Abstract

Integrated reporting has widely been promoted as the next evolutionary step in corporate disclosure, which would soon replace traditional reporting practices. Embedded in a zeitgeist that favors sustainability, this outlook would suggest high integrated reporting adoption rates among reporting organizations. Our analysis of integrated reporting in Germany from 2008 to 2019 shows, however, that organizations approached integrated reporting with a wait-and-see mentality. This approach cannot be described adequately by the existing conceptualizations of (partial) practice adoption. We therefore develop the notion of wait-and-see-ism, defined as the deliberate and potentially long-lasting postponement of a decision to adopt a practice while its further development is monitored silently. We see limited, though continuous, efforts to prepare for the prospect of adopting the practice of integrated reporting quickly at a later stage. Wait-and-see-ism expands on prior work on partial adoption by emphasizing its temporal dimension. This adds an important yet undertheorized option that organizations can employ to respond to ambiguous institutional demands, thus explaining the stalling of promising management practices.

Keywords

Introduction

In line with the current sustainability zeitgeist, it has become a common practice for companies to publish sustainability reports alongside traditional financial reports (KPMG, 2020). However, such a two-report system splits financial and non-financial information into silos. To address the limitations of such isolated perspectives, the practice of integrated reporting (IR) has been introduced. IR emphasizes the interconnectedness of financial and non-financial information and merges them in a single integrated report. IR has been praised as the next evolutionary step in corporate reporting, gained considerable support from practitioners and academics, and has seen promising uptake as several influential companies became early adopters (EY, 2014; IIRC, 2011; Villiers et al., 2014).

The literature suggests that such conditions, along with the pressure organizations face from stakeholders to display their sustainability efforts, lead to large-scale adoption of a novel practice such as IR (e.g. Ansari et al., 2010; DiMaggio and Powell, 1983; Oliver, 1991). This can come in the form of a substantive practice adoption implying that organizations truly implement it into their strategy and core business processes (Jacqueminet, 2020; Jacqueminet and Durand, 2020). Alternatively, organizations may also adopt a practice symbolically if, for instance, the expected benefits remain unclear (Durand et al., 2019; Misangyi, 2016).

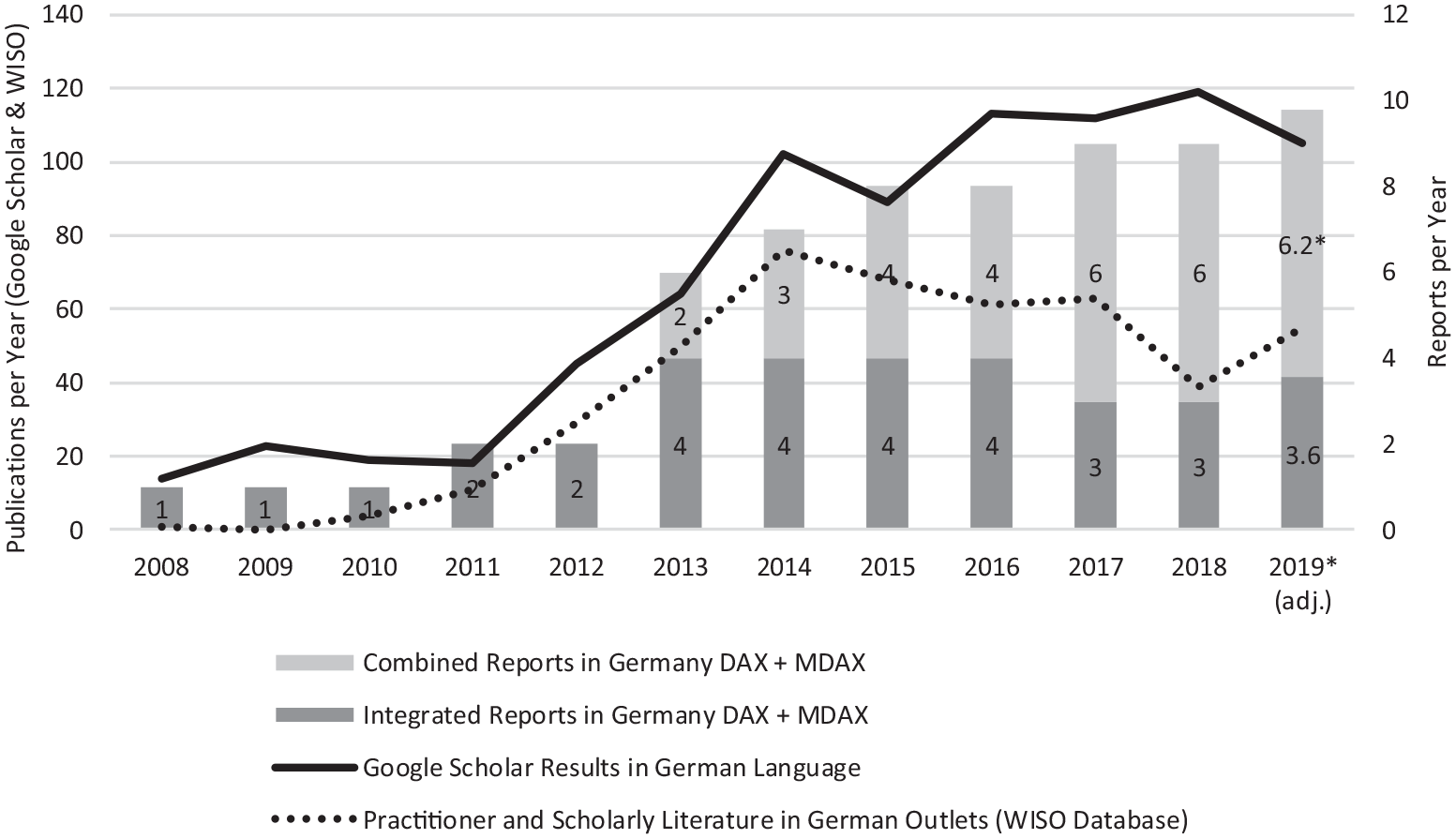

However, the case of IR points to an unresolved empirical puzzle: On one hand, IR continues to be on the agendas of businesses and industry associations as evidenced by various surveys (e.g. KPMG, 2020). On the other hand, this practice has neither achieved large-scale substantive adoption nor are there indications of widespread symbolic adoption of IR (see Figure 1). Both forms of adoption would result in a large number of integrated reports being published either in form of comprehensive reports or in form of broadly touted public commitments to IR that, however, lack evidence of actual implementation. Instead, despite its promising initial adoption rates, the further uptake of IR, in terms of the number of new adopters, has been stalling over an extended period of time (see the Corporate Register Database 1 ). Motivated by this empirical puzzle, our research question asks: why does the adoption of IR stall?

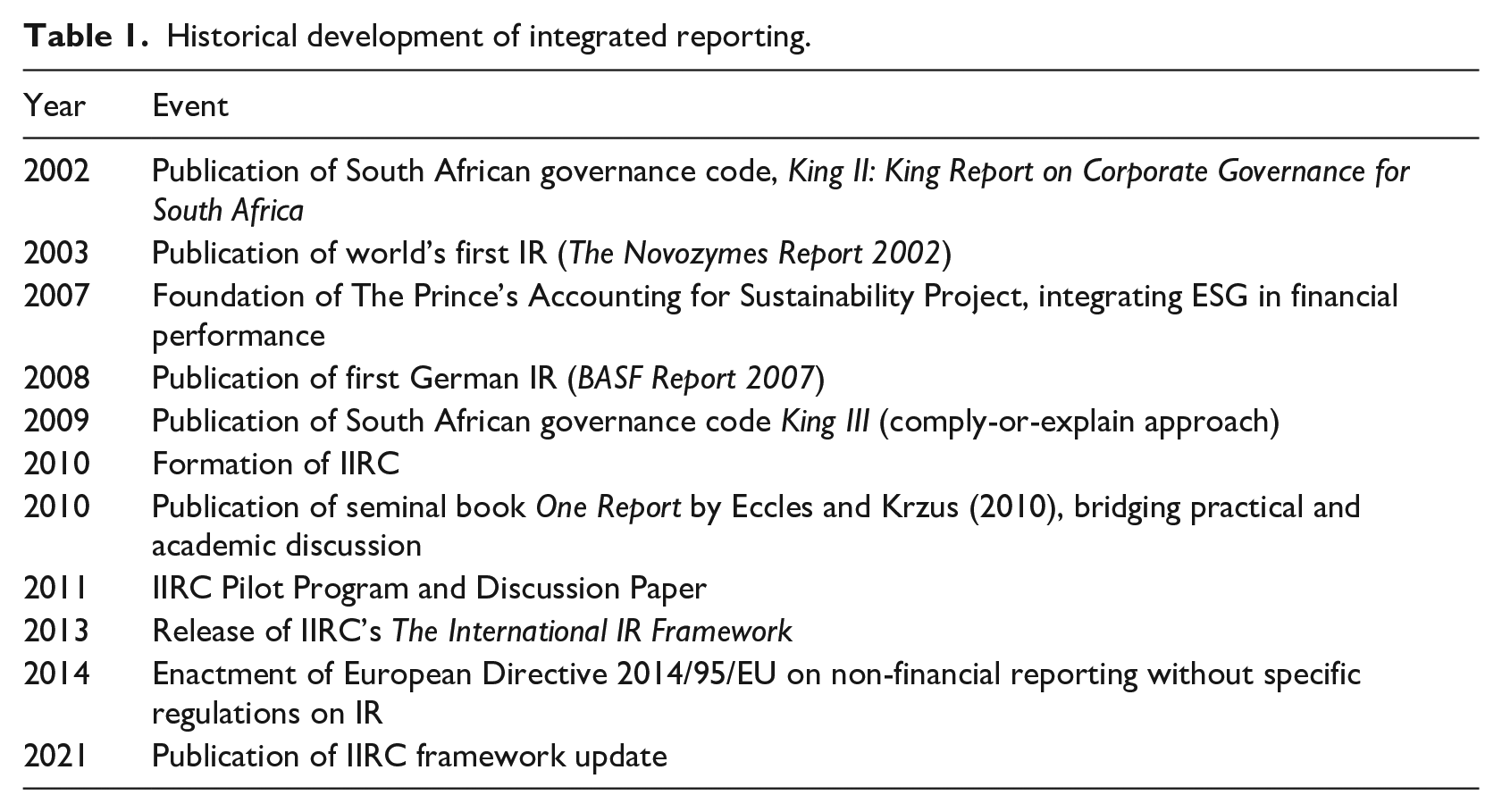

Development of practical and academic discussion of IR.a

We mobilize the practice adoption literature to answer our research question (e.g. Durand et al., 2019; Haack et al., 2020; Kim, 2020; Simon and Lieberman, 2010). This literature examines a central concern in organization theory, namely how and why organizations adopt new practices, defined as the “symbolic and material activities that reflect changes in management work [. . .] and that involve a departure from traditional processes, practices, structures and techniques” (Ansari et al., 2014: 1315). Drawing on this literature is conceptually useful to examine the relationship between how organizations adopt a certain practice and why this may lead to this practice’s stalling at the field level, because “organizations frequently imitate other organizations in order to appear legitimate [and] the adoption of practices is therefore often driven by a desire to appear in conformance with norms” (Ansari et al., 2010: 70). Therefore, as Jonsson (2009) has argued, “to develop predictions about limited diffusion it is necessary to (first) understand how and when initial resistance to adoption remains over time.” (p. 172)

Based on this intertwinement between field- and organizational-level dynamics of practice adoption the distinction between substantive and symbolic adoption continues to inform research (e.g. Durand et al., 2019; Haack et al., 2020). However, some studies have criticized it for being too simplistic and have identified more nuanced organizational responses to institutional demands that are different from the common alternatives of substantive and symbolic adoption. Such responses imply partial engagement with a given practice, typically in contexts of more ambivalent institutional demands (e.g. Crilly et al., 2012; Oliver, 1991; Pache and Santos, 2010; Slager and Gond, 2020). This literature shows that adoption can vary in its extensiveness (e.g. Ansari et al., 2010; Gondo and Amis, 2013; Oliver, 1991). Nevertheless, the empirical puzzle of IR still points to an important yet undertheorized problem in research on the partial adoption of practices in cases which reflect neither symbolic nor substantive adoption: the literature has yet to explain organizational responses to new management practices whose adoption rates stall over extended periods of time, even though these practices seem to correspond to the current zeitgeist (here of sustainability), have influential proponents and show promising initial adoption rates.

