Abstract

Thirsty for oil and other raw materials needed to fuel its breakneck development, China is funnelling money and manpower into an expanding number of countries in order to secure access to natural resources. This effort has successfully increased Chinese oil assets overseas but it has also exposed Beijing and Chinese national oil companies (NOCs) to significant risks. The present paper focuses on one type of risk – political risk – and how it has affected China's global quest for oil since 1993. It starts with a brief overview of political risk. It then looks at political risk management as applied to the oil industry in general. The paper continues with a discussion of the political risk management of Chinese national oil companies over time. This includes a concise examination of several instances in which the interests of Chinese NOCs have been undermined due to poor management of political risk. Recent developments suggest that Chinese NOCs are learning from these mistakes and adjusting their strategies accordingly. Still China's own socio-political context continues to hamper the ability of Chinese NOCs to deal with on-the-ground realities that are clearly much more unstable than their own.

Political Risk

Until 2007, the beginning of the credit crisis and the recent financial turmoil, many people in the market thought that you could predict the future with a spreadsheet and all you really needed was numbers about the economy. What the last crisis has shown is that it is really about politics and sociology now. And what is scaring people in the market is that you can't put that into a spreadsheet (Tett and Bremmer 2011; emphasis added).

Definition and Typology

Early scholarly efforts to assess and manage the impact of politics on businesses and investments date back to the Catalogue School in the 1950s and 1960s (Jarvis and Griffiths 2007: 5–21). In the intervening decades, work on so-called “political risk” waxed and waned in tandem with political developments. Bursts of scholarly production coincided with new events that were perceived to threaten the status quo and/ or future business prospects. A decline in threat perception gave way to periods of relative inactivity (Jarvis 2008). This episodic evolution of the study of political risk partly explains why there is still no generally accepted definition for this phenomenon (Jensen 2005).

Some authors see political risk as policy changes and/ or policy inactivity that affects the interests of business groups in both developed and developing countries. According to David Schmidt, political risk is “the application of host government policies that constrain the business operations of a given foreign investment” (Schmidt 1986: 43–60). Similarly, Otto and Cordes define political risk as

the probability that a project's economic value to the investor will be adversely affected by unilateral governmental actions over which the investor has little control or influence (Otto and Cordes 2002).

Other authors such as Haendel, West and Meadow define political risk as “the risk or probability of occurrence of some political event that will change the prospects for the profitability of a given investment” (Haendel, West and Meadow 1975: 11–13). Another group of authors define political risk more broadly as any political decision and/ or political event that negatively impacts the success of investments and/ or businesses. Lax, for example, declares that political risk refers to

the possibility that political decisions or events in a country will affect the business climate in such a way that investors will lose money or not make as much money as expected when the investment was made (Lax 1988).

Kennedy goes a bit further and defines political risk as

a strategic, financial or personal loss to a firm because of non-market events or factors that affect the fiscal, monetary, trade, investment, labour and industrial climate (Kennedy 1988: 26–33).

These, he notes, can stem from the orderly activities of governments, regulatory agencies or judiciaries. Equally, they can arise from dysfunctional political events like terrorism, coups, riots, insurrection, secession-ism, civil war, or violent political contestation.

For the purposes of this paper, I will draw on Kennedy's work and define political risk as the risk of a loss for a firm or an investor due to

unforeseen momentous and/ or gradual changes in the “rules of the game” under which businesses/ investors operate (fiscal, monetary, trade, labour, investment, industrial, income, environmental policies) and/ or

political instability (civil war, riots, coups, insurrection, terrorism).

Although many authors place greater emphasis on political instability, policy changes are the most frequent and likely source of political risk, according to Lax (1988: 30) and Otto and Cordes (2002: 5–11). Developed countries, for instance, which are not usually prone to political instability, frequently implement policy changes detrimental to the profitability of businesses and/ or investments (Egonu 2007: 10).

As Bremmer and Keat (2009: 9) point out, governments are not the only actors that can create political risk. Rebel groups, non-governmental organizations, individuals, and any other actors who engage in political action can be a source of political risk. New forms of political risk emerge as different players intervene and as political inclinations and other factors change on the national and international fronts. There are several typologies of political risk, but here I will adopt that outlined by Bremmer and Keat (2009: 8, 10, 84):

geopolitical: international wars, great power shifts, economic sanctions and embargoes;

global energy: politically decided supply-and-demand issues;

terrorism: destruction of property, kidnappings/ hijackings;

internal political strife: severe regime or government instability and crises such as state failure, revolutions, civil wars, coups d'état, nationalism, social unrest (strikes, demonstrations);

expropriation: confiscation of property and foreign domestic investments by the government, “creeping” expropriations;

breaches of contract: government frustration or reneging of contracts, wrongful calling of letters of credit;

capital market risks, currency, and repatriations of profits: repatriation of profits, currency controls, politically motivated credit defaults and market shifts;

subtle discrimination and favouritism: discriminatory taxation, corruption; and

unknowns/ uncertainty: political events that cannot be foreseen, effects of global warming or demographic changes.

These different types of political risk are often interrelated and the occurrence of one type of political risk may trigger another. For instance, Iran's support of terrorist organizations such as Hezbollah, Hamas, and Palestinian Islamic Jihad and its stepped-up nuclear programme led US President Clinton to issue Executive Order 12959 (6 May 1995), which banned US trade with and investment in Iran. Shortly thereafter, in 1996, the US Congress passed the Iran-Libya Sanctions Act (ILSA). Under ILSA, all foreign companies that provided investments over 20 million USD for the development of oil resources in Iran were sanctioned (Katzman 2007). In 1997, the US government threatened French oil company Total with sanctions over the 2 billion USD deal that it signed with Petronas and Gazprom to develop Iran's South Pars gas field. In response, Total decided to sell its assets in the US in order to avoid sanctions, and so that it could operate more easily in Iran and other politically sensitive places (Egonu 2007: 17). Total's manoeuvres allowed it to expand its production in Iran, but only for a limited period. In late 2010, following the approval of new and tighter sanctions against Iran by the US, Total along with Statoil, Eni and Royal Dutch Shell decided to abandon their Iranian activities (News Wires 2010). Total's difficult bout with US sanctions against Iran is only one of countless examples of how political risk can affect businesses and investments and result in significant losses. In this case, the oil industry was the main target of political action, but examples abound of other industries being impacted by this and other types of political risk. In August 2011, Venezuelan President Hugo Chávez ordered the expropriation of all farmland owned by Irish cardboard maker Smurfit Kappa Group Plc (SKG) in the states of Portuguesa, Lara and Cojedes (Pons and Orozco 2011).

Political Risk in the Oil and Gas Industry

Political risk is arguably more important in the oil and gas industry than in any other. First, it is relatively easy to sell oil and gas, which makes this industry particularly prone to expropriation. Second, oil and gas investments usually involve the long-term deployment of large fixed assets. Oil and gas projects can take seven years or more to transition from exploration to production, and the field life can be well over 30 years. The politics associated with the field will undoubtedly change over the project's life. Geology itself compounds vulnerability. Oil reserves are scattered across the globe, many in countries with unstable political systems and/ or weak legal systems. To succeed, industry players must interact intensively with national leaders, domestic politicians, and non-governmental interest groups. This includes dealing with different degrees of “resource nationalism” – that is, with distinct levels of state control of natural resources and the resulting potential to use this power to exert sovereignty whilst securing access to the large economic rents embedded in oil and gas prices (Click and Weiner 2010: 783–803; Bremmer and Keat 2009: 129).

