Abstract

Erik Olin Wright on last year's best-seller, Capital in the Twenty-First Century.

Capital in the Twenty-first Century Thomas Piketty Belknap Press, 2014 696 pages

Until recently, the only context in which inequality was treated as a problem was in discussions of opportunities and rights. Equal opportunity and equal rights are deeply held American values, and certain kinds of inequalities were seen as violating these ideals. Racial and gender discrimination, for example, are viewed as problems because they create unfair competitive advantages for some people. They violate the ideal of a level playing field. Likewise, poverty is viewed as an important problem, but the main issue has not generally been the distance between the poor and the rich. Rather, it has been the absolute material deprivations of people living in poverty and how their unmet needs harm them. Not surprisingly, then, the LBJ-era “War on Poverty” led to the creation of an office of economic opportunity, not an office for the reduction of inequality. The way poverty constitutes a disadvantage was of great concern, but almost no public attention was given to the degree of inequality of resources or conditions of life across the income distribution as a whole. Inequality was not an important publicly recognized problem.

The 1% vs. the 99% logic indicates antagonism rooted in inequality.

Even among scholars, discussions of inequality have historically focused on social mobility and the social production of advantages and disadvantages. There was a great deal of concern about inequalities in the way people got access to social positions and certainly much study of how hard life was for people living below the poverty line, but almost no concern with the magnitude of inequalities among the positions themselves. Inequality was not an important academically recognized problem.

Conservatives and liberals shared this inattention. To be concerned with the distance between the rich, the poor, and the middle class was seen as a thin veil for envy and resentment. So long as fortunes and high income were acquired legally, the degree of inequality generated was unobjectionable. And what’s more, as many argue even today, in the long run, the high incomes of the wealthy were said to benefit everyone. Out of this high income, people said, new investments were made, and these filled a necessary condition for proverbial “rising tide” that lifts all boats. Inequality was not an important politically recognized problem, either.

This situation has changed dramatically: today, talk about inequality is everywhere. The media, the academy, and politicians all speak to the problem of inequality in its own right. The slogan of the Occupy Movement is exemplary: We are the 99%. The 1% versus the 99% logic indicates an antagonism between those at the very top of the income distribution and everyone else. Now politicians and pundits speak of the dangers of increasing inequality. Scholars have begun to study it systematically.

It is in this context that Thomas Piketty’s book Capital in the Twentieth Century appeared. Nearly 600 pages long and published by an academic press, it is a serious, scholarly work (some lively bits notwithstanding)—not the sort of book anyone expects to be a bestseller. And yet it is. This reflects the salience of inequality as an issue of broad concern.

Piketty’s book is built around the detailed analysis of the trajectory of two dimensions of economic inequality: income and wealth. Previous research on these issues has been severely hampered by lack of data on the richest people. The people at the very top are not selected in survey samples, so it has been impossible to systematically study the historical trajectory of inequality for more than a few decades because of a lack of good data before the mid-20th century. Piketty has solved these problems, to a significant extent, by assembling a massive dataset that goes back to the early 1900s and is based on tax and estate data.

The Trajectory of Income Inequality

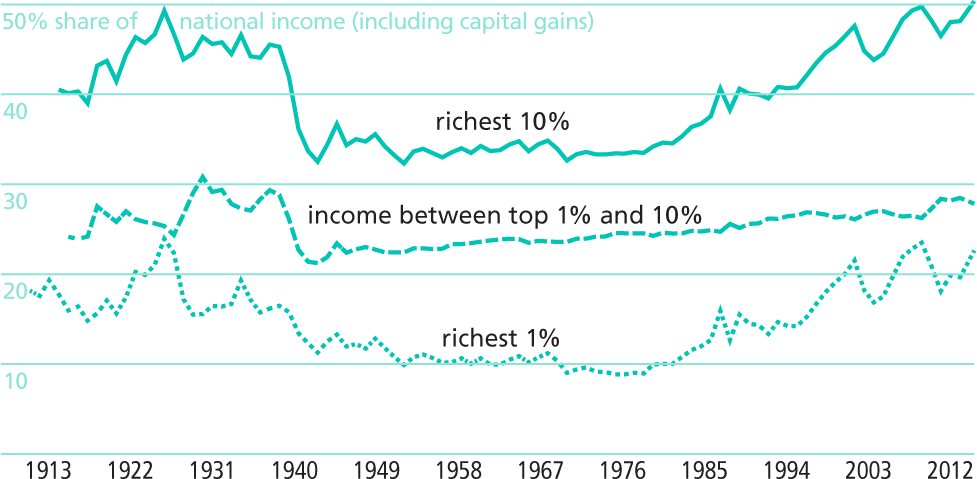

The central observation of Piketty’s analysis seen in the now-familiar U-shaped graph of the share of national income going to the top layers of the income distribution. A version is reproduced below, showing the percentage of national income in the United States going to the richest 10% and 1% from 1913 to 2012. The share of the top decile in total national income reached an early peak of 49% in 1928, then hovered around 45% until WWII, when it dropped precipitously to around 35%. There it remained for four decades, until it began to rise rapidly in the 1980s, reaching a new high of just over 50% in 2012. That is, in 2012 the richest 10% of the population received just over half of all income generated in the American economy.

