Abstract

This paper provides a diversification explanation in order understand the development of PTAs in Southeast Asia. I argue that an important reason why ASEAN states participate in PTAs has been to diversify existing trade ties and to reduce overdependence on a narrow range of export markets. Southeast Asian countries have formed PTAs with markets with which they had weak or unexplored economic relations, as demonstrated by three case analyses: the ASEAN Free Trade Area (AFTA), the ASEAN-China Free Trade Agreement (ACFTA) and the ASEAN-Japan Comprehensive Economic Partnership Agreement (AJCEP). To maximise the economic gains and the diversification effects of PTA participation, ASEAN countries have pursued a strategy of strengthening economic unity while keeping external economic linkages as diversified as possible. Although East Asia, and especially China, was an important alternative market to reduce ASEAN's dependence on trade with America, ASEAN countries have also pursued PTAs with a number of other trading partners. This paper explains how PTAs have helped ASEAN states to develop more policy autonomy in their trading environment.

Introduction

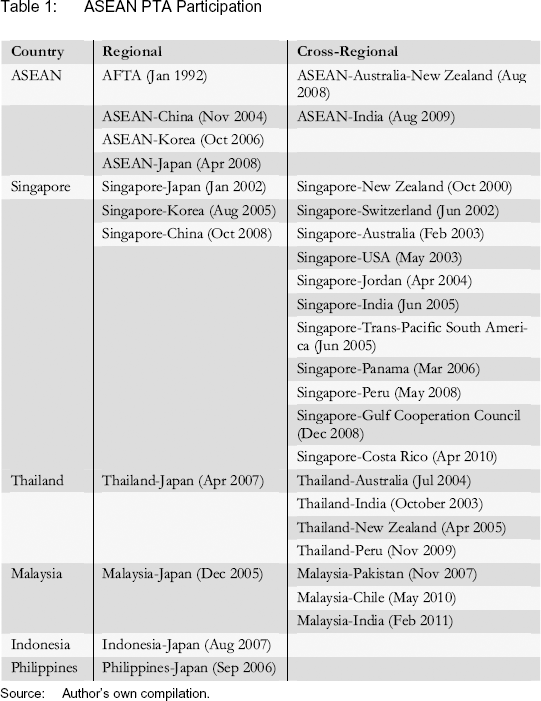

Since 1997, there have been one hundred seventy-six new preferential trade agreements (PTAs), 1 twenty-seven agreements are currently being negotiated (The Word Trade Organization (n.y.). The proliferation of PTAs has attracted scholarly attention with respect to both their welfare effects on signatories and the consequences for the global trading system. Southeast Asian nations have also joined the tide, first signing an agreement for an ASEAN Free Trade Area (AFTA) at the January 1992 ASEAN Summit in Singapore, which adopted a common effective preferential tariff (CEPT). In October 1998, ASEAN leaders agreed to implement an ASEAN Investment Area (AIA) and later launched a larger project in 2003, Bali Concord II, which aimed to transform the region into a single market and production base by 2020. Shortly thereafter, ASEAN states started to pursue regional or bilateral PTAs with other East Asian neighbours including China, Japan and Korea. ASEAN also paired with their Northeast Asian counterparts in a forum of ASEAN Plus X to coordinate regional integration. Besides entering intra-regional PTAs, Southeast Asian economies also signed PTAs with non-East Asian countries such as Australia, New Zealand and India (Table 1).

ASEAN PTA Participation

Source: Author's own compilation.

This paper will use the terms preferential trade agreement (PTA) and free trade agreement (FTA) interchangeably, although the author prefers to use the term PTA. FTAs require an entire elimination of tariffs on trade in goods, while PTAs only require a reduction in tariff rates (Panagariya 2000: 288).

As East Asian states led the surge of PTAs in the early 2000s questions have been raised about what drove East Asian states to pursue PTAs and the subsequent consequences of these PTAs on the global trading system (Pomfret 2007: 925). Analysts have tended to view Southeast Asian nations’ policy gestures as defensive actions triggered by external pressure, either to secure existing market access or to respond to great power competition. There was a concern that the formation of PTAs with non-ASEAN states would impede the cohesion of ASEAN itself. In contrast to much of the current literature, this paper argues that the overall pattern of PTA participation by ASEAN states actually reveals a consistent strategy. PTAs have helped ASEAN states develop more policy autonomy in managing the changing trading environment.

This paper provides what I term a “diversification logic” to explain the sequence of PTA development in which the Southeast Asian states have been collectively involved. I argue that the major goal of ASEAN states has been to diversify existing trade ties and to avoid or reduce overdependence on a narrow range of export markets. The facilitating condition that motivated Southeast Asian states to pursue a diversification strategy was associated with their exposure and vulnerability to international markets. If we realise that the ultimate goal has to reduce overdependence we can appreciate two trends. On the one hand, given that some ASEAN states are more dependent on trade and export than others, the interests among individual ASEAN states have diverged, reflecting differing incentives for diversification. 2 Some ASEAN states have been more active than others in pursuing bilateral PTAs. The logic of diversification also helps explain the pattern of partnership selection. ASEAN states have been more likely to pursue PTAs with those markets where they had weak or unexplored economic relations. In some cases, East Asian countries, including China, have been viewed as important alternative markets to reduce ASEAN's dependence on trade with America. While anchoring their economic linkages more with Northern Asian economies, ASEAN also pursued PTAs with a number of trading partners outside East Asia to expand market access and diversify economic linkages.

Among ASEAN members, Singapore has been the most active state to pursue bilateral PTAs, followed by Thailand and Malaysia.

This study will discuss the factors contributing to ASEAN's PTA policies and their consequent partnership selection. The case studies will examine three major PTAs in which ASEAN states have been collectively involved: the ASEAN Free Trade Area (AFTA), the ASEAN-China Free Trade Agreement (ACFTA) and the ASEAN-Japan Comprehensive Economic Partnership Agreement (AJCEP). These agreements have been selected because they were concluded relatively quickly and at an early stage. Also, the agreements included large trading countries such as China and Japan, and have acquired policy attention and in depth academic discussion in recent studies. In the following sections, I first review the current literature which seeks to explain the rise and spread of PTAs and the emerging partnership patterns, and then propose a diversification logic to explain the rise and partnership selection of PTAs, and the economic conditions that encouraged ASEAN to select neighbour countries for PTA partnerships. I then explain how these PTAs helped expand bilateral trade and investment ties between ASEAN and its partners. Finally, I examine how PTAs have helped diversify ASEAN's economic linkages and thus have helped to increase economic gains.

