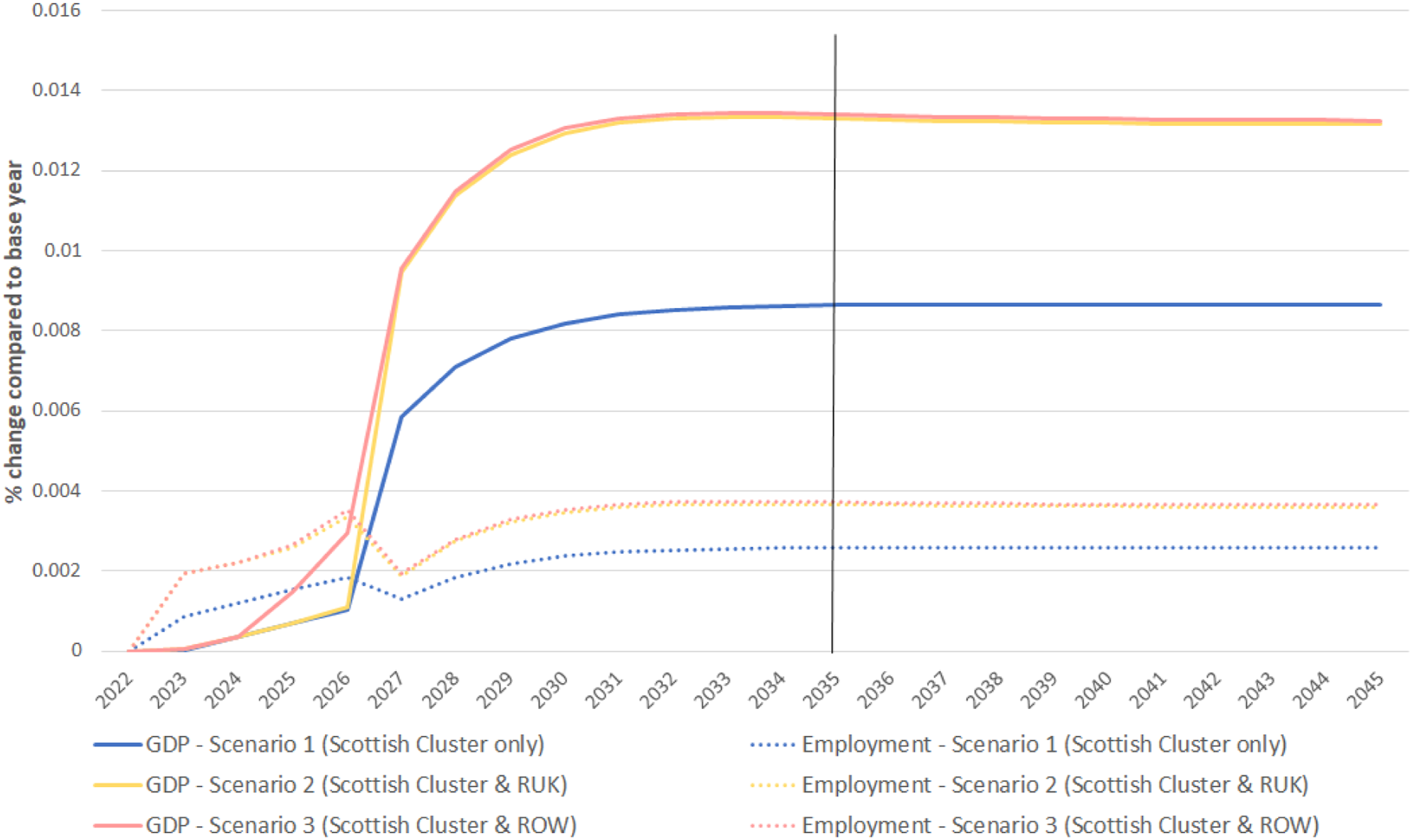

Impacts (%change) over time on UK GDP and employment of introducing the Scottish CO2 T&S industry (deficit funding).

