Abstract

While prior research has established a link between the attention an organization allocates to the external environment and its adaptations to environmental change, the nature of the cognitive processes that underlie this link remains underexamined. In this study, we explore how patterns of attentional engagement—that is, the extent to which attention allocation is focused and/or consistent over time—influence the organization’s formulation of strategic responses to discontinuous change. We advance a situated perspective on attentional engagement by suggesting how the type of learning and cognitive processes are situated in different attentional-engagement structures, and can, in turn, lead to heterogeneous strategic responses to the same discontinuous change. Specifically, we formulate a theoretical model elaborating how varied levels of attentional focus and attentional consistency affect whether organizations respond by breaking, reinforcing, hedging, or maintaining the status quo. Subsequently, we develop and test our arguments using a dataset covering US banking firms from 2002 to 2010—a period that includes the US housing crisis.

Keywords

Discontinuous environmental changes involve new configurations of technology, competitive dynamics, consumer preferences, and/or institutions that are inconsistent with the industry’s current trajectory (c.f., Meyer et al., 1990; Shepherd et al., 2017). As discontinuous changes are unfamiliar events, they challenge the existing belief systems and conventional assumptions of even the most seasoned managers (Barr, 1998). For instance, the emergence of the Internet and online publishing was a discontinuous change for newspaper publishers that relied on a traditional print readership model for their revenues (Gilbert, 2005). Similarly, the rise of digital-imaging technology was a discontinuous change for companies like Polaroid that relied on a razor and blades business model to sell film and analog cameras (Tripsas and Gavetti, 2000).

Studies have suggested that the attention an organization pays to new opportunities and threats can not only facilitate matches between organizational capabilities and discontinuous changes in the external environment (Barr et al., 1992; Cho and Hambrick, 2006; Tripsas and Gavetti, 2000; Yadav et al., 2007), but also compensate for the lack of such capabilities by driving the organization to take strategic action (Kaplan, 2008; Nadkarni and Barr, 2008). As attention increases, the issues and answers associated with the changing environment are more likely to be salient. Subsequently, top managers should become more responsive, as they are more likely to recognize, interpret, and formulate responses to changes that come into their focus (Kiss and Barr, 2014; Ocasio, 1997). Thus, the extant views on managerial cognition as the driver of organizational action assume that managers are able to quickly and readily update their beliefs about their strategy when they attend to new information about the external environment (e.g. Cho and Hambrick, 2006; Eggers and Kaplan, 2013; Kaplan, 2008).

However, scholars have recently theorized that more complex attentional processes may underlie how managers effectively deal with discontinuous changes in their external environment (Shepherd et al., 2017; Weick and Sutcliffe, 2006). As information about discontinuous changes can be difficult to interpret and assimilate, successful adaptations to those changes may require high levels of attentional engagement—the process of allocating focused and consistent attention over time—toward the sources of discontinuous changes to facilitate sensemaking (c.f., Ocasio, 2011; Shepherd et al., 2017). As cognitive resources are limited, sustaining high levels of attentional engagement is challenging and thus unlikely, as increasing attentional engagement with a focal issue may shift managerial attention away from other critical organizational issues by which they could be blindsided (Eggers and Kaplan, 2013; Ocasio, 1997). Therefore, patterns of attentional engagement are likely to vary in terms of either focus or consistency. Yet, whether and how the varied nature of attentional engagement shapes subsequent strategic action(s) has received relatively little attention. Given the potential for discontinuous change to cause significant disruptions to organizations, it is important to understand how and when patterns of attentional engagement can lead to different strategic behavioral responses.

This paper advances a situated perspective on how attentional engagement with issues emerging in the external environment affects the firm’s heterogeneous strategic responses to discontinuous changes. We examine four different strategic responses: (1) breaking the status quo, (2) maintaining the status quo, (3) reinforcing the status quo, and (4) hedging the status quo. We refer to breaking the status quo as a response that changes the direction of the current course of action (Rajagopalan and Spreitzer, 1997; Wiersema and Bantel, 1992), whereas we refer to maintaining the status quo refers to making no changes to the current course of action (Hambrick et al., 1993; Staw et al., 1981). Reinforcing the status quo refers to the escalating the current course of action (McNamara et al., 2002; Staw et al., 1997; Staw and Ross, 1978), and finally hedging the status quo refers to a response that reduces the outcome variability of the current course of action (George et al., 2006; Smith and Stulz, 1985). Our examination of these heterogeneous strategic responses (as opposed to treating response as a binary variable) follows prior work suggesting that decision-makers may enact varied strategic responses based on their interpretation of their environment (e.g. George et al., 2006; Shepherd et al., 2017).

Building on the extant research on situated cognition (Ocasio, 2011; Shepherd et al., 2017) and organizational learning (e.g. Tyre and Von Hippel, 1997), we theorize how learning and cognition processes are situated in the informational environment, enabled by the extent of attentional engagement. Specifically, we argue that attentional engagement characterized by both high attentional focus and high attentional consistency enables immersive learning and deliberative reasoning in the organization with the aim of making sense of discontinuous change. In turn, the organization can respond to a discontinuity by taking strategic action that breaks with the status quo. However, we also explain that the organization’s strategic responses are likely to differ under varying levels of attentional focus and consistency. When attentional engagement characterized by high focus and low consistency, selective learning is likely to dominate. This leads to heightened perceptions of certainty that lead to the formulation of strategic responses that reinforce the status quo. In contrast, when attentional focus is low and attentional consistency is high, we contend that noisy learning takes place. This increases perceptions of uncertainty, which leads to the formulation of strategic responses that hedge the status quo against potential downside losses. Finally, we suggest that when both attentional focus and consistency are low, no learning occurs, and the organization take actions that maintain the status quo.

To help illustrate our theory, we draw on the context of the US banking industry from 2002 to 2010. This period encompassed a discontinuous change in the housing market, which emerged toward the end of 2006 in the form of a housing-mortgage crisis. This period provides a fertile context for exploring the role of attentional engagement in driving organizations’ strategic responses to discontinuous changes in their external environments. We undertake this exploration in two parts. First, we make use of qualitative examples drawn from the transcripts of quarterly earnings conference calls. The examples are not intended to test our theory model but to illustrate how the types of learning and the cognitive processes are situated in different attentional-engagement structures. Second, in a series of quantitative analyses of a sample of 96 banking firms, we empirically examine how different patterns of attentional engagement influenced whether banks were more likely to formulate strategic responses associated with breaking the status quo (i.e. reducing exposure to real-estate loans), reinforcing the status quo (i.e. increasing exposure to real-estate loans), or hedging the status quo (i.e. increasing the bank’s liquidity-capital requirements).

This study contributes to research on managerial attention and strategic adaptation by considering how patterns of attentional engagement characterized by varying levels of attentional focus and consistency jointly have novel implications for firms’ strategic responsiveness to discontinuous change. While prior research has suggested how organizational adaptation can be enhanced by directing attentional focus toward sources of discontinuous change (Eggers and Kaplan, 2009; Kaplan, 2008; Nadkarni and Chen, 2014; Yadav et al., 2007), or increasing attentional consistency to these discontinuities over time (Joseph and Wilson, 2017; Shepherd et al., 2017; Weick and Sutcliffe, 2006), we theorize and find that the joint consideration of both attentional focus and attentional consistency can predict a variety of strategic responses, which would have otherwise been obscured. Our theory of attentional engagement provides a more robust explanation of how organizations (fail to) make sense of radically changing environments and formulate (in)appropriate strategic responses.

This study also contributes to the attentional-engagement literature. Whereas, prior work has theorized about how attentional engagement can activate and shape the necessary cognitive processes for decision-makers to form beliefs about radical changes in their environment (e.g. Ocasio, 2011; Rerup, 2009; Salvato, 2009; Shepherd et al., 2017), we build on this stream of research by explicating the cognitive and learning processes underlying how these beliefs formed through attentional engagement translate to heterogeneous strategic responses.

In addition, our study complements research on how organizational attention shape firm-level outcomes, such as firm growth (Joseph and Wilson, 2017; Penrose, 1959). Prior work in behavioral strategy research has conceptualized how sustaining attention to new opportunities can facilitate the firm’s ability to capitalize on these opportunities and translate them into new areas for expansion and development (Joseph and Wilson, 2017). Our findings suggest a boundary condition: when the sustenance of attention to emerging opportunities is inconsistent, firms may fail to differentiate threats from actual opportunities, and in turn might allocate resources to inapt growth initiatives.

Managerial attention to discontinuous change and organizational adaptation

The ways in which managers sense problems depend on the inferences they make from their perceptions (Hambrick, 2007; Hambrick and Mason, 1984). A focus on certain organizational issues can lead to higher levels of anticipation and awareness of those issues (Ocasio, 2011; Tushman and Rosenkopf, 1996). In the context of organizational adaptation to discontinuous change, a managerial focus on issues emerging in the external environment increases the likelihood that those managers’ organizations will be able to overcome inertia and core rigidities (Hannan and Freeman, 1984; Ocasio, 2011). A focus on a particular strategic issue is beneficial for the firm’s strategy formulation around that issue, as it facilitates the collection of a rich array of information (Aldrich, 1979), which is critical if the firm is to effectively anticipate and handle changes (Ocasio, 2011). The extant literature suggests that only when top decision-makers consciously and deliberately devote sufficient attention to the changing external environment can their problem-sensing capabilities—that is, their abilities to recognize, interpret, and incorporate information—be activated (Kiesler and Sproull, 1982).

Although the extant literature has examined the impact of managerial attention on firms’ strategic behaviors based on its directionality (Eggers and Kaplan, 2009; Kaplan, 2008; Nadkarni and Chen, 2014; Yadav et al., 2007) or its intentionality (Bouquet and Birkinshaw, 2008; Cho and Hambrick, 2006; Engelen et al., 2012; Tuggle et al., 2010), the nature of the cognitive processes underlying the formation of strategic beliefs leading to strategic change has received relatively little attention (Eggers and Kaplan, 2013; Ocasio, 1997). In fact, the question of how attention should be allocated over time remains relatively underexplored in empirical studies (Ocasio, 2011; Shepherd et al., 2017), although this line of inquiry has increasingly received attention from scholars interested in examining the finer-grained properties of attention (Bansal et al., 2018). Therefore, we extend the literature on the attention-based view of organizations by exploring the learning and cognitive mechanisms underlying how attentional engagement facilitates organizational adaptations to discontinuous environmental change (Shepherd et al., 2017).

Attentional engagement, situated cognition, and strategic responsiveness

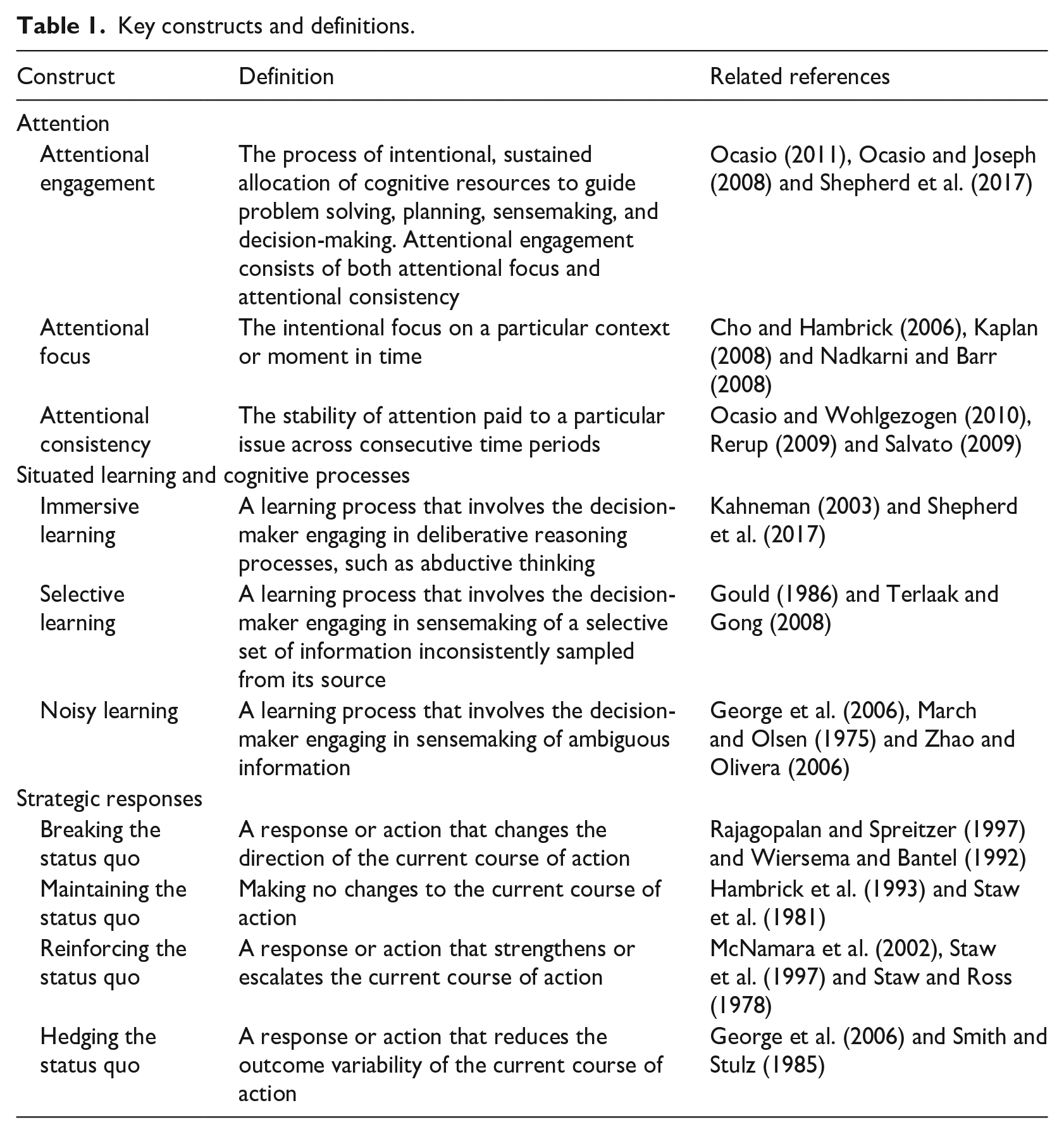

Attentional engagement is defined as “the process of intentional, sustained allocation of cognitive resources to guide problem solving, planning, sensemaking, and decision making” (Ocasio, 2011: 1289). It requires the focus of “time, energy, and effort on a selected set of environmental stimuli, repertoire of action responses, and the relationships between them” (Ocasio, 2011: 1289). More specifically, attentional engagement is a combination of two complementary attentional processes: attentional focus and attentional consistency (Ocasio, 2011). Whereas, attentional focus refers to the outcome of an intentional focus on a particular context or moment in time, attentional consistency refers to the stability or consistency of attention paid to an issue across consecutive time periods (Ocasio and Wohlgezogen, 2010). Thus, the level of focus and the consistency of attentional-engagement structures can vary.