Literature Review

A substantial literature has discussed the economic and political incentives that have caused states to pursue PTAs and also examined the emergence of partnership diversity. One major explanation centers on states’ intentions to avoid trade diversion costs while gaining welfare benefits from trade creation. The current literature in international political economy (IPE) has focused on domestic actors and the role of export and leading sectors as pro-PTA constituencies. With the help of trade agreements, business sectors and leading exporters could reduce transaction costs and increase profits from increased economic integration and economies of scale. They would be able to acquire access advantages against foreign competitors in trading partners’ markets (Solis, Stallings and Katada 2009; Ravenhill 2010: 174). The formation of a closer integration or a trading bloc by some countries can result in trade diversion, harming non-member states’ exports and making them less competitive vis-à-vis member states. The fear of being damaged through trade diversion has prompted non-members to seek membership, leading to a chain reaction of PTA engagement (Baldwin 1993). The momentum of economic integration via PTA participation in the 1990s, therefore, was the result of a “regionalism bandwagon” (Pekkanen, Solis, and Katada 2007: 950) driven by a “domino effect” of “competitive liberalisation,” with an attempt to “level the playing field” over foreign competitors (Mansfield and Reinhardt 2003; Dent 2003; Feridhanusetyawan 2005).

With regard to partnership selection, this literature tends to argue that states in similar competition networks woo their major trading partners in order to build close economic ties (Baldwin 1997). Many developing countries encounter strong competitive pressures and are desperate to secure market access and capital, so larger trading economies are popular candidates for partnerships (Gruber 2000; Elkins, Guzman, and Simmons 2006). Meanwhile, the business sectors in industrialised countries lobby hard for trading blocs with partners with which they already possess close production networks, in order to promote intra-industry specialisation and economies of scale (Milner 1997; Chase 2003). But while this approach addresses domestic actors’ preferences, its explanatory power is limited when applied to Southeast Asian states. According to this logic, if the cost of trade diversion and loss of export markets are the major concerns of ASEAN states, these states should seek PTAs with large trading partners to preserve competitiveness in these markets. Of the PTAs signed by ASEAN states, however, many have involved membership with minor trading partners. Even though Southeast Asian states also have signed PTAs with some large economies such as China, Korea and India, the importance of these economies as trade and export markets were often insignificant to ASEAN states prior to their PTA formation. In addition, while the occurrence of PTA partnerships between Japan and the ASEAN states might seem to fit this domestic logic given existing production networks, a question still remains why such PTAs did not occur earlier, in the late 1980s or early 1990s. Until very recently, PTAs did not usually occur between Southeast Asian states and their natural trading partners.

Another popular approach in the literature addresses the economy-security-nexus. The argument focuses on power politics and argues how power distribution and competition will affect states’ commercial policies. It is argued that the erosion of USA hegemony has stimulated an increasing number of PTAs. As a hegemon declines, it may engage in predatory actions pre-emptively reaping trade gains. Other rising states will also challenge the existing economic order to pursue their interests (Krasner 1976; Gilpin 1981; Gowa and Mansfield 1993). Here, a trade arrangement is an act of diplomatic pragmatism that ultimately serves a political goal. The utility of PTAs is portrayed as a means to add security externalities to political and military relations (Gowa 1989; Gowa and Mansfield 1993). Economic relations and trade ties help reinforce political commitments and cultivate domestic preferences that ensure the continuation of stable relations. Trade agreements and arrangements have often been viewed as diplomatic instruments of larger and powerful states in fostering weaker states’ dependence (Hirschman 1980; Abdelal and Kirshner 2000). Today, smaller states also perceive trade agreements as useful policy tools to magnify their strategic importance.

Based on these arguments, the proliferation of PTAs in East Asia has been a strategic response to power distribution. It has been argued that the contestation over regional leadership between China and Japan had propelled a series of economic projects for regional integration (Yoshimatsu 2005; Dent 2006b; Wong 2007). For smaller states, including the ASEAN nations, PTAs are proxy tools to fulfil the strategic goals of soft balancing or political hedging (Kuik 2005; Goh 2007). Economic agreements constitute both economic and institutional means of constraining participators’ policy and state behaviour (Rüland 2011: 90). This literature explains why PTAs do not always emerge between natural trading partners that share geographic proximity or close economic ties, as the domestic logic suggests. It stresses that power relations remain an important determinant in shaping the orientation of economic policy. Yet it is not clear how trade relations can be affected by strategic concerns. For instance, while ASEAN has pursued PTAs with important political powers such as China, Japan and even India, it is still not clear why ASEAN nations have spent time and resources seeking and forming PTAs with less significant political powers such as Chile, Panama, Peru, and Switzerland. This approach tends to evaluate the utility of PTAs as subordinate to political calculations, or as a policy substitute for military means. It also often downplays the enthusiasm of smaller countries in launching PTAs; many analyses focus on the role played by only the major powers. This paper will argue that states’ calculations of the economic implications of PTAs have often been underestimated. Other than simply being a supplementary means to achieve political and security goals, PTAs have helped offset economic uncertainty, which in the post-Cold War era has often increased for small nations.

Alternative Hypotheses

In this paper, I argue that one major goal of the ASEAN states has been to diversify existing trade ties and to reduce overdependence on a narrow range of export markets. Many Southeast Asian states perceived an increased sense of vulnerability as their economies became more dependent on trade and concentrated on the American market or Japanese investment. Southeast Asian economies’ dependence on foreign capital and markets for development and their narrow specialisation in agricultural and lower-end manufactured goods have made these economies susceptible to various destabilising effects, such as volatility in trade flows, increased competition in international markets and exposure to foreign pressures. Southeast Asian states are motivated to pursue policies to counteract rising economic vulnerability and uncertainty. PTAs have served the function of diversifying signatories’ pre-existing trade and investment patterns and avoiding overdependence on a limited range of imports and exports.

The flexibility of partnership selection and consequent trade and investment expansion and exploration have provided Southeast Asian states with alternative policy options. First, states involved in PTAs have more flexibility in selecting partners and issue coverage, and negotiations are less time consuming. By selecting specific partners for PTAs and by more direct policy cooperation between members, states can expand their economic ties with each other, diversifying existing trade ties and concentrated trade patterns (Fernandez 1997: 18-20). Second, PTAs also provide preferential access for member firms to member markets, which secure these firms’ commercial advantages and grant them better terms-of-trade over non-member firms. Furthermore, PTAs might redistribute production sharing networks and strengthen specialisation among signatories. Even states in the same competition network 3 or whose trade ties were previously less developed can improve their welfare by forming PTAs, which increase policy coordination and foster new complementarities.

Elkins, Guzman, and Simmons (2006: 819) observe that it was not uncommon for some highly indebted poor countries to sign trade agreements or investment treaties with each other even though they were all competing for capital from other parts of the world.

Third, ongoing policy coordination among signatories is a process which builds exchange trust and develop social linkages. These linkages can foster a common voice that helps increase bargaining power vis-à-vis non-member states in broader multilateral institutions (Fernandez 1997: 15; Mansfield and Reinhardt 2003: 830). Finally, PTAs have signal effects that help improve signatories’ terms-of-trade and stabilise trade flows. The predictability of policy commitment to trade cooperation makes these signatories attractive destinations for trade and capital flow from other countries (Davis 2003; Milner and Kubota 2005; Elkins, Guzman, and Simmons 2006; Mansfield and Reinhardt 2008).

With respect to power distribution, I would argue that ASEAN has viewed PTAs strategically to ensure its economies would not fully depend on one specific market, given past experience and concerns about economic overdependence. In contrast to the literature that predicts PTAs are most likely emerge between countries highly interdependent with each other, the diversification logic argues that the agreements emerge between countries whose trade ties are less significant or have experienced decline. Given the small size of ASEAN economies and the likelihood of their having concentrated trade structures, Southeast Asian states have sought PTAs with other countries on multiple fronts to enlarge the range of their market access. Preferred partners have been those states with which ASEAN states have had weak economic relations, but which provide opportunity for growth.