Here the 2035 results for Scenario 1 are qualitatively comparable with the ‘deficit funding’ case in an imperfectly competitive labour market setting characterised by real wage bargaining and involuntary unemployment reported for 2040 by Turner et al. (2021). That is, a modest but sustained economy-wide expansion is triggered by the emergence of a new industry and associated supply chain activity in the presence of a persistent labour supply constraint.

Note that the net improvements in most real macroeconomic indicators (except the public budget and exports) reported for Scenario 1 are smaller than found in the Turner et al. (2021) work. This is due to the greater capital intensity of the O&G benchmark for the nascent T&S industry in the 2018 SAM database update. That is, similar monetary investment delivers a smaller industry capacity, and associated upstream supply chain requirements, compared to what has been found previously. However, this also means a reduced demand for T&S output that the UK Government needs to guarantee. In Scenario 1, where this applies to Scottish demand for Scottish T&S only, this is level at £171m p/a once the industry is operational in 2027, but with revenue gains associated with the expansion (£96m p/a by 2035), albeit offset by CPI impacts on real government spending (£56m), limiting the sustained net public budget impact of guaranteeing T&S demand to £131m p/a.

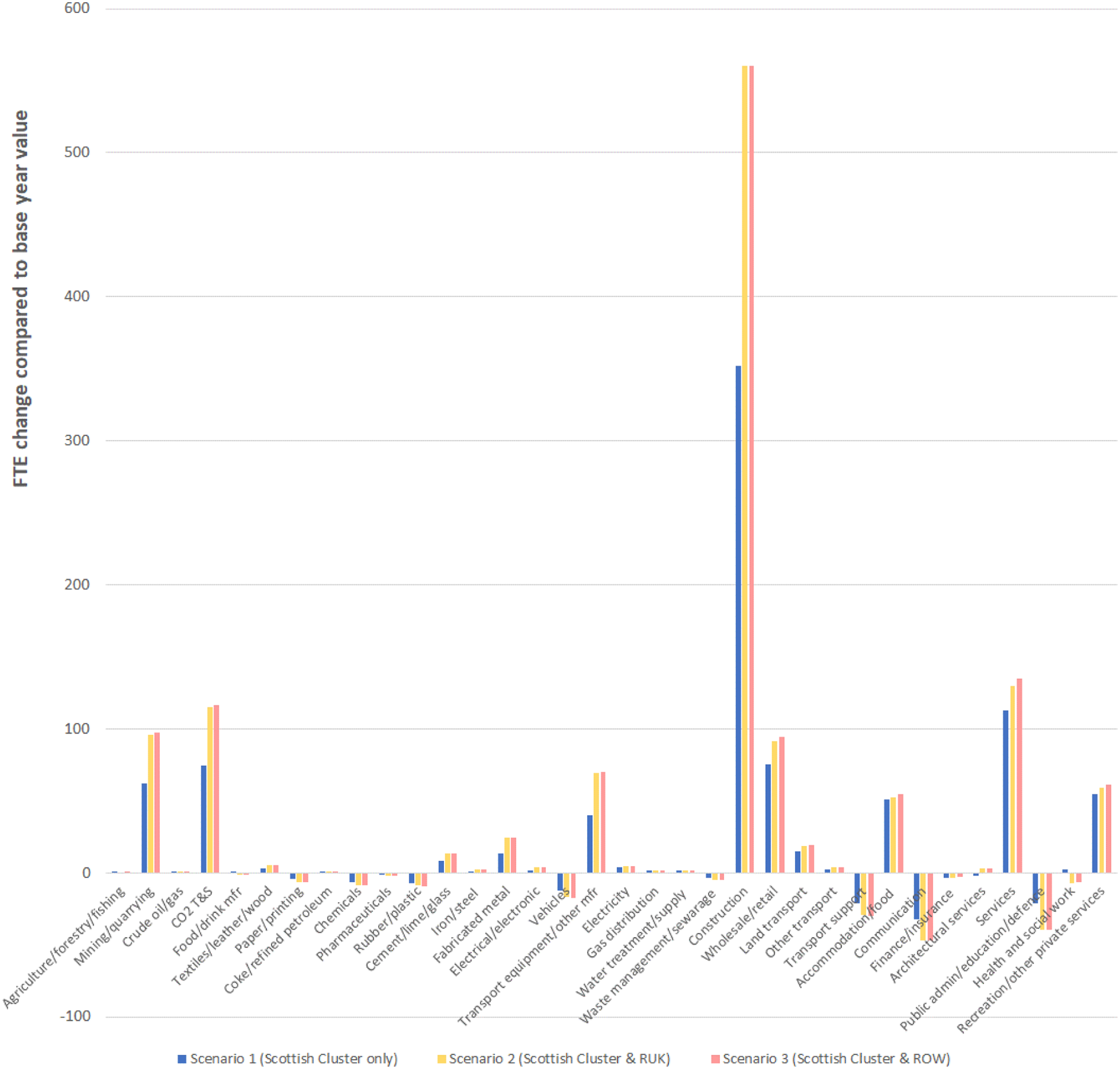

However, this is a constrained expansion. As soon as the investment stage begins, the presence of the labour supply constraint means that increased labour demand associated with the Scottish T&S industry rollout triggers increased real wage demands from the outset. This causes a sustained rise in the average nominal wage costs faced by all producers (ultimately sustained at +0.013%) and there is some displacement of employment across all UK sectors, as reflected in the first bar of Figure 2. The consequent increase in the CPI shown in the Scenario 1 column of Table 2 (+0.006%) erodes real wage gains to households but, coupled with sustained employment gains (+0.003%/761 FTE jobs by 2035) total household consumption rises (+0.009%), broadly in line with GDP. The main activity loss is in total export production, where there is a sustained drop of 0.012% due to the competitiveness implications of increased labour costs on UK producer prices. Impacts on sectoral (full-time equivalent, FTE) employment by 2035 of introducing the CO2 T&S industry to service the Grangemouth cluster (deficit funding).

As noted above, the CPI impact is also important in determining the net public budget impacts of supporting the T&S industry rollout (assuming the UK Government is committed to maintaining the real value of core transfers and public spending on goods and services).