We consider how the type of learning and cognitive processes are situated in different attentional-engagement structures. Unlike conventional behavioral theories that emphasize whether learning or cognition occurs, a situated perspective highlights how the type of learning and cognition underlying decision-making depends on how decision-makers allocate attention to issues over time (Ocasio, 1997; Tyre and Von Hippel, 1997). Consequently, the formation of strategic action reflects decision-makers’ situated cognition—their location, the richness of the available information, the diversity of knowledge sources, and their perceptions (Haynie et al., 2010; Zahra and Wright, 2011).

Thus, a situated perspective highlights how the context of the information environment enabled by attentional-engagement structures affects the emergence of the different forms of learning and cognition that shape heterogeneous behavioral responses. We focus on heterogeneous responses as opposed to response as a binary choice because prior studies have suggested that decision-makers may engage in a variety of response actions to change the status quo depending on their interpretation of their environment (e.g. George et al., 2006; Shepherd et al., 2017). Table 1 presents the list of key constructs and their definitions used in our study.

Key constructs and definitions.

The context: the US banking industry and the housing market crisis

To help illustrate the relationship between attentional-engagement structures, and various situated learning and cognitive processes in our theory development, we offer qualitative examples of managerial responses to the discontinuous change that emerged in the US real-estate market toward the end of 2006. These examples are drawn from quarterly earnings conference calls in which bank managers shared their views, which serve as a rich source of information on their cognitive appraisals of the changing external environment.

The US housing market crisis of 2006 and 2007 has been characterized as signaling the onset of the financial turmoil that evolved into a global recession in 2007 and 2008 (Beltratti and Stulz, 2012). Propelled by growth in the real-estate sector, many financial institutions issued large amounts of debt and aggressively invested in mortgage-backed loans prior to 2006 based on the belief that households would maintain their regular mortgage payments and that housing prices would continue to rise. The rapidly rising housing prices masked the problem of worsening real-estate loan quality (Demyanyk and Van Hemert, 2011). When US housing prices peaked in mid-2006 and subsequently began to fall, default rates on subprime loans rose, and losses on the securities backed by those loans began to accumulate. Many banks suffered heavy losses, but only some introduced strategic responses to reduce their exposure to the real-estate market before the assets lost their value (Farrell, 2007; Tully, 2008). As such, the housing market crisis provides an ideal context for investigating the relationship between an organization’s pattern of attention allocation and its strategic responsiveness to an emerging crisis.

We chose to analyze conference-call transcripts for several reasons. First, as the transcripts record the verbal content of conference calls, they provide valuable information on managerial attention. Typically, top-level managers hold extensive discussions before each conference call to ensure that the call will focus on information that can enhance corporate value and minimize litigation risk. In addition, prior research suggests that managers use conference calls to supplement the hard information included in quarterly reports or earnings announcements with soft information, such as forward-looking statements. Often, this soft information is highly informative (Frankel et al., 1999). Second, quarterly conference calls reflect managerial attention better than other sources, such as annual reports or surveys, because temporal changes in attentional patterns can be tracked over time. In addition, when compared to letters to shareholders that are prepared and filed annually, quarterly conference calls better reflect the mindsets of managers over a given time interval. Third, a growing body of research, especially in the accounting and finance fields, shows that the contents of post-earnings announcement conference calls reflect managers’ cognition and that these cognitive patterns can be meaningfully assessed through the use of content analysis (e.g. Price et al., 2012; Rogers et al., 2011). Thus, conference-call transcripts should provide fertile ground for research on attention in organizations.

As we are interested in how banks noticed and made sense of the US housing crisis that emerged in 2006, we temporally bracketed and examined a cross-sectional set of earning conference calls that took place in the fourth calendar quarter of 2006. We chose this period for two reasons: (1) banks would have been sufficiently exposed to the deteriorating conditions in the US housing market over the course of the year and (2) this is the quarter just before the public discourse about the housing crisis became clear and evident in early 2007, which ensures high variance is terms of how managers made sense of and interpreted the external environment. Moreover, post-earnings conference calls have become an increasingly important medium for providing timely and regular disclosures of information to the public (Bushee et al., 2004; Frankel et al., 1999). Thus, focusing on a particular quarter allows for more temporally appropriate comparisons of heterogeneous responses to an emerging but common discontinuity faced by all firms.

Classifying banks by attentional-engagement levels using conference calls

To examine how banks’ varying levels of attentional focus and attentional consistency toward the US housing market relate to their noticing and sensemaking of the housing crisis, we adopted a theoretical sampling approach (Glaser and Strauss, 1967) and selected cases as “polar types in which the process is observable” to illustrate the theory (Eisenhardt, 1989: 537). To that end, we classified whether the banking firms exhibited high or low levels of attentional focus and attentional consistency over the four quarters prior to the fourth quarter of 2006.

For our analyses, we constructed the attention variables using managers’ prepared statements found in the conference-call transcripts. To measure the variables related to managerial attention, we used managers’ prepared statements but excluded any Q&A sections found in those transcripts. 1 Prepared statements are typically presented by the chief executive officer (CEO) and then by the chief financial officer (CFO), although for some banks a statement may be given entirely by one or the other. Across our sample of 1743 transcripts, managers’ prepared statements averaged 3091 words. The shortest was about 115 words, while the longest had around 9477 words.

We measured the amount of attention an organization allocated to the real-estate market as the degree of attention paid to that market during post-earning conference calls for the four quarters prior to the fourth quarter of 2006. First, we measured the attention paid to the real-estate market in each quarter by counting the number of words related to that market: “home(s),” “household(s),” “housing,” “mortgage(s),” “residential,” and “real estate.” We then normalized this measure by dividing it by the total number of words in each quarter’s prepared statements, multiplied by 100. Finally, we calculated the average of the normalized measure over the four previous quarters (i.e. from t−4 to t−1) to derive the attentional focus measure. To measure attentional consistency, we computed the standard deviation using the normalized real-estate market attention over the four previous quarters. We then reverse-scored the value, so that, lower variation in the attention measure over the four previous quarters represented higher attentional consistency.