We address these limitations through a longitudinal qualitative analysis of IR in Germany from 2008 to 2019. We show that inconsistent stakeholder demands, ambiguous perceptions of costs and benefits, and uncertain future regulatory requirements conjointly result in what we call “wait-and-see-ism.” Wait-and-see-ism, we argue, is a temporally stretched organizational response that provides a novel theoretical explanation for the stalling of management practices over time. It adds an important type of partial practice adoption to the literature.

Our research makes several contributions to the practice adoption literature. We conceptualize wait-and-see-ism as a distinct form of partial adoption that allows organizations to avoid admitting to nonadoption (inaction). Furthermore, wait-and-see-ism circumvents the need for the substantive adoption of a costly but potentially inefficient or ineffective practice, and it forestalls accusations of window-dressing that are common in cases of symbolic adoption (Weaver et al., 1999). In contrast to inaction (Durand et al., 2019), wait-and-see-ism adds a temporal dimension to current forms of partial adoption because it connotes the deliberate and potentially long-lasting postponement of a decision to adopt a practice while its further development is monitored silently. Limited, though continuous, efforts are made to prepare for the prospect of rapid adoption at a later stage. Beyond conceptualizing wait-and-see-ism and delineating it from related organizational responses to institutional demands, the contributions of our study lie in identifying the antecedents of wait-and-see-ism and in outlining avenues for future research on this form of partial adoption.

Organizational responses and partial practice adoption

Departing from Oliver’s (1991) seminal work on the conditions under which passive conformity to institutional pressures is not a sufficient explanation for various types of organizational response, a rich stream of research has elaborated on nonadoption, symbolic adoption, and substantive adoption as the three basic organizational responses to institutional pressures (e.g. Durand et al., 2019; Haack et al., 2020). In the context of our research, studies that have moved beyond the “simple” but prevailing dichotomy between substantive and symbolic adoption are especially relevant as they examine more nuanced forms of partial engagement with a practice. Durand et al. (2019), for example, specify the concept of nonadoption—termed “inaction” in their study—by challenging Oliver’s (1991) model for its neglect of an organization’s “willingness and ability” to engage in specific responses. As a result, they consider inaction as a possible response to institutional pressures. Inaction differs from substantive and symbolic adoption since the organizations that embrace it do not address an issue at all. According to Durand et al. (2019), organizations decide how to respond based on the salience of the issue under consideration and the costs and benefits of taking or forgoing (any) action. Their model thus extended prior literature, which had largely been silent on organizational resource constraints. The prediction of the model by Durand et al. (2019) is that inaction will only occur when salience is very low or very high. When the salience of an issue is moderate, organizations will react with symbolic or substantive actions. Thus, inaction, as conceptualized by Durand et al. (2019), is a form of nonadoption based on the premise of cost-benefit deliberations in instances when pressure to conform is clearly articulated.

Other studies, such as Slager et al. (2021) specify how organizational responses are shaped by motivation and capacity. Specifically, they show that responses toward sustainability metrics can be explained through the organization’s motivation for responding but also through its capacity to respond. When both motivation and capacity are low, organizations respond “indifferent” and display “nonreactivity” as forms of nonadoption. Motivation (or the lack thereof) can be a result of pressure to conform, while capacity is often the result of cost-benefit deliberations. Likewise, Pache and Santos (2010) argue that if institutional environments impose conflicting pressures on organizations, “organizational paralysis” or “breakup” may result. While organizational paralysis, like inaction, has nonadoption as its outcome, it is not deliberate and may entail adverse consequences, such as long-term strikes (Pache and Santos, 2010).

Using the concept of selective coupling, Pache and Santos (2013) show how organizations respond to conflicting institutional logics by enacting elements of both logics (identified by Slager et al. (2021) as selective reactivity). Compared with symbolic conformity, that is, the ceremonial espousal of practices without actual implementation, selective coupling allows organizations to avoid accusations of fake compliance (Pache and Santos, 2013). Similarly, Crilly et al. (2012) discuss alternative organizational responses to institutional demands. Their multilevel framework highlights the importance of internal organizational factors and the external environment as antecedents of different forms of decoupling (i.e. symbolic adoption). The authors enrich our understanding of symbolic adoption and show that it need not result from managerial intent but instead can reflect organizational learning efforts that are fraught with complexity as well as inconsistent and dynamic stakeholder pressures. In contrast to intentional decoupling, where an organization purposefully avoids practice implementation or deceives stakeholders, unintentional “muddling through” (Crilly et al., 2012: 1443) results from oftentimes uncoordinated local behaviors inside an organization that contradict official policy.

Recently, some studies have begun to refine the distinction between nonadoption, symbolic adoption, and substantive adoption by elaborating on the temporal character of adoption decisions. Adoption of a practice is thus neither substantive or symbolic (or not happening at all), but may be a sequence of decisions that include both symbolic and substantive forms of adoption. Haack et al. (2020), for instance, theorize different organizational responses to institutional pressures for transparency (or the lack thereof, which they conceptualize as opacity) that may change over time. Assuming that both substantive adoption and the subsequent abandonment of a practice are difficult to achieve, Haack et al. (2020) suggest that higher rates of substantive adoption are achieved if organizations adopt a practice symbolically at first and then gradually transition toward more substantive responses. In this way, the cost of substantive adoption is postponed. Focusing on internal organizational dynamics that influence practice adoption, Gondo and Amis (2013) show that adopters have some degree of agency in their responses to field-level adoption pressures. Implementation might be delayed if actors fail to provide meaningful descriptions of “how a practice ought to work locally” (Gondo and Amis, 2013: 239). Thus, it is crucial to acknowledge that organizational characteristics, internal processes, and levels of acceptance matter when moving from the initial adoption of a practice toward its subsequent implementation.

Overall, research has moved beyond Oliver’s (1991) classic model of strategic responses to institutional demands and offers important insights into different forms of nonadoption, symbolic adoption, and substantive adoption. However, this literature still has some important limitations. On one hand, most studies that specify responses other than symbolic and substantive adoption implicitly assume that if a practice is not adopted substantively, the alternatives include symbolic actions such as selective coupling (Pache and Santos, 2013) or muddling through (Crilly et al., 2012). On the other hand, nonadoption is typically a response to clearly articulated institutional demands, taking the form of inaction (Durand et al., 2019), nonreactivity (Slager et al., 2021), or organizational paralysis (Pache and Santos, 2010). Thus, the literature has yet to explain organizational responses that are (a) the outcome of topical (i.e. reflective of current zeitgeist) but ambiguous (i.e. neither conforming nor clashing and possibly not even clearly articulated) institutional demands and that (b) do not include symbolic actions as alternatives to nonadoption and substantive adoption.

In addressing these limitations, we respond to recent calls to investigate incomplete practice adoption (e.g. Haack et al., 2020; Naumovska et al., 2021). Naumovska et al. (2021), for instance, call for further research on incomplete adoption because the binary distinction between complete (symbolic or substantive) adoption and nonadoption “is a simplifying assumption that hides theoretically interesting outcomes” (Naumovska et al., 2021: 32). Specifically, they argue that “because partial adoption and modification have been neglected for so long, delineating the mechanisms that affect these [. . .] outcomes is a promising area for future research” (Naumovska et al., 2021: 33). Contrary to the established categorizations, the case of IR suggests an alternative to nonadoption, symbolic adoption, and substantive adoption.

Empirical background and methodology

IR and its historical development

IR is a management and reporting practice that promotes the integration of the financial and non-financial components of corporate reporting into a single integrated report (e.g. Argento et al., 2019; IIRC, 2013; Villiers et al., 2014). The King Report on Corporate Governance for South Africa (Institute of Directors in Southern Africa, 2002) was instrumental in popularizing IR (see the historical overview in Table 1) because it provided initial recommendations for reporting companies. As a result of its publication, companies listed on the Johannesburg Stock Exchange have been required to publish an integrated report or to explain deviations since 2010 (Institute of Directors in Southern Africa, 2009). This comply-or-explain regulation precipitated the establishment of the International Integrated Reporting Council (IIRC) in the same year (Eccles and Saltzman, 2011). The IIRC is an international coalition of companies, standard setters, accounting firms, academics, and nongovernmental organizations (NGOs) that is tasked with promoting IR as a tool for improving reporting practices (IIRC, 2013). The foundation of the IIRC popularized IR (Villiers et al., 2014) worldwide. The proponents of IR praised it as the next evolutionary step in corporate reporting (see, e.g. EY, 2014; IIRC, 2011). In December 2013, IR published the International IR Framework (IIRC, 2013), which was updated in 2021 (IIRC, 2021) and which provides guidelines to potential IR adopters.

Historical development of integrated reporting.

The IIRC argues that IR provides a more holistic view of a company and its performance than the conventional practice of adding nonfinancial information to financial reports. IR entails engagement with the interdependencies between the two. The IIRC defines IR as “process founded on integrated thinking that results in a periodic integrated report by an organization about value creation, preservation or erosion over time and related communications regarding aspects of value creation, preservation or erosion” (IIRC, 2021: 53). Thus, IR emphasizes the connectivity between economic, social, and environmental value creation.

The final step of IR, which is visible and thus a manifestation of its formal and substantive adoption, is the publication of an integrated report (Busco et al., 2019). However, few companies publish an integrated report. Most firms are reluctant to commit to the new practice formally (see Corporate Register Database on https://www.corporateregister.com/frameworks/iirc/). This stalling of the adoption of IR is also observable in Germany, which serves as the setting of our research.

