Abstract

Despite the large-scale investments of both China and the EU in climate-change mitigation and renewable-energy promotion, the prevailing view on China–EU relations is one of conflict rather than cooperation. In order to evaluate the prospects of cooperation between China and the EU in these policy fields, empirical research has to go beyond simplistic narratives. This paper suggests a conceptual apparatus that will help researchers better understand the complexities of the real world. The relevant actors operate at different levels and in the public and private sectors. The main message of the paper is that combining the multilevel governance and value-chain approaches helps clarify the multiple relationships between these actors.

Keywords

Introduction

The prevailing view on China and the European Union (EU) in the fields of climate-change mitigation and renewable-energies promotion is one of conflictive rather than cooperative relations. Recent rows between the Chinese government and the European Commission over the support of renewable-energy industries (Kanter 2012) demonstrate the fact that climate and renewable-energy policies are also viewed through the lens of industrial policy rather than just environmental policy. Both the EU and China are making significant investments in renewable energies – not only to mitigate climate change but also to increase energy security and to promote national renewable-energy industries. While the policy goals of mitigating climate change and increasing energy security are leading to an alignment of interests among public and private actors at the national levels in China and the EU, enhancing the competitiveness of national renewable-energy industries could lead to conflicts at the international level.

Our main argument in this article 1 is that in order to evaluate the prospects of cooperation (as well as conflict) between China and the EU in the fields of climate-change mitigation and renewable-energy promotion, empirical research has to go beyond simplistic pictures. In order to investigate the complexities of the relationships between China and the EU, this article presents a conceptual apparatus that helps to identify where we can expect cooperation, conflict or competition. The relevant actors in the field of climate policy and renewable energy operate at different levels and in the public and private sectors. Combining the multilevel governance (MLG) approach and the global value-chain (GVC) approaches can help us better understand those interactions.

The paper is structured as follows: The next section explains why understanding relations between Europe and China is so important for the “low carbon” debate. We will then introduce the GVC and the MLG approaches and explain why a combination of them is especially promising from a conceptual point of view. The following section highlights how this conceptual framework might be used to analyse governance processes in the climate and renewable-energy sectors in China and the EU.

The authors would like to thank the German Ministry for Research and Education, the British Academy, and the Chinese Academy of Social Sciences for generously supporting the work on this paper through the European ERA-NET “Co-Reach” project entitled “The Impact of Emerging Power: China–EU Cooperation and Global Governance”. Furthermore, we would like to thank Matthew Lockwood, Dirk Messner, the anonymous reviewers, and the editorial team of the Journal of Current Chinese Affairs for their helpful comments.

Europe, China and Low-Carbon Development

In the face of the global challenge to mitigate climate change, transitioning to low-carbon development is imperative. Without reducing greenhouse gas emissions, the world is likely to experience “dangerous” climate change that can potentially lead to large-scale disruptions of natural, economic and social systems (Lenton et al. 2008). This threat is being taken seriously in the EU and in China. Both the EU and China are committed to substantially reducing emissions, though China has so far rejected binding international targets. Both China and the EU are key players in the development and deployment of renewable energies such as wind and solar photovoltaic (PV) power.

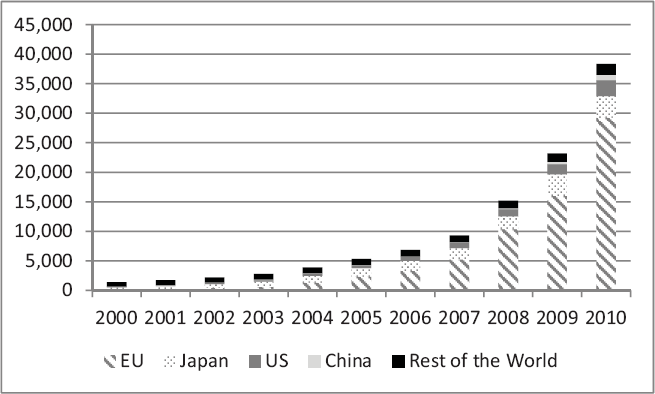

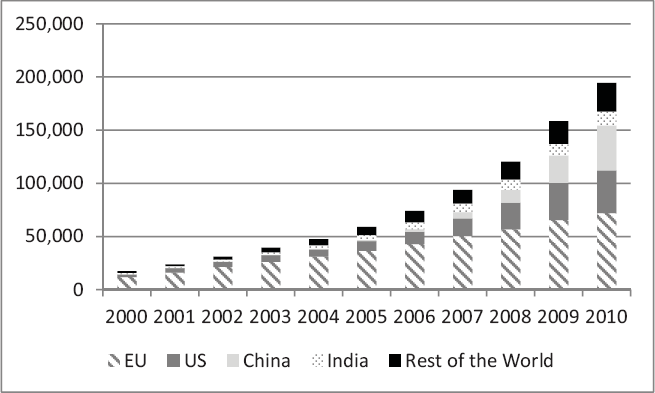

The concept of low-carbon development has been widely adopted due to the recognition that new, climate-friendly development pathways are needed worldwide. Low-carbon development means using less carbon for economic growth by, for example, using less energy, switching from fossil fuels to low-carbon energy, and promoting natural carbon sinks (DFID 2009). In addition to ambitious and binding emission-reduction targets, renewable-energy technologies play a key role in achieving low-carbon development. The potential of the exploration of renewable-energy resources is enormous: Solar energy has an estimated potential of 370 Petawatt hours per year (PWh/year); primary biomass has an estimated potential of 315 PWh/year; wind energy has an estimated potential of 96 PWh/year; and hydropower has an estimated potential of 41 PWh/year (WEC 2007). Renewable-energy technology, particularly solar PV and wind, has seen a dramatic increase in terms of the power capacity that has been installed in recent years, particularly in the EU and China (see Figures 1 and 2).