Thus, one question emerging is the extent to which these competing factors may evolve if greater Scottish T&S industry capacity were created to utilise Scottish North Sea storage potential more fully, by offering a T&S export service that would involve shipping in CO2 captured elsewhere in the UK (which would involve the same government intervention to guarantee demand) or from overseas (which would not).

Scenario 2: Introducing other UK industry demand for Scottish T&S services

Scenarios 2 and 3 involve increasing the Scottish T&S industry capacity created (between 2023 and 2026) so that it can service an additional 2.55 Mt of CO2. From 2027, this equates to an industry with an annual output of £285 million (final column of Table 1), 60% of which services Scottish demand using pipeline transportation, as in Scenario 1, with the other 40% servicing external demand with greater reliance on international shipping. That is, Scenarios 2 and 3 differ only in terms of the source of the external demand.

Under Scenario 2 the additional demand comes from elsewhere in the UK (which could involve Scottish T&S servicing CO2 sequestration requirements in any of the mainland, English and/or Welsh, regional industry clusters). Macroeconomic impacts by 2035 are reported in the second data column of Table 2.

A qualitatively similar picture to that observed in Scenario 1 emerges, but with the larger upfront investment in, and roll out of, Scottish T&S supporting a more substantial but still modest wider economy expansion. However, the expansion of key macroeconomic variables is generally less than proportionate to the increase in the size of the industry. The is due to the use of shipping rather than pipelines to service non-Scottish demand, which reduces the level of investment spending required per unit of capacity created but involves leakage of value-added to the international shipping sector. This constrains the additional gains to UK GDP, employment and household consumption as the Scottish T&S sector expands.

On the other hand, the additional cost and price pressure across the wider economy is also limited. The direct and indirect additional employment requirements of the Scottish T&S industry do not grow in proportion to the increase in new industry activity. On the other hand, this means additional real wage demands are limited, containing further nominal labour cost increases to all UK producers. Thus, while the sustained CPI increase (0.008% by 2035) and export losses (0.016%) under Scenario 2 exceed those in Scenario 1, these additional negative impacts are proportionately smaller than the increase in UK CO2 emissions sequestered by the larger Scottish T&S industry.

