Abstract

Many studies focus on microfinance institutions (MFIs) profitability, client retention, and default rate. Yet, they do not pay much attention to the way in which microfinance (MF) can improve the living conditions of the poor and satisfy their needs. This article presents a new way to assess the performance of MF lending process based on analytic hierarchy process (AHP)-fuzzy comprehensive evaluation method. The aim is to suggest some solutions to improve the performance of processes that create and support MF products and services. Not only should this study contribute to the research literature but it can also help the MFIs to control the risk derived from their operations and increase client satisfaction. Thus, MFIs can enhance their performance and their role in reducing poverty.

Introduction

Microfinance is a set of financial services designed to serve the unbanked poor. 1 The financial service needs of poor people are diverse and complex which represent opportunities that can be met on a profitable basis. 2 Poor people need access to financial services to reduce their vulnerability, to meet anticipated and unanticipated needs, and to take advantage of opportunities as they arise. To do so, microfinance institutions (MFIs) provide a web of different financial products like saving services, microcredit, insurance, payment services, 3 and even micropensions. 4 MFIs may also include different activities like skill training and entrepreneurial education directly or in partnership with other institutions. However, the majority of academics and practitioners focus neither on customers’ needs nor in the ways to improve their lives. Rather than that, studies are based on MFIs perception, that is, profitability, client retention, default rates, and the number of customers as the primary measures. 5,6 Kanyurhi 7 notes that the MFI’s weakness to satisfy their clients’ needs is one of the main reasons they lose customers.

Customer satisfaction results in designing appropriate products and services and in the efficiency and effectiveness of the processes creating them. Improving MF processes can help the MFIs achieving such objectives and manage the risks derived from their operations. 8 Several processes such as lending process, saving management process, and payments management process characterize the MFIs’ operations. However, the loan process represents the most typical one.

Zizlavsky 9 states that we cannot manage what we do not measure. Leyer et al. 10 affirm that measuring the process performance is a precondition for its analysis and subsequently its improvement. Therefore, the purpose of this study is to assess the performance of the lending process in Moroccan MF sector. Since 2007, the Moroccan MF sector has been considered as a leader in the Middle East and North Africa region and one of the most successful MF sectors in the world. 11 However, in 2008, the sector experienced a crisis due to uncontrolled growth. Some signs of stress mainly loan delinquency and multiple borrowing started to emerge. 12 To deal with this crisis, the leading MFIs in Morocco undertook some changes including strengthening their lending process. 13 Nevertheless, according to International Finance Corporation, 14 not all responses have been useful. The current research can give us a general idea about the present state of the Moroccan MF lending process (MLP) and present a new approach that can be applied for assessing the performance of the MLP in other countries.

The remaining sections are organized as follows. The next section introduces the theoretical background. Section “Methodology” presents the methodology adopted. In “Results” section, the results of the study are calculated. Finally, a conclusion and a discussion will be provided.

Research background

Poor people constitute the vast majority of the population in most of the developing countries. 15 Even so, they are excluded from the traditional banking. This stems from their inability to provide collateral, 16 the high level of asymmetric information, 17 and the high transaction costs associated with the small loans. The banks hold the tenet that serving the poor is risky and expensive.

To help the poor and low-income individuals, MFIs develop several innovative solutions such as group lending, sufficient incentive, and collateral substitutes. Likewise, they may provide nonfinancial services to solve the problems that have been pushing traditional banks away from the developing world since time immemorial. 17 However, all MFIs are susceptible to risks 18 such as default risk, loss of reputation, mission drift, and therefore loss of customers.