Some ASEAN states have been more active than others in pursuing bilateral PTAs, due to their vulnerability from highly exposure to concentrated external market. But most states have perceived the importance of strengthening intra-ASEAN economic unity before pursuing PTAs with extra-ASEAN countries. Why is this? On the one hand, ASEAN states themselves are also important alternative markets for each other, thus reducing their dependence on non-ASEAN markets. On the other hand, by acting as a collective unit when seeking PTAs with non-ASEAN states, Southeast Asian states are able to maximise economic returns, acquire better terms-of-trade, and send strong signals to attract attention in the international market.

PTA strategies recently pursued by ASEAN states as a collective unit have reflected several features of the diversification logic. PTAs strategies first emerged when ASEAN states’ sought to reinforce their solidarity as an economic group, and later engaged with extra-ASEAN states on multiple fronts to construct a web of interdependence. ASEAN states have turned to both Southeast Asian and Northeast Asian neighbours through the formation of AFTA, ACFTA, and AJCEP. These developments occurred when economic ties within signatories seemed less promising. ASEAN states also aimed to keep their external economic linkages as diversified as possible, sometimes forming PTAs with other regions. I now examine the economic conditions facing many Southeast Asian countries in the 1990s, and then examine the formation of three PTAs: AFTA, ACFTA and AJCEP.

Rising Economic Uncertainty

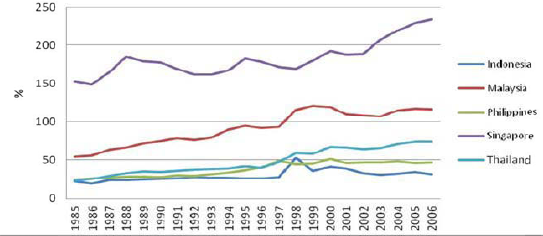

Integration into the global economy and global production networks had transformed Southeast Asian nations by the early 1990s, but the manner of their integration had left them highly dependent and vulnerable to external shocks. The export share of Gross Domestic Product (GDP) 4 in the 1990s and 2000s in the ASEAN states had maintained consistently high levels (Figure 1). In Singapore and Malaysia, the export ratio consistently exceeded 100 per cent of GDP, followed by Thailand, the Philippines and Indonesia, which all had a significant export/ GDP ratio. While a shift to an export- and FDI-led model 5 did expand manufacturing sectors and foreign capital inflows, particularly after the Plaza Accord, the expansion of manufacturing industries across ASEAN states (particularly in the early members) developed narrow specialisations in lower-end goods in the production network. It also increased dependency in two ways: dependency on foreign capital and imports of capital intermediates and goods, and dependency on foreign markets for exports (Bernard and Ravenhill 1995; Peng 2000). More specifically, during the late 1980s and early 1990s, Japan and the United States were the major trading partners for the five ASEAN states (Figure 1). Southeast Asian states ran trade deficits with Japan and trade surpluses with the USA, as the Southeast Asian states imported capital intermediates from Japan while exporting the final products to the USA (Beeson 2002: 556).

ASEAN-5 Exports of Goods and Services (% of GDP) (1985-2005)

The data cover the original members in ASEAN (i.e. Indonesia, Malaysia, the Philippines, Singapore and Thailand), as data for new members were not available.

Since the 1950s, Southeast Asian states have deregulated investment restrictions and received three types of FDI: first, investment in natural resources; second, investment that could produce cheap consumer goods for local markets and help foster national producers; and third, investment that produced export-oriented goods (Arnold 2006: 197). Capital flows helped offset the domestic capital shortages of early ASEAN members.

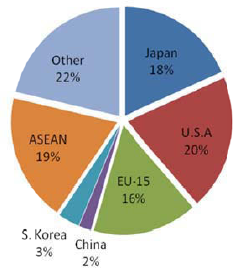

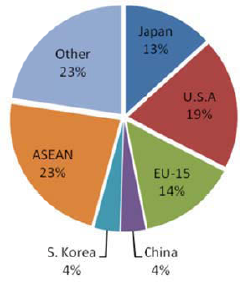

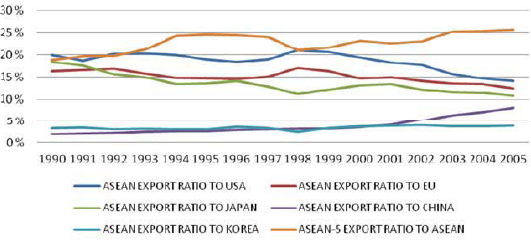

The dependency on foreign capital and a limited number of external markets increased ASEAN's exposure to volatility, competition and foreign pressure, and constrained ASEAN states’ policy flexibility, resulting in uncertainty over the sustainability of future growth. The American market had been the largest market for Southeast Asian exports, holding a share of around 20 per cent of total exports of ASEAN's original members during the 1990s and 2000s (Figure 2 and Figure 3). The dependence on Western markets made Southeast Asian states vulnerable to exchange rate shocks, as many of them pegged their currencies to the US-American dollar in order to facilitate trade and exports. The pegging strategy resulted in sensitivities to the fluctuations in third country currencies. The depreciation of Japanese and Chinese currencies during 1994-1995, the years preceding the Asian Financial Crisis, affected Southeast Asian states’ export performance and trade balances.

ASEAN-5 Exports to Major Trading Partners, in % (1990)

ASEAN-5 Exports to Major Trading Partners, in % (2000)

Furthermore, narrow specialisation in processing lower-end electronics and automobiles made several Southeast Asian economies susceptible to the volatility of trade flows and price shocks. The dependence on importing capital goods placed cost-increasing pressures on these economies. The sudden rise in the price of imported capital goods caused difficulties for ASEAN states in maintaining trade balances and sustaining growth (Peng 2000: 187). When encountering price shocks, it was difficult for Southeast Asian states to scale up export production, given there were more competitors in manufacturing lower-tier goods engaging in price wars. The specialisation in the electronics industry also resulted in deflationary pricing pressure, liming the pace of the economic recovery in the post-crisis era (Ernst 1999).

Southeast Asian economies also faced increased competition with other countries, which exported similar goods to a limited number of export markets. Competition for market and capital access put Southeast Asian governments under both domestic and international pressure. Competition encouraged Southeast Asian economies to engage in price wars, affecting profits (Holzinger and Knill 2005: 782). By the end of the 1980s, more developing countries rose up, including China and countries from the former Soviet bloc, entered the lower-end of the manufacturing process (Bowles and MacLean 1996: 366). ASEAN states were concerned about investment diversion to these developing countries, and were also worried about a policy shift of developed countries that tilted toward expanding investment and trade ties with these rising developing countries (Bowles and MacLean 1996: 366). They became increasingly pessimistic about the level of FDI inflow in the late 1990s, as they experienced a decline in the proportion of FDI flows within Asia compared to the mid-1990s. From 1997 to 2002, FDI inflows to Southeast Asia dropped from USD 27.7 billion to USD 14 billion (Arnold 2006: 198).