The oil and gas industry has proven to be vulnerable to several major forms of political risk, as illustrated in the following examples:

Breaches of contract: In 2007 the Ecuadorian government declared that all foreign oil companies would be required to hand over to the government all earnings over 24 USD per barrel, a significant divergence from the initial contracts the foreign oil companies signed, by which only 50 per cent of the earnings over 24 USD were to be handed over. The Ecuadorian government also gave the companies the option of switching to new service contracts, whose terms are equally unfavourable (Bremmer and Keat 2009: 224).

Expropriation: In May 2006, Bolivian President Evo Morales issued a decree that forced 25 private gas companies to sell at least 51 per cent of their holdings to the state-owned Yacimientos Petrolíferos Fiscales Bolivianos (YPFB). Firms were given six months to renegotiate their contracts with the Bolivian government or face expulsion. The decree also stated that the companies in control of the two largest oil fields had to absorb an immediate 32 per cent hike (82 per cent total) in royalties and taxes (Zissis 2006).

“Creeping expropriation”: In 2003, the Russian government took several steps that culminated in the expropriation of property held by Yukos, a private Russian oil company. First, it filed charges of tax evasion and fraud against Yukos and the company's leaders and had them arrested. The government subsequently froze most of Yukos’ assets, which made payment of back taxes and fines nearly impossible. The government intervention culminated when the government announced that Yukos’ main production asset, Yuganskneftegaz, would be sold to pay off the company's debts, regardless of Yukos’ success in repaying its debts (Barnes 2007).

Subtle discrimination and favouritism: In a 2003 filing to the US Securities and Exchange Commission, Halliburton, a US oil-services company, declared that in the two previous years it had made improper payments of approximately 2.4 million USD to a tax official in Nigeria for favourable tax treatment regarding an oil and gas facility. Later, both the US Department of Justice and a French judge separately initiated enquiries into allegedly illicit payments of 180 million USD to Nigerian officials in the late 1990s by a consortium that included a Halliburton subsidiary (McMillan 2011).

Internal political strife: In July and in September 2011, violent protests over labour, social and environmental concerns erupted at Pacific Rubiales’ installations in Colombia, shutting down production. In both instances, the Canadian oil firm was eventually able to reach temporary agreements with the protesters (mostly oil workers and local residents) and resume production (Otis 2011).

Terrorism: In November 2011, eight pirates boarded an oil supply vessel belonging to Chouest, a service company working in Chevron's Agbami field in Nigeria. The pirates took three hostages (Reuters 2011c).

A quick look at current industry exploration activities indicates that there are few countries where political risk is an insurmountable factor. The assessment of and aversion to political risk, however, varies among companies. On the whole, it seems that the willingness to accept political risk is shaped by geological and commercial attractiveness (that is, the size of potential/ proven reserves, how they fit strategically into corporate goals, objectives and the overall portfolio of assets), and by a company's financial strength and level of experience in managing political risk (Stauffer 1997).

Political Risk Management in the Oil and Gas Industry

Oil and gas companies’ political risk management has not been uniform over time. Historically, oil companies have enlisted the services of home governments to deal with volatile political environments (Zakariya 1988: 206–209). Despite some initial success, this approach eventually proved insufficient. In response, oil and gas companies developed a variety of additional strategies to manage all pertinent forms of political risk:

Flexible contract terms and openness to renegotiation: If the contracts’ structure and terms are inflexible, they will not be able to adapt to the changes that often occur in the relationship between governments and companies, as described by the “obsolescing bargain” in 1971 (Moran 2000) and the “private-nationalization cycle” (Chua 1995).

Stabilization clauses: When an oil and gas company has enough clout, it may be able to negotiate “stabilization clauses” into the contracts. These clauses “preclude the application to an agreement of any subsequent legislative (statutory) or administrative (regulatory) act issued by the government […] that modifies the legal situation of the investor” (Coale 2002; Kinsella and Comeaux 1994).

International arbitration clauses: These clauses stipulate international arbitration as the method used to settle any disputes arising in connection with the contract that cannot be resolved through negotiation. They define the jurisdiction, the scope, and procedures by which the arbitration shall be conducted. This includes the selection of international arbitral bodies from a long list of institutions that includes the prominent International Chamber of Commerce (ICC) and the International Centre for Settlement of Investment Disputes (ICSID).

Investment protection treaties: International investment treaties like the Energy Charter Treaty and bilateral investment treaties (BITs) contain guarantees that certain standards of treatment of investors and investments will be upheld. This includes protection against contract breaches and commensurate compensation if such breaches occur.

Political risk insurance: Insurance provides financial support to oil companies when they experience losses due to material changes unilaterally imposed by a host government on contracts. Insurance is available from a number of sources, including private insurers, nationally sponsored insurance agencies like the Overseas Private Investment Corporation (OPIC), and the World Bank's Multilateral Investment Guarantee Agency (MIGA) (Kinsella and Comeaux 1994: 25, 30–31).

Same as above (A)

Production-sharing agreements (PSAs): These contracts give foreign investors control of operations while ownership remains with the host country. Although sub-optimal from the perspective of international oil companies (IOCs) because they prefer “no sharing”, PSAs have been used to deal with resource nationalism.

Joint Ventures (JVs): Forging joint ventures with local equity partners can help reduce risk exposure, but the success of this strategy depends entirely on choosing the right partner. This can be especially important in emerging markets, where the history of a local company and its political connections are often unclear.

“Network of interdependence”: Firms and private corporations, non-governmental organizations, international institutions, and private stakeholders that come together through “creative financing” (including financing from local banks that increases the default risks that expropriations pose for the host country's banking system or other means) in order create a domestic and international constituency with a stake in the firm's continued success.

Same as above (B)

Cui bono (“who benefits”): Context matters, as does the realization that individuals are behind the decisions affecting regulations and other matters. Those who hold social and political power have particular and identifiable sets of motivations and limitations. This makes them predictable. If companies map these incentives and constraints, it is considerably easier to forecast how the regulatory climate will evolve (Bremmer and Keat 2009: 149, 152).

Development of good relationships with well-connected individuals, especially government officials: Although lobbying is important (and extensive) in developed countries (Froomkin 2011), it is particularly relevant in countries with poorly established legal systems where officials at both the national and regional levels have considerable personal discretion over decisions pertinent to the operations of foreign businesses.

Early warning and agile response: A firm's success in adapting to the often game-changing events in the regulatory environment depends on its ability to spot them as early as possible and on the speed, flexibility and competence with which it adapts to these changes.

Domestic and international anti-bribery laws: One way for oil and gas companies to avoid getting entangled with corruption is to cite domestic laws like the US Foreign Corrupt Practices Act (1977) and international conventions like the OECD Anti-Bribery Convention (1997). While this may reduce some business opportunities, generally it can help insulate oil and gas companies from the fall-out that usually occurs when power changes hands (Andrews-Speed 2008: 148–149).

