Abstract

This article calls for systematic analysis of the accumulation and exercise of institutional platform power in the digital economy. We examine how the relatively open mobile advertising ecosystem is nevertheless dominated by a handful of platform conglomerates, most prominently Google, Facebook, and Apple. Although extant scholarship acknowledges the concentration of corporate power in digital advertising, as well as its cultural, societal, and environmental harms, a comprehensive approach to platform power is missing. Providing a framework to develop such insights, we analyze how shifts in the advertising ecosystem are driven by four interrelated institutional platform strategies: infrastructuralization, platformization, conglomeration, and financialization. The 2021 introduction and subsequent rollout of Apple’s App Tracking Transparency framework serves as an example to demonstrate that even though institutional relationships of dependence are constantly evolving, control over infrastructural nodes tends to entrench the already dominant position of leading platform conglomerates.

Introduction

One of the main drivers of the online economy is digital advertising. It is the principal source of revenue for some of the most valued tech conglomerates in the world. Because of its size—generating $600+ billion globally (Lebow, 2023)—even a minuscule stake in this market translates into a significant sum of money. As a result, a wide range of institutional actors—platform companies, technology start-ups, data intermediaries, ecommerce and retail giants, and many others—are actively vying for control not only over market share, but also over trading protocols and technology standards (Braun, 2023; MacKenzie et al., 2023), over advertising tracking and targeting infrastructures (Srinivasan, 2020; Turow, 2011), and over definitions of what constitutes privacy (Crain, 2021; McGuigan et al., 2023).

Fueling the already dynamic nature of the digital advertising industry has been a constant influx of businesses entering a decidedly crowded and institutionally complex ecosystem (Van der Vlist and Helmond, 2021). This means that, at its core, the market for digital advertising has relatively low barriers to entry. Achieving growth depends on a company’s ability to advance one (or more) of the industry’s key imperatives: (1) aggregate supply or “advertising inventory” (i.e. publishers selling “impressions”); (2) aggregate demand (i.e. “eyeballs” or consumers); or (3) decrease friction in matching supply and demand via various kinds of market intermediation by providing services such as automated auctions (“exchanges”), data management tools, and advertising attribution technology (McGuigan, 2023). Further indication of the low barrier to market entry is the arrival of incumbent businesses that seek to increase their digital advertising revenue. For example, large US-based retailers, such as Target and Walmart, with large pools of known customers have been increasingly successful in “monetizing” their customers by enabling advertising in their digital storefronts.

Yet, despite the market’s openness, like most sectors of the platform economy (Srnicek, 2017), only a handful of institutional actors dominate the market and have an outsized influence over digital advertising (Barwise and Watkins, 2018). Most prominent are Google (Alphabet), followed by Facebook (Meta), which together rake in half of worldwide digital advertising revenues. As a result, the former faces significant legal scrutiny because of a seemingly endless series of anticompetitive industry practices (Geradin et al., 2021; United States of America v. Google LLC, 2023). Notably, many of these practices are not only economic or financial—for example, acquiring competitors or manipulating ad auctions and prices—but also very much infrastructural in nature. Google, for example, has been found to force corporate customers to adopt its tools and technology, or to deny competitors and partners access to key data, products, and services (Srinivasan, 2020). This behavior has contributed to a high level of industry integration, both economically—for example, preferred partnerships and revenue sharing—and infrastructurally—for example, exchange of data (Helmond et al., 2019; Van der Vlist and Helmond, 2021).

This article examines how these leading platform companies accumulate and exercise power in the relatively open, yet highly integrated digital advertising industry. As such, we are less concerned with the myriads of privacy-related issues pertaining to individuals in their role as ad targets. There is a rich body of scholarship on the broader implications of “tracking technology” on end-users and the emergence of pervasive surveillance on democracy writ large (Turow, 2011; Zuboff, 2019). We aim to contribute to these urgent conversations by providing insight into the operationalization of institutional platform power in the digital advertising ecosystem. A key question in this inquiry is how leading platform conglomerates have developed and gained control over key infrastructures for datafication. In the case of digital advertising, these infrastructures primarily revolve around access to cookies and device identifiers, which enable the identification, tracking, and targeting of individual devices. The platform conglomerates that control access to these data signals wield significant institutional power.

We understand institutional platform power as the ability of dominant platform conglomerates to sustain, influence, or impede the actions of other institutions—which in the case of digital advertising are predominantly corporate actors—through economic, infrastructural, and regulatory interventions. 1 These interventions, as the article will show, can have far-reaching consequences for entire economic sectors, from large sections of the media and telecommunication industries to the advertising and platform ecosystems themselves. Analyzing how, when, and where platform companies wield institutional power over other corporate actors is necessary not only because of the advertising industry’s economic impact, but also because of its opacity and startling complexity (Broughton Micova and Jacques, 2020; Rieder and Hofmann, 2020). Detailed empirical investigations focused on specific infrastructural objects and datafication practices are meant to induce effective policy interventions related to platform competition, privacy debates, or digital advertising as a key revenue source funding the media and communication industries.

To address the question of institutional platform power in digital advertising, we focus our investigation on the mobile advertising ecosystem, which in 2024 constitutes the fastest growing segment of the digital advertising industry. After reviewing the extant literature on platforms and advertising, we pursue our inquiry in two steps. First, we analyze how a handful of dominant platform conglomerates have accumulated power in the market for digital display advertising over the past two decades. We argue that these conglomerates have done so by deploying four interrelated platform strategies: infrastructuralization, platformization, conglomeration, and financialization. Second, we closely examine how one of these conglomerates—Apple—exercises platform power as it reshapes the mobile digital advertising ecosystem. 2 In practice, it is not necessarily straightforward to separate these two steps. Nevertheless, it is analytically useful to separate the accumulation of power, which refers to forging institutional relations and amassing infrastructural and financial resources, from the exercise of power, which refers to moments during which platform companies substantially alter the circumstances under which third parties can operate. When a platform has accumulated significant power, such moments can have an outsized impact on the overall market.

