Abstract

This paper examines how digital platforms have come to embody a new form of media power, reshaping the Australian media economy and challenging traditional understandings of media influence. While legacy media power was grounded in content ownership and political influence, platform power today stems from infrastructural dominance, algorithmic control, and the commodification of user data. Drawing on the concept of the network media economy, the paper explores how tech giants like Alphabet and Meta have overtaken traditional Australian media firms in advertising revenue and market influence. Using metrics such as Concentration Ratio (CR4) and the Herfindahl–Hirschman Index, the paper demonstrates the extreme consolidation within digital services sectors. It also considers the political implications of this shift, highlighting how platform companies are increasingly influential in shaping public discourse and policy, both directly and through their economic leverage. The paper argues for a reframing of media power that encompasses both traditional and emerging forms of dominance, urging policy responses that reflect the integrated, multi-sectoral nature of today's media landscape.

Keywords

Introduction

The observation that the media are powerful seems so obvious that it seems barely worth restating. The capacity of powerful men (and very few women) to reshape economies, political systems and cultures through their ownership and effective control over mass media outlets has been a commonplace of politics with the observed power of media moguls such as Rupert Murdoch to influence national elections and global debates about issues such as climate change (McKnight, 2012), Silvio Berlusconi's rise to public office in 1990s Italy from control over a media conglomerate as well as a leading football team to creation of a political party and three terms as Prime Minister (Newell, 2017), to Donald Trump's transformation from high-profile real estate developer and host of 14 seasons of The Apprentice to becoming the 45th and 47th President of the United States (Boczkowski and Papacharissi, 2018). Popular culture resonates with the ongoing image of the all-powerful media tycoon, from Orson Welles in Citizen Kane to Brian Cox's portrayal of Logan Roy in HBO's Succession.

At the same time, a specter clearly haunts the great media empires of declining influence in the digital age. The growth of the Internet and social media has seen audiences around the world migrate from traditional mess media towards a range of digital platforms, and importantly, they have been followed in this migration by commercial advertisers. While traditional media have responded by themselves developing their digital offerings, these have rarely been able to replicate the revenue streams that were available in the heyday of mass communication. As documented by multiple sources (e.g. Australian Competition and Consumer Commission, 2019a; Cairncross, 2019; Tow Center, 2019), one of the consequences has been a crisis of journalism, as traditional advertiser funding business models can no longer sustain print and broadcast journalism at the levels at which they have historically operated their news operations (Pickard, 2020). This has in turn led to calls for the major digital platforms, most notably Google and Meta, to pay news publishers for the professionally produced news content that partly drives audiences—and advertisers—to their platforms (Bossio et al., 2022; Flew et al., 2023).

In this paper, we will argue that modern day platform power mirrors traditional media power, including economic power and market influence, as well as social and political influences, but this power is enabled by new mechanisms of accumulation and control—namely the influence of algorithms and data commodities. We also highlight the Australian context and how, even at a local level, these international tech giants have become dominant figures within the network media economy. It can be noted that Australia is a country where considerable data on telecommunications and traditional media industries is readily accessible through the Australian Communications and Media Authority (ACMA) as the principal government regulator, although data in areas such as streaming media revenues, digital advertising, and measures for the Internet economy are not gathered by public authorities, and there is a reliance upon secondary sources such as industry reports and trade publications. The fact that many of the major new players in the Australian network media economy such as Alphabet, Meta and Netflix do not provide annual company reports for their Australian activities means that information for these foreign-owned entities needs to be extracted from non-official sources.

Media power in a digital age: Old and new debates

Media power has often been defined as much by its effects as by its attributes. For critical political economists such as Peter Golding and Graham Murdock, media power manifests itself in such as dominance over media markets, the ability to extract monopoly profits and block the entry of new competitors, the capacity for political influence derived over the ability to reach large audiences, and the capacity to shape political and cultural agendas (Murdock and Golding, 2005). From a Weberian perspective, John Thompson placed media power in the context of cultural and symbolic power, which co-exists with economic, political and coercive power (Thompson, 1990). Cultural power refers to the capacity of individuals, institutions, or social groups to shape the production, circulation, and reception of meaning through cultural forms that include the media, but also through art, language and rituals. Both Golding and Murdock and Thompson relate media and cultural power to what Steven Lukes termed three-dimensional power, or the power to not only shape agendas but to define the parameters of “common sense” (Lukes, 2005). This is similar to Des Freedman's account of media power as “the relationships—between actors, institutional structures, and contexts—that organize the allocation of the symbolic resources necessary to structure our knowledge about, and by extension our capacity to intervene in, the world around us” (Freedman, 2015: 274). Freedman stresses that such media power is never absolute domination, but is marked by conflict, contestation and contradiction: it is closest to the concept of hegemony as it was developed by Stuart Hall and others (Hall, 1986).

