Abstract

Microfinance refers to the provision of financial services like saving, microcredit, and insurance to the poor who have limited access to traditional banking services with the aim of reducing their poverty. However, in the last decade, the literature stresses that the microfinance institutions focus more on their profit rather than the customer. Numerous methods have been used to model customer satisfaction in microfinance. However, a large majority of these methods is unable to take into account complex interactions and dependencies between variables. They may also find difficulties in handling limited and uncertain knowledge. The objective of this article is to model the effect of microfinance-lending process operations on overall customer satisfaction. We managed to develop a fuzzy Bayesian networks model; such an approach is widely required for modeling complex systems characterized by sparse or uncertain information as well as for conducting the cause and effect analysis.

Introduction

One distinguishing feature of microfinance compared to traditional finance is the target customers. 1 Poor people need access to financial services to reduce their vulnerability, to meet anticipated and unanticipated needs, and to take advantage of opportunities as they arise. Thus, targeting poor people with inappropriate products and services is likely to damage their interests. Kanyurhi 2 notes that one of the most important reasons for which microfinance industry loses customers is its failure to satisfy their needs. Customer satisfaction is achieved when the actual perceived quality surpasses the consumer’s expectations. 3 Customer satisfaction results from designing appropriate products and services, as well as the efficiency and effectiveness of the processes creating them. 4 Customer satisfaction is a key performance indicator for any business managers as it is considered as a basis for securing market position and attaining the institution’s objectives. 2,5 As per Kralikova, 6 modeling and measuring customers’ satisfaction is one among the central points of discussion in the microfinance industry. Understanding customer satisfaction determinants helps microfinance institutions (MFIs) to improve client retention, fulfilling their social mission as well as to enhance their financial performance.

Numerous techniques and methods have been used to analyze customer satisfaction in microfinance sector. These include descriptive statistics, analysis of variance, factor analysis, regression analysis, and structural equation modeling. 2,6 –12 A large majority of these methods is unable to take into account complex interactions between variables and may find difficulties in handling limited and uncertain knowledge.

The purpose of this study is to model the effect of different microfinance-lending process (MLP) operations and activities on the overall customer satisfaction using a fuzzy Bayesian networks (BNs) model. BNs are very suitable for this study as they can include different factors, model the complex interactions between them, and show their effect on the factor of interest. BNs is also a valuable tool for representing and analyzing uncertain knowledge. 13 Tarantino and Cernauskas 14 confirm that BNs are crucial when modeling processes characterized by scarce or missing data; they can also help managers determine the most serious risks within a such kind of processes.

The remainder of the article is organized as follows: The next section provides a general idea about customer satisfaction determinants in microfinance sector, especially those related to the MLP. The third section provides a theoretical background of the BNs. The fourth section introduces the proposed model and presents the results of the study. Finally, the fifth section concludes and gives some perspectives for future research.

Customer satisfaction determinants

Customer satisfaction can be seen as a result of an interaction between different factors. It depends on the loan product design, the quality of service related to it, and the customer’s characteristics as well. 2,6 The key elements of the product design include maximum and minimum loan amount, grace period, loan maturity, effective interest rate, payment schedule (monthly or seasonal payments), guarantee requirements, loan type (group lending or individual lending), and the size of the initial loan. Wright 15 sets that many MFIs lose their customers mainly because their products do not suit them. A product needs to be designed based on a deep knowledge of the client, the competition, and the market context. 16 The wrong product design choice that does not match the local culture and limitations of the MFI’s client can lead to disaster; a large loan size can lead to overindebtedness, a small loan size can make it difficult for the borrower to meet operational expenses. Furthermore, a long grace period may increase the risk of default. 17 A deep understanding of customers’ profiles, needs, preferences, beliefs, attitudes, and behaviors through market research is critical to achieving better quality of products and services. 16 Thus, the MFIs are required to gather sufficient market data and then analyze and interpret theme adequately to develop a strategic action plan.

