Abstract

The World Bank promotes integration into global value chains as the path towards development. By liberalising their respective national economies, African countries are expected to benefit from economic impulses, with more and more activities beyond resource extraction being relocated to peripheral locations and generating so-called linkages there. This analytical report focuses on the upstream oil and gas sector, showing that Africa’s hydrocarbon-rich countries do not achieve economic progress merely because of being part of global value chains. The reason for this is endogenous obstacles to investment. Services – especially in engineering and logistics – are carried out by South African firms, which bring their own equipment and staff or work in South Africa. The emerging economy therefore benefits from linkages that exploration and extraction of oil and gas in developing countries generate.

Introduction

Following the latest World Development Report, Africa should pursue a liberal economic agenda in order to achieve what the authors of the report temptingly call “development in the age of global value chains.” Integration into global value chains is promoted as the path towards growth and prosperity. It will “create better jobs, and reduce poverty” (World Bank, 2020a: 1). In the World Bank’s thinking, developing countries benefit from tying themselves to nearby leading areas – that is, the relatively large markets of emerging economies such as South Africa. Unlike developing countries, emerging economies feature strong industrial and services sectors. This economic density allows for integrating regions of continental scale into the world economy. Density moreover generates impulses for development at peripheral locations, with more and more segments of value chains being relocated to developing countries. Readers of corresponding World Bank publications are left with the impression that for such processes to happen, developing countries only have to lower distance and division – meaning trade barriers (World Bank, 2009).

This liberal agenda has not, of course, been without criticism. Nonetheless, numerous African states have implemented policies of economic liberalisation so as to facilitate investment and trade. Most prominently, the G20’s Compact with Africa (CwA) aims at promoting private investment across the continent. Although the CwA acknowledges that African countries have to increase their attractiveness to private investors by improving domestic business, financing, and macro-economic frameworks, little is said about the corresponding reforms. 1 In this analytical report, I show that mere integration into global value chains is not enough to trigger development. African countries suffer from numerous endogenous obstacles that hamper investment, diverting activities that generate more value than resource extraction to places that interlink the continent globally, especially to South Africa. My analysis focuses on the upstream oil and gas sector, which includes searching for resources, drilling wells, and operating these wells. Compared with processing and storing oil and gas, upstream activities are much more likely to happen in resource-abundant countries because of the apparent need for physical proximity. Proving the relating expectations on development wrong would be a clear falsification of hopes of growth and prosperity through integration into global value chains.

The empirical insights presented below rest on indexes that describe the respective business environments of African countries and fifteen interviews with key stakeholders. I conducted the interviews with the help of a guideline of eight questions, modified slightly before each interview, reflecting on the interviewee’s area of expertise and the exact nature of his/her company. The interviews were recorded and later structured along topics such as inter-firm relations, intra-firm division of labour, location strategy, and, most importantly, obstacles to doing business in Africa.

The analytical report consists of two main sections. First, I discuss the widely used concept of linkages and the relating role of gateways – the latter being spatial intermediaries in global value chains, for example cities that interlink peripheral sites globally. They are the academic backdrop to the policy debates driven by the CwA and World Bank, and reveal causal mechanisms of development in global value chains as well as obstacles to such processes. Second, I analyse challenges faced by South African firms involved in oil and gas projects all over the continent, showing how they adapt their business strategies and how this reduces the prospects of development in resource-rich countries.

Economic Development Through Linkages and the Impact of Gateways

While the World Development Reports do not go into details regarding causal mechanisms that explain why integration into global value chains triggers economic dynamics in developing countries, publications by the Policy Research in International Services and Manufacturing (PRISM) unit at the University of Cape Town shed light on this critical issue. They also call the scepticism on resource-based development that results from the vast resource curse literature into question, hence offering a far less pessimistic reading of a topic that is essential for many African countries.