Southeast Asia was also exposed to fluctuations in the policy preferences of major trading partners on which they were dependent. Southeast Asian states’ trade conditions became vulnerable to the business cycles and structural economic instability of these external markets. While Japan had been the most important investor, its investment flows reached a peak by the mid-1990s. Japanese FDI and bank lending in Southeast Asian states rapidly declined by the second half of the 1990s, as a result of Japan's stringent economic conditions. ASEAN states’ export growth were also affected by the periodic downturn and recession in the American market (Beeson 2002: 555-556). Many ASEAN states were concerned about the capacity of the American market to absorb goods from the rest of the world, particularly if there were a slowdown in the USA economy.

The pattern of dependence also affected ASEAN's bargaining power and limited its policy autonomy (Bayard and Elliott 1994; Gruber 2000; Drezner 2003). Foreign multinational corporations (MNC) and their home governments tried to pursue economic policies which pressured Southeast Asian governments (Hatch and Yamamura 1996; Yoshimatsu 1999, 2002). Particularly after the Plaza Accord, Southeast Asian economies’ rising trade surpluses with the USA increased tensions with Washington. Since the 1988 Trade Act, Southeast Asian countries had been placed on the watch list, while the USA began exerting pressure on Southeast Asian governments to protect American property rights (Sinha 1992). Later, America's active push for comprehensive and legalised liberalisation in the Asia-Pacific Economic Cooperation (APEC) raised resistance from ASEAN states. 6 They were concerned about APEC as a challenge to the unity of ASEAN, and saw it as imposing Washington's preferred economic agenda on weaker members (Nesadurai 1996: 32; Ravenhill 2002: 105).

The USA was initially lukewarm in responding to Australian and Japanese efforts to establishing the APEC. But the Clinton Administration viewed this forum as an effective tool to further open Asian markets and as a bargaining leverage against the European Union (Ravenhill 2002: 93).

The shift of Washington to pursue bilateral trade negotiations to ensure its national and economic interests also posed uncertainty for small ASEAN states, who were worried about the possible effects of trade diversion. Negotiations for the IMF stabilisation program, aimed to handle the post-crisis situation, exacerbated tensions between Southeast Asia and Western countries (Narine 2002: 139). 7 Exposure to the crisis and to the intervention of the IMF raised Southeast Asian countries’ awareness of their vulnerabilities. They perceived the IMF's rescue measures as a way of protecting foreign investors and banks at the expense of Asian nations. 8 The weakness of member states in these negotiations and their dependence on external powers and institutions further aggravated their feeling of powerlessness.

The IMF prescription required crisis-hit countries to cut spending and subsidies and raise interest rates to stabilise their currencies and reduce the deficit. This led to further bankrupticies. See Wade and Veneroso 1998.

Not only did the IMF provisions lead to the transformation of domestic rules and policy structures, the provisions also granted leverage to foreign companies to acquire full ownership of local business operations and to get advantage in mergers and acquisitions. The USA's veto of the Japanese proposal to form an Asian Monetary Fund forced member states to turn to the IMF assistance with no alternative option (Beeson 2002: 555).

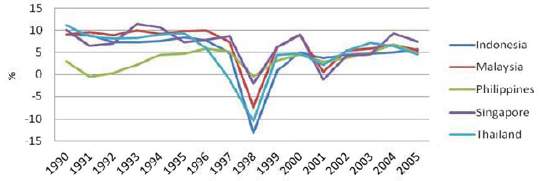

After the 1997/98 crisis, the trading environment facing Southeast Asian states became less stable and their exposure to external shocks increased. GDP growth rates across ASEAN-5 fluctuated around a downward trend between 1995 and 2005 (Figure 4). It is perhaps paradoxical that it was during these unstable years that Southeast Asian states shifted to a PTA strategy.

ASEAN-5 GDP Growth Rates (1990-2005)

After both the Asian Financial Crisis and the bursting of the dot-com bubble, ASEAN states began to negotiate PTAs with other states. Moreover, in the face of economic uncertainty, the preferred partners were new markets or secondary trading partners. The next section examines the reason for this partnership selection.

Unfavourable Economic Conditions Foster PTA Formation

Since the early 1990s, ASEAN states have made economic goals the raison d'être of the organisation (Narine 2002: 125; Dent 2006a: 47-48). ASEAN states started to institutionalise economic cooperation and signed an agreement for an ASEAN Free Trade Area (AFTA) in January 1992. ASEAN as whole signed a PTA with Korea in October 2006 and signed a PTA with Japan in April 2008. 9 The ASEAN-China FTA became operational in 2010. Although North American and European countries were still the most important trading partners for ASEAN, ASEAN countries’ concerns over dependency encouraged them to secure ties with other economies, especially in East Asia. It was expected that the trade and investment expansion with East Asian neighbours would be vital. 10 Furthermore, neighbouring economies in East Asia could provide alternative markets for consumption, considering their large populations and resilient economies.

ASEAN and Japan reached agreement on the General Framework for Comprehensive Economic Partnership (AJCEP) with ASEAN in October 2003, Japan pursued several bilateral free trade agreements with individual members; with Singapore (Oct 2001), Malaysia (Dec 2005), the Philippines (Sep 2006), Thailand (Apr 2007), Brunei (Jun 2007) and Indonesia (Aug 2007). A negotiation between Japan and Vietnam also began in January 2007.

According to Sasatra and Prasopchoke's model, ASEAN could benefit largely by signing PTAs with trade partners where trade ties had experienced decline or were insignificant. Among varied PTAs, ASEAN-China PTA would bring the largest trade potential to ASEAN, compared to the ASEAN-USA, ASEAN-Japan and ASEAN-India PTAs. At the same time, among countries that are major trading partners with each other, there could be small space to improve trade, which implicitly indicated the limited utility and lack of interest for PTAs (Sasatra and Prasopchoke 2007: 352-53).

Prior to the formation of AFTA in 1992, the USA, Japan and EU accounted for most of the ASEAN-5 total exports (Figure 5). But the older ASEAN members’ trade ties with Japan did not seem promising throughout the 1990s and early 2000s. Japan had initially been the second largest market for ASEAN-5 exports, but its share declined during the 1990s and early 2000s. China's market for ASEAN was very small until the late 1990s, accounting for under five per cent of ASEAN-5's exports.

ASEAN-5 Export Ratio to Major Trading Partners (1990-2005)

The Emergence of an ASEAN Free Trade Area

Prior to the formation of AFTA, ASEAN was a small economic entity, compared to NAFTA and the European Economic Community (EEC). In 1990, NAFTA accounted for 27.8 per cent of world output and 18.1 per cent of world trade, while the EEC accounted for 26.9 per cent of world output and 42.1 per cent of world trade (Chng 1993). It was estimated that the formation of NAFTA would divert four per cent of the value of ASEAN exports and the integration of the European market would divert 8 per cent of the value of ASEAN exports (Kreinin and Plummer 2008). The integration process in North America and Europe would also induce some negative effects on major industries that had contributed to the development of ASEAN, including the textile, clothing and machinery sectors (Plummer and Imada-Iboshi 1994). In contrast, ASEAN's original members only accounted for 1.5 per cent of world output and 4.5 per cent of world trade; intra-ASEAN economic ties remained weak, as intra-regional trade was only around 18-19 per cent of ASEAN's total trade in the early 1990s. ASEAN's intra-regional trade became even less if Singapore was excluded as a transshipment entrepôt (Chng 1993).