MFIs are also required to perform good screening for each applicant. That would help them determine her/his ability and willingness to use the money as agreed and to place the appropriate conditions, such as the amount of loan and the repayment terms. Alimukhamedova et al. 18 suggest that unfavorable geographical conditions can hamper the outreach of MFIs in isolated areas. The difficulty of gathering high-quality information about applicants in remote areas may also push the MFIs to adopt more restrictive loan conditions. 19 Ledgerwood and White 20 affirm that an MFI may have all the right products in place, but if the quality of services is inappropriate, customer satisfaction will be low. Díez-Mesa et al. 21 confirm that the relationship between service quality and customer satisfaction has been tested in a variety of fields. Bashir et al. 22 Saeed et al. 23 demonstrate that the service quality is positively and significantly influences customer satisfaction in microfinance. Parasuraman 3 identifies five dimensions of service quality (reliability, responsiveness, assurance, empathy, and tangibles) that link service characteristics to consumers’ expectations.

CGAP 24 emphasizes that the customers handled by the MFIs are exceptional. Therefore, the competencies required by the staff to deal with them need to be exceptional as well. The MFIs should recruit the right people with the right skills in terms of technical, organizational, and personal competencies, or at a minimum have the capacity to learn them through training. Staff training is another key point to ensure good quality and to provide better service to customers. Staff training may contribute in building knowledge and skills required to meet the institution’s goals. Training can include the company’s mission and objectives, microfinance principles, skills for right delivery, knowledge of products and processes, code of conduct, and communication skills. Training can also cover market research techniques, more advanced credit analysis, computer technology, and accounting.

Ledgerwood and White 20 highlight that providing excellent customer service involves not only areas that come in direct contact with the client, but the entire institution is concerned. The MFIs should treat their staff in the same manner that they expect customers to be treated. 24 They should ensure a balance between their interests, customer interests, and staff interests. If an institution’s staff are not satisfied, they may not offer good customer service. Low employee morale caused by bad working conditions or lack of incentives can cause external customer dissatisfaction. Thus, the MFIs should provide a working environment where employees feel they are encouraged to participate, discuss problems and issues, share knowledge and experience, participate in solving problems, and understand the importance of their contribution and role in the organization. Good incentives are also important in keeping the staff motivated, boosting their morale, and then improving service quality. 24 Motivations can include salary increment, learning and skill enhancement for staff professional development, opportunities for graduation, and so on. Through staff satisfaction, MFIs should be able to enhance productivity and keep full awareness of customers’ expectations.

BNs: Theoretical background

BNs are an artificial intelligence model used to represent and analyze uncertain knowledge from a probabilistic standpoint.

21,24

–27

This modeling technique has other labels in the literature, such as Bayesian belief networks, causal probabilistic networks, causal networks, and influence diagrams.

7,28

BNs are a directed acyclic graph (DAG) that represents the probabilistic dependencies between a set of variables. Simon et al.

29

defines the BNs as a couple

DAG representing a BNs. DAG: directed acyclic graph; BN: Bayesian network. Source: Tarantino and Cernauskas. 14

In a BNs, the relationships between nodes are described by a conditional probability (CP) distribution that captures the dependencies between variables.

30

Each node with parents has a conditional probabilities table that quantifies the effect of its parents’ nodes

31

; it has a probability distribution for each combination of possible values of the parent nodes.

28

The nodes without parents have a prior probabilities table. The probabilities in BN are simplified by Markov property assumption; the probability distribution of any variable depends on its parents only. Thus, the joint probability distribution in a BNs with n nodes (

where

The BNs are based principally on Bayes’ rule. It helps determining the probability that a random variable will be in a given state if we know the values of some other random variables. Let A and B are two events, Bayes’ rule can be defined as follows:

where

As per Wu et al. 32 and Salini and Kenett, 33 BNs can support two types of inferences: predictive analysis for children nodes through their parents and diagnostic analysis for parent nodes through their children. BNs have several other advantages that make them useful in many areas. According to Wu et al. 32 and Liu et al., 34 BNs can provide a way to overcome data limitations through the integration of qualitative and quantitative data from various resources. These data can include results from previous experiments, experts’ judgments, and published literature. 27 Constantinou and Fenton 13 stress that a BNs model can be easily converted into a decision support system (DSS), which is readily updated when new knowledge is available.

