Abstract

Experts have shown that anti-corruption actions can improve the quality of public policies. The issue is that we are not certain if this occurs because politicians reduce their involvement in misconduct. Through an experiment informing mayors of their high audit risk, this paper compares incumbents' personal wealth, as corruption is often defined as the misuse of public power for private gain. Results indicate that politicians aware of higher audit risk ended their term with 46 per cent lower private wealth. Simulations confirm statistical significance even if the treatment group hides part of its assets. The evidence strengthens the argument that audit risk awareness demotivates politicians from corruption.

Introduction

It is challenging to determine which policies effectively reduce corruption. The difficulty lies in the fact that corruption can hardly be objectively measured (Donchev and Ujhelyi, 2014; Gutmann et al., 2020; Olken, 2009). Hence, experts have focused on testing how audit programmes can facilitate the punishment of public authorities and improve the quality of public policies (Di Tella and Schargrodsky, 2003; Ferraz and Finan, 2008; Funk and Owen, 2020; Zamboni and Litschig, 2018). The issue is that the risk of punishment and improvements in public policies are not sufficient to conclude that politicians reduce their involvement in misconduct. They may enhance the efficiency of public services to avoid potential electoral backlash arising from the disclosure of corruption. Additionally, incumbents may try to cover their tracks left by misconduct in several ways. 1

This paper aims to fill this gap by comparing the personal wealth of politicians facing different chances of being audited. Corruption is often defined by experts as the misuse of public power for private gain (Pozsgai-Alvarez, 2020; Thompson, 2018). Comparing politicians’ wealth strengthens the argument that audit programmes, besides encouraging the improvement of public services, can indeed be effective in reducing corruption practiced by political authorities.

Incumbents face the risk of being held accountable by voters when they become targets of investigations. In Brazil, natural experiments indicate that mayors with irregularities exposed by an audit programme have lower chances of being re-elected (Ferraz and Finan, 2008), although this effect disappeared after the initial two years of this anti-corruption policy (Rundlett, 2018). Moreover, survey experiments reveal that voters are inclined to punish corrupt politicians when provided with information about misconduct, even when incumbents efficiently deliver public goods (Winters and Weitz-Shapiro, 2013). Although voters might forgive corrupt politicians who increase public spending (Pereira and Melo, 2015), incumbents involved in corruption might face conviction by the justice system (Assumpcao and Trecenti, 2020; Zamboni and Litschig, 2018).

Due to the difficulty of directly measuring corruption, experts have focused on analysing the impact of audits on public policies. The premise is simple: if politicians refrain from diverting resources intended for public policies, the quality of public services will improve. Evidence suggests that costs for medications decreased after audit operations in Argentinean hospitals (Di Tella and Schargrodsky, 2003). Controlled experiments point out that local governments reduce waste in road construction policies in Indonesia (Olken, 2007) and leave their citizens more satisfied with healthcare services in Brazil (Zamboni and Litschig, 2018) when they become aware of the risk of being audited. A well-known audit programme in Brazil, which randomly selects municipalities for inspection, has also encouraged local governments to make improvements in health, education and sanitation policies (Funk and Owen, 2020), and to reduce public spending in the election year as well (Diaz, 2023). 2

However, improving public policies and giving up engaging in corruption are not the same thing. Incumbents may provide efficient policies to compensate for the exposure of irregularities, and even so, continue diverting public resources while they cover their tracks in several ways. Our tests contribute to filling this gap by comparing the personal wealth of Brazilian mayors rather than their policy performance because experts usually conceive of corruption as the illegal use of public power for private gain (Pozsgai-Alvarez, 2020; Thompson, 2018). 3 Personal wealth is not a direct measure of corruption, but if authorities constrained by the inspection risk refrain from corrupt behaviour, this means that they are not going to increase their wealth. Using data from the controlled experiment designed and implemented by the Controladoria Geral da União (CGU, Office of the Comptroller-General), our results suggest that mayors who were informed of having a high probability of being audited accumulate less wealth compared to mayors with low chances of facing audits.

The only experiment that we are aware of, which tests the impact of anti-corruption on future misconduct by directly measuring corruption, use audits actually carried out as treatment (Avis et al., 2018). 4 In contrast, our study deals with a treatment group consisting of incumbents who have been informed via letters about their heightened risk of being audited. This research strategy allows us to contribute to the understanding of whether merely being aware of their risk status is sufficient to influence corruption.

Brazil provides an excellent political environment to test our main hypothesis. With slightly over five thousand municipalities exhibiting significant socioeconomic and public management diversity akin to that found across Latin America, it offers an ideal setting. Furthermore, its political and bureaucratic institutions make a plethora of data readily available in a transparent manner, encompassing audit reports, electoral data and candidates’ personal information. This abundance of data has spurred numerous experts in comparative politics and political economy to test theories that would be challenging to examine in other political contexts (Boas et al., 2019; Ferraz and Finan, 2008; Nichter and Peress, 2017; Zucco, 2013).

The results suggest that mayors informed about their high risk of being audited ended their political term with a lower private wealth than mayors with low audit risk. Additionally, simulations show that the estimated effects maintain their statistical significance even if mayors facing greater audit risk hide part of their assets, personal property and livestock. Indeed, additional tests were performed by excluding municipalities that had actually been audited from both the treatment and control groups in order to isolate the causal effect of an increased risk of being audited from the causal impact of the audit itself. The estimated effects remained statistically significant for total assets, as well as assets that are less visible and more challenging to trace, like personal property and livestock. The results suggest that merely the risk of exposure, without the necessity of an actual audit, curbs incumbent politicians from engaging in corruption.

Compared to previous works that pointed out politicians in power may enhance public policies to circumvent potential electoral consequences arising from audits (Assumpcao and Trecenti, 2020; Olken, 2007; Zamboni and Litschig, 2018), our analysis strengthens the argument that politicians also refrain from engaging in corruption when they become aware of the high risk of an audit, as the incentive to accumulate wealth illegally diminishes. The focus on personal wealth aligns with the widely accepted definition of corruption, which emphasises the misuse of public authority for personal gain (Pozsgai-Alvarez, 2020; Thompson, 2018).

Our findings align with Melo and Pereira (2013), who show that checks and balances and political competition curb state deputies’ wealth accumulation. Their analysis links political oversight to reduced opportunistic behaviour. Similarly, our results indicate that a higher risk of audits reduces politicians’ wealth.

On the other hand, while no significant differences in wealth are observed between elected and non-elected candidates in close elections (Izumi, 2019), when the sample is limited to elected officials, audit risk appears to discourage personal enrichment through corruption. 5 This suggests that audit risk makes holding elected office less financially advantageous than operating in the private sector. 6

The findings have implications that extend beyond the Brazilian context, highlighting how audit mechanisms curb political corruption globally. While grounded in Brazil's context, the core mechanism – how audit risk shapes politicians’ behaviour – are relevant across diverse governance systems. Evidence that audit awareness reduces incumbents’ wealth underscores the universal potential of transparency and accountability. In contexts with strong media and law enforcement (Szakonyi, 2023), the deterrent effect of audits could be amplified. Similarly, in countries like India, where voters link wealth to corruption (Chauchard et al., 2019), audits could complement disclosure systems to strengthen public trust. These results reinforce that raising the perceived risk of detection can discourage corruption across different contexts.

In the next section, we present our argument about the expected behaviour of politicians who face a high risk of inspection. Next, we describe the CGU's audit programme that randomly selected municipalities to be targeted with information regarding their high probability of being audited. The empirical strategy is presented in the “Empirical Strategy” section. The main results in the “Results” section support the argument that mayors aware of their high probability of being audited have accumulated less wealth than mayors with low risk. Finally, we discuss the main implications of our findings for anti-corruption policies and the literature discussing political corruption.