This graph has undoubtedly received the most widespread publicity of any of the findings reported in Piketty’s book. But there is a second finding that is of almost equal importance: The sharp rise in income share of the top income decile is largely the result of the dramatic rise in income share of the top 1%. Of the 17 percentage point increase in the share of income going to the top decile between 1975 and 2012, 13.6 percentage points (80% of the increase) went to “the 1%.” The share going to the next richest 9% of the population only increased by 3.4 percentage points. Income is not merely becoming more concentrated at the top; it is being much more concentrated at the top of the top.

Share of Total National Income going to different high income categories

A third finding on the trajectory of income inequality is significant: While in every country studied, income concentration at the top of the distribution declined sharply in the first half of the 20th century, there is considerable variation across countries in the degree to which concentration increased by the century’s end. These trends are much more pronounced in the United States than in other countries, and are quite muted in some.

Piketty’s book is built around the detailed analysis of the trajectory of two dimensions of economic inequality: income and wealth.

How does Piketty explain these broad patterns? The crux of Piketty’s analysis boils down to two main points. First, the rapid increase in concentration of income since the early 1980s is mainly the result of increases in super-salaries, rather than dramatic increases in income from capital ownership. This reflects the fact that the high income concentration in the early 20th century had a very different underlying basis than in the present day: In the earlier period, “income from capital (essentially dividends and capital gains) was the primary resource for the top 1 percent of the income hierarchy… In 2007 one has to climb to the 0.1 percent level before this is true” (p. 301).

Second, the universal decline in income inequality in the middle of the 20th century and the variations across countries in the extent of its increase by the end of the century are largely the result of the exercise of power, not the natural workings of the market. Power exercised by the state is especially important in counteracting the inegalitarian forces of the market through taxation, income transfers, and a range of regulations. But also important is the power of what Piketty terms “supermanagers”: “these top managers by and large have the power to set their own remuneration, in some cases without limit and in many case without any clear relation to their individual productivity” (p. 24). The exercise of power is constrained by social norms, which vary across countries, but is very weakly constrained by ordinary market processes.

The Trajectory of Wealth Inequality

Piketty uses the terms wealth and capital interchangeably. He defines capital in a comprehensive manner as “the sum total of nonhuman assets that can be owned and exchanged on some market. Capital includes all forms of real property (including residential real estate) as well as financial and professional capital (plants, infrastructure, machinery, patents, and so on) used by firms and government agencies” (p. 46). Ownership of such assets is important to people for a variety of reasons, but especially because it generates a flow of income, which Piketty refers to as the return on capital. A fundamental feature of any market economy, then, is the division of the national income into the portion that goes to owners of capital and the portion that goes to sellers of labor.

Author Thomas Piketty signing autographs in a scene uncommon to 700-page nonfiction books.

blu-news.org via Flickr Creative Commons

The story Piketty tells about wealth inequality revolves around two basic observations: First, levels of concentration of wealth are always greater than concentrations of income, and second, the key to understanding the long-term trajectory of wealth concentration is what Piketty calls the capital/income ratio. The first of these observations is familiar: In the U.S. in 2010, the top decile of wealth holders owned 70% of all wealth and the bottom half of wealth holders owned virtually nothing. As with the income distribution, during the middle of the 20th century this concentration at the top declined from considerably higher earlier levels (in 1910 the top decile of wealth holders in the US owned 80% of all wealth), but the rise in wealth concentration has been more muted than the rise in income in recent decades. Still, the main point is that wealth concentration is always very high.

The second element of Piketty’s analysis of wealth, the capital/income ratio, is less familiar. It is a way of measuring the value of capital relative to the total income generated by an economy. In developed capitalist economies today, this ratio for privately owned capital is between 4:1 and 7:1, meaning that the value of capital is typically 4 to 7 times greater than the annual total income in the economy. Piketty argues that this ratio is the structural basis for the distribution of income: All other things being equal, for a given return on capital, the higher the capital/income ratio, the higher the proportion of national income going to wealth holders.

A substantial part of Piketty’s book is devoted to exploring the trajectory of the capital/income ratio and its ramifications. These analyses are undoubtedly the most difficult in the book. They involve discussions of the interconnections among economic growth rates, population growth, productivity, savings rates, taxation, and other things. Without going into details, a number of Piketty’s conclusions are worth noting:

As economic growth in rich countries declines, the capital/income ratio is almost certain to rise unless counteracting political measures are taken.

Over time, the rise in the capital/income ratio will increase the weight of inherited wealth, so concentrations of wealth should begin to rise more sharply in the course of the 21st century.

Given the presence of unprecedented high concentrations of earnings among people who also receive considerable income from capital ownership, concentrations of income are likely to exceed levels observed in the 19th century.

