Abstract

This study aims to investigate how the use of cyber-physical production systems (CPPS) in small manufacturing firms can facilitate the implementation of the activity-based costing (ABC) method in calculating production costs, thereby increasing the reliability of costing information for decision-making purposes. The collaboration between the research team and managers allowed an in-depth knowledge of the manufacturing problems at the investigated firm, facilitating the analysis of the manufacturing process through both a costing and a managerial perspective. Findings show that the integration of CPPS investments with the ABC method, through real-time measurement of resources by sensors, apps and part programs, leads to useful information about operations, allowing firms to improve performance and reduce resource consumption. As a result, a model of integration between the factory control system, communication network and production system is proposed.

1. Introduction

This paper aims to investigate whether the implementation of technological innovations in small and medium enterprises (SMEs) can facilitate the adoption of management accounting tools that yield more reliable data on production costs, execution time and the efficiency of the production process as a whole. The study focuses on engineer-to-order production processes, which are not standardised and whose starting point is an order received from a customer. Accordingly, these firms have to plan manufacturing activities, including design development, and must comply with due dates defined by customers, reducing production time. Furthermore, they need to estimate production costs correctly in order to have an adequate base upon which to define the price of the product. Therefore, it is important for firms to monitor activities, their execution time and related costs.

Technological innovations are rooted in the current industrial revolution, called Industry 4.0, 1 which aims to revise organisational structures and improve the efficiency of production processes by reducing costs and increasing service quality. This requires the implementation of cyber-physical production systems (CPPS) coupled with the Internet of things (IoT), which integrate hardware and software within mechanical or electrical systems designed for a specific purpose. 2 This technological innovation could revitalise a well-known management accounting methodology, activity-based costing. Indeed, the main disadvantages of the ABC method are the high cost of collecting data on production costs and the difficulty embedded in the selection and measurement of both resource and activity drivers. Traditionally, these drivers have been assessed through surveys with employees and managers 3 or have been identified ex-ante, 4 with a high risk of obtaining non-reliable data. Technological devices and sensors, data acquisition systems and computer networks, which provide managers with a high-volume of data on the manufacturing process, 5 allow circumvention of these obstacles, as they make it possible to estimate resource absorption correctly. Furthermore, this can allow costs to be allocated directly to a cost object, avoiding indirect allocation methods. Therefore, the information provided by the ABC system and based on CPPS data is useful for managers in controlling activities, their execution time and related costs.

This study relies on an interventionist approach, characterised by the direct involvement of researchers in concrete problems, aiming to solve them while contributing to the expansion of scientific knowledge. 6,7 The case of Stamec, an engineer-to-order firm located in the south of Italy, was investigated. This approach suggests adopting a critical perspective while interpreting the results in order to surpass a mere representation of the reality being investigated. Taking a critical approach means discussing results by seeking to generate new ideas and theoretical contributions, 8 following three steps: insight, critique and transformative re-definitions. 9

This study’s results offer interesting insights from three perspectives. First, they enrich the literature on the effects of CPPS implementation, documenting how these technological innovations facilitate better monitoring of production processes in SMEs by optimising the activities and resource consumption and increasing productivity. 10 Second, it provides evidence that integrating CPPS with the ABC method provides reliable and timely information which supports decision-making processes better than information obtained from traditional cost-accounting methodologies or the traditional ABC method. In fact, from a cost-accounting perspective, CPPS facilitate the collection of data, making possible a reliable estimation of production costs and aiding in the monitoring of the time needed to execute activities, which is crucial in engineer-to-order firms. Furthermore, CPPS allow circumvention of the disadvantages of the traditional ABC method, especially the high costs of implementation and maintenance in engineer-to-order production processes. Third, this study proposes a generalisation of the results emerging from the analysis by presenting a model consisting of three parts: the factory control system, the communication network and the production system where manufacturing process takes place. The integration of these three parts can be used to implement a new control system that helps SMEs deal with actual problems with production processes.

The remainder of the paper is structured as follows. Section two depicts the scientific background for the development of both industry 4.0 and management accounting methodologies and introduces the study’s research questions. Section three illustrates the research method, while section four present and discusse the case study. The last section discusses the results and concludes, highlighting limitations and future research trajectories.

2. Scientific background

2.1. Industry 4.0 and cyber-physical production systems

In recent years, we are witnessing a new industrial revolution called Industry 4.0. Based on revisited organisational structures and new technological challenges, Industry 4.0 aims to improve the efficiency of production processes, reduce costs and increase the quantity and quality of services. The following definition of Industry 4.0 (Industrie 4.0 in the original definition), provided by Hermann et al., 11 summarises the new paradigm for modelling and creating intelligent production systems:

Industrie 4.0 is a collective term for technologies and concepts of value chain organisation. Within the modular structured Smart Factories of Industrie 4.0, cyber-physical systems (CPS) monitor physical processes, create a virtual copy of the physical world and make decentralised decisions. Over the IoT, CPS communicate and cooperate with and humans in real-time. Via the IoS [Internet of services], both internal and cross-organisational services are offered and utilised by participants of the value chain.

CPS, IoT and IoS technologies play a key role in this definition. Adopting a definition for these terms general enough to be widely shared is no trivial matter. Greer et al. 12 list many definitions of CPS, each highlighting one or more aspects being studied. For the purposes of this work, the following definitions will be adopted.