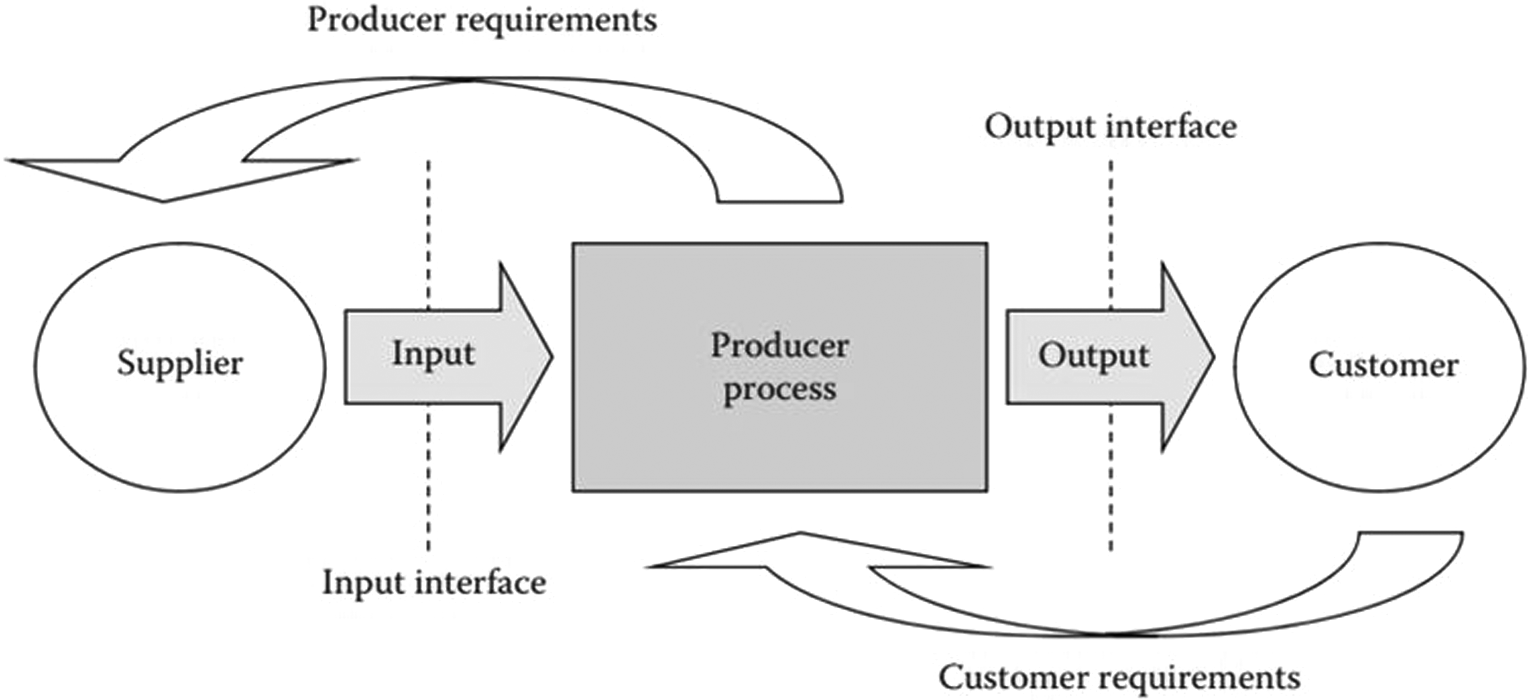

Adopting a process approach can help the MFIs achieve their objectives and control the risks linked to their activities. 8 A process approach refers to the management of an organization as a system of processes and their interactions to produce the desired outcomes efficiently and effectively (Figure 1).

Example of generic process. Source: Corrie. 20

As per Hoyle,

19

the process approach can be better expressed through a series of 10 actions as follows: defining the process’s objectives and outputs; deriving measures of the process’s success; identifying the activities that are critical to achieving the goals of the operations; setting the process’s inputs (information, competencies, etc.); identifying the risks related to the process and putting in place the measures that reduce these risks; determining how the process performance is to be measured; executing the process as planned; measuring what has been achieved and comparing it with the process’s objectives; finding better ways to attain the process’s targets and improving its efficiency; and sustaining the efforts to better performance.

Ortolani 8 asserts that for each MF activity, financial as well as socio-ethical, certain processes are established to allow the production of the services and its distribution to the beneficiaries. Mastering these processes may improve the individual borrower’s social and economic conditions and enhance the MFI sustainability. 5

In this study, we will focus our attention on the lending process considered as the typical process of MFIs.

Ledgerwood et al. 3 affirm that lending methodologies can range from individual to group lending and whether they must adhere to Islamic banking principles. The chosen lending methodology significantly influences the product design, client selection, application and approval process, loan repayment, monitoring, and portfolio management. Likewise, it may affect the institutional structure and staff requirements, including training and compensation. The choice of lending methodologies may also influence the risk level of an MFI’s loan. 6

The most popular lending methodology is group lending. It refers to arrangements by individuals without collateral to form groups with the aim of obtaining loans from a lender. The typical group-lending scheme can be summarized as follows

17

: Each member is jointly liable for the other member’s loan. If any member does not repay, all the members will be punished (exclusion of future credit access). Prospective borrowers are required to form groups by themselves.