Global Cumulative Installed Solar PV Capacity, 2000–2010 (in MW)

Global Cumulative Installed Wind Capacity, 2000–2010 (in MW)

What China does in terms of climate-change mitigation and low-carbon development matters for the rest of the world. China's heavy reliance on coal and the country's rapid economic growth – which to a large extent is a result of over-investment in heavy industries (Rosen and Houser 2007) – has propelled it into the position of the world's biggest polluter in absolute terms, accounting for more than 22 per cent of global emissions in 2007 (IEA 2011). The proportion of China's energy supply provided by coal in 2009 was 67 per cent; the corresponding figure vis-à-vis the country's electricity supply for that year was 79 per cent (IEA 2012). Nevertheless, despite being the world's largest emitter, China still has low per capita and historic emissions compared with developed countries. It also has to be noted that approximately 23 per cent of Chinese emissions are due to China's industrial exports, which result to a large extent from the EU and the US outsourcing production to China (Watson and Wang 2007).

Whether China's emissions are going to increase or decrease in the future will have a significant impact on global climate change. Although worries about climate change have not been a driving force of China's energy policies until very recently (Richerzhagen and Scholz 2008; Hallding, Han, and Olsson 2009), concerns over energy efficiency and the environmental impacts of energy production have resulted in increasingly ambitious targets for the reduction of carbon dioxide emissions. As part of the autonomous domestic action under the Copenhagen Climate Accord of the United Nations Framework Convention on Climate Change (UNFCCC), China promised to reduce emissions per unit of GDP by 40 to 45 per cent by 2020 compared to the 2005 level and to increase the share of non-fossil fuels in primary energy consumption to approximately 15 per cent by 2020. Shortly after announcing the autonomous action, the latter policy goal was revised upwards to a share of 20 per cent of non-fossil fuels in primary energy consumption by 2020. However, in contrast to the EU, China is hesitant to commit to binding international commitments that would interfere with its national sovereignty (Lewis 2010).

Though China is known as the world's largest polluter, it is also known as the world's champion of the production of low-carbon technologies. The Chinese government today identifies renewable energies and renewable-energy technologies as important building blocks for China's future economic development (12th Five-Year Plan 2011). China is already the world's largest producer of wind turbines and solar panels and it is often suggested that China has the potential to become a provider of affordable renewable-energy technology worldwide. Chinese companies have started moving into African renewable-energy markets, and in 2010 Prime Minister Wen Jiabao announced the construction of 100 Chinese renewable-energy projects in Africa covering solar power, biogas and hydropower facilities (Conrad, Fernandez, and Houshyani 2011). As shown by Lema, Berger and Schmitz (article is part of this issue of JCCA), China's entry into the wind energy industry is reshaping the relationships between the key players in the global market in a major way. As seen in Figure 2, China is increasing its market power in the wind energy industry. This has been closely accompanied and followed by producer power, which has put incumbents under pressure and driven down costs in external markets. China has also caused major disruption and driven down costs in the solar panel industry, but the dynamics are different (Fischer 2012): Here, Chinese firms have managed to build up producer power and take large market shares in Europe without using solar energy as a key means to reduce greenhouse gas emissions domestically (see Figure 1).

Similar to China, the EU and its 27 member countries are major emitters of greenhouse gases (GHG). After China and the US, the EU as an entity is the world's third-largest emitter. Similar to China, most of the economies within the EU member states are heavily dependent on fossil fuels, mainly on oil and natural gas (IEA 2011). At the same time, and in contrast to China, the EU is an active player in global climate governance. The EU and its individual member states – except for Malta and Cyprus – have signed the UNFCCC as Annex 1 countries, thus agreeing to cut emissions and promote technology transfer to less-developed countries (Lema and Lema 2012). Under the Kyoto Protocol, the EU aims to reduce its GHG emissions by 8 per cent compared to 1990 levels. As a follow up to the Copenhagen Accord, the EU pledged to reduce its GHG emissions by 20 per cent by 2020, and by 30 per cent as long as other main actors reduce their GHG emissions to the same degree compared to 1990 levels (UNFCCC 2010). In 2007 the EU set binding targets to reduce emissions by 20 per cent and to increase the share of renewable energies to 20 per cent by 2020. The 2007 European Strategy Energy Technology Plan (SET Plan) advocates for the EU to become carbon neutral by 2050 to tackle climate change, increase energy security, and increase industrial competitiveness based on the promotion of low-carbon energy technologies (EC 2007).