Empirical context: IR in Germany

In Germany, there is a rich discourse on IR among academics, practitioners, and regulators. In line with global trends, the adoption of IR in Germany accelerated significantly in 2008 (see Figure 1). In 2008, German chemicals giant BASF became one of the first large international companies to issue an integrated report for the 2007 fiscal year. Its publication sparked a heated debate between the proponents and opponents of IR; stakeholders such as accounting firms, consultants, and the media picked up the topic. The number of published integrated and combined 2 reports by German companies and the academic and practitioner-oriented literature on IR (see Figure 1) suggest that, after a slow start, IR gained significant traction. However, it has not been able to sustain its initial momentum. The number of published reports has been stalling, a trend that endured until the end of our research in 2019.

Data collection

Our data collection was embedded in a broader field immersion strategy (see Palermo et al., 2017). We began effectuating it in 2015, when we visited, organized, and participated in various conferences, symposia, and roundtables on IR, both collectively and individually. Contact with key actors in IR in Germany helped to build our understanding of the research context and allowed us to identify relevant interview partners.

To collect primary data, we conducted 32 interviews with 37 3 informants between 2016 and 2018. We interviewed representatives from pioneer companies that published integrated reports (interview identifier: “IR,” e.g. #2-IR) and from companies that did not (“NonIR”). In addition, we interviewed representatives from IR lobby groups (“Lobby”), auditing firms (“Audit”), consultancies (“Consult”), and academia (“Acad”) as well as investors (“Invest”; see Appendix 1). This sampling strategy contributed to a holistic understanding of the development and state of IR and captured its demand- and supply-side dynamics.

We conducted interviews in person, via telephone or by videocalls. Whenever it was possible, two of the researchers involved in the project conducted the interviews jointly. 4 This allowed us to distribute tasks during the interviews (e.g. asking questions, taking notes, and overseeing the interview process), to ask ad hoc questions, and to develop on-site interpretations. The interviews were supported by a semistructured interview guideline (see Appendix 2). They were recorded and then transcribed in full. Transcripts were sent to the interviewees for approval. The interview questions focused on respondents’ perceptions of IR, its strengths and weaknesses, its drivers and barriers, their approaches to the (potential) adoption of IR, and their evaluations of IR’s future. Discussing both past developments and the prospects of IR allowed us to expand the temporal range of our analysis. Overall, the data allowed us to construct a comprehensive case narrative (Yin, 2018) of IR in Germany.

To enable empirical triangulation, we added secondary data for the period between 2008, when the first German integrated report was published, and 2019, when our research concluded. Specifically, we included practitioners’ reports about IR, which had been published mostly by auditing and consulting firms in Germany that had been active participants in the field (data identifiers PR1–PR10). These publications contain normative guidance (Palermo et al., 2017) that has the potential to shape the reporting practices of companies, as well as descriptive overviews and comments for practitioners. Appendix 1 summarizes the primary and secondary data sources and provides information about our contacts.

Data analysis

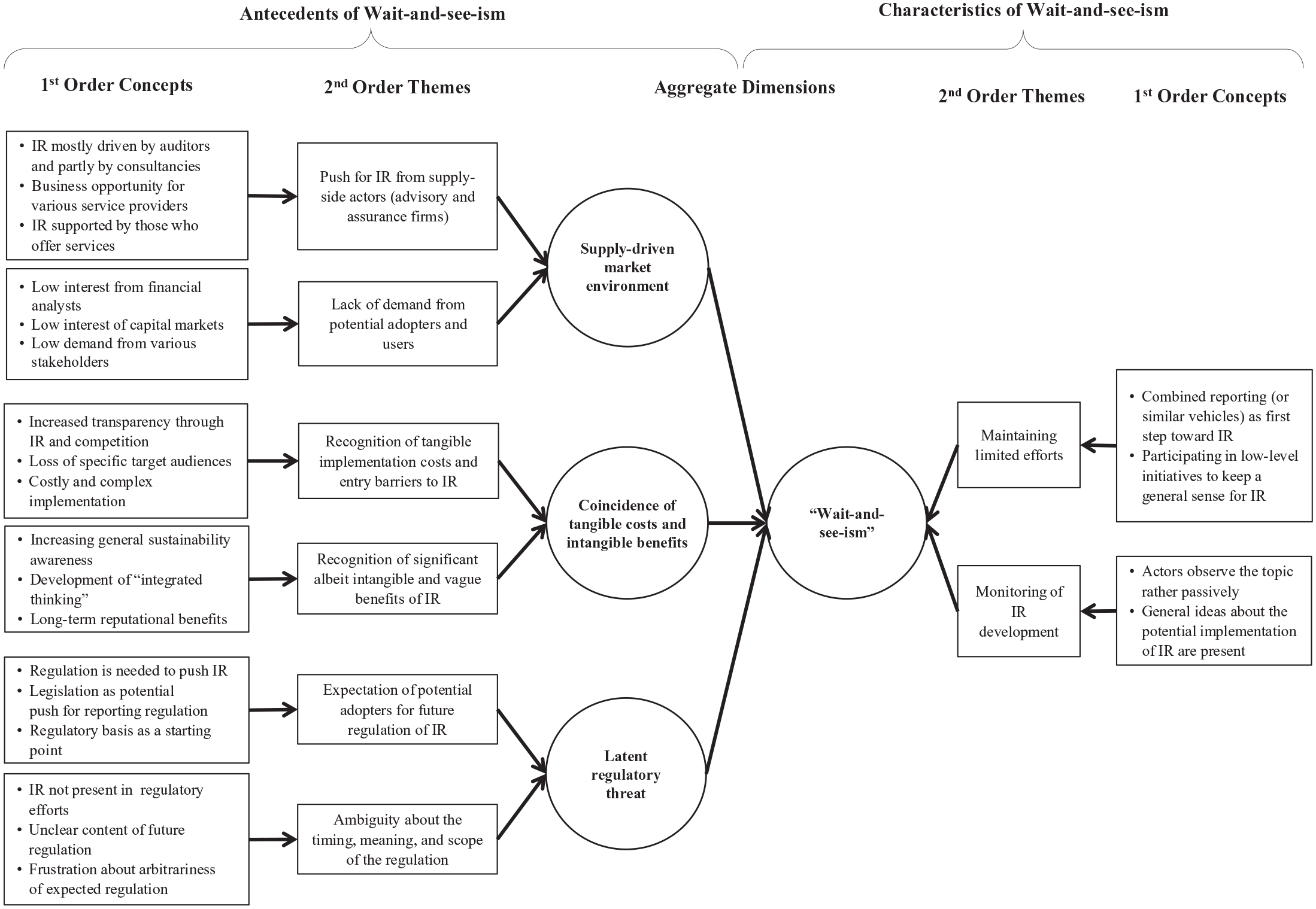

We coded the data in several consecutive steps, and we followed an inductive approach to analyze it (e.g. Corbin and Strauss, 2015; Gioia et al., 2013). In the first-order analysis, we focused on our primary data from the interviews. We processed the raw data to identify an initial set of open codes, and we classified the descriptions of those codes into different groups of first-order concepts. The result of this analysis was our initial insight that there was a considerable degree of uncertainty about the benefits and pitfalls of IR and that the key actors in the field seemed to have put IR on hold. Using informant-centric data terms, we categorized our first-order analysis into two sets of descriptors that mirrored these insights. One describes the broader market environment of IR (see the left side of the data structure in Figure 2), and the other set describes how the organizations that are involved, including potential adopters as well as other stakeholders, responded to IR (see the right side of the data structure in Figure 2). Joint discussions of the results of this coding yielded our first common understanding of the empirical material.

Data structure.

We also consulted our secondary sources to substantiate our assessment of the interview data about potential adopters’ approach to the practice and their perceptions of the concomitant benefits and pitfalls, which create a shared sense of ambiguity about IR (see Appendix 1). For instance, we analyzed the adoption rates of IR among German companies, as shown in Figure 1, and read reports by companies as well as other stakeholders, such as auditing firms. The goal of these activities was to obtain a firmer grasp of the portrayal of the benefits and pitfalls of IR and of the argumentation that companies provide in formal statements about its adoption or nonadoption.

Based on these insights, we commenced the second-order analysis. To move from descriptive insights toward more theoretical explanations, we grouped the first-order codes into four pairs of second-order categories that represent a higher level of abstraction. Each of the first three pairs illustrates a factor that complicates the adoption of IR (see the data structure in Figure 2 and Appendices 3–6). The last pair illustrates the common organizational response to IR and thus includes the components from which we later derive the notion of wait-and-see-ism.

We then consolidated the second-order categories into four aggregate dimensions. The three aggregate dimensions, namely “supply-driven market environment,” “coincidence of tangible costs and intangible benefits,” and “latent regulatory threat,” represent antecedents as perceived by potential adopters and other involved stakeholders. They help explain the prevalence of wait-and-see-ism as a response to IR, which contributes to its stalling. The aggregate dimension “wait-and-see-ism,” in turn, describes the components of this type of organizational response to ambiguous institutional demands and presents an important but hitherto underconceptualized type of partial practice adoption.

In all of the steps, we established tabular displays to structure and analyze our data (see the additional illustrative quotes in the data tables in Appendices 3–6). The triangulation of our interview data with the other secondary data (Appendix 1) further validated the second-order categories and their correspondence to the four aggregate dimensions. Therefore, our analysis had reached “category saturation,” and it was unnecessary to collect further data (Strauss and Corbin, 1998).

Findings

A supply-driven market environment elicited the initial uptake of IR in Germany

After the formation of the IIRC in 2010, auditing and consulting firms emerged as key drivers of IR in Germany. They were particularly influential in this initial phase of IR proliferation. Many interviewees mentioned that the so-called Big Four

5

auditing firms pushed the IR debate because they supplied the market with the necessary expertise. The Big Four actively positioned themselves as opinion leaders by organizing conferences, “publishing professional articles, participating in working groups” (#1-Audit), and advising clients. Many interviewees shared that auditing and consulting firms, as well as communication agencies, attempted to promote IR to sell related consulting and assurance services. One informant indicated that it

is not surprising, that the big audit firms, as well as companies such as [leading global consultancy firm], sell IR packages: “We show you how it works!” (#14-Invest)

The informants who worked at auditing firms acknowledged that “for us as an audit company, this [IR] obviously also represents a business case” (#6-Audit) and that IR

is a topic also in the context of new products and new opportunities—business opportunities—to distinguish yourself from the competitors. (#7-Audit)

This finding suggests that a supply-driven market environment prevailed and was most salient during the initial uptake of IR. Auditing and consulting firms published a significant number of topical overviews, descriptive empirical studies, and commentaries to demonstrate their expertise in IR, its benefits, and its usefulness for potential adopters (see Appendix 1). Not surprisingly, these publications were enthusiastic in their tone, extolling IR as an “answer to the complexity of the world” (PR1), an “opportunity for companies’ value enhancement” (PR5), and a “revolution in corporate reporting” (PR7). We also observed the proactive attitude of the leading auditing and consulting companies and their promotion of IR at the various conferences, roundtables, and presentations in which we participated. And indeed, many informants who worked at (potential) IR adopters initially seemed to buy into the benefits touted by its supply-side promoters. IR was often considered a “nice supporting tool” (#4-IR) for strategic management that could also “trigger” (#4-IR) the reconceptualization of established strategic processes.