Political Response to Anti-Corruption Programmes

Experts widely agree that corruption has adverse effects on economic growth, inequality and public policies (Fisman and Gatti, 2002; Gingerich, 2013; Gupta et al., 2001; Lambsdorff, 2006; Mauro, 1995; Samphantharak and Malesky, 2008; Shleifer and Vishny, 1993). However, the effectiveness of various solutions to reduce corruption remains ambiguous. While increasing public bureaucracy earnings may deter corrupt practices (Armantier and Boly, 2011; Borcan et al., 2014; Van Rijckeghem and Weder, 2001), it can also inadvertently foster acceptance of bribery (Foltz and Opoku-Agyemang, 2015). Merit-based evaluations for public sector recruitment are often touted as a means to mitigate corruption (Dahlström et al., 2012; Rauch and Evans, 2000), yet political appointments have been shown to enhance public service delivery by establishing closer ties between politicians and bureaucrats (Brollo et al., 2017; Toral, 2024).

On the other hand, monitoring public management is an advocated recommendation by experts to curb corrupt practices and enhance public policies. Few countries around the world have no anti-corruption agency or ombudsman (Mungiu-Pippidi, 2015). Audits have contributed to the exposure and punishment of corrupt governments (Assumpcao and Trecenti, 2020; Ferraz and Finan, 2008; Zamboni and Litschig, 2018), as well as the improvement of the quality of public policies (Di Tella and Schargrodsky, 2003; Funk and Owen, 2020; Zamboni and Litschig, 2018). This occurs because audits release information about malfeasance to voters and judicial actors who can impose costs on corrupt politicians (Banerjee et al., 2018; Cordis and Warren, 2014; Fisman et al., 2016; Reinikka and Svensson, 2005).

Audits alone may not be capable of decreasing the chances of re-election for incumbents. Voters would be encouraged to punish candidates at the polls only when corruption is disclosed by audits and reaches them (Chong et al., 2015; Ferraz and Finan, 2008; Pereira et al., 2009; Weitz-Shapiro and Winters, 2017). Voters are inclined to punish corrupt politicians, even when incumbents efficiently provide public goods (Vera, 2020; Winters and Weitz-Shapiro, 2013). In certain situations, this does not occur. Corrupt politicians often escape punishment despite the exposure of their misdeeds when voters derive benefits from corruption (Chang and Kerr, 2017; Fernández-Vázquez et al., 2016), harbour pre-existing negative opinions about incumbents (Arias et al., 2022), and perceive that challengers are equally corrupt (Pavão, 2018). Nonetheless, the exposure of malfeasance can boost voter turnout (Arias et al., 2022), encompassing potential supporters of challengers. 7 In other words, corrupt politicians can only be punished if social or judicial actors, capable of restraining them through public pressure or legal action, are informed of their illegal use of public resources.

Similarly, merely auditing governments may not necessarily curb them from engaging in corrupt practices. This is because audits reveal misconduct that has already taken place, and so, seldom can reverse them. Audits themselves may have an effect on corrupt behaviour only when they target former governments, which serve as an example to new ones about the costs of being caught (Avis, Ferraz and Finan, 2018). However, there is no reason to expect that audits can reverse corruption that has already been perpetrated by governments.

On the other hand, being aware of the risk of being audited may lead incumbents to give up diverting resources for illicit enrichment to avoid future sanctions. Experimental designs suggest that local governments, when informed of a high probability of being audited, decreased wastage in road construction projects in Indonesia (Olken, 2007) and achieved a high level of approval among users of public health services in Brazil (Zamboni and Litschig, 2018). When incumbents receive information that audit reports will be released before elections, they refrain from engaging in corruption before the audit occurs to avoid facing judgment from the voters (Bobonis et al., 2022). Such behaviour is not limited to politicians, as controlled experiments point out that informing agents of being monitored reduces the acceptance of bribes (Armantier and Boly, 2011). The impact of audit risk on corrupt behaviour is mediated by a mechanism: the fear that the political costs resulting from audits outweigh the benefits of corruption. This fear holds true if three assumptions are valid: if corruption indeed exists, if misconduct can be identified, and if those responsible for irregularities will face electoral and judicial consequences. These three assumptions are consistent with the Brazilian context. First, Brazilian mayors often divert funds. In a randomly selected sample of municipalities, audits have revealed that 78.6 per cent of local governments engaged in at least one corrupt action, with 8 per cent of audited resources being diverted from public funds (Ferraz and Finan, 2011). Among local political representatives, mayors derive the greatest advantages from corruption: 87.8 per cent of local politicians convicted by the Federal Audit Court (TCU) are mayors, while only 13.6 per cent are city councillors. 8

Second, audits in Brazil can uncover misconduct by politicians aimed at private enrichment at the local level. Audit reports frequently reveal that mayors divert funds from education and health programmes to expand their personal wealth, including the acquisition of assets such as cars and apartments (Ferraz and Finan, 2011). While financing electoral campaigns is another possible motive, qualitative evidence indicates that mayors often engage in corruption primarily for personal gain.

For instance, in Paranhos, a municipality in the state of Mato Grosso do Sul, public funds intended for a rural electrification project were partially redirected to benefit a farm owned by the mayor. Similarly, in Itapetinga, a municipality in the state of Bahia, the procurement process for school meals was manipulated by posting bids only an hour before the deadline. This ensured that the sole company able to participate was owned by the mayor's brother, allowing the mayor's family to profit from public resources (Ferraz and Finan, 2011: 1281–1282).

Compatible with the third assumption, audits in Brazil yield significant consequences, including the potential disruption of political careers. Unlike contexts where politicians often go unpunished (P. Lagunes, 2021), in Brazil, voters hold corrupt politicians accountable when instances of government malfeasance are exposed with the help of the media (Ferraz and Finan, 2008), and politicians may face criminal convictions by judicial institutions (Aranha, 2017; Assumpcao and Trecenti, 2020; Zamboni and Litschig, 2018). The consequences generated by anti-corruption institutions are not confined to the municipal level. At the state level, better-developed checks and balances lead to increased public goods provision, as well as a reduction in spending on civil servants and the private wealth of politicians (Melo and Pereira, 2013).

In the Brazilian context, mayors have not been able to sufficiently conceal traces of corruption to avoid being penalised by audits. Hiding embezzled funds in offshore locations or in bank accounts of intermediaries (known as “laranjas” in Brazil) also does not shield corrupt politicians from the costs imposed by audits, as identifying the agents responsible for administrative irregularities and diversion of resources is already sufficient for anti-corruption institutions to impose penalties. Moreover, our results indicate that assets that are less visible and more challenging to trace, such as personal property and livestock (Trevisan et al., 2003), are also impacted by the risk of audit. This suggests that corrupt politicians are deterred from continuing their irregular practices due to the potential detection. 9

Therefore, our hypothesis suggests that incumbents who are aware of the high probability of being audited will be disinclined to pursue personal enrichment through corruption. Persisting in diverting funds under conditions of high audit risk would entail the risk of losing political office, facing sanctions by the criminal justice system, or even ending one's political career. These conditions are not limited to the Brazilian case. As mentioned earlier, audits uncover corruption and impose costs on corrupt politicians in various parts of the world (Banerjee et al., 2018; Bobonis et al., 2022; Chong et al., 2015; Cordis and Warren, 2014; Di Tella and Schargrodsky, 2003; Fisman et al., 2016; Reinikka and Svensson, 2005; Weitz-Shapiro and Winters, 2017).

Our research contributes to the corruption debate in two key ways. Firstly, we have managed to estimate the impact of the audit risk rather than solely focusing on the direct effects of the audit. As outlined in the following section, we used a treatment group composed of randomly selected municipalities informed of their high probability of being audited. This allows us to examine whether incumbents refrain from engaging in corruption upon learning about the audit risk. Thus, our approach differs from the methodology proposed by Olken (2007), in which all informed local governments designated for audits were indeed audited.