The concept of CPS can be seen as an evolution of embedded systems, which consist of hardware and software integrated within a mechanical or electrical system designed for a specific purpose.

2

CPS comprise interacting digital, analog, physical and human components engineered for function through integrated physics and logic. These systems will provide the foundation of critical infrastructures, form the basis of emerging and future smart services and improve the quality of life in many areas.

13

The main characteristic of CPS is their ability to merge the physical and virtual worlds. In particular, through their embedded software, CPS are able to do the following: Capture data from sensors and store it in local servers or in cloud architectures; Drive physical processes using actuators; Connect themselves with other CPS; Interact with machines as well as human beings; Provide a real-time response to stimuli generated both from the surrounding environment and the CPS itself.

A new generation of smart systems can be built on the conceptualisation of CPS, whose economic impact will grow considerably in the coming years. Disruptive technologies emerging from the combination of the cyber and physical worlds 14 will create entirely new markets and platforms for growth. Some of the most important application domains of CPS are manufacturing, transportation, infrastructure, health care, emergency response and defence.

Focusing on the manufacturing application domain, we shall refer to the specialisation of CPS described by Kagermann et al., 15 cyber-physical production systems (CPPS): ‘CPPS comprise smart machines, warehousing systems and production facilities that have been developed digitally and feature end-to-end ICT-based integration, from inbound logistics to production, marketing, outbound logistics and service’.

The distinction between CPPS and CPS is that in CPPS, the role of manufacturing systems, integrated with ICT systems, can offer new services to manufacturing industry stakeholders. This role is also underlined by Monostori, 16 who discusses how CPPS, relying on the newest and foreseeable further developments of computer science, information and communication technologies, manufacturing science and technology, may lead to the Fourth Industrial Revolution.

The second key concept in the definition of Industry 4.0 is the Internet of Things (IoT), declined in its industrial specialisation of the Industrial Internet of Things (IIoT). Several definitions of IoT have been proposed, each trying to put into evidence one or more characteristics. 12 The following definition provides a convenient conceptual base for the concept of IIoT 17 : ‘The Internet of Things is a network of physical objects – vehicles, machines, home appliances, and more – that use sensors and APIs to connect and exchange data over the Internet’.

Sisinni et al. 18 remark on the difference between IoT and IIoT. The two concepts are closely related, but they cannot be used interchangeably. Given IoT’s numerous application fields, a more specialised definition is necessary for its application in manufacturing. Essentially, IIoT can be seen as a specialisation of IoT in manufacturing; indeed, the Industrial Internet of Things is about connecting all industrial assets, including machines and control systems, with information systems and business processes.

Looking at industrial software applications, the trend is to implement web services, autonomous software components that are uniquely identified by a universal resource identifier (URI) and can be accessed using standard Internet protocols. 19 The service orientation of Industry 4.0 is one of the six principles for its implementation, as mentioned in Hermann et al. 11 As discussed in Schroth and Janner 20 and Reis and Gonçalves, 21 IoS technology was derived from the convergence of other two concepts: Web 2.0 and service-oriented architecture. Such technologies allow us to describe, revise and adapt the characteristics, functions, processes and usage patterns of customisation targets on the basis of machine-understandable content representation, enabling automated processing and information sharing between human and software agents. 22

The terms IoT and IoS are also combined in the Internet of Things and Services. 23 These technologies involve resources, information, objects and people brought together to create networks, incorporating the entire manufacturing process that converts factories into a smart environment.

2.2. The ABC costing method

A cost-accounting method aims to support strategic planning and decision-making processes, 24 providing managers with useful cost information with which to formulate plans and operate controls. Costing methods change over time to take into account modifications in manufacturing processes that change a firm’s cost structure. 24 In the last decade of the 20th century, Cooper and Kaplan 25 developed activity-based costing (ABC), a method focusing on the activities that are consumed by the product. Therefore, while direct costs are directly traced to cost objects, the ABC method uses a two-stage allocation process to allocate manufacturing overheads to cost objects.

In the first stage, costs of activities are calculated by assigning them manufacturing overhead costs using ad hoc allocation bases named resource cost drivers. Therefore, at the end of this stage, the cost of each activity supporting the production process is known.

In the second stage, costs of activities are allocated to cost objects using specific activity-cost drivers (transaction, duration and intensity drivers 25,26 ) and an overhead rate based on the cost per unit of activity driver. The activity cost driver estimates the cost of an activity consumed by a cost object (cost per unit). These activity-cost drivers are not volume-related, as they reflect the demand of each activity by the cost object. Other (non-manufacturing) overheads are then allocated to cost objects using an ad hoc allocation basis.

In the rest of the paper, we focus on direct costs and manufacturing overheads as they are strictly related to the production process. It is worth observing that the ABC method selects activity-cost drivers using the different levels of activities, including unit, batch, product and facility-level activities, 25,26 in order to have a better understanding of the expenses at each activity level. 27 The main disadvantage affecting ABC 28 –30 is the collection of data on activities, which is very time consuming and costly. 31 To overcome this and other ABC disadvantages, new technologies such as IoT and CPPS could be exploited 32 to create value and reduce production costs by monitoring the consumption of resources 33 in real time.