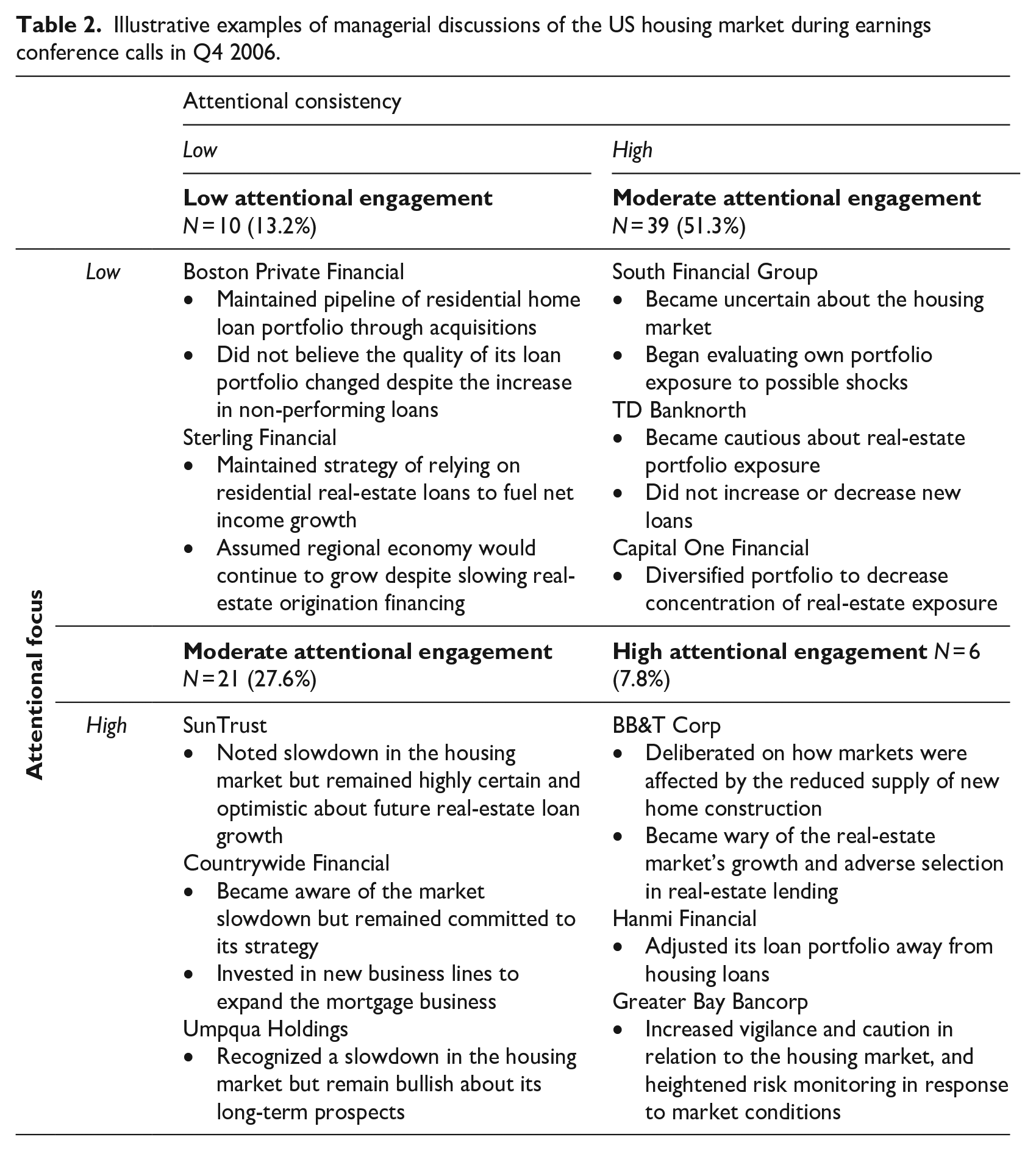

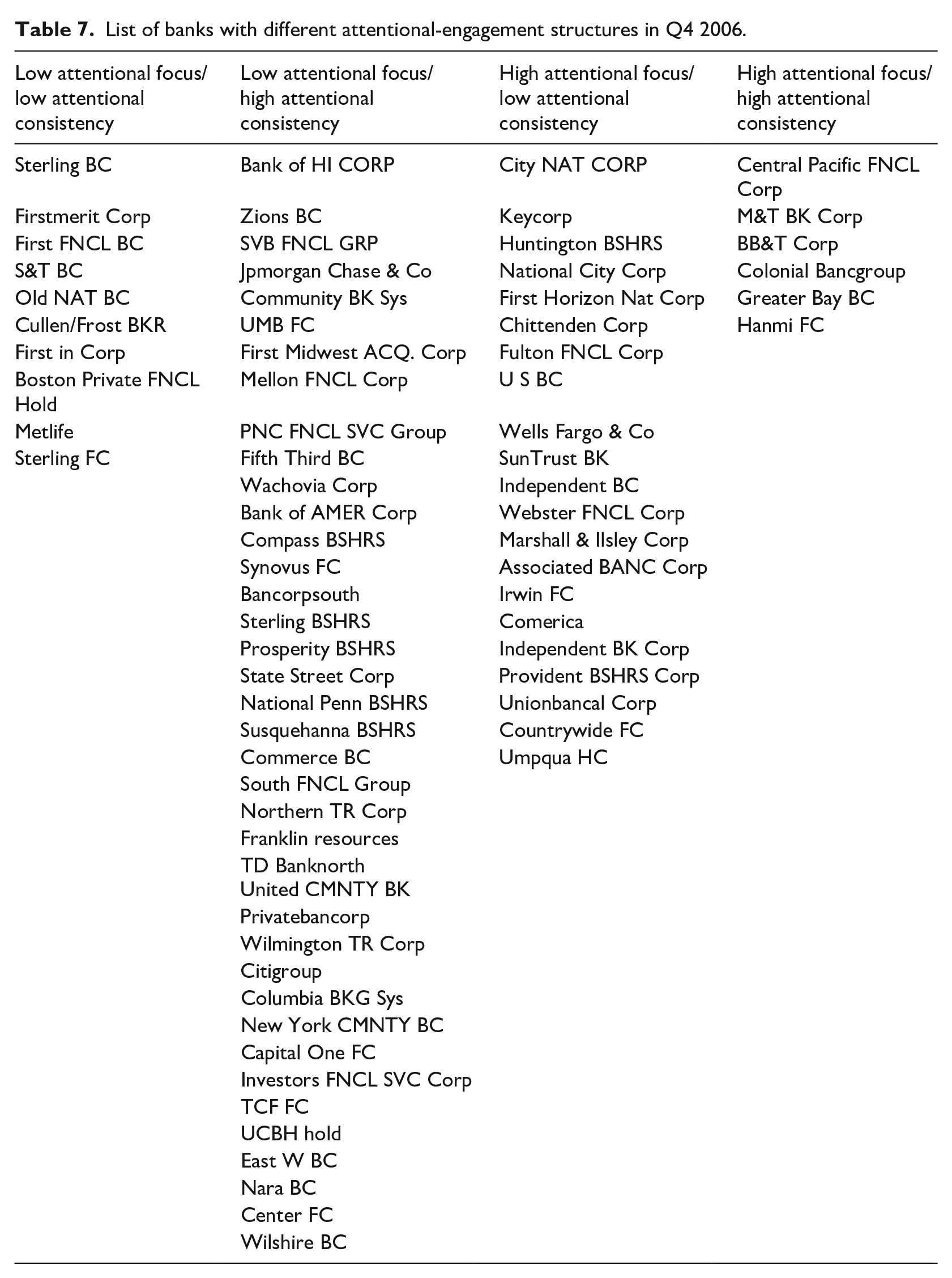

We used the median scores of attentional focus and attentional consistency measured for all firms from 2002 to 2010 as the thresholds for the high and low scores. We then classified our sample of firms into a two-by-two matrix using attentional focus and attentional consistency as the two dimensions (refer to Appendix 1, Table 7, for a list of banks classified into each of the four categories). Within the cross-sectional subsample of firms in 2006, 7.8% of the banks were high on both attentional focus and attentional consistency, 27.6% were high on attentional focus but low on attentional consistency, 51.3% were low on attentional focus but high on attentional consistency, and 13.2% were low on both attentional focus and attentional consistency.

Next, for each transcript from Q4 2006, we ran a key word in context (KWIC) search that extracted paragraphs of the conference call in which the top managers discussed issues related to the US housing market. We read through the extracted paragraphs and openly coded them. Where applicable, we appraised and coded the subject matter (e.g. “loan growth,” “real-estate investments,” “mortgage-servicing fees,” “adjusting reserves”) as well as the underlying cognition associated with the subject matter (e.g. “Our commercial real estate portfolio continues to perform well” was coded as high on managerial certainty). Table 2 presents the classifications of qualitative examples from managerial discussions based on high and low levels of attentional focus and attentional consistency allocated toward the US housing market.

Illustrative examples of managerial discussions of the US housing market during earnings conference calls in Q4 2006.

In the following sections, we develop our theory in the context of these qualitative examples. In particular, we show how managers’ cognition patterns are situated in different attentional-engagement structures.

High attentional engagement (high focus and high consistency) to discontinuous change: immersive learning and deliberative reasoning

Scholars have suggested that unfamiliar and novel information—especially information related to discontinuous change—is more likely to be introduced and integrated into an organization’s knowledge system when there is high attentional engagement (e.g. Joseph and Wilson, 2017; Shepherd et al., 2017). When both attentional focus and consistency toward an issue are high, the organization can accumulate and document a rich set of information about the focal issue over time. In an information-rich context, decision-makers are more likely to find themselves in an immersive learning environment that allows for and facilitates deliberative reasoning processes, such as abductive thinking (Kahneman, 2003; Shepherd et al., 2017).

Shepherd et al. (2017) speculate that decision-makers are more likely to engage in abductive-reasoning processes when an issue receives constant attention. Abductive reasoning involves the “act of proposing speculative but plausible conjectures about the nature of a phenomenon, and hence what kinds of evidence might increase the prospects of further insights into it” (Folger and Stein, 2017: 307). After encountering indications of discontinuous change, managers engaging in abductive reasoning are more likely to deliberate on, question, or revise their prior understandings and assumptions about complex organizational subsystems that interface with the environment (Shepherd et al., 2017: 634). This deliberation process, which is more likely to be initiated when there is both greater focus on and consistent attention paid to the changing environment, allows weak cues on discontinuous change to be better understood and appropriated by decision-makers, which subsequently enables them to formulate appropriate strategic responses (Gavetti et al., 2005). In this regard, Rerup (2009) argues that the complexity of an issue can be analyzed “only when it is looked at with accuracy and discipline over time” (p. 878). This fosters more efficient and disciplined accumulation of knowledge from an organizational-learning perspective (Weick and Sutcliffe, 2006).

Among the banks exhibiting high attentional engagement, characterized by high attentional focus and attentional consistency toward the US housing market, top executives were more aware of the economic slowdown in the environment by the end of 2006. These deliberated assessments were evident even when recent firm performance did not reflect the deteriorating economic conditions:

Given the recent national attention focused on the housing market I would also want to share that while we were made vigilant to market conditions, we remained quite comfortable with the quality and performance of our construction loan portfolio. (Greater Bay Bancorp, Q4 2006)

Moreover, managers were skeptical about the prospects for the US housing market, even when public experts’ opinions remained bullish:

Factors which all line with the views recently expressed by the chief economist of the California Association of Realtors as well as a report from Moody’s, would suggest the Bay Area housing market is likely to outperform the state as a whole. Again, we are not so cavalier as to apply this broad brush to every individual project, and we steadily intensified our risk monitoring practices in response to current market conditions. (Greater Bay Bancorp, Q4 2006) We—I’d be wary of anybody having great commercial real estate growth rates in this market. They might be getting adverse selection. It slowed quicker than we expected. (BB&T, Q4 2006)

Notably, bank executives exhibiting high attentional engagement with the real-estate market over the previous year tended to provide a richer deliberation on and assessment of the factors underlying the downturn in the fourth quarter of 2006. For instance, BB&T’s managers discussed the causes of the slowdown in the housing market, which they viewed as supply driven:

That was almost totally driven by a significant slowdown in our commercial real estate lending activity, primarily single-family residential construction. We kind of hit a wall in July, and mostly client driven—where our clients stopped building new homes. Stopped—starting as many subdivisions and reflecting slower activity in the residential markets. So it’s largely driven by what I call borrowed adjustments, we got a little tighter reflecting the slower activity particularly in the condo markets. Part of it might have been driven by us. (BB&T, Q4 2006)

We also contend that as managers or decision-makers engage in the deliberative reasoning processes afforded by high attentional-engagement structures, they become more likely to formulate appropriate strategic responses with respect to the imminent discontinuous change. If the discontinuity has the potential to disrupt the organization’s existing strategies and routines, managers are more likely to take actions that break with the status quo (Rajagopalan and Spreitzer, 1997; Wiersema and Bantel, 1992). This is consistent with our observation in banks with high attentional engagement with the real-estate market. As these bank executives revealed, they tended to make changes to their strategies by reducing their exposure to real-estate loans, which reflected their beliefs about the deteriorating housing market:

With uncertainties and a low cap rate, activity in the commercial real estate market has slowed [. . .] within the loan portfolio, there was a slight shift out of real estate loans into commercial and industrial loans accounting for 61% of the performance and grew 4.6% over the second quarter. (Hanmi Financial, Q4 2006)

Overall, these illustrative excerpts are consistent with and support our argument that organizations with greater attentional engagement with the external environment are more likely to notice, make sense of, and respond to discontinuous environmental changes.

Low attentional engagement (low focus and low consistency) to discontinuous change: no learning

In contrast to high attentional engagement, we contend that if attentional engagement is low in terms of both focus and consistency, the quality of managerial sensemaking may suffer (Levinthal and Rerup, 2006; Weick and Sutcliffe, 2006). When attentional focus and consistency to a particular issue are low, little information about the issue is gathered over time. In such an organizational environment, decision-makers are unlikely to engage in the deliberative or abductive-reasoning processes crucial for the formation of beliefs about radical changes. Rather, little to no learning about the discontinuous change is likely in a low attentional-engagement environment.

In cases where banks had low attentional engagement (i.e. allocated low attentional focus and low attentional consistency to the US housing market), top managers generally did not discuss the housing market conditions during their quarterly earnings conference calls. In the few cases where managers did discuss this issue, they largely downplayed the deteriorating conditions and the rising losses in their real-estate portfolios:

A strong loan base of commercial and industrial loans, commercial real estate loans, residential real estate construction loans continued to fuel the significant growth in our net income. While the Western regional real estate market is experiencing some cyclical adjustments; the Northwest remains solid with a slowing to more normal levels. [. . .] We have seen an increase in nonperforming loans due to one large commercial real estate loan relationship. We believe we have more than enough collateral and will be made whole on this particular relationship. (Sterling Financial, Q4 2006)

Moreover, some banks maintained their strategy of increasing the proportion of real-estate-related products in their portfolios despite the declining housing market conditions. Their maintenance of the status quo was partly driven by their lack of learning about the discontinuity in the housing market and its potential impact. For instance:

With the acquisition of Gibraltar, the mix of our loan portfolio has shifted toward residential, which generally have a lower interest rate than commercial loans. Residential loan originations for the third quarter, excluding loans held for sale, were approximately $156 million . . . So the third quarter saw many new strategic relationships for Boston Private and the pipelines on both coasts for loan activity looked solid. If you look at [our] Loan Portfolio Quality, our ratio of nonperforming loans to total loans was 30 basis points, compared to 15 basis points at June 30, 2006. The increase was primarily due to one loan of $6.4 million that we expect to be resolved without a loss. This loan is well secured. We also charged down a repossessed asset to an appropriate carrying value. While our nonperforming loans increased during the quarter, we do not believe it reflects a fundamental change in the quality of our loan portfolio. (Boston Private Financial, Q4 2006)

Taken together, these qualitative examples suggest that by the fourth quarter of 2006, organizations that exhibited low attentional focus and low attentional consistency were more likely to fail to perceive the changing market conditions as a discontinuous change that required a shift in assumptions and strategy. In turn, they are more likely to maintain the status quo and not make any changes to their operations (Hambrick et al., 1993; Staw et al., 1981). On the other hand, banks with both high attentional focus and high attentional consistency toward the housing market were more likely to be cognizant about the emerging changes, as evident in their elaborate discussions of the deteriorating market conditions. These banks were also more likely to view the market slowdown as a discontinuity, and to respond by reducing or limiting their exposure to real-estate loans. 2 Such actions are consistent with the idea that high attentional focus and high attentional consistency in relation to the external environment enhances organizations’ noticing and sensemaking activities. Given the contrast in cognitive learning processes between high attentional engagement (high focus and high consistency) and low attentional engagement (low focus and low consistency), we proffer the following hypothesis:

Trade-off between attentional focus and consistency

Thus far, we have examined the extremes of the two dimensions of attentional engagement—attentional focus and consistency. Although we theorized how high attentional engagement with a discontinuous change is crucial for the activation of deliberative reasoning processes that enable managers to formulate appropriate strategic responses, enacting high attentional engagement can be costly for the organization. As cognitive resources are limited, high attentional engagement implies that managers have to reduce the attention they pay to other issues pertinent to the organization. Prior research suggests that managers must constantly divide their attention among issues as they prioritize which issues to attend to Ocasio (2011) and Ocasio and Wohlgezogen (2010). As managers increase their attentional focus and consistency toward a particular issue, they learn and update their beliefs regarding that issue. The downside of attentional engagement to particular issue is that managers are also less able to focus and sustain attention toward other emerging issues by which they could be blindsided. Thus, there may be an inherent trade-off between attentional focus and attentional consistency—as managers increase their attentional focus on a particular issue, it becomes more effortful and costly to consistently sustain that focus over time; conversely, managers can sustain consistent attention to an issue over time if that attention is not too high. An implication of this trade-off is that fewer firms are likely to maintain both high attentional focus and consistency, and that more firms should exhibit moderate levels of attention engagement, that is, intermediate levels of attentional focus and attentional consistency. This is consistent with the distribution of the cross-sectional subsample of firms in Q4 2006 (see Table 2).

In the following section, we consider how the situated learning and cognitive processes differ under moderate attentional engagement characterized by varying levels of attentional focus and attentional consistency.