Of course, absolute impacts are important, not least in terms of distributional outcomes. For example, comparing the Scenario 1 and 2 bars in Figure 2 shows that the extent of employment displacement across sectors of the UK economy grows in the face of even limited additional nominal wage pressure. Moreover, while not explored here, that job losses are concentrated in more labour-intensive service sectors will ultimately have distributional effects across different kinds of workers and households. The wider household impact is reflected in one of the smallest proportionate gains in moving from Scenario 1 to 2 being that of total real household consumption. This reflects both the slower growth in income from employment and the greater CPI pressure.

On balance, it will be a policy decision for UK Government actors as to how the economic costs and benefits are weighted in the context of an improved picture on reducing territorial emissions through the deployment of CCS capacity and capability within the UK. Scottish T&S capacity is only one part of the wider picture that must ultimately be explored. Such decisions will be set in the context of considering how new regional industry activity in delivering CO2 T&S services (and contributing to the associated transition of existing oil and gas industry activity and supply chains) may be supported.

Here, the impact on the national public deficit will be one policy focus. For example, consider the move from Scenario 1 to 2 in Table 2. If the additional Scottish T&S capacity created is used to service other UK as well as Scottish sequestration demand, the total net increase in the government deficit (70%) is larger than the increase in the spending requirement to guarantee demand for T&S output (66%). This due to the limited increase in revenues from additional activity being partly offset by the nominal spending implications of the greater increase in the CPI.

Such cost driven impacts may be expected wherever greater T&S capacity is created in the supply constrained UK economy. Economy-wide analysis of other domestic delivery options required is required to determine what outcomes may be. For example, going forward, the type of research presented here should extend to consider and compare scenarios one or more of the other Track 1 or Track 2 UK CCUS clusters extends to service demand in other UK regions (e.g. South Wales, where capture is required but T&S infrastructure and direct links to offshore storage are more problematic – see Welsh Government, 2021).