The basic idea behind PRISM research is that increasing competition due to globalisation incentivises firms to outsource non-core activities to low-cost suppliers, usually located in countries that specialise in capabilities instead of wholly manufactured products (Kaplinsky and Morris, 2001; Sturgeon and Memedovic, 2010). Developing countries may, therefore, participate in global value chains without necessarily setting up entire industries. They focus on a narrow range of activities, broadening them at a later stage, once they have successfully plugged into the corresponding value chains (Kaplinsky and Morris, 2016). Extractive industries have adapted to this pattern, and particularly in Africa, it makes sense for lead firms from overseas to contract suppliers in close proximity to the site of operation because of challenges with customs clearance and in-country transport. The optimistic notion advanced by Morris et al. (2012) is that beyond direct effects on local development (growth opportunities for suppliers, job creation etc.), outsourcing to local suppliers or transnational ones with a local presence triggers linkages with the surrounding economy that reinforce themselves:

First, the exploration and extraction of resources require inputs. Extracted resources have to be processed. This creates opportunities for backward and forward production linkages. Related activities such as security, transport, as well as the production and maintenance of equipment – ranging from machinery to clothing for workers – also fall into this category. Second, horizontal linkages are about skills gained in one sector that allow companies to expand into another sector. Bidaurratzaga Aurre and Colom Jaén (2019) add externalities such as new roads built for extractive industries that can be used by everyone and thus reduce transport costs in general. Third, fiscal linkages comprise royalties and taxes on corporate and private income related to extractive industries. The income a state obtains this way can be used to facilitate development in non-extractive sectors or increase national wellbeing through social spending. Fourth, consumption linkages result from income earned in the extractive sector. They boost overall demand for products and services, most apparently through the rising purchasing power of the local labour force.

For all linkages, development is a matter of breadth – the proportion of local inputs – and depth, meaning how thick linkages are in terms of local value added (Morris et al., 2012). In consequence, PRISM researchers find the extent to which African countries benefit from resource extraction to be very different from one case to another. At the one end, South Africa has developed a technologically sophisticated sector for mining equipment and specialist services. The corresponding firms are capable of internationalising their business (Kaplan, 2012). Angola’s oil industry exemplifies the other end, with backward production linkages being limited to labour and, to a lesser degree, generic services (Teka, 2012). Yet, even these basic linkages are vital to the Angolan economy. Case studies on gold mining in Ghana and oil extraction in Nigeria indicate that there are always opportunities for local businesses to integrate into global value chains and benefit this way (Adewuyi and Ademola Oyejide, 2012; Bloch and Owusu, 2012).

Whereas PRISM research deals with economic dynamics in developing countries that have plugged into global value chains, some recent articles analyse the impact of so-called gateways on peripheral development. Readers familiar with peripheral locations across Africa or, more broadly, across the entire Global South will agree that such sites do not integrate directly into the world economy. Intermediate steps are taken – most demonstratively for logistics and transport, but also in terms of industrial processing, corporate control, service provision, and knowledge transmission (Scholvin et al., 2019). Gateways can, hence, be defined as “an entrance into (and necessarily an exit out of) some area” (Burghardt, 1971: 269). They connect, for example, resource-abundant countries to global markets.

Especially in parts of the world marked by economic and political instability, gateways are highly attractive locations for transnational companies because they form islands of stability in seas of unrest (Nijman, 2007). This is not to say that the entire African continent is a sea of unrest or that South Africa does not face important problems of its own. Nonetheless, in particular Cape Town, with its density of skilled engineering firms, and Johannesburg, which is for various reasons the city from where Africa does business, offer locations advantages not available elsewhere on the continent (Scholvin, 2020).