Secondly, our evidence further supports the notion that politicians respond to the audit risk by refraining from involvement in corruption. Although incumbents may improve public policies as a way to offset potential voter backlash caused by corruption or attempt to cover up the traces left by corruption, our study shows that they accumulate less wealth once they become aware of the higher probability of being audited. This outcome aligns with the concept of corruption commonly used by experts, which highlights the misuse of public authority for personal gain 10 (Pozsgai-Alvarez, 2020; Thompson, 2018).

Institutional Context

The Programa de Fiscalização por Sorteios Públicos

Anecdotal and cross-sectional evidence suggests that corruption is rampant in developing countries (Mauro, 1995; Olken and Pande, 2012; Svensson, 2005). In response to this problem, many countries have turned to external audits to monitor public accounts and the behaviour of politicians. Empirical evidence indicates that these programmes are effective in combating the misappropriation of public resources (Di Tella and Schargrodsky, 2003; Olken, 2007).

The case of Brazil is no exception. In 2003, by Law 10,683/2003, the federal government established the Controladoria Geral da União (CGU) 11 to combat corruption. The CGU is a typical anti-corruption agency that assists the federal government in matters related to the defence of public assets, transparency in management, internal control activities, public audits, correction, prevention and combating corruption. Essentially, it centralises the government's activities in the fight against corruption. According to Bersch et al. (2017), the CGU is one of the most autonomous and least politicised government agencies in Brazil.

Starting in 2003, the CGU launched the Programa de Fiscalização por Sorteios Públicos (Monitoring Programme with Public Lotteries), aimed at overseeing the use of federal transfer funds to states and municipalities. Generally, sixty municipalities are randomly selected across states by the Caixa Econômica Federal (a national lottery). Once chosen, a municipality becomes ineligible for selection in the subsequent three to twelve lotteries. Additionally, only municipalities with up to 500,000 inhabitants, excluding state capitals, are eligible for selection. 12 Between April 2003 and February 2015, forty lotteries were conducted resulting in 2,241 audits across 1,949 different municipalities. When a municipality is selected, a team of auditors is dispatched to analyse its accounts, inspect projects and services funded by federal transfers and interact with the local community. For each municipality audited, the CGU compiles a report detailing the identified irregularities. After aggregating the information, these reports are made available online and are also sent to the Tribunal de Contas da União, public prosecutors and the municipal legislative branch (Avis et al., 2018; Batista, 2013). Auditors are recruited through competitive public examinations and receive highly competitive salaries, which diminish the incentives for corrupt behaviour. Additionally, inspections in municipalities are conducted in groups, reducing opportunities for auditors to engage in corrupt practices (Avis et al., 2018). While it would be implausible to assume that audits can identify all possible forms of corruption, the data suggest that a significant portion of misconduct is uncovered. CGU auditors primarily identify issues related to illegal procurement, diversion of funds and overinvoicing (Ferraz and Finan, 2011).

The Declared Wealth of Brazilian Politicians

The transparency of politicians’ financial assets and government actions has been a key theme in anti-corruption movements (Olken and Pande, 2012). The idea is that access to information empowers citizens to observe and evaluate the behaviour of politicians, influencing their electoral decisions based on performance. There is evidence that public disclosure of politicians’ assets is associated with the quality of government and the reduction of corruption (Djankov et al., 2010), although it also reduces the quality of candidates who enter the electoral competition (Fisman et al., 2016; Szakonyi, 2023).

Under Brazilian legislation (Law 9504/1997), politicians must submit their asset declarations to the Regional Electoral Court (Tribunal Regional Eleitoral, TRE) to run for office. This declaration includes the candidate's assets, such as houses, vehicles, land, farms, cattle, balances in current and savings accounts and other financial investments. This measure aims to provide voters with the necessary information to evaluate candidacies and to monitor the evolution of their representatives’ assets.

The limitation of the data is that the declarations may contain errors, some of which might be unintentional, such as typographical errors, while others might be intentional, as politicians may under-report their wealth to obscure it from voters (Souto-Maior and Borba, 2019). This occurs because the Electoral Court's responsibility is limited to receiving, registering and disclosing the asset declarations; it does not analyse their accuracy. In other words, there is no verification of the values declared by candidates.

However, we believe that the incentives for incumbents to hide assets as a function of audit risk are likely minimal for two reasons. First, under current law, candidates cannot be sanctioned or absolved by the justice system if the assets they declare to the Electoral Court do not match their actual wealth. Indeed, since 2006, the Brazilian Constitutional Court has upheld the stance established by the Supreme Electoral Court, which holds that omitting assets from the electoral declaration does not constitute an offense. In other words, anti-corruption institutions do not regard declared assets as proof of misconduct or as an indication of absolution.

Second, incumbents may also have incentives to display their wealth in contexts where clientelistic practices are prevalent. While survey experiments in developing countries have shown that voters generally do not favour wealthier candidates (Campbell and Cowley, 2014; Carnes and Lupu, 2016), in highly unequal settings like South Africa, poorer voters often support wealthy “tycoons” due to their ability to provide clientelist benefits (Justesen and Markus, 2024). In India, survey experiments show that voters punish politicians for rapid wealth accumulation, but this effect weakens when incumbents deliver strong performance or use identity-based appeals (Chauchard et al., 2019).

Particularly in the case of Brazil, Silva (2023) emphasises that the display of material resources is a strategic tool for candidates to project an image of wealth and influence – attributes often perceived by voters as indicators of competence and success. While vote-buying is a prominent example of this strategy (Nichter and Peress, 2017), it is by no means the only approach. Candidates also leverage visual and material cues – such as attire, campaign vehicles and promotional materials – to project affluence and strengthen their political image.

Nevertheless, even if politicians under a high risk of being audited aimed to hide part of their wealth, we also conducted simulations to determine the percentage of assets that mayors in the treatment group would need to conceal to observe a null effect of the treatment condition. The bias resulting from the data limitation will be discussed later (in the “Do Mayors with High Audit Risk do not Re-run?” section).

Empirical Strategy

In order to estimate the causal effect of increasing the audit risk on wealth accumulation by politicians, we take advantage of the Programa de Fiscalização por Sorteios Públicos. Uniquely at the time of the 32nd lottery, the CGU carried out the selection of municipalities in two steps. As illustrated in Figure 1, in May 2009, they announced that thirty municipalities out of 120 would be selected for a regular audit one year later. 13 It is important to note that mayors received a letter from the CGU to ensure that they were aware of their status. In April 2010, the remaining thirty municipalities that would be audited were selected from the remaining 5,175 municipalities. 14 Consequently, on average, the first group of 120 municipalities had a 25 per cent chance of being audited. In contrast, the remaining 5,175 municipalities were eligible to be randomly selected through regular lotteries, resulting in varying probabilities of being audited depending on the state of the federation, typically ranging from 3–6 per cent. 15

Timeline of Elections and Lotteries.

In summary, the municipalities in the treatment group were subjected to an approximately 20 percentage point increase in the annual likelihood of being audited compared to those in the control group. Even though municipalities with high audit risk were under treatment for only about one year, this is significant as it represents a quarter of a political term. Moreover, the fact that they are not under treatment for the entire term does not favour the main hypothesis, which further strengthens the validity of the results.

Given that the attribution to the treatment or control status is random, the estimation of the causal effect is straightforward. We estimate the difference in means of outcomes from the treatment and control groups using ordinary least squares (OLS) regression models with robust standard errors:

The main outcome variable (Wealth) is the total sum of declared wealth by the mayor to the Electoral Court at the time of the 2012 election. If the mayor (elected in 2008) does not re-run for the same office (2012), we do not observe his wealth. Consequently, our sample is restricted to municipalities where mayors re-ran for office. The self-selection bias resulting from this fact will be discussed in detail later (in the section “Do Mayors with High Audit Risk do not Re-run?”). From the universe of 5,295 municipalities that could have been selected by the CGU in the 32nd lottery, we actually observe 2,266 (42.8 per cent). Out of this total, 2,210 (97.5 per cent) are in the control group and 56 (2.5 per cent) are in the treatment group.