2.3. Research questions

As already noted, one of ABC’s main disadvantages is the high cost of collecting data. This is particularly true for SMEs, where ABC implementation has been less frequent 34 because of the perceived high cost of development and implementation. 35 More generally, SMEs lack access to technologies and have little knowledge about modern accounting techniques, limiting their growth on the worldwide market. 36 However, the economic instability related to the worldwide financial crisis has incentivised SMEs to change, focusing more on manufacturing processes 36 to improve their profitability 37 and reducing idle capacity, an expense impacting the bottom line through the ABC method. In this way, managers can make all efforts to reengineer manufacturing processes, using excess capacity to minimise production costs. 36

Indeed, ABC requires not only architectural changes and software design. To be effective, it also requires behavioural, organisational and administrative changes. 26 The implementation of CPPS would support such changes: sensors, part programs, Human Machine Interface (HMI) and mobile app gather considerable data on production process flow (e.g. the consumption rate of resources such as cost of employees, energy, raw materials, services, etc.). Managers can use this data to detect and optimise no-value added activities. 38 CPPS allow managers to calculate the cost of each order exactly, to monitor the length of the production process and estimate the delivery date reliably because it provides real-time measurements of the consumption rate of resources and the execution time of operations. With more reliable information incorporated into their decision-making processes, SMEs can improve their efficiency and profitability. 36 Additionally, data collected by CPPS can be used by ABC to analyse and reduce the cycle time, another critical issue of a firm’s strategy, other than the optimisation of activities and resource consumption, 10 impacting on production cost. These issues are particularly relevant when the production process is not standardised, as in the engineer-to-order type; in such cases, a careful cost estimation is required for each order during the negotiation phase so that a competitive price can be proposed.

On this basis, it can be hypothesised that investments in CPPS can facilitate the implementation and maintenance of the ABC method,

39

leading to several benefits from both a costing and a managerial perspective. The research questions this study aims to investigate are thus as follows:

3. Theory and research methods

This study focuses on a collaboration between the research team and the management of an engineer-to-order industrial firm, Stamec, with the management team serving as ‘an active participant in the process being researched’ (p. 152). 40 As will be explained further in the following section, Stamec had to solve a central issue: how to accurately calculate and manage the costs of orders placed by customers, how to negotiate the prices and how to control the timing of production. Accordingly, an interventionist research approach was adopted to solve practical problems while expanding scientific knowledge. 6,7

The interventionist research team cooperates with the organisation’s managers, with the main aim being to develop solutions to problems jointly. In this way, benefits are expected to be obtained both by practitioners, who can rely on the collaboration and knowledge of researchers, and by researchers, who can develop insights into the implementation of managerial innovations. 41 –44

One member of the research team has been collaborating with Stamec top managers since 2016, contributing to the analysis of the potential benefits deriving from more intense use of technological solutions to solve specific manufacturing issues. Subsequently, the research team started to investigate production processes in more depth from September 2018 onwards. As a consequence, the researchers have been perceived throughout the process as ‘insiders’ 45 as they are well known among the managers involved both in preparing projects to be submitted to potential customers and in forecasting the related costs. The researchers’ collaboration was intense: They were involved in the main steps of the analysis of the economic convenience of orders, addressing technological, managerial and cost-accounting issues.

Data were collected through participant observation, with researchers participating in several meetings with managers and their staff. Additional data were collected from internal documents and reports, which were analysed thoroughly to gain a complete understanding of the context for decision making. Finally, several informal talks with managers were held to help researchers gain additional information and perceive managers’ perspectives on the innovations being implemented.

Researchers discussed all of the information collected through the sources mentioned above (participant observation, document analysis and informal talks), implementing a triangulation process. Triangulation leads to a more reliable interpretation of the emerging output and allows researchers to compare personal feelings with information collected through documentary analysis. Furthermore, researchers were able to uncover both managerial and technological issues arising from the implementation of strategic innovations. In doing so, a critical perspective was used, with the aim being to distinguish the method adopted in the actual research project from the methodology employed in analysing interventionist research. 46

The researchers have retained this critical perspective when necessary. Indeed, they sought to avoid the risk that the interventionist approach could be retained as a mere methodological procedure implemented to generate more accurate representations of reality or to capture the experiences and meanings of people. Following Alvesson and Sandberg 8 (p. 23), critical management research is supposed ‘to discuss ways of generating interesting and potentially influential new ideas and theoretical contributions’. Accordingly, from a theoretical perspective, results have been investigated by referring to three pillars 9 : insight, critique and transformative re-definitions.

Insight means achieving a hermeneutic understanding of specific problems embedded in real situations, to unveil the different ways in which particular events are formed and sustained. Accordingly, section 4.1 set the scene by investigating both the technological and the management-accounting sides of the engineer-to-order production process, to understand if and how strategic innovations can influence key actors and their organisational routines.

Critique aims to avoid taking for granted that strategic innovations provide only benefits, so researchers are expected to disclose and understand any potential resistance to change and the related potential disadvantages. Accordingly, section 4.2 illustrate the implications of the integration of CPPS and ABC, examining the advantages and disadvantages for Stamec from both a costing and a managerial perspective.

Transformative re-definition aims to develop ‘managerially relevant knowledge and practical understandings that enable change and provide skills for new ways of operating’ 9 (p. 19), supporting managers in developing both practical understanding and critical knowledge and enabling changes and improvement of skills for new ways of operating. Section 4.3 deals with these issues by proposing a model for a generic manufacturing process which aims to generalise the results of the analysis.