This begs a question. Given ASEAN's low intra-regional trade and high dependence on extra-regional markets, why would it choose to establish AFTA? One reason was that ASEAN states recognised the difficulty of taking the lead in negotiations and forming trade pacts with Western trading partners, even though seeking more cooperation with Western trading partners might have been the preferred option. ASEAN would have little control over the progress of negotiations. By strengthening economic ties as a group, ASEAN could establish a stronger position with a common voice and command more attention. AFTA would provide ASEAN with some leverage in APEC and global negotiations (Frankel and Wei 1997: 359-60). Some research has indeed demonstrated that ASEAN could benefit through intra-regional integration before integrating with other countries (Sasatra and Prasopchoke 2007: 353).

The Emergence of an ASEAN-China Free Trade Agreement

While political and diplomatic relations between ASEAN and China in the post-Cold War era rapidly improved, economic ties remained limited. But several ASEAN states were worried about China's rising competitiveness in the international market. By the early 2000s, Southeast Asian economies and China directly competed in third markets such as the USA, EU and Japan. In the early 2000s, after WTO accession, China's access to the American market grew, while ASEAN-5's market share in the USA fluctuated (Liu and Ng 2010: 668). Competition was particularly intense in the labour-intensive sectors (Tongzon 2005: 201). Southeast Asian leaders were also worried about losing the contest for FDI to China. The evidence showed that

at the beginning of the 1990s, Southeast Asia received 61 per cent of all FDI going to developing countries in Asia, while China got 18 per cent. After a decade, the proportions had been reversed: China secured 61 per cent of the FDI inflows, while ASEAN states only claimed 17 per cent (South China Morning Post 2002).

According to the USA-ASEAN Business Council, FDI to China in 1999 totalled USD 40 billion, or 42 per cent of the total capital flowing into Asia. In contrast, FDI to ASEAN was USD 16 billion, or just 17 per cent of the total (Agence France-Presse 2001). ASEAN's attraction was falling as China emerged as a regional and global production base. Even Singapore, a country that had attracted innovative industries and also had a large modern service sector, experienced a drastic decline in FDI after 1992 (Liu and Ng 2010: 679). China's accession to the WTO and its MFN status made it a more attractive destination for FDI (Financial Times 2000). A survey conducted by the Japanese External Trade Organization (JETRO) in October 2001 showed that many Japanese firms were considering relocating their operations to China from Southeast Asia to take advantage of China's greater openness (Rajan 2003: 2641).

At the same time, trade and investment ties between China and Southeast Asian economies remained negligible. During the 1990s, China accounted for only about five per cent of trade of the ASEAN-5. Most Southeast Asian economies had trade deficits with China. While China's direct investment in ASEAN-5 increased during most of the 1990s, China's FDI accounted on average for less than one per cent of ASEAN's total FDI inflows (Srivastava and Rajan 2004: 176). In addition, economic uncertainty increased after the Asian Financial Crisis in 1997. While trying to recover from the severe growth collapse of 1998, Southeast Asian states faced another economic challenge in 2001, with the bursting of the dot-com bubble. The outbreak of Severe Acute Respiratory Syndrome (SARS) in 2003 further exacerbated economic uncertainty in ASEAN (Liu and Ng 2010: 666).

It was under these unfavourable conditions that economic relations between Southeast Asia and China moved to a new stage. ASEAN-China relations strengthened during the Asian Financial Crisis, as China demonstrated its commitment to assisting ASEAN crisis-hit countries (Ba 2003: 635). Meanwhile, ASEAN states viewed the relative decline of the USA economy as unavoidable after 9/11, and were concerned that the slowdown of the USA economy would hit ASEAN's economies (Business Times 2001). Singapore in particular perceived the need to reduce its “overwhelming dependence on the United States by strengthening economic cooperation with East Asian economies” (Business Times 2001; Straits Times 2001). In addition, given China's rise, it was argued by some ASEAN leaders that it would be better for ASEAN to implement a cooperative plan with China as soon as possible to offset the effects of dependence on other markets. ASEAN could reap large benefits with a PTA and send a strong and early signal to foreign investors amidst a global recession (Strait Times 2001). ASEAN states expected that China's continuing growing urbanisation and increasing consumption would provide greater opportunities for ASEAN's export products and services. China's proposal of a PTA with ASEAN encouraged ASEAN states to rethink their trade strategies and view a rising China as a new market opportunity.

The Emergence of an ASEAN-Japan Economic Partnership Agreement

ASEAN's economic ties with Japan strengthened after the 1970s and their relations reached a peak during the late 1980s and early 1990s. But these ties gradually weakened during the 1990s, which encouraged the pursuit of PTAs to reinforce economic relations. Japan was the second largest trading partner and export destination for ASEAN states in the early 1990s. Japan and ASEAN had formed vertical production networks while Japan had transplanted the Keiretsu system to ASEAN (Fujita and Hill 1997; Yoshimatsu 2002; Hatch 2005). Japan had also provided grants, aid and Official Development Assistance (ODA) to ASEAN which also promoted Japanese firms’ commercial interests there. ASEAN affiliates and local firms received reinvestment funds and imported upstream components from parents firms in Japan. Investment flows to ASEAN reached a peak during the late 1980s and early 1990s after the yen appreciated; between 1985 and 1990, Japan's FDI grew at an annual average rate of 62 per cent (Bowles 1997: 222). During this time, market-driven mechanisms drove the growth of ASEAN-Japan economic relations. This informal connection discouraged ASEAN from pursuing further integration through formal agreements with Japan (Grieco 1997).

The stagnation of the Japanese economy in the early 1990s restrained investment, and reduced the ODA budget to ASEAN states, while the rise of China diverted Japanese investment. 11 The Asian Financial Crisis harmed Japanese investors, as more Western firms were able to access ASEAN markets. ASEAN's weakening economy after the Asian Financial Crisis also reduced its member states’ imports from and exports to Japan. Paradoxically, the decline of Japanese importance to the ASEAN states encouraged them to seek formal agreements and reinforce trade ties with Japan. ASEAN viewed Japan's economic presence as an important source to revive and balance its economies in the long term. Japan was viewed as a crucial partner for upgrading technology and for facilitating integration, even though economic ties between ASEAN and Japan shrank. 12

Japan's investment flow to ASEAN in 1998 was USD 5.1 billion but reduced to USD 4.4 billion in 1999 and to USD 2.7 billion in 2000 (Japan External Trade Organization (JETRO) n.y.). Japanese ODA reduced from USA USD 12 billion in 1995 to USD 9.6 billion in 1996. In 1997 and 1998, the amount dropped another 10 per cent. It increased to USD 15.3 billion in 1999 after the Asian Financial Crisis but reduced to USD 13 billion in 2000 (Tsai 2005: 117).