The dataset also incorporates more detailed measures of politicians’ wealth. We have categorised this wealth into three distinct types. 16 The first category is real estate, which represents the total value of real estate declared by the candidate (e.g., houses, farms, land). The second category is personal property, indicating the total value of personal assets declared by the candidate (e.g., vehicles, bank accounts, shares, investments, jewellery). The third category is livestock, representing the total value of livestock declared by the candidate (e.g., cattle, pigs, goats). This classification is an important gauge for understanding whether politicians seek to conceal traces left by corruption when faced with the risk of an audit, considering that personal property and livestock are assets that are less visible and more challenging to trace (Trevisan et al. 2003).

Results

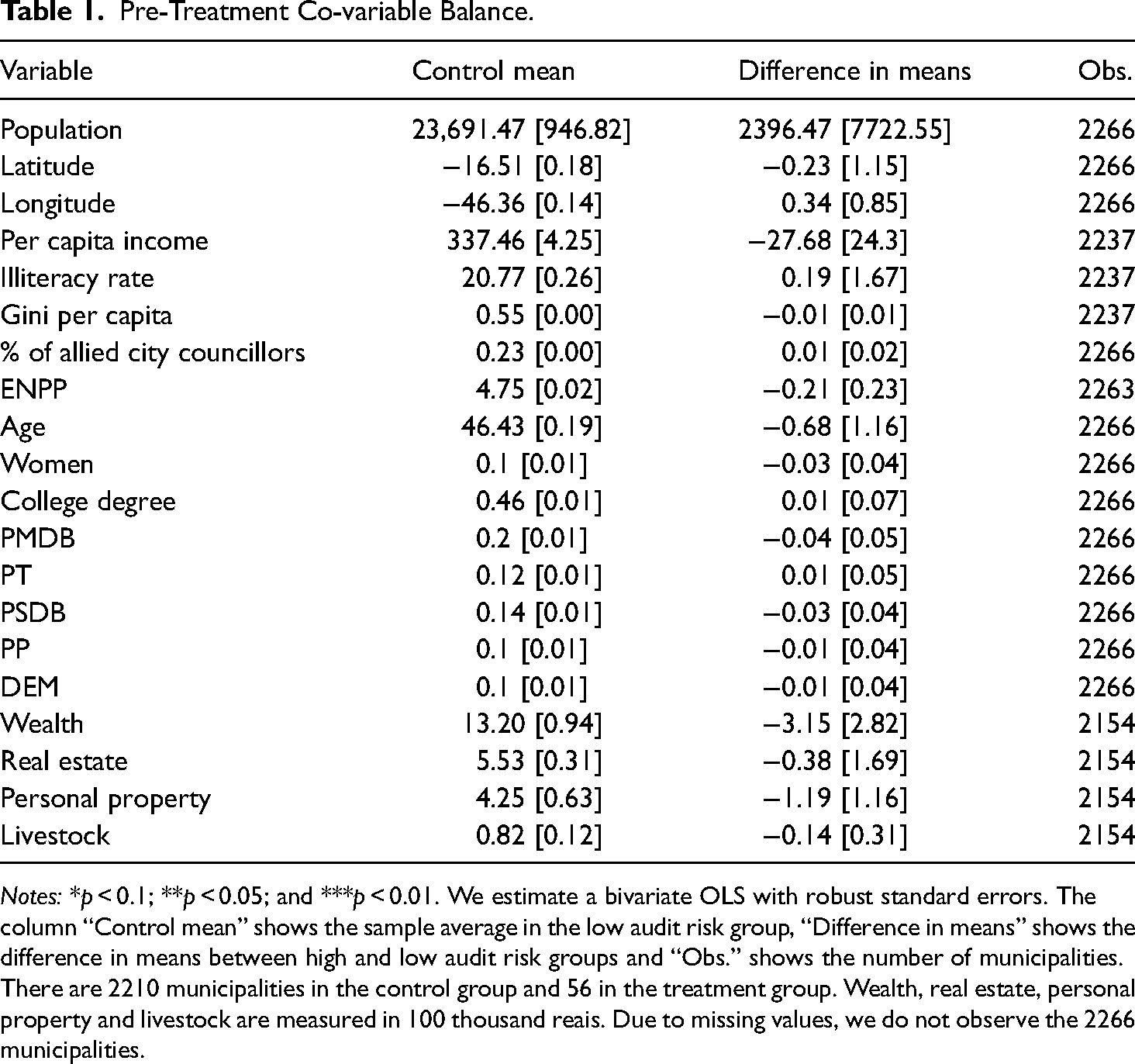

Pre-Treatment Covariate Balance

As a check of the randomisation, Table 1 presents whether any systematic differences exist between municipalities in the control and treatment groups. The second column (Control mean) presents the mean for the municipalities with a low risk of being audited, whereas the third column (Difference in means) presents the difference in means between the control and treatment groups. The number of observations is listed in the fourth column (Obs.). Variables 1–6 come from the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística) and contain socioeconomic characteristics of the municipalities measured during the 2000 population census. 17 The political competition dimension (variables 7–8), the mayors’ characteristics (variables 9–16) and the wealth in 2008 (variables 17–20) come from the Tribunal Superior Eleitoral (TSE).

Pre-Treatment Co-variable Balance.

Notes: *p < 0.1; **p < 0.05; and ***p < 0.01. We estimate a bivariate OLS with robust standard errors. The column “Control mean” shows the sample average in the low audit risk group, “Difference in means” shows the difference in means between high and low audit risk groups and “Obs.” shows the number of municipalities. There are 2210 municipalities in the control group and 56 in the treatment group. Wealth, real estate, personal property and livestock are measured in 100 thousand reais. Due to missing values, we do not observe the 2266 municipalities.

As expected, none of the results are statistically different from zero, indicating that the treatment and control groups are similar in all dimensions evaluated. The first set of variables (1–6) confirms that there are no differences between municipalities in the low-risk and those in the high-risk groups of being audited. Thus, demographic, economic and social characteristics do not appear to be associated with the chances of a municipality being in the treatment group. Furthermore, treated and untreated municipalities are similar in terms of political competition (7–8), as illustrated by the proportion of mayors’ political allies in the city council (measured as the proportion of city councillors affiliated with the mayor's party) and the effective number of political parties (ENPP).

The third (9–16) and fourth (17–20) sets of variables also indicate no differences between the mayors of these municipalities in both political dimensions and previous wealth. On average, the groups have the same proportion of mayors from different parties, and the mayors have similar demographic characteristics. It implies that municipalities are selected irrespective of the mayor's identity. Collectively, these findings support the idea that treated and untreated municipalities, on average, are comparable.