While such accounts present media power as something distinct from economic power, there is a sense that it has its roots in economic dominance in media markets. In particular, it implicitly draws upon accounts in media economics that see media markets as being principally monopolistic (one seller) or oligopolistic (few sellers). In oligopolistic market environments, there are implicit incentives for providers to collude so as to protect their favorable market positions, even if they ostensibly compete with one another (Albarran, 2010; Cunningham et al., 2015; Doyle, 2013; Wildman, 2006). Such environments lend themselves well to the formation of powerful industry associations, extensive lobbying of politicians for favorable legislation, and collective bargaining to deal with stakeholders including trade unions. Two important measures of such market dominance have been:

Concentration Ratio (CR), which measures how much market share is held by the largest companies, helping to evaluate market competition or monopolistic tendencies. It does this by calculating the combined market share of the top n firms in an industry (e.g. CR4 = market share of the top four firms), expressed as a percentage. Herfindahl–Hirschman Index (HHI), which provides a more precise measure of market share distribution across all firms in an industry. HHI is calculated by squaring the market share (%) of each firm in the industry and summing these squared values. The HHI formula is:

si = Market share of firm i (expressed as a percentage, e.g. 30% = 30).

n = Total number of firms in the market.

Economic standards for concentration vary between regions, with most thresholds indicative of either a five- or four-player market. The Australian Competition and Consumer Commission's Merger Assessment Guidelines designate a HHI of 2000—a 5 player markets equivalency—as highly concentrated (Australian Competition and Consumer Commission, 2008). By comparison, the US Justice Department designates a six-player HHI threshold of 1800 as highly concentrated (U.S. Department of Justice, 2010) while the Global Media and Internet Concentration Project uses four-player HHI threshold of 2500 (Flew et al., 2024; Winseck, 2023).

An explicit requirement of metrics such as CR and HHI is that three things can be defined. First, there is a need to be able to define a product or service. In media economics, this has most typically been done with reference to the platform on which content or services are delivered, such as newspapers, magazines, books, radio stations, broadcast TV stations etc. This means that it can be difficult to get measures based upon content. For example, trying to identify the market for news is challenged both by news being carried across multiple platforms, and because the news providers typically bundle news in with other content, such as entertainment. Second, there is a need to define markets through which content is supplied by providers and demanded by consumers. Media markets are typically two-sided, as revenue streams are derived both from consumers (through payment, attention etc.) and advertisers, with the preferences of advertisers largely shaped by the demand of consumers. As we will note below, this picture has been further complicated by digital platforms, which operate across multi-sided markets (Evans and Schmalensee, 2016; Parker et al., 2016). Third, if we can define the product and the market, we can define the industry. Measures of industry concentration such as CR and HHI derive from the existence of relatively stable industries, notwithstanding the challenges presented by industry strategies which go across industries, such as vertical integration (mergers along the supply chain) and conglomeration (acquisition of firms across multiple industries that may be unconnected to only tangentially connected) (Doyle, 2013).

Digital platforms challenge many of the assumptions that have framed the economic underpinnings of media power analysis. While there is debate as to whether Apple, Microsoft, Google, Meta, Amazon and others can be considered to be digital platforms in the same way (see e.g. Lotz, 2021), 1 all have broadly data-driven business models insofar as access to multiple and diverse sources of data allows for refinement of products and services so as to appeal to both consumers and advertisers (Parker et al., 2016). Moreover, they engage simultaneously with multiple stakeholders, which in media markets can also include content creators, while also having sufficiently diverse business interests that they are not obligated to derive profit from their media-based properties (Flew, 2021). For example, streaming services such as Amazon Prime and Apple TV + can operate as loss-leaders for overall business interests, as they make it more attractive to do online shopping (Amazon) or buy digital hardware (Apple) than their competitors. This is very different to the streaming platforms that are outgrowths of traditional media businesses, such as Disney+, Paramount+, HBO Max, Peacock and others, which are all firmly rooted in the entertainment industries. Finally, they are for the most part distributors rather than producers of media content. Critics argue that they unfairly derive benefit from the professionally produced media content that traditional media publishers invest in and take commercial risks through that investment (Sims, 2019), while having a “frenemy” relationship to the media industries, as companies such as Google and Meta are direct competitors for advertising revenues and indirect competitors for audiences in the attention economy. 2

From the perspective of media power, this data would all suggest that digital platforms have something comparable to what we have traditionally understood to be media power, or the capacity, as Freedman (2015) describes, to organize the allocation of symbolic resources. But there is a conceptual lag between the changing media environment in this regard, and the tools we use to understand it. This may be in part because platform companies themselves deny having such power and present themselves as simply the intermediaries or brokers between content producers on the one hand and those accessing content on the other (Hutchinson et al., 2024: 104). The concept of the “neutral platform” has had considerable policy and industry purchase, as evidenced by their immunity from publisher liability in many jurisdictions; however, scholars have long pointed to the extent to which platform companies manage and curate the algorithms that connect content to consumers (e.g. Gillespie, 2018).

