Abstract

The success of microcredit lending programs depends in part on the regulatory framework that policymakers create to support them. A fact that many microcredit analyses often ignore or overlook is that this framework is shaped by both ideological and partisan political considerations of policymakers. In Argentina, the Peronist governments of Néstor and Cristina Kirchner launched and supported a state-centered microcredit program characterized by strict loan conditions and direct state grants for capital and operational costs to existing non-profit organizations that were largely supportive of Peronism. Provinces and municipalities governed by anti-Peronists refused to participate. As a result, the National Microcredit Program has come to mimic past patronage based policies to a significant extent, engendering dependency on government resources, and thereby threatening its long-term viability. This article explores the impact of the left's ideological and political project on microcredit policy, implementation, and outcomes in Argentina.

Introduction

Latin America is well into its second decade of major growth in microcredit financing. While many microcredit and microfinance projects began as early as the 1970s, these programs have taken off in the new century, growing from a regional portfolio of USD 590 million in 2000 to over USD 40.2 billion in 2014 (Mix Market 2016). This surge is due to several factors that have increased microcredit as an attractive alternative to extant anti-poverty programs, including the UN's declaration of 2005 as the Year of Microcredit, the awarding of the 2006 Nobel Peace Prize to Muhammad Yunus for his work with the Grameen Bank in Bangladesh, and the subsequent promotion of microcredit methodologies by international and regional development banks and other international financial institutions (IFIs).

Notwithstanding the amount of passion and resources put toward microcredit programs in Latin America, several studies have pointed to the dangers, pitfalls, or limits of the same (Bédécarrats, Bastiaensen, and Doligez 2012; Brett 2006; Bastiaensen et al. 2013; Bateman 2006; Chowdhury 2007; Lucarelli 2005; Warby 2016). Throughout these analyses, scholars have emphasized how unquestioned assumptions about incentives, cultural differences, and differentiated strategies to overcome credit failure have undermined or limited the positive impact of microcredit programs in many locales. The results of such studies often emphasize caution regarding the power of microcredit to achieve the practice's major goals of poverty alleviation and social inclusion, and call for specified program design reforms (Schreiner and Colombet 2001; Bekerman and Cataife 2004).

However, an issue that is often underemphasized, if not absent, from these studies is the critical variable of politics. Analyses of microcredit policy in the economic development, business, and anthropology literatures have focused on institutional structure, lending processes, financial incentives, cultural constraints, and domestic or global contexts to explain key outcomes such as overall efficacy, efficiency, growth, breadth and depth of lending patterns, and repayment rates. In so doing, these studies commonly ignore the manner and style in which government leaders design and implement microcredit programs in ways that fit with their ideological principles or partisan political goals.

In the 1970s and 1980s, as microcredit practices began to spread, Latin American governments were far less proactive in fostering microcredit programs than they are now, and thus these initial analytical approaches may be justified. Recently, however, policymakers and other actors have played a more prominent role in supporting and regulating the emerging microcredit sector. Beyond fostering and nurturing the dissemination of microlending practices, their actions and strategies are sometimes motivated by more myopic, shorter-term political goals such as fostering electoral support or aligning state policy with one's partisan views. Thus, factors such as the ideological worldview of the current government, and key characteristics of political parties and the political party system, are likely to influence the nature and shape of microcredit policy.