Transparency and clear reporting: Transparent and regular reporting of payments made to governments dramatically reduces exposure to corruption, but it may have a significant opportunity cost. Only when all companies disclose the same information, as proposed by the Extractive Industries Transparency Initiative (2002), will there be a level playing field.

Same as above (C)

Social accommodation: Oil companies can build support amongst local stakeholders, NGOs and community groups by addressing their concerns, including over labour issues, environmental degradation, and the protection of the poor and of ethnic minorities. Accommodation usually involves such substantive goodwill gestures like the construction of schools, hospitals, playgrounds, and the provision of jobs, all of which directly enhance the quality of life of local residents (Bremmer and Keat 2009: 101–102, 153).

Gathering of intelligence: By cultivating relationships with key domestic players, oil companies may gain access to information that can provide a useful hedge against the risk of violent conflict.

Risk avoidance: Hydrocarbon firms can either divest from a project or region or delay market entry as they wait for a change in the political circumstances. The ability to do so can be sharply limited, however.

Effective management of political risk requires an understanding of which tools and methods (such as the ones described above) are best suited to a particular political environment. A significant number of oil and gas companies, particularly the majors and super-majors, have developed the in-house capacity to assess and manage political risks. Other companies hire specialized consultants – Wood Mackenzie, PFC Energy, Oxford Analytica, IHS CERA, Eurasia, etc. – to

bridge the wide gap between what the individual business manager knows or can find out by the use of his own resources and what he would have to know to conduct his business in a perfectly intelligent fashion (Knight 1921: 261).

Some companies fail to do either because they generally believe that the use of scarce resources to increase knowledge is, as influential economist Knight once wrote, “an operation attended with the greatest uncertainty of all” (Knight 1921: 318).

They argue that there is much that cannot be known, whether because chains of events are too complex or because ingrained bias prevents analysts from fully understanding the reality of situations. Politics is also notoriously hard to quantify. Furthermore, as Bremmer and Keat point out, the observation of a risk changes the risk itself. Finally, what holds today may not hold tomorrow, as circumstances constantly change (Bremmer and Keat 2009: 24, 196, 197).

Recent years have tested oil and gas companies’ political risk management skills. In a relatively short period of time, the industry experienced the rebirth of resource nationalism; significant political instability in North Africa and the Middle East (the source of one-third of the world's oil production); piracy targeting major oil lines in the Arabian Sea and the Indian Ocean; an increasing number of kidnappings for ransom (in Nigeria, Colombia, Ethiopia, Mexico, and other locations) (Chaskin and Noel 2011); major anti-oil protests in Peru, Ecuador, Canada, and the US; and, finally, political and economic volatility in the aftermath of the 2008 financial crisis.

Dealing with this uncertainty and volatility has proven challenging even for the experienced IOCs like Exxon and national oil companies (NOCs) such as Petrobras. For instance, as the Standard General Counsels Group recently observed, these companies were not able to use existing political management tools to ensure minimal losses following the return of resource nationalism in countries such as Russia, Venezuela, Ecuador and Bolivia (Andrews-Speed 2008: 142). If experienced oil and gas companies are having problems protecting their interests, one wonders how companies that have only recently become active and visible in the international arena are coping with this uncertainty. A case in point is Chinese NOCs. Since 1993 Chinese NOCs have significantly raised their profile and exposed themselves to increasing amounts of political risk through overseas investment. By late 2010, Chinese NOCs were operating in 31 countries and owned equity oil in 20 of these countries, though their equity shares are mostly located in four countries particularly prone to political risks: Sudan, Venezuela, Angola and Kazakhstan (Jiang and Sinton 2011).

Political Risk Management: Chinese NOCs

To understand Chinese NOCs’ political risk management, one must understand the origins of these companies. China's three major oil companies – China National Petroleum Corporation (CNPC), China Petrochemical Corporation (Sinopec) and China National Offshore Oil Corporation (CNOOC) – were all part of the all-encompassing former ministries of petroleum and chemical industries. It was only in the late 1980s that the Chinese government decided to move toward a system based on companies and rooted in the marketplace. Previously enjoying administrative and market privileges, companies were now expected “to earn a living” and “to be competitive”, according to Zhou Qingzu, CNPC's chief economist (Yergin 2011: 202). In the midst of adjusting to this massive cultural change, Chinese NOCs faced very difficult challenges at home: artificially low retail prices of crude set by the government, a massive workforce, ageing oil fields, and low reserves-to-production (R/P) ratios. By 1993, Chinese NOCs’ petroleum production could no longer meet the country's growing oil demand. As a result, China became a net oil importer. A Chinese oil expert reported that “from an industry point of view, we felt very ashamed. It was a loss of face. We couldn't supply our own economy” (Yergin 2011: 202).

1993–2002: Early Endeavours

If Chinese NOCs were to become more competitive and develop supplies to serve China's future growth, they had to “go out”. The reserves they needed were overseas but so, too, were the risks. Fortunately for the Chinese NOCs, the difficult exploration and production (E&P) environment in China had reared adventurous explorers. In 1993, with limited funds and little overseas experience, Chinese NOCs took their first steps abroad, acquiring minor stakes in Canada and Peru. Small projects followed in several countries, including Ecuador, Kazakhstan, Malaysia, Mongolia, Russia, Sudan, Thailand and Venezuela.

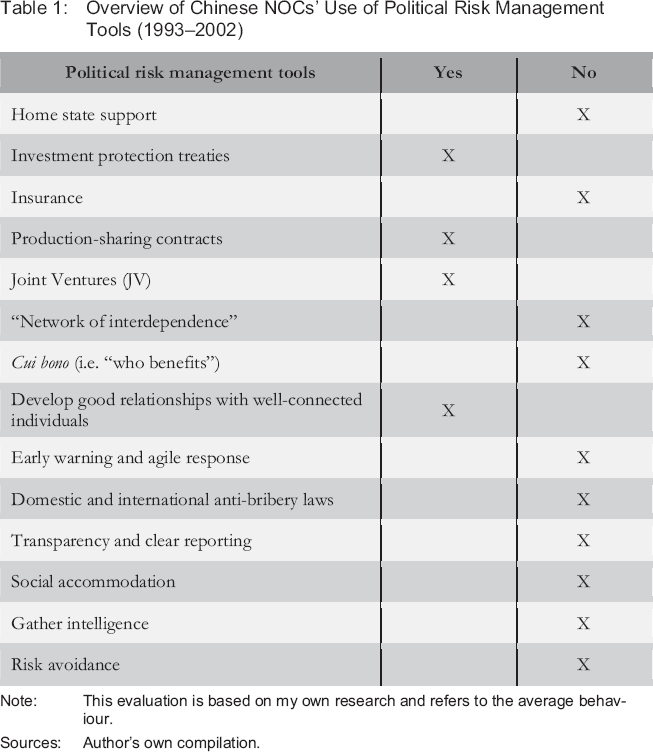

After stepping out from under Beijing's wings, Chinese NOCs were forced to deal with the risks they encountered overseas. Previous lack of exposure to these risks combined with little experience operating overseas culminated in Chinese NOCs’ rather unsophisticated risk management during the first phase of their internationalization (1993–2002). With respect to political risks, Chinese NOCs opted not to tailor their responses to different forms of risk, but instead applied a “one-size-fits-all” approach primarily rooted in the development of good relations with well-connected individuals:

The Chinese NOCs’ preference for developing good relations can be partly

explained by the priority given to building personal relationships in China. The

Chinese customarily build personal relationships ( , guanxi)

of mutual trust and obligation to develop business relationships. This requires

a lot of time, money and effort, which is why it is preferable to focus on a

select few. Suffering from “mirror imaging” – assuming that those we assess

think, behave, and understand their interests as we do – (Bremmer and Keat 2009:

175) Chinese NOCs concentrated on political elites, whom the Chinese believed

could protect and facilitate deals by themselves. However, just because

communist party and government leaders (both national and regional) have

undisputed control over major decisions that affect China's oil and gas

industry, this does not mean that leaders in other countries operate under the

same set of incentives, constraints and perceptions.