Several software packages are available for building BNs models, such as Bayes Net Toolbox of Matlab, BayesiaLab, Hugin, JavaBayes, and Netica. 28,35,36 In this study, Netica is used, it is has a graphical interface and can provide sensitivity analysis (SA) and other numerous functions.

BNs model development

Building a BNs model requires generally respecting several steps (Figure 2).

BNs model development. BN: Bayesian network. Source: Wu et al. 32

Define the main objective of the study: The goal may be to increase the understanding of the system or making a prediction. This phase will also result in a clear idea of the system that is to be modeled. Build the model structure: This phase aims to identify the key factors that influence the principal objective (the top-level node), to determine the relationship between them, and to specify the number of states for each factor (node) as well as the corresponding linguistic variables. That can be done based on the literature review and discussions with domain experts and stakeholders involved in the problem. We note that the relationships between the factors can also be learned from data if available. Nevertheless, a validation from the domain experts is highly required. Quantify the BNs model: This task consists in estimating the probability distribution of each factor, the marginal probabilities for terminal nodes (without parents), and CPs for nodes with parents. The marginal probabilities can be quantified through survey data, from literature or through discussion with experts or stakeholders. The CPs of the other nodes can be estimated using empirical data, by simulation or using subjective estimation (experts’ judgment) when it is difficult to obtain sufficient data. Interrogate the developed model: Once the BNs model is quantified, the next step is to interrogate it. Interrogation can include current status analysis, SA, influence analysis, and scenario analysis. Current status analysis pertains to the effect of the initial probabilities of terminal nodes on the variable of interest. SA measures how particular nodes (factors) can influence the model outcomes; it helps analysts identify the sensitive parameters. SA can be performed using mutual information (MI). The MI or the mutual dependence between two random variables quantifies how much one random variable tell us about another; more specifically, if we have two discrete random variables Y and X, Y as an output variable and X as an input variable. The MI refers to the reduction in the uncertainty of Y due to the knowledge of X.

37

The MI is given as follows: where H(Y) refers to the entropy (uncertainty) of Y and H(Y|X) refers to the entropy of Y given the knowledge of X. From the results of SA, the input variables can be ranked according to their influence on the variable of interest, generally the outcome.

30

SA may be very helpful in a decision-making, as it will provide insights on how to achieve or to avoid a given outcome.

27

The model is also to be interrogated using influence analysis. Its main objective is to identify the degree to which the different child nodes are influenced by their parent nodes. Such an analysis can provide an insight into the most significant factors. Another way of interrogating the BNs model is through scenario analysis, also known as “what if” analysis. It refers mainly to both prediction and diagnostic analysis. The first shows the relative changes in the outcome probabilities according to the changes in the system parameters. While the second shows the change in the system parameters according to the changes in the outcome probabilities. The model evaluation and testing: The purpose of this phase is to ensure that the proposed BNs model adequately represents the objective of the study. The model results need to be validated with the help of domain experts and stakeholders; they should test whether the model behavior reflects the system of interest.

38

The model results can be compared with literature data or with results from similar models if available. A quantitative evaluation is also possible using SA and comparison of the model predictions with observed data if available. Once the model is validated, it can be used as an interactive decision-making tool that can be updated with new information when it is available.

The proposed model

The study is based mainly on the Moroccan microfinance sector recognized as one of the vibrant microfinance sectors in Middle East and North Africa region. 39 As indicated earlier, our purpose is to model the effect of MLP-related operations on the overall customer satisfaction. In this section, we identify the model nodes (key factors) and their causal relationships (network), we estimate the CPs, and finally, we interrogate and validate the developed model.