European countries have also been early movers in the field of renewable energies. Some of them have been investing in renewable-energy technology for decades and are technological leaders in the development and deployment of renewable energy. The EU uses the most renewable energy in the world, followed by China (IEA 2011). Wind and solar PV power are particularly important within the EU; key leading countries in wind power are Germany, Spain and Denmark (EWEA 2010). The EU is also a global leader in solar energy – 75 per cent of the world's installed solar PV capacity can be found in the EU, mainly in Germany, Spain and Italy (REN21 2010).

Even though at first sight there are similarities between China's and the EU's goals to reduce the carbon intensity of economic growth, the original rationales of the two entities for investing in low-carbon energy were different. While the initial push in the 1980s and 1990s in European countries can be explained by a growing ecological consciousness, China's turn to green technologies was mainly a function of economic and energy security interests, and to a lesser extent a result of environmental and climate considerations (Lim 2010; Heggelund 2007). This may be explained by China's lower level of development as well as the need of the Chinese government to legitimise itself through high rates of economic growth. However, in the course of the global financial and economic crisis of 2008/ 2009, the EU also identified investing in renewable-energy development as a way to overcome the crisis, create jobs and develop new growth perspectives. China is also increasingly considering the environmental impacts of its growth strategies.

While the positions of China and the EU are converging on environmental issues, we need to recognise that political processes and policy instruments are different. While the EU relies mainly on market mechanisms to reduce emissions and foster renewable energies, China, more often than not, applies command and control instruments. This may be partly explained by the predominance of state-owned companies in the Chinese economy in contrast to the mixture of private and state-owned companies in the EU. China and the EU furthermore differ with respect to the level of centralisation of decision-making processes, at least formally, and the role of civil society organisations in policy-making processes. At the same time, China's decision-making process is different from the EU's decision-making process, which is exemplified by China's Five-Year Plans. These and other differences make it hard to judge the nature of interaction at the international level. The purpose of this article is to suggest a way of dealing with these complexities. Our central proposition is that the MLG and GVC frameworks help to do this. Applying these two approaches shows that the formula that states that “cooperation results from climate-change mitigation efforts, and conflict results from the economic potential of the renewable-energy sectors” is misleading and fails to capture the many different layers of China–EU relations in these areas. These approaches help to delineate the issues and then recompose them in order to draw conclusions.

The Analytical Challenge: Grasping Complexity

This section provides the conceptual framework for an empirical investigation of China–EU relations in the allocation of emission-reduction targets and in the wind and solar PV sectors. The task of specifying where cooperation, competition and conflict are most likely is difficult because the relevant actors are embedded in different economic and political systems. We need to unpack these systems. Dealing with this challenge requires a conceptual framework that recognises that the relevant actors operate at different levels of governance and focuses on actors from both the private and public sectors.

With respect to the first requirement, private and public sector dynamics are insufficiently explained by developments on one level of governance alone. Essentially, politics in China and Europe are a function of decisions taken on various levels. While this argument is well established in the literature on policy-making within the EU, we argue that it is equally important to approach policy-making in China from an MLG perspective. In addition, private sector dynamics, too, are influenced by decisions taken by actors operating on various levels of value chains.

With respect to the second requirement, shifts of productive and innovative capabilities in the wind and solar PV industries are not sufficiently explained by dynamics within the private sector alone. Instead, government-induced demand has been – and still is – important for the development of renewable energies due to high up-front investments and the difference in price compared to electricity produced from fossil fuels (Lewis and Wiser 2007). Furthermore, in contrast to other sectors, governments are supporting renewable energies not only due to economic interests (for instance, employment generation and competitiveness of national companies) but also due to domestic public interests (for example, energy security), and eventually global public interests (for example, climate-change mitigation).

In the subsequent two sections, we will explain that the MLG and GVC approaches together comply with these requirements and are therefore well suited for use in analysing the complexities of the nexus between the climate and renewable energy in China and the EU.

Multi-level Governance Approach

The MLG concept was developed as an analytical tool to understand the development of complex political systems in post-World War II Western Europe – in particular, the formation of the European Union (Piattoni 2010). Based on this differentiation of policy-making, in the EU the term MLG encompasses three analytical dimensions of governance: decision-making that 1) takes place on multiple levels, 2) involves multiple public and private actors, and 3) uses various forms of governance (Bache and Flinders 2004). These three dimensions will be elaborated in the subsequent paragraphs.

The first dimension stresses political processes and structures that connect institutions on a transnational, national and subnational level. These processes and structures cut across the boundaries of specific political constituencies or organisations in order to address and manage interdependencies in political decision-making (Benz 2005). MLG addresses issues that cannot be sufficiently dealt with at a single level of governance. Such multi-level systems result from a division of power and resources among separate territorial or functional organisations. The division of power and competencies may be formal or factual. The crucial criterion for constituting an MLG system is that it coordinates various actors on different levels of governance. Actors on different governance levels interact with one another because their tasks are interrelated.

The second dimension of MLG emphasises the multitude of actors in governance processes. First, various actors are involved in the process of coordination between governmental bodies with sometimes overlapping responsibilities (Hooghe and Marks 2011). Second, governments at whatever level may not be homogenous actors. Different ministries, different political decision-makers, different decision-making bodies, different representatives, etc., may pursue different interests and strategies even if they are formally located at one level of governance. Third, private actors (actors not belonging to formal government bodies) may play an important role in the coordination processes that constitute governance (Pattberg 2004).