Gateways play a critical role in how developing countries benefit from integrating into global markets. They have been conceptualised as drivers of economic growth – or, using the terminology of the World Bank, leading areas – that transmit impulses to their wider hinterlands. A case study on Cape Town by Scholvin (2017) shows that this city plays such a positive role in spite of certain limitations, which are further investigated in this analytical report. Yet, other scholars – especially Breul and Revilla Diez (2019) as well as Breul et al. (2019) – argue that gateways may also concentrate economic activities to the detriment of subordinate places. The prospects of developing countries are, therefore, reduced to resource extraction and generic services such as catering, security, and transport of personnel. Many of the linkages that PRISM scholars expect to materialise in the periphery rather occur in gateways. Several studies on resource-rich regions as diverse as Antofagasta in Chile and Pilbara in Australia share this negative assessment of how resource peripheries perform in global value chains (Arias et al., 2014; MacKinnon, 2013). 2

While the just-mentioned research is focused on exogenous factors such as economies of scale in gateways, sector-specific entry barriers, and the power wielded by transnational corporations, the following section reveals that endogenous conditions also hamper the extent to which oil and gas-abundant countries benefit from being plugged into global value chains. Challenges to doing business in Africa reinforce the concentration of economic activities in gateways, particularly in South Africa, whereas resource peripheries stagnate.

Challenges to Investment in Resource-Rich Countries and Strategies of South African Firms

The list of African countries that possess oil and gas is long. It begins with established producers that are among the world’s most important hydrocarbon exporters: Algeria, Angola, Libya, and Nigeria. Others – Chad, Equatorial Guinea, Gabon, and South Sudan, for example – possess reserves of smaller quantities. In Ghana, Ivory Coast, Mozambique, Tanzania, Uganda, and other countries, recent discoveries have attracted international investors. They have just begun with extraction or are still evaluating the corresponding commercial viability. Further countries hold prospects of making large-scale findings, most importantly Namibia.

Fewer than a dozen firms worldwide – Baker Hughes, Halliburton, Schlumberger, and the like – perform the most sophisticated tasks that oil field operators such as Chevron, ExxonMobil, and Shell outsource, but these service providers subcontract smaller companies for engineering, logistics, and other activities that range from somewhat sophisticated (e.g. toxic waste disposal and welding) to generic (e.g. catering and transport of personnel). Following the concepts of gateways and leading areas, South African firms can be expected to venture into regional countries, engage with local partners and suppliers, and relocate more and more activities to peripheral locations.

In the following pages, I begin with very basic obstacles to investing, hiring labour, and purchasing inputs in Africa’s hydrocarbon-rich countries. I then elaborate on public safety and challenges that result from legal/regulatory systems. The last paragraphs deal with problems that occur once a branch operation has been established. I furthermore explain how the various difficulties lead to firm strategies that work against consumption, fiscal, horizontal, and production linkages.

Interviews with South African firms involved in service provision to the oil and gas sector revealed numerous obstacles to doing business with and – even more so – operating in other parts of Africa. The owners of a Cape Townian company that provides basic equipment and services to the offshore sector – painting of boats and ropes used on rigs, for instance – said that they were very interested in the Angolan and Mozambican markets, but they abandoned the idea of investing there because of corruption, language barriers, and difficulties in finding a trustworthy local partner. 3 Language barriers were also mentioned with regard to Francophone countries. 4

An interviewee argued that in some countries, especially in Mozambique, “there are no skill-sets.” 5 His firm cannot, therefore, contract local labour, although doing so would be much cheaper than sending South Africans, who must be paid at an expat rate. Another Cape Townian firm flies its staff into other Africa countries to work there on a “regular in-and-out basis,” for example going to a rig once a month during a year. 6 Generalising from these interviews, consumption linkages at peripheral locations do not occur as expected by PRISM scholars because there are few to no local employees. These positive effects concentrate in South Africa.

Further difficulties relate to public services and production inputs. A firm that runs a workshop in Takoradi, Ghana, had to bring its own power generators – obviously at an enormous cost – because “you can’t rely on local electricity. You have to be 100 percent self-sufficient.” 7 For all markets except Ghana and Namibia, this firm carries out prefabrication in South Africa and then sends everything to wherever it is needed, along with staff who handle final assembly on site. A large maritime service provider would like to buy as many inputs as possible in Angola, Ghana, and Tanzania, but, in their experience, these countries lack a sufficiently developed industrial base, which is why the firm obtains most inputs in South Africa and has them delivered to its workshops abroad. 8 Against this backdrop, it appears doubtful that oil and gas-rich countries benefit from production linkages.