4. The case of Stamec

Stamec was founded in 1969, a family industrial company based in Avellino, in the south of Italy. Stamec produces moulds for pressure die-casting, injection moulds for plastic, permanent moulds for gravity and low-pressure casting. Moulds and other semi-finished products are mainly obtained through an engineer-to-order production process, while only a small portion of the production is devoted to the market. A mould is a combination of several parts. Some of the parts are purchased from suppliers, while others are produced internally according to the client’s requirements. This study focuses on these parts, as Stamec must make all efforts to deliver an order by the due date (imposed contractually by the customer) and at a profitable price. The traditional cost-accounting method, utilised by Stamec to calculate the cost of an order, does not reveal to managers the hidden sources of firm profitability and embedded costs, and it does not allow them to control the production flow to optimise the production time within the scheduled delivery time.

4.1. Insight

Figure 1 provides a concise view of the Stamec production process, which can be divided into two main phases: engineering and manufacturing. Information was obtained by interviewing the production manager and workers, as well as through internal documents.

The production process in Stamec.

The analysis of the manufacturing process allows for the identification of bottlenecks or critical points to remove by classifying activities as ‘value added’ or ‘no-valued added’. Any delay or redundancy in the manufacturing process can cause a delay in the client’s specified delivery time and an increase in the full cost because of abnormal resource consumption (the no-value added activities). As a consequence, the starting point to improve the firm’s performance is real-time monitoring of the overall manufacturing process in term of resources absorbed and time requested to complete each step of the production process. Therefore, the research team and Stamec’s production manager analysed carefully the overall manufacturing process (Figure 1) and identified the critical activities to monitor, specifically two steps in the manufacturing process. The first step is ‘engineering’, in which Stamec receives an order from a customer and begins its technical and economic assessment. Currently, Stamec’s financial manager estimates the full cost of an order using the traditional cost-accounting methodology based on standard costs. The main concern of managers is to contain the real production cost within the selling price, leaving the expected gross profit. Without reliable and real-time information on the production process, the cost containment is difficult to realise. Once the customer accepts the proposal, finding that it meets technical and economic expectations, engineers prepare the Master Acceptance Schedule (MAS), a document showing all details on the production process. At the same time, the purchasing office buys raw materials. The MAS is the first tool to monitor the production process as it drives machines.

The second phase, production, includes the production process and the (real-time) monitoring process undertaken to ensure that quality and execution time are respected. This phase, in its turn, can be further divided into processing and assembly operations. Processing operations may be identified by the machines that use resources to transform an input into an output. In this stage, the production process is largely automated and controlled by machines. Workers limit their work to controlling the flow of the inputs and outputs through the machines. The assembly process is the second stage of the manufacturing process at the shop floor level and is carried out by workers, who assemble the separate parts (as the output of the automated processing operations) into the finished goods (the order) to be delivered.

Having analysed the production process, the managers and the research team discussed two critical issues: time constraints and the reliability of estimated production costs. The first issue concerns the ability to deliver finished goods at the time specified by the customer, as any delay can be costly for the firm. The second issue concerns the calculation of reliable production cost information along with the entire production process.

The production manager emphasised that, in an engineer-to-order production process, the main issues are complying with the established quality criteria and delivering the mould on time or ahead of schedule. Therefore, strict controls over each production phase are critical. The production manager showed awareness of the need to implement ad hoc strategic innovations aimed at both improving product quality and respecting the scheduled time of production: Our first problem consists of adequately controlling the quality of the output of each step of the whole production process. The second issue concerns the time required by each step, to be compared with the scheduled time. Our production processes are characterised by a low level of standardisation, so taking decisions based on reliable data is essential to assess both the quality and the time adequately. (Production Manager) Our production processes are not standardised, as they depend on the specific requirements of customers. This means that the estimation of costs to be incurred to produce moulds is not an easy task. However, an accurate estimation is necessary, as it is the basis of the negotiation with customers. We are utilising a traditional cost system, estimating production costs through a “rule-of-thumb” approach (namely a standard-based procedure), but it does not provide a reliable measure of production costs in our engineer-to-order processes. (Financial Manager).

The research team assisted managers in planning and implementing these innovations, and it suggested combining them with the implementation of a revised version of the ABC method. Indeed, even though the production processes at Stamec were not standardised, the adopted approach was essentially based on standard procedures. The financial manager retained traditional cost methods which, having been designed for standardised processes, were inappropriate. Stamec needed a costing method focused on the products, as ABC does. The implementation of strategic innovations in line with the CPPS paradigm can facilitate the utilisation of the ABC method.

4.2. The integration of CPPS and ABC

The research team sought to demonstrate that ABC and CPPS could remove the concerns of both the production and the finance manager, who were aware that the approaches used at Stamec were not completely adequate but still resisted change, believing ABC too complex to implement and manage. Therefore, the research team proposed a pilot test, implementing the ABC method on a milling operation to demonstrate that more reliable data can be obtained, both in an ex-ante and ex-post perspective, to support decision-making processes. This step of the manufacturing process was selected because one of the milling machines was the first to be vested by sensors. The effects of this integration are analysed from both a costing and a managerial perspective.

Costing perspective

From a costing perspective, the analysis focuses mainly on the relevant topics influenced by CPPS. The analysis was carried out both ex-ante and ex-post to assess the reliability of the data. Moreover, a comparison was also made with ex-ante and ex-post data obtained using Stamec’s traditional costing methods. To save space, only the main results of the pilot test are illustrated.