The third dimension of MLG refers to the fact that policies are not solely the result of hierarchical and formally structured decision-making and implementation processes, thereby stressing the difference between government and governance. This differentiation mainly results from the acknowledgement of the role of private actors (Richards and Smith 2002; Rosenau and Czempiel 1992). Private actors may

independently [be] engaged in self-regulation, or a regulatory task may have been delegated to them by a public authority, or they may be regulated jointly with a public actor. This interaction may occur across levels (vertically) or across arenas (horizontally) (Heritier 2002: 3).

These characteristics make MLG suitable for analysing both climate policy and renewable-energy policy (Chen and Fischer 2011). In the context of climate-change issues, global governance and MLG help us to conceptualise 1) the processes of climate-change negotiations at the global level, 2) the role of institutions such as the Intergovernmental Panel on Climate Change, and 3) the impact of civil society initiatives (Schreurs 2010). In the context of renewable-energy policies, the application of the MLG approach results from the acknowledgement of the importance of regulation and standards, the significance of coordination among different actors, and the importance of local initiatives (Smith 2006).

While the MLG literature traditionally focused on Western European countries, we argue that it is also a useful analytical tool to analyse and understand policy developments in China. The MLG approach, of course, is also a useful analytical tool to analyse Sino-European relations at the international level. However, we argue that it is necessary to understand the multi-level governance processes within China and the EU before one can analyse China–EU relations on the international level.

As China is a very large country in terms of both territory and population, top-down, autocratic and one-size-fits-all approaches are often not suitable or even feasible. During the early socialist period (before 1978), this problem was mirrored in discussions regarding the complex processes of coordination, implementation and supervision among different ministries at the national, provincial and sub-provincial levels as well as via regional constituencies (Lyons 1987). Producing units were said to face the challenge of serving “multiple step-mothers”, meaning that they received different instructions from line ministries’ local offices responsible to the central government, on one side, and from local planning institutions on the other. Coordination, communication, planning and supervision worked somehow within the vertical and regional systems but not between them, thus creating coordination failure and inefficiency (Fischer 2000).

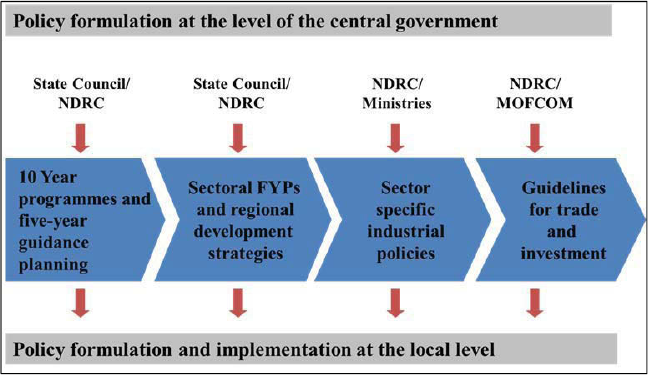

Today, at first glance, policy implementation in China is clearly a top-down process with the central government defining the policy frameworks through national plans, programmes, and legislation (see Figure 3), which are then translated into plans, programmes and rules at the provincial and local levels. However, this process allows for policy variation at the local level, and the strictness of implementation is not uniform. In fact, governance failure in China is often attributed to weak implementation or to actors at the local level outright ignoring policies developed at higher administrative levels.