In this article, we will demonstrate the two steps through a case study on the 2021 introduction of Apple’s App Tracking Transparency (ATT) framework—a “privacy” feature newly integrated into version 14.5 of Apple’s iOS mobile operating system (Apple Inc, 2024a). This new setting, which after installation of the new version of iOS was switched on by default, cuts off access for advertisers and data intermediaries to a mobile device’s “identifier for advertisers” (IDFA). 3 Crucially, without this key piece of data or “signal,” competing platforms, advertisers, and data intermediaries find it more difficult to identify and track individual users across websites and apps. Consequently, publishers cannot “attribute” the impression of an advertisement to an individual’s in-app action, such as a purchase (i.e. a “conversion”). As we will demonstrate, even though the recent history of mobile advertising is littered with numerous changes in technology, standards, and affordances, changing the IDFA functionality profoundly altered the relationship among platforms within the digital advertising market. This article thus provides a framework for analyzing evolving relationships of dependence in platform ecosystems.

Theorizing institutional platform power

This inquiry builds on scholarship situated at the intersection of critical advertising studies, critical political economy and business studies, and platform studies. We begin with the advertising-related literature and how it allows us to analyze institutional platform power.

The broader field of marketing and advertising studies is vibrant and expansive, as indicated by review articles charting current and future research (Boerman et al., 2017). Hewing close to management science (McGuigan, 2023), this field’s central concern is how to target users in their role as recipients of advertisements (i.e. consumers). Research focuses on consumer behavior, advertising perception and its effectiveness, as well as on the role of intermediaries. In the same vein, recent research on advertising in computer science is concerned with measuring the effectiveness and privacy impact of advertising technologies. We will draw on a subset of this work (Cheyre et al., 2023; Kollnig et al., 2022), as it has made valuable empirical contributions to measure the material impact of Apple’s infrastructural changes central to our analysis. Yet, missing in this literature is research on institutional dependencies and power dynamics within an ecosystem that is fully under the purview of platform conglomerates.

Situated in the broader fields of media and communication, critical advertising studies does bring a series of normative issues to the fore that question the functioning, or even the necessity of targeted advertising by: (1) debating the legitimacy of this type of advertising because of its discriminatory practices and negative impact on user privacy (Braun, 2023; Crain, 2021; McGuigan, 2023); (2) recognizing that the constant introduction of novel technologies increases institutional opacity, which frustrates the ability to adjudicate how corporate actions and infrastructures impact other actors (Rieder and Hofmann, 2020; Van Dijck et al., 2019); and (3) showing that this market is prone to corporate concentration and rife with asymmetrical institutional relationships (MacKenzie et al., 2023; Srnicek, 2017).

Critical advertising scholars thus enhance our understanding of vital historical developments, dominant industry practices, and key tools and technologies. For example, they have shown that one of the main catalysts of the industry’s complexity and opacity has been the introduction of “programmatic” (i.e. automated) buying and selling of advertising inventory (Braun, 2023; McGuigan, 2023). This maddeningly convoluted industry practice favors the large-scale collection of historical and real-time data (on consumers) to be able to make an informed “bid” (on inventory) in automated auctions. To make and accept better bids, buyers and sellers thus far benefited immensely from access to a persistent user or device identifier. Until recently, mobile operating systems included such an identifier via Apple’s IDFA or the Google advertising ID (GAID) for Android-powered devices. Because user data is non-rival—collecting it does not preclude other companies from also collecting it—the industry favors institutional logics that seek scale, aggregation, and integration. As platform scholars have noted, these are exactly the economic and infrastructural imperatives that constitute platform markets (Blanke and Pybus, 2020; Poell et al., 2019).

We draw on this body of work as it helps us to institutionally and historically contextualize the introduction of Apple’s ATT framework. Yet, because critical advertising scholars take the digital advertising ecosystem as their focus, less attention is paid to the continued strategic maneuvering of key institutional actors. Nor has this field connected its overall normative assessment of digital advertising’s negative externalities with detailed analyses of how platforms companies have achieved a dominant market position. While critical advertising scholars are keenly aware that a handful of institutional actors have gained control over vital digital advertising infrastructures, practices, and standards, the question of inter-platform power—competition among Apple, Google, and Facebook in particular—vis-á-vis intra-platform power—control over third parties or “complementors”—has been less of a concern. This leads us to scholars who have engaged with the economics and infrastructures of digital advertising platforms.

The platformization of advertising markets

For any economist—whether mainstream economists, critical political economists, management scholars, or economic sociologists—the observation that the advertising industry is prone to corporate concentration would not be the least bit surprising. Why? At its core, advertising constitutes a multi-sided market, populated by newspapers, websites or apps providing inventory on the supply (or sell) side, versus a demand (or buy) side populated by those seeking to persuade end-users. Any platform company that aims to act as an intermediary to facilitate transactions between these two sides is heavily incentivized to pursue aggregation on one or both sides of the market to benefit from economies of scope and scale (Barwise and Watkins, 2018; Gawer, 2021). Moreover, on the supply side, owning large amounts of advertising inventory, for example, by operating a search engine or popular “social” apps, provides a clear competitive advantage. Likewise, an advertising aggregator’s ability to establish relationships with other publishers (cf. Helmond et al., 2019), translates into more advertising inventory, which, in turn, provides access to data on a larger, more diverse set of customers.