However, the supply of IR did not correspond to demand from potential adopters. Traditional business units, which are often found to be skeptical of new sustainability-related tasks, were not the only ones to voice concerns—even sustainability departments worried that IR had no real target group and that they

might need to bid farewell to target groups, which could be reached through traditional reporting [i.e., stand-alone sustainability reporting]. (#4-IR)

These departments were chary of complicating their outreach to traditional target groups, such as NGOs, actual and future employees, and other stakeholders who are typically concerned with sustainability. Even if these stakeholder groups occupied positions of prominence in the early days of the IIRC, the 2013 framework circled primarily on financial investors. Some informants thus perceived IR as being stuck between the two traditional reporting formats, both of which had a clearer focus on their respective target audiences.

Moreover, despite the potential influence of large professional investors in the future dissemination of IR, our interviewees regarded the interest of this stakeholder group as extremely limited. The reason for this perception was that sustainability-conscious investors were expected to find the necessary information through existing reporting channels or in ready-to-use formats on specialized databases. Relying on established reporting formats, however, further circumscribed the supposed benefits of IR that supply-side actors promoted.

The IIRC indicated that the target group is the financial community. But they neither read sustainability reports, nor annual reports, nor integrated reports. They draw on their database providers that pick up this information. (#3-Acad)

In summary, it was mainly auditing and specialized consulting companies and the IIRC as suppliers of IR expertise that pushed the initial proliferation of IR vigorously (see Appendix 3 for further illustrative quotes). Indeed, a majority of the interviewees who were working for actual and potential adopters bought—at least initially—into the positive arguments about IR that were being ventilated from the supply side of the market. These positive perceptions, however, changed significantly after the initial enthusiasm and demand for the adoption of IR waned.

Coincidence of tangible costs and intangible benefits led to fading interest in IR

The interplay of two factors seemed to contribute to the fading of interest in IR. First, the benefits of implementing IR, as emphasized by its promoters, were perceived as significant yet mostly intangible and rather vague. Second, demand-side actors increasingly realized that there were tangible drawbacks and entry barriers to adoption.

Interviewees mentioned several significant benefits of IR, above all an enhanced understanding of business processes and increased awareness of sustainability issues within the company. Such considerations were expressed by academics who dealt with IR in their research and in their engagement with practitioners:

I think that the actors that benefit most from it [IR] are the reporting companies themselves. Because they need to develop a better understanding of these processes and these interrelations [of financial, societal, and environmental issues], and they also need to try to monetize them. (#3-Acad)

However, our data also shows that potential adopters increasingly perceived the benefits of IR—especially those promoted by supply-side actors—as being significant but also vague and intangible. For example, some interviewees referred to the idea of “integrated thinking” as a crucial objective of IR that was espoused by auditing and consulting firms (e.g. #3-Acad, #5-Acad, and the published secondary data sources). Other informants, however, worried that it remained unclear how the benefits of integrated thinking would materialize into a business case. These perceptions, which were common to several stakeholder groups, sometimes even led to integrated thinking being characterized as “sloppy and not meaning anything” (#14-Invest).

Although we found very few voices that were overtly critical of the general concept of IR, the expected benefits typically remained vague at best because direct links to economic or other, more tangible benefits were mostly viewed as difficult to identify. Informants suggested that IR “may have far-reaching consequences: an increase in reputation, and, ultimately, firm value” (#20-NonIR) and that it “promises a long-term commitment of stakeholders to the company and an increased overall reputation” (PR4). What this implied for daily corporate practice, however, remained largely unknown, also because “binding specifications” for IR were lacking (PR8). The interviewees’ regular use of ambiguous language when identifying the benefits of IR, which seemed too vague to “generate an impact somewhere” (#3-Acad) and to trigger strong demand, evince this uncertainty further. Informants often seemed to engage in wishful thinking and “hope that we will benefit from it [IR] in the future” (#1-Audit).

Furthermore, the “deliberately” (#19-Acad) vague formulations of the IIRC guidelines were perceived to provide insufficient guidance for companies that intended to issue integrated reports.

The framework is quite vague and there is—also from our side—a particular uncertainty regarding what should be included [in an integrated report] and what should not. (#1-Audit) [. . .] clear guidance is very important for companies, but it is still missing. (#3-Acad)

The ambiguity of the IIRC framework was further reinforced by strong competition from existing providers of non-integrated sustainability reporting frameworks, such as the GRI (Global Reporting Initiative) or the German national framework DNK (Deutscher Nachhaltigkeitskodex (German Sustainability Code)). Informants emphasized that they preferred to stick to the established practice of separate reports as long as there was no consensus over a uniform approach:

There are definitely visible ambitions of geographically restricted or industry-specific guidelines to enlarge the field of application. And these are not integrated guidelines; I am not referring to the IIRC but to DNK, GRI, and whoever else is out there. They all center around the same topics, more or less . . . As long as there is no consolidation, I see restraints for a large leap in integrated reporting. (#20-NonIR)

Other than the benefits described in the previous subsection, the interviewees considered the barriers to implementing IR to be tangible and immediate. In contrast to the benefits described above, which were often highlighted by other stakeholders, the barriers where often identified directly by potential adopters. This hindered the establishment of IR as a standard business practice. According to our informants, these barriers only manifested after IR had been around for several years because potential adopters needed to accumulate experience or learn from early adopters. Our analysis shows how these experiences challenged the positive attitude advanced by the proponents of IR in its early phases.

Informants from potential adopters that chose not to report in an integrated manner were concerned primarily with the significant outlay of resources that was necessary to initiate IR before the eventual publication of a report:

I am not only talking about the cost for the creation of the report, which obviously also requires a new concept, etc., and thus the corresponding resources. Moreover, however, you first need to lay the groundwork in the company to have something about which you can report in an integrated way. And this requires more time . . . (#20-NonIR)

An informant from an auditing firm that worked regularly with potential adopters said that these companies feared being “stuck in these old structures, so that it would be a lengthy issue to change something” (#1-Audit). This concern was especially relevant because of “the complexity of the topic” (#7-Audit) that

requires a fundamental strategic realignment; that is, the CSR [corporate social responsibility] topic becomes part of the corporate strategy . . . Thus, this will be a massive modification. (#7-Audit)

As far the resources that are necessary for initiating IR were concerned, interviewees regularly considered it “a question of HR capacities” (#11c-Invest) and of “[IT] systems that need to be extended” (#10-NonIR). Moreover, the release of an integrated report involves the simultaneous publication of financial and nonfinancial information, which would pile pressure on the departments in charge because it would “tie up an enormous amount of time if you cannot stretch this into two separate reports” (#11c-Invest). These concerns were further corroborated by our secondary data, as demonstrated by the following report from a consulting firm:

For most companies, this [the simultaneous publication of financial and nonfinancial data] is still a significant challenge and requires establishing coordinated management and implementing the respective IT systems. (PR1)

In addition to the time and financial resource-related drawbacks of IR, interviewees also regularly mentioned a “fear of companies exposing themselves further” (#6-Audit):

Companies have no interest in transparently reporting the creation of values . . .They don’t want to divulge further information because this is the most elemental thing competitors could use as an orientation. (#13-Acad)

In sum, potential adopters continued to engage with IR in a limited way. The potentially sizable yet obscure benefits of IR were countered by several important barriers on the demand side of the market, which impeded the further uptake of IR in Germany (see Appendix 4 for further illustrative quotes). In addition, this development complicated the more substantive organizational implementation of IR. Another reason why many potential adopters were reluctant to adopt IR substantively was regulatory uncertainty.

Uncertainty and a latent regulatory threat inhibited the further uptake of IR

Interviewees emphasized the latent threat of further regulation. Even though informants expressed certainty that some regulation would be introduced in the near future, its scope and content remained highly uncertain (see Appendix 5 for further illustrative quotes). The threat was coupled with ambivalence about the importance of IR vis-à-vis other reporting formats.

I think that regulators will react to these new challenges for IR very slowly and with a huge time lag. (#10-NonIR) I don’t think that the European Commission, which has just begun to engage with the topic of sustainability reporting [rather than IR] will say: “Ok, in 1–2 years everything will change, and we will make it [IR] mandatory.” Rather, I think [. . .] it will not become regulated within the next 10 years. (#13-Acad)

However, our data suggested that only explicit regulatory emphasis on IR could push the practice forward. The lingering doubts expressed by informants and our secondary sources were a significant cause of reluctance:

Who can push IR forward? It could be the legislator who establishes an appropriate framework. But, for IR, I do not see this happening in the next five years. When you see how the CSR guideline was implemented in Germany, I do not see a legally binding IR in the next 5 years. (#20-NonIR) A legally binding basis for integrated reporting cannot be expected in the near future. (PR1)

In general, uncertainty about the roles, design, and regulatory foundations of IR was reinforced by the heterogeneity of the actors involved in the IR debate, as well as by “too many players” (#7-Audit) attempting to establish themselves as IR thought leaders. Informants generally expressed skepticism about the proliferation of IR in the near future and predicted that it would develop sidewards, a point that one of our interviewees summarized aptly.

Realistically, I would expect that [in five years] the state [of IR] will be the same as today: [. . .] a small number [of companies] doing it. Some will stop doing it, and others will start doing it and say: “Potentially it might be a good idea.” But this [the whole development of IR] is rather moving sideward. (#5-Acad)

Characterizing wait-and-see-ism

To react to these interrelated factors, potential adopters responded with what we call wait-and-see-ism, that is, monitoring the development of IR and maintaining limited but continuous efforts to prepare for the prospect of its quick adoption in the future. Companies seemed eager not to overinvest in IR and to keep their primary focus on current reporting practices because their stakeholders held those practices in higher regard. An illustrative example of this kind of low resource commitment and limited effort was the “mere combination” (#20-NonIR) of existing financial and sustainability reports into a combined report, without making a formal commitment to adopting IR.

We referred to it as combined reporting when we merged the [financial and nonfinancial] reports because I think that one can only draft an integrated report that truly earns this label if one manages the entire company accordingly. And this was not the case at that time, so we deliberately did not call it an “integrated report.” (#20-NonIR)

This “simple clapping together” (#11a-Invest) was characterized as a low-level engagement with IR. It would make potential adopters “more flexible” (#9-NonIR). However, the combination neglects the most central (but also the most challenging) facet of IR, that is, integrating and connecting financial and nonfinancial information to demonstrate the connectivity and interdependency of the two. Thus, combined reporting cannot be considered equal to IR. Still, it signals initial engagement with IR. This idea was also echoed by investors.