Policy Formulation in China across Government Levels

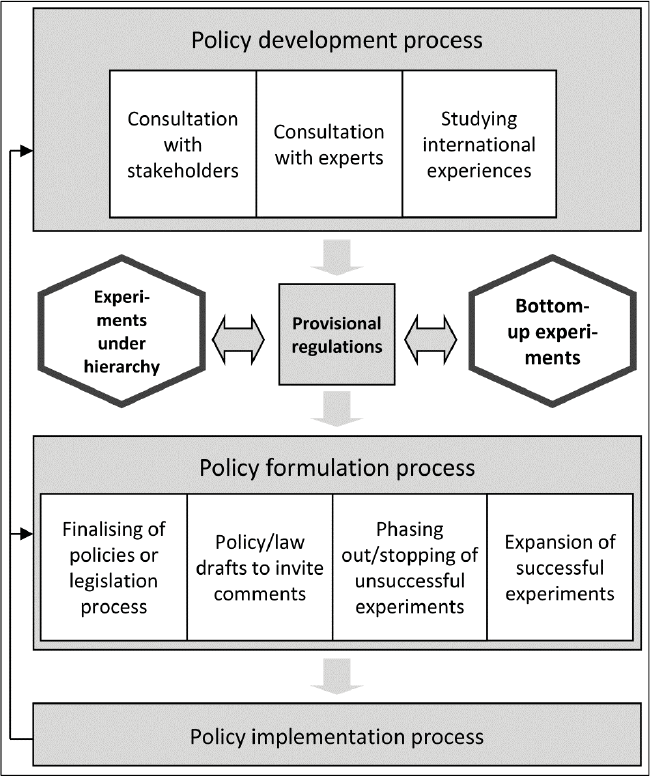

Different from policy implementation, policy development and policy formulation follow a process that is less top-down. In the course of economic reforms, the coordination problem mentioned above was partly aggravated by the deliberate decentralisation of policy-making and implementation that took place during the 1980s and early 1990s. During this early period of reform, provinces gained considerable economic decision-making autonomy, and fiscal income generation capacities also shifted toward the provinces (Wong 2000). As a result, central government decision-making today goes hand in hand with a myriad of preceding consultations and lobbying involving actors from lower levels of government as well as the business sector (Kennedy 2008; Huang 2006). In fact, at least in recent decades, the Chinese practice of policy-making has developed processes to actively incorporate the interests and creativity of different regions and actors. The integration of differing interests and experiences has become crucial in the way learning and consultation is organised before and during policy formulation and in the way policies are tested through “experimentation under hierarchy” and finally implemented at the local level (see Figure 4) (Heilmann 2008; Fischer 2000). The analytical power of this approach is demonstrated in the study of local energy efficiency policy implementation in China. Progress resulted from bridging the gap between national priorities and local interests (Kostka and Hobbs 2012).

Policy Learning Process in China

In fact, learning and consultation, experimentation and implementation can be seen as the major elements of a Chinese policy-making cycle (Rodrik 2008). Wang (2009) argues that China's politicians have been eager to learn from “bottom-up” experiences (practices) – local or “grass-roots” developments that emerged without explicit input from higher governance levels – as well as from the experiences of other countries. In this context, he stresses the growing role of policy advocates (government agencies, local governments, international organisations, and domestic as well as foreign academic institutions) in the learning processes, and addresses the importance of the development of experiments and – consequently – policy processes.

This general conceptualisation of policy-making and implementation in China is also applicable to the Chinese wind and solar PV sector and the burden-sharing system of emission reductions. First of all, the technical and geophysical conditions for energy production from renewable energies differ considerably from one region to the other as does their endowment with traditional fossil fuel resources; hence, provinces have different interests with regard to the promotion of their specific industries and are facing different cost–benefit ratios in terms of emissions reductions. It is, therefore, essential to come from a multi-level understanding of policy-making and implementation in China to grasp these differences between provinces. Furthermore, in the case of wind and solar PV energy industries it is necessary to systematically trace the public–private nexus as there is a clear relationship between political support and the success of national renewable-energy industries (Lewis and Wiser 2007). This general observation is even more relevant in the case of China, where considerable shares of producers of wind and solar PV technologies – and operators – are state-owned.

Global Value-Chain Approach

The GVC approach builds on Porter's (1985) attempt to understand competitive advantages of companies. From a business management perspective, he argued for disaggregating corporate structures into different activities like design, production, marketing and distribution – the value chain – in order to understand their cost structure and competitive advantages. The GVC approach goes beyond Porter in three important respects: First, it is centrally concerned with value chains in which activities are divided between different firms. Second, it deals explicitly with relationships between firms in different countries, hence the term “global value chain”. The approach seeks to analyse how firms in different countries occupy different positions in the chain, thereby creating an international division of labour. Third, the approach does not merely map the chains, but also seeks to understand the uneven relationships between firms in the chain and is particularly concerned with the role of the lead firms in governing the chain (Gereffi 1999).

The GVC approach thus emphasises that the relationship between firms within and between countries can be organised in different ways, with different types and degrees of outsourcing and chain coordination. These relations often extend far beyond pure market transactions (Messner 2002). Accordingly, GVC research does not aim to merely describe which products or services are produced where and by whom – instead, the focus lies on governance structures: “A chain without governance would just be a string of market relations” (Humphrey and Schmitz 2002: 4).

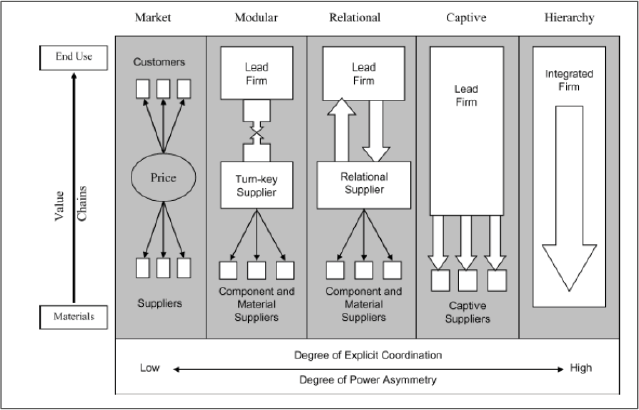

Gereffi, Humphrey, and Sturgeon (2005) identified a range of value-chain governance forms. Two of these are well described in economics and business studies. First, value-chain coordination can be left entirely to the market. Buyers and suppliers do not have a close relationship with one another, and switching costs are low for both buyers and suppliers. Coordination is largely a result of prices in spot markets. Second, chain coordination can be internalised in firm hierarchies. This is the case of value chains that span headquarters and subsidiaries of multinational corporations (MNCs). Such MNCs are becoming increasingly important in renewable-energy industries as markets become global.