Definitions of platform power tend to understand the concept in infrastructural terms, as being able to profit from the multiple interactions which occur across platforms and the data generated for the companies involved. van Dijck, Poell and de Waal define platform power as “the concentrated control that a handful of tech giants (e.g. Google, Facebook, Amazon) exert over data, infrastructure, and public discourse—reconfiguring markets, states, and civil society” (van Dijck et al., 2018: 4). This new form of power is primarily seen as being less about the capacity to use media outlets to shape public conversations than about the ongoing capacity to profit from control over infrastructure and thus differentiated from media power as understood through the media moguls. Interestingly, an earlier attempt to define this new form of power, that of Manuel Castells in his 2009 book Communications Power, did not differentiate between infrastructural power and power through content, defining communications power as “the power to shape minds by shaping the communication process itself—who communicates what to whom, and under what conditions” (Castells, 2009: 3). Nieborg and Poell (2025) have recently sought to differentiate institutional platform power from infrastructural power, seeing the latter as an element of the former, and calling for a more strategic understanding of how institutional power can be used in different contexts. They define institutional platform power as “the ability of dominant platform conglomerates to sustain, influence, or impede the actions of other institutions … through economic, infrastructural, and regulatory interventions” (Nieborg and Poell, 2025). Such a definition provides the opportunity to bridge theories of platform power based on infrastructure to the focus of media power discourses on market conduct, content and political influence.