Scenario 3: Introducing overseas export demand for Scottish T&S services

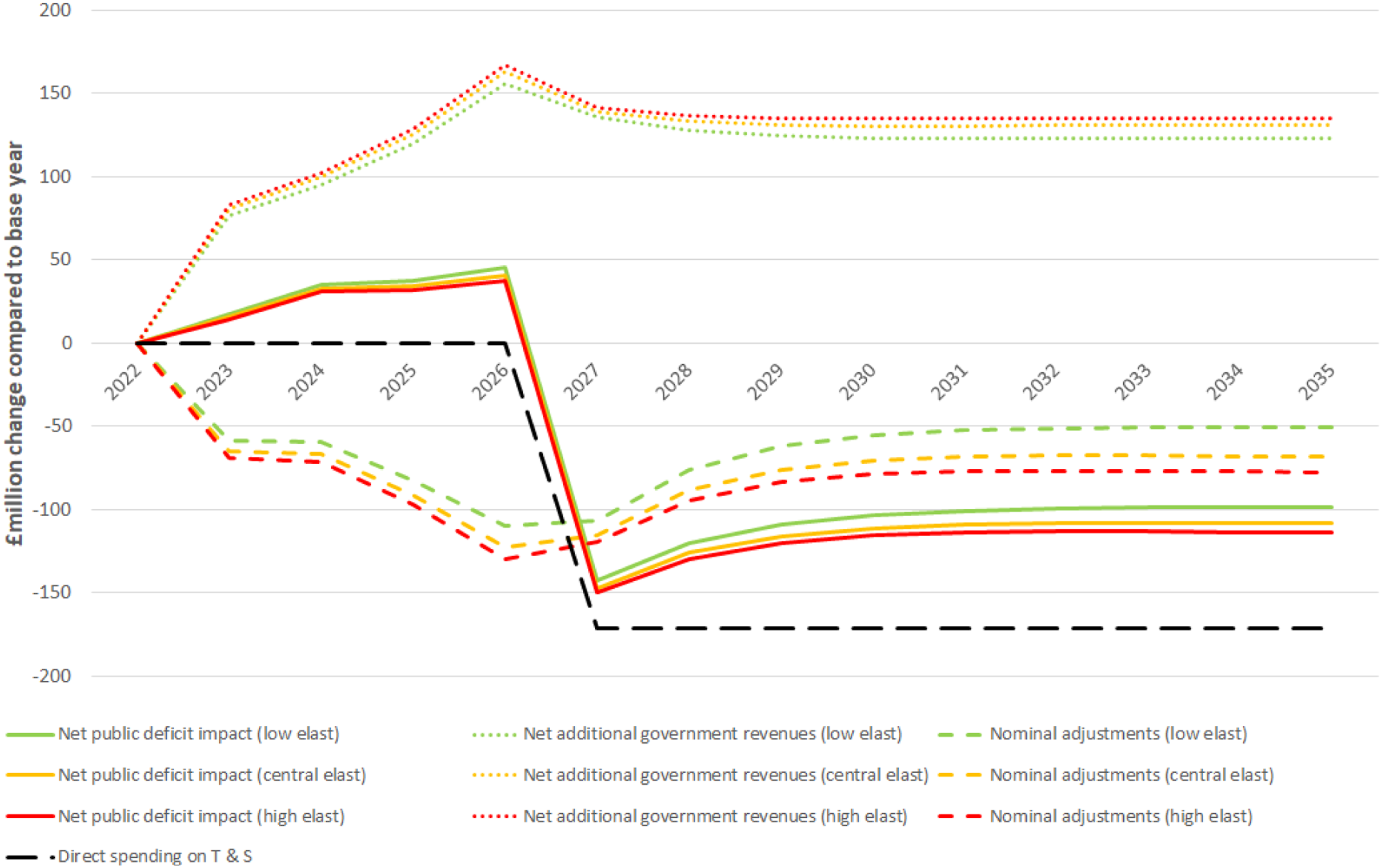

However, where policy interest lies in both exploiting new T&S industry opportunities and ensuring utilisation of the infrastructure-intensive capacity created, development of an export base should be considered. Scenario 3 focuses on an alternative use of additional Scottish T&S capacity, which could involve focussing on servicing overseas demand only. Consider the results in the final column of Table 2 and the Scenario 3 cases in Figures 2 and 3. Broadly the economy-wide and sectoral picture is almost identical to that emerging under Scenario 2, with two key exceptions. Impacts (£million) over time on components of the UK government balance of introducing the Scottish CO2 T&S industry for different unemployment-wage elasticities (scenario 3 – overseas exports).

First, there is no longer a contraction in total UK export production. Given that the CPI and underlying producer costs are higher than they were prior to the introduction of the Scottish T&S industry, this is entirely due to new export demand for CO2 sequestration services. On the other hand, this may not be a very important result given that the absolute difference is very small and has a relatively minor (+£2m) positive impact on government revenues.

The main difference in the outcomes of Scenarios 2 and 3 is that the net annual public deficit outcome by 2035 in the latter (−£108m) is substantially reduced relative to Scenario 1 (−£131m) and Scenario 2 (−£223m). Compare the composition of the public budget outcomes for Scenarios 2 and 3 in Table 2. The net revenue gains are very similar (+£129m and +£131m, respectively). Thus, it becomes clear that the overall government budget outcome is almost entirely due to the Scottish T&S sector being able to expand to service external demand without any further direct requirement on the UK public purse. That is, the national government only needs to guarantee demand for that element (60%) of the new industry’s output that services the CO2 sequestration requirements of the Scottish cluster. There is, however, an indirect cost. This is CPI impact (+0.0087% in the final column of Table 2) on the nominal spending adjustments required to maintain real government spending commitments (£68m). Thus, a picture emerges where the wider economy gains of extending capacity can be secured without additional direct – but potentially some indirect – requirements on the public purse if overseas export opportunities are exploited.