Moderate attentional engagement (high focus and low consistency) to discontinuous change: selective learning and certainty perceptions

Similar to high levels of attentional engagement, we contend that an attentional-engagement structure characterized by high attentional focus and low consistency is likely to create an information-rich environment. However, the lack of consistent attention on a particular issue suggests that the flow of informational cues about potential discontinuities is irregular. Thus, even though information is likely to be rich whenever attentional focus is high, the lack of attentional consistency suggests that there are periods when information is inevitably omitted. As such, attentional engagement characterized by high attentional focus and low consistency is likely to lead to selective learning processes (Gould, 1986; Terlaak and Gong, 2008) in which managers make sense of the potential discontinuity based on a selective set of information or knowledge that is inconsistently sampled from its source.

Selective learning processes can be problematic when it comes to making sense of potential discontinuities because of the nature of informational cues about those discontinuities. First, informational cues about imminent discontinuities are unlikely to arrive in a timely or predictable fashion (Ansoff, 1975). Moreover, as any cues regarding a radical change challenge the current status quo and understanding of the environment, they might be ignored (Lampel and Shapira, 2001). Second, informational cues from the external environment about imminent discontinuities are arguably rare, at least initially. In addition, as informational cues related to emerging discontinuities might be presented in forms that are distant and irrelevant to the eventual discontinuous change, they may not be obvious or salient to observers in the initial phases (Weick and Sutcliffe, 2006). Taken together, the scarcity and irregularity of informational cues about emerging discontinuities suggest that sustained attention on the external environment over time is crucial. When attentional structures are low on attentional consistency, managers are likely to miss vital signs of discontinuity.

Selective learning processes are also problematic because they heighten managerial perceptions of certainty about their external environment (Moore and Healy, 2008). As managers make sense of a set of rich information that is inherently biased because of missing cues regarding the discontinuous change in the environment, they are likely to discount the very possibility of a discontinuous change (Gervais and Odean, 2001). Over time, selective learning using inconsistently sampled information leads managers to develop overly certain and erroneous perceptions about their external environment (Moore et al., 2015). Even if decision-makers are subsequently presented with strong evidence of imminent discontinuous change, their sense of certainty may lead them to ignore or misinterpret that evidence (Rerup, 2009).

Just like banks exhibiting high levels of attentional engagement, we find that banks with high attentional focus but low attentional consistency exhibited an awareness of the slowdown in the housing market. For example, SunTrust bank noted the slowdown in the US housing market:

Continuing with mortgage, although production was down in the third quarter compared to the second quarter, application volume remained very strong at $22 billion for the third quarter, slightly under the record application volume we generated in the second quarter. The drop in production, on the other hand, is simply the result of a decrease in application pull through rates which is not unexpected given rate conditions and the slowdown in the housing market. With production generally being slower and no expectation of any MSR gains in the fourth quarter, we do expect mortgage related income to decline in the fourth quarter. (SunTrust, Q4 2006)

However, unlike banks that were high on both attentional focus and consistency dimensions, SunTrust remained rather certain and optimistic about the growth potential in the US housing market and real-estate-related products for the following year. In this regard, its managers stated:

Growth has been particularly strong in real estate related products, mortgage, home equity line and construction lending. We think a similar result in 2007 is obtainable with loans growing in the upper single-digits with some slowdown in the residential real estate areas offset by growth in other categories, however, overall not materially different from what we experienced this year. (SunTrust, Q4 2006)

Similar to SunTrust, Umpqua’s executives displayed a clear awareness of the deteriorating housing market:

While we remain optimistic, we are cautious about the transitioning economy and are confident in our ability to react quickly to the changing environment. Further, as we will show, despite a softer economy, our credit performance in all key majors remains excellent relative to both our peers and to our own historical results. (Umpqua, Q4 2006)

At the same time, they maintained a belief that the housing market could grow even more than before:

Adding to the challenge of bringing in new operations, there have been recent signs of economic softening in some of our markets, particularly within central California’s home building industry. Management believes a slowdown in housing starts in the greater Sacramento area could, in fact, produce favorable results in the long-term for the area. Even with the current slowdown, housing starts remain above levels produced just a few years ago and should create a more sustainable level of growth that the current infrastructure and supply and demand can rely upon. (Umpqua, Q4 2006)

A consequence of high certainty perceptions driven by selective learning is that managers are likely to formulate strategic actions that reinforce the status quo, that is, escalate the current course of action (McNamara et al., 2002; Staw et al., 1997; Staw and Ross, 1978). In fact, the qualitative examples from Q4 2006 suggest that managers remained optimistic about market conditions despite signs of deterioration in the US housing market. Given these confident beliefs that market conditions would improve, these banks’ not only maintained their strategies but also announced plans to expand their portfolios’ exposure to the real-estate market. For instance, the top executives of First Horizon National Corp and Countrywide Financial Corp stated:

The good news in mortgage is that we have been able to grow our sales force in a down market. Although the first quarter will be impacted by the normal seasonal declines in home purchase volume, mortgage banking is expected to become profitable again in 2007, as a continuation of productivity initiatives, rationalized with our fixed costs to the clear market demand and growth in our mortgage sales force return. Also, the incremental growth of our national expansion initiatives is unfavorably impacted by a contraction in mortgage origination activities. As the mortgage market stabilizes and our mortgage sales force growth returns, cross-sell opportunities should increase. Mortgage has been and will continue to be a double-digit growth business over the long term and also provides us with an important strategic national growth platform. (First Horizon National Corp, Q4 2006) The company has invested in new business lines to supplement its current residential mortgage originations, as evidenced by the recent introduction of its reverse mortgage commercial real estate lending, and builder finance lending units . . . In summary, while we expect the continuation of a traditional environment in the near term, we are bullish on the positive long-term growth prospects for the mortgage lending industry and for countrywide in particular as a result of the proven power of our business model and our strategic positioning. We believe Countrywide’s core strategies, our profitable market share expansion, growth in our mortgage loan investment portfolio and associated spread income, continued synergistic diversification and ongoing capital optimization will continue to deliver long-term shareholder value. (Countrywide Financial Corp, Q4 2006)

In summary, the above discussion and examples suggest that when attentional focus is high but attentional consistency is low, selective learning is likely to dominate, which fosters perceptions of certainty among managers. This increases the likelihood that managers will formulate strategic actions that reinforce the status quo. We therefore posit the following:

Moderate attentional engagement (low focus and high consistency) to discontinuous change: noisy learning and uncertainty perceptions

We now consider how attentional engagement affects an organization’s response to an environmental change when attentional focus is low but attentional consistency to the potential discontinuity is high. Given such an attentional-engagement structure, the flow of information about the external environment into the organization is consistent over time and, thus, unlikely to be erratic. However, because attentional focus is low, the nature of information on potential discontinuities that the organization receives is unlikely to be rich or well-elaborated. With such an attentional-engagement structure, the quality of information about potential discontinuities accumulated over time is likely to be noisy.

We contend that when faced with this type of information environment, managers engage in noisy learning, as they must make sense of low-quality information about their environment. Noisy learning occurs when decision-makers engage in sensemaking based on ambiguous information (George et al., 2006; March and Olsen, 1975; Zhao and Olivera, 2006). This is analogous to a low signal-to-noise ratio in which the signal is the true, underlying information, but it is obscured by uncorrelated and seemingly random information (Zhao and Olivera, 2006). Noise is high under such attentional-engagement structures for at least two reasons. First, constant managerial attention to the external environment invites the collection of a wide variety of information, which may or may not include vital cues on potential discontinuities. Second, even if the organization picks up informational cues about potential discontinuities because of its consistent attention, those cues are likely to be poorly captured or represented because attentional focus to the external environment is low.

Noisy learning processes can be effortful for managers, as they must engage in sensemaking to differentiate between valuable information and noise. Given the large amount of noise, managerial learning is also likely to be slower (March, 1991) than if managers exhibited full attentional engagement. Even when presented with evidence of imminent discontinuous change, this evidence may be poorly represented owing to managers’ low attentional focus. Managers may, in turn, unintentionally ignore or misinterpret that evidence (Rerup, 2009). A consequence of noisy learning is that managers are likely to have perceptions of greater uncertainty. These perceptions are likely to increase over time, as managers must constantly make sense of noisy information and choose which pieces of information to focus on or discard.

In our subsample of banks with attentional-engagement structures characterized by low attentional focus and high attentional consistency, we found that top executives tended to exhibit greater uncertainty about the real-estate market. One example is South Financial Group. Its top executives indicated uncertainty about the bank’s real-estate portfolio while speculating on several factors affecting its loan growth:

One of this team’s key projects over the last year has been to evaluate and shock our commercial real estate portfolio by product and by market to see how it would react in certain situations. We believe our current loan growth has slowed due to several factors, an increase in payoffs as several commercial real estate projects completed and went to the permanent market, a leadership change in our South Carolina bank and other various internal efforts that we have underway, and an overall slowdown in the market activity. (South Financial Group, Q4 2006)

Other banks also noted that the markets were becoming increasingly skittish:

The commercial loan growth was in real estate and construction lending, where activity continues to be driven by housing demand as Delaware’s population rises, although the housing market is coy. (Wilmington Trust Corp, Q4 2006)

In light of the heightened uncertainty regarding a potential discontinuous change, we posit that organizations are also less confident about making changes to the status quo. Therefore, when faced with such dissonance or uncertainty, managers are more likely to formulate actions that help them cope with the rising uncertainty (Festinger, 1962; Hinojosa et al., 2017), especially when the opportunity costs of failing to anticipate the effects of a discontinuous change are high. These actions help to “hedge” against the possibility that any form of discontinuous change will be realized (George et al., 2006; Smith and Stulz, 1985). However, we posit that there is a boundary condition: when the opportunity costs of adapting to the discontinuous change are low, we suggest that such status quo-hedging actions are likely to be muted, as managers will choose to maintain the status quo instead.

In the context of the US housing market, we posit that bank executives who were uncertain about the market were less likely to reinforce or reduce their exposure to the real-estate market. Instead, they were more likely to take steps to hedge against possible downsides, especially when their portfolio exposure to the real-estate market was high. For example, banks with such attentional structures discussed how rather than limiting their exposure to housing loans, they became more cautious of making changes to their portfolios:

Annualized, on a linked quarter basis, consumer loans up a little bit less, and mortgage loans continued to decline as they have over the past quarters. So, therefore, we’ve not gotten a number of new loans booked that we historically have and at the same time, on a good news/bad news scenario, we’ve gotten a lot of repayments on some of our real estate projects. (TD Banknorth, Q4 2006)

As such, some banks took actions to hedge their strategies by increasing their capital-liquidity requirements or their liquidity to buffer against possible losses from changing market conditions:

We anticipate that the provision for loan losses for the upcoming quarter will not be as high as the third quarter. We have targeted to securitize about 400 million in residential loans in the next quarter. This will help improve liquidity, lower capital requirements, and should help to reduce the provision for loan losses. (East West Bancorp, Q4 2006)

Other banks hedged their real-estate portfolios by taking steps to diversify their businesses:

Achieving our earnings growth in these two lines of business will allow us to continue to lessen the concentration of real estate loans in our portfolio. (UCBH Holdings, Q4 2006) More importantly, the steep rise in bankruptcies is like to continue, given the large stock of highly indebted households and the aggressive marketing by debt management companies. Our diversified set of home loan products reduced the impact of interest rate cycles on our home loan business. (Capital One Financial, Q4 2006)

Overall, we suggest that noisy learning processes are likely to be situated in attentional-engagement structures with low attentional focus but high attentional consistency. In turn, noisy learning processes are likely to increase uncertainty in managerial perceptions of changes in the external environment. This facilitates the formulation of status quo-hedging strategic responses, especially when the opportunity costs of not doing so are high:

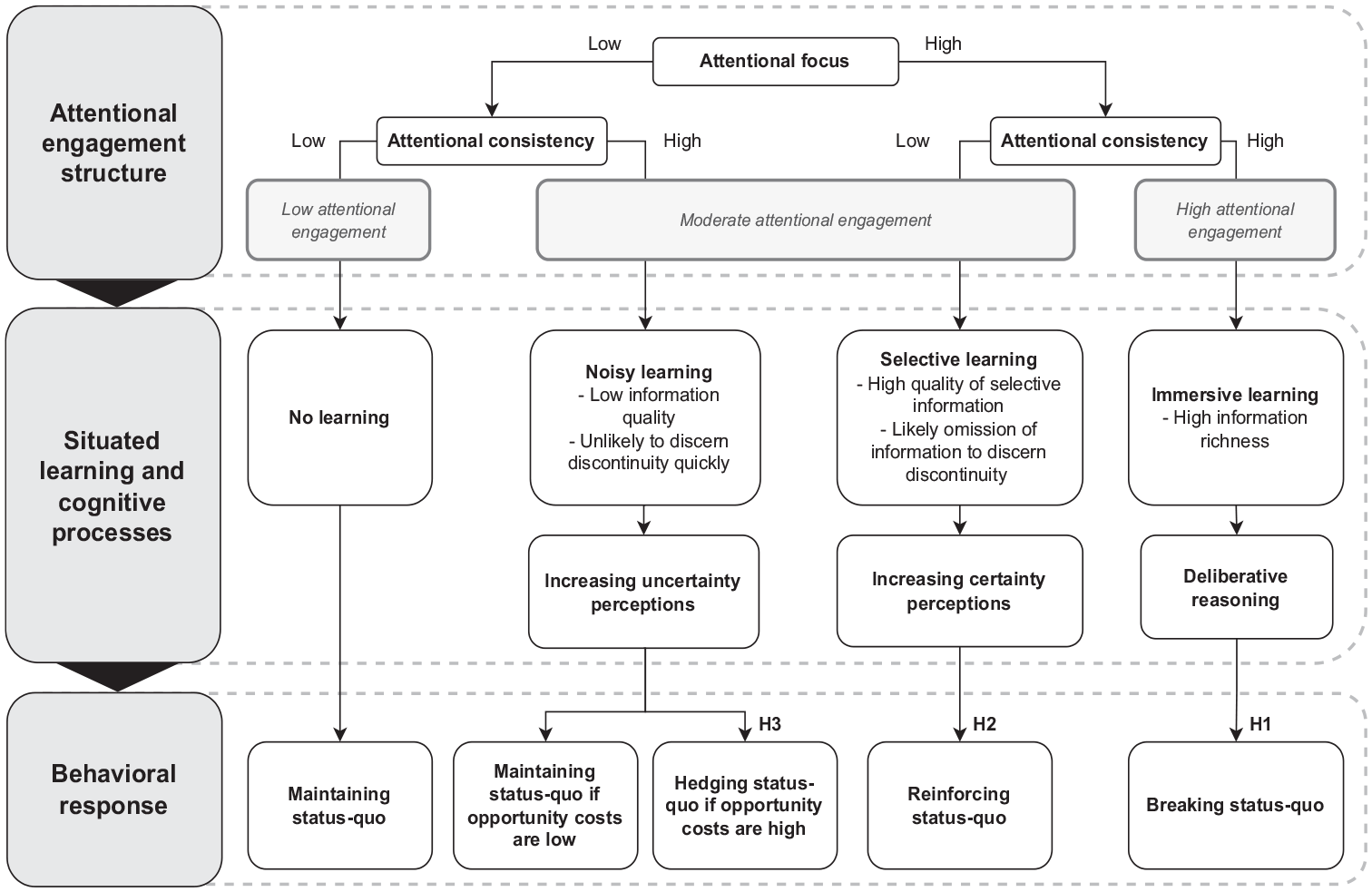

Our discussion thus far highlights how different attentional-engagement structures induce different forms of learning, cognitive processes, and strategic responses. Figure 1 presents a summary of the how managerial learning and cognition processes are situated in different attentional structures. Although the qualitative excerpts illustrate our arguments in context, we note that managers’ cognitive and learning processes, as well as their strategic responses, are not necessarily determined by the particular type of their attentional engagement to the external environment. For instance, even though Webster Financial only had moderate levels of attentional engagement (i.e. high attentional focus and low attentional consistency) to the real-estate market in 2006, the bank decided to break the status quo early by reducing their exposure to the segment, reporting that they “would sell all residential fixed rate mortgage production, again, starting in July of 2006.” Nevertheless, to ensure that our inferences about the cognitive and learning are generalizable beyond the cited examples in Q4 2006, we also conducted additional quantitative text analyses on a larger sample of transcripts and found that these results are similar to our qualitative examples above (see Appendix 1 for additional analyses on these learning and cognitive processes).

Situated learning and cognition process model of attentional engagement and behavioral responses to discontinuous change.

In the next section, we formally test our hypotheses in a quantitative examination of longitudinal panel data on US banks. 4

Data and method

Sample

We tested our hypotheses using longitudinal data covering US banking firms from 2002 through 2010. We focused our analyses on bank holding companies rather than individual commercial banks or savings institutions because strategic management and risk management are usually handled by executives at the highest level of a banking group. We collected transcripts of earnings conference calls from the Dow Jones’ Factiva, Lexis-Nexis, and FactSet’s Callstreet databases. In addition, we gathered data on the banks’ accounting and loan portfolios from the Federal Reserve Board’s (FRB) Regulatory Banking Database and Compustat. The intersection of all available data for the focal time period yielded a final sample of 96 US bank holding companies. Despite the small number of firms, our sample is representative of the majority of the US banking system. More specifically, the firms in our sample represented approximately 70% of total bank holding company assets reported to the FRB in 2007.

Dependent variable

Status quo-reinforcing and status quo-breaking responses

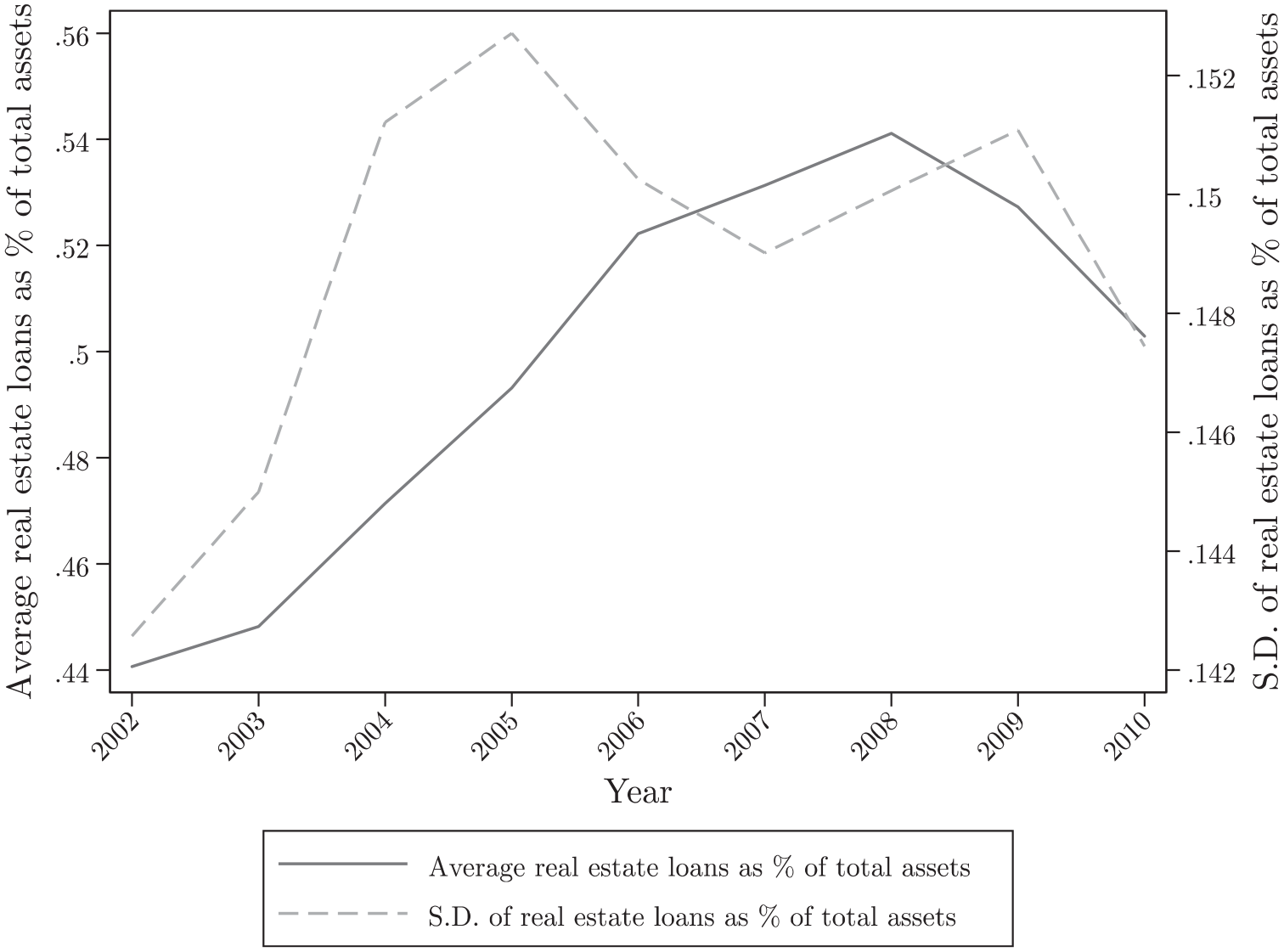

According to the quarterly surveys conducted by the FRB, banks began tightening lending standards, especially in the real-estate market, when market conditions began to deteriorate in 2006 (Federal Reserve Board (FRB), 2007). Our data suggest a similar trend in the banks’ lending practices during the study period (see Figure 2). Prior to 2006, banks had generally been increasing their exposure to the real-estate mortgage market. Notably, the variance in the banks’ exposure to the real-estate market also increased during this period. This suggests that some firms might have been reducing their exposure to real-estate loans or even exiting the market before the onset of the housing market crisis. As shown above, the qualitative examples from the conference-call transcripts also suggest that banks varied in their responses to conditions in the real-estate market.

US banks’ real-estate loan holdings, 2002–2010*.

Given the considerable heterogeneity among the banks’ responses, we were interested in understanding why certain banks enacted a status quo-breaking (i.e. decreasing their exposure to real-estate mortgage market) or status quo-reinforcing (i.e. increasing their exposure) response when the market seemed to be declining. We measured the amount of real-estate loans as a percentage of each bank’s total assets over time to gauge the type of each bank’s strategic response to the discontinuous change in the US housing market. Thus, we measured a bank’s response as status quo breaking if it decreased its exposure to real-estate loan assets, and as status quo-reinforcing if it increases its real-estate loan asset exposure.

Status quo-hedging response

We captured the extent to which firms responded to the imminent discontinuous change with a status quo-hedging response by measuring their total risk-based capital ratio, which is the ratio of the bank’s total capital to its risk-weighted assets. While banking organizations are required to maintain a minimum total risk-based capital ratio, well-capitalized banks often increase the allocation of capital against risky assets, such that they have a higher total risk-based capital ratio to buffer them against liquidity shocks or portfolio losses (Hogan, 2015). Thus, we expect banks to increase their total risk-based capital ratio to hedge their existing asset portfolios against downside risks (George et al., 2006; Smith and Stulz, 1985).

Key independent variables

As our key construct, attentional engagement, is a combination of the extent of both attentional focus and attentional consistency, we measured these two components separately. 5 Hence, we captured attentional engagement as the interaction between the attentional focus and attentional consistency measures.

Attentional focus

We measured the amount of attention an organization allocated to the real-estate market as the degree of attention paid to that market during post-earning conference calls in the four quarters prior to the focal quarter. First, we measured the attention paid to the real-estate market in each quarter by counting the number of words related to that market: “home(s),” “household(s),” “housing,” “mortgage(s),” “residential,” and “real estate.” We then normalized this measure by dividing it by the total number of words in each quarter, multiplied by 100, to facilitate the interpretation of the estimated coefficients. Finally, we calculated the average of the normalized measure over the four previous quarters (i.e. from t−4 to t−1) to derive the attentional focus measure.

Attentional consistency

To measure attentional consistency, we computed the standard deviation using the normalized real-estate market attention over the four previous quarters. We then reverse-scored the value, so that, lower variation in the attention measure over the four previous quarters represented higher attentional consistency. This empirical measure is consistent with the notion that consistency refers to paying prolonged or sustained attention to a particular source of stimuli (Ocasio, 2011; Ocasio and Wohlgezogen, 2010; Rerup, 2009).

Control variables

We included several organizational-level variables to control for a firm’s motivation to respond to changes in the real-estate mortgage market. We included a bank’s return on assets (ROA) to control for its performance. We also controlled for non-performing assets because they provide an indication of the bank’s asset quality. A bank with a higher level of non-performing assets should be more motivated to respond to changing conditions in the real-estate market. We used two proxies to control for a bank’s ability to respond to the declining market: the level of loan securitization and the use of credit derivatives. Banks that engaged in loan securitization practices packaged loans into securities and then sold them to investors to raise capital. Banks also used credit derivatives, such as credit default swaps and collateral debt obligations, to transfer the credit risks associated with the underlying loans to other financial institutions. A bank that relies more on loan securitization and credit derivatives should be better able to manage its loan portfolio risks than banks that are less involved in such practices. We measured securitization and credit derivatives using the total amount of banks’ securitized loans and credit exposure to derivative contracts, respectively, both of which were divided by total assets. To control for possible organizational inertia, we included firm age as the total number of years since establishment. We also included a dummy variable to capture whether the bank acted as a primary dealer with the New York FRB, as primary dealers may be subject to additional regulatory commitments that influence their strategic actions. To control for heterogeneity related to bank complexity, we included three variables: firm size, loan-portfolio breadth, and the number of subsidiaries.