Tech companies and the Australian Media economy

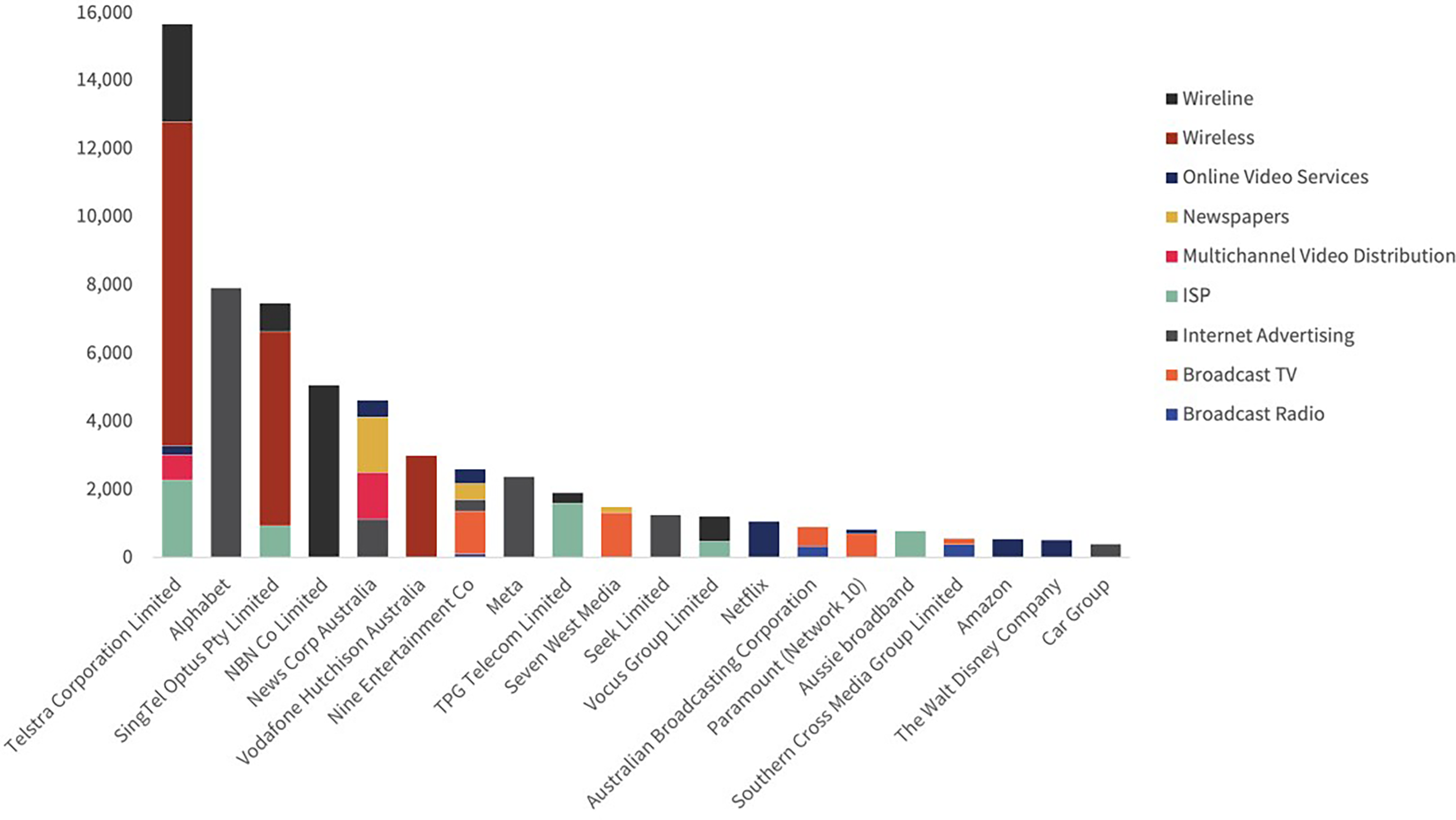

Australia has long been known for having one of the most concentrated media and telecommunications systems in the world with oligopolistic and monopolistic structures being the norm across print and broadcast media (Papandrea and Tiffen, 2016). Examples include a single player in the Pay TV market, a three-player market in Wireless, and increasingly fewer players in television, radio and print (Flew et al., 2024). It can also be noted that the Australian media system has always included a significant international presence, and this has grown substantially in recent years. When Papandrea and Tiffen reviewed Australian media. Telecoms and Internet ownership in 2011 (Papandrea and Tiffen, 2016), there were seven major Australian-owned media and telecommunications conglomerates: News Corporation Australia, Nine Entertainment (formerly PBL Media), Fairfax Media, Telstra, Seven West Media, Ten Network, and Southern Cross Austereo. 3 By 2021, this number had been reduced to five, with Ten Network sold to Paramount CBS in 2017 and Fairfax taken over by Nine in 2019. Of the top 20 companies in the Australian networked media economy (shown in Figures 1 and 2 below), only five of the top 10 companies (Telstra, NBN Co, News Corp Australia, Nine Entertainment and Seen West Media) are Australian-owned, with another five in the top 20 also being Australian-owned (Seek, Australian Broadcasting Corporation (government-owned), Aussie Broadband, Southern Cross Media Group, and Car Group).

Revenues of the top 20 telecommunications, internet and media companies operating in Australia, 2021 (millions, $AUD).

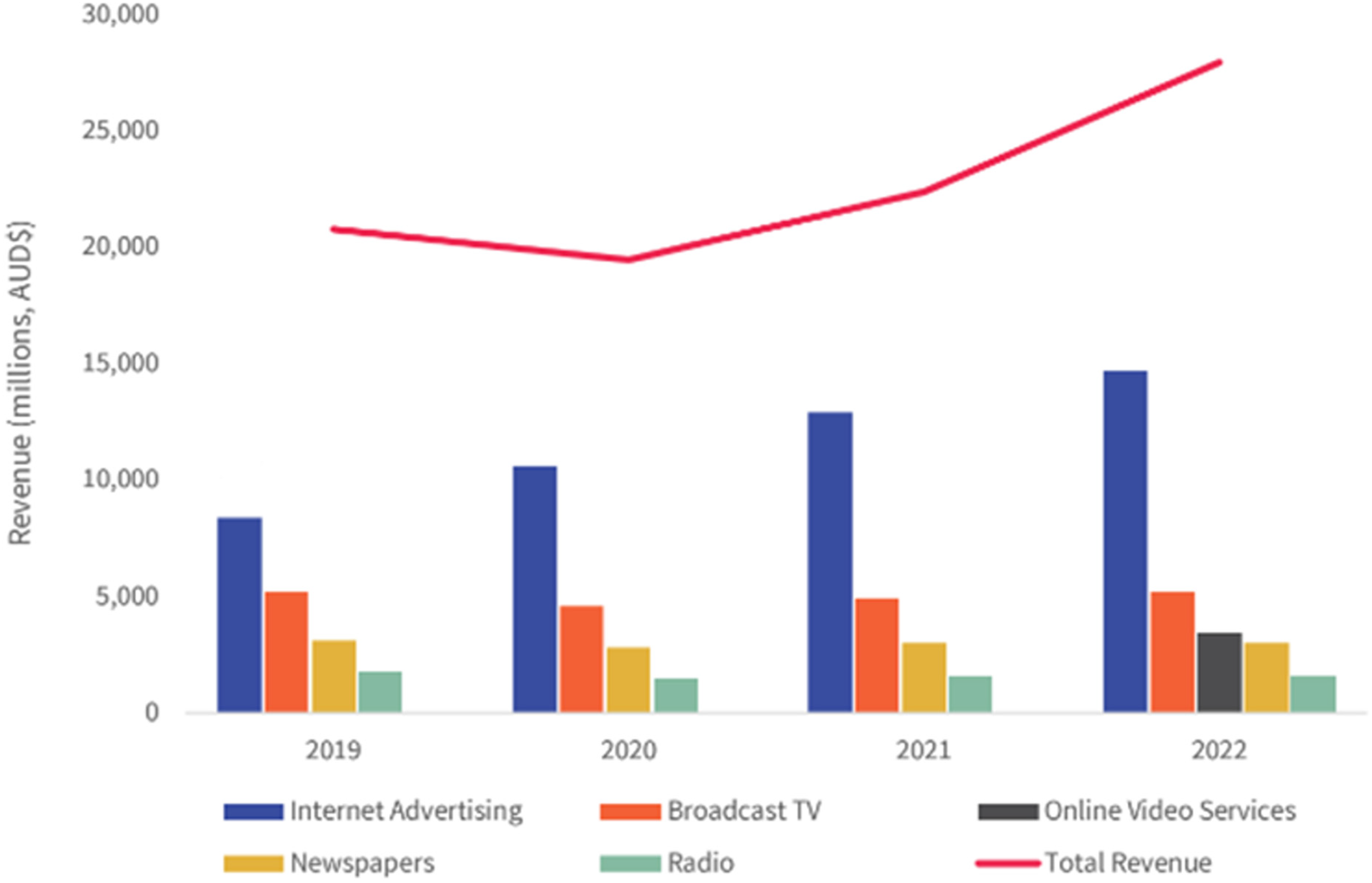

Revenues of online and traditional Media services in Australia, 2019–2022 (millions, $AUD). Source: Flew et al., 2024.