In a group-lending contract, each borrower obtains a loan for her/his project, but the liability is joint. This joint liability induces group members to self-select each other and provides an incentive for peer monitoring. Various researchers argue that the group-lending mechanism as a major innovation of MF movement 1 can potentially deal with information asymmetry and improve the lender’s repayment rate. 3,17 Borrowers in the group lending have perfect knowledge of each other. Moreover, everyone wants to form a group with safe borrowers, which reduces adverse selection on the one hand, and since joint liability encourages borrowers in a group to monitor each other on the other, it will alleviate moral hazard problems. 17

Armendariz and Morduch 21 note that the group-lending methodology can transfer the whole or part of the job usually done by the lender into customers. This position comprises screening clients and monitoring their efforts. Figure 2 summarizes the dynamics of the group lending.

The dynamics of group lending. Source: Kaicer and Aboulaich. 22

Despite its advantages, the group-lending methodology suffers from some disadvantages such as the risk of contagion if one of the members is unable to meet the repayment.

Khavul 16 concludes that group-based MF has attracted more attention in the literature, but little is known about individuals who take microloans out of the group-lending formula, that is, the individual loans.

The individual loan is a loan provided to a one borrower who is solely responsible for its repayment since collateral is required. 23 Individual lending requires greater up-front analysis of clients and their cash flow and, sometimes, frequent contact with customers during the term of the loan. Mortgage approvals and amounts are based on an applicant’s eligibility and her/his debt capacity, which in turn are dependent upon some factors, including personal and business characteristics (age, gender, reputation, source and amount of income, the purpose of the loan, etc.).

The majority of the Muslim population is excluded from conventional MF programs because of their religious sensitivities, which explains the need for an appropriate model that conforms to their beliefs and cultures. 24 Adopting the Islamic banking principles by some MFIs can fill this lacuna. In this case, the MFI can neither charge nor pay interest (Riba). Instead, they can adopt the Islamic approach to poverty alleviation. This approach is a composite of charity-based and for-profit-based interventions. The charity-based approach involves several non-for-profit mechanisms, such as zakah (compulsory annual levy on wealth), waqf (perpetual trust), and qard-hasan (interest-free loan). These mechanisms must be used first to fulfill consumption needs, and then the profit-based instruments may be utilized in the second stage where microenterprises may be encouraged. The for-profit approach is based principally on trading, leasing, or direct financing in profit–loss sharing. 17 According to Obaidullah and Khan, 25 the Islamic banking principles can be used with prevalent MF models such as Grameen model, village bank model, credit unions, cooperatives, or self-help groups.

Viewing lending methodologies as a process or a system of processes would help MFIs achieving both their social and financial objectives. The organization performance significantly relies on the efficiency of its business processes. 26 A process is defined as some interrelated or interacting activities that convert inputs into outputs. 20 When it is managed successfully, the process can increase productivity, efficiency, profitability, and customer’s satisfaction. However, an inadequate process may lead to numerous problems.

To give a general idea about the MLP (Table 1), we use the supplier, input, process, output, and customer (SIPOC) diagram (Figure 3). It would explain the key processes and how they are connected.

SIPOC for microfinance lending process.

Source: Authors’ elaboration.

MFI: microfinance institution; NGOs: non governmental organizations.

An SIPOC diagram. Source: Laguna and Marklund. 27

Improving a process performance requires precision in its measurement. Performance measurement can determine the necessary action needed to the organization. It can also detect problems and identify achievement and opportunities for the future. 28 Soltani et al. 29 note that many studies have been conducted to design performance assessment systems, which result in the proposal of several performance evaluation methodologies. Examples may include those based on input–output relations such as stochastic frontier approach, distribution-free approach, thick frontier approach, data envelopment analysis, and free disposable hull. However, focusing on measurements of the input–output relations is not sufficient as it does not indicate the causes of a low performance. 10 To overcome this limitation, another method called “process mining” is suggested. However, the later needs large data sets, which is not often available.

This article presents a new way to assess the performance of MLP based on AHP-fuzzy comprehensive evaluation method (FCEM). This approach is implemented for the Moroccan MFIs using the MATLAB [version MATLAB R2010a] software. The AHP-FCEM is a convenient methodology to evaluate the performance of MLP as it is composed of several steps and phases, which are assessed according to many criteria. Also, it is a very suitable tool for the purpose above as the decisions are to be made with limited information. 30 Other advantages of the related approach are its ability to take into consideration any level of details about the system that is of interest and the relative priorities of the different indicators involved in it. The combination of the AHP and fuzzy comprehensive evaluation can provide a reliable decision for the managers.