Much GVC research has focused on two governance forms in the grey area between markets and hierarchies (see Figure 5). In modular value chains, suppliers produce in accordance to a buyer's product specifications but take full responsibility for the production process. Typically, this type of governance arises in industries where the information regarding product specifications is easy to codify and can be exchanged with little explicit coordination. As we discuss later on in the paper, such modes have been observed in China in both the solar and wind power industries. Relational value chains are characterised by complex relationships between buyers and highly competent suppliers. In the case of this type of value chain, it is difficult to codify product specifications, transactions are complex, and the required capabilities of suppliers are high. The costs of switching to other partners are high because of sunk costs arising from prior investment in relationships. This type of governance has tended to underpin commercial relations between assemblers and component suppliers in the European wind industry.

Types of Governance in Global Value Chains

Understanding chain governance is important because lead firms define the barriers of entry for other companies into different segments of the value chain and consequently determine the returns that actors are able to draw from particular activities. In this way, the main analytical focus of GVC research is on the role of lead firms as drivers of economic activities in a particular industry. The governance structures of various industry value chains have been analysed in different sectors as diverse as apparel, automotive, electronics, furniture and software (Gereffi 1999; Lema, Quadros, and Schmitz 2012; Navas-Alemán 2011; Sturgeon 2002; Sturgeon, Van Biesebroeck, and Gereffi 2008), where lead firms are in most cases large retailers, assemblers and brand-name companies. These studies have shown that global leading firms often have the leverage to structure their relationships with upstream and downstream corporate actors in order to sustain their position in relation to current and new competitors. They also show that competitiveness often depends on supply base characteristics of individual value chains. It is no longer just lead firms that operate globally. In many industries, multinational suppliers are capable of supporting lead firms in distinct markets across the globe (Sturgeon, Humphrey, and Gereffi 2011). Lead firms may have shared supply bases for particular components or services, while for others they may have separate supply bases.

Such chain characteristics are critical determinants of the relative competitiveness of different lead firms. The literature has shown that distinct national models of chain organisation have emerged and that these models influence key sources of competitive advantage (Sturgeon 2002). For example, Fujita (2010) argued that a Chinese value-chain model gained advantages over its Japanese counterparts in the motorbike industry. By using licences for outdated motorbike designs, Chinese assemblers were able to make motorbikes comprised largely of standardised components. The use of such standard components increased price competition in the supply base and this gave them cost advantages that enabled them to take substantial market shares from the Japanese in Southeast Asian markets. A very similar model of competitiveness can be observed in the wind turbine industry (Lema et al. 2011).

One of the distinctive features of the value-chain approach is its focus on how chains evolve over time and what the consequences are. While such changes have multiple sources, two factors have received particular attention: First, the chains are shaped by the location of leading markets (Kaplinsky, Terheggen, and Tijaja 2010). Many sectors have experienced declining demand from OECD countries and increasing demand from large emerging economies such as China, India and Brazil. This alters the role and nature of product and process standards and it changes (negatively) the upgrading prospects for many suppliers that compete with firms in the rapidly growing emerging economy supply bases (Kaplinsky, Terheggen, and Tijaja 2010). Such trends can be observed in a range of green technology industries in which the markets have shifted to China. Second, suppliers in individual chains may acquire new capabilities and address new markets or market segments. This changes the power relations in the chains as new lead firms emerge among them (Schmitz 2007). This is what happened in the Chinese solar industry, where component suppliers upgraded to assemble entire PV panels for export markets such as Germany.

To sum up, the GVC concept offers a useful analytical framework that emphasises the importance of various forms of private governance in global industries. Yet, most of the available studies on the Chinese and global wind and solar PV sectors build implicitly on Porter's concept, analysing “production” value chains in these sectors (e.g. Kirkegaard, Hanemann, and Weischer 2009; Kirkegaard et al. 2010). These studies map the different stages of the value-adding process: the upstream segment of the value chain (for example, provision of key material inputs), the actual production of the wind turbines and solar panels, and the downstream segment (for instance, marketing, deployment, maintenance). These studies show what is produced, who produces it, and how much value addition is linked to each of the different segments. However, the studies lack a focus on governance structures. Understanding these governance structures is essential to being able to comprehend the sources of relative competitive advantages and the possible opportunities for cooperation between different value-chain actors. In fact, the GVC approach suggests that international competition in one part of the chain can coexist with cooperation in other parts of the chain. This in turn is essential for our purposes because Chinese wind and solar PV producers seek to compete globally and are integrating into global value chains in which European companies have hitherto played the major roles.

The Value Added by a Multidimensional Framework

We argued above that there are no easy answers to the question of how relations between China and the EU will proceed regarding climate and renewable-energy issues. Views range from predominantly conflictual relations to scenarios of a “triple-win”, in which relationships are beneficial to the global climate, China, and the EU. We have argued that understanding the prospects for cooperation, competition or conflict requires distinguishing between actors at different levels of governance in China and Europe and including public and corporate actors (lead firms and suppliers of specific technologies). We need to distil the multi-level governance systems on both the Chinese and European sides because different actors have different interests and time frames. It is also necessary when making an analysis to take into account the possibility that certain groups of Chinese and European actors might cooperate, or that conflicts within China or Europe might develop.