Recent work undertaken through the Global Media and Internet Concentration Project (gmicp.org) has sought to develop a new understanding of media concentration in Australia framed around the concept of the network media economy (Flew et al., 2024). The network media economy is defined as the comprehensive ecosystem encompassing various sectors of communications, internet and media industries with three sub-sectors:

Telecommunications and Internet infrastructure (mobile wireless and wireline telecoms, internet service providers (ISPs), and cable, satellite, and IPTV provider services), Online and traditional media services (broadcast television, pay television, online video services, broadcast radio, podcasting, newspapers, magazines and the music industries (recorded music, streaming and download services, publishing royalties, and concerts), Core Internet applications and sectors (internet advertising, social media and video sharing platforms, console, PC, and mobile games, app stores, operating systems and browsers).

The framework of the network media economy is intended to better capture the interconnected nature of these sectors and their collective impact on the overall media landscape, and to address the challenges facing industry-specific measures such as CR and HHI without eliminating the benefits that can be derived from quantitative benchmarks.

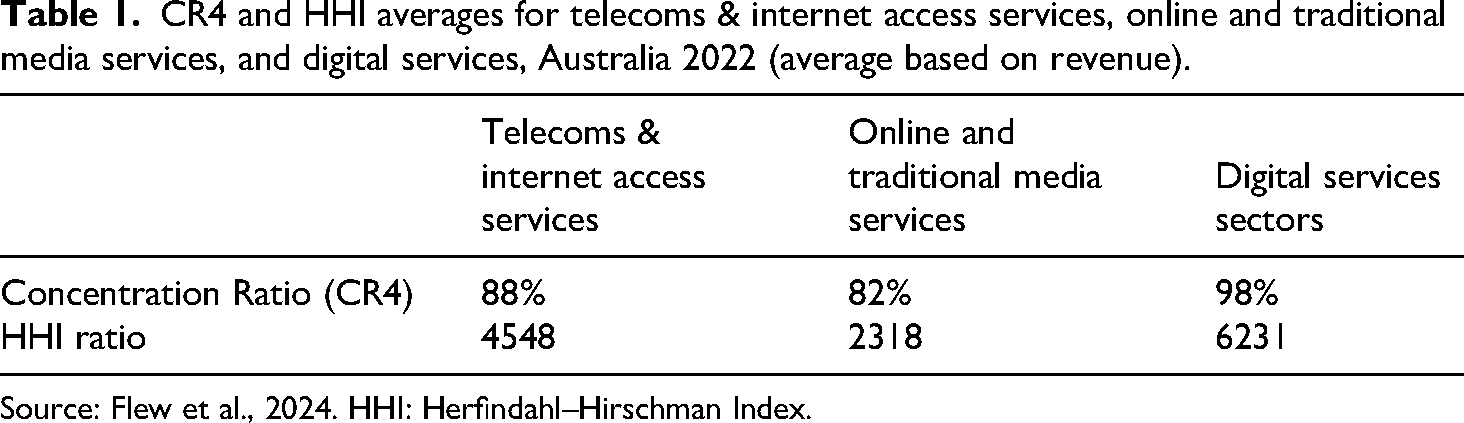

Australia continues to have some of the most highly concentrated telecommunications, print and broadcast media sectors in the world. The average HHI across the online and traditional media sectors of radio, newspapers, television and streaming was 2318 in 2022 (see Table 1). For telecoms and internet services, which includes wireless mobile, ISPs and wireline wholesalers, the pooled HHI was 4548 (Table 1)—a number well in excess of thresholds set by local and international competition regulators. However, the CRs for these traditional media and communications industries are significantly exceeded in all digital services sectors, where market dominance by one or two providers is very much commonplace. Alphabet, Microsoft, Meta and Apple's unprecedented market dominance in this sector is evidenced by a pooled HHI of 6231 for the same year (Table 1).

CR4 and HHI averages for telecoms & internet access services, online and traditional media services, and digital services, Australia 2022 (average based on revenue).

Source: Flew et al., 2024. HHI: Herfindahl–Hirschman Index.

This raises the question of whether the economic power of companies such as Alphabet (Google) and Meta now significantly exceeds that of the traditional media giants such as News Corporation and Nine Entertainment. While it has long been the case that telcos are considerably larger than media companies yet fly somewhat “under the radar” in discussions of media concentration and power, it is clearly now the case that Internet companies increasingly compete in spaces that have historically been the focus of traditional media, most notably digital advertising, as well as providing the underlying digital infrastructure and service platforms from which the content of other media content providers is accessed.

The Australian Report from the Global Media and Internet Concentration project sought to quantify this power by drawing upon publicly available data using ASX results, annual reports and industry reporting. What is shows is that while telecommunications and Internet access providers are highly dominant in terms of revenue share (Telstra, SingTel Optus, NBN Co and Vodafone Hutchinson), the digital service company Alphabet is now the second largest company in the network media economy and is larger than traditional media giants News Corporation and Nine Entertainment Co. Meta is the 8th largest company and is larger than all other media companies than the big telcos, News Corp and Nine.

The revenues of Alphabet and Meta in Australia are derived almost exclusively from digital advertising. Internet advertising was worth $14.7 billion in Australia in 2022, growing from $4.1 billion in 2012 and $10.6 billion in 2020. As Figure 2 below shows, digital advertising revenue in Australia is larger than television, streaming, print and radio revenues combined.