Japan had consistently pledged a development agenda to ASEAN to help boost the lagging economies. The Hashimoto Doctrine in 1997 called for joint efforts between Japan and ASEAN to overcome economic challenges (Singh 2002: 289). In 1999 Japan also launched the Obuchi Plan, providing USD 80 billion as emergency financial assistance to crisis-hit countries (ASEAN Secretariat 1999).

Trade and Investment Expansion among Signatories

PTAs are intended to grant commercial privileges to signatories and early access to new economic sectors. Gradually, the expansion of trade and investment ties among signatories help to diversify pre-existing economic ties. The AFTA, the ACFTA and AJCEP were all expected to bring an enlargement or reinforcement of trade and investment among the signatories. ASEAN states had hoped to establish a niche market for their own products in an emerging market such as China (Liu and Ng 2010: 681).

First, the ASEAN states sought to strengthen links between themselves. To prevent being marginalised amidst rapid changes in the international environment, ASEAN states began to institutionalise economic cooperation in the early 1990s. Four new members, Vietnam, Myanmar, Laos, and Cambodia, joined ASEAN in the mid-to-late 1990s. The AFTA treaty aimed to reduce all tariffs on intra-ASEAN trade in manufacturing and processed agricultural products to the range of zero to five per cent by 2015. ASEAN states pushed for more integration and legalisation of economic cooperation, even in the face of the economic crisis. The relevant policy projects included extending the AFTA agreement to services, and investment flows. ASEAN also signed the protocol on the Dispute Settlement Mechanism (DSM). Amidst an ongoing economic crisis in October 1998, ASEAN leaders agreed to implement an ASEAN Investment Area (AIA). ASEAN leaders later launched Bali Concord II in 2003, aiming to further reduce non-tariff barriers and facilitate trade integration.

ASEAN states attempted to use AFTA to explore new economic opportunities themselves (Imada 1993: 18). AFTA offered an opportunity to foster and nurture ASEAN's own investors and industries (Nesadurai 2003). The design of AFTA and the later AIA aimed to not only attract more FDI, but to also ensure access privileges to ASEAN-based investors. ASEAN investors, treated as domestic investors, were allowed full market access and national treatment privileges years earlier than foreign investors, and could acquire more time to be more competitive in the ASEAN market. 13 From 1993 to 2000, the average tariff rate among the ASEAN countries was lowered and intra-ASEAN exports grew from USD 44.2 billion to USD 97.8 billion (Ong 2003: 64). When the original aims of AFTA were largely completed by 2003, ASEAN leaders signed the Bali Concord II in 2003 with an ASEAN vision 2020. 14 ASEAN members also signed the Framework Agreement for the Integration of Priority Sectors at the Tenth ASEAN Summit in November 2004. Eleven major sectors were set up as targeted areas for integration. Those selected sectors included agro-based products, air travel, automotive products, e-ASEAN, electronics, fisheries, healthcare, rubber-based products, textiles and apparel, tourism, and wood-based products. This further integration also aimed to promote economic growth and reduce socio-economic disparity among members (Oktaviani, Rifin, and Reinhardt 2007).

AFTA and AIA also imposed local content rules, 40 per cent of equity shares, to facilitate joint ventures between foreign and domestic/ ASEAN firms to take advantage of technology sharing and transfer.

The goal of the ASEAN Economic Community was to facilitate a free flow of goods, services, investment and labour within the region, remove non-tariff barriers, and harmonise custom procedures and mutual recognition arrangements on product scrutiny and regulations (Severino 2008: 411).

The arguments in favour of the ASEAN-China PTA included the assertions that ASEAN would have the advantage of early entry into China's market, and that the agreement would help make ASEAN an attractive “priority market” for Chinese investment abroad (Ba 2003: 639). Supachai Panitchpakdi, former deputy prime minister of Thailand, claimed that China would be the major engine of growth in the region in coming decades, and integration with China would help sustain ASEAN's economic growth and “override any fluctuations or vicissitudes coming from the rest of the world” (Straits Times 2002b). According to the ASEAN-China Expert Group on Economic Cooperation, both ASEAN and China recognised the current barriers that had hampered trade and investment flows, and stated that ACFTA would facilitate appropriate measures so that “the trade and investment potentials between ASEAN and China could be fully met” (ASEAN-China Expert Group on Economic Cooperation 2001). ACFTA would increase the efforts of both China and ASEAN to harness comparative advantage for their economies (Wong and Chan 2003: 525), while propelling intra-ASEAN trade and the growth of specialisation and complementarities within ASEAN (Srivastava and Rajan 2004: 198; Devadason 2010: 665).

A key feature of ACFTA, the early harvest program, was to allow ASEAN to expand its agricultural products and trade to China's market. More than 600 of all tariff lines would be subject to tariff elimination and goods not included on the list for the early harvest program could be renegotiated later (Rajan 2003: 2642). Other sectors such as textiles, chemical, rubber and plastic products, and vehicles and parts would also be able to increase exports to China. Some Chinese food products, and apparel and leather products would also increase access to ASEAN's market (Chirathivat and Mallikamas 2004: 95). ACFTA would increase Southeast Asian trade in services by accessing China's market (Srivastava and Rajan 2004: 192). 15

China committed to opening new markets to ASEAN in construction, environmental protection, transportation, sports, and commerce. In return, ASEAN countries would open their markets to China in finance, telecommunications, education, tourism, construction and medical treatment. Other service-related sectors, such as distribution, professional and infrastructural services, would also develop or increase.

ACFTA is the largest free trade area in the world, involving about 1.9 billion people and over USD 4.6 trillion in aggregate GDP. Some estimates suggested that an ASEAN-China free trade area would increase ASEAN's exports to China by 53.3 per cent while ASEAN's imports from China would rise by about 23 per cent (Chirathivat and Mallikamas 2004: 94). The gradual tariff reductions prior to the final implementation in 2010 rapidly increased trade between ASEAN and China; from USD 59.6 billion in 2003 to USD 192.5 billion 2008 (Strait Times 2010). During the global downturn in 2008-2009, China's demand for services remained strong, benefitting Southeast Asian neighbours (Bangkok Post 2009). 16

There would also be greater expansion in travel and tourism services. Border trade and development projects targeting subregional economies were also major subjects for cooperation under ACFTA.

ASEAN countries welcomed the increase of Chinese FDI, given the decline of Japanese and American FDI inflows (Cheng 2004: 270). The Chinese government had encouraged state-owned enterprises and private firms to invest in resource-related sectors, while investment in manufacturing and the service sectors also increased. ASEAN governments had hoped to ensure that FDI flowed into development-related projects including infrastructure construction. ACFTA was expected to create a network of investment cooperation between signatories and their investors. China also promised to increase development assistance to ASEAN members, particularly to new members. 17 Investors from ASEAN could also take advantage of early entry in a booming Chinese market before investors from other developed or developing countries. 18

More coordinated projects had emerged between China and ASEAN's older members to develop and construct road, rail and water transport links cross borders, aiming to promote economic growth in areas such as the Mekong River Basin (Cheng 2004: 271).