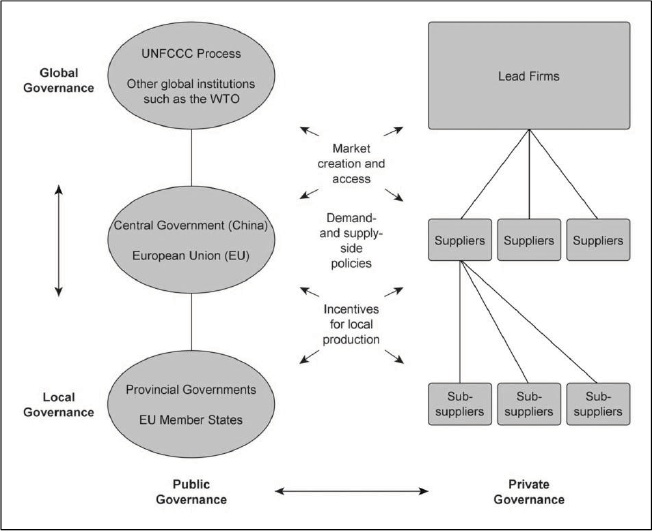

Figure 6 shows an integrated governance perspective that brings together the key elements of the approaches discussed in the preceding section. The key is to view public and private governance in conjunction and to take into account the multiple geographical scales of governance, ranging from local to global governance. We are not claiming that this figure captures all actors, but it does include the most important actors.

Integrated Perspective on MLG and GVC in the Renewable Energy Sector

The MLG approach is a useful analytical tool, especially in the context of the Chinese and European climate policy as it takes a multi-actor perspective and comprehends politics as a multi-level game. Chen and Fischer (2011) apply the MLG approach to show that the potential for conflict and cooperation varies between different levels. Starting with the global level, China and the EU hold antagonistic positions in the context of the UNFCCC when it comes to issues such as burden-sharing, historical responsibilities, or measurement, reporting and verification (MRV). In contrast, at the national and subnational level, actors face similar issues and undergo similar learning curves in both the EU and China, providing greater potential for cooperation. Fischer and Chen suggest that this potential for cooperation and common policy learning at the national and subnational levels can have positive spill-over effects on the international climate negotiations.

The MLG approach also helps us to understand the impact of decisions in the fields of climate and renewable-energy policy taken by public actors on various levels on behalf of corporate actors. The case made by businesses for investing in renewable energies depends to a large extent on the demand created by government regulations and market entry conditions. Here a combination of the MLG and GVC approaches is useful due to the influence of public actors on the design of institutions – defined as the “rules of the game” (North 1990) in the form of formal laws and regulations and informal actions – that influence business relations and industrial location. On the other hand, the negotiations in the context of the UNFCCC cannot be isolated from corporate sector developments. The main example in this respect is the recurring calls for transfer of low-carbon technologies as a means to support mitigation efforts in developing countries. The prospects for cooperation in the international climate regime, therefore, depend on the willingness of private companies to transfer technology to developing countries.

In this respect, Lema, Berger, Schmitz and Song (2011) show that the changing global market shares in wind turbine manufacturing are largely an effect of Chinese government policy. Within the Chinese market, tensions have increased since the creation of a “dual market structure” for wind power projects, in which the Chinese firms have tended to get preferential access to supplying large government-led projects. With the absence of mutually binding rules on public procurement within the WTO, such potential sources of conflict will linger. Governments therefore have a major role to play in securing mutually beneficial relationships for the future.

A weakness of the MLG approach is that it does not account for the governance structures within and among the business actors involved. The nature of the relationships within and among private actors is not considered in a purely MLG analysis. The GVC perspective helps to overcome this deficiency: It takes into account the interests of private actors, these interests being dependent on their technological capacities and the industry segment in which the actors are operating. By opening the black box of the private sector, it becomes possible to grasp the potential for cooperation, competition and conflict.

This analytical potential has been utilised by Lema, Berger, Schmitz and Song (2011). On the one hand, the shift of market demand and production capacity from Europe to China results in an increased competition among Chinese and European lead firms in the Chinese market. However, by dissecting the value-chain perspective, it is possible to show how changes within these firms may lead to new areas of increased cooperation. Based on their analysis of GVCs, Lema, Berger, Schmitz and Song (2011) describe new areas of collaborative relationships that are emerging and increasing with the globalisation and maturity of the industry. As competition among leading firms is increasing, new cooperative relationships are emerging. As shown by the authors, Chinese and European actors that occupy different positions in the value chain are increasingly likely to join forces in future wind power projects. Hence, they identify cooperative competition as a likely scenario for the future relationship between the EU and China in this industry.