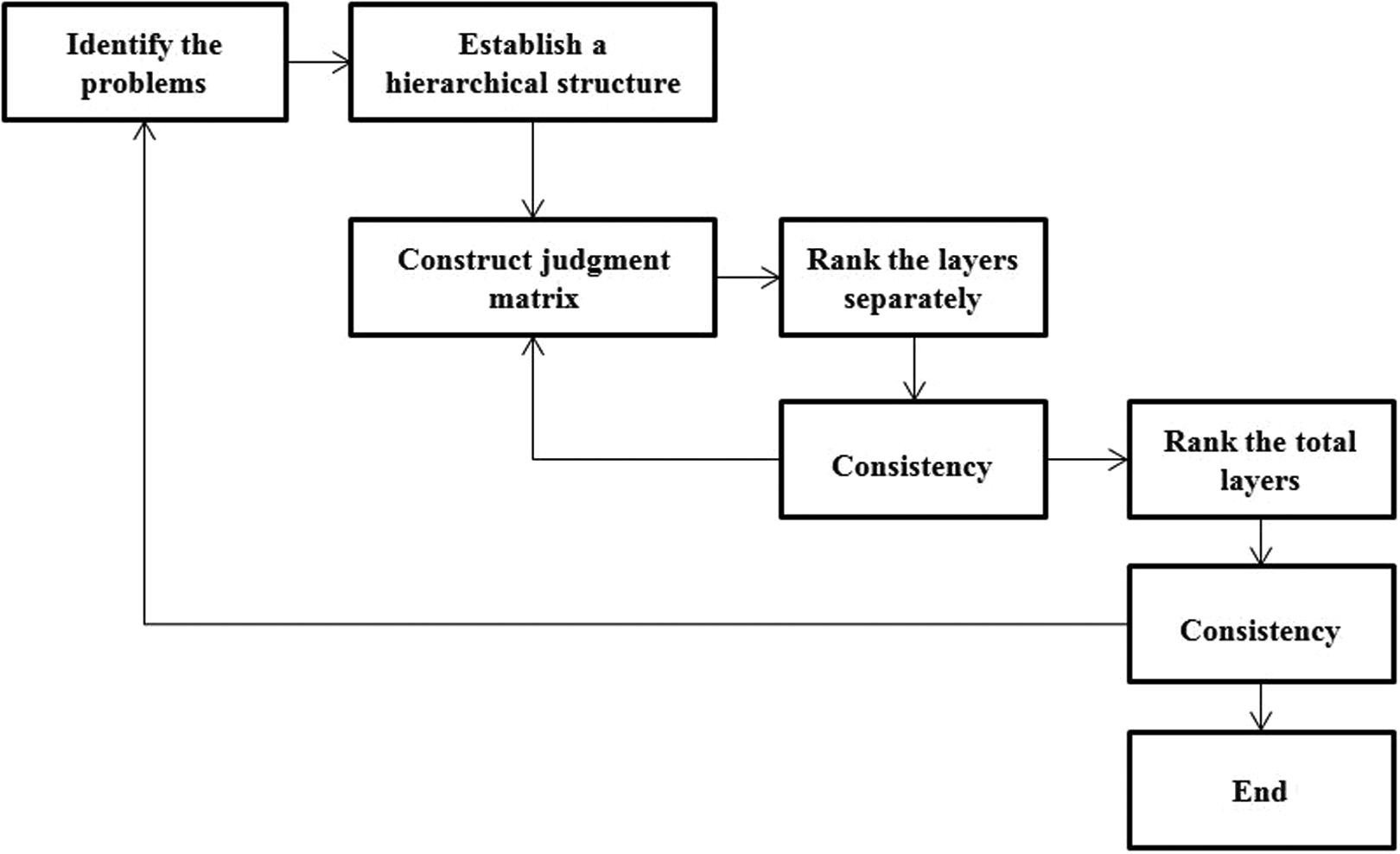

AHP 31 is a multicriteria decision-making method that combines qualitative and quantitative analysis. This technique is based principally on pairwise comparison matrix and consistency test. It has been widely applied to conditions of uncertainty. The hierarchical structure used by the AHP can decompose the complexity of the decision which involves numerous criteria 32 and uses experts’ opinions to measure the relative contribution of each criterion or subcriteria. The AHP may be regarded as a quick fix in decision-making for the complex problem. 33 It also assists the policymakers to precisely decide their judgment and then measure its consistency. The methodology of the AHP can be outlined in a step-based manner in Figure 4.