For instance, ACFTA could level out the playing field for Thai businesses that wanted to expand their investments in China to tap the potential of China's expanding service sector (Bangkok Post 2009).

The third PTA was that with Japan, concluded in April 2008. The AJCEP aimed to eliminate tariffs on 90 per cent of Japanese imports from ASEAN, and on 90 per cent of six ASEAN members’ imports from Japan within 10 years. 19 Individual ASEAN members’ bilateral PTAs with Japan set up more detailed enforcement procedures and wider cooperation between ASEAN original members and Japan. 20 ASEAN states and Japan are now working on extending liberalisation to service sectors and working to strengthen technical standards and mutual recognition procedures. The scope of trade and investment ties was estimated to widen given the tariff eliminations. Under these PTA networks, Japanese interest to invest in ASEAN revived (The Nation 2005). ASEAN states hoped the Japanese government and firms would provide assistance in capacity-building and in development projects. For instance, Indonesia was desperate to secure massive industrial projects. Bambang Trisulo, the chair of the Association of Indonesian Automotive Manufacturers, had said “the EPA (with Japan) is positive as an umbrella for the increase of cooperation in market access and industrial capacity development” (The Jakarta Post 2007). Indonesia expected that the PTA would encourage more investment from Japan and target investments in energy development and infrastructure projects (Japan Focus 2008). Thailand and Japan also agreed to increase their development projects in the agricultural, fishery and energy sectors.

New members such as Cambodia, Myanmar, Laos and Vietnam would have gradual tariff elimination; Vietnam would eliminate tariffs on 90 per cent of imports from Japan within 15 years and others would abolish 85 per cent within 18 years (Japan Today 2007).

When Singapore and Japan signed the first bilateral PTA across ASEAN, about 98.5 per cent of total goods had their tariffs abolished, compared to an earlier figure of 65 per cent. Singapore removed tariffs on all imports from Japan and Japan increased the number of Singaporean goods that had zero tariffs, from 3,087 to 6,938 (Terada 2006: 17). Malaysia's tariff elimination would increase from the existing 86 per cent to 94 per cent within 10 years for imports from Japan. Of Malaysian exports to Japan, an expected 99 per cent would enjoy further tariff cuts from the existing 70 per cent. Under the Indonesia-Japanese EPA, Indonesia would eliminate 59 per cent of existing 11,163 tariff posts immediately after the agreement was enforced, and about 93 per cent of existing posts would cut tariffs (The Jakarta Post 2007).

The PTAs also granted ASEAN members more leverage when they bargained with Japan on investment projects, exchange of human resources and the liberalisation of domestic agricultural sectors. The PTAs also increased their access to Japanese markets in a few sensitive sectors, where Japan had been resistant in previous negotiations. 21 Although some sensitive items such as rice and processed agricultural goods remained subject to tariffs, the ASEAN states did demand some concessions from Japan on several protected items. Indonesia and the Philippines's exports of tropical fruits and fishery products improved their access. Thai farmers were expected to benefit from import tariff cuts in many product items, such as shrimp, chicken, pineapple, fish products, bananas, vegetables, processed foods, chemical products and wood (The Nation 2008). Southeast Asian producers of textiles, clothing and footwear also gained improved market access.

For example, ASEAN states were promised by Japan assistance in development projects. ASEAN and Japan also touched upon the issues of exchanges and mobility of human resources. The PTAs made Japan more flexible in restrictions of the labor market, as Japan had agreed to reduce restrictions on employment of foreign nurses and caretakers to Indonesia and the Philippines (BBC Monitoring Asia Pacific 2006; United Press International 2008).

Southeast Asian states also expected an enhanced Japanese role in narrowing income and development gaps between ASEAN states and in facilitating integration. They hoped Japanese aid funds and FDI would lead to more technology transfer and capacity building, and Japanese MNCs could link up with local ASEAN firms through subcontracting. Some Southeast Asian governments urged Japanese companies to play a greater role in encouraging division of labour and cooperation through their investment strategies. 22 ASEAN was especially eager for Japanese expertise to explore new sectors in manufacturing and services. ASEAN and Japan are also keen to increase their cooperation in technical and custom harmonisation and in the liberalisation of the service sectors. PTA networks are thus expected to assist the ASEAN countries to access new and unexploited markets and help them enjoy ‘early entry’ advantage over non-member states. ASEAN leaders also hope that PTAs would open Japan's domestic market and serve as a catalyst for politically sensitive domestic reforms within ASEAN (Japan Times 2005).

Some development projects had been set up between Southeast Asian countries and Japan during PTA negotiations. The Indonesia government had formed the Manufacturing Industry Development Centre and asked Japan to extend technical assistance to various sectors including manufacturing, energy, agriculture and fisheries under the Centre's monitoring and assistance. Japanese FDI was invited to develop Special Economic Zones (SEZs) in order to spread economic development more evenly around the country. JETRO also promised to hone in productivity and quality control in the auto parts industry by offering lectures and guidance from Japanese experts to Indonesian employees (Japan Focus 2008). Malaysia and Japan also started to operate 24 economic cooperation projects upon the implementation of their bilateral PTA and set up the Koizumi-Abdullah Training Programme for Economic Partnership by which Japan promised to help train 1,000 Malaysian employees in various professions within ten years. Thailand's partnership with Japan also granted Thailand a role in delivering various ODA funded projects to new ASEAN members, which would strengthen Thailand's position in subregional development (Prasirtsuk 2006: 228).

Returning to Figure 5, export ratio patterns of the ASEAN-5 show how PTAs facilitate the expansion of economic ties among signatories. After the formation of AFTA, intraregional exports within ASEAN-5 jumped from 19 per cent to around 25 per cent. While intraregional exports within ASEAN-5 suffered a setback because of the Asian Financial Crisis, they rebounded after 2003, to around 25 per cent. ASEAN-5's exports to China also increased after the formation of ACFTA and the implementation of the Early Harvest Program, from below five per cent in 2000 to around nine per cent in 2005. In the next section, I address the diversification effect in more detail.

Diversifying the Source of Market Dependence and Fostering ASEAN as a Hub via PTAs

This paper has stressed the diversification aim for the formation of PTAs in ASEAN, which has not just been limited to diversifying trade and investment ties, but also to broadening cooperation and assistance for development projects. There has also been an expectation that extra-regional PTAs would lead to further integration within ASEAN. Member states such as Singapore, Thailand and Malaysia, were active states in seeking extra-ASEAN PTAs. Being extremely reliant on trade and foreign investment, Singapore tended to pursue bilateral PTAs, even though it had been the major initiator of ASEAN-centered PTAs. Singapore's enthusiasm for bilateral PTAs was perhaps paradoxical, given that it was more dependent on intra-ASEAN trade than the other four original ASEAN states. To some extent, Singapore regarded bilateral PTAs with non-ASEAN states as a way to offset the perceived negative effects of its dependence on intra-ASEAN trade (Lee 2006: 187-189).