Because this work of aggregation involves building networks and partnerships on both the demand side and supply side, to put it in economic terms, advertising platforms are subject to indirect network effects. With positive effects, the more supply—publishers joining an advertising network—the more valuable that network becomes on the demand side—that is, for advertisers. Thus, the literature on multi-sided (or “platform”) markets provides a series of explanations as to why the industry is “bifurcated” (Braun, 2023: 266), with a small group of big players (i.e. predominantly platform companies), and a big group of small players, think of many thousands of data intermediaries, ad networks, and specialized tool and technology providers. Getting at the root of this bifurcation is important to be able to contextualize the role of Apple in the mobile ecosystem, as well as the institutional implications of the introduction of the ATT framework. In sum, these economic perspectives deepen our understanding of institutional platform power by providing a macro perspective on platform markets. To understand the material politics of platform power, we turn to platform and app studies, which theorized and analyzed how corporate actors integrate infrastructures and partnerships.

In “early” work in the emerging fields of platform and app studies, the ability of platform companies to connect an ecosystem of third parties has been theorized as platformization, or the ability to extend beyond their own infrastructural boundaries through integrations in external (i.e. third-party) websites (Helmond, 2015), and more recently, integrations in third-party mobile apps (Nieborg and Helmond, 2019). The prototypical example of such an integration from a decade ago is the now defunct Facebook Like button, which was integrated in external web properties of “first-party” websites. This institutional logic afforded “decentralized” data gathering—that is, taking place outside a platform’s own boundaries—not only fueled the expansion of ad tracking, but also found its way into mobile devices (Blanke and Pybus, 2020).

Platform scholars show that in the realm of mobile advertising, data is not primarily gathered via login functionalities, but via the integration of so-called software development kits or SDKs, provided by the familiar platform companies, as well as data management platforms and businesses providing attribution technology (Blanke and Pybus, 2020). For example, a generic app—such as a mobile game—can opt to integrate Google’s SDKs to gather in-app insights or Facebook’s SDKs to “monetize” its in-app ad inventory. Your typical app is therefore integrated with many dozens of external (i.e. “third-party”) SDKs. Not all SDKs function as “ad trackers,” a great many are used for app development as well (Pybus and Coté, 2024). As such, from the perspective of platform studies, apps can be seen as modular software that consist of a number of SDKs, each of which incorporate Application Programming Interfaces (APIs) that allow for automated data exchanges among SDK operators, data intermediaries, advertisers, and publishers (Dieter et al., 2019). Crucially, third-party SDKs, together with their embedded APIs, are fully integrated into an app’s codebase and cannot be switched off, removed, or blocked by users. This material embeddedness shifts control over data collection away from end-users and toward the operators of mobile operating systems (i.e. Apple and Google). SDKs, as digital utilities for app developers, make developers “platform-dependent” as they come to rely on the services provided by SDK providers (Poell et al., 2021).

The reason to pay specific attention to how the process of platformization is operationalized via SDK and API integrations is that such a material perspective addresses an issue frequently raised by platform scholars: the extent of infrastructural power (Lomborg et al., 2023; Plantin et al., 2018). One of the key questions we will return to in our analysis is how institutional platform power is made explicit by controlling access to and usage of “infrastructural nodes” (Broughton Micova and Jacques, 2020; Van Dijck et al., 2019) or “chokepoints” (Braun, 2023). Past scholarship suggests that the control over ad targeting and tracking is determined by both administrative and contractual means—the governance frameworks formulated by SDK providers, such as platform companies—and via material means, granting access to key infrastructural (data) objects (Van der Vlist and Helmond, 2021). The introduction by Apple of the ATT framework, therefore, should be seen as a part of a longer historical shift in the political economy of digital advertising marked by fierce inter-platform rivalry over access to and control of infrastructural nodes.

Finally, platform scholars have argued that besides the twin strategies of platformization and infrastructuralization, it is also vital when analyzing platform power to examine the more traditional corporate strategies of conglomeration and financialization (Jia et al., 2022). We understand the former as the centralization of corporate control within an industry through horizontal and vertical integration, and by establishing and incorporating subsidiaries via corporate mergers and acquisitions (Mosco, 2009). Transnational corporations seeking synergies and scale through a conglomerate structure do so by leveraging the strategy of financialization, which is defined as nonfinancial firms engaging “in financial operations—such as investing in financial securities, increasing leverage, or repurchasing their own shares and acquiring potential competitors” (Klinge et al., 2023: 336). As we will see in the following analysis, Google, Meta, and Apple have pursued a combination of all four strategies in their efforts to gain control over the digital advertising ecosystem.

How platforms accumulate institutional power

A key driver behind the complexity and opacity of advertising technology ecosystems has been the relentless pursuit of an unfulfilled promise: the ability to match a tailored ad with a specific individual, ideally in real time (Turow, 2011). This deterministic desire became increasingly plausible with advances in computing and connectivity, translating into sizable corporate investments in research and development (Crain, 2021; Srnicek, 2017). As noted in the introduction, any company able to deliver on this promise at low cost, at scale, and with high precision is set to make billions. To be sure, given the technological complexities of this endeavor, let alone its privacy implications, there has been an ongoing debate whether digital advertising is really as effective as has been implied by both its proponents and detractors (Braun, 2023; Broughton Micova and Jacques, 2020). Despite these reservations and the enduring specter of regulatory intervention, a seemingly straightforward industry practice has morphed into a convoluted “calculative evolution” (McGuigan, 2023): matching an “impression” with an action (i.e. to facilitate a “conversion”); verifying this matching process (i.e. an “attribution”); automating its ‘optimization’; and doing so preferably in milliseconds.

What became immediately apparent in the early days of digital advertising, and still rings true today, is that for any effective targeting to take place, both advertisers and publishers benefit from access to persistent, unique identifiers. This perceived imperative—to gather personal data at scale—prompts the question which corporate actors are ultimately in control over access to any such signals. We will address this question, which effectively concerns the accumulation of platform power in the digital advertising market, by examining four platform power strategies pursued by the leading conglomerates. In doing so, we are reminded that institutional relationships are constantly shifting, but also that markets such as those for digital advertising are not natural phenomena but the result of ongoing negotiation.

Infrastructuralization

The genesis of digital advertising lies in the mid-1990s, with the mass diffusion and domestication of desktop computers, affordable Internet connectivity, and the adoption of accessible web browsers (Crain, 2021). Historical studies covering digital advertising’s formative first decades from the mid-1990s to 2010 point to two complementary developments: browser-based cookies and the automated trading of ad inventory via advertising networks (McGuigan, 2023; Mellet and Beauvisage, 2020; Turow, 2011). These became the vehicles to deliver on digital advertising’s aforementioned promise: cookies afforded user targeting and tracking, while ad networks—and later ad exchanges—facilitated ad transactions at scale. Their evolution is marked by constant corporate conflicts over the openness of the infrastructural ad stack, ultimately leading Google to become infrastructurally dominant. But how did Google attain this institutional position?

Invented in 1994, “web cookies” or “http cookies” are simple text strings that allow website operators to place text files “into the memory of the browser” (Jones, 2020: 89). Initially, such first-party cookies—set by the website a user visited—came with recall functionality, for example, to ensure that the contents of an online shopping basket did not disappear when closing a browser window. In the late 1990s, however, advertisers recognized the inherent tracking capabilities of cookies, which led to “the birth of profiling and behavioral targeting” (Mellet and Beauvisage, 2020: 118). This functionality was soon complemented by the ability of external companies unrelated to the first-party to also set “third-party” cookies to facilitate “cross-site” tracking and the large-scale gathering of personal data (Lomborg et al., 2023: 356). The widespread adoption of third-party cookies positioned the developers of web browsers as infrastructural arbiters of ad tracking technology.

If cookies are the rocket fuel (i.e. data) that “added an unprecedented level of granularity to existing advertising techniques,” then ad networks became the engine to propel the advertising ecosystem forward (Crain, 2021: 67). That is, in the late 1990s, ad networks emerged as infrastructural conduits to buy and sell users at scale. First and foremost, they solved a logistical challenge by positioning themselves as “intermediaries between web publishers looking to sell ad inventory and marketers looking to reach sizable audiences” (Crain, 2021: 61). Against the background of the dot-com bubble, which popped in the year 2000, the US-based company DoubleClick went on to become one of the most successful ad networks. During its ascendance, it built foundational advertising infrastructures, developing targeting and tracking software tools, and building data centers to store cookie data (Crain, 2021: 89). Importantly, DoubleClick leveraged its institutional position as an intermediary to integrate infrastructurally with both advertisers (the demand side) and publishers (the supply side) by providing accessible services. This strategy paid dividends and led to a successful public offering in 1998.

In the 2010s, the advertising ecosystem saw two more major infrastructural shifts, which consolidated Google’s control over the ad ecosystem while also laying the foundations for a counterforce. First, ad networks were complemented by ad exchanges, or “centralized markets” for the automated or “programmatic” buying and selling of “audience impressions” accessible to “any party—networks, publishers, and even advertising agencies” (Turow, 2011: 79). Because this process favors speed—think milliseconds—the advertising ecosystem became more dynamic and even more intricate. Seizing on its momentum, Google went on to cement its infrastructural position in the ecosystem by positioning its own ad exchange, AdX, as the go-to destination for automated ad trades (Srinivasan, 2020).

Second, spurred by the 2007 introduction of the Apple iPhone, the eyeballs of consumers started to move from the web to apps (Goggin, 2021). Although automated ad trading technologies and ad exchanges, as well as data intermediaries and aggregators, remained relevant, the locus of infrastructural control shifted from the web browser to the mobile operating system. Desktop operating systems and web browsers have historically been more open than Apple’s integrated approach to fusing mobile hardware and software combined with controlling app distribution via its App Store. This has meant that both app developers and end-users are much more limited in their ability to access or block mobile device data. We will revisit the nuances of these industry and ecosystem transitions in our analysis of the ATT framework. Foreseeing the threat to its dominant position in digital advertising, Google, once again, made a pre-emptive strategic infrastructural move by acquiring Android, the mobile operating system, in 2005. Android came to serve as Apple’s operating system’s principal competitor.

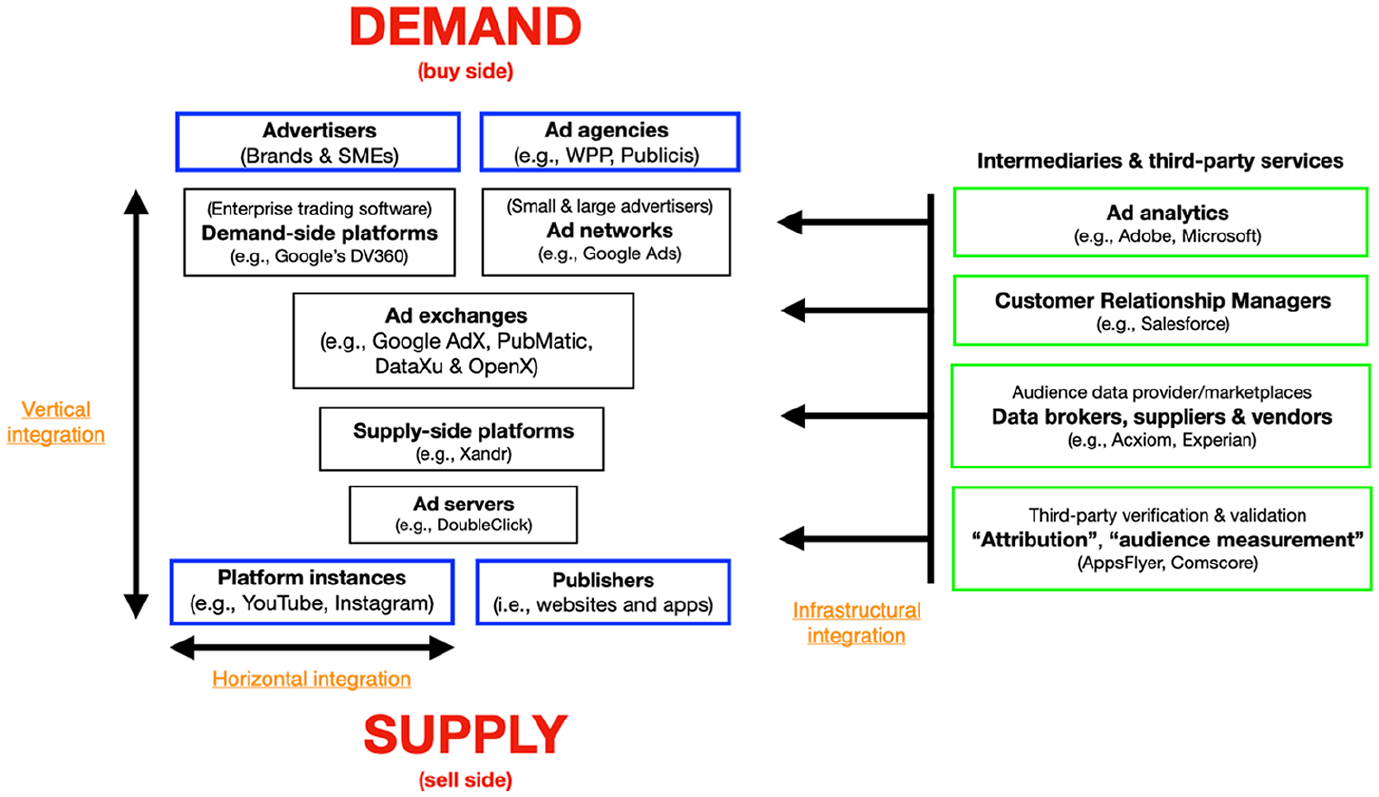

With this, the key infrastructural components of the mobile advertising ecosystem were in place. Drawing on past visualizations (Broughton Micova and Jacques, 2020; Srinivasan, 2020; United States of America v. Google LLC, 2023), Figure 1 presents a simplified version of the programmatic ad stack. Here, we use the notion of a stack rather than a network or ecosystem not only because it is a common industry term, but also because the notion of an integrated stack draws attention to Google’s ambition to control individual infrastructural nodes and combine them into an integrated series of infrastructural objects (Van Dijck et al., 2019). The black boxes all denote infrastructural nodes, whereas the green boxes represent data intermediaries and technology providers, which relate to various nodes across the stack. As suggested by the vertical arrow, the entire ad stack is prone to both vertical infrastructural and corporate integration, with Google in particular owning and operating various key nodes. The blue boxes consist of many thousands of actors on either the demand side (e.g. small and medium enterprises or SMEs) or the supply side, while at the bottom of the stack we find platform and app instances—for example, YouTube and Instagram. At this level, horizontal integration occurs, as platform companies aggregate diverse audiences on the supply side. In the following sections, we unpack how this strategy of platformization is leveraged to facilitate seamless communication across infrastructural nodes.

The programmatic ad stack.

Platformization

Even though Google has made many successful and highly lucrative efforts to control key nodes in the digital advertising stack, the entire ecosystem remains decentralized. For instance, as illustrated in Figure 1, on the demand side one finds an abundance of aggregators (e.g. Demand Side Platforms or DSPs) and numerous ad networks other than Google’s. Management scholars might argue that this level of decentralization stems from a platform firm’s incentive to “open” their economic and infrastructural “boundaries” (Gawer, 2021). No single platform owns a dominant share on the supply side, which is populated by many thousands of apps and websites. Likewise, the ability to carry out basic business practices, such as making informed bids at ad auctions, requires vast amounts of data that are difficult for any single company to acquire, store, and process. Therefore, digital advertising necessitates infrastructural integration of third parties, which alongside infrastructuralization, leads us to platformization, the second strategic lever constituting institutional platform power.

As discussed in the previous section, platformization can be seen as decentralized data capture (Blanke and Pybus, 2020), or more accurately, the marshaling of economic and infrastructural resources by platform companies to extend their reach beyond the boundaries of their own firms. By virtue of their multi-sided nature, platform companies are inherently incentivized to forge institutional relationships (Gawer, 2021; Helmond et al., 2019). Thus, platformization and infrastructuralization go hand in hand—forging infrastructural intra-platform relationships through extensions and integrations (Helmond, 2015; Plantin et al., 2018).

More so than their competitors, Facebook and Google have each become increasingly capable in integrating their extensions with third-party publishers and apps, thereby aggregating ad inventory and transmitting accurate, real-time user data in a “platform-ready” format (Helmond, 2015). For example, Facebook’s advertising SDKs are integrated into popular apps and their “social plug-ins,” such as login buttons, extend the platform’s infrastructural reach deep into the app economy (Nieborg and Helmond, 2019). Likewise, Google’s Firebase SDK, dubbed a “super-SDK,” is integrated in over 3 million third-party mobile applications (Pybus and Coté, 2024). Privacy concerns have emerged around SDK integration, as SDKs have historically been the primary means to access device identifiers, which facilitate user tracking. For those concerned about privacy, which Apple purports to be (cf. McGuigan et al., 2023), limiting or downright denying access to information on a users’ mobile device presents a relatively straightforward way to frustrate tracking users and building comprehensive user profiles. In other words, the owners of mobile operating systems are positioned to limit the process of platformization, which aligns precisely with ATT’s intended purpose.

Conglomeration and financialization

As the above analysis suggests, both Google and Facebook have aggressively pursued the corporate strategy of conglomeration. Google, in particular, has aimed from early on to vertically integrate the ad stack (Geradin et al., 2021; United States of America v. Google LLC, 2023). Central to this ambition was the previously mentioned acquisition of DoubleClick (Crain, 2021: 140–141). Acquiring the ad network in 2008 for $3.1 billion, Google in one fell swoop gained control over two central infrastructural nodes in the digital advertising stack. Through DoubleClick, it acquired both a nascent ad exchange (AdX) and, more importantly, the network’s ad servers (see Figure 1). After the acquisition, Google restructured these services to operate at a larger scale, facilitated by the data centers it had built in the previous decade (MacKenzie et al., 2023). Integrating DoubleClick in its burgeoning conglomerate, Google became the central player in the emerging programmatic advertising market, facilitating “automated real-time choice between the highest real-time bids for a publisher’s ad slots and the demands of the publisher’s direct deals with advertisers” (MacKenzie et al., 2023: 563). In addition, as can be seen in Figure 1, Google went on to integrate and expand demand-side platforms in its digital advertising stack, including Google Ads (for small advertisers) and DV360 (an end-to-end marketing platform), an outgrowth of Google’s 2010 acquisition of Invite Media (Srinivasan, 2020: 88).

At the same time, Google and Facebook have pursued a strategy of horizontal integration on the supply side. Both companies have done so by establishing and incorporating subsidiaries, most prominently, through acquisitions. In 2006, Google bought YouTube, while in 2012 Facebook acquired Instagram. Besides these high-profile examples, both companies have bought numerous smaller firms, as well as invested in tech start-ups, primarily to strengthen their position in the digital advertising market (Srnicek, 2017: 59). Having integrated key nodes in the advertising ecosystem, the two conglomerates often act as both agents and counterparties to advertisers, which, not surprisingly, has raised concerns among regulators (Geradin et al., 2021; McGuigan et al., 2023; Srinivasan, 2020).

Of course, these corporate strategies to diversify business operations can only be pursued successfully if they run parallel to the process of financialization. As Crain (2021) has argued, the strategic use of capital first became apparent during the dot-com bubble of the late 1990s. Inflated valuations “generated a kind of marketing/finance feedback loop in which the most important business competency was attracting investment capital [. . .] toward transforming the web into an advertising channel” (Crain, 2021: 78). DoubleClick was the embodiment of this feedback loop, with finance capital pumping up its valuation to great heights. While the company lost a lot of its market capitalization when the bubble burst, ready access to capital laid the infrastructural foundations of the digital advertising ecosystem. Google, in turn, an early market leader in contextual search advertising, quickly came to dominate web advertising (Crain, 2021: 138–139). In this position, it could mobilize substantial financial resources to expand the range of its subsidiaries by acquiring Android (2005), YouTube (2006), and DoubleClick (2007), among others. As Klinge et al. (2023) point out, the financialization of leading tech conglomerates is reinforced by the other platform power strategies: “feedback loops between mounting market dominance, data extraction, and above-average profits” (p. 332).

Vital for our inquiry, then, is the recognition that institutional platform power not only concerns building and sustaining infrastructures—as is the case in owning and operating ad exchanges as the central clearing houses of transactions—or gaining control over data flows and datasets, but also the ability to exercise control “through the shaping and dismantling of infrastructure critical to the functioning of markets” (Lomborg et al., 2023: 359).

As we will argue in the next section, the introduction of the ATT framework serves as an example of such dismantling or “sabotaging” (McGuigan et al., 2023). To gain better insight how changing a seemingly simple privacy setting tucked away in an iPhone or iPad can have such an outsized ripple effect, we followed an approach similar to critical advertising scholars (cf. Broughton Micova and Jacques, 2020; Crain, 2021; McGuigan, 2023). That is, to draw on documentation that involves (1) developer-focused material provided by Apple, (2) ongoing litigation, (3) computer science scholarship (e.g. Kollnig et al., 2022), and (4) a review of industry commentary and analysis. Through such an inquiry, we gain insight into how leading platform conglomerates exercise power, enabled by their central infrastructural position in the digital advertising ecosystem.

App Tracking Transparency: how platforms exercise institutional power

Considering the economic and infrastructural implications of Apple’s ATT policy framework in the short and medium term, its announcement and rollout were surprisingly haphazard. In the summer of 2020, a brief announcement aimed at app developers was made by Apple’s privacy manager Katie Skinner during the company’s annual Worldwide Developers Conference:

This year, we want to help you with tracking and apps. We believe tracking should always be transparent and under your control. So moving forward, app store policy will require apps to ask before tracking you across apps and websites owned by other companies. (Apple Inc, 2020)

As with many Apple announcements regarding the technical implementation of its guidelines or their enforcement mechanisms, details were sparse. Only after the April 2021 rollout of a new version of Apple’s mobile operating system—iOS version 14.5—were developers, advertisers, and the broader public confronted with the material impact of Apple’s announcement.

What had changed? Before ATT, advertisers were granted permission to gather a variety of granular data primarily through integrated SDKs, such as the IDFA, a target’s IP-address, or combinations of individual signals. Apple refers to the industry practice of tying a user to a device as “fingerprinting,” which may combine “a user’s web browser and its configuration, the user’s device and its configuration, the user’s location, or the user’s network connection” (Apple Inc, 2024a). If advertisers can fingerprint end-users, they can also follow them across apps. Conversely, without access to such “user-level data,” advertisers “lose the conversion-level attribution capabilities that have distinguished digital advertising” (Johnson et al., 2022: 52).

For end-users, ATT’s rollout and discernible impact were far less noteworthy. After installing the new operating system, users were automatically opted out of “app tracking.” That is, from that point onwards, app developers were prohibited from accessing the device’s IDFA, the random, but persistent “signal” that afforded advertisers the opportunity to relay detailed information about a user’s in-app behavior (particularly in-app purchases), and attributing app installations to specific in-app advertisements. As such, ATT demonstrated that Apple was willing to implement what, from the perspective of digital advertisers, is one of the most, if not the most profound infrastructural intervention in mobile advertising. Apple could do so because it is in a decidedly sovereign institutional position. Apple is not dependent on advertisers for its growth, and vice versa, advertisers have little legal or moral standing to force access to its mobile operating system.

Developers, advertisers, and platform incumbents, such as Snapchat and Meta, were reportedly caught off guard (Cheyre et al., 2023), which is somewhat surprising considering the other instances where Apple cut off access to data signals: the 2017 introduction of Apple’s Intelligent Tracking Prevention (ITP)—restricting cookie functionality in the Safari browser—followed by a wholesale blocking of third-party cookies in 2020.

Considering our analysis of the strategies deployed by platform companies to accumulate institutional power, it is important to remember that Apple has historically pursued different revenue sources than Google and Meta. This observation explains why ATT was introduced in the first place. Apple’s approach to conglomeration is hardware based; it is a luxury brand manufacturing innovative devices at a massive premium (Goggin, 2021) and advertising revenue has always ranked lower in its revenue mix. Similarly, Apple’s retail and server infrastructures are predominantly geared toward direct sales and supporting device-related services, such as the App Store and iCloud. Yet, with the mass diffusion of iOS-powered devices in 2007, users moved from browsers to apps; the functionality of the latter is managed at the operating system level, granting Apple near total infrastructural control over data flowing in and out of apps rather than mobile browsers (Dieter et al., 2019). While initially wary of opening its mobile platform to external developers, Apple’s decision to facilitate mobile app tracking cannot be emphasized enough. One of its early design decisions was to outfit each iOS device with a Unique Device Identifier (UDID), which could be accessed by any developer, as well as SDK providers. Like the cookie, the UDID was not intended to facilitate user tracking and surveillance, but also like the cookie, it was soon used for tracking purposes. With the 2012 release of iOS 6, Apple replaced the UDID with the IDFA to better regulate the privacy impact of this persistent identifier, but still allow advertisers to track users.

Seen in this light, ATT solved a problem that Apple itself created. Publicly, Apple presented “privacy” as the main rationale for the ATT framework. Regulatory pressures to enhance user privacy, such as the EU’s 2018 General Data Protection Regulation (GDPR), heightened its need (Geradin et al., 2021). Yet, critical advertising scholars also note that ATT’s implementation directly sabotaged its competitors, “while preserving” Apple’s “own abilities to collect and cross-reference user data” (McGuigan et al., 2023: 39). For Apple, enhancing privacy while also seeking to grow advertising revenue are not mutually exclusive long-term goals.

Reshaping the mobile advertising market

Simply put, the way platforms exercise institutional platform power impacts other companies and reshapes markets. The implementation of ATT, then, can be seen as a moment of intentional infrastructural breakdown (Braun, 2023; Lomborg et al., 2023). In the process, it reaffirmed—discursively, infrastructurally, and administratively—the distinction between “first-party” and “third-party” personal data, as well as between “targeting” and ad “tracking.” App developers, as first parties, can still gather personal data to target the users of their app(s). As such, while ATT curtails indiscriminate tracking, it does not prevent tracking of users across apps by platform conglomerates operating much-frequented app instances. Conversely, external actors—that is, third parties, or those data intermediaries and advertisers infrastructurally integrated in apps via SDKs and other means—are no longer allowed to track users across websites and apps. As a result, ATT disrupted the strategy of platformization, while simultaneously codifying and legitimizing targeted advertising.

In terms of its effectiveness, Apple’s “new policies largely live up to its promises on making tracking more difficult” (Kollnig et al., 2022: 10). Difficult, but certainly not impossible, given the challenges of enforcing regulations around invasive data collection practices, such as fingerprinting. For example, the tracking of users’ IP addresses, which could also be blocked by Apple, remains possible. After all, the history of the advertising business has shown numerous examples of “disruptive” innovations, as well as behavioral shifts among end-users; for example, the introduction of digital video recorders or the use of ad-blockers in browsers. Yet none of these impeded revenue growth. Ironically, ATT’s infrastructural disruption favors platforms with large user bases, which happen to be Meta, Alphabet, and Apple itself. Thus, Apple “traded more privacy for more concentration of data collection with fewer tech companies” (Kollnig et al., 2022). Finally, lacking a deterministic identifier, ATT stimulated an increase in probabilistic targeting and the use of generative AI to create and optimize ad material (“copy”). This last development plays directly into the hands of Meta and Google as well, as they have invested heavily in such technologies and capital-intensive data infrastructures.

At the end of the day, the introduction of ATT serves as a powerful reminder of the layeredness of infrastructural power and that “even the largest platforms depend on the technical productions of others” (Blanke and Pybus, 2020: 11). The introduction of the ATT framework is a pivotal moment in which platform power is exercised; more of a tactic, one among many. It reflects long-term institutional strategies that seek to centralize infrastructural control and accumulate capital. The battle for such control is far from over. Apple’s next goal is to curtail SDK capabilities (via so-called “Privacy Manifests” and SDK signatures) and the transfer of end-user data via SDK-embedded APIs, dubbed “required reason APIs” (Apple Inc, 2024b). Further evidence of Apple’s commitment to digital advertising is the introduction of its own advertiser-focused frameworks, such as AdAttributionKit and SKAdNetwork, which allow for ad attribution and measurement of conversions. These frameworks emerged alongside the deprecation of persistent identifiers and seek to replace third-party tools and services.

Conclusion

This article serves as a call to more systematically analyze the accumulation and exercise of institutional power in the digital economy. Over the past two decades, capital and infrastructural control have been concentrated among a handful of platform conglomerates. This has become especially evident in the market for digital advertising, which constitutes one of the main drivers of this economy. In combination, Alphabet (Google) and Meta (Facebook) rake in over a half of global digital advertising revenues. The dominance of platform companies not only has significant consequences for other corporations—for example, ad analytics firms, advertising and marketing agencies, data brokers, and audience measurement companies—but also for media organizations and individual content creators trying to generate revenue through digital advertising. The latter groups, more so than in the past, have very little bargaining power in any of the clashes over mobile device permissions, standards, and defaults, or the broader infrastructures of digital targeting and tracking. Instead, platform-dependent companies are collectively subject to the decisions of platform conglomerates, with Apple leaving the most recent mark on the direction of the advertising ecosystem.

While platform scholarship has recognized the concentration of capital and power in digital advertising, as well as its cultural, societal, and environmental harms, a comprehensive understanding of how institutional strategies are deployed to accumulate platform power is still missing. These insights are essential to understanding why and how such power is, subsequently, exercised via control over infrastructural nodes. Without taking both these analytical steps, it is difficult to regulate the market for advertising or otherwise set limits to the unilateral control over platform markets and infrastructures. Building on the work of Rieder and Hofmann (2020), Leerssen (2024) notes that the enforceability of platform regulation, such as the European Union’s Digital Services Act (DSA), depends on platform observability. To address this opacity challenge, we have proposed that the accumulation of platform power takes shape through four complementary institutional strategies: infrastructuralization, platformization, conglomeration, and financialization. In turn, we retraced how pursuing these strategies enabled Google, Meta, and Apple to attain central positions in the advertising ecosystem. To sustain economic growth, platform conglomerates must maintain infrastructural integrations with external companies. As such, institutional platform power is not absolute, nor static; it is asymmetrical (dependent), relational (distributed), and inherently contingent (dynamic).

While the long-term accumulation of platform power is widely recognized and for all to see, its exercise occurs largely out of sight, through a constant series of infrastructural interventions that are accompanied by developer conferences and documentation. The ATT case, then, serves as a powerful reminder of constantly evolving institutional relationships and that infrastructural objects and nodes, and its embedded objects and capabilities (e.g. IDFA, SDKs, APIs), are all subject to abrupt intervention or even decommissioning, keeping ad technology inherently unstable. The reason to single out the introduction of the ATT framework in the first place is because its impact and legibility as an intervention. It reveals how control over one seemingly small data signal allowed Apple to fundamentally disrupt their competitor’s ability to leverage the strategy of platformization.

Somewhat paradoxically, something that should jolt platform regulators awake is the recognition that Apple’s “privacy” efforts are strengthening the positions of incumbent platform conglomerates (Geradin et al., 2021; Kollnig et al., 2022; McGuigan et al., 2023). The simple fact that Google is following in lockstep with Apple in deprecating key functionalities in Google’s advertising ecosystem—for example, blocking third-party cookies in Chrome and deprecating the GAID in Android—is indicative of its ability to leverage first-party data at the expense of third-party data. If incumbents emerge stronger, who are left holding the proverbial bag? In terms of institutional power that would be the many thousands of small and medium-sized companies that are integrated with platform conglomerates and that thus far heavily relied on having access to persistent identifiers, such as the IDFA, to facilitate quality matches between advertisers and publishers. This is not to say that we are advocating for shifting back institutional control to third-party trackers. On the contrary, the digital advertising economy gives way to, as economists would say, significant negative externalities—discrimination, misinformation, and so on. Yet, given these stakes, should we be comfortable putting Apple and Google not only in the position of judge, jury, and executioner, but also as hosts of the court and framers of what constitutes ad tracking, targeting, and privacy?

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.