The rise of digital advertising has been monitored by Australian regulatory agencies such as the Australian Competition and Consumer Commission (Australian Competition & Consumer Commission, 2019b), and it has been observed that Internet advertising continues to pull ahead of traditional media sectors at a rapid pace. While the relationship between traditional media and the Internet companies has long been a “frenemy” one–news media and broadcasters amplify their produced content through distribution on YouTube, Facebook, Instagram, TikTok etc. (Tow Center, 2019)—the platform companies increasingly compete directly with traditional media. This is most apparent in the advertising space but is also increasingly a feature of the media content markets. In late 2024, it was estimated that YouTube accounts for over 10% of U.S. television viewing, while Amazon and Apple are major players in the global streaming market (Shapiro, 2024).

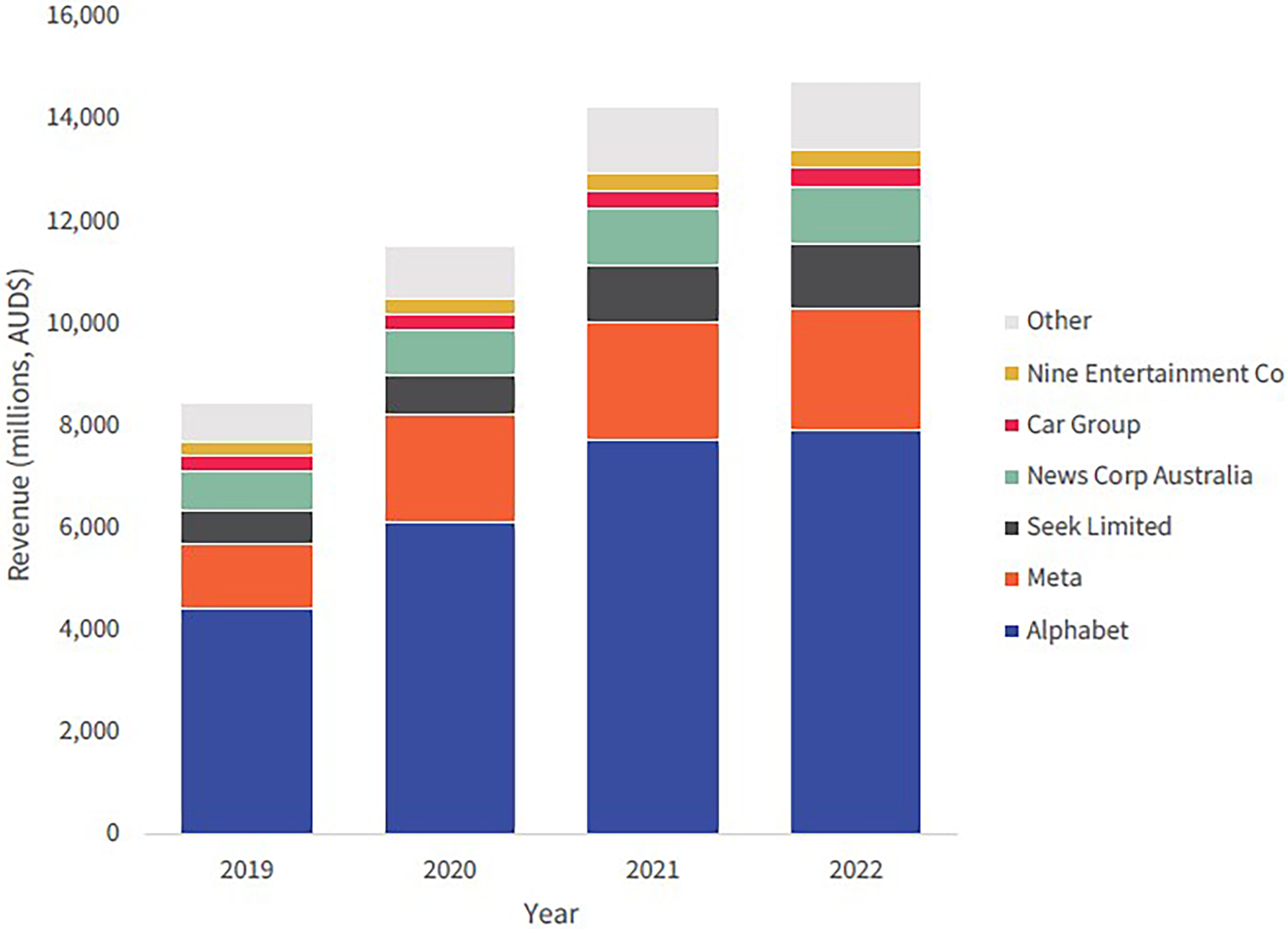

When we examine the digital advertising market in Australia in more details, we find that that Alphabet accounts for 53.3% of market share, with over $A8 billion in revenue in 2022. Their next largest competitor, Meta made $A2.3 billion revenue in 2022, or 13.3% of market share. Between them, Alphabet and Meta account for 2/3 of digital advertising revenues in Australia, followed by digital-only classified advertisers such as Seek and Car Group, and the online real estate arms of News Corp (realestate.com.au) and Nine Entertainment (Domain) Figure 3.

Revenues of internet advertising in Australia, 2019–2022 (millions, $AUD). Source: Flew et al., 2024.