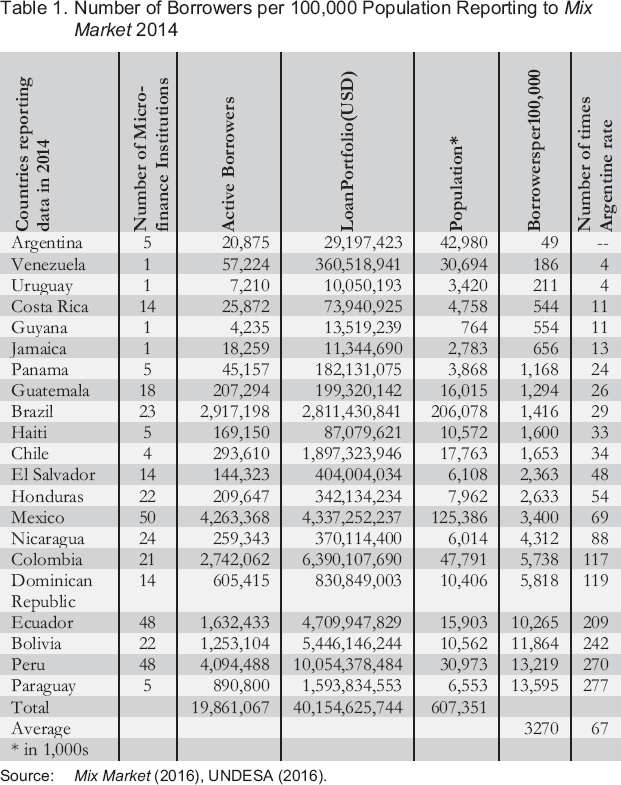

The main purpose of the present study is to examine these relationships in the case of Argentina under Presidents Néstor and Cristina Kirchner. Why Argentina? The focus on Argentina as a case study is justified because of the strong anomaly it represents in the field of microcredit. Specifically, Argentina has a very high level of unmet demand with respect to microcredit services. Among 21 Latin American countries for which sufficient data are available, Argentina has the absolute lowest number of microcredit borrowers per capita. At least four countries that are less wealthy than Argentina have rates that are more than 200 times the level of Argentine microcredit borrowers. In addition, Argentina passed a new microcredit law (Law 26,117) in 2006 to tailor, guide and disseminate microlending practices throughout the country. This analysis seeks to understand how partisan politics influenced the making of this law, and explores the consequences for the program's implementation and outcomes.

The central argument presented here is that leftist ideology played a major role in shaping how microcredit policies are fashioned and implemented in Argentina. To wit, the Kirchners proposed and implemented a state-centric model as they viewed the state as a key instrument in countering negative market outcomes and forging a more just society. Recent studies have focused on explaining the rise Latin America's “pink tide” (Levitsky and Roberts 2011; Weyland 2009) and assessing the various goals of leftist governments (Teichman 2009; Huber and Stephens 2012). Weyland, Madrid, and Hunter (2010) assessed major social policies along three major dimensions or self-proclaimed goals of leftist governments: increasing social equity, ensuring macro-economic sustainability, and increasing political inclusion. Their analysis suggests that leftist governments can be usefully characterized along a continuum according to the extent to which the government respects democratic practices and sees value in economic market mechanisms.

On one hand, governments such as Bachelet's in Chile or Lula's in Brazil exemplify a more social democratic path in which democratic processes are maintained, strengthened or solidified, and social and economic policies play a more moderate role in income distribution and poverty alleviation as market mechanisms continue to play a central role in guiding private development decisions. On the other hand, populist governments, exemplified by the likes of Chavez in Venezuela and Morales in Bolivia, are less concerned with market signals and instead institute policies and programs that are less constrained by democratic accountability mechanisms. Ultimately, Weyland, Madrid, and Hunter (2010) found that social policies in the latter countries were rife with political payoffs, inefficient, did not take corrective action, and ultimately failed at major leftist goals. Interestingly, those authors saw the case of Argentina – while not one of the four key case studies of their study – as representing a middle path between the two extremes of the “contestatory” and “moderate” lefts.

Beyond goals, however, one may also examine how political considerations ultimately had an impact on design, implementation, and outcomes. Indeed, part of the explanation for policy success or failure may be found in how politics shapes these areas. With respect to microcredit programs, several studies have suggested that leftist projects are more likely to include a prominent role for the state in seeking redistribution of income and greater social inclusion. In this case, a contestatory leftist administration would be more likely to control funding mechanisms or establish strict funding conditions (such as capping interest rates) that may not be congruent with market forces (Olsen 2010). Sustainability may be less of a concern, while breadth and depth of financial and social inclusion are paramount.

Once adopted, however, policies may also be executed in a way that reinforces partisan political bias along familiar patterns of patronage and clientelistic relations (Weingod 1968; Levitsky and Roberts 2011). Madrid, Weyland, and Hunter (2010) argued that a propensity for clientelistic implementation and a lack of accountability mechanisms have been key characteristics of the “contestatory left” in Latin America. Even if programs were designed explicitly to be non-partisan in nature, administrators and politicians may seek to employ these newly created programs to advance their political project and sustain their patronage networks. Robinson and Verdier (2013) argued that patronage is more likely when clients and patrons can hold each other accountable for delivering benefits and political support, respectively. They argued that public employment is one of the most well suited forms of patronage that provides for mutual accountability because “a job is selective and reversible, and thus ties the continuation utility of a voter to the political success of a particular politician” (Robinson and Verdier 2013: 260). I argue below that the design of the Argentine National Microcredit Program is similar in nature to public employment program and created strong incentives for policymakers to engage in exactly these types of patron-client relations with this program.