Sensitivity analysis

Of course, it is important to consider the extent to which our results may be sensitive to model assumptions, particularly those affecting the drivers, and wider economy transmission mechanisms, of the key impacts identified above. The earlier analyses of Turner et al. (2021) demonstrated the importance of parameters governing the sensitivity of international trade responses. There, particular focus was on how the export responses to changing UK producer prices play an important role in governing the extent of activity displacement across sectors when new Scottish T&S activity rolls out in a supply constrained context. However, that was identified as most important under a ‘polluter pays’ scenario where there may be extensive negative competitiveness impacts. Here, with our focus on the near/mid-term context where public funding is more relevant, the key driver of outcomes is the source of the cost and price pressures emerging. That is, responses in the supply constrained labour market.

Our central (preferred) assumption regarding the functioning of the supply constrained UK labour market is one of real wage bargaining in an imperfectly competitive setting. Here, our model specification involves worker bargaining power being inversely linked to the unemployment rate via the elasticity in equation (1) in the Methods section.

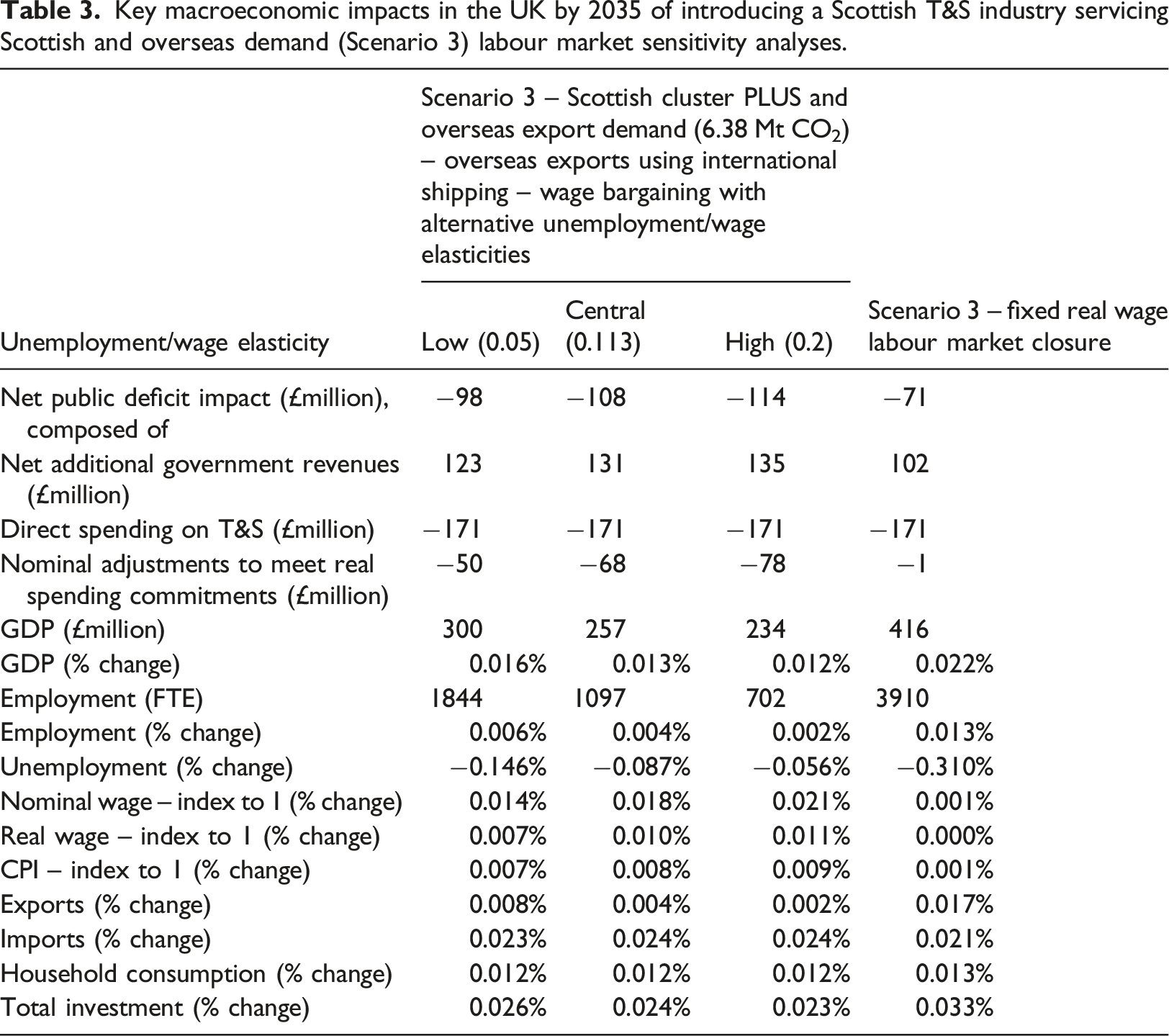

Key macroeconomic impacts in the UK by 2035 of introducing a Scottish T&S industry servicing Scottish and overseas demand (Scenario 3) labour market sensitivity analyses.

In practice this may map to the availability of appropriately skilled labour within that pool, and willingness to move back into employment based on the wages offered. Such imperfectly competitive labour market considerations could be crucially relevant in governing outcomes for all sectors of the economy. That is, it could have implications both for those supply chain industries that need to expand in responding to the introduction of the T&S industry and for others that do not, but which may be affected by rising labour costs and/or displacement of workers as the new industry and associated activity emerge.

Focussing on Scenario 3 as the main case of interest in this paper, the initial results from the final column of Table 2 are replicated as the central case (shaded) in the second data column of Table 3 for comparison with the outcomes of re-running the scenario under different labour market assumptions. First, the results in the third data column show that the greater the worker bargaining power, the more upward pressure on both average real and nominal wage rates. This means that the sustained expansionary power of introducing the larger Scottish T&S sector is further constrained. Crucially, the net employment gain is notably limited, with the GDP expansion becoming more capital-intensive. However, more limited gains in employment numbers attract a higher real wage, with the implication that the proportionate change in total household consumption is not affected to the two decimal places reported (though the underlying value result is slightly smaller).