Main Results

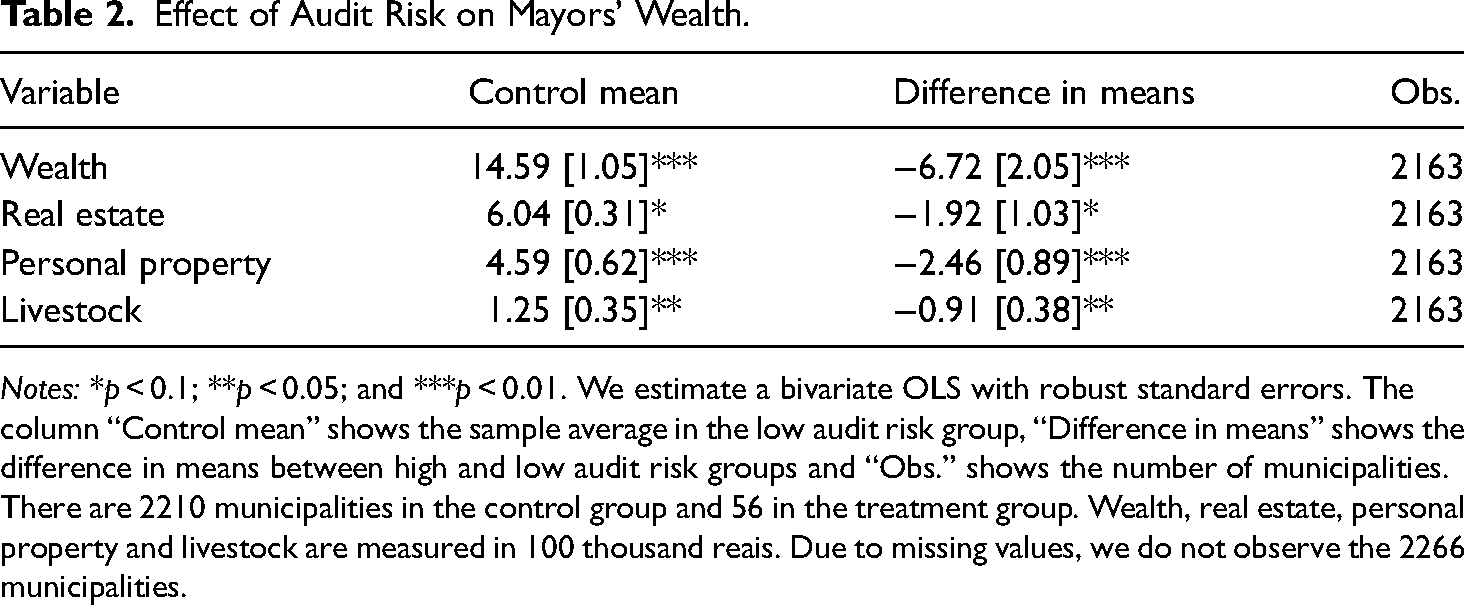

Table 2 presents OLS results from Equation 1. The first line details the impact of treatment on the total wealth declared by politicians, while lines 2–4 focus on other measures of a politician's wealth (real estate, personal property and livestock).

Effect of Audit Risk on Mayors’ Wealth.

Notes: *p < 0.1; **p < 0.05; and ***p < 0.01. We estimate a bivariate OLS with robust standard errors. The column “Control mean” shows the sample average in the low audit risk group, “Difference in means” shows the difference in means between high and low audit risk groups and “Obs.” shows the number of municipalities. There are 2210 municipalities in the control group and 56 in the treatment group. Wealth, real estate, personal property and livestock are measured in 100 thousand reais. Due to missing values, we do not observe the 2266 municipalities.

The evidence indicates that increasing the risk of being audited leads to a reduction in the declared wealth of politicians. On average, mayors in the treatment group declare R$672 thousand (US$ 327 thousand) less than their counterparts in the control group. Considering that the average wealth of mayors at low risk of being audited in our sample is R$1.459 million (US$ 720 thousand), this represents a substantial 46 per cent decrease in the declared wealth of mayors facing a high risk of being audited.

The estimated effects are significant, aligning well with the Brazilian context. Previous random audits have shown that, on average, R$804.8 thousand was diverted from public funds due to corruption (Ferraz and Finan, 2011: 1285), which is 19.8 per cent more than our coefficient estimate. 18 Furthermore, as noted earlier, corruption at the municipal level tends to be highly concentrated among mayors.

Disaggregating assets by type (real estate, personal property and livestock), we observe consistent results. In line with existing literature (Trevisan et al. 2003), personal property and livestock are more likely to be avenues for wealth accumulation through corrupt practices. These types of assets are typically less visible and more challenging to trace than real estate, possibly facilitating corruption. Additionally, personal property and livestock, particularly those of lesser value, may involve simpler and more direct transactions, making them more susceptible to corrupt practices. Despite potential efforts by corrupt politicians to conceal their misconduct, these results provide strong evidence that they are cautious about masking their activities for fear of detection.

The results in Table 2 support these observations. For real estate, an increased likelihood of being audited results in a 32 per cent reduction in the declaration of such assets. For personal property and livestock, the treatment-induced reductions are 53 per cent and 73 per cent, respectively, further reinforcing our argument that incumbents under a greater risk of being audited avoid illicit enrichment.

As a robustness check (detailed in the Appendix 7.2), we re-estimate the models including fixed effects by state and the mayor's previous wealth and cluster the errors at the state level. In these models, the findings remain statistically significant at conventional levels for total wealth and personal properties. Although the results for real estate and livestock lack statistical significance, the coefficients maintain the same direction and nearly identical magnitude.

Additionally, as a robustness check for outlier observations (outlined in the Appendix 7.3), we perform a leave-one-out test. That is, we re-estimate the models each time removing one observation. The results remain practically unchanged across all samples.

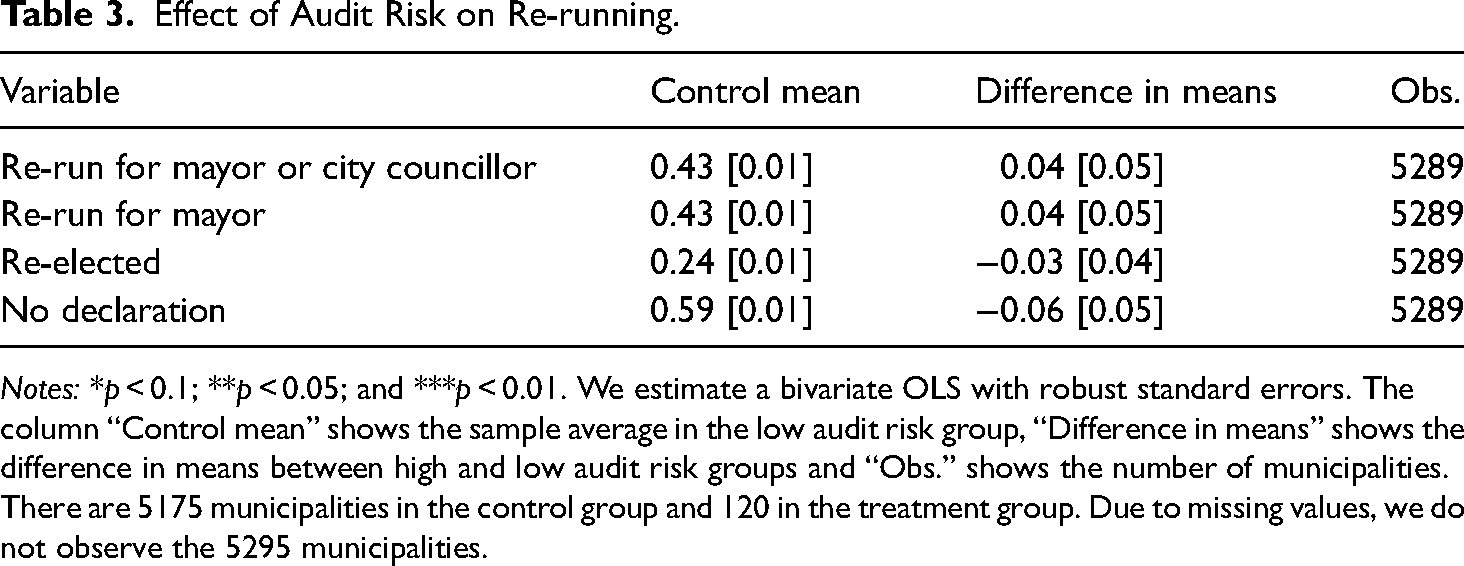

Do Mayors with High Audit Risk do not Re-run?