A second argument is that the shape and nature of the political arena also influenced, to some degree, how the policy was implemented and administered. Levitsky and Roberts (2011) moved beyond the often observed dichotomy of supposed “good” and “bad” lefts, proposing a four class typology of leftist populist regimes along two dimensions: relative dispersion of authority and whether leaders are attached either to an established party organization or are part of a new movement (Roberts and Levitsky 2011: 13). In their view, established party organizations have more limited choices because they must appease organized sectors with patronage, whereas leaders with more amorphous social movements enjoy greater latitude in terms of policymaking and are less bound by accountability mechanisms. For example, in their analysis the administrations of Néstor and Cristina Kirchner are characterized by concentrated authority attached to an established party organization. Etchemendy and Garay (2011) noted that, unlike Chavez, Correa, or Morales, the Kirchners also found it necessary to appease the organized sectors of the Peronist movement with this program by providing direct patronage to them, a dynamic that clearly affected the Argentine microcredit approach (Etchemendy and Garay 2011: 295). Thus, the type of populist regime is important because it shapes the array of policy levers that are open or closed to policymakers as they shore up legitimacy and support for their policies.

In sum, I examine the impact of leftist politics on Argentina's microcredit policy along three phases: structure/design of policy, implementation, and outcomes. I seek to uncover the ways in which ideologically driven partisan decisions by the leftist Peronist government and the structure of the political party organizations shaped legislation, common practices, and outcomes in this area. The analysis enhances our understanding of how and why microcredit has not grown as quickly in Argentina as in other countries in the region.

The empirical evidence for this study consists primarily of interviews of key stakeholders in the microcredit lending sector, including government leaders and policymakers, leaders of non-profit organizations who work with microcredit, and leading private sector actors involved in microfinance. I conducted 33 formal interviews in June and July of 2012 and 2015 in five different major cities in different provinces: Buenos Aires, Córdoba, Lomas de Zamora, Mendoza, and San Miguel de Tucuman. 1 The findings gleaned from these interviews are buttressed by published and unpublished reports from national, provincial, and municipal governments, as well as business associations that are directly involved in microcredit practices.

To avoid recriminations on interviewees for their frank views on government performance, I report interviews confidentially unless the individual is a widely known public figure.

Leftist Politics and the Design of Microcredit Policy

As in other Latin American countries, Argentina had some experience with microlending through international foundations and agencies prior to the arrival of Néstor Kirchner as president in January of 2003 (Bekerman and Cataife 2004). Almost immediately after taking power, however, Kirchner's administration began a concerted effort to develop microcredit as a key instrument of social inclusion under the Ministry of Social Development. Minister Alicia Kirchner, Néstor's sister, led the effort by calling together practitioners who had experience with micro-lending to discuss the creation and implementation of a new national microcredit program. After substantial consultation with different groups, the government passed Law 26,117 on 28 June 2006 entitled Promoción del microcrédito para el desarrollo de la economía social, and created the National Microcredit Commission (CONAMI) within the ministry to administer the National Microcredit Program (CONAMI 2012a).

Argentina's National Microcredit Program differs substantially from other national programs in the region in several ways. First, with respect to terminology, the government carves out a narrow concept of “microcredit” and distinguishes it from microfinance. “Microcredit” refers exclusively to the provision of microloans in a state subsidized fashion to entrepreneurs employing classic parameters of this now well-known methodology. These parameters include (1) small loan amounts paid back over a relatively short period of time (six to 24 months), (2) clients with little or no collateral in the informal sector, (3) the use of solidarity groups to guarantee loans, and (4) credit decisions based on interviews with clients rather than formal credit scores. Microfinance, on the other hand, includes not only the provision of credit at unsubsidized rates and use of formal credit procedures and guarantees, but also other financial services such as checking and saving account services, personal or home loans, and unemployment and life insurance services (Gandulfo 2012).