Steps for the AHP. Source: Li and Jun. 34

The FCEM is a mathematical technique to evaluate systems using fuzzy set theory principles. It allows dealing with the fuzzy phenomenon affected by numerous factors. FCEM would overcome the subjectivity, the uncertainty, and fuzziness of evaluation indexes using both qualitative and quantitative analysis.

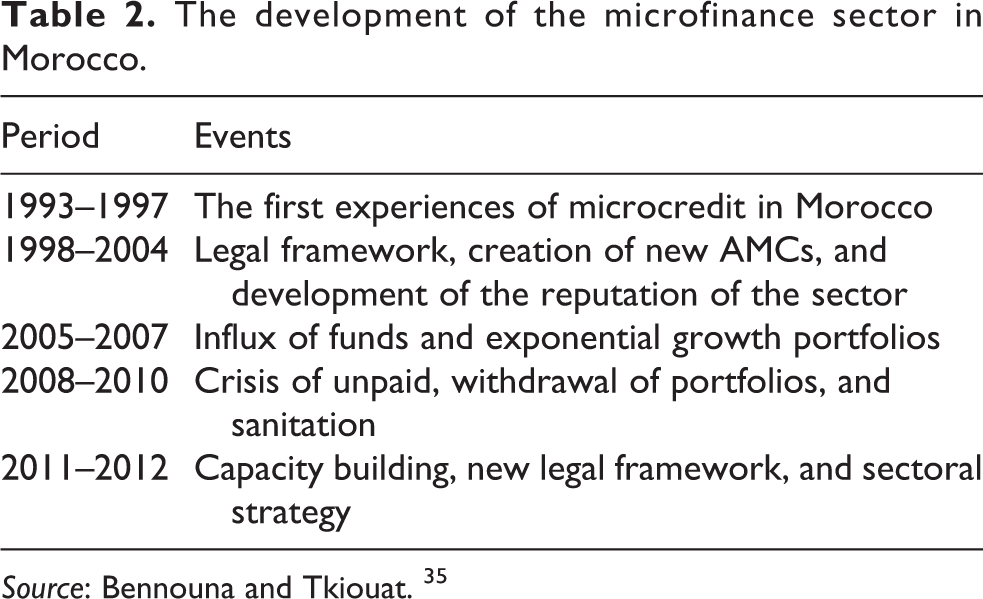

MF sector in Morocco includes 13 Moroccan MF Associations with about one million beneficiaries. Three of these institutions, principally Al Amana, Albaraka, and Attawfik concentrate on 90% of the market share. The primary product offered is microcredit with good coverage in rural areas. Table 2 shows the development of the MF sector in Morocco since 1993 until 2012.

The development of the microfinance sector in Morocco.

Source: Bennouna and Tkiouat. 35

Methodology

The goal of this section is to assess the performance of Moroccan MFIs lending process, that is, how well the executed processes work about the chosen indicators. 10

The evaluation index system

In performance assessment, using a system with several individual indicators can be seen as a complete perspective that is highly recommended. 9 The MLP is composed of several steps and phases; if they work correctly, it will result in fewer delays, less duplicated effort, the augmentation of product quality, and enhancement of customer satisfaction. In this study, the MLP phases as well as the selected indicators according to which the process performance is measured construct our evaluation index system (EIS; see Table 3) described as follows.

EIS for MLP.

Source: Authors’ elaboration.

EIS: evaluation index system; MLP: microfinance lending process.

Product planning

The product planning is the first step of microcredit process. Every design choice, no matter how small, can create additional risks. 36 Key elements of the design include maximum and minimum loan, grace loan, loan maturity, effective interest rate, payment schedule (weekly, monthly or seasonal payments, etc.), and collateral requirements. The wrong product design that does not match the local culture and MFIs constraints can lead to a dilemma. In fact, loans that are too large can result in over-indebtedness while a loan that is too small can make it difficult for the borrower to meet operational expenses. The MFI can reduce the risks by offering loan products designed to reflect the client’s preferences; cash flow profile versus the ability to repay, seasonal cycle, and other opportunities or risks. To measure the performance of this step, we select four indicators: the diversity of products, the customer’s voice, the services quality, and the provision of nonfinancial services.