Supported by Stamec’s administrative office, the research team gathered data from sensors, part programs, human machine interface (HMI) and mobile apps, and were able to analyse accurately the cost of resources absorbed by the milling activity and a possible relationship with the cost object. Part programs run on the computer numerical control (CNC) processor of a production machine to execute step by step the instructions that drive the machine to operate on a work part. The running interval of a part program is registered by the CNC so that the exact duration of a machine cycle can be automatically determined. The machine is also equipped with a personal computer, on which interactions with the worker operating the machine occur by means of the HMI software. Whenever there are no other possibilities for automatic data collection, mobile apps are used. Such is the case in assembly operations, which are frequently performed by workers in a dedicated area far from the production machines. In these circumstances, a worker adopts a mobile app to record relevant data about the production process.

In assigning the direct costs, the research team identified, with the support of the production and financial managers, three main operations needed to mill a work part (Table 1). This made it possible to control the time consumed by each step. Stamec’s control system gathered and continuously recorded time and cost performances. In addition, each operation, if needed, was articulated in sub-operations to allow a more in-depth control of cost absorption. For each sub-operation, a sensors part program, HMI and apps measured the time required to transform a given work part. Direct costs were calculated by multiplying the quantity of the resources absorbed by each operation/sub-operation by the unit cost of the resource. This cost information was provided by the financial manager and estimated according to the practical capacity.

The data collection devices allowed automatic measurement of the resources consumed by the operations under investigation. Therefore, a significant portion of the cost of the resources required to mill a part could be traced directly to cost objects. Among these costs, electric power (which was considered an indirect cost under Stamec’s traditional approach) was also considered direct, as an energy sensor was used to measure the exact consumption during a machine work cycle. Table 1 illustrates direct costs arising in this step. Start/stop events triggered by a worker were recorded by HMI software and smart apps.

Direct manufacturing costs traced to a part during the milling operation.

The cost of the resources is expressed in cost per minute (or Kwh per minute) because time allows the exact cost of resources to be traced to cost objects.

Table 1 shows that the direct costs of resources absorbed to mill a part are € 46.75. The cost of other resources cannot be traced directly to the cost object (the order) as a direct relationship is not clearly identifiable. Therefore, using the ABC method, these costs are allocated through two stages, as described in section 2.2.