Second, while most other Latin American countries have structured their microcredit programs around microfinance institutions (MFIs) that almost exclusively offer microcredit and related services, Argentina has decidedly opted out of such a financial agency-centric approach. CONAMI administrators explained that there are at least two reasons why they consciously designed the program to fit into and strengthen the existing structure of civil society instead of creating new, stand-alone MFIs. First, they viewed the organization of civil society in a nascent democracy (or one that has recently re-democratized) as a key component of democratic deepening. They felt that creating a wholly new and different sector of MFIs would most likely pull apart the existing mesh of social organizations and networks in a way that would weaken rather than strengthen civil society. Such a move would work against the leftist project of consolidating democracy in the country through a vibrant and powerful civic sector. They also often expressed the notion that a microcredit program that places MFIs at its center would reflect the same conservative, capitalistic, exploitative, and neoliberal principles they had defeated at the ballot box instead of supporting economic and social solidarity (Gandulfo 2012).

In addition, federal government administrators felt their model embodies an economically astute strategy in that it takes advantage of existing and known social relations among network and neighborhood groups. If one of the key elements to a successful microcredit program is the intimate knowledge between lender and client (as opposed to the financial relations established through a credit board in the formal sector), then why not tap into that knowledge possessed by local neighborhood groups? The alternative of supporting the creation of MFIs means that the new agencies would take a longer time to get off the ground given that they would most likely be established by new personnel who are unfamiliar with the peculiarities and challenges of a given locale's economic and social conditions. 2

To be clear, some for-profit and not-for-profit MFIs exist in Argentina, but they are very few in number. See RADIM (2017).

This strategic choice to funnel microcredit funding through civic organizations bears out the expectation that, in the presence of an established, organized populist party, leaders meet the demands for patronage and mollify those sectors or risk losing political support (Levitsky and Roberts 2011). This aspect of the program appears to fit well with the Peronist Party's emphasis on nurturing links to grass-roots organizations (Freidenberg and Levitsky 2006). In the case of microcredit, state funding provided some of the operational costs of civic organizations that were beholden to Peronism, bankrolling a part of their labor bill while shoring up and strengthening support for the regime. One key consequence for the microcredit sector is that it remains dispersed, loosely connected, heterogeneous, and operates more as an appendage of other non-profits instead of creating microcredit institutions in their own right. Indeed, one key difference in Argentina is that it does not have a host of microcredit banks or agencies compared to most Latin American countries where MFIs that specialize in microcredit thrive.

On a slightly more technical, but not insignificant level, a third way to perceive how partisan politics has shaped the program is simply by noting the use of language. In their materials and during my interviews, personnel from CONAMI refused to use the word cliente (client), or even prestadores de crédito (credit borrowers). The notion was to see entrepreneurs not as economic agents, but rather as political ones – as “subjects with rights” (sujetos de derecho) (Gandulfo 2012). This imposition of cumbersome jargon ended up being more taxing than elucidating. On the surface, the mere use of a specific type of an overbearing leftist nomenclature may not have serious repercussions to revealing its nature. Nevertheless, at a minimum such jargon signals to supporters and opponents alike the extent of government channel funds from the program to support their ideological project.

Fourth, the program encompasses three major “modes” of microcredit delivery that also differ substantially from other models in the region and can be linked to partisan concerns. These modes are the Consortium, Network, and the Good Faith Bank (CONAMI 2012a). Consortia are created at the municipal or provincial level of government and typically include a range of governmental and non-profit actors who have an interest in supporting microcredit programs. The consortium is led by a board of directors and includes various government administrators such as the local or provincial ministers of social development, education, or economic development, as well as leaders of non-profit organizations, directors of cooperative federations, associations of small entrepreneurs, etc. A distinct advantage of this mode of microcredit is that local and provincial governments also commit financial resources to the consortium's work, thereby expanding the impact of federal assistance and creating a “buy-in” model that is designed to support success. The consortia also help the federal government disseminate best practices while sharing the burden of costs with local governments, allowing for some flexibility to attend to specific local needs. The downside of this methodology is that municipalities or provinces controlled by political elites of the president's opposition parties often refused to cooperate in creating consortia in their locales, which limited the spread of the microcredit program.

The second form of microcredit methodology is via various types of networks. These networks may consist of geographically concentrated groups of entrepreneurs from many different branches of economic activities, or may alternatively be associated through their common economic activities. Red Gesol, for example, is a locally based network in Lomas de Zamora (province of Buenos Aires) that aggregates entrepreneurs from many different areas of economic activity. Other networks, such as those of artisans or farmers’ markets, aggregate members according to their similar activities, whose members organize trade shows or fairs to help commercialize their products.