This leads to questions about what it means for theories of media power to conceptualize platform companies as being dominant in what in the networked media economy. It has traditionally been assumed that other forms of power, such as political power and communications power, are downstream of economic power, particularly in critical political economy. But this leaves open the question of “power to do what?”. Historically, we associated concentrated media ownership with the desire for political influence, and this certainly remains relevant for understanding traditional media industries and markets. If we are to move analyses of media power from simply focusing upon “bigness” as evidence in itself of power (Flew, 2011)—noting that the media giants of previous eras are now in many cases battling for survival in an age of digital platforms and AI—the question of the ends and means of media power emerge in new ways.

Platforms and power: Moguls old and new

The 2024 US Presidential Election and its aftermath will be seen as marking a watershed moment in the relationship of platform owners to political power. The highly visible campaign of Elon Musk in support of Trump in the wake of the 13 July 2024 assassination attempt led to the America PAC, through which Musk managed his financial contributions, spending over $US200 million on the Trump campaign, making Musk by far the largest financial contributor. This investment in US Presidential politics proved to be remarkably lucrative to Musk and his companies. It is estimated that the stock market boom that followed Trump's election on 5 November added $US54 billion to Musk's net worth in 1 week alone, through the impact on the share prices of his listed companies Tesla and SpaceX. Even more remarkably, Trump made Musk the co-chair of his new Department of Government Efficiency (DOGE, named after Musk's favorite cryptocurrency), where he had unprecedented levels of access to government departments and agencies, including those that have regulatory oversight of the activities of his companies, and departments that make decisions on purchasing the products and services of his companies, including the Department of Defense. While 2025 saw a falling out in relations between Musk and Trump, and a related decline in the share market value of Tesla by 25% as of August 2025, there remains a degree to which Musk and other libertarian tech leaders such as Peter Thiel and Marc Andreeson have retained substantial influence over the Trump Administration, with particularly strong connections to US Vice-President JD Vance.

Where Musk went, other tech leaders followed. While Elon Musk's use of X to explicitly promote a right-wing, pro-business and pro-Trump agenda was in itself unique, tech leaders such as Amazon's Jeff Bezos, Apple's Tim Cook, Meta's Mark Zuckerberg and Google's Sundar Pichai were fulsome in their praise of Trump once elected, and all donated heavily to Trump's Presidential Inauguration. Subsequent to Trump's election, Zuckerberg declared that Meta had lacked “masculine energy,” and wound back measures to block misinformation and moderate content so as to be less “culturally neutered” (Morgan, 2025). Less metaphorically, Amazon CEO Jeff Bezos made it clear that the Washington Post, historically a beacon of liberalism and independent journalism, would be reorienting its opinion section in support of “personal liberties and free markets” (Folkenfirk, 2025).

The involvement of billionaires in politics is of course not new. Moreover, media owners have long had an inclination to use their news media outlets to intervene in the politics of the day, from Randolph Hearst and Lord Northcliffe in the first half of the twentieth century, to Rupert Murdoch, Silvio Berlusconi and Axel Springer in the second half of the twentieth century and the early twenty-first century. There is also a vast literature on the power of media moguls and the ways in which concentration of media ownership intersects with the capacity to achieve political power through the ideological influence that their media publications and broadcast networks can have over public political opinion (Birkinbine et al., 2016; Hardy, 2014; Mosco, 2009; Murdock, 1982; Wasko et al., 2014).

At the same time, there has been a sense that the model of power that is implicit in such frameworks, where powerful individuals and families appointed people to leadership roles who shared their values, and that such elite networks ensured that media content stays within particular ideological lines—what Chomsky and Herman famously termed the propaganda model of media power (Chomsky and Herman, 1988)—has been in decline. Three reasons are typically presented for this claim. First, while the figure of the all-powerful media mogul retains a high profile in the popular imaginary, there has been a shift over time from personal to impersonal ownership, with the separation of ownership and control, which as has characterized other sectors of the capitalist economy (Just, 2020; Scott, 2014). Eli Noam observed that, in the US context, the big investors in media companies were no longer colorful media moguls but rather a more anonymous set of institutional investors and investment banks (Noam, 2009).

Second, there has been a view that traditional print and broadcast media companies are facing unprecedented turbulence arising from the impact of the Internet and digital technologies. As a result, their overall influence over the media and information environment is challenged by the Australian media system rise of a variety of non-traditional media formats, including podcasting, blogging, Substack newsletters, YouTube videos and other formats that enable media content creators to reach audiences without reliance upon traditional media gatekeepers. The positive relationship of the Trump campaign to podcasters and YouTubers operating outside of the media mainstream, which of course Trump has spurned as purveyors of “fake news,” was taken to be the latest instance of the decline of mass media (Siegel and Spangler, 2024).

The third critique would arise from the perspective that companies such as Alphabet, Amazon, Apple, Microsoft, Meta and others are primarily technology businesses, whose engagement with media is incidental, contingent, and not at the core of their business models. This argument, as presented by Hesmondhalgh (2019), Lotz (2021) and Winseck (2023), has understood claims that these companies as de facto media companies as resting upon a fundamental category error. Referring to the once-popular acronym of the GAFAM (Google, Apple, Facebook, Amazon and Microsoft), Winseck summarized the two lines of critique as: (1) while these companies invest in media content production and distribution (YouTube, Apple + TV, Amazon Prime etc.), this constitutes only a small fraction of their overall revenues; and (2) the processes through which content is moderated on social media platforms is profoundly different to that of traditional media decision-making, and these platforms have not become publishers in the sense in which the term is understood in legal and policy discourse. Winseck concludes that “the GAFAM + group of companies are better seen as giant IT conglomerates with significant media subsidiaries” (Winseck, 2023: 239).