If, on the other hand, if worker bargaining power is low – as in the first data column of Table 3 – there is less wage-driven price pressure in the economy and the expansion is less constrained. However, compare the first and final data columns of Table 3, where the latter involves the extreme assumption of the real wage being fixed/unchangeable. This comparison demonstrates that, even with very limited bargaining power persisting, any extent of wage-driven cost-price will lead to a constrained expansionary picture. Crucially, the absence of wage pressure equates to the national labour supply constraint effectively being nullified, certainly for a shock of the scale simulated here, with minimal displacement of activity and employment across other sectors.

While not shown, we find very similar sensitivity of results in the other two scenarios, particularly Scenario 2, where the scale of Scottish T&S activity introduced is the same. However, the distinctive feature of Scenario 3 is that the utilisation of the additional capacity created to service non-UK demand does not require additional direct government spending to guarantee demand. Thus, we have observed in the results analysis for Scenario 2 that additional net revenues associated with the greater expansion are only eroded by the nominal government spending impacts of what we assume is a commitment to maintain the real value of public spending on goods and services. Figure 3 shows that the impact on nominal spending requirements is dependent on the extent of worker bargaining power, as is – though to a lesser degree – the net revenue gains that help offset the overall impact on the public budget.

However, the public budget impact is complex. In all time frames under Scenario 3, the reduced CPI pressure of the larger Scottish T&S sector rolling out under conditions where worker bargaining power is low reduces the overall net negative impact on the public budget (where the direct spending requirement is constant). On the other hand, the net revenue gains associated with the expansion are larger where worker bargaining power is greater, despite the fact the GDP gains are smaller. This is because of the greater real wage income effect in a country like the UK, where income tax is the dominant source of government revenue.

Conclusions

This paper has considered the potential for new CO2 T&S industry activity associated with clustered CCUS networks in one regional location to extend to service sequestration needs of others domestically or overseas. We consider the example of a Scottish T&S industry linked to the ACORN project that may extend from sequestering emissions captured within the Scottish industry cluster, using a domestic pipeline infrastructure, to also servicing sequestration needs elsewhere in the UK or overseas, via shipping.