The final method of microcredit delivery in Argentina is called the Good Faith Bank (Banco de la Buena Fe, commonly referred to as banquitos). The banquitos are a service offered by organizations that do not belong to either a network or a consortium, but are most commonly instances of grass-roots non-governmental organizations (NGOs) that are already providing a variety of services to poor clients and wish to add microcredit loans to their list. In some cases, however, a banquito may be created independently of any existing organization for the express purpose of providing microcredit.

In all three modes of microcredit delivery, the National Microcredit Commission (Comisión Nacional de Microcrédito or CONAMI), located in the federal Ministry of Social Development, authorizes larger and more formally constituted member organizations to carry out the role of second-tier lenders called “administrative organizations” (organizaciones administradoras or OAs). The OAs receive funds directly from CONAMI and pass these funds on to roughly a dozen smaller organizations, which then lend directly to entrepreneurs. Because they execute the loans, these latter organizations are called “executor organizations” (organizaciones ejecutores or OEs). Thus, CONAMI deals directly with the OAs, which oversee the work of the OEs (CONAMI 2012a).

The reliance on existing networks has two important consequences for microcredit in the country. First, it opens the door for the program to be used in a clientelistic and thus less efficient manner depending on implementation. The structure strengthens ties between civic groups and the state, but especially those that are strongly supportive of the Peronist project (see next section, below). Second, this institutional design forgoes one of the advantages of the region's more common practice of creating or supporting MFIs – namely, the strong central focus on one type of activity and the accumulation of know-how and best practices that ultimately lead to microcredit success. A small non-profit organization may be able to add some microcredit loans to its portfolio of services offered to local community members, but may not be able to afford separate or specialized training, conference travel, and other exchanges of microcredit professionals. The result is that less qualified and trained credit agents are doing their best to make what are really tough calls when it comes to the potential creditworthiness of clients. They also often lack expertise in advising entrepreneurs with respect to forming or revising their business plans or improving basic accounting practices. The lack of professional expertise ends up limiting the success rate of the microlending program.

A fifth key and fundamental aspect of the design of the program that can clearly be traced to partisan politics is the decision to limit the interest rate for this program to six percent annually. For populists like Kirchner, setting an interest rate at something high enough to cover costs (closer to 25–35 percent annually) is politically untenable. If economic logic suggests that interest rates are set by a combination of the cost of capital, operational costs, and the relative risk of the borrower, political logic suggests that the poorest citizens of society should be entitled to pay the lowest interest rate on state subsidized loans. If a larger farmer or corporation receives loans at 10 percent or less, the poor should not pay more than they do. Indeed, the government decided to opt for the ceiling of six percent annually after it was determined that the lowest interest rate charged among all other loan assistance programs at the federal level was seven percent. 3

Interview E, Representative of non-profit microcredit network, Buenos Aires, 28 June 2012.

The cap on interest rates has forced the government to provide heavy subsidies to lending agents – more so than most microcredit programs in the region. CONAMI subsidizes microcredit in two ways. First, CONAMI provides working capital for microcredit services at zero cost to the lending organization. The funds are granted to the organization and become their funds on receipt, although they must provide an accounting of their eventual use to CONAMI. In contrast to other models, funds are not repaid to the state, and the principal returned to the OEs from clients remains with them to be lent out again. Second, CONAMI realizes that even the subsidy of providing “free” capital does not go far enough to sustain microlending practices. Thus, of the amount passed on to the lending agents, a minimum of 70 percent is restricted to loan capital while up to 30 percent may be used to cover operating expenses. The amount allowed for operating costs does vary from OE to OE, and must be demonstrated by need of the organization (Gandulfo 2012).