The implication of these arguments is sobering: “The world to come may well combine the worst of the two past worlds: both very large inequality of inherited wealth and very high wage inequalities justified in terms of merit and productivity (claims with very little factual basis, as noted). Meritocratic extremism can thus lead to a race between supermanagers and rentiers to the detriment of those who are neither” (p. 417). The only remedy, Piketty argues, is political intervention: “there is no natural, spontaneous process to prevent destabilizing inegalitarian forces from prevailing permanently” (p. 21).

His preferred policy solution is the introduction of a global tax on capital. Even if one is skeptical about that specific proposal, the basic message remains convincing: so long as market dynamics are left largely unhindered, the polarization of the extreme concentration of income and wealth is likely to deepen.

The Problematic Role of Class

On the first page of Chapter One, Piketty recounts a vivid example of the salience of capital ownership in a bitter class conflict in South Africa in 2012: the strike of workers at the Marikana platinum mine which resulted in the massacre of 34 miners by police. He writes:

“For those who own nothing but their labor power and who often live in humble conditions (not to say wretched conditions in the case of eighteenth-century peasants or the Marikana miners), it is difficult to accept that the owners of capital—some of whom have inherited at least part of their wealth—are able to appropriate so much of the wealth produced by their labor” (p. 49).

This is a potent class analysis. In this account, classes are not arbitrary divisions within some distribution of income or wealth—a top, middle, and bottom—but real social categories constituted through social relations. The owners of capital do not simply receive a return on capital; they exploit the miners by appropriating “wealth produced by their labor.” Rather than a division of the national income pie into shares, it is a transfer.

Though the terms “capital” and “labor” continue throughout the book, with very few exceptions, this relational concept of class largely disappears after the first salvo. I do not think that this undermines the value of Piketty’s empirical research or the interest in his theoretical arguments. But it does obscure some of the critical social mechanisms at work in the processes he studies.

Let me elaborate with two examples, one from the analysis of income inequality and one from the analysis of returns on capital.

One of Piketty’s important arguments is that the sharply rising income inequality in the U.S. since the early 1980s “was largely the result of an unprecedented increase in wage inequality and in particular the emergence of extremely high remunerations at the summit of the wage hierarchy, particularly among top managers of large firms” (p. 298). This conclusion depends, in part, on what, precisely, is considered a “wage” and what is “capital income.” Piketty adopts the conventional classification of economics and includes stock options and bonuses as part of top managers’ “wages”. This is obviously correct for purposes of tax law and the theories of conventional economics, in which a CEO is just a particularly well-paid employee. But this accounting becomes less obvious when we think of the position of CEO as embedded in class relations. As Piketty himself points out, to a significant extent, the top managers of corporations have the power to set their own remuneration. This power can be viewed as an aspect of ownership. Because of this, rather than a wage, in the ordinary sense, a significant part of the earnings of top managers should be thought of as an allocation of the firm’s profits to their personal accounts. Although different from stock holding, CEOs’ earnings and other compensation should thus be thought of as, in part, a return on capital.

The growing attention to inequality is good, and Piketty deserves credit. But he gets it wrong by overlooking class relations.

It would, of course, be extremely difficult in a relational class analysis of corporate cash flow to figure out how to divide the earnings of top managers into one component that is functionally a return on capital and another that is functionally a wage. The problem is quite similar to dividing self-employment income into a wage component and a capital component, since (as Piketty notes) the income generated by sole proprietors’ economic activity inherently mixes capital and labor.

The absence of a relational class analysis is also reflected in the way Piketty combines different kinds of assets into the category “capital” and then talks about “returns” to this heterogeneous aggregate. In particular, he folds residential real estate and capitalist property into capital. This is important because residential real estate comprises somewhere between 40 and 60 percent of the value of all capital in the countries for which Piketty provides data on real estate. Combining all income-generating assets into a single category is perfectly reasonable from the point of view of standard economic theory, in which these are simply alternative investments, but combining them makes much less sense if we want to identify the social mechanisms through which returns are generated.

Owner-occupied housing, for instance, generates a return to the owner in two ways: as housing services, which are valued as a form of imputed rent, and as capital gains, when the value of the real estate appreciates over time. In the U.S. in 2012, about two-thirds of the population was home owners; roughly 30% owned their homes outright, while another 51% had positive equity but were still paying off mortgages. The social relations in which these returns are earned are completely different from those depicted in Piketty’s story about London owners and South African miners. Furthermore, the social struggles unleashed by these different forms of wealth inequality are completely different, as are the public policies needed to respond to the harms generated by different kinds of returns to capital.

The growing attention to inequality is good, and Piketty deserves credit for contributing to that. But Piketty gets it wrong by treating capital and labor exclusively as factors of production each earning a return. If we want to really understand—and even alter—what’s going on as inequality creates social and economic distance, we must go beyond income and wealth trends to identify the class relations that generate escalating economic inequality.