The model structure

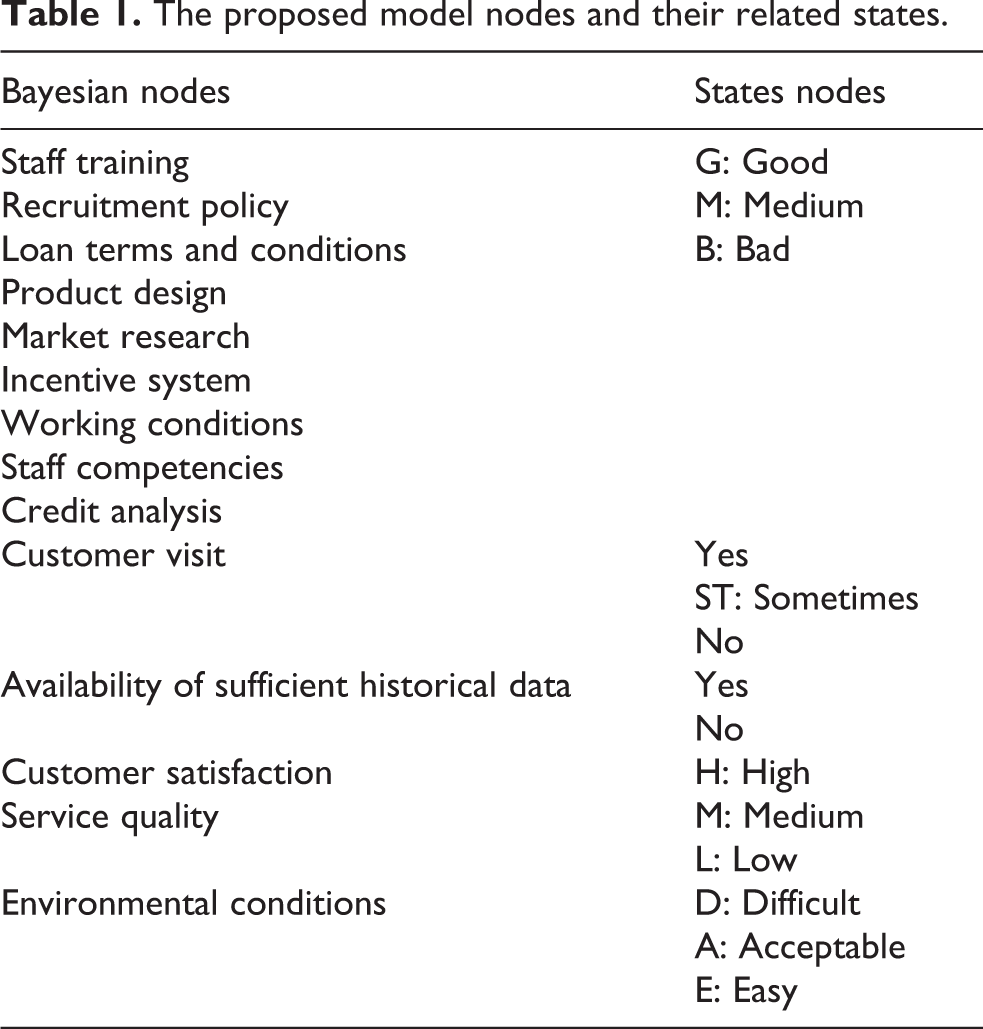

The activities and factors affecting customer satisfaction as well as the relationships between them are identified by means of literature resources and discussions with some microfinance researchers and practitioners who are supposedly well informed about the Moroccan MLP. Figure 3 shows the proposed model structure. Table 1 illustrates the model nodes and their related states (high, medium, etc.).

The model structure.

The proposed model nodes and their related states.