Why are subsidies needed? One of the central debates of microcredit methodology is the weight afforded to the two competing goals of maintaining low interest rates without threatening sustainability. The reality is that processing microcredit loans is costlier than traditional loans as the former require the loan agent to travel to the microenterprise location, conduct several in-person interviews with potential borrowers, their neighbors, and business clients to verify information, and undertake a more intensive study of personal financial data (instead of gleaning a formal credit score from a centralized bureau). More importantly, since the loans are smaller than traditional loans, a higher percentage rate must apply in order to cover these higher costs. The mix of low interest rates applied to small loan amounts via an expensive processing methodology can easily render the model economically unviable. This dilemma is succinctly expressed by Microcredit Enterprises CEO Jonathan Lewis:

We in microfinance uphold the market reality, which demands that interest rates sustainably cover a local microfinance institution's expenses. No margin, no mission. Nonetheless, there is something unseemly about the very wealthy earning unnecessarily excessive profits off the unbearably poor. (As quoted in Daley-Harris 2007: 29)

The challenge of sustainability becomes exacerbated in the face of two additional common problems in Latin America: a high inflationary environment and the relatively high cost of formal (vs. informal) labor. Loans have had negative real interest rates in Argentina according to both official and private estimations (IMF 2016). In addition, several interviewees noted the difficulty of hiring credit agents due to the high cost of formal labor arrangements, including deposits to government regulated insurance and pension programs. These elements constitute a significant barrier to expansion and have resulted in some cases of organizations charging higher interest rates than those officially permitted by law to cover these costs.

Clearly, then, the level of state subsidy for the microcredit sector is determined primarily by political and ideological factors championed by the left rather than economic or market criteria. The cap of the annual interest rate at six percent reflects the leftist target of granting the highest level of state subsidy to the poorest of society. To support that rate, grants for operational costs to microlending organizations are required. The program was originally designed to allow organizations to use up to 50 percent of their grant for operational costs, but this was reduced for political reasons when Muhammad Yunus criticized the Argentine government for using so much of its microcredit funding for bureaucratic administration (Gandulfo 2012). The level was reduced to 30 percent, a number that was largely determined as politically defensible, but did not take into account the real costs of microcredit processing (see below).

In sum, the design of Argentina's National Microcredit program clearly bears the imprimatur of a leftist ideological and political project that emphasizes state-centered control over microcredit lending in the ways noted above. These observations notwithstanding, we must also recognize that other, more myopic partisan political motives may lie behind the program's structure. Any aid offered to unorganized or semi-organized sectors of society could strengthen support at the ballot box for the government from that sector, helping to solidify the government's goal of election and re-election. In addition, providing grants to low-income NGOs that use funds to sustain and expand personnel is, in some real ways, analogous to offering public employment. Third, since funds are not paid back to the state, reporting mechanisms to the state can constitute a weak form of accountability. These observations point to the ability of administrators to achieve these other political goals through program implementation, to which I now turn.

Leftist Politics and Microcredit Policy Implementation

To what extent have partisan political considerations affected the manner in which Argentina's microcredit program has been implemented? While the design of the program opens the way for clientelistic practices, the actual implementation of the program in a clientelistic manner is not a logical necessity. Indeed, administrators emphasized the non-partisan nature of the program. Yet ample evidence suggests partisan quid-pro-quo concerns have motivated government administrators in determining who and when organizations received funding through the program.

My interviewees differed sharply on this question depending on whether they personally felt in sync with the Kirchner wing of the Peronist Party. One anti-Peronist, for example, opined that the “entire program is politically motivated, pure and simple.” 4 Another was a bit more forgiving, noting that:

Interview A, Representative of NGO, Córdoba, 17 July 2013.

After what started as a program that was designed to work with several of us organizations working in microcredit, it quickly became fragmented politically, and we […] did not have any interest in supporting any partisan political project. That is why we have not participated with [the National Microcredit Program]. 5

Interview B, Representative of NGO, Córdoba, 16 July 2013.

Other interviewees were slightly less emphatic about the partisan nature of the program, admitting that funds were undoubtedly funneled in the direction of political supporters, but not seeing patronage as the main objective of the program.

Logically, many of the social justice based organization leaders of the OAs or OEs of the microcredit program with whom I spoke were full-throated supporters of the anti-neoliberal nature of Argentina's microcredit policy and its strong pro-social justice nature. These program administrators clearly identify with the Peronist ideology of supporting social policies that help rescue and defend citizenship, and help the poor recover their rights and basic standing as subjects with rights. For example, one interviewee stated unabashedly:

We help [entrepreneurs] organize fairs and trade shows and invite members of the community so that they can see that we work with entrepreneurs, and so that it's possible to see that we have a new line of social policies that we are implementing in this country since 2003. We are very grateful for and have great admiration for this great national and popular project that was led by Néstor Kirchner, and today by Cristina Fernandez de Kirchner. Clearly our province is of the same line as the national government. We come from the same place and we're walking together. 6

Interview C, Government administrator, Tucuman, 11 July 2012.