, guanxi)

of mutual trust and obligation to develop business relationships. This requires

a lot of time, money and effort, which is why it is preferable to focus on a

select few. Suffering from “mirror imaging” – assuming that those we assess

think, behave, and understand their interests as we do – (Bremmer and Keat 2009:

175) Chinese NOCs concentrated on political elites, whom the Chinese believed

could protect and facilitate deals by themselves. However, just because

communist party and government leaders (both national and regional) have

undisputed control over major decisions that affect China's oil and gas

industry, this does not mean that leaders in other countries operate under the

same set of incentives, constraints and perceptions.

Overview of Chinese NOCs’ Use of Political Risk Management Tools (1993–2002)

Note: This evaluation is based on my own research and refers to the average behaviour.

Sources: Author's own compilation.

In addition to developing good relations, Chinese NOCs have entered into joint ventures with governments and strategic investors like Pluspetrol in Peru (1993) and Petronas, ONG Videsh and Sudapet in Sudan (1996). However, Chinese NOCs have not applied this political risk mitigation strategy consistently. In fact, whenever possible, they have tried to secure sole control of the reserves. A case in point is CNPC's acquisition of the Caracoles and Intercampo oil fields in Venezuela (1997). This suggests that the decision of Chinese NOCs to join JVs was more an external imposition than the product of a thought-out political risk mitigation strategy.

The same can be said about production-sharing agreements. Chinese NOCs signed several PSAs in this early internationalization phase mostly because they were operating in countries where PSAs had emerged as the main type of petroleum contracts. PSAs were not, at least not initially, the favoured form of oil contract signed by Chinese NOCs, or for that matter by IOCs, as oil reserves remain in the hands of the local governments and/ or national oil companies.

It is not easy to gather information on oil contracts, as the industry places a high premium on confidentiality. Therefore, it is difficult to determine whether Chinese NOCs consistently adopted any of the existing legal risk management tools. Based on the limited sample I have had the chance to survey, the oil contracts signed by Chinese NOCs adhere to industry standards. They contain international arbitration clauses, flexible terms and often stabilization clauses, which can be used by Chinese NOCs to protect their interests overseas.

Chinese NOCs have no direct input in the signing of international treaties but they can (and often do) use them to deter and/ or mitigate the impact of political risks. When Chinese NOCs first began their forays overseas, the number of BITs was relatively small. Out of the 45 BITs in force in 1993, only one was with a major oil-producing country (Kuwait). In less than a decade, the number of Chinese BITs grew ninefold as 41 new BITs entered into force by 2002. Particularly relevant to Chinese NOCs were the BITs signed with several oil producers, including Saudi Arabia (1997), the United Arab Emirates (1994), Kazakhstan (1994), Uzbekistan (1994), Indonesia (1995), Peru (1995) and Ecuador (1997) (ICSID Database of Bilateral Investment Treaties 2011). In addition to signing this multitude of BITs, China joined the Energy Charter Treaty as an observer in 2001 (Energy Charter 2011).

As with the BITs, governments can adopt domestic and international anti-bribery laws. As mentioned earlier, these laws are beneficial in the long term because they tackle the political risk that arises from corruption. In the short term, however, promoting transparency may cost business opportunities that latecomers such as China's NOCs can ill afford to lose. (Un)fortunately for Chinese NOCs, during the initial stages of their international foray Beijing did not address the issue of corruption, one of the deleterious by-products of its opaque rule. As a result, Chinese NOCs were limited to the most common disclosures required by the stock exchanges on which they are listed: London, Hong Kong and New York.

Chinese NOCs, much like the Chinese central government, are quite opaque in their management. Indeed, Beijing became aware of Chinese NOCs’ early overseas ventures only after the fact. Chinese NOCs purposefully kept the details of their early dealings secret because they feared the government would see this international push as a distraction from their mission to increase domestic production to meet the country's burgeoning demand. When the central government finally learned of the NOCs’ overseas incursions, Beijing showed its disapproval by making it extremely difficult and time-consuming to secure the necessary government approvals and government credit (Anonymous 3).

With limited host-country support – particularly until the late 1990s – and a shortage in funds and management resources, Chinese NOCs were forced to weigh priorities regarding their overseas investments. Priority was given to identifying and acquiring the assets. After securing access, focus then shifted to the short-term needs of the project – mostly technical and geological. Chinese NOCs tapped into their surplus workforce and cheaper Chinese suppliers to minimize the costs of production. Political risk insurance was viewed as an expensive superfluity as were all efforts to understand, gather intelligence and/ or accommodate the interests and concerns of the societies in which they operated (Anonymous 2). Chinese NOCs at the time operated under the belief that no great benefit would accrue from securing support amongst local stakeholders because they were believed to have little influence, like their Chinese counterparts (“mirror-imaging” bias). Furthermore, local realities were too complex and daunting and there was nothing that the resource-poor and inexperienced Chinese NOCs could actually do to impact them. Failed projects, expropriations and other potentially negative events were doomed to occur but the NOCs were willing to absorb that risk because the alternative was much worse: Chinese NOCs not having access to new profit-generating operations and to the reserves needed to replenish their dwindling domestic resource base.

Gradually, the initial approach of Chinese NOCs to political risk started to falter under the weight of events, including indigenous protests against CNPC's labour and environmental practices in Peru and violent attacks against Chinese workers in Sudan (Anonymous 1). Despite these and other troubles, Chinese NOCs continued pursuing opportunities in a growing number of regions, fuelled by their desire to acquire equity stakes. As a result, Chinese NOCs – particularly CNPC – amassed an eclectic assortment of small assets that spanned the world (Downs 2008: 27–31). Most of these assets had originally been passed over by the IOCs due to their low rate of return and significant above-ground risks.