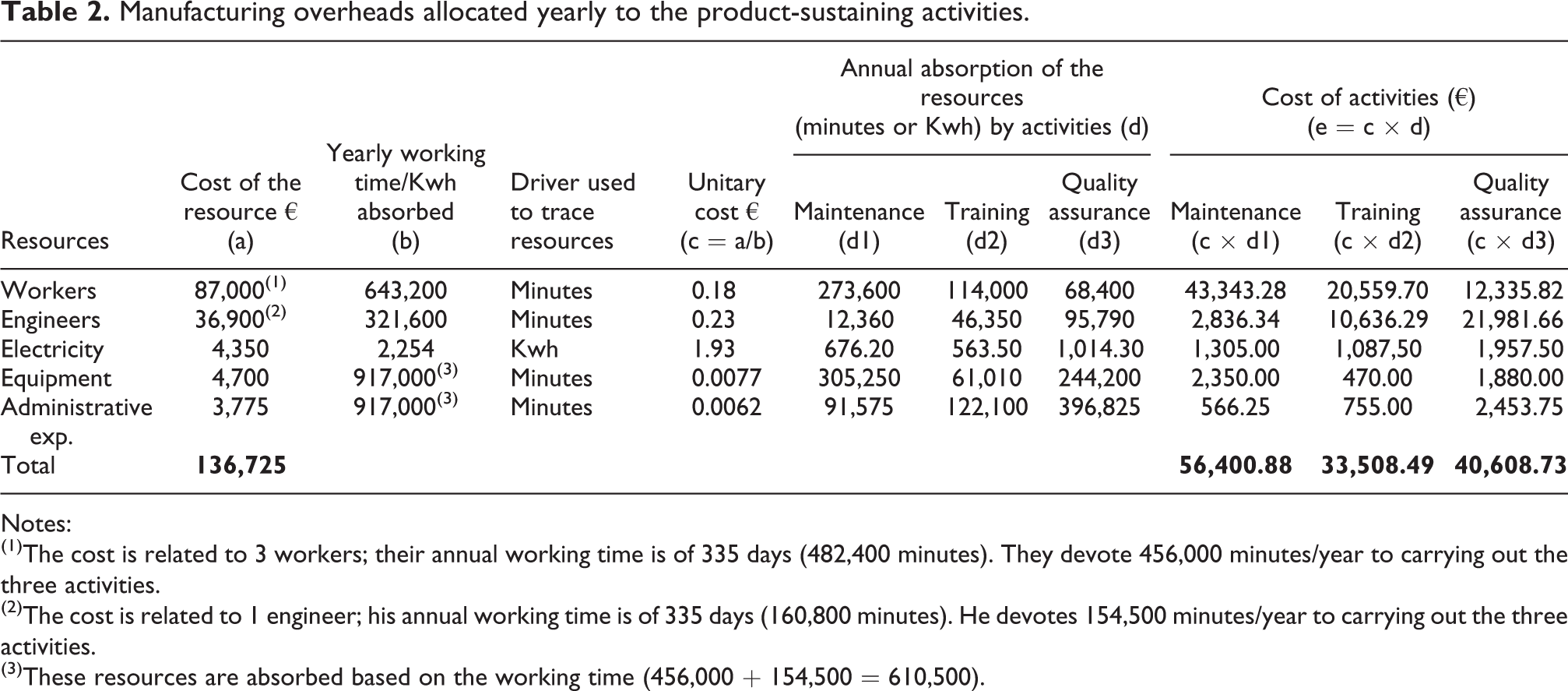

The first ABC stage consists of allocating manufacturing overhead costs to the sustaining activities supporting the manufacturing process. In the pilot test, three product-sustaining activities were mapped, ‘maintenance’, ‘training’ and ‘quality-assurance of the whole manufacturing process’. CPPS also allowed the costs of resources to be traced easily to each activity using the machines’ time, the workers’ time and the electricity power absorption recorded by Stamec’s information system. Based on these figures, the research team, supported by the financial manager, calculated the annual cost of each activity by tracing the costs of the following resources involved in carrying out the sustaining activities: workers (including engineers), the electricity power consumed by machines servicing sustaining activities, equipment depreciation and administrative expenses. The drivers used to trace the costs of these resources to the three activities were the cost per minute for employees, equipment depreciation and administrative expenses; kilowatt hours (Kwh) were used to trace the cost of electricity power. Table 2 shows how the manufacturing overhead costs were traced to sustaining activities.

Manufacturing overheads allocated yearly to the product-sustaining activities.

Notes:

(1)The cost is related to 3 workers; their annual working time is of 335 days (482,400 minutes). They devote 456,000 minutes/year to carrying out the three activities.

(2)The cost is related to 1 engineer; his annual working time is of 335 days (160,800 minutes). He devotes 154,500 minutes/year to carrying out the three activities.

(3)These resources are absorbed based on the working time (456,000 + 154,500 = 610,500).

In the second ABC stage, the costs of activities (Table 3) are allocated to cost objects using specific activity-cost drivers. The research team decided to use operation execution time as a driver, as sensors, part programs and apps can measure it accurately and in real time. The advantage of such a system is that the activity cost rate is not predetermined but also measured in real time. Table 3 shows the second stage of ABC.

Allocation of the costs of the sustaining activities to the cost objects (a part).

Notes:

(1)See Table 1.

Actually, Stamec allocates indirect costs to cost objects using cost standards, calculated using the working time of workers as the allocation basis. This leads to wrong costing information, as the worker time also includes the time the worker spends carrying out other jobs, allocating unabsorbed resource costs to the cost object.

Finally, to calculate the full cost of the part at the end of the manufacturing step (Table 4), other overhead costs must be added to the direct costs (immediately traced to the cost object).

Determination of the full cost of the milling operation.

The other overhead costs were allocated to the cost object using the time to work (91.4 minutes) a part as a cost driver. Finally, the cost of the part after the milling activity was found to be € 1,913.44. Comparing this cost information with the information obtained by the traditional cost-accounting method typically used by the firm, the managers noted an enhancement in the cost information in term of reliability, timeliness and relevance for decision making.

Managerial perspective

The methodology illustrated above was implemented in an ex-post perspective, measuring the actual time of production and assessing ex-post costs. This data was then compared with ex-ante data so to have strict control over the ability to respect the scheduled time. Furthermore, data obtained during the pilot test were used to forecast the time and costs of production, simulating the decision-making process. This leads to defining the price to be negotiated with a customer. In this, it is possible to develop a business analytics system fuelled by the integration of CPPS and ABC. Table 3 shows that the indirect costs allocated to a part are higher than direct costs. This indicates that Stamec should make all efforts to enhance CPPS in measuring all steps of the manufacturing process, including those related to the sustaining activities.

From a managerial perspective, the availability of time information, as measured by sensors, part programs and apps, allows the production manager to compare the scheduled time with the real time in each stage of the manufacturing process. If relevant differences exist, the production manager can re-engineer the manufacturing process by removing any bottlenecks in the production process which threaten to delay the order or increase production costs. Furthermore, this data can converge in a decision support system, helping product and finance managers undertake actions to improve all steps of the production process. The integration of CPPS and ABC can help Stamec continuously monitor the efficiency and effectiveness of the production process as a whole. Managers can focus more on value-added data organised by a system of business analytics. As a consequence, a communication network between the factory control system and the manufacturing process can be useful as it allows data to be gathered from sensors, part programs and apps to support the management’s decisions and eliminate concern about delivery time.

Indeed, managers determined that data gathered from the pilot test seemed to be more reliable and detailed than that provided by Stamec’s traditional costing method used, finding that it improved the decision-making process and allowed real-time control of the cost flow at each step of the manufacturing process.

4.3. Transformative re-definition: A proposal for a CPPS model

Despite the pilot test’s positive results, the production and financial managers argued that a more comprehensive implementation of the described methodology would require time and further effort. Therefore, the research team supported the workers and managers in improving their practical understanding and developing critical knowledge, with the main aim being to enable changes and enhance skills for new ways of operating. 9 Indeed, the benefits offered by the realisation of CPPS include better management of planning and control systems in terms of compliance with delivery times, reduction and control of costs and increases in quality.