As discussed earlier, we only observe the wealth of mayors who re-ran in 2012, as we can only assess the assets of candidates who ran for office in both 2008 and 2012. This is because, in Brazil, mayors can only serve two consecutive terms; therefore, mayors who won the elections in 2004 and 2008 – and were thus ineligible to run in 2012 – were not included in our sample. This limitation introduces the potential for self-selection bias. If the treatment status affects attrition propensities, then within the selected sample, the treatment and control groups may no longer have similar compositions, even if the treatment was perfectly randomised initially. It is also plausible that mayors facing a high risk of being audited might choose not to run again to avoid disclosing their assets. Thus, the observed negative result could be attributed to sample self-selection rather than the impact of the treatment. Unfortunately, there is no perfect method to adjust for this problem. To evaluate this possibility, we estimate the effect of being in the high audit risk group on re-running. This test provides some evidence on whether the treatment impacted selection into the sample. Although failing to reject the null hypothesis of no difference does not completely prove the absence of sample selection, a rejection would strongly suggest the presence of a problem.

Table 3 shows the results. The findings suggest that mayors in municipalities with high audit risk do not abstain from seeking re-election to evade the disclosure of their assets. Mayors in both the treatment and control groups have equal probabilities of seeking re-election for the positions of mayor and councillor. Likewise, their chances of being re-elected are also comparable. It ' noteworthy that a considerable number of candidates do not disclose their assets; however, there are no discernible differences between the two groups in this aspect.

Effect of Audit Risk on Re-running.

Notes: *p < 0.1; **p < 0.05; and ***p < 0.01. We estimate a bivariate OLS with robust standard errors. The column “Control mean” shows the sample average in the low audit risk group, “Difference in means” shows the difference in means between high and low audit risk groups and “Obs.” shows the number of municipalities. There are 5175 municipalities in the control group and 120 in the treatment group. Due to missing values, we do not observe the 5295 municipalities.

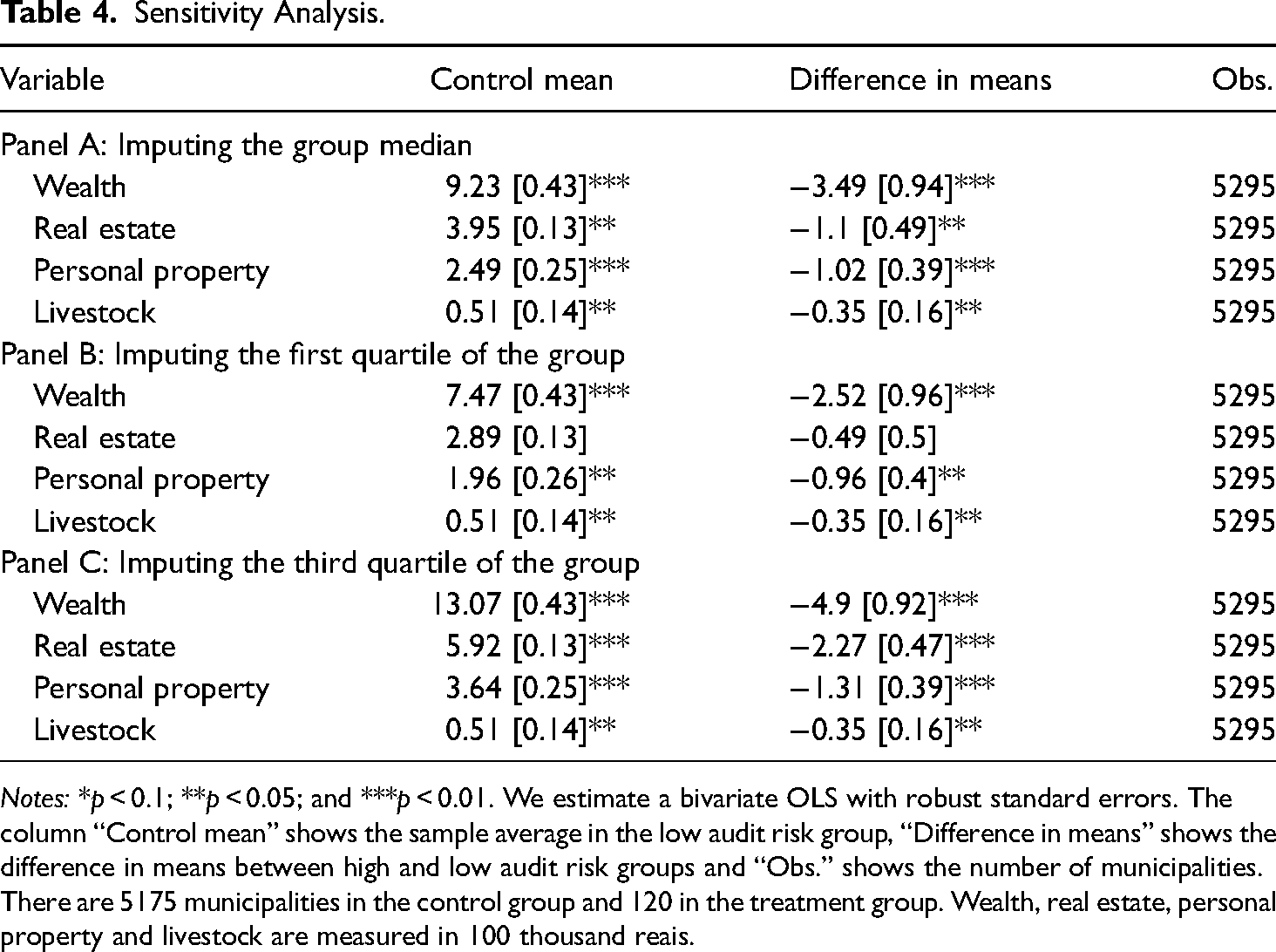

An alternative method for assessing the influence of self-selection on our results is through a sensitivity analysis (detailed in Table 4). This analysis involves imputing the wealth for instances where candidates choose not to re-run (i.e., instances where their wealth is not observed) and estimating the treatment effect as if the database were complete. We imputed three distinct values (the median, the first quartile and the third quartile of declared wealth for both treated and untreated observations). The aim of this test is to check the robustness of our results by imputing different values for the missing data. Overall, the outcomes closely align with our primary findings. Instead of assigning these values, we can also implement an algorithm for multiple imputation of missing values, such as Amelia II (King et al., 2001). Multiple imputation involves imputing different values for each missing value in the data and subsequently generating multiple completed datasets. Across these completed datasets, the observed values remain constant, while the missing values are filled in with different imputations that reflect the uncertainty about the missing data. In Appendix 7.4, we implemented the Amelia II algorithm for this task. We generated 100 different datasets and estimated our model from Equation 1. For our primary dependent variable (Wealth), 97 per cent of the results remained negative and statistically significant at 90 per cent. For personal property and real estate, 77 per cent and 78 per cent of the results were still negative and statistically significant, respectively. Finally, for livestock, the percentage was lower at 43 per cent. We acknowledge that this is an imperfect solution. However, we believe that we did the best that could be done given the data limitations.

Sensitivity Analysis.

Notes: *p < 0.1; **p < 0.05; and ***p < 0.01. We estimate a bivariate OLS with robust standard errors. The column “Control mean” shows the sample average in the low audit risk group, “Difference in means” shows the difference in means between high and low audit risk groups and “Obs.” shows the number of municipalities. There are 5175 municipalities in the control group and 120 in the treatment group. Wealth, real estate, personal property and livestock are measured in 100 thousand reais.

Do Mayors with High Audit Risk Declare Less Than They Actually Have?

An alternative explanation for the observed result could be the incomplete declaration of assets by mayors. We believe that candidates have little reason to omit their personal wealth to avoid judicial convictions, given that hiding assets from the Electoral Court is not considered an offense, as already declared by the Supreme Court. Additionally, in underdeveloped countries, personal wealth can serve as an electoral advantage for incumbents, as it signals to voters that the candidate has the means to provide clientelist benefits (Justesen and Markus, 2024). According to Silva (2023), the display of material resources aims to create the impression among voters that candidates possess abundant means, which is often perceived positively as a sign of power, capability and success. The clearest example of this strategy is signalling the capacity to buy votes. However, candidates also seek to reinforce their appeal as well-funded and influential political actors.