Some researchers have argued that Singapore's PTAs with extra-ASEAN countries would also benefit other ASEAN members given the shared ties between Singapore and other ASEAN members in intermediate goods, sourcing and distribution (Dent 2006: 97). Singapore's PTAs may have encouraged other ASEAN members to access non-ASEAN member markets. Thailand also pursued bilateral PTAs from the Chuan Cabinet to the Thaksin Cabinet (Dec. 1997-Sep. 2006). The partners Thailand sought included both developed and developing states (Kiyota 2006: 207). Thailand hoped to strengthen its position as a regional hub within ASEAN while impressing the international market with its commitment to a free trade regime, even amidst economic difficulties (Dent 2006: 121-123; Kiyota 2006).

But by the early 2000s, ASEAN Plus One became the preferred format when ASEAN negotiated PTAs with extra-ASEAN countries. This partly reflected the goal of ASEAN states to promote ASEAN as a regional hub and to ensure it could diversify its markets and even the providers of development projects. But ASEAN could only present itself as a credible PTA partner if it first turned inward to strengthen economic ties within the region. Since the formation of AFTA, ASEAN states have pushed for more integration and legalisation of economic cooperation.

Although some members continued to pursue PTAs with extra-ASEAN states and doubted whether intra-ASEAN economic integration would succeed, ASEAN has committed to an agenda of economic integration. The paper has discussed some of the policies adopted, such addressing trade in services, and investment and industrial projects. ASEAN states had also sourced more imports from each since the 1997/98 crisis and brought the date of AFTA implementation forward. At the ASEAN summit in 1998, ASEAN leaders agreed to implement an ASEAN Investment Area, in order to signal their commitment to the integration of international trade and investment (Narine 2002: 130-31). These initiatives have brought some advantages to ASEAN states. First, formal agreements have strengthened ASEAN's position as an attractive destination for investment. The commitment to a single market has signalled that ASEAN is a competitive destination for foreign investors who want to diversify their investment and assets (Bowles 1997). Second, Southeast Asian states by acting together as a group, have marketed ASEAN as a potential regional hub. This explains why ASEAN states have in recent years preferred the ASEAN Plus X formula to bilateral deals.

When ASEAN and China signed the ASEAN-China Free Trade Agreement (ACFTA) on November 4th, 2002, many viewed the move by China as a type of “economic statecraft”. While there may be truth in this, I have argued that the pursuit of a PTA with China also accorded with ASEAN's diversification strategy, which intended to revive and sustain ASEAN economies following the formation of ACFTA. A more integrated market across China and ASEAN has expanded trade, and may have helped to reduce inflationary pressures in the region. The Chairperson of Indonesia House's Budget Committee, Harry Azhar Azis, has argued that “the ASEAN-China FTA is one of the instruments to lower inflation since the agreement will trim prices” (Bisnis Indonesia 2010). Trade with China also helped some export-dependent Southeast Asian economies to sustain growth in the middle of the global recession, as these economies have benefited from the rapid rebound and early recovery of China. A World Bank survey released in 2009 argues that “take China out of the equation, and the rest of the region (East Asia) […] will grow more slowly in 2009 than South Asia, the Middle East and North Africa” (The Edge Malaysia 2009). In spite of mounting pressure to postpone full tariff reductions on several items under the ASEAN-China PTA, even the Indonesian government has praised the wider market access to China that brought more benefits and sustained a recovery for Indonesia's exports (The Jakarta Post 2010). 23

The benefits from greater access to emerging markets in Asia encouraged Indonesia's trade ministry to expand trade ties with “non-traditional markets, including those that were previously not pursued by Indonesia, such as Russia and the Eastern European Countries” (The Jakarta Post 2010).

It is argued that ACFTA has also encouraged more investment flows. ASEAN officials believe that the ACFTA would make their economies attractive not only to Chinese FDI but also to investors that would like to diversify their investment and avoid excessive exposure to China (Rajan 2003; Tanaka 2011). 24 Meanwhile, ASEAN countries also tried to diversify sources of development assistance. As China committed to various projects on capacity building and development, at least some ASEAN countries would be able to get another source of funding. We should not neglect that although ASEAN has increased trade and aid flows with China, ASEAN states are also intent on “diversifying instead of being hitched to the China behemoth alone” (Straits Times 2002a).

Many MNCs had conducted risk hedging and considered setting up business operations in Southeast Asian countries to prevent disruption to global supply chains (Rajan 2003: 2642) or the possible effects from Chinese currency adjustments.

Japan's PTA with ASEAN can be viewed as a response to China's PTA initiatives, and thus as a type of statecraft. To some extent, ASEAN's embrace of Japanese PTA initiatives resulted naturally from their past economic interdependence. But the PTAs with Japan also help fulfil ASEAN's aims to diversify trade and reduce economic dependence, especially given that Japan and ASEAN's economic ties had declined since the early 1990s. ASEAN has also become more eager to strengthen relations with Japan after concluding the ACFTA with China, which could make China the largest and dominant trading partner to ASEAN in the future. By pursuing PTAs with both Japan and China, ASEAN stays hope to maneuver into a more stable position in East Asia. To ASEAN, strengthening cooperation among other East Asian countries could produce a ‘multi-focal and multi-connected pattern of growth,’ so that China would not become the only growth engine in East Asia, as once remarked by Prime Minister Lee Hsien Loong when Singapore launched its PTA strategy in the late 1990s (Lam 2006: 215).

It is also expected that PTAs with Japan would encourage diversification in another way. ASEAN's PTA networks would not only attract more investment directly from Japan, but could also make ASEAN a favourable destination for investment from a third party. Other non-member states, which may not have had trade pacts with ASEAN's PTA partners, would then prefer to invest in ASEAN to benefit from the ASEAN PTA networks. Japan could increase its access to other countries via ASEAN, such as with China, South Korea, Australia, all countries with which Japan had not concluded PTAs (The Nation 2010; The Nikkei Weekly 2011).

Conclusion

My research has found that while becoming more integrated with global economy, many ASEAN states also feel that they have become more vulnerable to external shocks and volatility. The flexibility of partnerships and coverage selection under PTAs has helped ASEAN reduce dependence and increase policy autonomy by diversifying economic linkages. This paper also shows how ASEAN states viewed the implementation of AFTA as the principle priority before seeking PTAs with non-ASEAN states. ASEAN states, acting together, would benefit more and gain more bargaining leverage than when acting alone in negotiations with extra-ASEAN states. East Asian economies have become important alternative markets for ASEAN to reduce dependence on the EU and American markets. The proposal by China to negotiate an ASEAN-China PTA strengthened ASEAN's status and encouraged ASEAN to conduct an extra-ASEAN PTA as a group.

Apart from China and Japan, Southeast Asian countries have in recent years pursued PTAs with key players in new markets from different continents, such as Australia, New Zealand, Mexico, Canada, Peru, India and the European Free Trade Association (EFTA). These efforts have aimed to expand overseas markets and to signal ASEAN's potential as a bridge to Asia, Oceania, the Americas, and Europe (Daquila and Huy 2003: 92). But concerns remain about how the slow progress of AFTA might affect ASEAN integration (Ravenhill 2010). Some authors also argue that the pursuit of bilateral PTAs would affect the unity of ASEAN (Dent 2006). This paper agrees with the assessment that continuous study will be required, as these challenges may reduce ASEAN's potential as a regional hub and limit the effects of diversification.