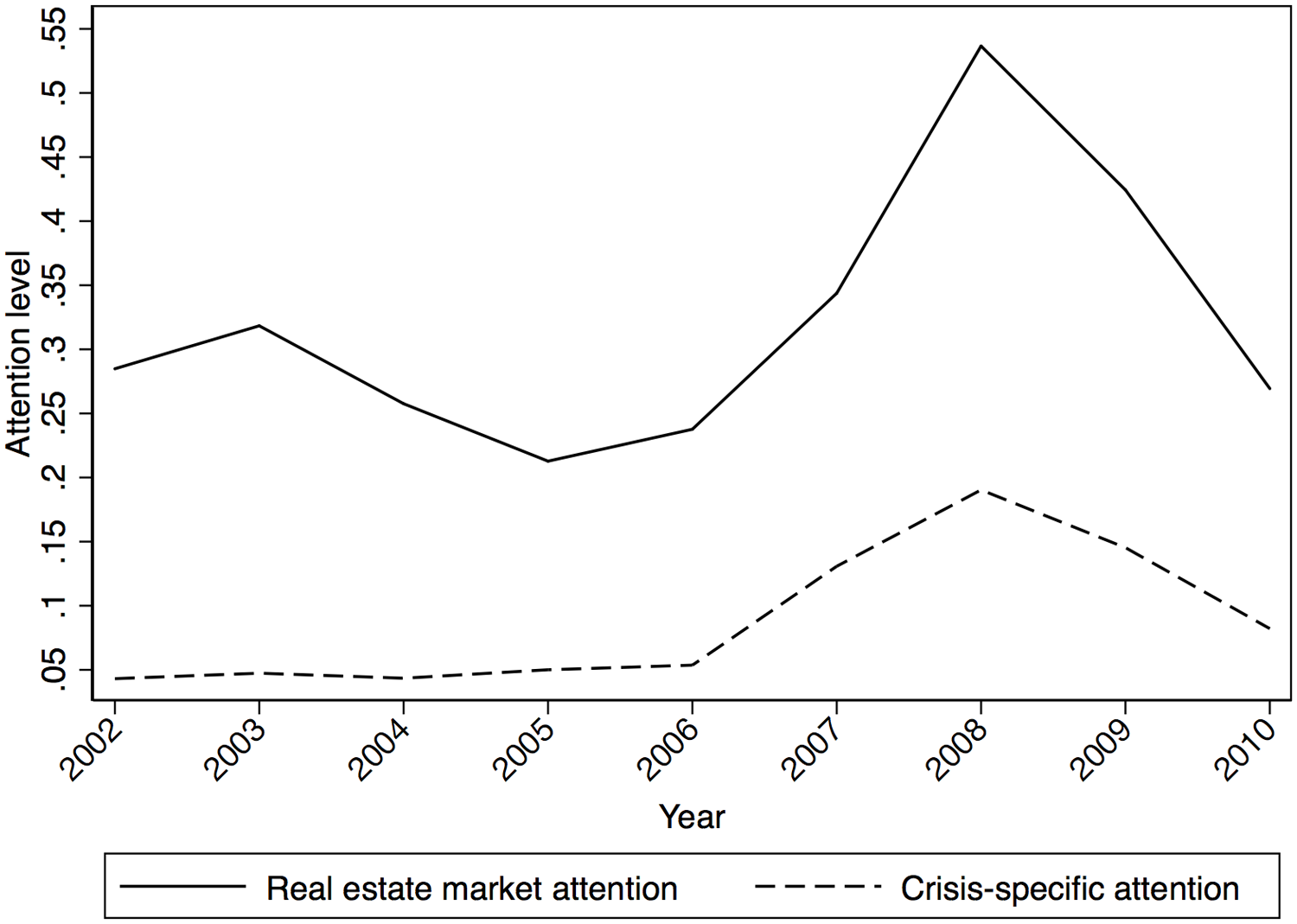

Finally, to control for the possibility that banks that were more attentive to the emergence of the housing crisis also paid more attention to the US housing market and reduced their exposure to real-estate loans, we included a housing-crisis attention variable, which we calculated as the percentage of total words related to the housing crisis (i.e. “foreclosure(s),” “subprime,” or “crisis”). In Figure 3, we compare the average attention the banks in our sample paid to the real-estate market over time to the attention they paid to the housing crisis. Consistent with our expectations, attention to the housing crisis rose starting in 2007 and peaked in 2008. However, prior to 2007, housing-crisis attention was consistently low and almost non-existent when compared to the attention paid to the real-estate market in general.

US real-estate market attention versus housing-crisis attention.

Estimations

For our quantitative analyses, we were interested in estimating the within-bank effect of attention on subsequent changes in real-estate loan investments or the liquidity position—that is, how changes in a bank’s attentional patterns relative to the real-estate market affected subsequent changes in its real-estate exposure or its liquidity position to buffer against losses. We used an ordinary least squares (OLS) specification with firm fixed effects with standard errors clustered at the firm level. Our results are robust to possible cross-sectional correlations among observations. We reran our analyses with standard error clustering by firm and calendar quarter (Petersen, 2009), and obtained the same results. We also included calendar-quarter dummies to control for unobserved time effects. All independent and control variables were lagged by one quarter in our regression models to alleviate reverse-causality concerns.

Given that we expect firms with high attentional engagement (i.e. high attentional focus and consistency) in our empirical context to engage in a status quo breaking responses by reducing their exposure to real-estate loans, we would consider Hypothesis 1 to be supported if attentional focus negatively predicts the firm’s real-estate loans when attentional consistency is high. Hypothesis 2, which suggests that firms with high attentional focus but low attentional focus will engage in status quo reinforcing responses, would be supported if attentional focus positively predicted the firm’s real-estate loans when attentional consistency is low. Finally, Hypothesis 3, which proposes that firms with low attentional focus but high attentional consistency will engage in status quo-hedging responses, would be supported if attentional focus exhibits a negative relationship with the total risk-based capital ratio when both attentional consistency and exposure to real-estate loans are high.

Results

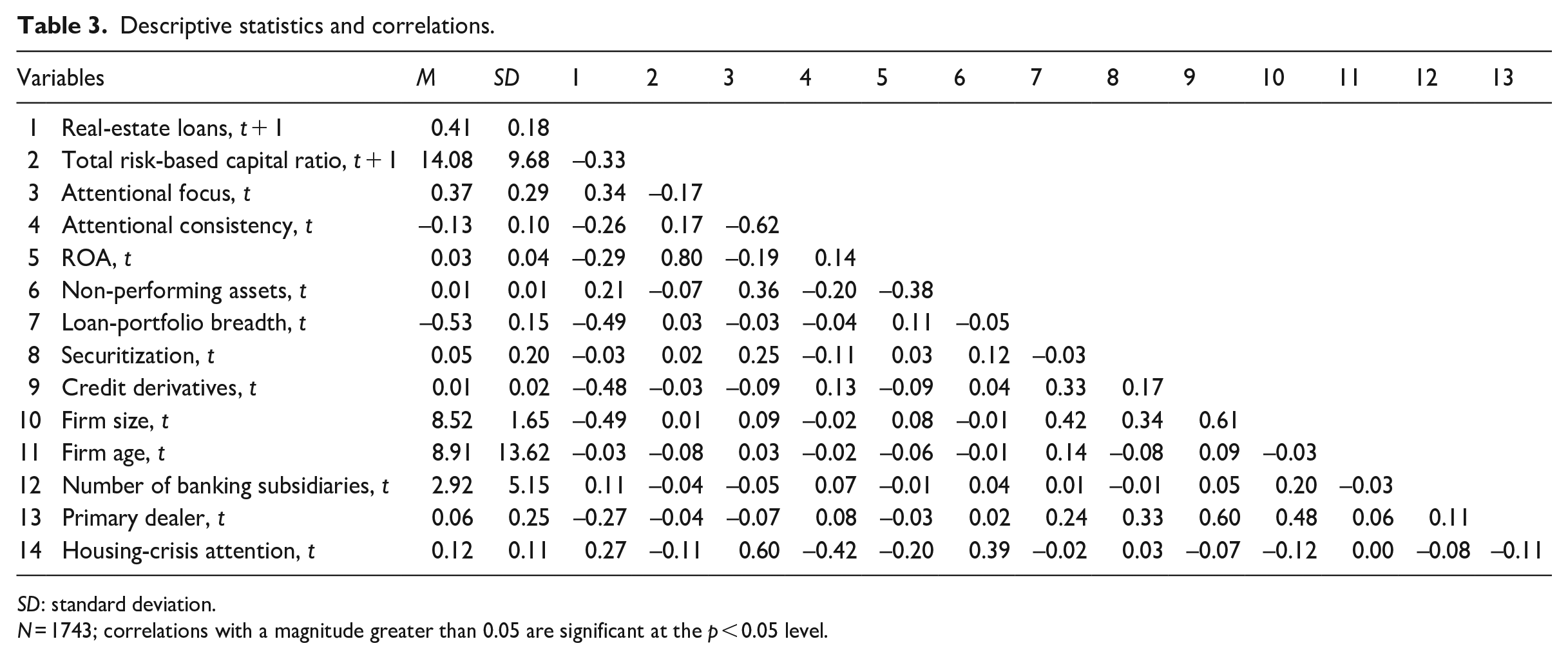

Table 3 presents the descriptive statistics and the correlations among the variables.

Descriptive statistics and correlations.

SD: standard deviation.

N = 1743; correlations with a magnitude greater than 0.05 are significant at the p < 0.05 level.

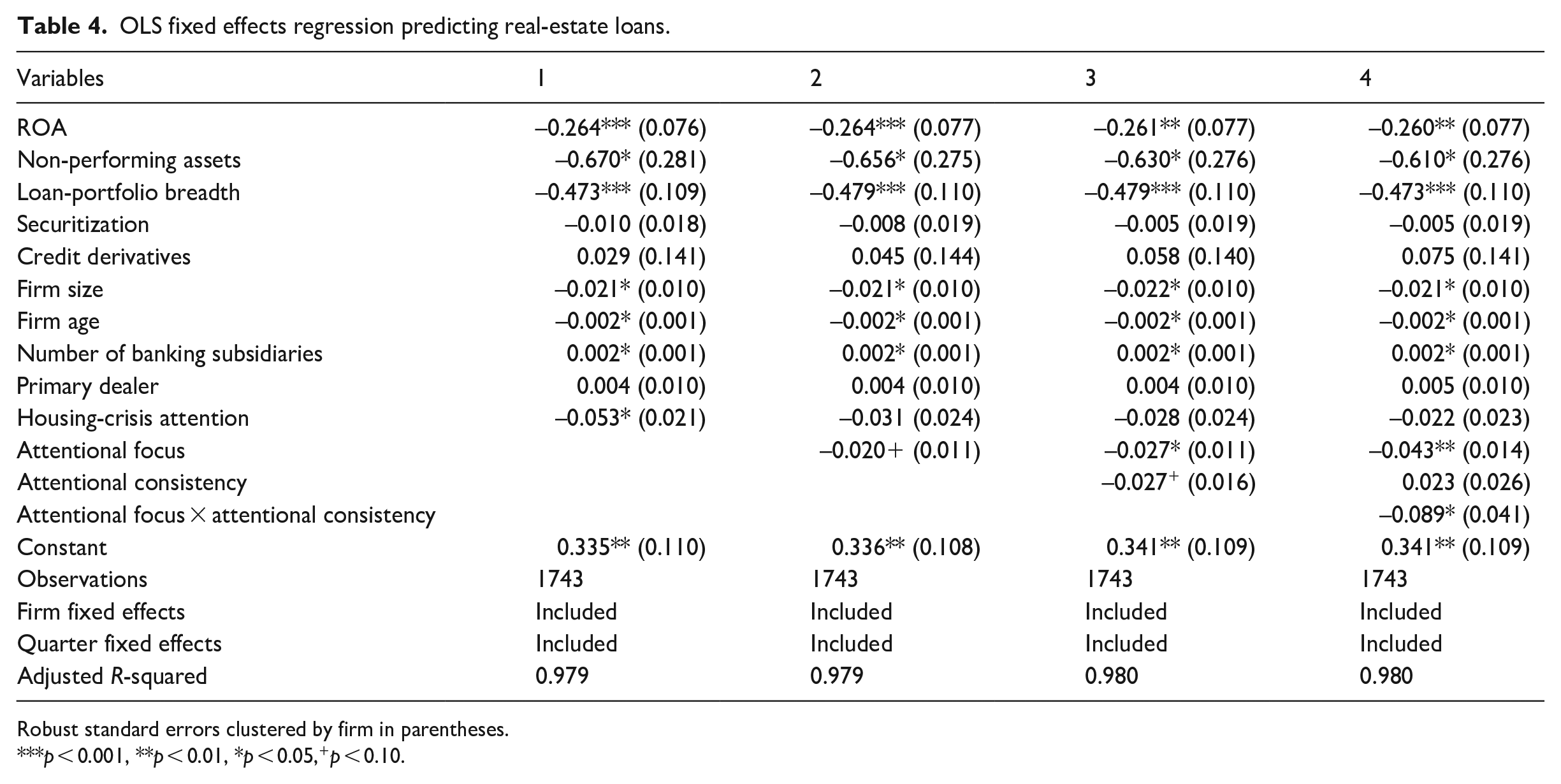

Table 4 reports the tests of Hypotheses 1 and 2. Model 1 in Table 4 includes only the control variables. The effect of attentional focus on the real-estate market in Model 2 is negative and significant (β = 0.020, p < 0.10). In Model 3, we add the attentional consistency variable. Its coefficient is also negative and significant (β = –0.027, p < 0.10). This suggests that the components of attentional engagement—attentional focus and attentional consistency—individually affect the organization’s strategic response.