Even so, if mayors in the control group indeed declared all their assets, while mayors in the treatment group disclosed only a portion, the previously observed negative result might be attributed to the incomplete declaration of assets rather than to the increased risk of being audited.

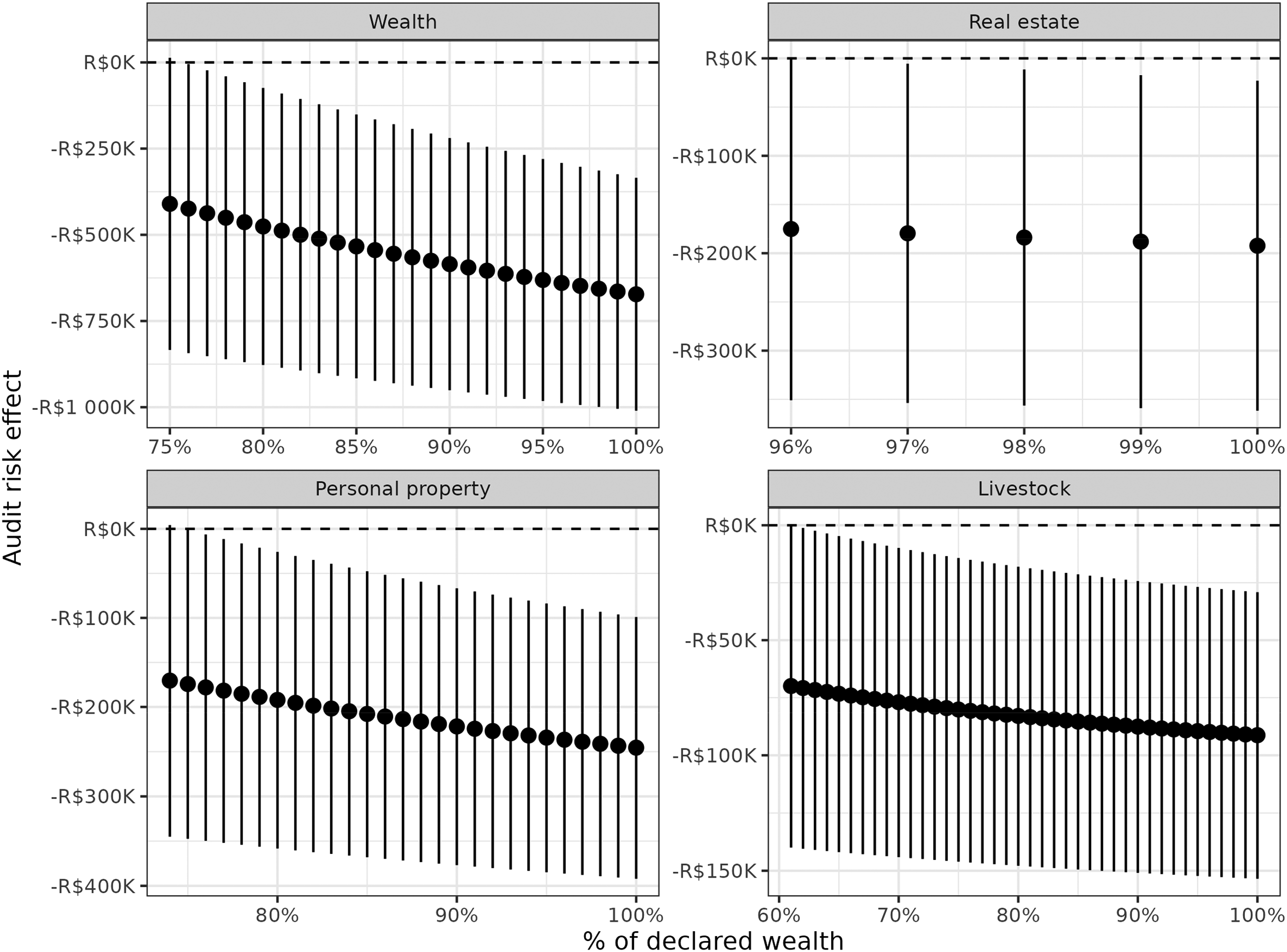

To assess this hypothesis, we conducted simulations to determine the percentage of assets that treated mayors would need to cease disclosing in order to observe a null effect of the treatment. In the simulation, we assume that mayors in the control group declared 100 per cent of their assets, while those in the treatment group disclosed only a portion. Thus, we are modelling the worst-case scenario.

The results presented in Figure 2 show that the effect becomes null when we assume that mayors in municipalities with high audit risk are declaring only 75 per cent of their wealth. In other words, the increased risk of being audited no longer has an effect when we assume that the mayors in the treatment group hide 25 per cent of their assets and the mayors in the control group declare 100 per cent. Similar results were found for assets more susceptible to being incorporated through corrupt practices, i.e., personal property and livestock, 74 per cent and 61 per cent, respectively. Only for real estate do we find the null effect at a higher level, 96 per cent.

Simulation. Notes: Confidence intervals of 90%.

Nevertheless, it ' crucial to bear in mind that we are simulating the worst-case scenario, where mayors in the treatment group refrain from declaring a portion of their assets while mayors in the control group declare 100 per cent of theirs. However, a plausible scenario would be the opposite. Rather than mayors in the treatment group avoiding the declaration of some assets, they might have more incentives to disclose everything, given the higher likelihood of being audited.

Is it About Actually Being Audited or Having a High Risk of Being Audited?