Most representatives who were supportive of the Kirchners also rejected the patronage claims of other OE and OA representatives, and were adamant that the microcredit program was being administered strictly according to the non-partisan criteria set by laws and regulations.

While the evidence presented here may not be whole or complete, it does suggest that the manner in which some policymakers have used the program was shaped by partisan political concerns. Specifically, the state used the program to help sustain civic organizations whose aim is to fight for greater social justice – an aim that is well in line with Peronism. In addition, the anti-Peronist governors of San Luis Province and the city of Buenos Aires refused to cooperate with the national government on the program in their locales specifically because it was incubated, formed, and implemented by their political adversaries. These facts help to explain the lack of continual growth in the microcredit sector in Argentina.

Leftist Politics and National Microcredit Program Outcomes

The first way to measure outcomes is simply to measure success in terms of some of the “normal” parameters employed by microcredit agencies worldwide. The three parameters considered in this section are (1) expansion of microcredit services, (2) repayment rates, and (3) the extent to which the programs are sustainable. Some evidence suggests that Argentina's microcredit model has been a success with respect to diffusion of microlending. With the inception of the Microcredit Law in 2006, the government passed the mark of 250,000 loans in May of 2012 according to an unpublished government report (CONAMI 2012b). Both Minister Alicia Kirchner and President Cristina Fernandez Kirchner marked the occasion with a special press covered celebration/rally at the Bicentennial Museum in Buenos Aires (Visión Siete 2013).

While crossing such milestones is to be lauded, the question is whether reaching this mark after six years should be considered successful. As noted above, however, Argentina had the lowest number of borrowers for its size in the region. Argentina has expanded significantly more slowly than Brazil, Colombia, and Peru, where diffusion rates are 29, 117, and 270 times greater, respectively, than in Argentina (Table 1).

Number of Borrowers per 100,000 Population Reporting to Mix Market 2014

Source: Mix Market (2016), UNDESA (2016).

What are the main causes of this lack of dissemination, and are they tied to political considerations? Even absent a full comparative analysis in the region, some clues are evident through my interviews and other data. Most notably, the program has had a hard time keeping up with the required bureaucratic paperwork for OAs to receive their annual funding disbursement. One OA representative explained just how frustrating it was to wait for such second and third time funding remittance from the central government. He noted:

There may be political will, but the state is bureaucratic, and if you're not the nephew of [President] Cristina [Fernandez], or if you have a bad relationship with the Ministry [of Social Development], it's going to take longer. We had to wait for over two years to get refunded from CONAMI. That is two years without salaries for credit agents. 7

Interview F, Representative of NGO, Cordoba, 4 July 2012.

Another OA representative also noted that trying to run a program that is dependent on a state where funds do not arrive on time makes it exceedingly difficult to maintain services. He stated:

A credit agent may stay on for a month or two receiving no salary in the hope that the money from the federal government will be arriving soon, but these people have families to feed and cannot work for free. Thus, all the work of training them and all they learned during their first year of experience gets lost. 8

Interview G, Representative of NGO, Tucuman, 11 July 2012.

High level administrators of CONAMI admitted both in 2012 and in follow-up interviews in 2015 that problems of bureaucracy have plagued the program from inception, even as they claimed that resolving these problems was a priority for them and well on its way to being resolved (Gandulfo 2012; Solís 2015). They emphasized that heavy regulation was a necessary evil in order to prevent corruption and ensure accountability.

These outcomes are at least indirectly linked to the government's decision to structure and implement the microcredit program in the fashion it does. Other countries commonly regulate MFIs whose focus is solely on microcredit. These MFIs have a greater incentive to seek out other funds for their lending programs, and to build up their own funds over time from microlending. At times, subnational or national government agencies and/or regional or national development banks may offer a limited level of funds at partially subsidized rates (as is the case in various parts of Brazil). The restrictions of six percent annual interest rate and 30 percent of grants to cover operational costs – again, decisions based on leftist political concerns – undercut the spread of microlending in Argentina.