When travelling to some African countries, there are problems with public safety. The risk of being kidnapped on the way from the airport to the hotel or workshop is a serious issue in Nigeria. 9 An interviewee, who has been to the West African country on short-term missions, explained that “I will land in Lagos. There will be somebody [that is, a personal protection detail] there to collect me. I will be taken to a hotel and looked after until I go offshore […] Try and do that yourself is a nightmare.” He went on saying that “I would never drive around in Nigeria [on my own]. If there is a problem, you [will] get into so deep shit.” As a consequence, few firms are interested in working in countries like Nigeria because “it’s so difficult, it’s not attractive,” not even from a business point of view. The interviewee’s firm now works in South Africa only. Customers must pick up the equipment they purchase or have international freight forwarders deliver these goods. Payment must be made before any shipment leaves South Africa, which is “sensible when doing business with Nigeria,” as the interviewee stressed. 10

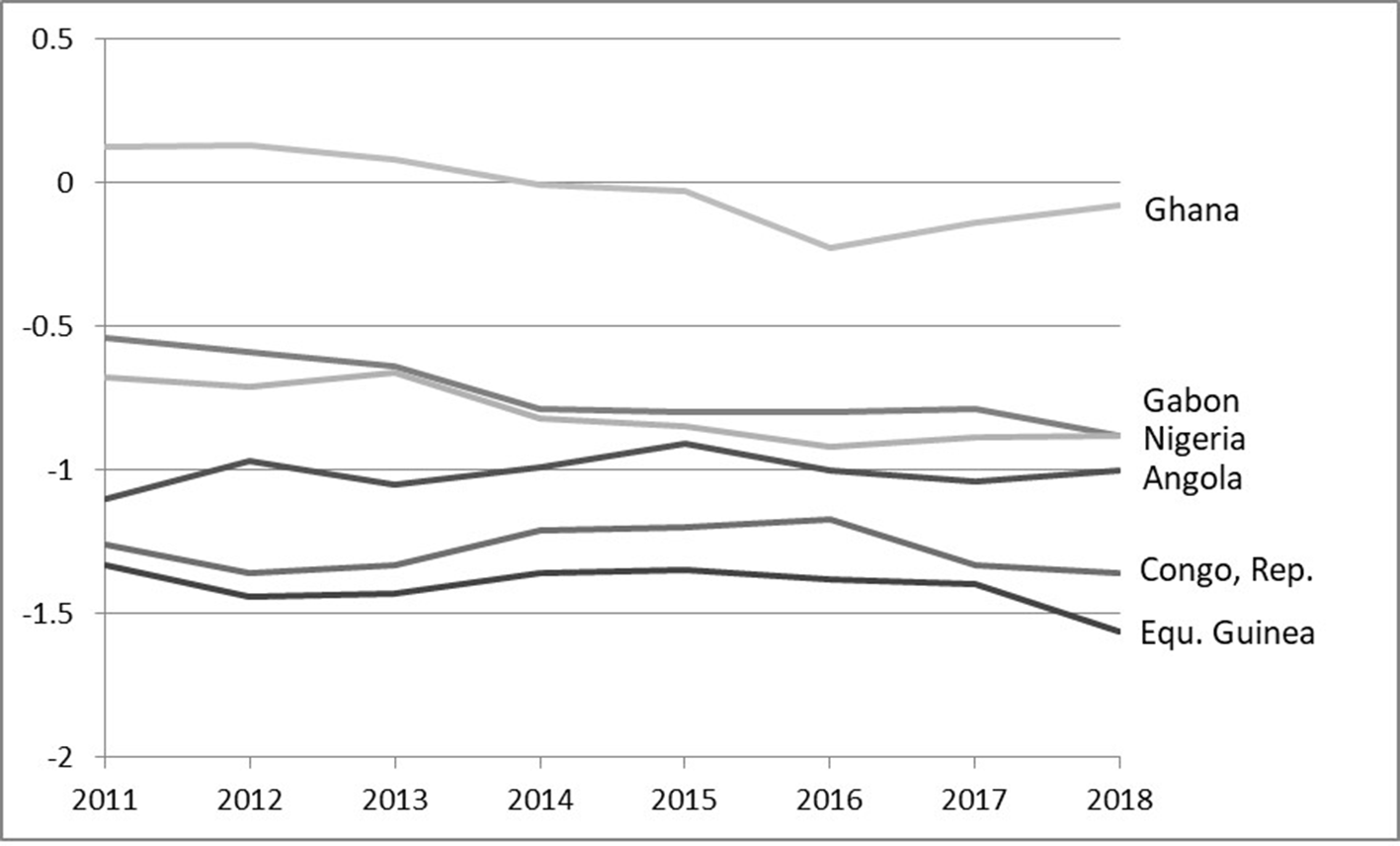

The list of obstacles goes on. Referring to Ghana, which is one of best performers in terms of a functional legal system on the continent, an interviewee explained that “there is an official system and then there is also a bit of unofficial that you have to do […] What they tell you from a legal perspective and what happens on the ground is sometimes slightly different.” 11 This apparently creates uncertainty among potential foreign investors. As Figure 1 shows, the regulatory systems of sub-Saharan Africa’s main hydrocarbon exporters are of poor quality. Equatorial Guinea and the Republic of the Congo are among the worst performers worldwide. Even Ghana does not perform overly well, although the World Bank (2018) rates its government effectiveness much better than that of the other countries from Figure 1. Among the countries that may soon export oil and gas in large quantities, Ivory Coast, Namibia, and Uganda reach values similar to those of Ghana. Mozambique and Tanzania perform worse.

Regulatory Quality of Hydrocarbon Exporters. Source. World Bank (2018). Note. The World Bank rates regulatory quality on a scale from −2.5 (worst) to 2.5 (best).