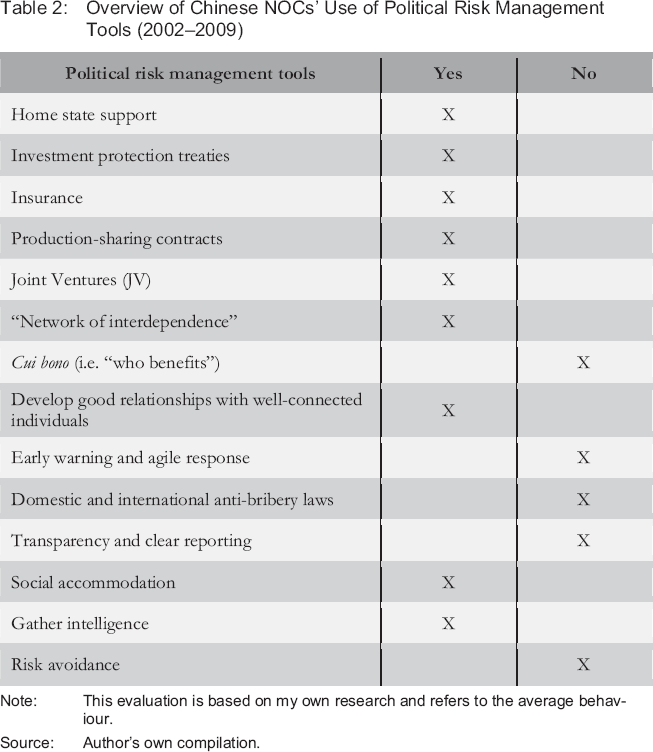

2002–2009: Growing Pains

By the beginning of the new century, Beijing realized that the overseas expansion of Chinese NOCs played a central role in meeting China's rapidly growing demand for oil. In March 2001, the Chinese leadership made its support for the international expansion of the NOCs known, when it wrote the “going-out” strategy into China's 10th Five-Year Plan. It reiterated that commitment at the 16th National Party Congress in 2002. Apart from encouraging internationalization, the “going-out” strategy implemented a variety of policies that ensured state support in the forms of an investment-friendly policy framework – for instance, relaxation of foreign currency controls, direct and indirect subsidies, and favourable financing such as credit lines and low-interest loans from state-owned financial institutions like the Export-Import Bank of China (China Exim Bank) and the China Development Bank (CDB) (Lunding 2006).

Beijing's 2002 announcement ushered in a new phase of internationalization for Chinese NOCs. This phase, which lasted until 2009, was marked by an important shift in Chinese NOCs’ investment patterns. After familiarizing themselves with the international operating environment, Chinese NOCs moved away from small and often challenging low-profit projects – including frontier acreage and enhanced oil recovery (EOR) – and focused on large and medium-sized projects with low risk. In addition, they invested in exploration projects with higher risks and expanded developments from onshore fields to shallow seas. Finally, long-term supply contracts and mergers and acquisitions became increasingly popular, whilst equity oil acquisitions declined.

The changes in the investment patterns of Chinese NOCs were facilitated in part by the advances made in terms of human resources. Another factor that contributed to the shift was the experience that the NOCs accumulated whilst exploring methods for managing overseas projects and subsidiaries. At the core of the shift was Beijing's decision to support Chinese NOCs’ overseas efforts. Not only did Beijing's support mean access to plentiful and relatively cheap financing, but it could also be used as a significant political risk management tool.

Home-state support can be both a blessing and a curse for Chinese NOCs’ political risk management. On one hand, direct association with Beijing can be costly, particularly in societies where there are anxieties vis-à-vis China's political regime characteristics and global ambitions. Chinese NOCs have tried to counter this issue by establishing and/ or using existing international subsidiaries, often listed on major stock exchanges, to lead international investments. Ostensibly, the international market will bind NOCs to international management and operating norms, thereby insulating or removing them from Beijing's direct bidding. When this strategy has not been effective, it at times has resulted in significant damage to Chinese NOCs’ interests.

On the other hand, the Chinese government can use its diplomatic and economic influence to promote good relations between the host government leadership and the NOCs, which may facilitate and, most importantly, insulate Chinese NOCs’ investments from a potentially unstable socio-economic environment. Similarly, knowing that Beijing may perceive any attacks against Chinese NOCs as attacks against the Chinese government may deter some governments and/ or groups from acting against Chinese assets. If attacks do occur, the Chinese government can be a source of additional protection and guidance for Chinese NOCs. Finally, home-government support, particularly financial support, frees up resources that Chinese NOCs can invest in other political risk management tools to improve their ability to assess and manage risk.

One such tool is political risk insurance. As the size and number of Chinese NOCs’ projects overseas increase, their capacity to absorb potential losses declines. Under these circumstances, political risk insurance becomes increasingly important as a means of offsetting risks in overseas investments. This partly explains the uptick in purchases of political risk insurance by Chinese NOCs since the early 2000s. Another factor contributing to the popularization of political insurance amongst Chinese NOCs was the 2001 establishment of China's first and only policy-oriented insurance company, the China Export & Credit Insurance Corporation (Sinosure). Unlike traditional insurance providers such as MIGA, Sinosure is backed by the Chinese government's bountiful reserves – a reassurance for many Chinese NOCs. Furthermore, Sinosure's familiarity with China's business environment and Beijing's inner workings allows it to tailor services to the potential policyholder's needs, which makes it more appealing. Amongst the Chinese NOCs, CNPC has been the most active client of Sinosure, acquiring several policies, including an insurance policy for CNPC's share acquisition of the company Petro-Kazakhstan in October 2006. CNPC was also the first to sign a strategic partnership with Sinosure (2008) to expand its cooperation regarding capital security and political risk assessment and management.

Sinosure is only one of several players participating in networks of interdependence, which were established to support the overseas expansion of Chinese firms in line with the country's “going-out” strategy. These networks are designed to minimize economic, financial and political risks by fostering interdependence between the multiple parties involved. At the centre of these networks lies a government-owned financial institution: China Exim Bank. The bank connects resource-rich countries that have no adequate financial guarantees needed to finance infrastructure projects with Chinese NOCs and construction firms, both anxious to access those resources and business opportunities. The Exim Bank provides preferred lines of credit to the host-country government to cover infrastructure projects undertaken by Chinese contractors. The money never reaches the government. Instead, it is used to pay the Chinese contractors in China. Repayment is in the form of oil or other raw materials. This strategy follows a long history of natural resource-based transactions in the oil industry.

The first iterations of these networks emerged in 2001 in the Democratic Republic of the Congo and in Sudan, where the Congo River dam (280 million USD) and the Al-Jaily power plant (128 million USD), respectively, were backed by crude oil supply guarantees (Foster et al. 2009). Since the landmark oil-backed deal with Angola in 2004 (1.02 billion USD), the “resources for infrastructure” or “Angola mode” approach has become more popular. Despite its success, this strategy has significant downsides. First, it supports the perception that Chinese NOCs are not driven by a strong commercial interest, but instead by the state's energy security concerns. Second, it exposes Chinese NOCs to the risks associated with corruption and with working too closely with the governing elites.

Along with network development, political insurance and home-state support, Chinese NOCs also started investing, albeit modestly, in social accommodation and intelligence-gathering. They were responding to the protests like those experienced by CNPC in its previous expansionary phase in Peru. The goal of the intelligence-gathering was to appease the population without incurring any significant expenses. All of these developments significantly expanded the political risk management toolkit of Chinese NOCs.

Overview of Chinese NOCs’ Use of Political Risk Management Tools (2002–2009)

Note: This evaluation is based on my own research and refers to the average behaviour.

Source: Author's own compilation.

Access to more tools is a necessary but not sufficient condition for success in political risk management. To be successful, one needs to have experience and the capacity to know when and which of the available instruments or combination thereof needs to be applied. Chinese NOCs, unfortunately, were still lacking that capacity from 2002 to 2009 and as a result experienced several substantial setbacks. Although costly and painful, these unfortunate events provided valuable lessons to Chinese NOCs.