The importance of linking the MLG perspective with the GVC perspective is additionally highlighted by developments in the Chinese PV energy sector as presented by Fischer (2012). As in the wind energy sector, China has emerged as the new leader (replacing the EU) in producing solar PV equipment. However, in contrast to the wind sector, in which Chinese manufacturers still predominantly produce for the Chinese market, the Chinese PV sector has emerged on the basis of policy support for solar-energy deployment schemes outside China, mainly in Europe. The development of China's PV sector originated from the production of PV cells and modules. By focusing on cells and modules, enterprises concentrated on the segments of the PV energy technology value chain where they had competitive advantages due to low labour costs, economies of scale, and the comparatively weak environmental standards applied to production processes in China. Government support for these activities was driven by local considerations and was similar to support given by local government to other export-oriented industries. Support schemes for the use and deployment of PV energy technology in China evolved only in the context of the global financial crisis when export-oriented producers of PV cells and modules faced serious risks. However, evolving support schemes at the national level left considerable leeway for local governments to decide on additional support. As Li and Wang (2011) show, these local support schemes vary considerably depending on the characteristics of the local PV sector development and characteristics as well as the potential of PV energy use in different geographic regions.

Overall, the development of the Chinese PV sector has been facilitated by the geographic mobility of solar panel production and the modularisation of the value chain. Hence, when the central government started to support PV energy use in China in 2009, the Chinese PV industry was already a fierce competitor in global markets. While European companies need to cooperate with Chinese partners in order to develop price competitiveness and gain access to the potentially large but fragmented Chinese market, cooperation with European partners can be interesting for Chinese enterprises where the latter can seek access to specific knowledge or pursue potential allies in their fierce struggle with competitors from within China.

Conclusion

China and the European Union are key actors in the global attempt to mitigate climate change. Both rank among the major emitters of greenhouse gases, but more importantly, both are also key actors in the provision of renewable-energy technologies such as solar PV panels and wind turbines, and both are investing in the development of biomass technology.

Due to the commercial interests on both sides, climate-change mitigation is being viewed by Chinese and European governments as a matter of industrial policy – not (just) environmental policy. This is why conflictive rather than cooperative relations are often thought to dominate. Although there is no shortage of contentious issues in Sino-EU relations in this respect, our research highlights the need to go beyond “headline rhetoric” to find sound ways of assessing the potential for future cooperation leading to mutual benefits.

For this purpose, our article provides a multidimensional framework for analysing the prospects for cooperation, competition and conflict between China and EU. Our main argument is that the notion of conflict more often than not arises from a simplistic understanding of policies and industry actors. We argue that a multidimensional framework is necessary because climate and renewable-energy relations between China and the EU take place on different levels involving various private and public actors. Furthermore, we argue that a more differentiated look on governance, industry development and innovation dynamics increases the potential for cooperation, for policy learning, and for a more positive assessment of competition.

By investigating the contents of the black box of Sino-European climate and renewable-energy relations, it is possible to address both conflictive and cooperative patterns. We show that the perception of cooperative versus conflictive relationships differs among the actors involved. However, the main differences in actor perceptions are not between China and the EU but between positions in the value chain and in the governance systems on both sides.

We provide an analytical framework that takes the complexities of climate and renewable-energy policy-making in both China and the EU into account. The MLG approach was developed to analyse intra-EU policy-making and has been applied in the analysis of global climate negotiations. We argue that China should also be regarded as an MLG system comparable to the EU when it comes to the interdependencies of policy development, formulation and implementation across different levels of governance.

Furthermore, we suggest combining the MLG and the GVC approaches to analyse governance processes in the renewable-energy sectors in China and the EU. While the MLG accounts for interactions of public and private actors, it insufficiently deals with the complexities of governance processes within and among firms. Here, the GVC approach is a useful analytical tool as it highlights inter- and intra-firm governance beyond the scope of mere market relations.

Cutting through the complexities is essential in order to understand the rapidly changing world. Currently, we observe that competition between the lead firms of the wind and solar PV industries is increasing rapidly, not least as a result of China's increasing production and innovation power. From a global public goods perspective, this development should be welcomed as it drives down the price of renewable-energy technology, supporting the reduction of greenhouse gases. Policy-makers in China and Europe, of course, are concerned about not only the global gains, but also the distribution of gains among nations.

In a rapidly globalising renewable-energy sector, however, it becomes ever more difficult to define the “national content” of a wind turbine or a solar PV panel. Production and innovation in both sectors are increasingly globalised. To mention some examples: The Chinese system of renewable-energy production is entering a new stage where it is increasingly important to improve the quality and reliability of technology. Hence, Chinese lead firms should seek to collaborate with European companies at various stages of the value chain to develop this expertise. To continue the transition to low-carbon energy production, Europe, in its current stage of prolonged economic crisis, is in need of affordable renewable-energy technology. European lead firms, under pressure to reduce costs, should seek to cooperate with Chinese firms and learn from their business and financing models.

Of course, these examples of enhanced cooperation should not suggest that the future will definitely bring about gains for all actors at the various levels of governance. Competition, understood as creative destruction (Schumpeter 1962), inevitably also produces losers. At first sight, the current downturn in the European solar PV industry may serve as an example. However, looking at these developments through our multidimensional analytical lens, we find that the story is more complex and less alarming that many view it. While it is true that European lead firms of the production value chain are losing market shares due to increased competition from Chinese lead firms, European operation and maintenance companies in the downstream segment of the value chain are likely to benefit from the expansion of the market as a result of falling prices for solar PV equipment.

The important message for policy-makers interested in mitigating climate change and promoting renewable-energy industries – and for researchers giving policy advice – is, therefore, not to follow simplistic narratives but to rely on multidimensional analyses of the renewable-energy industries worldwide.