It is evident that some companies that first report in a combined way take a first step toward IR. (#11c-Invest)

In a similar vein, an informant explained that their firm deliberately engaged with IR so as to neither ignore it nor adopt it fully. This stance was rooted in ambiguous pressures from different stakeholders:

So, we didn’t say, “let’s ignore the topic until we have to adopt it,” but we said, “we need to get acquainted with all the new reporting and corporate communication trends and how to publish things, and we have to evaluate how far this is relevant for us and our stakeholders.” This is important, if we later need to make a solid decision to either adopt [IR] or not adopt it. (#23-NonIR)

Interviewees emphasized that it was important to “stay tuned” (#23-NonIR), to monitor regulatory developments continuously, and to avoid ceding ground to the competition. These objectives were attained, for instance, by reading newsletters or by attending IR-related events.

We held the internal discussion together with the finance department and investor relations to evaluate this [the topic of IR]. And we engaged externally, for example at [a German business economics society] to express our expectations in this circle and what had to be considered. (#9-NonIR)

By engaging in such activities, potential IR adopters made sure that they would have the necessary know-how to implement IR quickly if, for example, it became law or if their stakeholders began to press for its adoption. One informant mentioned that employees at their firm kept “discussing the topic peripherally” (#17a-NonIR) and monitored IR to keep abreast of recent IR developments. Thus, the more thorough adoption of IR at a later point in time would “ . . . not be a huge step operationally” (#17b-NonIR). This initial low-level interest was also stressed by an informant whose employer was a leading consultancy that specialized in IR:

Even before I started to work at [my employer] there was a workshop with Professor Eccles in Berlin for company representatives. Our customers ask us about the topic [IR] every now and then . . . They are aware that there is this new format, and they want to know what that means for them. (#16-Consult)

However, informants made it very clear that they refrained from more substantive adoption because “bandwagon pressure” (#32-Invest) remained insufficient. In addition, our secondary data reveals no evidence of IR being espoused symbolically: companies refrained from committing to making IR an integral part of their future reporting practice in public. Instead, IR was regarded by many observers as “a topic that is observed but not pushed” (#7-Audit). Potential adopters were reluctant to take further steps toward the publication of integrated reports or the promotion of the practice:

For every reporting trend . . . we need to develop a feeling and check how far it is relevant for us or for our target groups . . . (#23-NonIR)

This attitude was described succinctly by one of our informants, who worked for a large audit firm.

I think that many companies are doubtful whether this is an initiative that will prevail or whether it is something that will fizzle out. For this reason, it is an argument to say, “let’s wait and see.” (#1-Audit)

Overall, potential adopters seemed to wait and see how competitors would implement IR, thus creating useful best practices for the industry, and whether a more formal standardization of IR would follow.

. . . the situation is a bit of wait and see, critically observing, because it is not yet accepted broadly enough . . . so that all DAX companies would commit to it [publishing an integrated report]. (#26a-Invest)

As our data suggest, wait-and-see-ism implies putting a practice adoption process on hold for an indeterminate period of time while maintaining limited but continuous monitoring efforts with a view to adopting the practice later. This wait-and-see-ism, we found, allowed companies to avoid the costs of more substantive implementation without making themselves accountable by undertaking symbolic commitments to engage with IR more thoroughly (see Appendix 6 for further illustrative quotes).

Discussion

IR is a practice that corresponds to the current sustainability zeitgeist, has influential proponents, and initial adoption rates were promising. However, despite these favorable conditions for large-scale adoption, further adoption has been stalling for a long time. To solve this empirical puzzle, we developed the concept of wait-and-see-ism, defined as the deliberate and potentially long-lasting postponement of a decision to adopt a practice while monitoring its development silently and maintaining limited but continuous efforts to prepare for the prospect of its rapid adoption at a later stage. Wait-and-see-ism is thus an organizational response to ambiguous stakeholder pressures that puts the substantive adoption of a practice on hold. An attempt is made to limit exertion while maximizing preparedness. For example, efforts may be made to accumulate expert knowledge, and to observe peers, regulators, and other stakeholder groups. These efforts would allow the practice in question to be implemented from a competitively advantageous and prepared position.

Conceptualizing wait-and-see-ism

Wait-and-see-ism is a temporally stretched form of partial practice adoption that is conceptually distinct from the commonly examined responses of nonadoption and substantive or symbolic adoption. Wait-and-see-ism allows organizations to avoid admitting to nonadoption (inaction), it circumvents the need for the substantive adoption of a costly but potentially inefficient or ineffective practice, and it forestalls accusations of window-dressing that are common in cases of symbolic adoption (Weaver et al., 1999). Introducing wait-and-see-ism to the literature, we argue, therefore contributes to a better understanding of the widespread but undertheorized partial adoption of management practices (Durand et al., 2019; Haack et al., 2020; Naumovska et al., 2021). It helps to explain not only how but also why the adoption of practices is deliberately put on hold for indeterminate periods of time. This explanation is important, because “to develop predictions about limited diffusion it is necessary to (first) understand how and when initial resistance to adoption remains over time” (Jonsson, 2009: 172). Specifically, we shed light on three interrelated antecedents of wait-and-see-ism that help explain the stalling adoption of IR.

First, our findings show a strong supply-side push for IR mainly from auditing and consulting firms. This supply push played an important role in the initial uptake of IR. However, later, it was not met by corresponding demand from potential adopters and the strong engagement of the supply-side even triggered suspicion that IR might rather represent a business case for consulting companies than benefiting publishers and readers of integrated reports. Standard economic reasoning would predict that if excess supply is not matched by sufficient demand, the product or service in question would disappear from the market. In the context of IR, however, we observed wait-and-see-ism. We argue that this development can be attributed to a market environment where the sustainability zeitgeist made IR a salient issue which meant that most businesses could not ignore this practice entirely and saw preparing for its potential adoption as a necessity.

Issue salience has been argued to influence adoption rates (Durand et al., 2019). Durand et al.’s (2019) conceptual model, for example, predicts that inaction can only occur when issue salience is very low or very high. As a general matter, accountability and sustainability are highly salient at the present time. However, the same is not true of IR as a particular practice. That is not to say that the salience of IR is very low, a proposition that is controverted by the large initial buzz that it generated. In respect of medium-salience issues, Durand et al.’s (2019) model predicts symbolic or substantive actions. Conversely, our results point to wait-and-see-ism as an alternative. Wait-and-see-ism extends beyond organizations that do not (yet) publish integrated reports. After their initial enthusiasm had waned, other stakeholders also began to wait and see instead of investing more resources in IR. Slager et al. (2021) argue similarly that nonreactivity as an organizational response only occurs when organizations show little motivation to adopt a practice. For IR, however, there was no general lack of motivation. Instead, just as with salience, the motivation seemed to rest on an intermediate and “half-hearted” level of interest.

Second, Durand et al. (2019) argued that, at a conceptual level, practice adoption is determined by a combination of issue salience and cost-benefit calculations. Here, too, the empirical case of IR complicates this perspective. The responses of potential IR adopters are partly a result of cost-benefit calculations, in that potential adopters perceived highly tangible implementations costs and intangible benefits. However, our research also shows that the ambiguity of the benefits of IR was a critical feature that impelled organizations to engage in wait-and-see-ism. We thus expand on Ansari et al.’s (2010) expectation that “organizations will frequently find it difficult to conduct rational calculations on the cost-benefit trade-offs of adoption when the meaning of the diffusing practice is still in flux” (p. 84).

Third, regulatory uncertainty may cause organizations to delay actions (e.g. Holburn and Zelner, 2010; López-Gamero et al., 2011). In the case of IR, this possibility appears to be particularly germane. IR entails “unmeasurable” regulatory uncertainty (Knight, 1921), partly due to regulatory instability and partly due to the expectation that regulation would take a long time to (potentially) become effective. This regulatory uncertainty was further fueled by the foreshadowing of IR regulation through auditing and consulting firms which they used to demonstrate their own expertise (see also Brès and Gond, 2014; Gond and Brès, 2020). These factors generated perceptions of opaqueness among potential adopters. Although “uncertainty avoidance” (Cyert and March, 1963) has long been recognized as a potential driver of adoption, the case of IR shows that it does not necessarily lead to symbolic adoption. Instead, a wait-and-see approach emerged: organizations avoid significant commitments of resources, such as time or attention, until they can obtain more reliable information (Dutt and Joseph, 2019), not least on regulatory issues.

Theoretical implications

In general, the concept of wait-and-see-ism and its antecedents expand the understanding of the form and scope of partial adoption in important ways, going beyond what has previously been discussed in the literature. Oliver’s (1991) classic typology of organizational responses to institutional pressure supplies an important benchmark that enables us to position wait-and-see-ism as an alternative mode of practice adoption. Similar to Oliver’s (1991) “balance” tactic of the “compromise” strategy, where organizations try to accommodate the expectations of multiple constituents, wait-and-see-ism entails balancing. However, that balancing does not take the form of adopting a practice to reconcile competing objectives and expectations in an acceptable manner. Instead, the question of whether more substantive adoption should be pursued is postponed.

Thus, in the case of wait-and-see-ism, balancing has a temporal meaning: salient issues raised by stakeholders are acknowledged, but substantive action is only taken when a dominant stakeholder expectation crystalizes. This is the central point of difference between wait-and-see-ism and decoupling and symbolic adoption. A symbolic adoption of IR would imply widely touted commitments to IR and the visible publication of a report claimed to integrate financial and non-financial information. In contrast, our data suggests that potential adopters do not pretend to have adopted IR to use it as a marketing or PR tool, as is typical of symbolic adoption under conditions of high institutional pressure (Cho et al., 2015). Instead, wait-and-see-ism is mobilized for potentially long-lasting periods of screening the development of the practice and balancing the costs versus benefits of adopting it.

One of the antecedents of wait-and-see-ism in the context of IR is the absence of strong pressure from stakeholders. Overall, institutional pressure differs between situations with symbolic adoption outcomes and wait-and-see-ism. A central aspect of symbolic adoption is the implicit assumption that organizations are exposed to strong institutional pressures to conformity (Oliver, 1991). Kostova and Roth (2002), for instance, suggested that symbolic adoption is likely to result when adopters perceive a practice as being highly uncertain and do not consider it valuable while facing strong external pressure to adopt it.

Wait-and-see-ism, however, seems to be mobilized when external pressure is weaker and more ambiguous because stakeholders cannot articulate their expectations clearly. In the case of IR, those expectations would revolve around the choice between integrated and standalone sustainability reports. In other words, pressure toward conformity does not (yet) exist, but potential adopters still see the value of the practice in question. In this sense, wait-and-see-ism is an important refinement to organizational practice adoption responses in situations of low perceived pressure, and it contrasts with Oliver’s (1991) theory. Oliver (1991) suggests that companies might simply dismiss or ignore institutional rules and values when the possibility that institutional rules will be enforced externally is deemed remote.