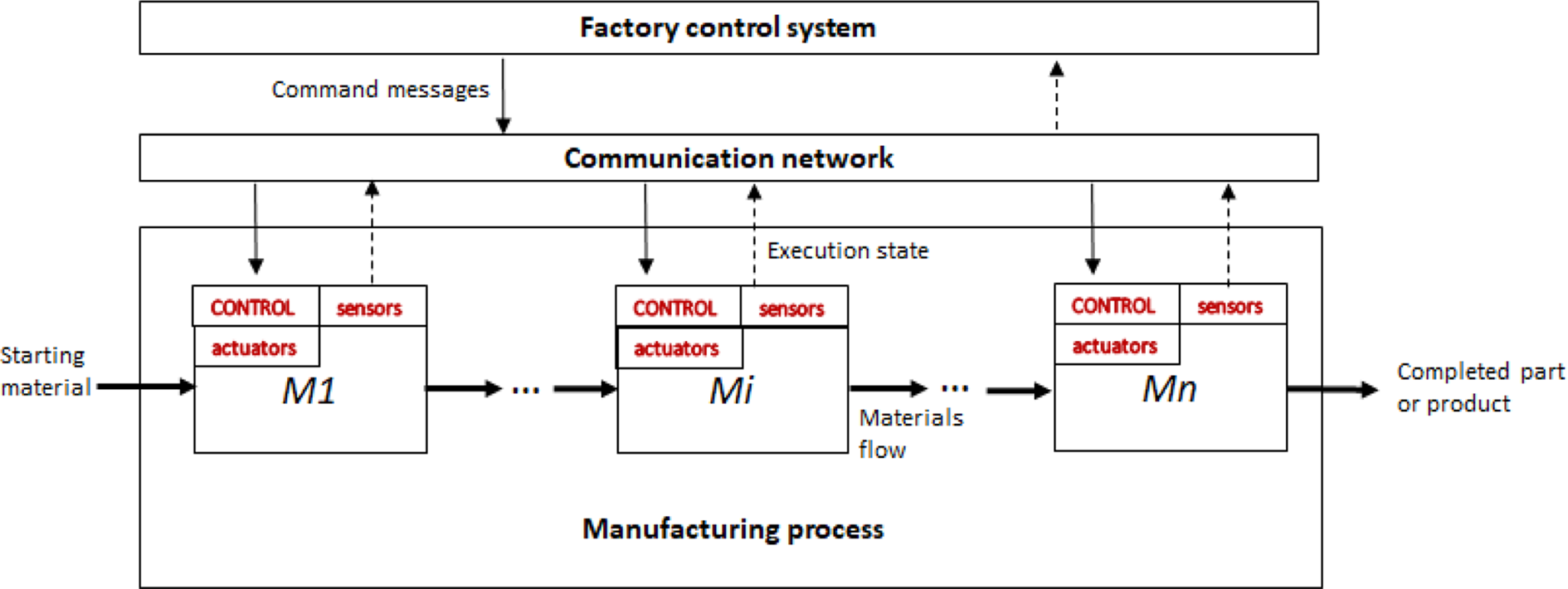

The research team then proposed a model for the implementation of CPPS at Stamec (see Figure 2). The model consists of three main parts: the factory control system, the communication network and the production system where the manufacturing process takes place.

Production planning and control for a generic manufacturing process.

The planning function of the factory control system generates command messages (represented by thin arrows in the figure) which, through the communication network, reach the resources in charge of the command execution. For example, a part program generated by computer-aided design and computer-aided manufacturing (CAD/CAM) software is sent to a machine Mi so that its control logic (the part program executed using the computer numerical control on Mi) can drive the electromechanical components of Mi to do the job, starting with the input material. Another example concerns a command message directed to a worker, such as a work order to be carried out during the day. To act as a control system, the CPPS needs that execution data be collected as the process advances. Execution data captured by the sensors (parts of the implemented IIoT) are sent (dashed arrows) via the communication channel to the factory control system. Here, the feedback loop is closed, and feedback actions can eventually be taken through comparisons between planning data and execution data.

From the perspective of cost control using the ABC method, the main concept to consider is the operation of a manufacturing process. As stated above, it is usual to distinguish between:

a processing operation, which uses energy to alter a work part’s shape, physical properties or appearance to add value to the material; and

an assembly operation, in which two or more separate parts are joined to form a new entity.

In Figure 2, a processing operation is performed by the generic machine Mi, either in a fully automated mode or as a worker-machine system in which a human worker operates powered equipment.

In Stamec, assembly operations are executed by workers with the aid of powered tools. To be compliant with ABC terminology, in the following, the term ‘operation’ will be used alongside the more general term ‘activity’. In Figure 3, the abstract view of a generic operation is taken into consideration together with the production factors necessary for its execution. The concrete elements of the physical world necessary for its execution are located in the physical layer.

Logical links between the abstract view of an activity and its concrete implementation for an ABC monitoring and control system.

The figure highlights the role of IIoT devices and of IoS applications that extend the traditional worker-machine system. The logical links between the concrete element of the physical layer that implement a particular aspect of the abstract view of an operation are also shown. For example, one of the activity cost drivers of an operation is the power required for work, estimated by the time required by a machine to complete the work. Therefore, the power consumption is measured precisely using a power sensor. In this way, the used capacity is measured; moreover, the web services made available by the power sensor module allow the transfer of consumption data to the ABC planning and control software application that runs in the application layer. A particular role is played by the control unit made by the CNC, the part program and the related web service. As a matter of fact, the control unit can record the time interval [START, STOP] during which the part program is in execution; this allows a firm to estimate the contribution of the machine and workers to the operation cost. Indeed, the human cost of the execution of a part program may be only a fraction of the total cost of one worker (or multiple workers) on the operation; related costs could include, for example, loading and unloading parts and machine setup. In this case, a worker’s time is evaluated using a personal computer near the machine or a smart device such as a mobile phone or tablet. As an example, Figure 4(a) shows the screenshot of an HMI as a worker-machine system executes a production order. By means of a start/stop button, the worker can interact with the HMI, signalling to the ABC planning and control system the time interval in which the machine remains in the states of LOADING, OPERATING, PAUSE and UNLOADING. The HMI is as simple as possible so that the data entry activity (pressing a button) is minimal for the worker operating the machine. In Figure 4(b), the trends in voltage and current absorbed by a machine are shown. The voltage and the mean current values combined with the duration (running time) of a part program provide the energy consumption for a given operation.