The model quantification

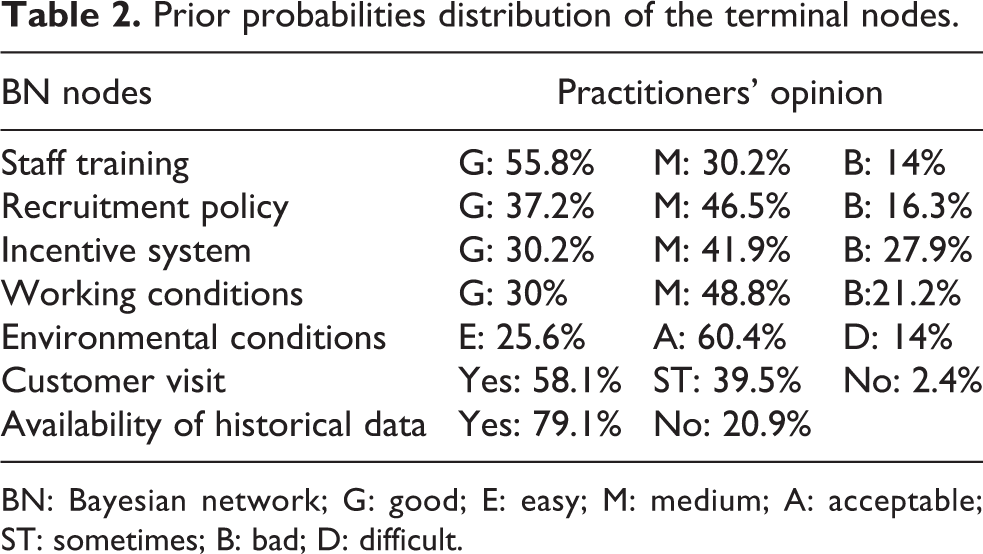

To estimate the probability that the overall customer satisfaction will be in a given state, we establish the prior probabilities distribution for terminal nodes and the CP distribution for nodes with parents. For terminal nodes (without parents), the prior probabilities (Table 2) are collected from microfinance practitioners; an online questionnaire is used for that purpose. The population is selected from the three principal Moroccan MFIs, that is, Albaraka, al Amana, and Attawfik using LinkedIn networking. Forty-three complete questionnaires were analyzed. The population is composed principally of credit officers, risk analysts, market research executives, consultants, portfolio managers, and branch managers.

Prior probabilities distribution of the terminal nodes.

BN: Bayesian network; G: good; E: easy; M: medium; A: acceptable; ST: sometimes; B: bad; D: difficult.