Some regulations even work against foreign investment. “It’s very difficult to get your money out of Angola, ” the owner of an engineering firm pointed out. 12 They do not operate in that country for this reason. Clients that extract oil in Angola use their respective European business units to pay for engineering work – refitting of boats, for example – that is done in South Africa. A further challenge to investment in Angola is that tremendous up-front transfers into Angolan bank accounts are mandatory in order to register a business there. An interviewee explained that the owners of his firm do not want to put money into Angola, knowing that they may not be able to get it out again. He added that up-front transfers and registration are not a guarantee for obtaining contracts (or being able to carry out the corresponding work). 13 Doing work for the Angolan market in South Africa and being paid into a South African bank account apparently means that fiscal linkages occur in the leading area, not in the resource-rich country.

The Doing Business rankings by the World Bank (2020b) confirm how difficult it is to run a firm in Africa’s oil and gas-rich countries. With the exceptions of Ghana, Ivory Coast, Namibia, and, in some respects, Niger, Tanzania, and Uganda, the continent’s resource-abundant countries are also the worst performers on these rankings (and Africa performs worst by global comparison). In particular, enforcing contracts in Angola, starting a business and paying taxes in Chad, the Republic of the Congo, and Equatorial Guinea, registering property and trading across borders in Nigeria and South Sudan, and protecting minority investors in the latter country could hardly be more difficult.

South African companies that operate permanently or temporarily across the continent face further challenges. To begin with, goods are often stolen at customs. Bribes are necessary “to keep the right people happy” and make customs clearance proceed. 14 “The problem with dealing with [other countries in] Africa […] is that a lot of them [meaning, public employees] expect underhand dealings […] It’s like ‘We’ll get this pump in quicker, but it’s gonna cost you extra, ’” a businessman from Durban explained. 15 An engineer who travels frequently from Cape Town to other African countries added that “it’s impossible to get your stuff there on time.” 16 While it appears that the amounts of money used by South African service providers to bribe people are rather low, 17 corruption at borders causes serious delays, which drives up the costs of doing business. 18 This is particularly problematic in the oil and gas sector, where prices may change tremendously from one day to another, meaning that every day lost at a border stop may decrease revenues significantly.