Staff training

Staff training is a key point to ensure the high quality and to provide better service. It should emphasize customer service, soft skills, technical competencies, and ethical behavior. The MFIs personnel should also be aware of the company’s mission, vision, and strategy. Four indicators are selected to measure the performance of this phase: data handling, dealing with clients, delinquency management, and accounting.

Client recruitment and application

In this phase, the MFI promotes its products and provides product specifics to the potential customers, and then applicants may submit their requests for a first loan. The MFI collects financial, nonfinancial, and collateral information. This information can be gathered from the applicant, from references (home, business neighbors, suppliers, and guarantors), or the available database (credit bureau etc.). The financial data may include income, expenditures, assets, and liabilities of the applicant’s business and family. This phase is measured according to the relevance of the promotion, the respect of loan applicant, and the collection of financial and nonfinancial data.

Credit approval and disbursement

After collecting financial and nonfinancial data of the claimants, MFIs are required to screen and assess the customers’ ability and willingness to use the money as agreed. In the light of the evaluation process, and the applicant’s risk profile, the MFI decides to approve the loan or not. The performance of this phase is assessed according to the business and household visit, the data management, the disbursement and ongoing customer services, and finally the loan utilization check.

Collection and recovery

This is the task of collecting on-time payment, late payment, and recovering loans. Its performance is measured according to delinquency management, on-time collection, and dealing with the clients.

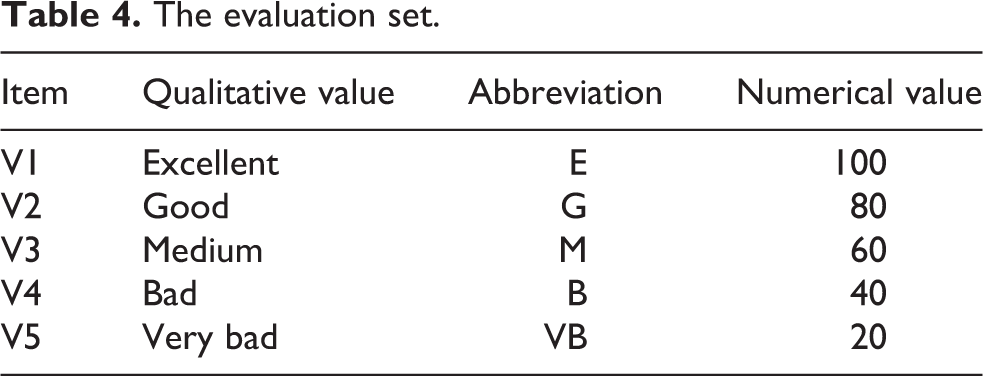

The evaluation set

The evaluation set V = {V1, V2, V3, V4, V5} is presented in Table 4.

The evaluation set.

The weight set

According to the experts’ judgment, a weight vector of the different factors should be established based on their importance degree. The AHP is used to this end.

After representing the system under evaluation graphically (Table 3) and illustrating its different levels, the pairwise comparison matrices should be established. They are the result of comparing every element of each level to the other elements in the same level with respect to the common element of the higher level. Each matrix is presented as follows:

where

Number scale and its description.

For example concerning the product-planning phase (A1), we compare the importance of the four indicators: diversity of product (A11), customer voice (A12), quality of service (A13), and providing nonfinancial services (A14) as shown in Table 6.

Pairwise comparison matrix.

In this example, the quality of service (A13) is 2.8284 more important than diversity of product (A11).

To determine the weight of each factor, the judgment matrix is to be solved, and eigenvectors and eigenvalues are to be calculated. The method of calculating the weights is as follows.

The components of W represent the weights of the factors. Once the weights are determined, the consistency of each matrix is tested based on the consistency index (CI) and the consistency ratio (CR). These two indexes are given by

Average random index.

RI: average random CI.

A CR less than 0.1 is acceptable. The same procedure is used to calculate both the factors and the subfactors weights.

Based upon the experts’ judgment, we establish the pairwise comparison matrices, and then we use the geometric mean calculation to combine the individual matrices collected from different experts. 37 Finally, we calculate the weight set, and we verify the test of consistency (see Tables 1A to 1F in Appendix 1).