Furthermore, wait-and-see-ism is also distinct from other in-between forms of partial adoption. Pache and Santos (2010), for example, have described how the imposition of conflicting demands on companies by their institutional environments may lead to organizational paralysis. Prima facie, organizational paralysis and wait-and-see-ism seem closely related, in that both imply a certain degree of inactivity. However, in the case of organizational paralysis, inactivity may precipitate disastrous consequences, such as prolonged industrial action (Pache and Santos, 2010). Wait-and-see-ism, in contrast, reflects a more conscious inactivity—the decision to adopt a practice is postponed deliberately. Importantly, this should not be confused with the concept of procrastination that is well documented in social psychology and economic theory (e.g. Akerlof, 1991). Procrastination is typically the result of a present-bias in preferences, so that agents delay completion of tasks relative to what would be efficient (O’Donoghue and Rabin, 2008). The connotations of wait-and-see-ism are thus more positive than for organizational paralysis or procrastination; it provides firms with agency and flexibility and can thus be an effective organizational response.

For this reason, wait-and-see-ism shares some conceptual ground with the idea of “muddling through,” which Crilly et al. (2012) identified as an alternative to existing explanations of firm responses to institutional pressures. Muddling through, a potential result of an interaction between internal organizational and external environmental factors, is typified by “ . . . uncoordinated, exploratory attempts to respond to diverse and conflicting demands in a generally well-intended [. . .] process” (Crilly et al., 2012: 1443). While muddling through does not involve the calculated deception that inheres in the conventional notion of decoupling, firms still “decouple their behavior from stated commitments” (Crilly et al., 2012: 1443) because managers explore different options to adopt and implement a practice to satisfy and balance competing stakeholder expectations. In contrast, firms that engage in wait-and-see-ism are temporarily inactive, possibly owing to the insufficient strength of institutional pressures at a given point in time.

Our research also expands on prior studies that develop a temporal perspective to practice adoption, which, for instance, argued that symbolic adoption is a predecessor of substantive adoption. Considering adoption as a sequence of responses, “before an organization would bear the costs of substantive adoption, it would first do so only ceremonially and then move forward” (Haack et al., 2020: 21; see also Haack et al., 2012). Haack et al. (2020), however, only consider three possible adoption scenarios (nonadoption, symbolic adoption, and substantive adoption). Wait-and-see-ism, in describing a viable alternative to symbolic adoption, broadens the conceptual range of responses. Companies that engage in wait-and-see-ism are better positioned to avoid the trap of greenwashing accusations when they wait and see instead of making symbolic commitments. In line with the view that practice adoption is not static but transitory (Christensen et al., 2013; Haack et al., 2012), wait-and-see-ism could also be considered an intermediate step between nonadoption and substantive adoption, whereby organizations may avoid the route of symbolic adoption that Haack et al. (2020) suggest. In fact, these authors mention that “rather than directly adopting a CSR practice substantively, organizations will often first implement it incompletely or ceremonially” (Haack et al., 2020: 21; our emphasis). However, when they elaborate on ceremonial (i.e. symbolic) adoption, they do not identify the concrete implications of incomplete or partial adoption. Rather than suggesting a sequence of adoption decisions as the study of Haack et al. (2020) elaborates, wait-and-see-ism implies ongoing scanning of the practice, and the devotion of limited attention and resources.

In their examination of the temporal character of practice adoption in the context of CSR, Christensen et al. (2013) highlight the potentially positive effects of symbolic adoption: “aspirational talk” may be triggered by initially ceremonial commitments. Over time, however, it may induce actors to make more substantive changes to organizational CSR practices. From the point of view of a business firm, aspirational talk might be risky, especially when the aspirations become public and visible but remain unfulfilled. Wait-and-see-ism provides a less perilous alternative to potential adopters who are unsure about adopting a practice.

Limitations and opportunities for future research

The limitations of our study are common to this type of qualitative research. For instance, the focus was on Germany and its specific socio-economic setting. Factors such as regulatory intensity and the salience of stakeholder pressure may differ in other settings. Moreover, we examined a particular practice, IR. One of its features is a strong emphasis on sustainability. More technical practices that receive more or less attention from firms and their stakeholders may be approached differently.

Future research can address these limitations. The antecedents of wait-and-see-ism that we identified can also serve as starting points for further inquiry. When opportunities for future research on other practices in other sociocultural and economic contexts arise, scholars could also develop a more refined understanding of the precise sequence in which the conditions that we highlighted materialize with the highest degree of salience. The mechanisms through which those conditions influence adopters should also be studied. In addition, although we examined IR, contested practices exist in many other fields, such as new technologies or work practices. Scholars might also find wait-and-see-ism there, along with other factors. Moreover, the uncertainty caused by the COVID-19 pandemic might push more organizations to engage in wait-and-see-ism instead of mobilizing resources to adopt new management practices substantively.

Wait-and-see-ism also offers opportunities to those who are interested in understanding how practices spread because it transforms the commonly asked question “What makes practices spread more successfully?” into “What makes practices spread less?.” This links to Jonsson’s (2009) argument that theorizing about the causes and mechanisms of persistent resistance to adoption is an important building block of the study of limited and failed diffusion processes. Indeed, we found that potential adopters have considerable leeway to postpone substantive adoption.

Importantly, we have framed wait-and-see-ism as an organizational response to ambiguous institutional demands. At the same time, we acknowledge that in our empirical context, a broad set of heterogeneous stakeholders exhibit a wait-and-see attitude. While wait-and-see-ism allows individual organizations to postpone a decision to adopt a practice, it is its embeddedness in a broader attitude held by many influential actors that results in a management practice stalling.

Conclusion

Our research has addressed the empirical puzzle of the stalling adoption of the seemingly popular sustainability reporting practice of IR in Germany. We established a theoretical connection between this phenomenon and the practice adoption literature, and we developed the notion of wait-and-see-ism, a hitherto underspecified mode of partial adoption. Our main contribution thus lies in expanding the conceptual spectrum of organizational responses to institutional demands. Wait-and-see-ism is an alternative to the oft-theorized approaches of symbolic and substantive adoption. When exhibited collectively by multiple actors in a given field, wait-and-see-ism can explain why the adoption of a practice stalls over an extended period of time.

Our research also has societal relevance. Its message for practitioners is that proponents of sustainability reporting should be wary of one-size-fits-all approaches, such as IR, because they do not offer tailored reporting instruments to stakeholders. For instance, NGOs typically favor reports that include a strong narrative of a company’s CSR activities and provide illustrative cases and evidence of concrete CSR actions. Socially responsible investors prefer highly standardized facts and figure-driven reports, akin to those that regular investors typically demand. IR, however, seems to have no real target group, as noted by some of our informants. Therefore, stakeholders involved in the future development of IR should consider these insights when they deliberate on its meaning and scope. This is important because urgent action is needed to advance organizational practices that promote sustainability.

Footnotes

Appendix 1

Panel B: secondary data sources.

| Type | Characterization of source |

|---|---|

| Practitioners Report 1 (PR1) (Consultant firm) | Akzente kommunikation und beratung GmbH, & HGB Hamburger Geschäftsberichte GmbH & Co. KG. (2012). integrated: Integrierte Berichterstattung. Von der Herausforderung zum Praxismodell. Last retrieved May 3, 2018 from https://www.akzente.de/fileadmin/Publikationen/PDF_Publikationen/Integrated_Studie_akzente_HGB_2012.pdf |

| PR2 (Federal ministry) | Bundesministerium für Umwelt, Naturschutz und Reaktorsicherheit. (2012). Nachhaltig und verantwortlich investieren—ein Leitfaden: Die UN Principles for Responsible Investment (PRI). Last retrieved May 3, 2018 from https://www.bvi.de/fileadmin/user_upload/Regulierung/UNPRI.pdf |

| PR3 (Audit firm) | Deloitte & Touche GmbH Wirtschaftsprüfungsgesellschaft. (2012). Nachhaltigkeit: Warum CFOs auf Einsparungen und Strategie setzen. Last retrieved May 3, 2018 from https://www.iasplus.com/de/publications/german-publications/other/nachhaltigkeit-warum-cfos-auf-einsparungen-und-strategie-setzen/file |

| PR4 (Audit firm) | Deloitte & Touche GmbH Wirtschaftsprüfungsgesellschaft. (2012). Fokus Mittelstand: Einzigartiger Erfolg (2). Last retrieved May 3, 2018 from https://www2.deloitte.com/content/dam/Deloitte/de/Documents/Mittelstand/Fokus-Mittelstand-Newsletter-2-2012.pdf |

| PR5 (Audit firm) | EYGM Limited. (2014). Integrierte Berichterstattung: Wertsteigerungsmöglichkeiten für Unternehmen (EYG no. AU2356). Last retrieved May 3, 2018 from http://www.ey.com/Publication/vwLUAssets/EY_Broschuere_-_Integrierte_Berichterstattung/$FILE/EY-Broschuere-Integrierte-Berichterstattung.pdf |

| PR6 (Consultant firm) | Imug Beratungsgesellschaft für sozial-ökologische Innovationen mbH. (2016, July 5). Integrated reporting: Impulse für einen nachhaltige Unternehmensentwicklung. Last retrieved May 3, 2018 from https://www.imug.de/fileadmin/user_upload/Downloads/imug_csr/imug_positionspapier_ir_2016_07_05.pdf |

| PR7 (Audit firm) | PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft. (2012, July). 10 Minuten: Integrated Reporting. Last retrieved May 3, 2018 from https://www.pwc.de/de/rechnungslegung/assets/10_min_integrated_reporting.pdf |

| PR8 (Audit firm) | PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft. (2012, April). Auf dem Weg zum Integrated Reporting. Last retrieved May 3, 2018 from https://www.pwc.at/de/publikationen/studien/pwc-studie-integrated-reporting.pdf |

| PR9 (Consultant firm) | Steinert, A. (2012, November). Der Weg zur integrierten Berichterstattung: Wie CSR Experten die Entwicklung mitgestalten können. Last retrieved May 3, 2018 from http://bits-communication.de/wp-content/uploads/2014/07/Steinert_Der-Weg-zur-Integrierten-Berichterstattung_121230v2.pdf |

| PR10 (Consultant firm) | Wullenkord, A. (2014). Der Integierte Geschäftsbericht (“One Report”)—Ein neuer Ansatz für eine zeitgemäße Unternehmensberichterstattung (Straight2 Compact Newsletter). Last retrieved 3 May 2018 from http://www.administraight.de/wp-content/uploads/2014/06/Straight-Hoch-Zwei-Nr.-4-Zukunft-der-Berichterstattung-Der-integrierte-Gesch%C3%A4ftsbericht.pdf |