OLS fixed effects regression predicting real-estate loans.

Robust standard errors clustered by firm in parentheses.

p < 0.001, **p < 0.01, *p < 0.05,+p < 0.10.

Hypotheses 1 and 2

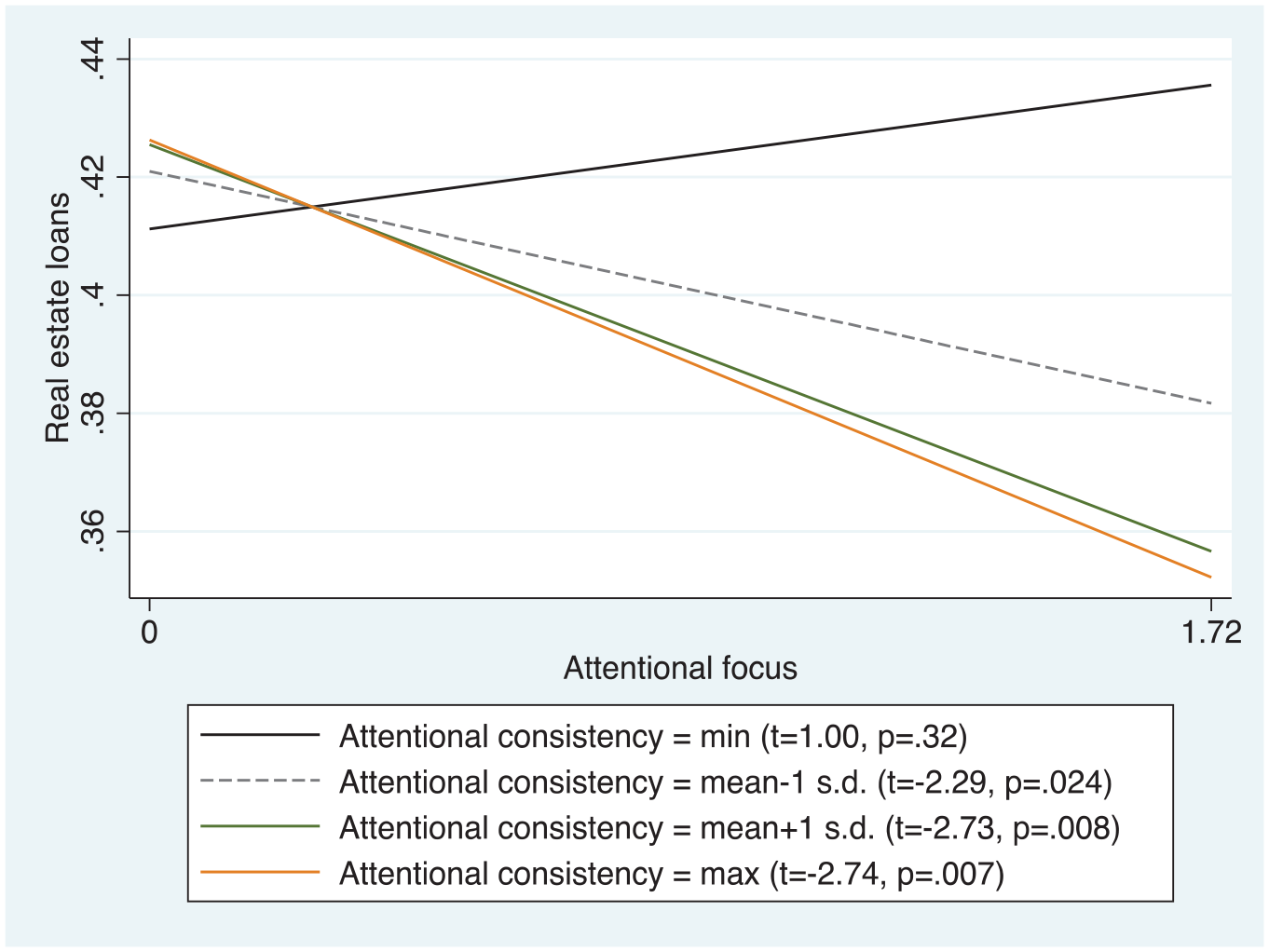

Hypothesis 1 posits that when attentional consistency is high, the relationship between attentional focus and real-estate loans is negative. In Model 4 of Table 4, we introduce the interaction term between attentional focus and attentional consistency. We find a negative and significant coefficient for the interaction term (β = –0.089, p < 0.05). This suggests that beyond their individual main effects, attentional focus and attentional consistency complement each other in strengthening the organization’s status quo-breaking response to the external environmental change. To visually examine Hypothesis 1, we used the estimates from Model 4, and plotted the relationship between real-estate loans and attentional focus at various levels of attentional consistency (minimum; one standard deviation below the mean; one standard deviation above the mean; maximum) in Figure 4. As Figure 4 shows, the relationship between attentional focus and real-estate loans becomes increasingly negative as attentional consistency increases. When attentional consistency is at its maximum, the slope for attentional focus is negative and significant (t = –2.74, p = 0.007), suggesting that when attentional engagement is high, firms are more likely to engage in the status quo-breaking response of reducing their exposure to real-estate loans. Thus, we find support for Hypothesis 1. In terms of economic significance, the coefficient estimate of −0.089 in Model 4 of Table 4 indicates that an increase in attentional consistency from one standard deviation below the mean to one standard deviation above the mean amplifies the average negative effect of attentional focus on real-estate loans by −0.0066 (–0.089 × 0.20 × 0.37). Using the mean value for real-estate loans, the magnitude of change is about 1.6% (–0.0066/0.41).

Effect of interaction of attentional focus × attentional consistency on real-estate loans.

Hypothesis 2 posits that when attentional consistency is low, the relationship between attentional focus and real-estate loans is positive. As Figure 4 shows, the relationship between attentional focus and real-estate loans becomes increasingly positive as attentional consistency decreases. However, for most of the range of values for attentional consistency, the relationship between attentional focus and real-estate loans is downward sloping. Although the relationship between attentional focus and real-estate loans is positive when attentional consistency is at its minimum, which is in line with the prediction of Hypothesis 2, the positive slope does not attain significance (t = 1.00, p = 0.32). Thus, we do not find statistical support for Hypothesis 2, which proposes that firms are more likely to engage in status quo-reinforcing responses when their attentional focus is high, and their attentional consistency is low.

Although we did not find support for Hypothesis 2, we suspect the lack of statistical support may be due to the weaker statistical power inherent to our research context and sampling: Most firms would have inevitably recognized that increasing exposure to real-estate loans is no longer ideal after the crisis in 2007, thus, there will be fewer firms engaging in status quo reinforcing responses after 2007. In additional analyses, we limited our sample to observations to the end of 2007 and repeated the slope analyses. We found that the positive slope between attentional focus and real-estate loans when attentional consistency is at its minimum becomes statistically significant (t = 2.31, p = 0.02), thus lending support for Hypothesis 2 in this subsample. This suggests that firms are more likely to engage in status quo reinforcing responses only in the earlier years when the nature of the discontinuous change remains uncertain.

Hypothesis 3

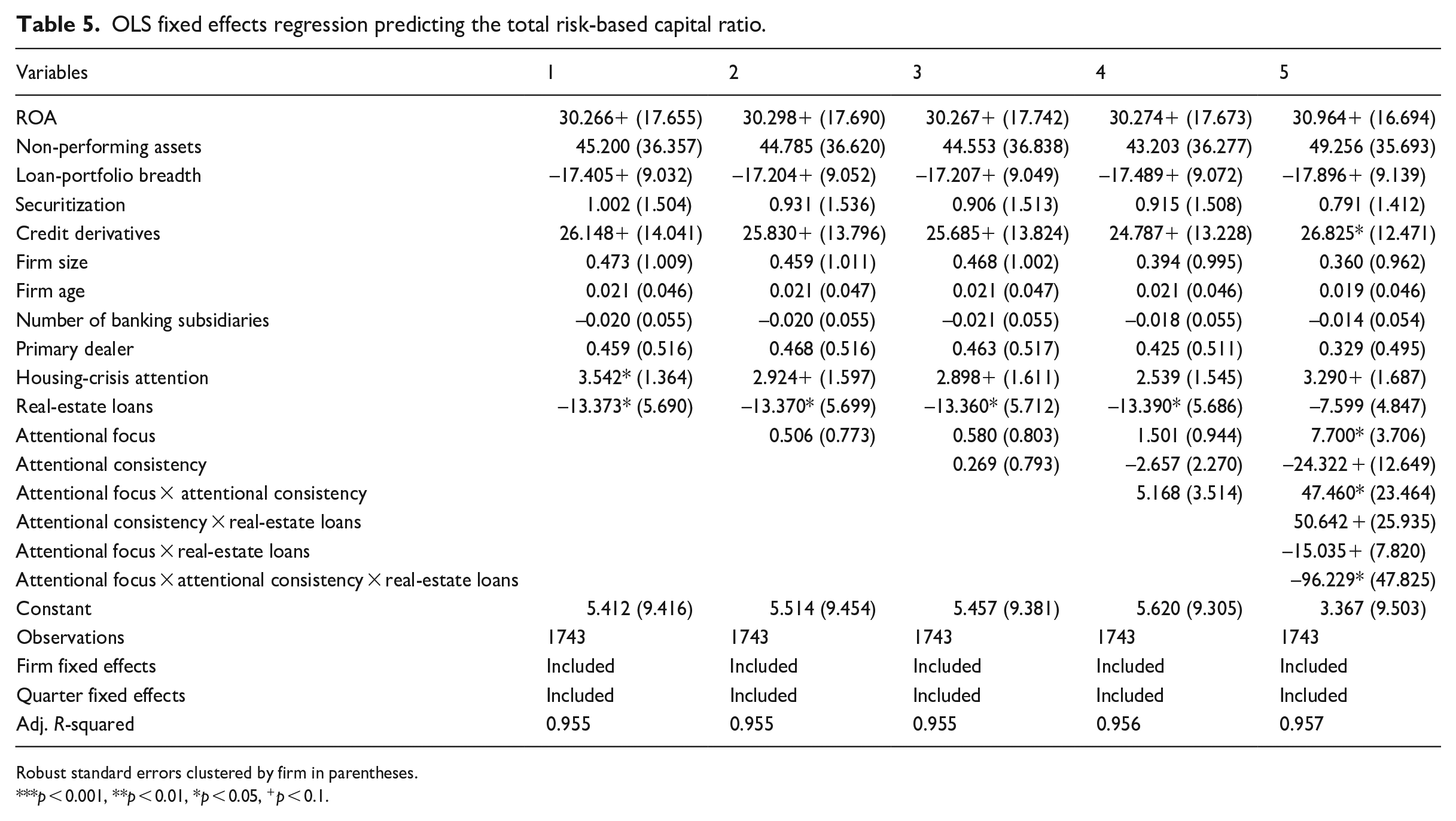

Table 5 presents the results of the test of Hypothesis 3, which examines the effect of attentional engagement on the total risk-based capital ratio as the dependent variable. Model 1 of Table 5 includes only the control variables. Models 2 and 3 include the stepwise additions of the attentional focus and attentional consistency variables. Model 4 includes the interaction between attentional focus and attentional consistency. Model 5 includes the three-way interaction among attentional focus, attentional consistency, and real-estate loans. The coefficient for the three-way interaction is negative and significant (Model 5, β = –96.23, p < 0.05), indicating that firms with greater attentional consistency and lower attentional focus adopt a status quo-hedging response to the discontinuous change by increasing their total risk-based capital ratio. We thus find support for Hypothesis 3.

OLS fixed effects regression predicting the total risk-based capital ratio.

Robust standard errors clustered by firm in parentheses.

p < 0.001, **p < 0.01, *p < 0.05, +p < 0.1.