If we shift the analytical lens from questions of media content production and distribution to that of power and focus less upon whether or not digital platform companies engage in traditional media production practices and instead upon how platform dominance can shape political discourse and the public sphere, then we can see several ways in which the economic dominance of digital platform companies matters to media and communications. The capacity of tech companies to exercise political influence has been widely noted (Popiel, 2018, 2022) and clearly took a step-change with the election of Trump in 2024. It is also the case that such influence within U.S. politics is being used as a catalyst to take on regulations in Canada, Australia, the United Kingdom and the European Union viewed as unfavorable to the conduct of platform businesses. The capacity to shape the broader cultural and ideological agenda is also something that needs further unpacking. Again, Musk is an outrider in that he has 200 million-plus followers of his comments on X as its owner, but the question of whether platforms are essentially agnostic about the content that appears on the sites that they own is open to question. The conscious decision of Meta to downgrade news on its Facebook and Instagram sites is a less visible, but no less powerful, manifestation of political preferences on digital platforms as Musk's conscious strategy of promoting right-wing influencers and cryptocurrency evangelists on X.

More generally, we would argue that the attributes that scholars, activists and regulators have associated with the concentration of ownership and dominance of markets in traditional media industries can be seen to apply with regard to the dominance of particular tech companies over digital markets. Market power reduces overall levels of competition by squeezing out both potential competitors within digital markets (e.g. the difficulties in setting up a competitor to Google in search, or Meta in social media), and in cognate markets. The relevant case here is that of digital advertising, where the power of other media companies to compete with Google and Meta is significantly constrained (Nieborg and Poell, 2025). The focus of our analysis on distribution and its relationship to revenues reveals that both traditional media and platform companies are competing for advertising revenues, for audiences, and to an increasing degree to content and content creators. The concept of the network media economy provides us with a framework through which we can think holistically about telecommunication, print and broadcast and digital economy industries and markets that recognizes the increasingly conglomerate and multi-sectoral nature of such entities.

Media concentration data and analyses of the changing media supply chain provide us with tools to think through the relationship, not only of Alphabet and Meta to traditional media, but also Apple, Amazon, Netflix, Spotify and potentially other “born digital” businesses. It also draws attention to the increasing centrality of digital revenue streams to traditional media businesses, manifesting itself not only in competition in existing markets (e.g. Netflix and Amazon moving towards live sports on streaming platforms), but also how businesses such as online real estate increasingly fund traditional media giants such as News Corporation and Nine Entertainment.

One implication of our analysis is that it continues to make sense to think about concepts such as the public sphere as providing normative principles that can inform public policy towards digital platforms. The case of misinformation is an example. Legislating against misinformation on digital platforms is one option, although as we have seen in Australia, it opens up big questions about who are the “arbiters of truth,” and whether this is a process that can be removed from the space of the political. A more effective guardrail against misinformation is provided by continuing to invest in professional news production and the sustainability of news businesses. Concepts such as news media bargaining codes make more sense when considered in this way, rather than in terms of propping up incumbent news publishers.

We can also think about different sectors, not just as competing firms, but as competing fractions of capital. The extent to which digital tech policy is tied up with communications regulation draws attention to the degree to which inter-capitalist competition is fought, not only in the economic marketplace, but also through political bargaining and the competition for economic rents. While the pursuit of economic profits through political bargaining in order to access economic rents has typically been associated with the incumbent media in their responses to digital challenges, with the Australian News Media Bargaining Initiative (formerly Code) as an example, we are likely to see increasing rent-seeking by tech companies in the U.S. under the Trump Administration as they increasingly move towards the center of executive power (the relationship between tariffs and tech policy being one possible example).

Finally, the case of Elon Musk alerts us to the possibility that the relationship between economic power and the pursuit not only of political power, but also cultural and ideological power, is not simply an artifact of the twentieth century era of media moguls. Indeed, X—which in its former incarnation as Twitter was once promoted as the digital infrastructure of the new public sphere (Bruns and Highfield, 2015)— has in fact turned out to be one of the most effective vehicles through which a media mogul can broadcast viewpoints to an audience of hundreds of millions that can amplify and shape the policies of his preferred political leader. How platforms matter, then, has started to look a lot like the ways in which media power has long mattered in critical communications studies. The rise of the global Internet has not led to the much-anticipated decentralization of media power and associated decline of powerful media owners.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author received financial support for the research, authorship, and/or publication of this article through their participation in the Social Sciences and Humanities Research Council of Canada-funded Global Media and Internet Concentration Project.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

All data generated or analyzed during this study are included in this published article and supplementary information files, while the data sets for it and all contributors to the GMICP can be found on Dataverse, which is a public archive dedicated to preserving scholarly publications and data sets that is operated by a consortium of Canadian universities ![]() .

.