Appendix 2

Appendix 3

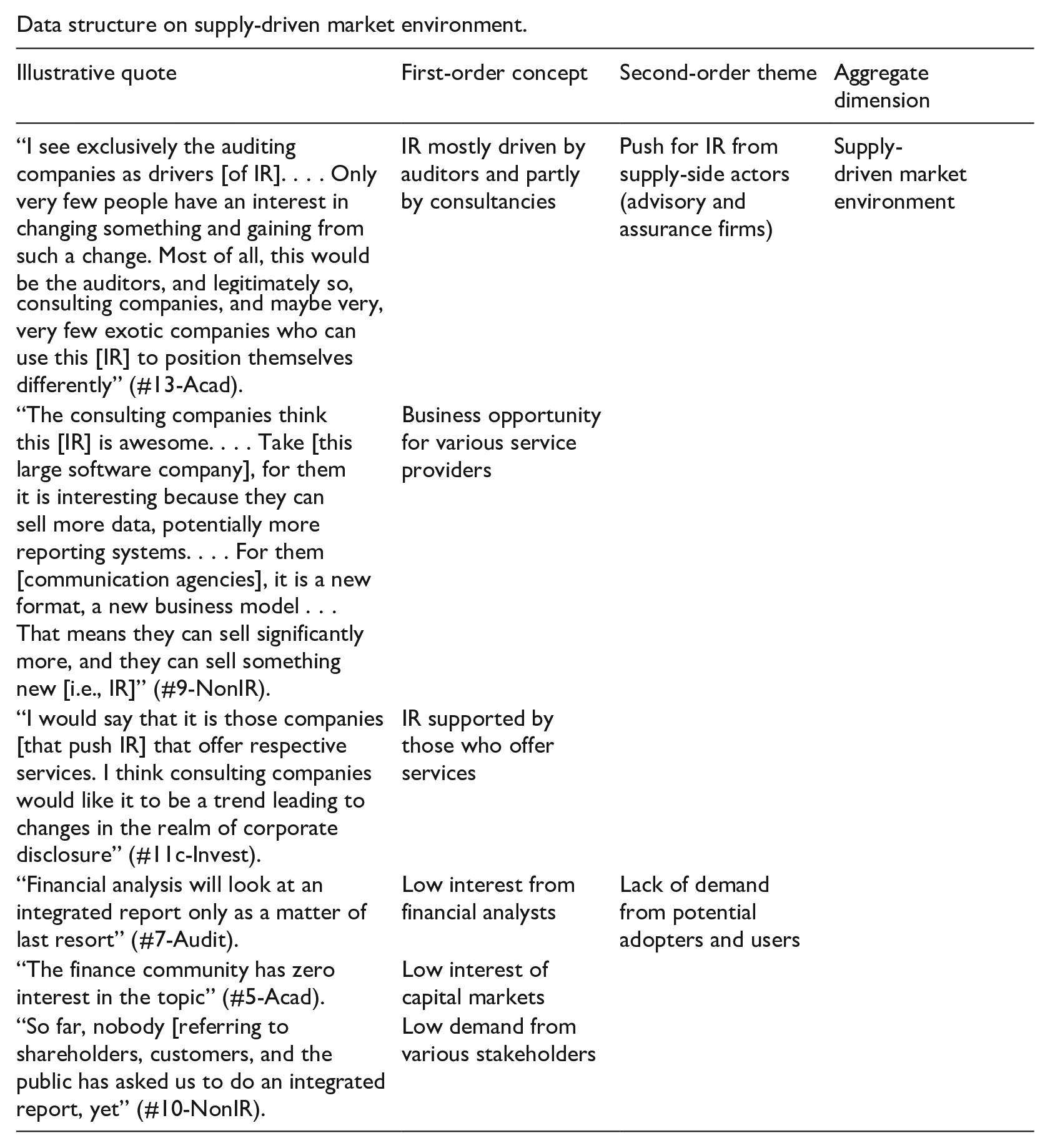

Data structure on supply-driven market environment.

| Illustrative quote | First-order concept | Second-order theme | Aggregate dimension |

|---|---|---|---|

| “I see exclusively the auditing companies as drivers [of IR]. . . . Only very few people have an interest in changing something and gaining from such a change. Most of all, this would be the auditors, and legitimately so, consulting companies, and maybe very, very few exotic companies who can use this [IR] to position themselves differently” (#13-Acad). | IR mostly driven by auditors and partly by consultancies | Push for IR from supply-side actors (advisory and assurance firms) | Supply-driven market environment |

| “The consulting companies think this [IR] is awesome. . . . Take [this large software company], for them it is interesting because they can sell more data, potentially more reporting systems. . . . For them [communication agencies], it is a new format, a new business model . . . That means they can sell significantly more, and they can sell something new [i.e., IR]” (#9-NonIR). | Business opportunity for various service providers | ||

| “I would say that it is those companies [that push IR] that offer respective services. I think consulting companies would like it to be a trend leading to changes in the realm of corporate disclosure” (#11c-Invest). | IR supported by those who offer services | ||

| “Financial analysis will look at an integrated report only as a matter of last resort” (#7-Audit). | Low interest from financial analysts | Lack of demand from potential adopters and users | |

| “The finance community has zero interest in the topic” (#5-Acad). | Low interest of capital markets | ||

| “So far, nobody [referring to shareholders, customers, and the public has asked us to do an integrated report, yet” (#10-NonIR). | Low demand from various stakeholders |

Appendix 4

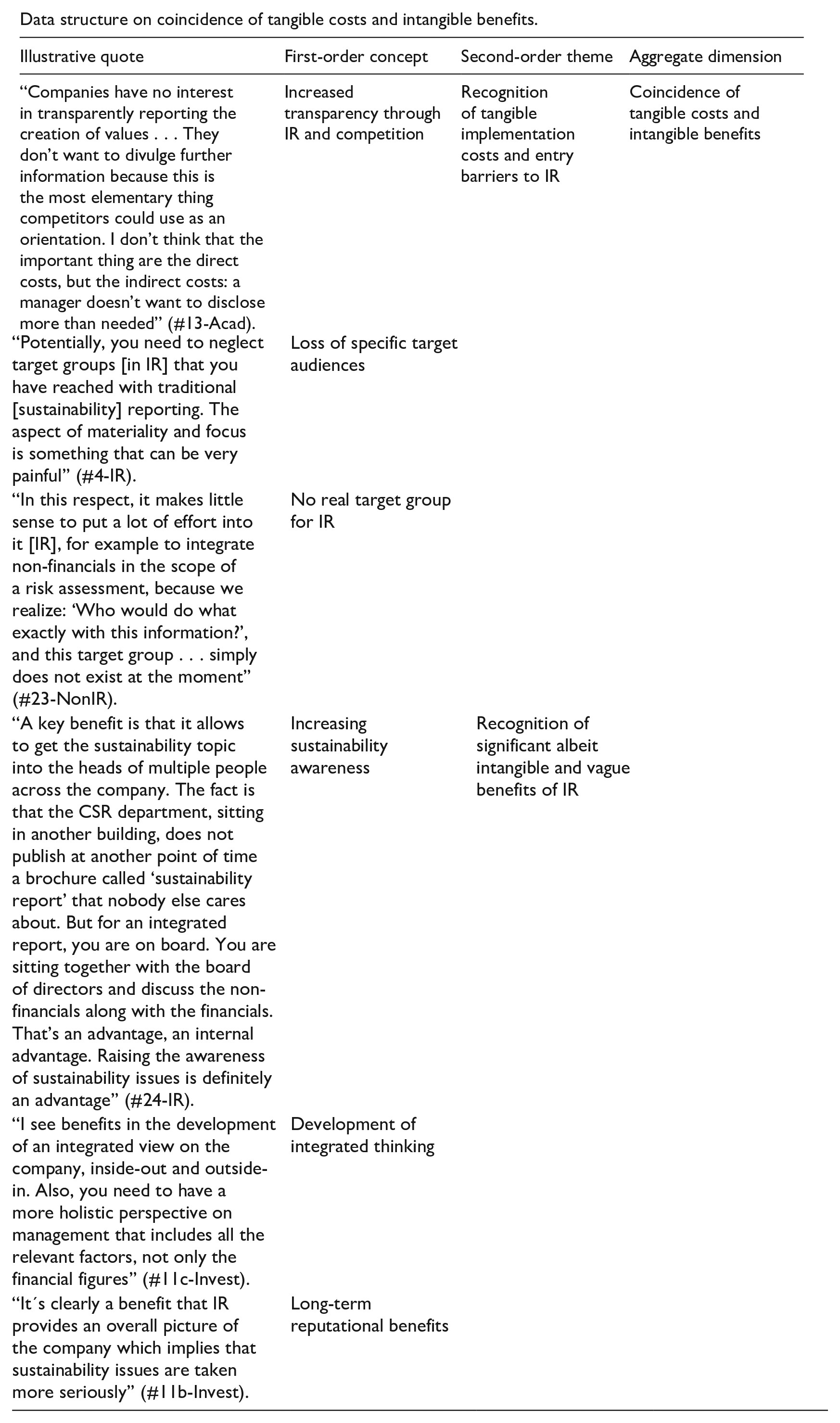

Data structure on coincidence of tangible costs and intangible benefits.

| Illustrative quote | First-order concept | Second-order theme | Aggregate dimension |

|---|---|---|---|

| “Companies have no interest in transparently reporting the creation of values . . . They don’t want to divulge further information because this is the most elementary thing competitors could use as an orientation. I don’t think that the important thing are the direct costs, but the indirect costs: a manager doesn’t want to disclose more than needed” (#13-Acad). | Increased transparency through IR and competition | Recognition of tangible implementation costs and entry barriers to IR | Coincidence of tangible costs and intangible benefits |

| “Potentially, you need to neglect target groups [in IR] that you have reached with traditional [sustainability] reporting. The aspect of materiality and focus is something that can be very painful” (#4-IR). | Loss of specific target audiences | ||

| “In this respect, it makes little sense to put a lot of effort into it [IR], for example to integrate non-financials in the scope of a risk assessment, because we realize: ‘Who would do what exactly with this information?’, and this target group . . . simply does not exist at the moment” (#23-NonIR). | No real target group for IR | ||

| “A key benefit is that it allows to get the sustainability topic into the heads of multiple people across the company. The fact is that the CSR department, sitting in another building, does not publish at another point of time a brochure called ‘sustainability report’ that nobody else cares about. But for an integrated report, you are on board. You are sitting together with the board of directors and discuss the non-financials along with the financials. That’s an advantage, an internal advantage. Raising the awareness of sustainability issues is definitely an advantage” (#24-IR). | Increasing sustainability awareness | Recognition of significant albeit intangible and vague benefits of IR | |

| “I see benefits in the development of an integrated view on the company, inside-out and outside-in. Also, you need to have a more holistic perspective on management that includes all the relevant factors, not only the financial figures” (#11c-Invest). | Development of integrated thinking | ||

| “It’s clearly a benefit that IR provides an overall picture of the company which implies that sustainability issues are taken more seriously” (#11b-Invest). | Long-term reputational benefits |