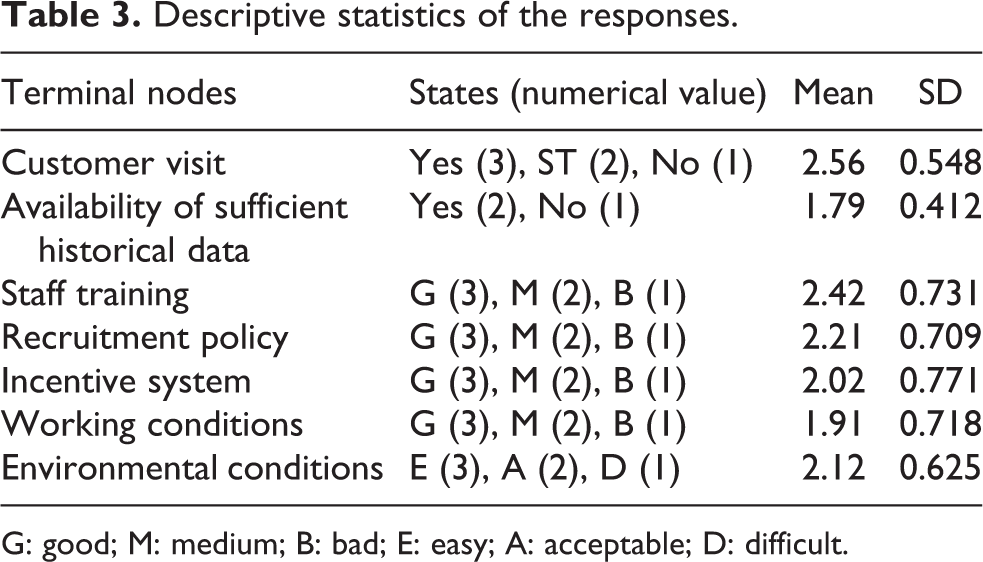

The reliability of the questionnaire is confirmed by Cronbach’s α coefficient (0.78 > 0.7). 40 The descriptive statistics of the responses are shown in Table 3.

Descriptive statistics of the responses.

G: good; M: medium; B: bad; E: easy; A: acceptable; D: difficult.

Due to the limited statistical data related to the Moroccan MLP, the CPs are determined using experts’ knowledge and fuzzy logic inference system. The degrees of possibilities, that is, membership values,

41

are to be calculated and then a transformation possibility–probability is to be performed. Dubois et al.

42

assert that converting possibility measures (membership values) into probability measure can be useful in any problem of decision-making where it is necessary to deal with heterogeneous, uncertain, and imprecise data. They argue also that a possibility–probability transformation should respect two conditions: The probability–possibility consistency principle, that is, the possibility measure is the upper bound of the probability measure: Let P and Preference preservation: A possibility distribution π induces a preference ordering on Ω, such that,

In this study, the fuzzy logic inference system is used to calculate the conditional possibilities (membership values) and then the conditional possibilities are assumed to be proportional to the CPs. 34 For instance, service quality is determined by the conditions of the staff competencies, incentive system, and the working conditions (Figure 4)

Fuzzy logic model for the evaluation of service quality.

In this example, the evaluation rules for generating the associated conditional possibilities are seen in Table 4, where “staff competencies,” “incentive system,” and “working conditions” are linguistic variables. Good (G), Medium (M), Bad (B), Low (L), and High (H) are the possible fuzzy values defined by a Gaussian distribution.

Fuzzy rules for service quality.

G: good; M: medium; B: bad; H: high; L: low.

To make the output of fuzzy logic model sensitive to each input, we have chosen the “product” as the T-norm (Triangular norm) operator instead of “min.” Let X be a set, A and B two fuzzy subsets of X,

Let SQ refers to service quality, CO refers to competencies, IS refers to incentive system, and WC refers to working conditions. To calculate:

Fuzzy inference system for service quality.

The conditional possibility for the “SQ = H,” “SQ = M,” and “SQ = L” are edited as follows:

The summation of these possibilities is 1.0241. As the upper bound of a probability measure is the possibility measure, 42 the CPs related to customer service are calculated as follows:

The model interrogation and results

After the BNs model is quantified, the next step is to question it in terms of current status analysis, SA, influence analysis, and scenario analysis. To show the overall customer satisfaction level resulting from the current status of the Moroccan MLP, we propagate its associated initial probabilities (Table 2) through the BNs. We show that the customer satisfaction level is high at 36.4%, medium at 44.3% and low at 19.2% (see Figure 6 for more results).

Current status analysis.