Data collection in a CPPS: (a) Downtime and operational time of a machine; (b) voltage and current trends measured by an energy sensor.

The purpose would be to collect real-time execution data in order to calculate with a high degree of precision the costs of all the production factors (resources) necessary to execute the operation.

5. Discussion and conclusions

This study has investigated the integration of technological innovations (CPPS) and management-accounting methods (ABC) in SMEs, focusing on engineer-to-order processes. Through an interventionist approach, two main issues have been investigated.

The first concerns the usefulness of the ABC methodology in this specific context. Indeed, resistance to change were identified. ABC was perceived to be a complex and costly methodology that would be inadequate in an engineer-to-order production process. During the first steps of collaboration (insight), the research team analysed in depth the characteristics of this production process, as well as the approaches Stamec was utilising at the time. Critical analysis was thus carried out to understand if and how CPPS could simplify the implementation of the ABC methodology. Furthermore, benefits deriving from CPPS were scrutinised to understand how they could improve product quality and support the production process in complying with time constraints and cost calculations. To overcome resistance to change, a pilot test was carried out. Results have been largely appreciated by Stamec’s management, who have significant incentives to implement the ABC costing system alongside CPPS technologies, as this combination would allow them to concentrate on offering quality products at competitive prices. However, certain complexities persist.

In attempting to generalise our findings, it is worth noting that the integration of CPPS and ABC leads to concrete advantages from both a costing and a managerial perspective, which relate to the first and the second research question, respectively. First, CPPS have reduced the complexity of the ABC method, as hypothesised. CPPS allow data to be gathered and recorded in real time at each stage of the manufacturing process. As a consequence, the implementation and maintenance of the ABC method have been substantially simplified. Therefore, from a theoretical perspective, this study’s findings enrich the literature on the effects of CPPS implementation, documenting that technological innovations make it possible to monitor production processes better, in SMEs as well as in other types of firms, by optimising activities and resource consumption and increasing productivity. 10 Furthermore, it is worth recalling that, while the vast majority of previous studies have dealt with standardised production processes, this study focused on engineer-to-order production processes. These are not standardised, as the production process starts when an order is received, requiring the firm to plan manufacturing activities, including design development, and comply with due dates defined by customers. Therefore, the need to monitor activities, their execution time and related costs is particularly important in this kind of production processes.

Second, integrating CPPS with the ABC method provides more reliable and timely information compared to that obtained from traditional cost-accounting methodologies or the traditional ABC method. CPPS facilitate data collection, making possible real-time monitoring of the time it takes to execute activities, which is crucial in engineer-to-order firms. According to Dumay and Baard, 47 the implementation of an ABC method per se could be classified as a moderate level of change along a continuum from weak to strong interventions. 45 However, integrating ABC with the implementation of strategic innovations, such as those based on CPPS, supports the decision-making process better, leading to a more intensive level of change.

As a result, implementing technological innovations can lead to several benefits from different but related viewpoints; therefore, a holistic perspective is required. In this respect, this study has proposed a generalisation of the results by presenting a model to show all the benefits that can derive from CPPS as well as from the integration of CPPS with the ABC system. This model, which consists of three parts (the factory control system, the communication network and the production system where the manufacturing process takes place) can be used to implement a new control system, helping SMEs deal with actual problems in production processes. The aim is to provide skills for new ways of operating in accordance with the transformative re-definition task of the interventionist approach. 7 This is an important contribution to the management accounting literature; by ascertaining product costs and operation execution time during the manufacturing process, all interested parties within the firm can base their decisions on real-time information, complying with the ‘strategic ABC’. 48 As a consequence, they can react to any lack in the manufacturing process, reducing its complexity. 39 Furthermore, the implementation of the proposed model in different contexts can help firms integrate manufacturing and marketing strategies. 49 Indeed, as the Cerved Report (2019) 50 shows, manufacturing SMEs are investing in manufacturing innovations and new technologies, including information technology, 51 to increase profitability. Therefore, this study’s findings can be also extended to other manufacturing SMEs, which in many countries represent a significant proportion of the total number of manufacturing firms. (For example, in Italy, there were 68,943 manufacturing SMEs in 2018, representing 31.3% of the total number of firms. 50,52 )

This study is not free from limitations, which can be addressed in future research. First, the analysis of the benefits of integrating CPPS and ABC was carried out through a pilot test. More widespread implementation of the ABC method would offer more complete data to assess its benefits. Second, the study focused on engineer-to-order production processes. Future studies could investigate other kinds of processes, taking into account that digital business strategies currently implemented by firms are affecting other areas, such as marketing and supply chains.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: MISE project ‘SMART INDUSTRY 4.0’ n. F/050493/01-02/X32, decree MISE n.5195 del 19/12/2017.