Another common outcome measure is to examine the repayment rate. For years, Yunus praised microcredit borrowers for their consistency in paying back their loans. Originally, the Grameen Bank typically experienced successful repayment rates of up to 97 percent. When these rates slipped down to 80 percent in the late 1990s, they adjusted their methodologies and performance improved (Dowla and Barua 2006). An unpublished CONAMI report from May of 2012 claims a repayment rate of 92 percent (CONAMI 2012b). Unfortunately, according to several of my interviewees, such a statistic seems unreasonable and unreliable in the case of Argentina. A former central administrator for CONAMI forcefully rejected the repayment rate as utter nonsense stating flatly:

I don't believe it. CONAMI doesn't do evaluations because there is no political will to do them. If CONAMI has a 92 percent repayment rate, and the average loan is for six months, and the program has been going on for at least five years, and with each successful loan an entrepreneur can increase the subsequent size of the loan, then at this point we should be seeing an average loan size of over 5000 pesos, and yet it remains at about 1500 pesos. So if all these people are paying back, where is all that money that has been paid back? In addition, CONAMI renews funding at 100 percent or more of the original amount. Why would they do that over and over again if entrepreneurs were really paying all that money back? 9

Interview H, Former CONAMI administrator, Córdoba, 5 July 2012.

Another OA representative noted that the repayment rate had fluctuated significantly with some periods as high as 95 percent, but with other periods as low as 50 percent. 10 Probably more telling, however, was the an interview with one OE director, who added:

Interview I, Representative of NGO, Tucumán, 11 July 2012.

We made a lot of mistakes in the beginning and truly it was a total loss. We had no idea what we were doing then like we do now. But we also knew that if we told CONAMI the truth, our entrepreneurs would not receive funding again. So we reported that all of the funds were paid back in full so that we could get a fresh set of funds to loan out again. 11

Interview J, Representative of NGO, Tucumán, 12 July 2012.

While the frankness of this latter interviewee is appreciated, it opens up the question of the integrity of the reporting system. If her group can have 100 percent failure rate, but freely admits that it reported 100 percent success to government officials, then clearly the bureaucratic delays in approving subsequent funding by CONAMI cannot be due to strong accountability mechanisms.

A third outcome for the program is sustainability. CONAMI claims to foster sustainability by subsidizing microcredit operations even while employing a limit of six percent annual interest rate. Beyond being too slow in the refunding process, one OA representative told me that the 70/30 ratio of capital funds to operational cost was still a major barrier to sustainability. He said:

Some of our OEs use a higher interest rate than CONAMI allows. They use 10 percent over six months. We allow them because we know it's necessary. CONAMI doesn't allow this, but CONAMI is not here in the trenches every day. 12

Interview K, Representative of NGO, Córdoba, 4 July 2012.

Another OE representative noted that his organization has access to funding from other sources that allow them to charge higher interest rates. He uses the funds generated from those lines to help cover operational costs of the CONAMI funds. In other words, were solely CONAMI funds and restrictions available to him, he would not be able to run the program. 13 The general consensus among interviewees is that the limit of 30 percent of funds for operational costs may be reasonable in some cases, but that the subsidy must be increased to 40 or even 50 percent in many cases to ensure sustainability.

Interview L, Representative of NGO, Córdoba, 17 July 2012.

Conclusion

This brief foray into the politics of microcredit policies suggests that partisan political considerations play a strong role in shaping microcredit policy design, implementation, and outcomes. The leftist Peronist government established a state-centered program that maintained extensive control over funding while dictating loan conditions that prioritized political considerations over economic viability. Implementation of the program was partially shaped by the political arena in which a large organized populist party was forced to respond to demands for patronage in order to maintain political support. Through its implementation, the government remained lax in its oversight, channeled funds to provinces and groups that were more in line with their specific ideological worldview, and was often unable to engender cooperation in locales led by its political opponents. In the end, these factors weighed heavily in limiting the impact of microcredit lending in Argentina compared to other countries in the region.

More broadly, this study points to the key factor of partisan politics, and how governments can “get in the way” of helping the poor in some cases (Warby 2016). Examining how microcredit policy can be harnessed (if not hijacked) to help support particular partisan goals or further a specific ideological project in the eyes of policymakers helps us understand how and why microcredit programs may experience limited success in some places. Moreover, understanding how local political interests and considerations intersect with those of other domestic and global actors in a more global context (Olsen 2010; Weber 2006) can lead to an honest evaluation of the real possibilities of microlending as a tool to reduce poverty and improve social inclusion. Studies of microcredit that do not appreciate the partisan political context in which actors and agents operate will likewise fail to elucidate the real possibilities and limits of reform and change.