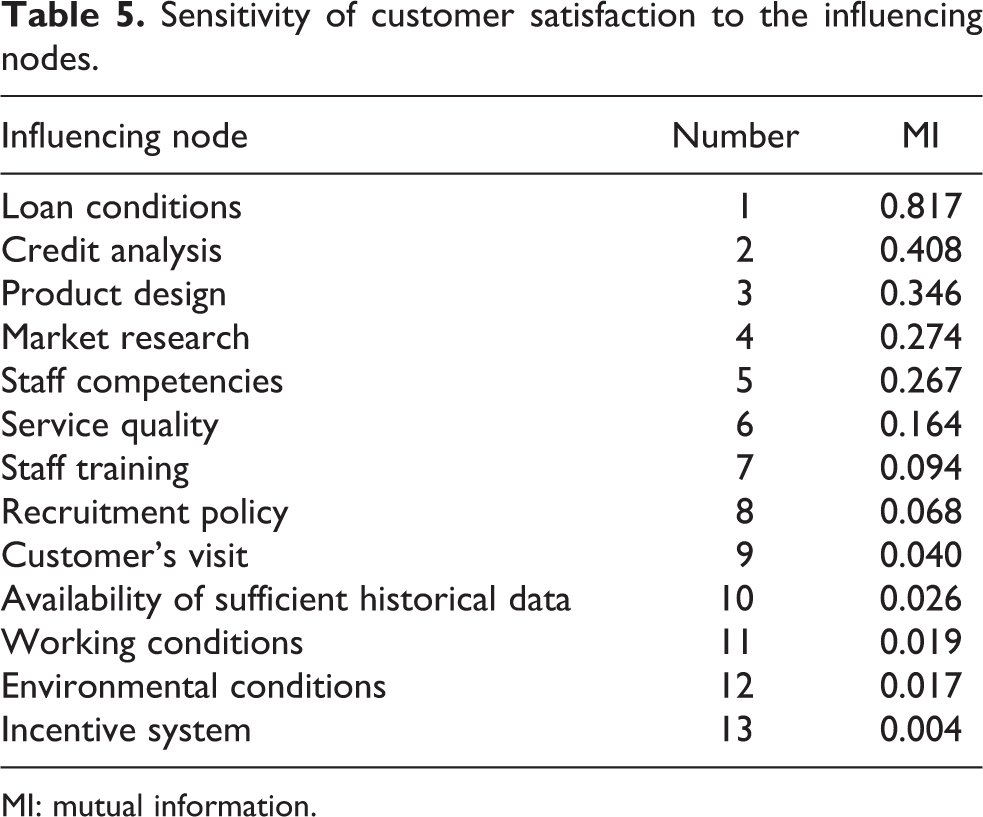

To determine the degree to which the different factors influence customer satisfaction, we perform a senility analysis; the MI of each influencing node is computed. The higher the MI value of a related node is, the more it influences the target variable. Table 5 and Figure 7 show the degree to which the customer satisfaction is influenced by the different variables. For terminal nodes, we notice that customer satisfaction is more influenced by the staff training, the recruitment policy, the customer’s visit, and the availability of sufficient historical data, respectively. In addition to the SA, an influence analysis is also conducted (Table 6) and the following conclusions are drawn:

Sensitivity of customer satisfaction to the influencing nodes.

MI: mutual information.

SA of the child nodes to their parent’s nodes.

MI: mutual information; SA: sensitivity analysis.

Sensitivity of customer satisfaction to the influencing nodes.

The customer satisfaction is more sensitive to loan conditions than to the quality of service. The incentive system has the strongest impact on the service quality. The credit analysis has the strongest impact on the loan conditions. The staff training has the strongest impact on the staff competencies. The staff competencies has the strongest impact on both the product design and the markets research. The customer’s visit has the strongest impact on the credit analysis.

The established model can be used as a DSS that can help managers to perform scenario analysis and to plan customer satisfaction strategies.