Perhaps the most notorious setback Chinese NOCs experienced in this period was CNOOC's failed attempt to acquire the Union Oil Company of California (UNOCAL). In 2005, CNOOC made an 18.5 billion USD bid to purchase UNOCAL, a large, independent US company, with significant presence in the gas sector in Thailand and Indonesia and pipelines in Central Asia. CNOOC initially expected to win because its bid was 0.7 billion USD higher than that of its direct competitor, Chevron. In the end, however, CNOOC withdrew its bid due to the harsh political reaction it encountered in the US.

At the core of CNOOC's failure lies its biased view of politics. The company's leadership seems to have operated under the assumption that the White House, much like the Central Committee in China, dominates the political system in the US. As such, if the White House was open to foreign investment, the US itself would be hospitable. This incredibly naive assumption points to a complete lack of understanding of the US political system and the diversity of interests at play. It also suggests utter ignorance of how geopolitics and, in particular, national security can and often do impact business dealings. CNOOC also showed complete disregard for timing and public opinion. China's large bid in a sensitive foreign domestic sector – energy – at a time when anti-China sentiment was on the rise was imprudent. That Chinese NOCs made little effort to cultivate a favourable investing environment by appealing to the US government or ingratiating themselves to the general public – for example, through a public relations campaign or political lobbying – exacerbated an already difficult situation (Grier 2005). As such, CNOOC's failure can also be attributed to its belated response to the US Congress’ forceful reaction. If CNOOC had intervened earlier and more effectively, it might have been able to shape rather than be shaped by the course of events.

CNPC and Sinopec experienced their own significant setback when Venezuelan President Hugo Chávez decided to apply the 2001 Hydrocarbon Law more strictly, starting in 2006. To this end, the Venezuelan government required the review and resigning of all contracts that Petróleos de Venezuela SA (PDVSA) had signed with foreign oil companies. PDVSA took 80 per cent control of the Intercampo and Caracoles fields, which CNPC had purchased for 360 million USD in 1997 and for which CNPC had acquired 20-year exploitation rights. Sinopec was also forced to change its PSA into a JV, majority owned by PDVSA (Millard 2007; Sinocast China Financial Watch 2007; Ng 2007). CNPC also received a circular from Seniat, Venezuela's taxation organ, which required its subsidiary in Venezuela to make a supplementary payment of 11 million USD for overdue taxes in 2005 resulting from the application of an incorrect income tax rate (Sinocast China Financial Watch 2007). Despite their dissatisfaction, CNPC and Sinopec, like most IOCs, ultimately acquiesced to Venezuela's state control strategy, subsequent to warnings that the government would expropriate their assets if they refused to follow suit (Liu 2007). The IOCs and foreign NOCs, including CNPC, had already invested heavily in the Orinoco Belt and still wanted to have access – even if limited – to one of the world's largest oil reserves.

The Venezuelan case is a clear example of how developing good relations with key well-connected individuals is not always a reliable political risk management tool. This is particularly true when the rule of law is weak (or non-existent) and the leadership is personalized such as Chávez’ (Andrews-Speed 2008: 144). Personalized leaders are primarily concerned with their own self-interests, which means that they may (and will) often sacrifice the interests of others – including the NOCs – in favour of their own. To succeed in this type of environment, Chinese NOCs need to move beyond the rhetoric and focus on the underlying drivers of behaviour. This requires in-depth knowledge not only of the leader but also of the socio-economic and political context in which he/ she operates. Only then can Chinese NOCs aspire to anticipate change – in contract terms, or tax or royalty rates, for instance – in time to defend their interests.

In addition to having their interests undermined by capricious political leaders, Chinese NOCs also experienced several attacks organized by members of the local communities in which they operated between 2002 and 2009 (Kong 2010: 113). In November 2006, for instance, local residents in Ecuador's Amazonian province of Sucumbios cut electricity to an oil field controlled by Andes Petroleum – owned by CNPC and Sinopec – and took 40 Chinese oil workers hostage. In July 2007, less than a year after the Sucumbios incident, Indian-led protests erupted once again in Ecuador, this time against PetroOriental, which is also owned by CNPC and Sinopec. Several people were injured, mostly military personnel. Violence escalated to such a level that Ecuadorian President Rafael Correa had to declare a state of emergency in the area. In both instances, demonstrators demanded that the Chinese-owned oil firms fulfil their commitment to hire local workers and make greater investment in health and education (EFE News Service 2007).

Demonstrations such as the ones in Ecuador underscore the importance of taking social accommodation seriously. Failure to do so, whether by action or by omission, has very significant costs, including damage to the NOCs’ international and domestic reputation, kidnappings/ killings of workers, delays and additional costs to the projects and, finally, loss of revenue. The protests also highlight the limitations of Chinese NOCs’ nascent community outreach efforts. Measures such as distributing toys to local children or providing vaccines to the population help generate goodwill, but they do not tackle the actual roots of discontentment: joblessness, environmental degradation and other social concerns (Economist Intelligence Unit 2007). Addressing these issues requires major adjustments that Chinese NOCs were reluctant to make. One area in particular needs reform: Chinese NOCs human resources policy. As long as Chinese NOCs keep employing a large number of Chinese oil workers in their overseas operations, there will be little room for local hires. If this policy remains in place, resentment amongst the local population is bound to increase, subjecting Chinese nationals to growing security risks (Asia Pulse News 2008).

Resistance to change will expose Chinese NOCs to increasing political and security risks. In some cases, however, it is precisely Chinese NOCs’ desire to change that makes them vulnerable to political risk. A case in point is the 2008 failed joint bid by Sinopec and CNOOC for a 20 per cent stake in Angola's Block 32. Sinopec and CNOOC, collaborating for the first time in such a venture, planned to pay 1.3 billion USD to Marathon and thereby secure access to the block's estimated recoverable reserves of 1.5 billion barrels of light crude. They successfully outmanoeuvred Brazil's Petrobras, India's ONGC Videsh and even a separate bid by CNPC. They were due to conclude the sale when Sonangol, Angola's NOC, exercised its pre-emption right and acquired Marathon's stake (Petroleum Economist 2009).

The main reason for CNOOC/ Sinopec's failure to acquire Block 32 was the Angolan elites’ unwillingness to accept any changes to the investment model that Sinopec had been using since its first foray in the country in 2004. To ensure market access, Sinopec entered a joint venture with China Sonangol International Holding (CSIH), which has the support of key stakeholders among the Angolan elite (Vines et al. 2009). Thanks to this JV – Sonangol Sinopec International (SSI) – Sinopec managed to be one of the few NOCs included in the network of personal friendships that controls Angolan politics and economics. Access to this network facilitated SSI's acquisition of stakes in several blocks in Angola, but at a significant cost (Vines et al. 2009). The opacity surrounding SSI and its companion CSIH has created fertile ground for corruption. Angolan elites view both SSI and CSIH as mechanisms that ensure that they will get paid twice for the same asset: first as part of the government (when it is sold) and second as part of the company (when the blocks produce). This extra-budgetary source of revenue is particularly important at a time when Angola's economy is under increasing pressure to become more transparent (Vines 2011). In contrast, Sinopec views SSI as a temporary solution, a stepping stone. Over time, Sinopec hoped to use the experience and contacts accumulated while operating as part of SSI to launch its own, independent ventures in Angola. It did not expect that by entering into the JV with key Angolan stakeholders it would create a constituency that would come to expect the benefits of this partnership (financial and otherwise) and would use its influence to prevent Sinopec from changing the status quo. For now, at least, Angolan elites have the upper hand and Sinopec has returned to investing in Angola through the “elite-approved” and “corruption-laden” SSI.