The key finding is that investing in greater capacity to this end enables a larger expansion of the UK economy and the creation of more jobs, mainly in the sectors linked with the operation of the Scottish T&S industry. However, the additional wider economy gains are less than proportionate than the increase in T&S demand. This is because some additional value-added, employment and investment activity are lost to the international marine transportation sector compared to domestic sequestration via pipelines.

There are crucial differences in public budget outcomes when additional demand for Scottish T&S comes from overseas rather than other industry clusters within the UK. In developing an overseas export base, the revenue gains associated with the wider economy expansion can be realised without any further direct government spending requirement to guarantee demand for the additional capacity created (though CPI pressure will impact wider nominal spending requirements). On the other hand, there is no additional reduction in industrial emissions within the UK. Going forward, the economic and environmental costs and benefits picture of additional Scottish T&S capacity being directed towards sequestering domestic or overseas emissions should be considered against outcomes if other T&S capacity in another location were used instead. For example, the most immediate potential within the UK could emerge via the other Track 2 cluster – the ‘Viking’ project the northeast of England – which is also being designed to service emissions from other UK clusters or from overseas via shipping. 15 The need to service sequestration demand in other parts of the UK is particularly pressing in the context of decarbonising those regional industry clusters not present in the core CCUS cluster sequencing process (e.g. Southampton, South Wales). It is also necessary to extend the type of analysis presented here to scenarios where CCUS is required to reduce emissions in fossil fuel powered electricity generation and/or in possibly large-scale centralised production of hydrogen.

Another key finding cutting across all our scenarios is that potential wider economy gains of establishing new industry activity are eroded by cost and price pressures driven by the persisting national labour supply constraint that characterises the UK economy. This is due to wage-driven cost-price pressures in an imperfectly competitive labour market triggering some displacement of consumption and other production activity, as well as eroding the real value of any public budget gains. Generally, our findings serve to reflect the wider public policy challenge inherent in considering the wider set of trade-offs and challenges in determining the most economically efficient and sustainable route to reducing emissions reductions.

Our analysis also reflects the importance of the quality of data to inform economy-wide scenarios. A key finding in this regard relates to the importance of understanding the capital intensity vis-à-vis investment requirements particularly in nascent industries like CO2 T&S. We have compared results here to the earlier Turner et al. (2021) study that used the same methodology, but older and less detailed data on the oil and gas extraction industry benchmark for T&S. Crucially, with better data suggesting that this benchmark is significantly more capital-intensive than assumed in that earlier study, the main implication is that a similar monetary investment delivers a T&S industry with smaller industry capacity and upstream supply chain requirements within the UK. The outcome is a substantially reduced wider economy expansion being triggered by the T&S rollout.

Going forward, a near term research priority will be to update the analysis reported here as more data emerge on the now-confirmed inclusion of the Scottish cluster in Track 2 of the UK’s CCUS cluster sequencing process. A wider priority will be to improve and refine the informing of databases and scenarios for economy-wide analysis of CCUS and other nascent industry developments required for the net zero transition. Similarly, a fuller range of counterfactuals need to be explored, including, in the context of the CCUS focus here, consideration of whether additional (to proximate industry cluster needs) T&S industry capacity in any one region is best focussed on servicing overseas demand or that of other domestic regional industry clusters. Here, it will be useful to extend to and/or compare analysis of scenarios for domestic and/or international T&S in other regional and national cases, where sequestration needs and capacity/capability to deliver T&S services will vary across nations. For example, a nation like Germany has extensive industrial decarbonisation requirements but no offshore storage capacity so that it is likely to engage in cross-border cooperation, for example, involving sequestration via the Port of Rotterdam in the Netherlands. The opposite is true for Norway – potentially the main European player in an international T&S market – where domestic industry sequestration requirements are more limited.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by UKRI (InnovateUK) through the ‘ISCF Decarbonisation of Industrial Clusters Phase 2’ initiative, under the project ‘Scotland’s Net Zero Infrastructure (SNZI) Onshore’ (Grant ref: 75989).

Data availability statement

For Open Access purposes, the authors have applied a CC licence to any Author Accepted Manuscript (AAM) version arising from this submission. The SAM database is publicly available at ![]() .

.