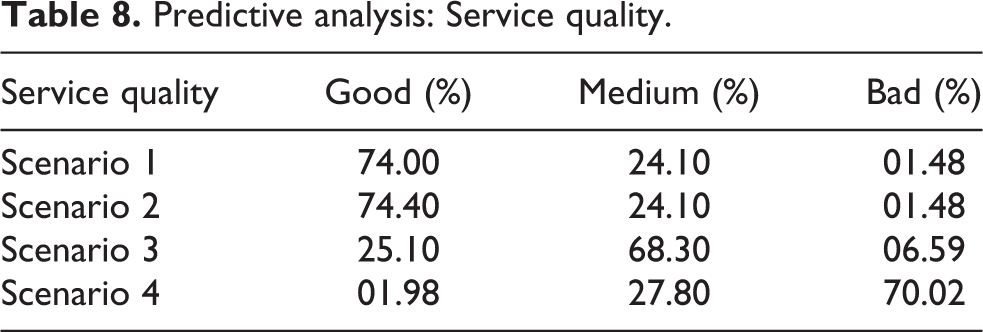

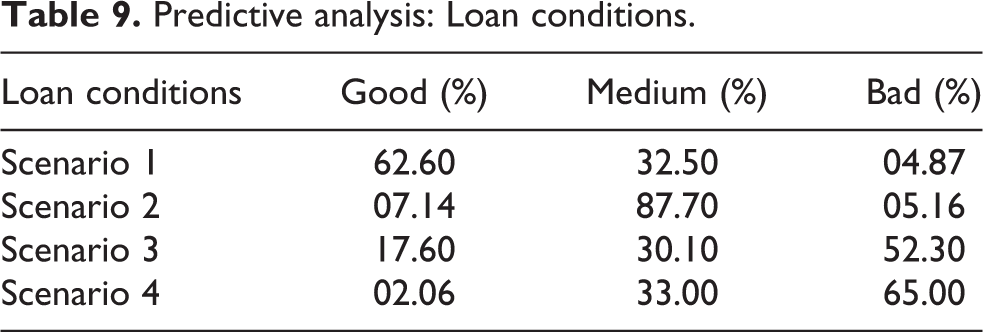

To illustrate this procedure, we perform both predictive and diagnostic analyses. For predictive analysis, we change the values of the terminal nodes and then we observe the changes in the model. To do so, four scenarios (Table 7) are analyzed.

Scenarios description.

Tables 8 to 10 show the probabilities that result from the three top-level nodes, that is, service quality, loan conditions, and customer satisfaction.

Predictive analysis: Service quality.

Predictive analysis: Loan conditions.

Predictive analysis: Customer satisfaction.

The complete results for all the nodes are illustrated in Figure 1A to 1D (see in Appendix 1). The results show that customer satisfaction, loan conditions, and service quality are more influenced by staff training and recruitment policy than by the customer’s visit and the availability of historical data.

In order to determine how we can achieve a target level of customer satisfaction, the model needs to be interrogated inversely (diagnostic analysis). The customer satisfaction level is set to high 100%, and then we observe the changes in terminal nodes. The results are shown in Figure 8.

Diagnostic analysis.

The diagnostic analysis shows that the customer’s visit and the availability of sufficient historical data along with good staff training and recruitment policy can significantly improve the customer satisfaction. It emphasizes also that an acceptable level of working conditions, incentive system, and environmental conditions can be enough.

The study findings fit well with other existing research. Beisland et al. 44 and Iruguthu 45 assert that training programs and incentives need to be well designed to avoid the microfinance mission drift. We have highlighted that MFIs need to focus more on staff training and coaching and to improve their customer relationship management system. The appropriateness of the model’s results is also obtained through discussions with a number of Moroccan microfinance stakeholders.

Conclusion

This article presented a general approach to develop experts’ driven BNs model based on fuzzy logic. The aim was to identify how different factors that do not come in direct contact with the customer can influence his/her satisfaction. The proposed model can help managers to plan customer satisfaction strategies and improve the allocation of resources. It can also be used as a customer satisfaction index to conduct a comparison between MFIs.

Despite the importance of BNs in modeling expert knowledge, there is a difficulty to select the adequate criteria to be included in the model as well as to build an appropriate structure. Another limitation of BNs is the difficulty for experts to express their knowledge as a probability distribution. 28 As a perspective for future research, the developed model can be extended to include customers characteristics considered as an important factor of customer satisfaction. The hypothesized relationships between the factors in the model can also be confirmed using the structural equation modeling. 21

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by the Islamic Development Bank.