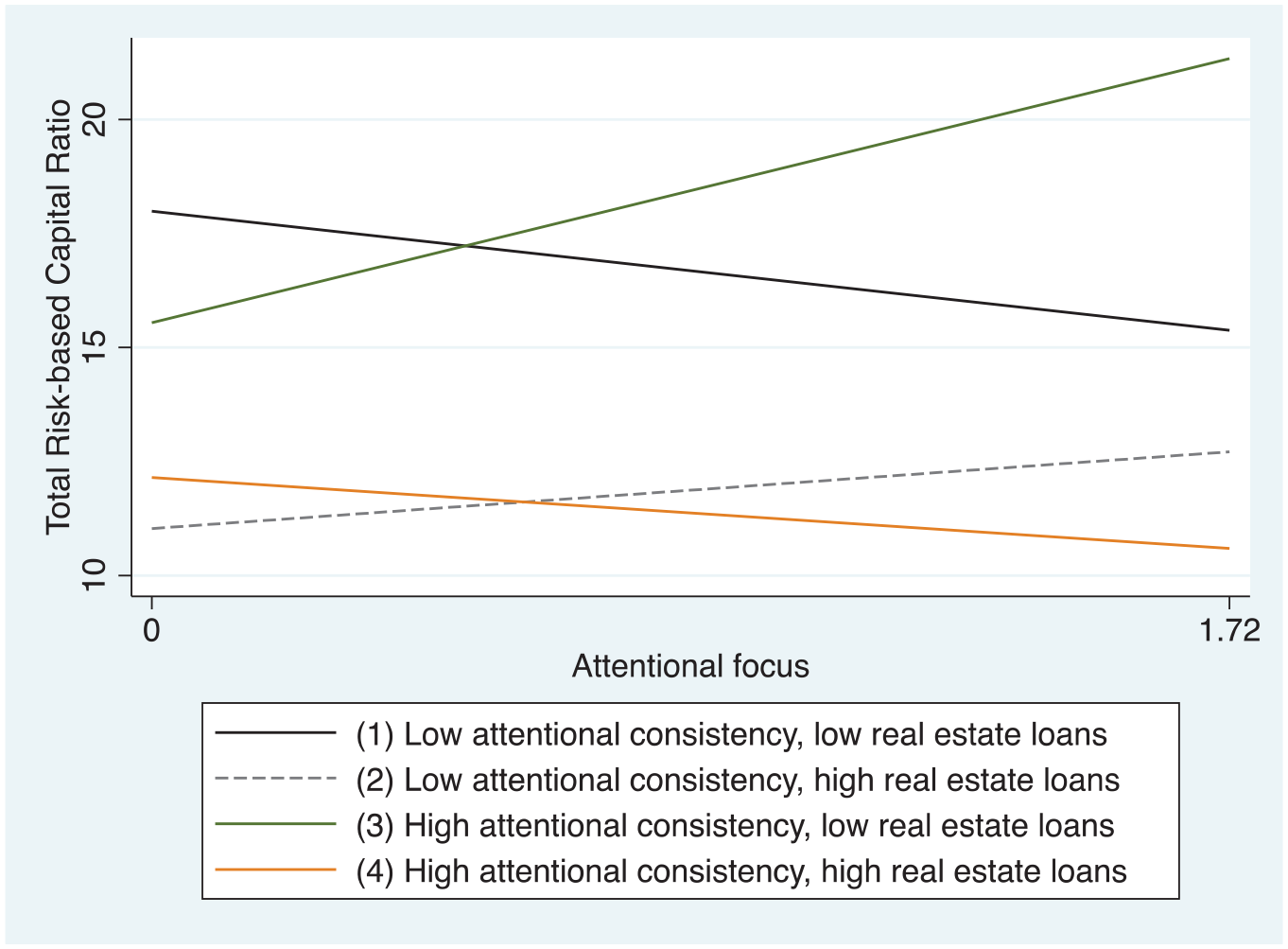

Figure 5 depicts the three-way interactions. We plotted the slope of attentional focus across its entire range of values, while varying the ranges of attentional consistency and real-estate loans to one standard deviation below and above their means. Figure 5 shows that when a firm’s exposure to the real-estate market increases from low to high, the slopes for firms with high attentional consistency becomes increasingly negative (i.e. Slopes 3 and 4; slope difference: t = 1.8, p = 0.075). Thus, these findings support the prediction that firms with attentional engagement that is high on attentional consistency but low on attentional focus are more likely to engage in status quo-hedging responses to external discontinuities. In terms of economic significance, a one standard deviation increase in attentional consistency and a one standard deviation increase in the firm’s exposure to real-estate loans weakens the average effect of attentional focus on the total risk-based capital ratio by −0.64 (–96.23 × 0.18 × 0.10 × 0.37). For firms with an average total risk-based capital ratio of 14.05, this represents a decrease of about 4.56% (–0.64/14.05 × 100).

Effect of three-way interaction: attentional focus × attentional consistency × real-estate loans on the total risk-based capital ratio.

Robustness checks

We performed several robustness checks using alternative operationalizations of our attentional-engagement measures and controls for possible omitted attention measures.

Number of prior quarters used to derive attentional engagement

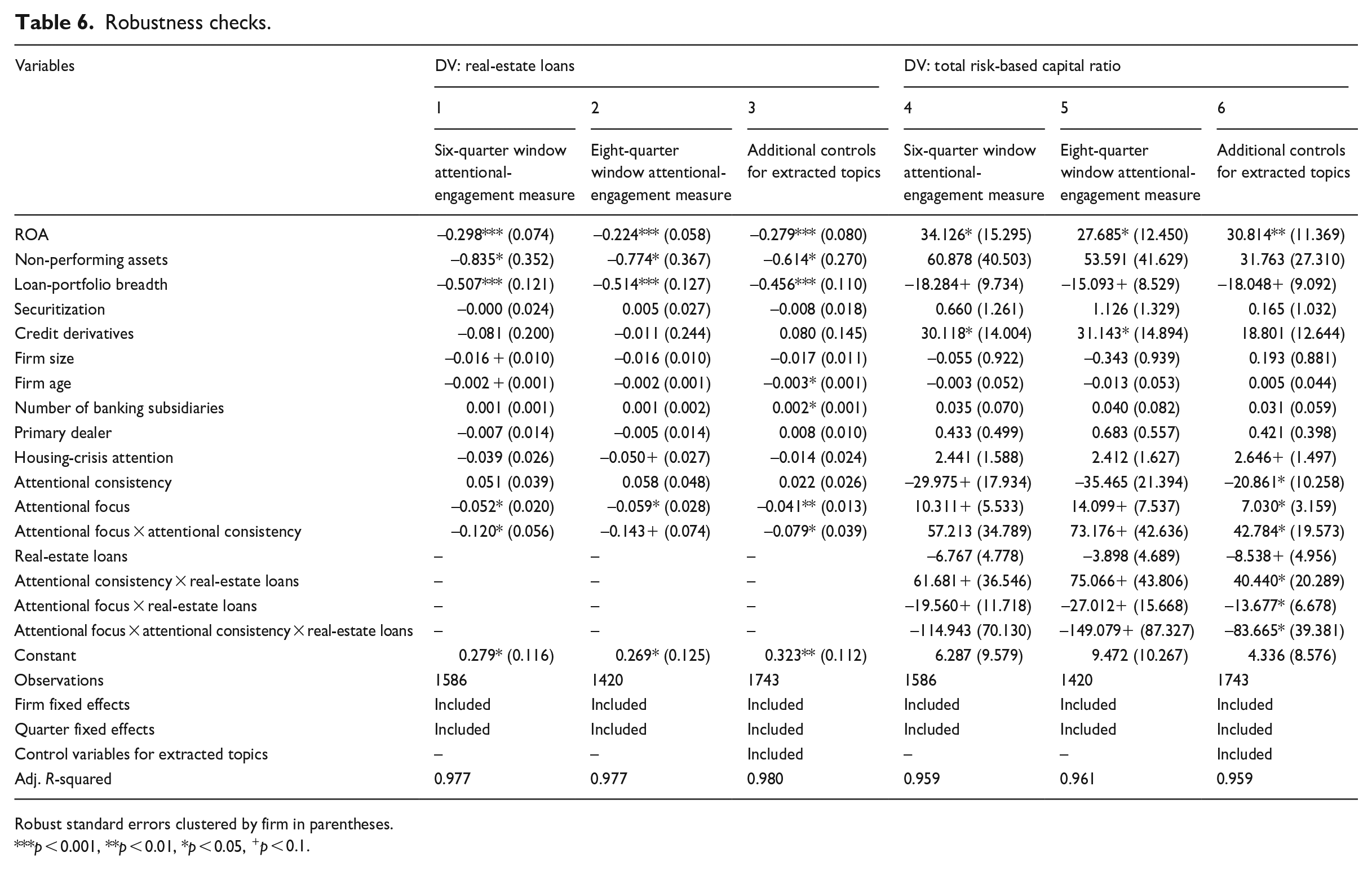

In deriving the attentional focus and attentional consistency measures, we used each firms’ attention to the housing market in the previous four quarters. To check whether our results are affected by the number of quarters used to calculate the attention measures, we derived alternative measures of attentional focus and consistency that accounted for the previous six or eight quarters. In Table 6, we present the results of the analyses using these alternative measures. In Models 1 and 2, we used these alternative measures to predict real-estate loans, while Models 4 and 5 use these alternative measures to predict the total risk-based capital ratio. Overall, we find that the patterns of results using these alternative measures of attentional engagement are similar to those from our main analyses in Tables 3 and 4, although the significance of the coefficients is weaker due to the reduced statistical power of the smaller sample size.

Robustness checks.

Robust standard errors clustered by firm in parentheses.

p < 0.001, **p < 0.01, *p < 0.05, +p < 0.1.

Controlling for alternative attention using topic modeling

As our study focuses on the attention that bank executives paid to the US housing market, one possible concern is that our results may be affected by how attention was allocated to other issues. Given the multitude of possible issues to which banks can pay attention and the difficult of specifying those issues ex ante, we used a topic-modeling approach. In line with prior work on text analysis, we treated each quarterly conference-call transcript for each bank in each quarter as a bag of words, and represented each transcript as a vector of word counts that identified how many times particular words were used in each quarter by each bank. Using the topic-modeling module in WordStat 6, we derived distinct topics across the corpus of transcripts by observing words that tended to co-occur frequently within each transcript. We then derived a dictionary of words pertaining to each extracted topic, which we used to track the extent to which banks allocated attention to each of those topics every quarter (see Appendix 2 for more details). We included the count of words for each extracted topic as an additional vector of control variables in Models 3 and 6 in Table 6. Despite the inclusion of these additional controls for managerial attention allocated to other issues, the pattern of results remains unchanged from our main analyses.

Discussion

Scholars have long been interested in how managerial cognition shapes a firm’s ability to respond to environmental change (Eggers and Kaplan, 2013; Ocasio, 2011). A key finding in this stream of literature is that the allocation of more attention to the external environment facilitates the firm’s adaptation to discontinuous change and, thus, the maintenance of fit with the environment (e.g. Cho and Hambrick, 2006; Eggers and Kaplan, 2009; Nadkarni and Barr, 2008). However, previous studies show considerable variance in the outcomes of attention allocation. Notably, these studies suggest that some organizations are unable to adapt adequately even though they devote attention to the external environment. Building on work on attentional engagement (Ocasio, 2011; Shepherd et al., 2017), we contend that the extant empirical work tends to examine the focus of attention rather than the cognitive processes that determine how such attention enables adaptive behaviors in organizations (Ocasio, 2011). These complex attentional processes are important, as they affect how managers make sense of and formulate responses to discontinuous changes in the external environment.

We sought to offer a more robust explanation of the relationship between attention and a firm’s response to the external environment by examining how attentional engagement with issues in the external environment facilitates the firm’s noticing and sensemaking of changes in those issues. Specifically, we theorized that attentional-engagement structures are varied in terms of their attentional focus and attentional consistency, and that the types of learning and cognitive processes are situated in different forms of attentional engagement. In doing so, we advance a situated perspective of how attentional engagement with issues emerging in the external environment affect the firm’s strategic responses to discontinuous changes.

Our study contributes to the literature on managerial attention and strategic adaptation in several ways. First, while the extant literature has considered how managerial attention influences strategic adaptation in terms of its directionality (Eggers and Kaplan, 2009; Kaplan, 2008; Nadkarni and Chen, 2014; Yadav et al., 2007) or its intentionality (Bouquet and Birkinshaw, 2008; Cho and Hambrick, 2006; Engelen et al., 2012), this study has examined the process aspect by disambiguating various cognitive processes and their relations to the firm’s adaptations to external change. Specifically, we demonstrate that attentional engagement is a complementary combination of both attentional focus and attentional consistency over time. In doing so, we are able to develop a more nuanced understanding of the association between attention-allocation patterns and firms’ heterogeneous strategic responses to discontinuous change, which would have otherwise been challenging to establish if attentional focus and attentional consistency were to be examined separately. In this regard, our theory of attentional engagement with external discontinuous change highlights the importance of how attention is allocated and not just where it is allocated. Moreover, we develop a situated perspective (Haynie et al., 2010; Zahra and Wright, 2011) of attentional engagement by articulating how different learning (e.g. selective or noisy) and cognitive processes (e.g. deliberative reasoning, certainty, and uncertainty perceptions) are involved in different forms of attentional engagement. These underlying situated mechanisms of learning and cognition describe how the type of attention allocated to novel information by organizations affects how those organizations integrate that knowledge and produce differentiated responses (Kiesler and Sproull, 1982).

Our framework also contributes to the extant literature on attentional engagement by articulating the nature and consequences of the underlying trade-offs of attentional engagement. For instance, Levinthal and Rerup (2006) and Joseph and Wilson (2017) suggest that sustained attention on a particular stimulus may involve trade-offs because other issues may be ignored. This suggests a trade-off between simultaneously allocating attention to multiple issues with a lower focus and allocating attention to a few issues with a greater focus. Our study builds on this research by articulating the downstream consequences of these inherent trade-offs. Managers who allocate greater attentional magnitude with less consistency are more likely to be subjected to the costs of selective learning, while managers who allocate lower attentional magnitude but with more consistency face the costs of noisy learning. These different modes of learning lead to different forms of cognitive processes (e.g. uncertainty or overconfidence perceptions) that shape subsequent behavioral responses.