Appendix 5

| Illustrative quote | First-order concept | Second-order theme | Aggregate dimension |

|---|---|---|---|

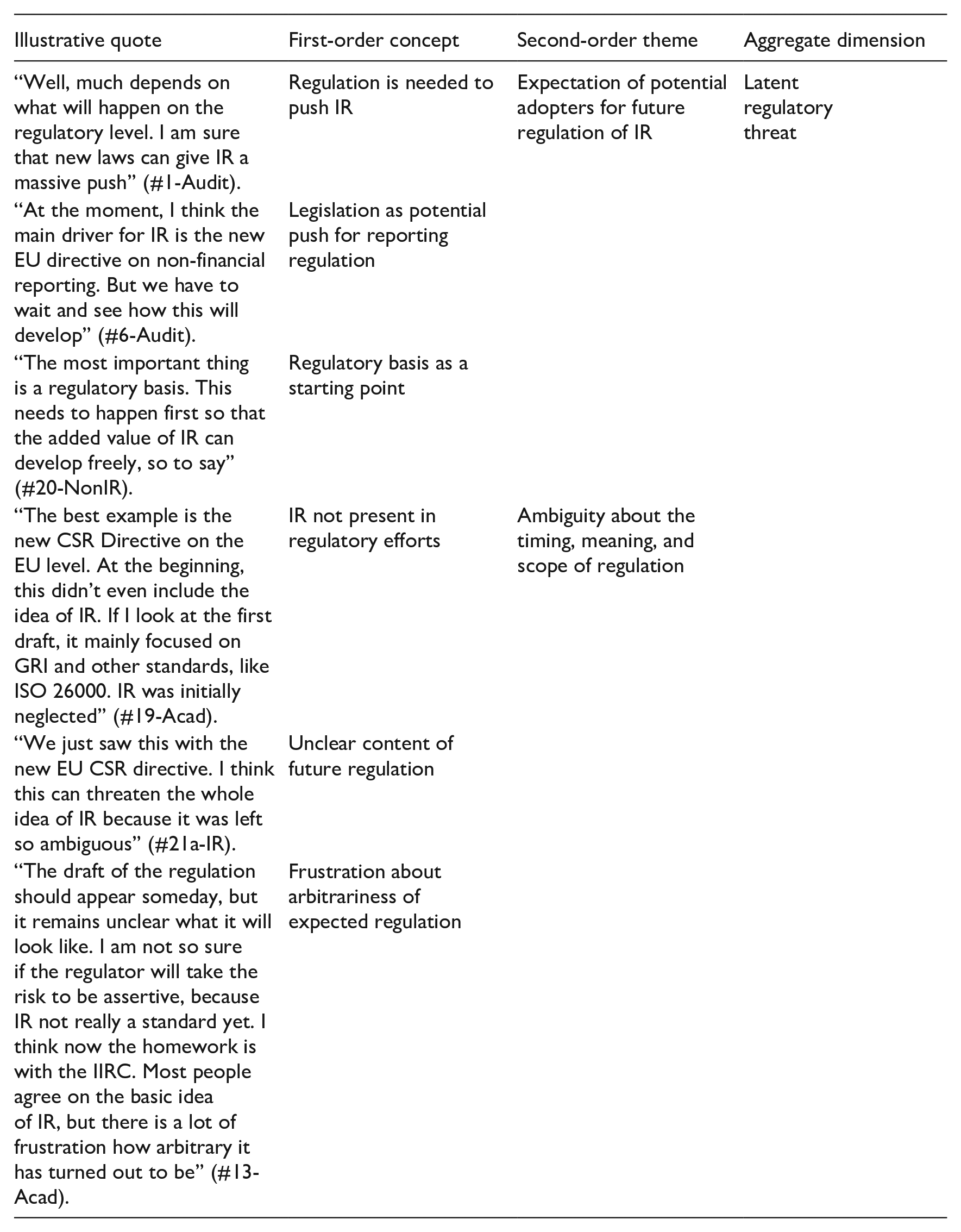

| “Well, much depends on what will happen on the regulatory level. I am sure that new laws can give IR a massive push” (#1-Audit). | Regulation is needed to push IR | Expectation of potential adopters for future regulation of IR | Latent regulatory threat |

| “At the moment, I think the main driver for IR is the new EU directive on non-financial reporting. But we have to wait and see how this will develop” (#6-Audit). | Legislation as potential push for reporting regulation | ||

| “The most important thing is a regulatory basis. This needs to happen first so that the added value of IR can develop freely, so to say” (#20-NonIR). | Regulatory basis as a starting point | ||

| “The best example is the new CSR Directive on the EU level. At the beginning, this didn’t even include the idea of IR. If I look at the first draft, it mainly focused on GRI and other standards, like ISO 26000. IR was initially neglected” (#19-Acad). | IR not present in regulatory efforts | Ambiguity about the timing, meaning, and scope of regulation | |

| “We just saw this with the new EU CSR directive. I think this can threaten the whole idea of IR because it was left so ambiguous” (#21a-IR). | Unclear content of future regulation | ||

| “The draft of the regulation should appear someday, but it remains unclear what it will look like. I am not so sure if the regulator will take the risk to be assertive, because IR not really a standard yet. I think now the homework is with the IIRC. Most people agree on the basic idea of IR, but there is a lot of frustration how arbitrary it has turned out to be” (#13-Acad). | Frustration about arbitrariness of expected regulation |

Appendix 6

Data structure on wait-and-see-ism.

| Illustrative quote | First-order concept | Second-order theme | Aggregate dimension |

|---|---|---|---|

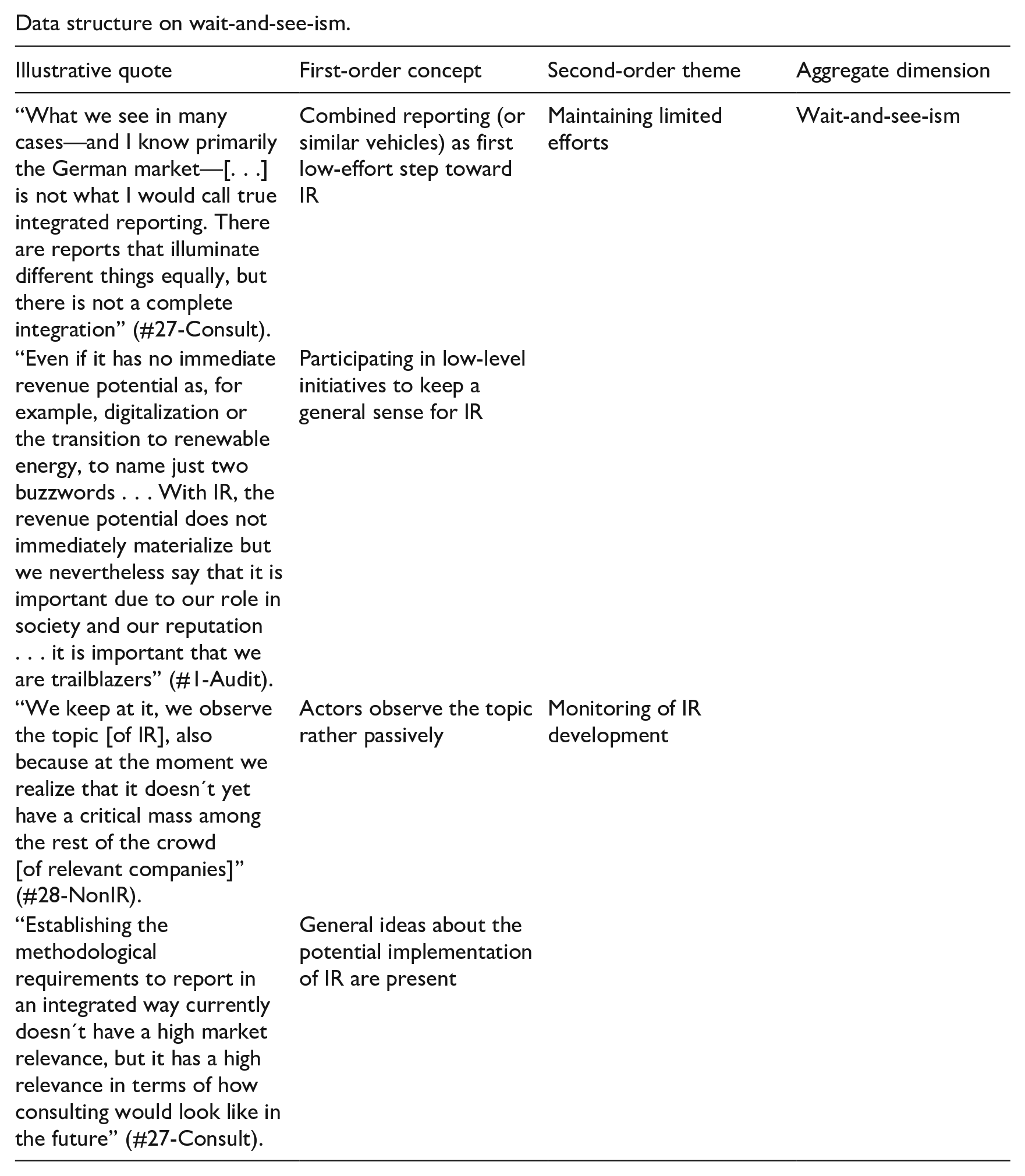

| “What we see in many cases—and I know primarily the German market—[. . .] is not what I would call true integrated reporting. There are reports that illuminate different things equally, but there is not a complete integration” (#27-Consult). | Combined reporting (or similar vehicles) as first low-effort step toward IR | Maintaining limited efforts | Wait-and-see-ism |

| “Even if it has no immediate revenue potential as, for example, digitalization or the transition to renewable energy, to name just two buzzwords . . . With IR, the revenue potential does not immediately materialize but we nevertheless say that it is important due to our role in society and our reputation . . . it is important that we are trailblazers” (#1-Audit). | Participating in low-level initiatives to keep a general sense for IR | ||

| “We keep at it, we observe the topic [of IR], also because at the moment we realize that it doesn’t yet have a critical mass among the rest of the crowd [of relevant companies]” (#28-NonIR). | Actors observe the topic rather passively | Monitoring of IR development | |

| “Establishing the methodological requirements to report in an integrated way currently doesn’t have a high market relevance, but it has a high relevance in terms of how consulting would look like in the future” (#27-Consult). | General ideas about the potential implementation of IR are present |

Acknowledgements

All authors contributed equally to this study. The sequence of authors was determined by a series of games of Rock, Paper, Scissors, Lizard, Spock. They thank the editor Amit Nigam and three anonymous reviewers for their developmental feedback. The comments helped to improve the original draft considerably. They are also grateful to Geert Braam, Stefan Heusinkveld, Bernard Leca, and Andrew Sturdy for their feedback on earlier drafts of this manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.