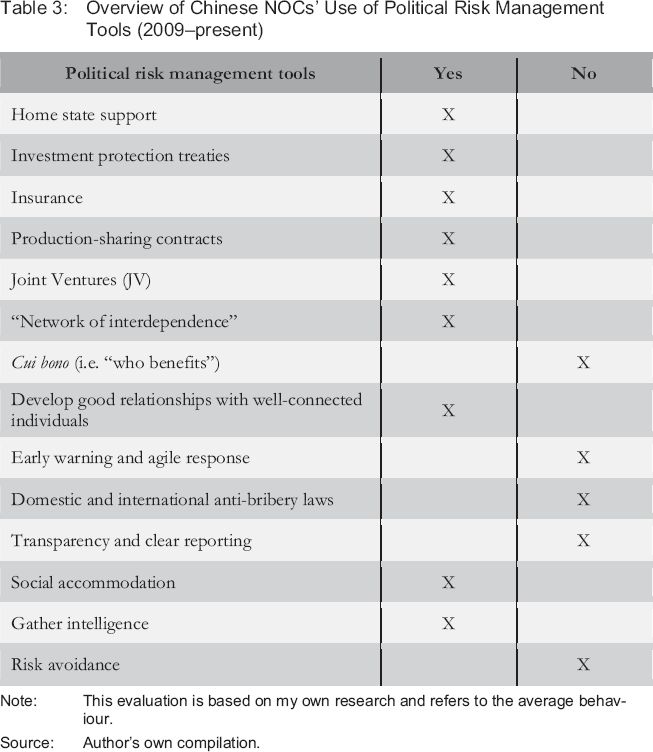

2009–present: Informed Expansion

The 2008 financial crisis launched a period of “creative destruction in the geopolitical and geo-economic space” that the world had “not seen since World War II” (Bremmer and Shalett 2011). Flush with cash in a post-crisis buyer's market, Chinese NOCs moved to expand their presence at the international level.

Unlike in the past, when investments were unfocused and ill advised, Chinese NOCs are using previous experiences to inform their investment decisions. They are also benefitting from the expansion of the NOCs’ political risk management toolkit in the previous phase.

A survey of the main international dealings of Chinese NOCs since 2009 suggests that M&A has become a favoured strategy. In 2010 Chinese NOCs’ M&A reached 26 billion USD, an 85 per cent increase vis-à-vis 2009 and equivalent to 15 per cent of global upstream deals. Implicit in these deals was an increased willingness to apportion significant value to technical expertise and long-term undeveloped resources in stable countries – such as US shale gas, Canadian oil sands and Brazilian pre-salt – rather than relying just on proven reserves and production.

Overview of Chinese NOCs’ Use of Political Risk Management Tools (2009–present)

Note: This evaluation is based on my own research and refers to the average behaviour.

Source: Author's own compilation.

The M&A deals were also shaped by Chinese NOCs’ realization of the importance of political risk and its management. As such, Chinese NOCs acquired large stakes in the following firms and operations:

Host-country firms like MMG in Kazakhstan (CNPC, 2009), Repsol Brazil (Sinopec, 2010), Galp Brazil (Sinopec, 2011) and Daylight Energy (Sinopec, 2011). Through these deals, Chinese NOCs acquired knowledge of and direct experience in the country, which are essential when managing several forms of risk, including: geopolitical factors, breaches of contract, subtle discrimination and favouritism, internal political strife and terrorism.

Mid- to large-size firms with proven and extensive regional presence such as Addax (Sinopec, 2009), SPC (CNPC, 2009), Emerald Energy Plc (Sinochem, 2009), Bridas (CNOOC, 2010) and Nexen (CNOOC, 2013). By purchasing these large stakes, Chinese NOCs acquired knowledge of and on-the-ground experience in West Africa (Addax, Nexen), Asia (SPC), the US (Emerald Energy Plc, Nexen) and Latin America (Bridas, Nexen and Emerald Energy Plc). They also obtained valuable proxies that can be used in environments hostile to Chinese NOCs. Both developments are useful when dealing with the same types of risk mentioned in host-country firms.

Projects led/ operated by host-country firms such as Canada's Athabasca Oil Sands Corps’ Mackay River and Dover oil sands projects (CNPC, 2009) and Chesapeake Energy's shale projects in Texas, Wyoming and Colorado (CNOOC, 2010 and 2011). In addition to access to technology and operations management expertise, these types of deals allow Chinese NOCs to enter areas that may otherwise not have been available due to national security and/ or social and environmental concerns. The main forms of political risk targeted by these strategic investments are geopolitical factors, internal political strife and subtle discrimination and favouritism.

Projects operated by or with majors such as Statoil (CNOOC, 2009 and Sinochem, 2010), Total (Sinopec, 2010 and CNOOC, 2010), Shell (CNPC, 2010) and Chevron (Sinopec, 2010). Working in partnership with respected majors improves the images of NOCs while burnishing the latter's analytical capacity and access to local and international networks. In addition to helping mitigate most of the political risks mentioned in host-county firms, these types of deals also may assist Chinese NOCs in dealing with the unknown and uncertainty thanks to the majors’ depth of experience and commitment to predicting and planning for the future.

As with all strategies for reducing political risk, there are limits to the effectiveness of those described above. Host-country firms as well as mid-sized regional firms are often confronted with political risk events they cannot predict and/ or affect. The same can be said about IOCs that have experienced several setbacks in the current decade. High oil prices, increased industry competition, the lack of alternative investment options for IOCs and an increasingly antagonistic political climate in many oil-exporting states has weakened IOCs’ bargaining power and often results in unfavourable outcomes for IOCs (Vivoda 2009). A case in point is Angola's November 2011 law that forces oil companies to use the country's banking system to pay taxes and overseas suppliers and subcontractors. IOCs lobbied against the law for years but only succeeded in delaying its implementation (Anonymous 4; Reuters 2011c).

In addition to M&A, long-term oil and gas supply contracts have become a preferred strategy to secure access to resources whilst minimizing risk. Risk is spread across the financial institutions that are lending the funds: primarily the China Development Bank, the Chinese government that owns these financial institutions, and the Chinese NOCs. Besides benefitting from the spread of risk, Chinese NOCs are insulated from geological risk and operational risk since the borrower is supplying oil to them. The fact that Chinese NOCs do not participate directly in the production of the oil offered as payment/ guarantee also shields them from most forms of political risk. This is particularly relevant since Chinese NOCs have incurred significant losses due to political risk events in several of the borrowing countries, including Venezuela, Russia, Ecuador and Bolivia. Two exceptions include Brazil and Ghana, where loans are intended less to mitigate political risk events and more to create goodwill in preparation for possible future Chinese NOC business opportunities with these promising oil producers.