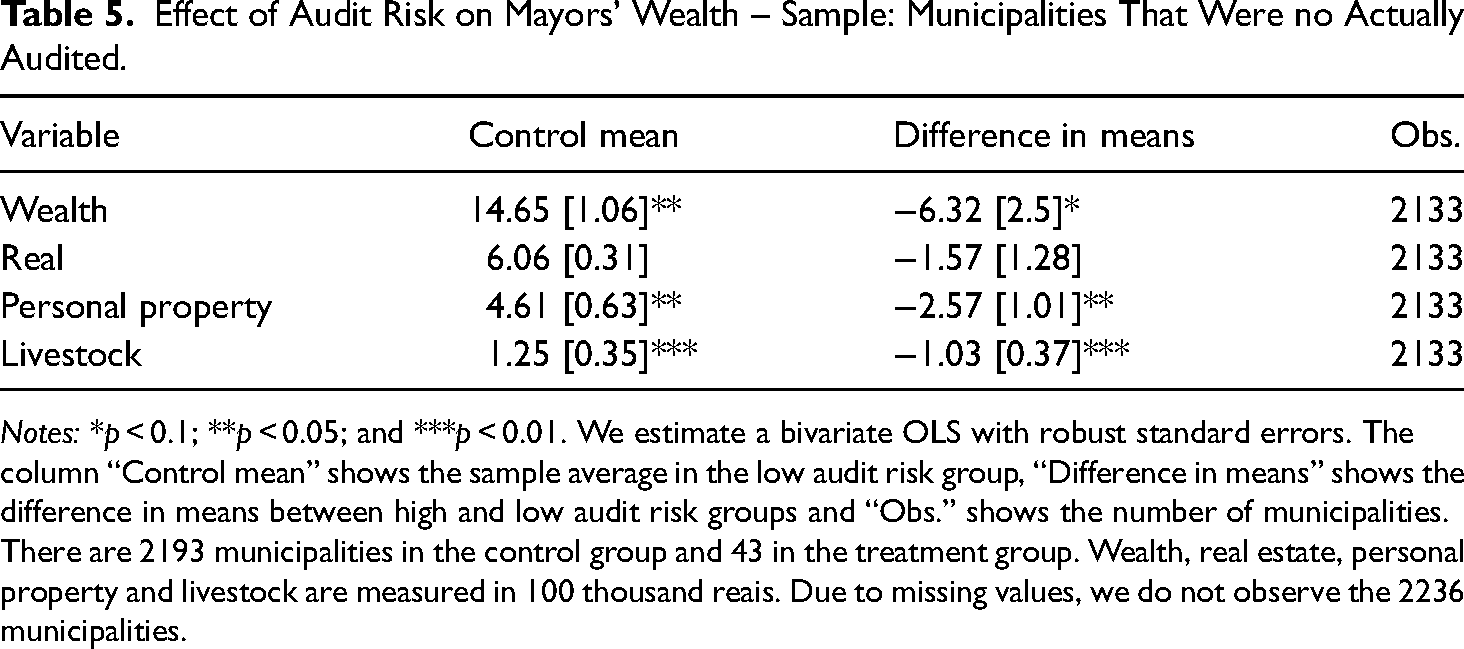

As an additional result, in this section, we explore whether our results reflect the causal effect of an increase in the risk of being audited or whether they indicate the causal effect of actually being audited. Out of the 120 municipalities in the treatment group, 30 were actually audited. In contrast, within the control group comprising 5,175 municipalities, only 30 were subjected to audits. To put it differently, 25 per cent of mayors in the high-risk-of-audit group were indeed audited, whereas a mere 0.58 per cent of mayors in the low-risk-of-audit group underwent the audit procedure. Consequently, there is a possibility that the observed result is attributable to the audit itself rather than solely to the heightened risk of being audited.

To evaluate this hypothesis, we replicate our primary findings in Table 5 using a subset of municipalities that were not audited. In other words, we excluded sixty audited municipalities from the dataset, i.e., thirty audited municipalities from each group. The findings suggest that, even when excluding municipalities that were actually audited, increasing the risk of being audited leads to a reduction of R$632 thousand in the assets declared by mayors - an amount very close to the previously reported value for the entire sample. Moreover, the outcomes for the other variables are likewise comparable. The sole noteworthy observation is that the result did not attain statistical significance for real estate. The result strengthens the argument that politicians alter their corrupt behaviour merely upon becoming aware of the potential for an audit capable of triggering political costs, even in the absence of an actual audit.

Effect of Audit Risk on Mayors’ Wealth – Sample: Municipalities That Were no Actually Audited.

Notes: *p < 0.1; **p < 0.05; and ***p < 0.01. We estimate a bivariate OLS with robust standard errors. The column “Control mean” shows the sample average in the low audit risk group, “Difference in means” shows the difference in means between high and low audit risk groups and “Obs.” shows the number of municipalities. There are 2193 municipalities in the control group and 43 in the treatment group. Wealth, real estate, personal property and livestock are measured in 100 thousand reais. Due to missing values, we do not observe the 2236 municipalities.

Discussion

Corruption is notoriously difficult to measure objectively (Donchev and Ujhelyi, 2014; Gutmann et al., 2020; Olken, 2009), making it challenging to determine whether politicians react to audits by refraining from misappropriating public resources. Instead of deterring corruption, audits might encourage politicians to either enhance the efficiency of public services to avoid voter sanctions or to conceal misconduct more effectively. This paper aims to bridge this gap by examining the personal wealth of politicians who face varying probabilities of being audited, as corruption is often characterised by the misuse of public power for private gain. We leverage a unique audit programme conducted by the Brazilian Office of the Comptroller-General, which randomly informed 120 municipalities about their increased likelihood of being audited, in contrast to another 5,175 municipalities. This setup provides a robust framework for assessing the impact of audit risk on the financial disclosures of elected officials, offering insights into their behaviour in the face of potential scrutiny.

The evidence indicates that increasing the risk of audit leads to a 46 per cent decrease in the declared wealth of politicians. The results hold when considering assets that are less visible and more challenging to trace, such as personal property and livestock. Robustness checks confirm that the coefficients retain the same direction and nearly identical magnitude. We conducted simulations to determine if the observed effects remain significant even if mayors with a high probability of being audited under-declare their wealth. It is important to note that we modelled the worst-case scenario, where mayors in the control group declare 100 per cent of their assets. To isolate the causal effect of an increase in audit risk from the causal impact of the audit itself, we excluded all municipalities from both the treatment and control groups that were selected for audits. The causal effects remained statistically significant for total assets, personal property and livestock.

Our findings have several important implications. Firstly, unlike other studies where the same treatment group receives information about audit risk and undergoes actual audits (Olken, 2007), our additional tests ascertain whether politicians alter their corrupt behaviour merely by becoming aware of the potential for an audit, even in the absence of an actual audit. This is particularly relevant in scenarios where implementing audit policies is cost-intensive and governmental resources are limited. Our results suggest that incumbent politicians refrain from engaging in corrupt practices simply by being informed about the risk of exposure, without the necessity of an actual audit, which is promising for contexts where audits do indeed trigger legal and electoral consequences for corrupt politicians.

Second, our findings corroborate those of Melo and Pereira (2013), who highlight the role of political competition and control institutions in diminishing the wealth of state deputies, demonstrating that audits increase the risk of exposure and curb politicians’ wealth accumulation. Third, our results do not contradict those of Izumi (2019), who found no causal relationship between winning elections and wealth gains. Instead, our findings reveal that audit risk makes holding elected office less financially advantageous than operating in the private sector, as it discourages personal enrichment through corruption among elected officials.

Finally, in estimating the causal effect on politicians’ personal wealth, we strengthen the argument that mayors abstain from corrupt activities in response to audit risk. Unlike prior studies using policy indicators as outcomes (Funk and Owen, 2020; Olken, 2007; Zamboni and Litschig, 2018), our analysis focuses on personal wealth, aligning with the widely accepted definition of corruption, which emphasises the misuse of public authority for personal gain (Pozsgai-Alvarez, 2020; Thompson, 2018). It is possible that corrupt politicians have devised new methods to disguise irregularities, a hypothesis future research could explore. However, our tests provide evidence to the contrary, as the risk of audit impacts assets that are less visible and more challenging to trace.

The observed reduction in declared wealth among mayors with a higher probability of being audited raises a crucial question: does this outcome reflect increased honesty in governance or decreased honesty in financial disclosure? Distinguishing between these explanations is vital for interpreting the broader implications of audits on political accountability. It is important to note that audits typically focus on evaluating public finances and the misuse of public resources rather than verifying the personal wealth declarations of politicians. Consequently, there is little direct incentive for mayors to conceal their assets as a reaction to the audit process itself, since hiding assets does not prevent the discovery of irregularities. Moreover, if voters tend to view wealth as an indicator of success or competence, as is the case in Brazil (Silva, 2023), candidates might have more to gain politically by projecting affluence rather than underreporting their wealth. Finally, our results align with existing literature that highlights the role of audits in reducing corruption by increasing the risk of detection and punishment, thereby incentivising more honest behaviour in public office (Avis et al., 2018; Di Tella and Schargrodsky, 2003; Olken, 2007; Zamboni and Litschig, 2018).

Although these considerations strengthen the case for reduced corruption as the underlying explanation, the limitations of self-reported wealth data make it imperative to approach this conclusion cautiously. Further research using more comprehensive and reliable data on both declared and actual wealth would be valuable in disentangling the mechanisms at play and providing a more definitive answer to this question.

Supplemental Material

sj-docx-1-pla-10.1177_1866802X251343637 - Supplemental material for Audit Risk and Wealth Accumulation: When Politicians Give up on Corruption

Supplemental material, sj-docx-1-pla-10.1177_1866802X251343637 for Audit Risk and Wealth Accumulation: When Politicians Give up on Corruption by Thiago do Nascimento Fonseca and Mauricio Yoshida Izumi in Journal of Politics in Latin America

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the Fundação de Amparo à Pesquisa do Estado de São Paulo (grant number 2021/11522-4).

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.