The single factor evaluation matrix (R)

Let

Based on the experts’ judgment, each element of the index

The

Aiming to establish the fuzzy comprehensive evaluation matrix, some experts are chosen as judgment group, and each expert evaluates all the elements of the process. Finally, we get a fuzzy evaluation membership matrix.

Results

To assess the performance of Moroccan MFIs lending process, we have selected 10 experts from the three principal Moroccan MFIs. The population (experts) is composed principally of consultants, market research executives, and credit officers, who are supposedly well-informed about the field of study. The data are collected using both face-to-face and online questionnaires. The main issues addressed by these questionnaires are twofold. First, assigning weights for the different steps of the MLP and the selected indicators. Second, establishing the assessment matrices (see Table 8).

Evaluation system of lending process in Moroccan MFIs.

Source: Authors’ elaboration.

MFI: microfinance institution; E: excellent; G: good; M: medium; B: bad; VB: very bad.

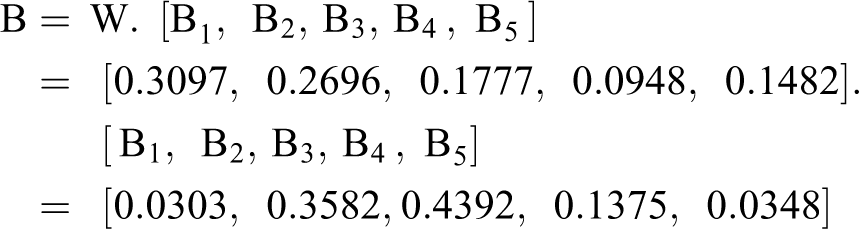

The weights calculated by AHP show that the experts highlight the significance of product planning (0.3097) and staff training (0.2696) phases of the MLP on the one hand and confirm the importance of the following indicators on the other: respect of loan applicant (0.5273), on-time collection (0.4705), delinquency management as staff training topic (0.4705), business and household visit during the loan approval (0.3928), providing nonfinancial services (0.3546), credit utilization check (0.3160) during the loan approval, good dealing with clients in collection and recovery (0.2968), and collection of financial and nonfinancial data of the loan applicant (0.2777); likewise, taking into account the quality of service (0.2735) and the customer voice (0.2417) in product planning phase.

The established assessment matrices suggest that the Moroccan MFIs do not pay much attention to staff training especially data handling and dealing with clients nor to the promotion of their products and need to give more importance to the loan utilization check during the credit approval. What is more is that these institutions do not focus enough on providing nonfinancial services.

The first-grade fuzzy comprehensive evaluation

The first-grade fuzzy comprehensive evaluation is given by:

Vectors

Interpretation of the first-grade fuzzy comprehensive evaluation.

The second-grade fuzzy comprehensive evaluation

The second-grade fuzzy comprehensive evaluation is calculated according to the results of the first-grade fuzzy comprehensive assessment, and it is written as the following:

where W represents the weight vector of the secondary level of MLP shown in Table 8.

The final evaluation of Moroccan MLP is given as follows:

With V = 100, 80, 60, 40, 20. This score indicates that the performance of MLP is medium and needs improvements.

Conclusion and discussion

In the manufacturing industry, many studies have addressed the subject of process management and improvement, while very few studies on the same were made in the service sector notably in the MF sector. This article is an attempt to assess the performance of MLP in Moroccan MFIs based on AHP-FCEM. The innovation of this article is the presentation of a new way to measure the performance of MLP. The proposed approach will provide practical guidance to both researchers and industry practitioners in developing AHP-FCEM in the MF industry.

In this case study, the final score obtained shows that the performance of the Moroccan MFIs lending process is not satisfactory and the different steps of this process need much more improvements. One way to validate the proposed model is to compare its predictions with known results 38 or with results from similar models. Unfortunately, there is no similar study in the field. Therefore, we conduct a series of interviews with different MF stakeholders, who confirmed the appropriateness of the results obtained.

There are numbers of limitations to this research. Firstly, AHP-FCEM has a subjective nature which makes the evaluation of the results quite difficult. Secondly, the experts must answer a much larger number of questions, which results in not having a significant number of respondents. Thirdly, the choice of the EIS and a judgment scale cannot easily be attained. 32

This model may be deemed applicable to measure the performance of the MLP within a particular MFI instead of all the industry in a country. It can also be extended by detecting and assessing the causes of delinquencies and failures of the MLP and then give some insights to reduce its variation.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by the Islamic Development Bank.