Once in the country, corruption goes on. An interviewee spoke of “facilitation fees” that government officials in Nigeria demand for each transmission, obviously without providing any sort of receipt. 19 Another interviewee, whose company repairs rigs and ships, has made similar experiences: “Everything you have to pay backhands […] So even if you are there, the risk that you are not going to execute the project on time is huge. Then you rather say [to the client], ‘No, we can’t do it there. Bring your rig down to South Africa’.” 20 Given that operators are aware of these reliability issues, they prefer to have their vessels maintained in South Africa. In addition to the aforementioned drag on consumption, fiscal, and production linkages, such a concentration of business activities in the leading area also works against horizontal linkages in oil and gas-rich countries such as the expansion and rehabilitation of harbours and shipyards.

The Corruption Perceptions Index by Transparency International (2019) confirms that most African countries that possess oil and gas resources suffer from outstandingly high levels of corruption. Reaching values as low as twelve (South Sudan) and sixteen (Equatorial Guinea) on a scale from zero to one hundred, where higher values indicate less corruption, they are among the worst performers worldwide. Angola and Nigeria – by far the largest markets for the upstream sector – both reach a value of twenty-six. Ghana (forty-one) and Namibia (fifty-two) are the only ones that perform relatively well by African standards.

If a South African firm decides to invest in other African countries, it will need a local partner to start a joint venture, which is mandatory by legislation on local content. Yet, there are few local businesspeople and companies that have the managerial and technical expertise necessary to make a contribution to joint ventures in the oil and gas sector. Interviewees argued that “to find a partner that can actually add value, not just having contacts, […] it’s difficult , ” 21 pointing out that “one is being forced […] to hold hands with a local company, even though they can’t really help you to do the job.” 22 A consultant explained that local partners often merely serve the purpose of bribing the right people. 23 Hence, money flows into obscure channels that are unlikely to trigger development.

Conclusion

Being part of global value chains undoubtedly offers considerable opportunities, but this analytical report showed that various endogenous obstacles need to be addressed before African countries can fully benefit from external impulses that the leading area generates, triggering linkages at peripheral sites. Although the oil and gas sector is not, certainly, representative of all value chains that matter to Africa, the obstacles identified above are not sector-specific. Language barriers, the lack of inputs and skilled labour, as well as unreliable public services, and, in some countries, issues with public safety make it difficult – perhaps impossible – to operate in many resource-abundant countries. Legislation that is poorly implemented or sometimes hostile to foreign investment as well as corruption further complicate the situation.

Given such an unfavourable business environment, activities beyond the mere extraction of oil and gas largely happen in South Africa – the gateway, which interlinks the continent globally. South African service providers try to do as much work as possible in their home country, instead of setting up branches abroad. They work rather temporarily than permanently in oil and gas-rich countries, bringing in South African equipment and staff. As a consequence, the linkages that PRISM scholars expect largely concentrate in South Africa, not in Angola, Gabon, Nigeria or any other hydrocarbon-exporting nation – obviously with the exception of the royalties and taxes that Chevron, Shell, and the like pay. This finding ties the analytical report to the resource curse literature, as institutional weaknesses or, in other words, governance problems that stand at the core of this literature (Robinson et al., 2006; Ross, 2012) account for some – but not for all – of the endogenous challenges identified above.

Footnotes

Author’s Note

The research for this analytical report was conducted while the author was employed at the University of Hanover. He now works at the Free University of Berlin.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The field research carried out for this article was financed by the German Research Foundation (Project Number: 275355279).

Notes

Author Biography

E-mail: