Abstract

Joshua McCabe on the fiscalization of social policy.

The tax cuts signed into law by President Trump in December 2017 represent a success for the Republican Party. After all, Wall Street Journal columnist Robert Novak famously remarked “God put the Republican Party on earth to cut taxes. If they don’t do that, they have no useful function.”

Critics of these tax cuts contend that, like the Reagan and Bush tax cuts before them, these cuts disproportionately benefit the rich. These critics focus on the marginal rates, the rate used to tax certain levels of income. The marginal tax rate for the highest income dropped from 70% when Reagan took office to 37% today. The lowest federal marginal tax rate, however, has only dropped from 14% to 10%.

But lawmakers used a different strategy—tax credits—to reduce the tax burden of lower- and middle-income families beginning in the 1970s. Rather than reducing the rate at which the government taxes income, tax credits allow taxpayers to claim a refund on a portion of their tax liability. Some tax credits, called refundable credits, even allow tax-payers to receive more money than they technically paid in certain taxes.

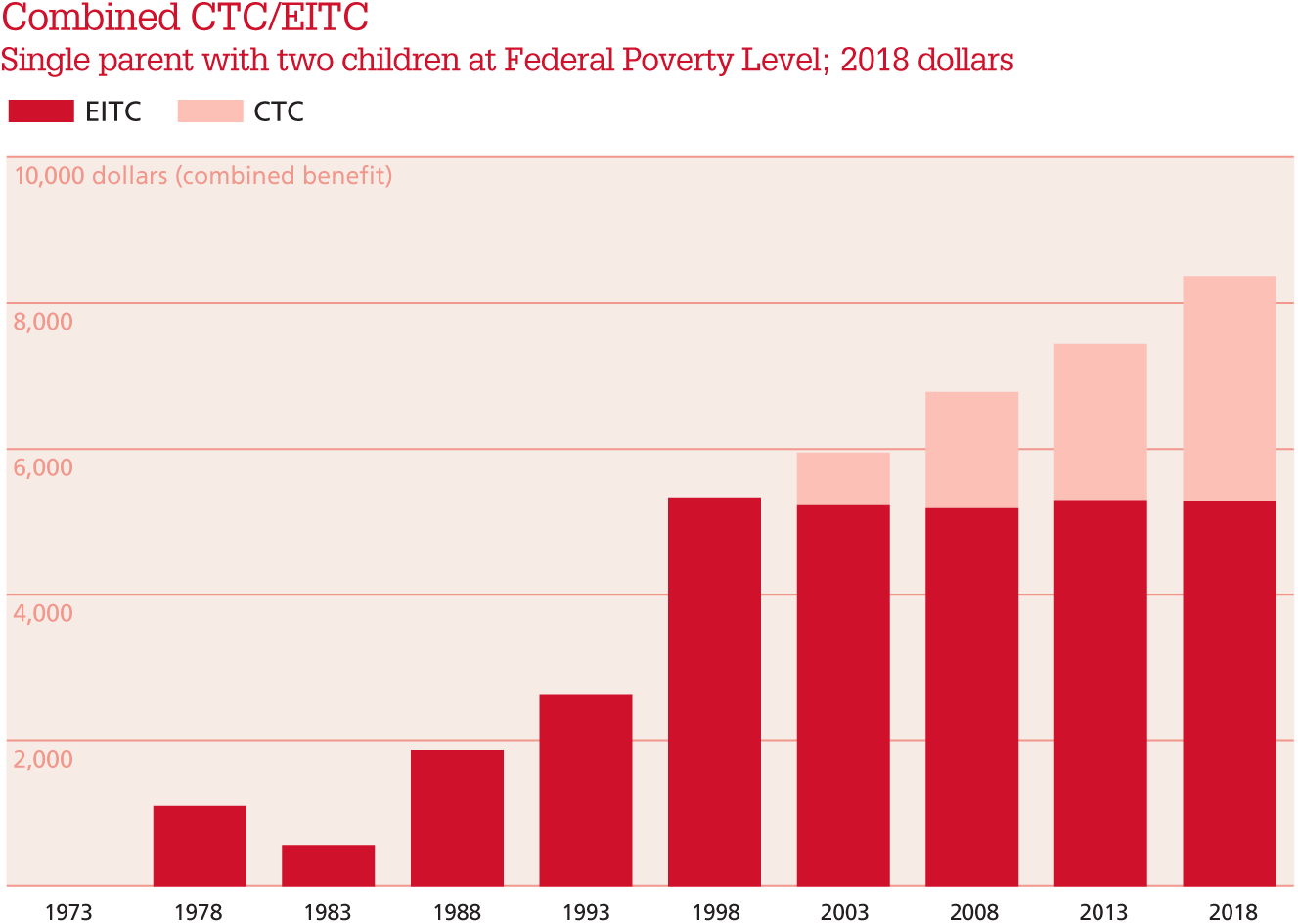

Lawmakers created two programs that affect the taxes of lower- and middle-class taxpayers: the earned income tax credit (EITC) and child tax credit (CTC). Neither program existed in 1973, but both Republicans and Democrats have expanded these programs so that a single parent raising two children with an income at the federal poverty line ($20,780) now receives a combined $8,370 from the EITC and CTC. These credits effectively reduce the parent’s federal income and payroll taxes to zero. The figure on the next page shows how the total amount of credits has changed over time.

The EITC and CTC represent the “fiscalization” of social policy, the use of the tax code—and tax credits in particular—to provide social support rather than traditional safety net programs. Liberal Democrats wanting to reduce poverty and conservative Republicans wanting to promote traditional families joined together to introduce and expand these two programs. In our current age of extreme political polarization, the history of the EITC and CTC reminds us that positive policymaking across parties is possible.

The Birth of the EITC

Inflation in the 1970s was eroding Social Security benefits, so Congress indexed them to keep up with the cost of living. To pay for the increases in benefits, Congress raised payroll taxes. As a result, the average payroll tax burden nearly doubled in 12 years. Lawmakers in both major parties turned to targeted tax relief as a solution to rising tax burdens.

In one hearing, Senator Lawton Chiles (D-FL) asked, “Why should we take dollar one of the working man?,” and then-governor Ronald Reagan (R-CA) suggested a policy to exempt “low-income families from federal and state income tax… and provide them with a rebate for their social security taxes.” Consensus that tax relief was the best way to help struggling families emerged.

Senator Russell Long (D-LA) eventually proposed what would become the EITC as a means to provide tax relief to the poor. “It is just not fair that these poor people should be taxed so heavily,” he argued, “especially when you recognize the fact that in many instances we are actually taxing these people into poverty.” By the end of the session, Congressional Democrats in both chambers passed and Republican President Gerald Ford signed the Tax Reduction Act of 1975 that introduced the EITC, made permanent three years later.

The new EITC worked by refunding 10% of a taxpayer’s income (corresponding to the amount that families had been paying in Social Security and Medicare taxes) up to $4,000 (about $19,000 in today’s dollars), then reducing the credit by one dollar for every ten earned above $4,000. When it was made permanent, the EITC also included a “plateau” whereby the total amount of the credit remained the same as a taxpayer’s income increased and the rate of reduction was lowered.

The EITC proved popular. It was expanded under the Carter (1978), Reagan (1986), Bush (1990), and Clinton (1993) administrations, as policymakers increased the maximum benefit and adjusted it based on family size. Today, a taxpayer with two children gets a refund of 40% of their income up to $14,320, at which point the taxpayer receives $5,728 (the “phase in”). The taxpayer receives the same $5,728 if she makes between $14,320 and $18,700 (the “plateau”), and then the taxpayer’s credit is reduced by $21 for every hundred dollars above $18,660 the taxpayer earns (the “phase out”).

The Birth of the CTC

Concerns about child poverty and stagnating incomes in the 1990s brought renewed attention to the taxation of families. Like many conservatives, Heritage Foundation policy analyst Robert Rector turned his focus from welfare cuts to families’ rising tax burdens. Seeing rising taxes as hurting families, he argued that “the federal government currently imposes heavy taxes on low-income working families with children [that]… promotes welfare dependence by reducing the rewards of work and marriage relative to welfare.” Rector and others worked to develop a $500 child tax credit as the “crown jewel” of the Republican platform.

The Clinton administration, seeing an opportunity to provide more tax relief to low-income families, soon proposed its own CTC, limiting it to families making less than $75,000. The CTC allowed Congressional Republicans to push for general tax relief for families and allowed Democrats to help low-income families beyond the EITC. The CTC came into existence after several failed attempts at a budget compromise when Congressional Republicans passed and President Clinton signed the Taxpayer Relief Act of 1997.

Although the initial structure of the CTC meant that families below the federal poverty line were excluded, subsequent expansions under Bush in 2001 and 2003, under Obama in 2009, and under Trump in 2017 have increased the maximum benefit and expanded eligibility to include more low-income families.

The Future of the EITC and CTC

The story of the EITC and CTC is an example of what political scientists Steven Teles and David Dagan call transpartisanship, or “agreement on policy goals driven by divergent, deeply held ideological beliefs.” Republicans, motivated by reducing taxes and providing support to traditional families, worked with Democrats, motivated by reducing poverty. Together, they found common cause in the tax credits.

The Congressional Joint Committee on Taxation estimates that the combined value of EITC and CTC will be $192.5 billion in 2018. The value of these programs puts them on track to outgrow traditional social assistance programs such as Temporary Assistance to Needy Families (TANF), Supplemental Security Income (SSI), and the Supplemental Nutritional Assistance Program (SNAP).

Combined CTC/EITC

Single parent with two children at Federal Poverty Level; 2018 dollars

Transpartisan support for the expansion of the the EITC and CTC continues today. Representative Paul Ryan (R-WI) and former President Barack Obama, for example, agreed on the need to expand the EITC for taxpayers without children. Senator Marco Rubio (R-FL) has argued for further expansions to the CTC.

But there are limits to the idea of providing tax relief as an anti-poverty strategy. The strategy may be a victim of its own success. While the pro-family and anti-poverty advocates who worked together to make this happen should celebrate their achievement, it remains an open question whether the coalition will survive when there is no more tax relief to provide to low-income families. The Tax Policy Center estimates that a family of four earning one-half of the median income in 1986 (about $40,000 today) paid a combined income and payroll tax rate of 21%. By 2014, that same family paid a combined income and payroll tax of only 6.8%, which will be even lower after the Tax Cuts and Jobs Act of 2017.

Focusing on tax relief also excludes the poorest families who pay little to nothing in income and payroll taxes. It would be possible to extend the credits to provide general assistance to all families, a position of some anti-poverty liberals, yet we cannot know whether enough pro-family conservatives are willing to support repurposing tax credits to achieve goals beyond tax relief. Without the transpartisan coalition, a universal expansion of credits for all families remains unlikely. Those on both sides of the political spectrum who are interested in stable, thriving families will have to continue to work together to find solutions to the most pressing problems facing families today.