As of now, these loans seem to be generally successful, so much so that the CDB provided an additional loan of 6 billion USD to Venezuela's PDVSA in November 2011 (El Universal 2011). Yet these loans might actually not be as safe a bet as Chinese NOCs may think. There remains doubt as to whether borrowers will fulfil their long-term commitments, especially since governments will probably change over the 15- to 20-year duration of the loans. The CDB is aware of this risk but it is apparently confident in its experience overseas (since 2005) and the knowledge and relationships developed by its teams, scattered across 141 countries. It is also engaging governments such as Venezuela's, insisting on stricter accountability regarding how its loans are used to mitigate the risk that the post-Chávez government will renege on the loan (Downs 2011). As this latter approach suggests, the CDB's international risk management skills are somewhat unsophisticated as compared to international best practices. This lack of sophistication (albeit unsurprising in view of the CDB's limited international experience and the breakneck pace of overseas lending – the Financial Times estimates that the CDB and China Exim Bank signed loans of at least 110 billion USD in 2009 and 2010, 10 billion USD more than the equivalent arms of the World Bank lent between 2008 and 2010) – may prove costly. There are already inklings of possible problems to come. In August 2011, Transneft representatives were quoted as saying that they will repay the 20-year, 10 billion USD loan early to the CDB if they need to take legal action against CNPC for underpaying for contracted oil supplies (RT 2011). In the end, the decision to use long-term oil and gas supply contracts to minimize risk and maximize access to resources depends upon the risk assessment and management capacity of the parties involved, and the outcome is only as good as the weakest link.

The year 2011 was marked by several major events that attest to the current state of Chinese NOCs’ political risk management capacity. The most recent and perhaps least critical event has been the collapse of CNOOC and Bridas’ (which is half-owned by CNOOC) acquisition of BP's 60 per cent stake in Pan America Energy (PAE), Argentina's second-largest producer of oil and gas. According to BP, the deal was terminated because CNOOC and Bridas were not able to secure the required Argentine anti-trust and Chinese regulatory approvals in time. It is not clear whether Bridas was unable to obtain the permits or chose not to apply in the face of an increasingly unfavourable political environment. On one hand, politicians publicly criticized the 7 billion USD deal because it would allow Bridas to control 100 per cent of PAE, further extending its – and, indirectly, China's – control of Argentina's oil sector. On the other hand, in October Argentine President Cristina Fernández introduced new rules requiring oil firms to repatriate all export receipts (Decree 1722/2011), a move many analysts believe may point to the government's desire to increase its control over the sector. Regardless, the demise of the PAE sale is proof that there are limits to Chinese NOCs using a host firm as a political risk management tool (de la Merced 2011).

In June 2011, CNPC and Canada's Encana decided not to pursue their initial 5.5 billion USD JV based around the Canadian company's Cutbank Ridge gas shale assets. It would have been China's largest North American deal to date. Little detail has been given as to why the deal failed. Political risk may have been an issue since Encana is a major supplier of natural gas to the US, but energy insiders believe that CNPC was too keen on obtaining and migrating shale gas exploration technology to monetize its vast domestic unconventional hydrocarbon resources. This case shows that pursuing stakes in projects operated by IOCs might be a good way to access technology and resources without attracting too much political attention, but deployment is difficult (Anonymous 2; Reuters 2011a; Krugel 2011).

The year 2011 was not an easy one for CNPC, which also had to deal with severe disruptions in its operations in Libya. Having operated in that country since 2002, CNPC partnered with Libya's NOC to build hundreds of miles of pipeline and explore for oil and gas offshore. CNPC's strong relationship with the regime became a source of vulnerability when the “Arab Spring” erupted. Members of the Libyan opposition attacked Chinese workers and infrastructure projects, forcing CNPC to halt its operations and evacuate more than one hundred employees in March 2011. As a result of the political instability, Great Wall Drilling Co., a wholly owned subsidiary of CNPC, cancelled several projects in Libya in August 2011. While the fighting persisted, China eventually engaged both sides, hosting and meeting with opposition leaders and representatives for Qaddafi in Beijing. After Qaddafi's death, opposition leaders declared that they would honour all legal contracts made during the Qaddafi regime, but some have suggested that China and Russia could face some retaliation for their lack of support for the opposition. CNPC's future in Libya is difficult to predict under the current circumstances. This incident has shown that direct association with ruling dictators has serious downsides, particularly in the long term. It also highlights the importance of home-state support, particularly when the backing offered is vigorous yet able to adapt to a volatile environment (Pierson 2011; China Daily 2011; Xinhua 2011b; Ide 2011).

The flexibility demonstrated in Libya by the Chinese government was also apparent in Sudan. As South Sudan's independence became inevitable, China began laying the groundwork to build a relationship with Juba – where the majority of the oil reserves lie – while maintaining its ties with Khartoum. Since South Sudan's independence in July 2011, the Chinese government has been very active. All of this engagement has insulated CNPC, Sudan's largest oil producer, from any political risk that might have arisen from the change in government. Nevertheless, CNPC remains vulnerable to possible (and perhaps inevitable) fighting between Sudan and South Sudan and to civil war within South Sudan (The China Post 2011; Madhani 2011).

By the end of 2011 it was clear that Chinese NOCs had made significant progress over the last 19 years in terms of adapting and strengthening their ability to manage political risk effectively. Like other NOCs and IOCs, Chinese NOCs are still exposed to many risks that cannot be anticipated or easily mitigated, like terrorism or geopolitical shifts. Chinese NOCs, however, also have to deal with an overhang of political risk assumed during their initial, unsophisticated approach to risk management, causing over-exposure to unstable investment environments such as Sudan and Venezuela.

Conclusion

Political risk is only one of many factors contributing to the constantly evolving nature of the world, but as the recent EU crisis has shown, if money makes the world go round, politics can make it stop in its tracks. All sectors of human activity are affected by politics in some shape or form; because of its omnipresence, there is no single formula for understanding or managing its impact. The current paper looked at one industry's take on political risk – namely, how the oil and gas industry defines and mitigates it. More specifically, the paper focused on how oil industry latecomers, specifically Chinese NOCs, deal with political risk.

Chinese NOCs’ trials and tribulations over the last 19 years attest to the importance of political risk management in the success of overseas ventures. Recent developments suggest that Chinese NOCs are learning from their early mistakes and adjusting their strategies accordingly. In terms of political risk management, Chinese NOCs greatly expanded their toolkit, which now includes, among other things, investment protection treaties, social accommodation, networks of interdependence and home-state support. Still, access to more tools is a necessary but insufficient condition for success in political risk management. To be successful, a company needs to have experience and the capacity to know when and which of the available instruments or combination thereof needs to be applied. This is why Chinese NOCs have opted to essentially delegate their political risk management to IOCs through M&A, and to the CDB/ Exim Bank through long-term supply contracts. Although IOCs are good at managing risk, at least compared with other companies and institutions, the CDB and Exim Bank have almost as little experience overseas as Chinese NOCs. By delegating, Chinese NOCs risk exchanging one evil for another. Chinese NOCs will only be truly masters of their fate (although they will still face risks) if and when they develop their own political risk management capabilities. Success will not come easy; it will require a dynamic worldview, one that considers different information sources and at the same time remains able to question assumptions and biases. It also requires flexibility and, most important of all, resilience. Chinese NOCs have proven to have the latter but seem to lack the former in terms of making the structural changes in behaviour that are necessary to deal with on-the-ground realities much more unstable than their own.